Financial Reporting: Conceptual Framework and Standards

VerifiedAdded on 2020/06/04

|14

|4423

|150

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with an introduction that outlines its context and purpose. It delves into the conceptual and regulatory frameworks, emphasizing their requirements, key principles, and the importance of accounting standards like IFRS. The report identifies major stakeholders, such as managers, suppliers, shareholders, and employees, and explains how they benefit from financial information. It includes an analysis of income statements, balance sheets, and the measurement of company performance. Furthermore, it examines the differences between International Accounting Standards (IAS) and IFRS, evaluates the advantages of IFRS adoption, and discusses factors impacting compliance. The report concludes with a summary of the key findings and includes references to support the analysis.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

(1)Outling context and purpose of financial reporting....................................................................1

(2) Examining conceptual and regulatory framework and their requirements as well as purpose

and key principles............................................................................................................................2

(3) Major stakeholders of an organization and way in which they benefit from financial

information......................................................................................................................................3

(4)Importance of financial reporting for meeting objectives and growth........................................4

(5)Statement of income, equity and financial position....................................................................5

(6) Measurement of company performance.....................................................................................7

(7) Difference between International accounting standard and International financial reporting

standard............................................................................................................................................8

(8) Evaluate the benefits of IFRS....................................................................................................9

(9)Compliance with IFRS and elements in country that have impact on compliance...................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

(1)Outling context and purpose of financial reporting....................................................................1

(2) Examining conceptual and regulatory framework and their requirements as well as purpose

and key principles............................................................................................................................2

(3) Major stakeholders of an organization and way in which they benefit from financial

information......................................................................................................................................3

(4)Importance of financial reporting for meeting objectives and growth........................................4

(5)Statement of income, equity and financial position....................................................................5

(6) Measurement of company performance.....................................................................................7

(7) Difference between International accounting standard and International financial reporting

standard............................................................................................................................................8

(8) Evaluate the benefits of IFRS....................................................................................................9

(9)Compliance with IFRS and elements in country that have impact on compliance...................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial reporting refers to way in which financial statements are presented. In the

current report, purpose of financial reporting is explained in detail. Apart from this, significence

of IFRS is also explained. Along with this, key principles of accounting are defined briefly.

Some of qualitative characteristics that an accounting information must have are also discussed.

In middle part of the report, income statement and balance sheet are prepared on basis of

additional information and trial balance. At end of the report, difference between IAS and IFRS

are explained in detail and reasons due to which nations are not adopting IFRS are also

explained.

(1)Outling context and purpose of financial reporting

Financial reporting refers to preparation of income statement, balance sheet and cash

flow statement. These statements are prepared by most of business firms because by using them

profitability in business is measured and financial position is measured. On other hand, in cash

flow statement cash flows from different activities like operating, investing and financing

activity is measured (Feng and et.al., 2014). It can be said that all these statements have

significent importance for the business firms. Major purpose behind preparing income statement

is to keep stakeholders and managers informed about company profitability and costing. On

other hand, major purpose behind preparing balance sheet is to measure company financial

position at end of the financial year. Thus, stakeholders and managers comes to know about

capial structure of the business firm and sort of risk to which firm is exposed. It can be said that

there is huge importance of these statements for the business firms. Cash flow statement is one

under which cash flow from operating, investing and financing activity are recorded and on that

basis it is identified that how much cash remain at end of the year. It can be said that there are

different purpose behind using all these statements in the business. Active usage of financial

statements in the business ensured that all operations will be performed in perfect way and good

amount of profit will be generated in the business (Gaynor and et.al., 2016). In past couple of

years many changes comes in the reporting standard and IFRS lay down modified standards that

need to be followed for reporting purpose. This is the reason due to which reporting structure

almost same is followed in the business by the firms. It can be said that financial reporting have

due importance for the firms and same need to be strictly followed in the business in order to

comply with international standards.

1 | P a g e

Financial reporting refers to way in which financial statements are presented. In the

current report, purpose of financial reporting is explained in detail. Apart from this, significence

of IFRS is also explained. Along with this, key principles of accounting are defined briefly.

Some of qualitative characteristics that an accounting information must have are also discussed.

In middle part of the report, income statement and balance sheet are prepared on basis of

additional information and trial balance. At end of the report, difference between IAS and IFRS

are explained in detail and reasons due to which nations are not adopting IFRS are also

explained.

