Financial Reporting: Analysis of Financial Performance and Ratios

VerifiedAdded on 2020/06/04

|17

|4117

|46

Report

AI Summary

This report provides a comprehensive overview of financial reporting (FR), including its objectives, conceptual frameworks (IFRS and IAS), and basic principles. It examines the stakeholders who use financial data and the value of FR in achieving business objectives and growth. The report includes the preparation of financial statements (P&L, Balance Sheet, and Statement of Changes in Equity) from a trial balance for Rita Plc. Furthermore, it interprets the business performance of Marks and Spencer using financial ratios such as profitability, liquidity, and gearing ratios, offering insights into the company's financial health and performance trends. The analysis highlights the importance of financial planning and cost management for improving business outcomes.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

At the workplace of an entity, it is mandatory to publish all the financial statements

among stakeholders in legal direction when it is a limited firm. Further, procedure in which main

accounts of the financial are prepared and published is known as financial reporting (FR). The

current assignment focuses on various objectives or purposes of FR through which company

become beneficial. The FR system consists with various standards as well as principles which

are also explained in this project. Moreover, throughout the project process of formulating

financial statements with the help of only trial balance of firm is reflected. Apart from this,

financial performance of Marks and Spencer is presented which is a retailer and listed in FTSE

100 component. Besides these, IFRS and IAS concepts are explained along with making

difference among these. At the end of current study, advantages of IFRS towards an enterprise

and factors influence to compliance with this are described.

1. Context along with key purposes of financial reporting

FR is considered as an important tool for assessing financials of the company in proper

way. Until adequate information related to financial is not transacted and tracked effectually then

entrepreneur or managers cannot make effective type of decisions towards it. Furthermore, its

various key objectives are stated below:

FR allows firms for tracking business information related to financials like cost, margin,

liquidity, expenditures etc. Therefore, firm can employ fruitful techniques to boost up its

performance across the sector.

When financial plan is needed to formulate, implement, analyse, monitor and execute in

the firm then also FR is helpful. Ultimately, management will become able to meet all

goals and purposes which are desired at the time of making this plan (Nandwa, 2016).

FR is an operation of accounting in which cash flows like payments as well as receipts

are properly disclosed in front of the company. Due to this, availability of cash level can

be ascertained which helps to make fund raising decisions using better alternative.

Using the concept of FR, entrepreneur can assess that firm is up to which extent sound in

terms of financials in the industry. On the basis of this, effectual techniques and tactics

are executed which help to enhance business performance in adequate manner.

1

At the workplace of an entity, it is mandatory to publish all the financial statements

among stakeholders in legal direction when it is a limited firm. Further, procedure in which main

accounts of the financial are prepared and published is known as financial reporting (FR). The

current assignment focuses on various objectives or purposes of FR through which company

become beneficial. The FR system consists with various standards as well as principles which

are also explained in this project. Moreover, throughout the project process of formulating

financial statements with the help of only trial balance of firm is reflected. Apart from this,

financial performance of Marks and Spencer is presented which is a retailer and listed in FTSE

100 component. Besides these, IFRS and IAS concepts are explained along with making

difference among these. At the end of current study, advantages of IFRS towards an enterprise

and factors influence to compliance with this are described.

1. Context along with key purposes of financial reporting

FR is considered as an important tool for assessing financials of the company in proper

way. Until adequate information related to financial is not transacted and tracked effectually then

entrepreneur or managers cannot make effective type of decisions towards it. Furthermore, its

various key objectives are stated below:

FR allows firms for tracking business information related to financials like cost, margin,

liquidity, expenditures etc. Therefore, firm can employ fruitful techniques to boost up its

performance across the sector.

When financial plan is needed to formulate, implement, analyse, monitor and execute in

the firm then also FR is helpful. Ultimately, management will become able to meet all

goals and purposes which are desired at the time of making this plan (Nandwa, 2016).

FR is an operation of accounting in which cash flows like payments as well as receipts

are properly disclosed in front of the company. Due to this, availability of cash level can

be ascertained which helps to make fund raising decisions using better alternative.

Using the concept of FR, entrepreneur can assess that firm is up to which extent sound in

terms of financials in the industry. On the basis of this, effectual techniques and tactics

are executed which help to enhance business performance in adequate manner.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

When economic resources are needed to analyse and disclose mandatory obligations then

also FR is taken into account by most of the businesses. The reason is that, it helps to

make effectual decisions related to making investment in the best option.

Moreover, financial reporting represents assets, liabilities of the firm along with capital

raised by owner in front of internal stakeholders (Nobes, 2014). Therefore, managers and

owner able to take those decisions which come under the financial position.