(1)Outling context and purpose of financial reporting

Financial reporting refers to preparation of income statement, balance sheet and cash

flow statement. These statements are prepared by most of business firms because by using them

profitability in business is measured and financial position is measured. On other hand, in cash

flow statement cash flows from different activities like operating, investing and financing

activity is measured (Feng and et.al., 2014). It can be said that all these statements have

significent importance for the business firms. Major purpose behind preparing income statement

is to keep stakeholders and managers informed about company profitability and costing. On

other hand, major purpose behind preparing balance sheet is to measure company financial

position at end of the financial year. Thus, stakeholders and managers comes to know about

capial structure of the business firm and sort of risk to which firm is exposed. It can be said that

there is huge importance of these statements for the business firms. Cash flow statement is one

under which cash flow from operating, investing and financing activity are recorded and on that

basis it is identified that how much cash remain at end of the year. It can be said that there are

different purpose behind using all these statements in the business. Active usage of financial

statements in the business ensured that all operations will be performed in perfect way and good

amount of profit will be generated in the business (Gaynor and et.al., 2016). In past couple of

years many changes comes in the reporting standard and IFRS lay down modified standards that

need to be followed for reporting purpose. This is the reason due to which reporting structure

almost same is followed in the business by the firms. It can be said that financial reporting have

due importance for the firms and same need to be strictly followed in the business in order to

comply with international standards.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(2) Examining conceptual and regulatory framework and their requirements

as well as purpose and key principles

Conceptual and regulatory framework have due importance for the firms because in these

frameworks different accounting concepts are well defined and it is clearly stated that in what

way accounting transactions will be recorded in the company books of accounts. Thus, it is very

important for accountants to follow all these regulations tightly in the business. Major purpose

behind prerparing these frameworks is to ensure that there is common system of accounting of

transactions and it is possible to measure and compare firms performance in proper manner

(Thomson, 2017). There are some of the key principles that need to be followed while preparing

financial statements. Economic entity principle state that accountant need to keep all transaction

of company and its owners separately from each other. In books of accounts personal account

related transactions can not be entered so that profitability of company can be measured fairly.

Monetary unit principle state that only those transactions can be recorded that can be measured

in terms of money. Cost principle state that assets must be recorded at their purchase value.

Means that asset must be recorded at their actual cost irrespective of their price in the market.

Full disclosure principle state that all important transaction related details must be theoritically

explained in the company annual report. By doing so in proper manner information can be

provided to the stakeholders. Going concern principle state that organization will remain in

existence consistently and its owners will change with passage of time. Hence, accounting

transactions are recorded on company name not on basis of individuals. Matching principle state

that accounting transactions must be recorded in relevant time period. Means that wages must be

recorded in the period of sales from which its amount is paid. By doing so, recording of

transactions is done in systematic way and performance of company is measured accurately.

Revenue recognition principle state that any amount can be treated as part of revenue once

transaction is completed irrespective of time by which cash amount is received in the business.

Materiality principle state that one can volate an accounting principle if an amount related to

business transaction is insignificent (Tan, 2016). Conervatism principle state that if there are two

acceptable alternatives for reporting of an item accountant must choose to select an alternative

that result in less income and less asset in the business.

There are some of the qualitative characteristics that make financial information relaible

for the firms and stakeholders. These qualitative characterisitcs are understandability, relevance,

2 | P a g e

as well as purpose and key principles

Conceptual and regulatory framework have due importance for the firms because in these

frameworks different accounting concepts are well defined and it is clearly stated that in what

way accounting transactions will be recorded in the company books of accounts. Thus, it is very

important for accountants to follow all these regulations tightly in the business. Major purpose

behind prerparing these frameworks is to ensure that there is common system of accounting of

transactions and it is possible to measure and compare firms performance in proper manner

(Thomson, 2017). There are some of the key principles that need to be followed while preparing

financial statements. Economic entity principle state that accountant need to keep all transaction

of company and its owners separately from each other. In books of accounts personal account

related transactions can not be entered so that profitability of company can be measured fairly.

Monetary unit principle state that only those transactions can be recorded that can be measured

in terms of money. Cost principle state that assets must be recorded at their purchase value.

Means that asset must be recorded at their actual cost irrespective of their price in the market.

Full disclosure principle state that all important transaction related details must be theoritically

explained in the company annual report. By doing so in proper manner information can be

provided to the stakeholders. Going concern principle state that organization will remain in

existence consistently and its owners will change with passage of time. Hence, accounting

transactions are recorded on company name not on basis of individuals. Matching principle state

that accounting transactions must be recorded in relevant time period. Means that wages must be

recorded in the period of sales from which its amount is paid. By doing so, recording of

transactions is done in systematic way and performance of company is measured accurately.

Revenue recognition principle state that any amount can be treated as part of revenue once

transaction is completed irrespective of time by which cash amount is received in the business.

Materiality principle state that one can volate an accounting principle if an amount related to

business transaction is insignificent (Tan, 2016). Conervatism principle state that if there are two

acceptable alternatives for reporting of an item accountant must choose to select an alternative

that result in less income and less asset in the business.

There are some of the qualitative characteristics that make financial information relaible

for the firms and stakeholders. These qualitative characterisitcs are understandability, relevance,

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reliability and comparability. Means that information which is presented in the financial

statements must be easy to understand on taking single look. Apart from this, there must be

relevance of the information that is presented in these statements. Along with this, financial

information must be reliable in nature and all facts that are included in them must be fully

authentic in nature (Lee, 2014). It must be easy to compare financial statements as they must be

prepared by using same accounting and reporting standards. Financial statements that cover all

these things are assumed reliable in nature.

(3) Major stakeholders of an organization and way in which they benefit from

financial information

Stakholders have significent importance for business enterprise as they are entities that

underpin growth of the companies by assisting managers in implementing their business related

decisions. Some of the important stakeholders in respect to company are given below. Managers: These are those lead an organization and play decisive role in success and

failure of the company. Managers always needed an input for making business decisions.

These inputs are some facts and figures as well as company accounts. By using these

statements performance of the company is measures. Hence, through analysis managers

comes to know that in which area company is strong and weak. Maangers wage work on

weak areas and try to convert in strong point of the company. By doing so firm core

competency is increased and it is ensured that good return will be earned in the business. Suppliers: Suppliers are the another entities that have very high importance for the firms

because suppliers supply raw material to the business firm. There are already limited

suppliers in the business and in case if one of suppliers withdraw its support from the

business firm its business is havily affected like usually observed in case of companies

(Ghosh. and Tang, 2015). Suppliers number of times sold goods on credit basis and they

need to ensure that on time debt amount will be recovered from the company. In this

regard suppliers needed company statement and by using same identify whether company

will be able to pay all its debt on time. It can be said that financial information have due

importance for the business firms. Shareholders: These are those entities that make investment in the company shares.

Shareholders needed company information in order to determine whether investment

need to be kept in the company or capital must be withdraw from the company.

3 | P a g e

statements must be easy to understand on taking single look. Apart from this, there must be

relevance of the information that is presented in these statements. Along with this, financial

information must be reliable in nature and all facts that are included in them must be fully

authentic in nature (Lee, 2014). It must be easy to compare financial statements as they must be

prepared by using same accounting and reporting standards. Financial statements that cover all

these things are assumed reliable in nature.

(3) Major stakeholders of an organization and way in which they benefit from

financial information

Stakholders have significent importance for business enterprise as they are entities that

underpin growth of the companies by assisting managers in implementing their business related

decisions. Some of the important stakeholders in respect to company are given below. Managers: These are those lead an organization and play decisive role in success and

failure of the company. Managers always needed an input for making business decisions.

These inputs are some facts and figures as well as company accounts. By using these

statements performance of the company is measures. Hence, through analysis managers

comes to know that in which area company is strong and weak. Maangers wage work on

weak areas and try to convert in strong point of the company. By doing so firm core

competency is increased and it is ensured that good return will be earned in the business. Suppliers: Suppliers are the another entities that have very high importance for the firms

because suppliers supply raw material to the business firm. There are already limited

suppliers in the business and in case if one of suppliers withdraw its support from the

business firm its business is havily affected like usually observed in case of companies

(Ghosh. and Tang, 2015). Suppliers number of times sold goods on credit basis and they

need to ensure that on time debt amount will be recovered from the company. In this

regard suppliers needed company statement and by using same identify whether company

will be able to pay all its debt on time. It can be said that financial information have due

importance for the business firms. Shareholders: These are those entities that make investment in the company shares.

Shareholders needed company information in order to determine whether investment

need to be kept in the company or capital must be withdraw from the company.

3 | P a g e

Shareholders also needed annual report because by reviewing them they comes to know

about company current business condition and direction in which company is performing.

Thus, it can be said that financial statements have huge importance for the firms because

it help them in making investment decisions. Employees: Employees needed company financial information because by analyzing

financial information they idenytify current company condition and decide whether they

must stay in the company or leave it (Sorrentino and Smarra, 2015).

(4)Importance of financial reporting for meeting objectives and growth

Financial reporting is give due priority by the business firms because it ensured that

accounting information will be presented in systematic manner and it will be easy to

understanding it just by taking single look on relevant statements. IFRS determine some of the

standards in respect to reporting of financial statements. IFRS also prescribe some of the formats

for income statement, balance sheet and cash flow statement. All firms in the specific nations

have to follow these standards tightly in the business so as to ensure that their financial

statements will be easy to compare with same of rivals and meaningful information will be

obtained easily. Thus, there is significent importance of financial reporting for the business

firms. Financial reporting helps firms in achieving growth this is because when any company

wants to form joint venture with any foreign company then in that case that nation firm will

demand firm financial statements and will measure firm performance. In case both firms

financial statements are prepared by following IFRS standards then in that situation it becom

easy to compare performance. Contrary to this, if IFRS is not followed then fair comparison is

not possible to be made between both firms. Long time is taken to make modifications in

financial statements in order to make comparison easy. Such kind of things demotivate firms

from entering in to such joint ventures easily because lots of time need to be spend on modifying

financial statements (Litt and et.al.,2014). Thus, it can be said that financial reporting assist firms

in achieving growth in their business. Main objective of many firms is to bring transparency in

the company business operations and to communicate more and more information to

stakeholders about the business. It is the financial reporting standards that ensure that only

relevant information will be depicted in the income statement and balance sheet and stakeholders

will be able to meausre company performance in proper manner. Thus, it can be said that

4 | P a g e

about company current business condition and direction in which company is performing.

Thus, it can be said that financial statements have huge importance for the firms because

it help them in making investment decisions. Employees: Employees needed company financial information because by analyzing

financial information they idenytify current company condition and decide whether they

must stay in the company or leave it (Sorrentino and Smarra, 2015).