2. Conceptual frameworks and basic principles of FR

In the FR different bodies and frameworks are included through which required

principles are amended. Due to lack of these, the company cannot consider in the workplace and

formulate needed statements properly. Under this, basic two kinds of the frameworks are

associated which are IFRS as well as IAS. These both give clear outline to the accountant that

which kind of transaction has to treated in which manner in final accounts. Further FR basically

comprises with several principles which help to make accounting adjustments effectively (Ball,

Jayaraman and Shivakumar, 2012). Among them, key principles are listed below:

Consistency principle

Expense or cost related

Going concern

Continuity

Unit-of-measure

Matching

Separate entity assumption

Revenue related principle

Objectivity etc.

Apart from this, the quantitative kind of research shows overall analysis in numerical way

which sometimes easily understood by all people. The reason is that, only financial employees

and stakeholders can create understanding about this. However, when study is of the qualitative

nature then presents whole interpretation in theoretical formate. Due to this, everyone can easily

2

also FR is taken into account by most of the businesses. The reason is that, it helps to

make effectual decisions related to making investment in the best option.

Moreover, financial reporting represents assets, liabilities of the firm along with capital

raised by owner in front of internal stakeholders (Nobes, 2014). Therefore, managers and

owner able to take those decisions which come under the financial position.

2. Conceptual frameworks and basic principles of FR

In the FR different bodies and frameworks are included through which required

principles are amended. Due to lack of these, the company cannot consider in the workplace and

formulate needed statements properly. Under this, basic two kinds of the frameworks are

associated which are IFRS as well as IAS. These both give clear outline to the accountant that

which kind of transaction has to treated in which manner in final accounts. Further FR basically

comprises with several principles which help to make accounting adjustments effectively (Ball,

Jayaraman and Shivakumar, 2012). Among them, key principles are listed below:

Consistency principle

Expense or cost related

Going concern

Continuity

Unit-of-measure

Matching

Separate entity assumption

Revenue related principle

Objectivity etc.

Apart from this, the quantitative kind of research shows overall analysis in numerical way

which sometimes easily understood by all people. The reason is that, only financial employees

and stakeholders can create understanding about this. However, when study is of the qualitative

nature then presents whole interpretation in theoretical formate. Due to this, everyone can easily

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understand the concepts and analysis mentioned (Dyreng, Mayew and Williams, 2012).

Therefore, qualitative research is highly better and effective for the company as compared to

another stated i.e. quantitative.

3. Stakeholders of an entity and reasons for which they use financial data

When the financial statements are published then utilised by various people whether are

associated with organisation internally or externally. The reason is that, it is one type of

indication for evaluating business performance and take decisions towards enterprise. Majority

of stakeholders when going to engage with a firm then use such data which are stated below:

Managers are associated with firm internally who use financial data to review all the

expenses, incomes and cash availability. Further, overall financial performance is to be

analysed where effective decisions related to investment, expenditures, purchasing etc.

are taken. Therefore, to make such types of the judgements in enterprise managers utilise

this data.

Shareholders utilise published financials to make investment decisions or purchase the

shares of it. These are concerned for dividend amount and returns which is possible with

profits of entity only (Cheng, Dhaliwal and Zhang, 2013). From the statements if

shareholders found that management provides adequate dividends, bonus shares, and

gains plenty profit then they will invest higher amount.

Employees are key assets for an organisation who expect that, it will give fair and

adequate wages, allowances, bonuses, monetary rewards etc. From the analysis of

financial data if they find out that firm has capability for generating huge incomes then

they will try to engage with it. On the other side, if cannot earn better level of margins

then they will not include with it.

Customers use such reports for assessing profit condition because when this aspect is

higher, then firm able to provide better quality of the goods and services. Along with this,

due to having huge benefits such stakeholders expect that company will offer products at

lower price as compared to rivals (Gibson, 2012).

3

Therefore, qualitative research is highly better and effective for the company as compared to

another stated i.e. quantitative.

3. Stakeholders of an entity and reasons for which they use financial data

When the financial statements are published then utilised by various people whether are

associated with organisation internally or externally. The reason is that, it is one type of

indication for evaluating business performance and take decisions towards enterprise. Majority

of stakeholders when going to engage with a firm then use such data which are stated below:

Managers are associated with firm internally who use financial data to review all the

expenses, incomes and cash availability. Further, overall financial performance is to be

analysed where effective decisions related to investment, expenditures, purchasing etc.

are taken. Therefore, to make such types of the judgements in enterprise managers utilise

this data.

Shareholders utilise published financials to make investment decisions or purchase the

shares of it. These are concerned for dividend amount and returns which is possible with

profits of entity only (Cheng, Dhaliwal and Zhang, 2013). From the statements if

shareholders found that management provides adequate dividends, bonus shares, and

gains plenty profit then they will invest higher amount.

Employees are key assets for an organisation who expect that, it will give fair and

adequate wages, allowances, bonuses, monetary rewards etc. From the analysis of

financial data if they find out that firm has capability for generating huge incomes then

they will try to engage with it. On the other side, if cannot earn better level of margins

then they will not include with it.

Customers use such reports for assessing profit condition because when this aspect is

higher, then firm able to provide better quality of the goods and services. Along with this,

due to having huge benefits such stakeholders expect that company will offer products at

lower price as compared to rivals (Gibson, 2012).

3

Government also use financial data of the firm in order to determine tax payable

capacity. Further, it enterprise has more profit, then it will insist to take some

responsibilities of social welfare.

4. Value of FR for achieving business objectives and growth

In the above section, it has been mentioned that for tracking financial information which

highly needed FR is a supportive method. Along with this, it helps to prepare and interpret

financials in proper structure. On the basis of these all, actual performance and status of the firm

can be seen in the relevant market segment. During this, if management founds that firm

generates adequate kind of profit and manage all the expenses in profitable direction then will

frame strategies for earning more. However, in the process of financial statement's evaluation if

any issues and lacks are determined then corrective actions can be taken. Therefore, the firm

easily able to raise performance as it is basic objective for every entrepreneur. Apart from this,

for deriving that up to which extent the firm utilise resources also FR supports properly

(Guerreiro, Rodrigues and Craig, 2012). By this, it can know tactics which are mandatory to

apply in workplace for boosting performance. In order to ascertain a global or national entity

whether achieve its financial goals or not also FR is highly useful. Therefore, can employ

effectual strategies and cam achieve goals and objectives smoothly. Further, ultimately growth of

that business will be enhanced on consistent basis in the industry where it has presence.

5. Preparing financial considering a Trial balance

The present part of whole reports reflects financial statements of Rita Plc company for

the accounting period ending 31st December 2016. Under this, with the help of Trial Balance

P&L, B/S and statements of equity and gains changes are formulated as below:

4

capacity. Further, it enterprise has more profit, then it will insist to take some

responsibilities of social welfare.

4. Value of FR for achieving business objectives and growth

In the above section, it has been mentioned that for tracking financial information which

highly needed FR is a supportive method. Along with this, it helps to prepare and interpret

financials in proper structure. On the basis of these all, actual performance and status of the firm

can be seen in the relevant market segment. During this, if management founds that firm

generates adequate kind of profit and manage all the expenses in profitable direction then will

frame strategies for earning more. However, in the process of financial statement's evaluation if

any issues and lacks are determined then corrective actions can be taken. Therefore, the firm

easily able to raise performance as it is basic objective for every entrepreneur. Apart from this,

for deriving that up to which extent the firm utilise resources also FR supports properly

(Guerreiro, Rodrigues and Craig, 2012). By this, it can know tactics which are mandatory to

apply in workplace for boosting performance. In order to ascertain a global or national entity

whether achieve its financial goals or not also FR is highly useful. Therefore, can employ

effectual strategies and cam achieve goals and objectives smoothly. Further, ultimately growth of

that business will be enhanced on consistent basis in the industry where it has presence.

5. Preparing financial considering a Trial balance

The present part of whole reports reflects financial statements of Rita Plc company for

the accounting period ending 31st December 2016. Under this, with the help of Trial Balance

P&L, B/S and statements of equity and gains changes are formulated as below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