(4)Importance of financial reporting for meeting objectives and growth

Financial reporting is give due priority by the business firms because it ensured that

accounting information will be presented in systematic manner and it will be easy to

understanding it just by taking single look on relevant statements. IFRS determine some of the

standards in respect to reporting of financial statements. IFRS also prescribe some of the formats

for income statement, balance sheet and cash flow statement. All firms in the specific nations

have to follow these standards tightly in the business so as to ensure that their financial

statements will be easy to compare with same of rivals and meaningful information will be

obtained easily. Thus, there is significent importance of financial reporting for the business

firms. Financial reporting helps firms in achieving growth this is because when any company

wants to form joint venture with any foreign company then in that case that nation firm will

demand firm financial statements and will measure firm performance. In case both firms

financial statements are prepared by following IFRS standards then in that situation it becom

easy to compare performance. Contrary to this, if IFRS is not followed then fair comparison is

not possible to be made between both firms. Long time is taken to make modifications in

financial statements in order to make comparison easy. Such kind of things demotivate firms

from entering in to such joint ventures easily because lots of time need to be spend on modifying

financial statements (Litt and et.al.,2014). Thus, it can be said that financial reporting assist firms

in achieving growth in their business. Main objective of many firms is to bring transparency in

the company business operations and to communicate more and more information to

stakeholders about the business. It is the financial reporting standards that ensure that only

relevant information will be depicted in the income statement and balance sheet and stakeholders

will be able to meausre company performance in proper manner. Thus, it can be said that

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial reporting help business firms in achieving their objective of making information to

stakeholders in simple manner.

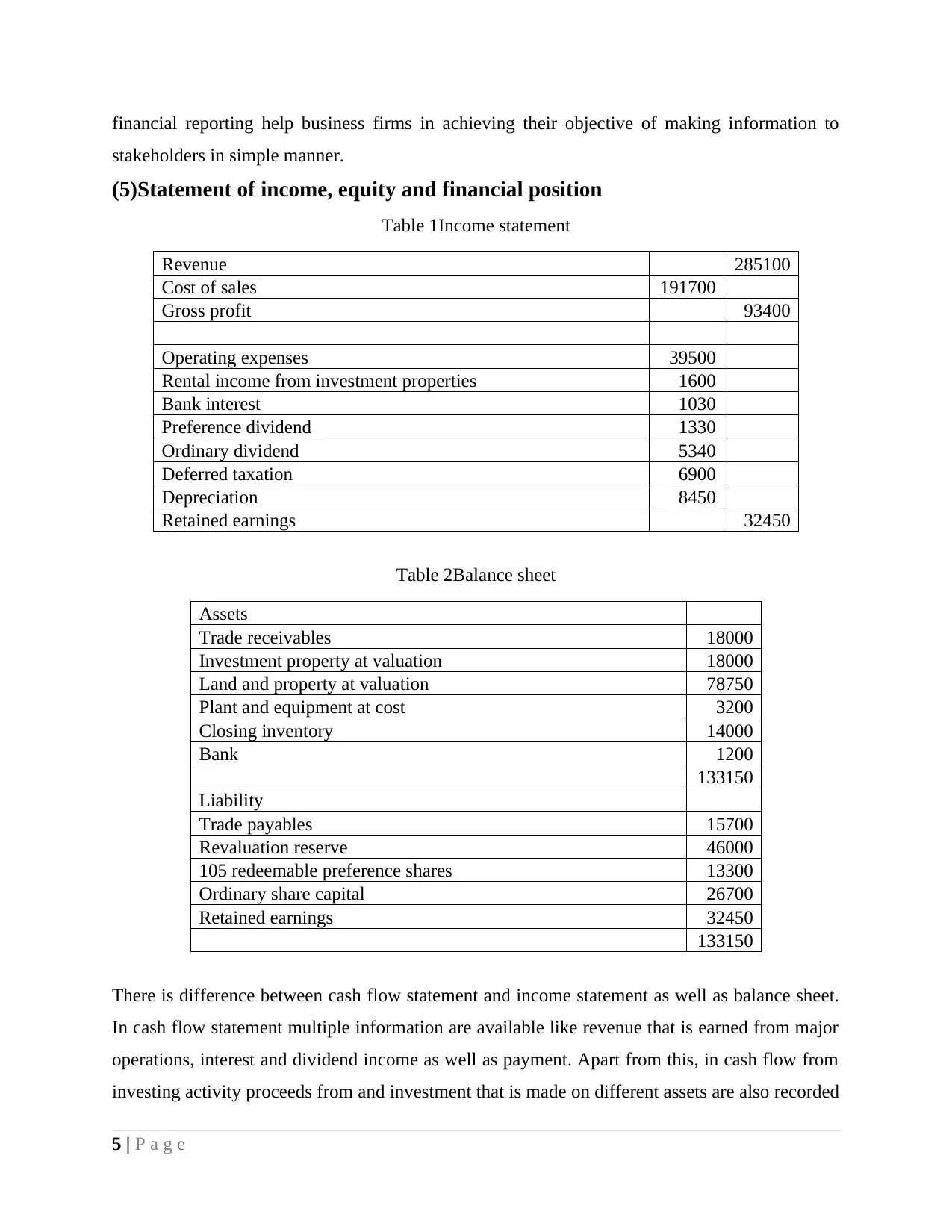

(5)Statement of income, equity and financial position

Table 1Income statement

Revenue 285100

Cost of sales 191700

Gross profit 93400

Operating expenses 39500

Rental income from investment properties 1600

Bank interest 1030

Preference dividend 1330

Ordinary dividend 5340

Deferred taxation 6900

Depreciation 8450

Retained earnings 32450

Table 2Balance sheet

Assets

Trade receivables 18000

Investment property at valuation 18000

Land and property at valuation 78750

Plant and equipment at cost 3200

Closing inventory 14000

Bank 1200

133150

Liability

Trade payables 15700

Revaluation reserve 46000

105 redeemable preference shares 13300

Ordinary share capital 26700

Retained earnings 32450

133150

There is difference between cash flow statement and income statement as well as balance sheet.

In cash flow statement multiple information are available like revenue that is earned from major

operations, interest and dividend income as well as payment. Apart from this, in cash flow from

investing activity proceeds from and investment that is made on different assets are also recorded

5 | P a g e

stakeholders in simple manner.

(5)Statement of income, equity and financial position

Table 1Income statement

Revenue 285100

Cost of sales 191700

Gross profit 93400

Operating expenses 39500

Rental income from investment properties 1600

Bank interest 1030

Preference dividend 1330

Ordinary dividend 5340

Deferred taxation 6900

Depreciation 8450

Retained earnings 32450

Table 2Balance sheet

Assets

Trade receivables 18000

Investment property at valuation 18000

Land and property at valuation 78750

Plant and equipment at cost 3200

Closing inventory 14000

Bank 1200

133150

Liability

Trade payables 15700

Revaluation reserve 46000

105 redeemable preference shares 13300

Ordinary share capital 26700

Retained earnings 32450

133150

There is difference between cash flow statement and income statement as well as balance sheet.

In cash flow statement multiple information are available like revenue that is earned from major

operations, interest and dividend income as well as payment. Apart from this, in cash flow from

investing activity proceeds from and investment that is made on different assets are also recorded

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which reflect the income from investment activities. In case of cash flow from financing activity

varied sources from which funds raised from the market and different income as well as

expenditures are recorded. From these things it can be said that cash flow statement is different

from income statement and balance sheet. This is because income statement does not reflect the

investment that is made in varied activties. Thus, it can be said that relative to income statement

cash flow statement provide more information to the managers and investors. Balance sheet and

cash flow statement are also quite different from each other (Li and Yang, 2015). It can be

observed that in case of cash flow statement operating activities information are also covered

whereas in balance sheet only information related to investing and financing activities are

covered. Hence, again it can be said that scope of cash flow statement is wide then income

statement and balance sheet. Investors, stakeholders and business owners must also make use

these statements altogether in order to make busines decisions and to find out areas where

organization strongly need to work in order to improve its performance at fast rate. However, it

is observed that sole properitors only prepare income statement because they just wants to know

about income earned and expenses made in the business. On other hand, partners give

importance to both statements because in balance sheet according to agreed proportion

classification of assets and liabilities happened. However, large firms require income statement,

balance sheet and cash flow statement because by using these they are able to evaluate business

widely and easily make business decisions.

6 | P a g e

varied sources from which funds raised from the market and different income as well as

expenditures are recorded. From these things it can be said that cash flow statement is different

from income statement and balance sheet. This is because income statement does not reflect the

investment that is made in varied activties. Thus, it can be said that relative to income statement

cash flow statement provide more information to the managers and investors. Balance sheet and

cash flow statement are also quite different from each other (Li and Yang, 2015). It can be

observed that in case of cash flow statement operating activities information are also covered

whereas in balance sheet only information related to investing and financing activities are

covered. Hence, again it can be said that scope of cash flow statement is wide then income

statement and balance sheet. Investors, stakeholders and business owners must also make use

these statements altogether in order to make busines decisions and to find out areas where

organization strongly need to work in order to improve its performance at fast rate. However, it

is observed that sole properitors only prepare income statement because they just wants to know

about income earned and expenses made in the business. On other hand, partners give

importance to both statements because in balance sheet according to agreed proportion

classification of assets and liabilities happened. However, large firms require income statement,

balance sheet and cash flow statement because by using these they are able to evaluate business

widely and easily make business decisions.