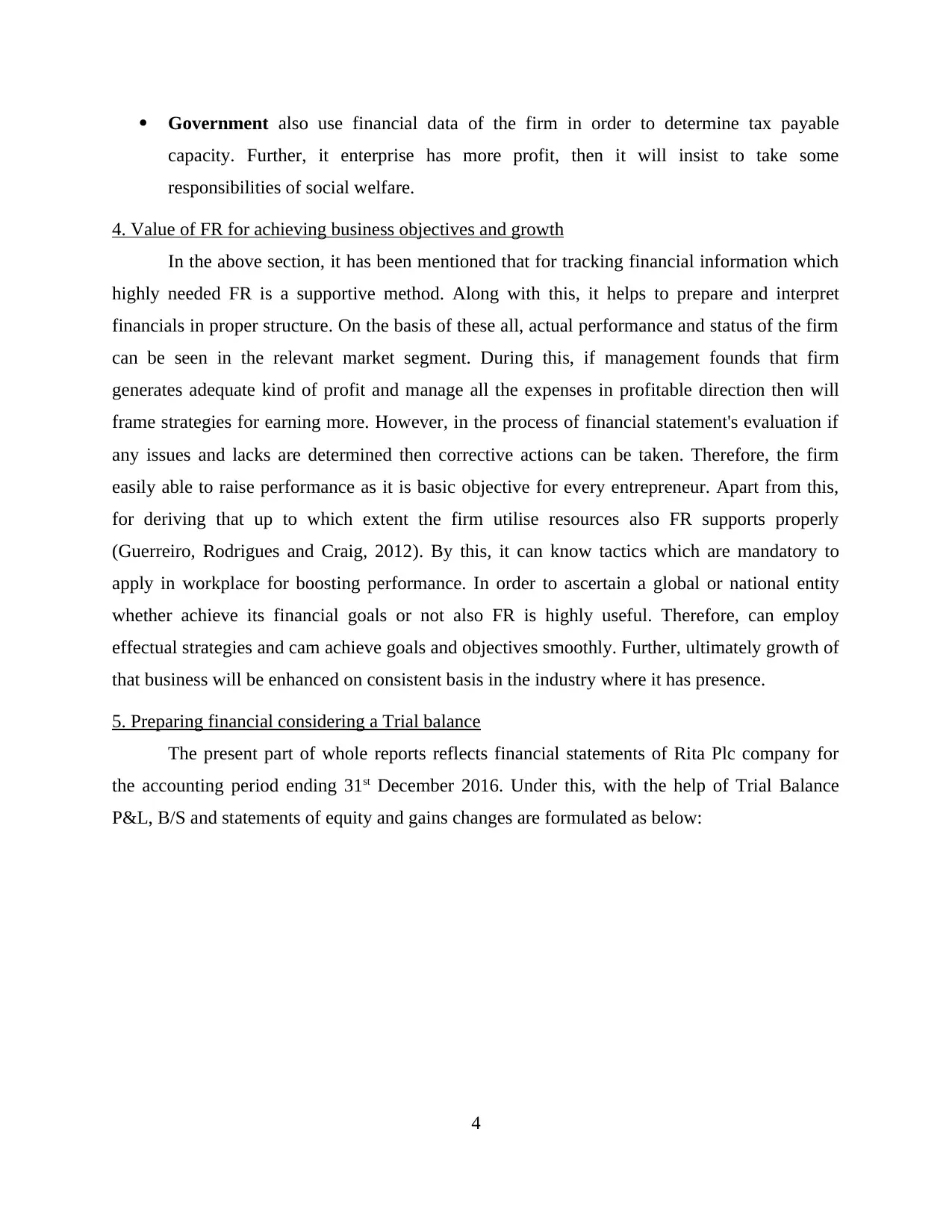

A. Statements of profit and loss

As per the above prepared P&L account, the Rita Plc generates gross profit worth of

272700 GBP at the end of FY 2016. When looking at operating incomes then it is also better

because expenses of operating are 39500 GBP. Moreover, OP of the cited enterprise is worth of

233200 GBP. Net profit which is final margin of the company earned by Rita Plc is worth of

161600 GBP at the sales amount of 285100 GBP in the accounting year ending 2016.

Considering the whole expenses and incomes it can be said that financial burden imposed is

worth of 123500 GBP (285100−161600) through the year 2016. At this position, Rita Plc

generates 56.68% net income which is adequate. On the basis of this it can be commented that,

the selected company used cost management techniques in whole year due to which performs

better in the industry.

5

As per the above prepared P&L account, the Rita Plc generates gross profit worth of

272700 GBP at the end of FY 2016. When looking at operating incomes then it is also better

because expenses of operating are 39500 GBP. Moreover, OP of the cited enterprise is worth of

233200 GBP. Net profit which is final margin of the company earned by Rita Plc is worth of

161600 GBP at the sales amount of 285100 GBP in the accounting year ending 2016.

Considering the whole expenses and incomes it can be said that financial burden imposed is

worth of 123500 GBP (285100−161600) through the year 2016. At this position, Rita Plc

generates 56.68% net income which is adequate. On the basis of this it can be commented that,

the selected company used cost management techniques in whole year due to which performs