6 | P a g e

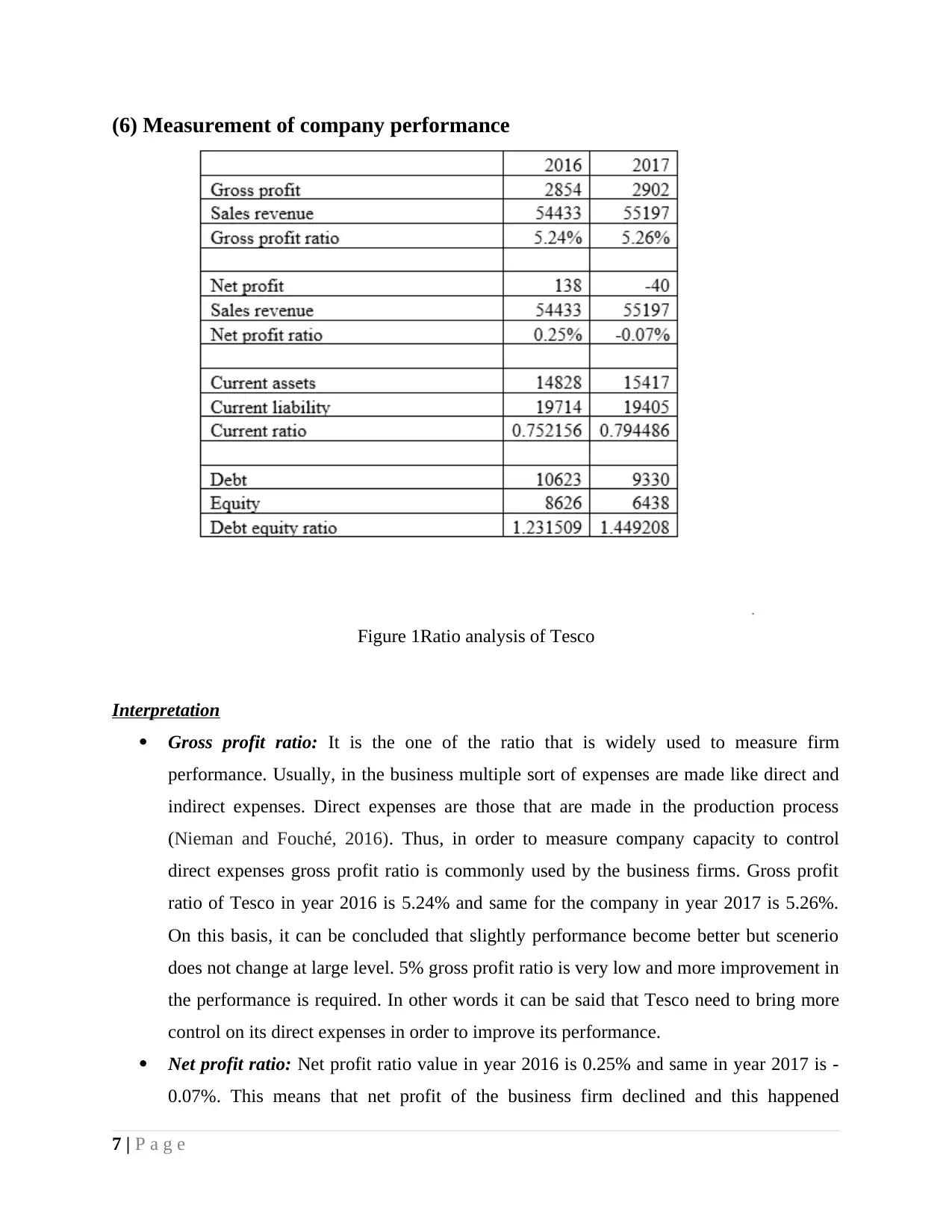

(6) Measurement of company performance

Figure 1Ratio analysis of Tesco

Interpretation

Gross profit ratio: It is the one of the ratio that is widely used to measure firm

performance. Usually, in the business multiple sort of expenses are made like direct and

indirect expenses. Direct expenses are those that are made in the production process

(Nieman and Fouché, 2016). Thus, in order to measure company capacity to control

direct expenses gross profit ratio is commonly used by the business firms. Gross profit

ratio of Tesco in year 2016 is 5.24% and same for the company in year 2017 is 5.26%.

On this basis, it can be concluded that slightly performance become better but scenerio

does not change at large level. 5% gross profit ratio is very low and more improvement in

the performance is required. In other words it can be said that Tesco need to bring more

control on its direct expenses in order to improve its performance.

Net profit ratio: Net profit ratio value in year 2016 is 0.25% and same in year 2017 is -

0.07%. This means that net profit of the business firm declined and this happened

7 | P a g e

Figure 1Ratio analysis of Tesco

Interpretation

Gross profit ratio: It is the one of the ratio that is widely used to measure firm

performance. Usually, in the business multiple sort of expenses are made like direct and

indirect expenses. Direct expenses are those that are made in the production process

(Nieman and Fouché, 2016). Thus, in order to measure company capacity to control

direct expenses gross profit ratio is commonly used by the business firms. Gross profit

ratio of Tesco in year 2016 is 5.24% and same for the company in year 2017 is 5.26%.

On this basis, it can be concluded that slightly performance become better but scenerio

does not change at large level. 5% gross profit ratio is very low and more improvement in

the performance is required. In other words it can be said that Tesco need to bring more

control on its direct expenses in order to improve its performance.

Net profit ratio: Net profit ratio value in year 2016 is 0.25% and same in year 2017 is -

0.07%. This means that net profit of the business firm declined and this happened

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because firm loose control on its indirect expenses. On basis of gross profit and net profit

ratio it can be observed that firm does not have control on its direct and indirect expenses.