better in the industry.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

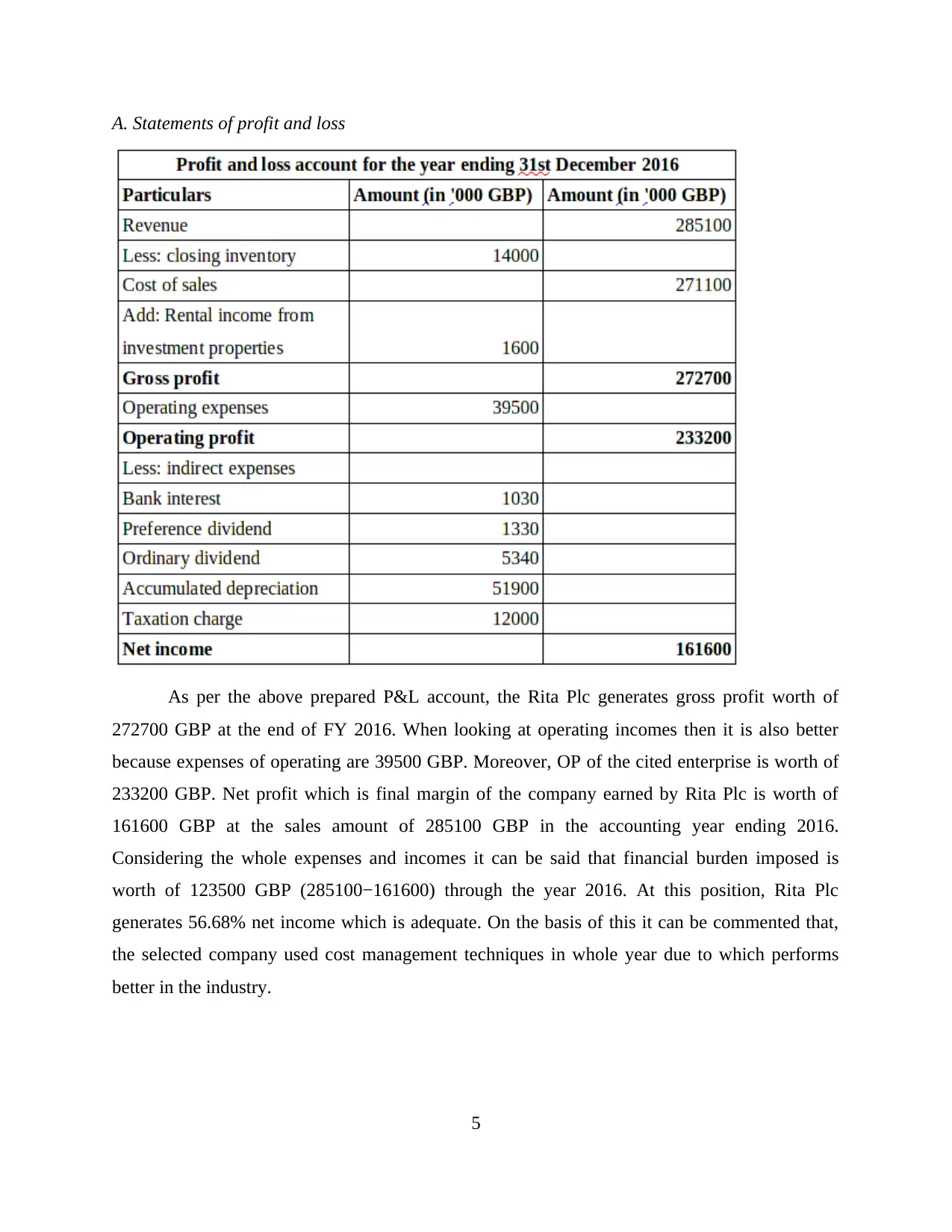

B. Statement for changes in equity and gains

C. Statement of the financial position

6. Interpreting business performance of Marks and Spencer by taking support of financial ratios

The present section of FR study comprises with the business performance for which some

ratios are calculated properly. In order to accomplish this task, Marks and Spencer organisation

is taken into account which has global presence in retail industry. When looking at the stock

market then it listed in LSE and FTSE 100 component. Further, it is public limited company and

originated from the country UK. In order to assess its financial performance, data gathered from

the past financials accounts like P&L, B/S etc (Flower, 2016). Higher the level of this kind of

performance creates brand image in the industry and attracts various stakeholders. In the present

scenario basically three financial ratios are computed which are profitability, gearing and

liquidity, stated below:

Profitability ratios Formula 2016 2017

Operating profit (OP) 515 190

6

C. Statement of the financial position

6. Interpreting business performance of Marks and Spencer by taking support of financial ratios

The present section of FR study comprises with the business performance for which some

ratios are calculated properly. In order to accomplish this task, Marks and Spencer organisation

is taken into account which has global presence in retail industry. When looking at the stock

market then it listed in LSE and FTSE 100 component. Further, it is public limited company and

originated from the country UK. In order to assess its financial performance, data gathered from

the past financials accounts like P&L, B/S etc (Flower, 2016). Higher the level of this kind of

performance creates brand image in the industry and attracts various stakeholders. In the present

scenario basically three financial ratios are computed which are profitability, gearing and

liquidity, stated below:

Profitability ratios Formula 2016 2017

Operating profit (OP) 515 190

6

Net profit (NP) 407 117

Sales revenue 10555 10622

Operating profit ratio OP / Sales revenue * 100 4.88% 1.79%

Net profit ratio NP / Sales revenue * 100 3.86% 1.10%

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.88%

1.79%

Illustration 1: Operating profit ratio

2016 2017

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

3.86%

1.10%

Illustration 2: Net profit ratio

7

Sales revenue 10555 10622

Operating profit ratio OP / Sales revenue * 100 4.88% 1.79%

Net profit ratio NP / Sales revenue * 100 3.86% 1.10%

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.88%

1.79%

Illustration 1: Operating profit ratio

2016 2017

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

3.86%

1.10%

Illustration 2: Net profit ratio

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis: From the above presented calculation and graphs it can be seen that, OP ratio

was 4.88% at the end of an accounting period 2016. As one year passed i.e. 2017 then same ratio

decreased which is as of now 1.79%. Therefore, the management of M&S is not efficient for

utilising available resources which lead to boost up operating expenses. Further, declining ratio

of NP from 3.86% to 1.10% is also one kind of indication of reducing business performance. As

per both ratios of profitability the retailer has poor performance. Basic reason behind is lack of

proper financial planning along with effective cost management (Marks & Spencer Group PLC.

2017). Hence, the firm requires using attractive marketing strategies and reducing cost methods.

These will help to enhance sales as well as margin in the future years.

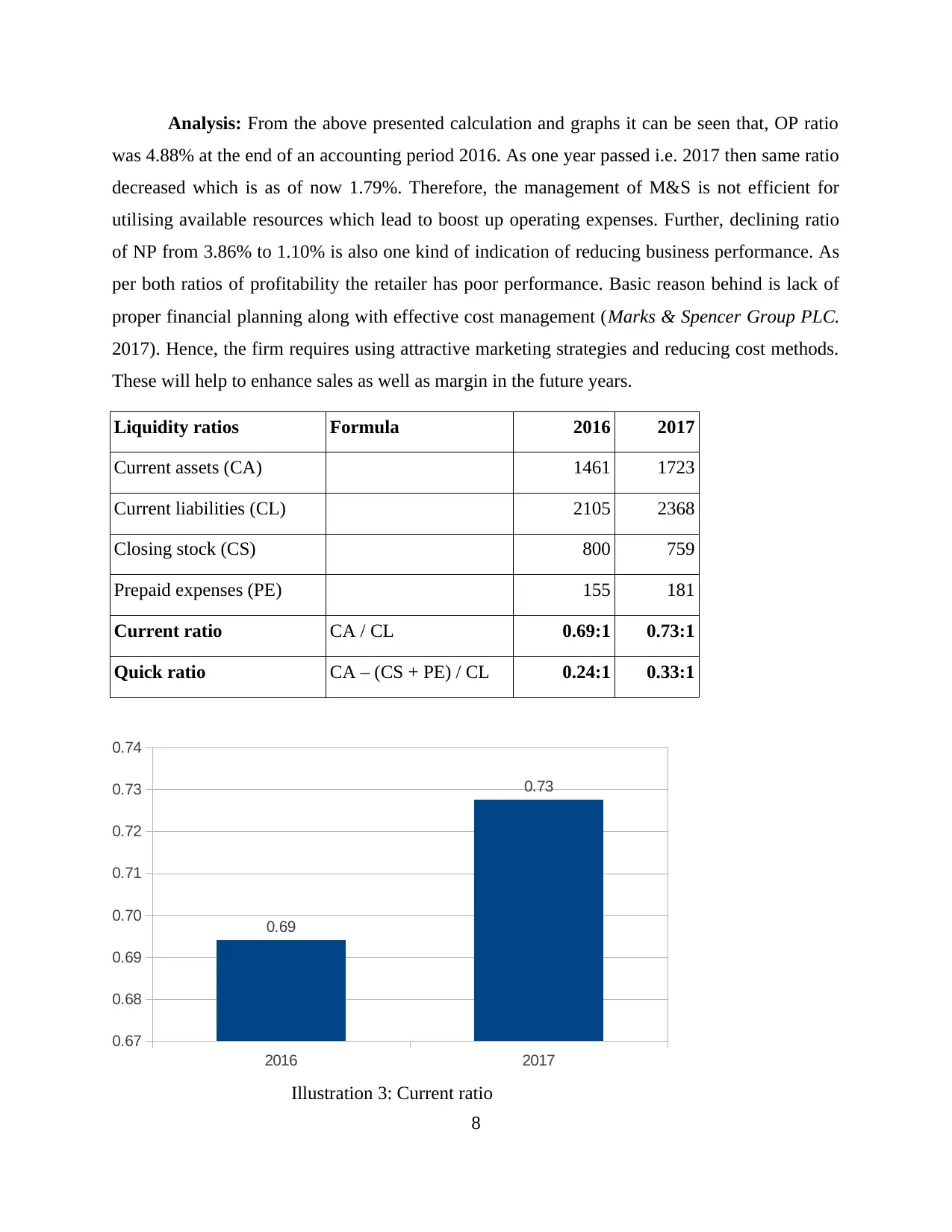

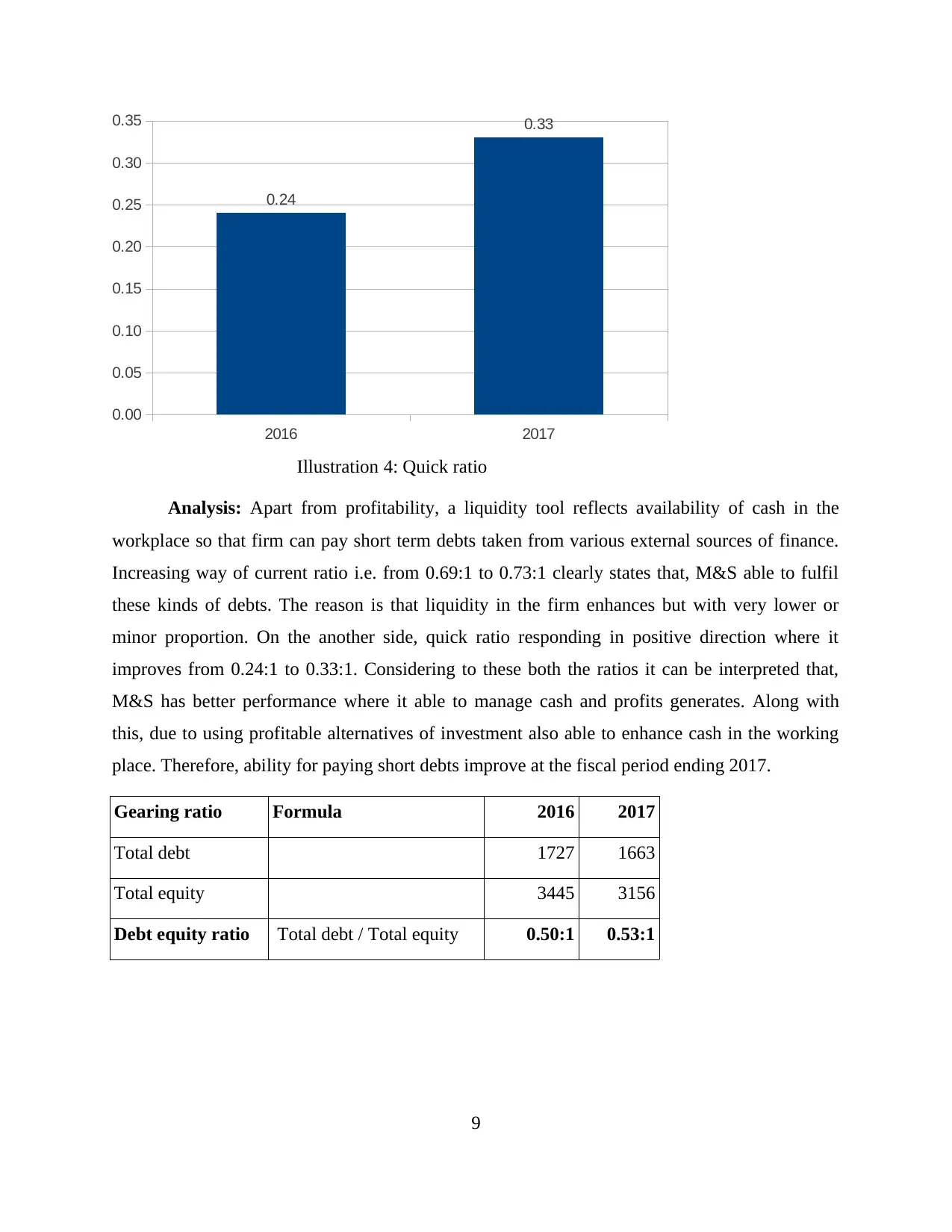

Liquidity ratios Formula 2016 2017

Current assets (CA) 1461 1723

Current liabilities (CL) 2105 2368

Closing stock (CS) 800 759

Prepaid expenses (PE) 155 181

Current ratio CA / CL 0.69:1 0.73:1

Quick ratio CA – (CS + PE) / CL 0.24:1 0.33:1

2016 2017

0.67

0.68

0.69

0.70

0.71

0.72

0.73

0.74

0.69

0.73

Illustration 3: Current ratio

8

was 4.88% at the end of an accounting period 2016. As one year passed i.e. 2017 then same ratio

decreased which is as of now 1.79%. Therefore, the management of M&S is not efficient for

utilising available resources which lead to boost up operating expenses. Further, declining ratio

of NP from 3.86% to 1.10% is also one kind of indication of reducing business performance. As

per both ratios of profitability the retailer has poor performance. Basic reason behind is lack of

proper financial planning along with effective cost management (Marks & Spencer Group PLC.

2017). Hence, the firm requires using attractive marketing strategies and reducing cost methods.

These will help to enhance sales as well as margin in the future years.

Liquidity ratios Formula 2016 2017

Current assets (CA) 1461 1723

Current liabilities (CL) 2105 2368

Closing stock (CS) 800 759

Prepaid expenses (PE) 155 181

Current ratio CA / CL 0.69:1 0.73:1

Quick ratio CA – (CS + PE) / CL 0.24:1 0.33:1

2016 2017

0.67

0.68

0.69

0.70

0.71

0.72

0.73

0.74

0.69

0.73

Illustration 3: Current ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.24

0.33

Illustration 4: Quick ratio

Analysis: Apart from profitability, a liquidity tool reflects availability of cash in the

workplace so that firm can pay short term debts taken from various external sources of finance.