This is one of the major problem that firm is facing in its business. It can be said that

company must formulate suitable strategy and under this it must use techniques like

process reengeniering and business analysis in its business. By using these approaches

business operations can be measured in proper manner and those stags that are

unproductive in nature can be removed from entire process. By doing so cost can be

controlled in the business and profitability can be elevated at fast rate.

Current ratio: Current ratio is the one of the important ratio that is used to measure the

liquidity position of the company (Warren, 2016). Higher is the value of current ratio it is

assumed that liquidity condition in the business is much better. Table given above is

reflecting that value of current ratio is 0.75 and same in year 2017 is 0.79. This means

that liquidity condition of company get improved to some extent. This means that firm

capability to pay current liability by using current assets increased to some extent in

comparison to previous time period. However, this is not sufficient as ideal current ratio

is 2:1 which means that for every one unit of current liability there must be double units

of current assets. In present case value of current ratio is less then 1 and this is indicating

that Tesco does not have sufficient quantity of current asset to pay current liability on

time. Hence, firm need to improve its performance and need to increase current assets in

business.

Debt equity ratio: Debt equity ratio is one of the ratio that is often used by finance

experts in their day to day work (Debt to equity ratio, 2017). Debt equity ratio value in

year 2016 was 1.23 which increased to 1.44 and this indicate that debt proportion relative

to equity increased but still situation is in control as debt is not just double of equity.

Hence, to large extent firm capital structure is balanced in nature but still work need to be

done and there is need to control debt in the capital structure.

(7) Difference between International accounting standard and International

financial reporting standard

There is difference between International accounting standard and International financial

reporting standards. Major difference between both is that former reflect the standards that need

to be followed in the business for recoding of transactions in the business. On other hand,

8 | P a g e

ratio it can be observed that firm does not have control on its direct and indirect expenses.

This is one of the major problem that firm is facing in its business. It can be said that

company must formulate suitable strategy and under this it must use techniques like

process reengeniering and business analysis in its business. By using these approaches

business operations can be measured in proper manner and those stags that are

unproductive in nature can be removed from entire process. By doing so cost can be

controlled in the business and profitability can be elevated at fast rate.

Current ratio: Current ratio is the one of the important ratio that is used to measure the

liquidity position of the company (Warren, 2016). Higher is the value of current ratio it is

assumed that liquidity condition in the business is much better. Table given above is

reflecting that value of current ratio is 0.75 and same in year 2017 is 0.79. This means

that liquidity condition of company get improved to some extent. This means that firm

capability to pay current liability by using current assets increased to some extent in

comparison to previous time period. However, this is not sufficient as ideal current ratio

is 2:1 which means that for every one unit of current liability there must be double units

of current assets. In present case value of current ratio is less then 1 and this is indicating

that Tesco does not have sufficient quantity of current asset to pay current liability on

time. Hence, firm need to improve its performance and need to increase current assets in

business.

Debt equity ratio: Debt equity ratio is one of the ratio that is often used by finance

experts in their day to day work (Debt to equity ratio, 2017). Debt equity ratio value in

year 2016 was 1.23 which increased to 1.44 and this indicate that debt proportion relative

to equity increased but still situation is in control as debt is not just double of equity.

Hence, to large extent firm capital structure is balanced in nature but still work need to be

done and there is need to control debt in the capital structure.

(7) Difference between International accounting standard and International

financial reporting standard

There is difference between International accounting standard and International financial

reporting standards. Major difference between both is that former reflect the standards that need

to be followed in the business for recoding of transactions in the business. On other hand,

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

international financial reporting standard reflect the rules that need to be followed for preparing

different sort of financial statements like income statement, balance sheet and cash flow

statement in terms of format and presentation of facts and information related to the company.

Thus, it is clear that both these are assisting organization and supporting accounting operations in

proper manner (Ewert and Wagenhofer, 2016). Standard related to IAS were published in 1973

and 2001 and in respect to IFRS standards were developed into year 2001. Issuer of both IAS

and IFRS are different from each other. IAS was issued by IASC and IFRS was developed by

IASB. Apart from this, there is difference between IAS and IFRS and it is that former does not

provide any information in which accounting related facts must be presented. On other hand, in

IFRS clearly some standards related to accounting are given and along with this way in which

financial information must be demonstrated is also clear. So, this is another area where IAS and

IFRS are different from each other.

(8) Evaluate the benefits of IFRS Focus on investors: IFRS assist firms in making all relevant information available to the

investors that can enable them to make business deicisons. It must be noted that in annual

report not only financial statements are available but along with this, varied information

are available in respect to company operations. Hence, it can be said that IFRS help firms

in treating their stakeholders in proper manner. Loss recognition timeliness: IFRS increase transparency of the company operations and

one just be taking a look at financial statements and annual report easily identify whether

firm make loss or earn profit in its business (Hope and Vyas, 2017). Comparability: IFRS is widely adopted by most of nations of the world and due to this

reason it become easy to compare financial statements of multiple firms operating in

different nations of the world. Apart from Europe in other continents also IFRS is

adopted and due to this reason it become easy to make comparison between different

firms operating in multiple nations of the world. Standardization of accounting and financial reporting: In IFRS on large scale many

rules and regulations are prepared in respect to accounting of records and presenting

these facts in annual report. Thus, it can be said that IFRS make presnetation of facts

effective in nature.

9 | P a g e

different sort of financial statements like income statement, balance sheet and cash flow

statement in terms of format and presentation of facts and information related to the company.

Thus, it is clear that both these are assisting organization and supporting accounting operations in

proper manner (Ewert and Wagenhofer, 2016). Standard related to IAS were published in 1973

and 2001 and in respect to IFRS standards were developed into year 2001. Issuer of both IAS

and IFRS are different from each other. IAS was issued by IASC and IFRS was developed by

IASB. Apart from this, there is difference between IAS and IFRS and it is that former does not

provide any information in which accounting related facts must be presented. On other hand, in

IFRS clearly some standards related to accounting are given and along with this way in which

financial information must be demonstrated is also clear. So, this is another area where IAS and

IFRS are different from each other.

(8) Evaluate the benefits of IFRS Focus on investors: IFRS assist firms in making all relevant information available to the

investors that can enable them to make business deicisons. It must be noted that in annual

report not only financial statements are available but along with this, varied information

are available in respect to company operations. Hence, it can be said that IFRS help firms

in treating their stakeholders in proper manner. Loss recognition timeliness: IFRS increase transparency of the company operations and

one just be taking a look at financial statements and annual report easily identify whether

firm make loss or earn profit in its business (Hope and Vyas, 2017). Comparability: IFRS is widely adopted by most of nations of the world and due to this

reason it become easy to compare financial statements of multiple firms operating in

different nations of the world. Apart from Europe in other continents also IFRS is

adopted and due to this reason it become easy to make comparison between different

firms operating in multiple nations of the world. Standardization of accounting and financial reporting: In IFRS on large scale many

rules and regulations are prepared in respect to accounting of records and presenting

these facts in annual report. Thus, it can be said that IFRS make presnetation of facts

effective in nature.

9 | P a g e

(9)Compliance with IFRS and elements in country that have impact on

compliance

It can be seen that with passage of time acceptance of IFRS increase at wide level. This is

because it become very difficult task to compare financial statements of two firms that operate in

two different nations if they are prepred by following different standards and reporting rules. In

last couple of years compliance with IFRS increased at rapid pace but there are number of factors

that have impact or affect compliance with IFRS. In every country there are different rules and

regulations related to reporting of financial statements. If any nation decide to follow IFRS then

in that case it have change its entire reporting system overnight which is not possible ( Pelger,

2016). In order amend nation reporting system lots of facts need to be taken in to account and

changes need to be made in standards which is long process and time consuming in nature.

Hence, many nations avoid to comply with IFRS. Apart from this, due to change in these

reporting standards tax reporting format and same of statutory reporting also get changed. Hence,

it can be said that change in reporting standards by doing replacement by IFRS is not an easy

task and due to this reason many nations avoid to comply with IFRS.

CONCLUSION

On basis of above discussion it is concluded that there is signficent importance of

acccounting standards for the business firms. This is because their usage ensured that all

transactions will be recorded at appropriate value. It is also concluded that more and more

nations are adopting IFRS but still there are many countries that are avoiding use of same for

accounting purpose. This is because it is hard task to change entire reporting structure overnight

in the nation. However, IFRS ensure that there will be transparency in the company operations

and shareholders will receive more information about company which will assist them in making

investment decisions. Hence, it can be said that there is huge significence of IFRS for the firms.

10 | P a g e

compliance

It can be seen that with passage of time acceptance of IFRS increase at wide level. This is

because it become very difficult task to compare financial statements of two firms that operate in

two different nations if they are prepred by following different standards and reporting rules. In

last couple of years compliance with IFRS increased at rapid pace but there are number of factors

that have impact or affect compliance with IFRS. In every country there are different rules and

regulations related to reporting of financial statements. If any nation decide to follow IFRS then

in that case it have change its entire reporting system overnight which is not possible ( Pelger,

2016). In order amend nation reporting system lots of facts need to be taken in to account and

changes need to be made in standards which is long process and time consuming in nature.

Hence, many nations avoid to comply with IFRS. Apart from this, due to change in these

reporting standards tax reporting format and same of statutory reporting also get changed. Hence,

it can be said that change in reporting standards by doing replacement by IFRS is not an easy

task and due to this reason many nations avoid to comply with IFRS.

CONCLUSION

On basis of above discussion it is concluded that there is signficent importance of

acccounting standards for the business firms. This is because their usage ensured that all

transactions will be recorded at appropriate value. It is also concluded that more and more

nations are adopting IFRS but still there are many countries that are avoiding use of same for

accounting purpose. This is because it is hard task to change entire reporting structure overnight

in the nation. However, IFRS ensure that there will be transparency in the company operations

and shareholders will receive more information about company which will assist them in making

investment decisions. Hence, it can be said that there is huge significence of IFRS for the firms.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.