Increasing way of current ratio i.e. from 0.69:1 to 0.73:1 clearly states that, M&S able to fulfil

these kinds of debts. The reason is that liquidity in the firm enhances but with very lower or

minor proportion. On the another side, quick ratio responding in positive direction where it

improves from 0.24:1 to 0.33:1. Considering to these both the ratios it can be interpreted that,

M&S has better performance where it able to manage cash and profits generates. Along with

this, due to using profitable alternatives of investment also able to enhance cash in the working

place. Therefore, ability for paying short debts improve at the fiscal period ending 2017.

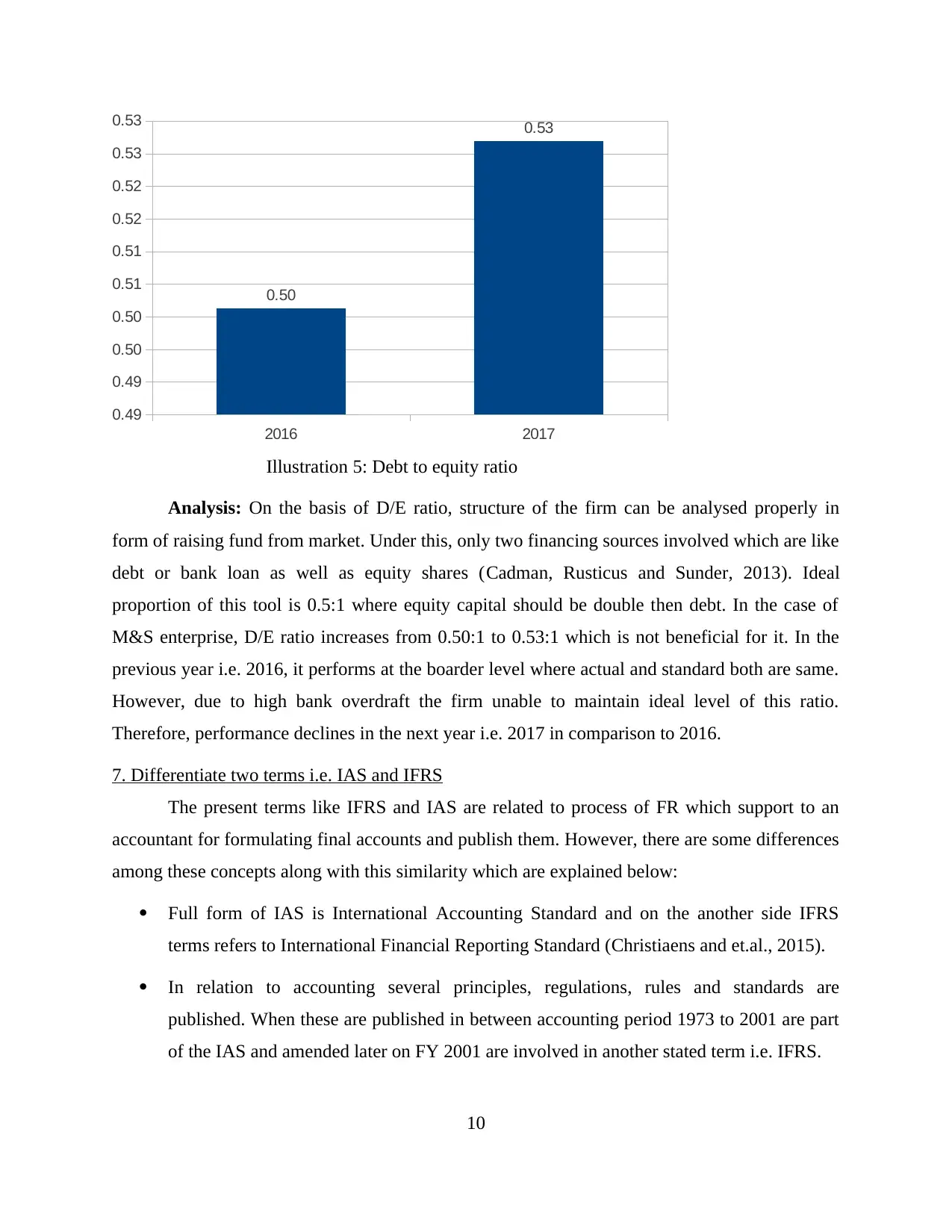

Gearing ratio Formula 2016 2017

Total debt 1727 1663

Total equity 3445 3156

Debt equity ratio Total debt / Total equity 0.50:1 0.53:1

9

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.24

0.33

Illustration 4: Quick ratio

Analysis: Apart from profitability, a liquidity tool reflects availability of cash in the

workplace so that firm can pay short term debts taken from various external sources of finance.

Increasing way of current ratio i.e. from 0.69:1 to 0.73:1 clearly states that, M&S able to fulfil

these kinds of debts. The reason is that liquidity in the firm enhances but with very lower or

minor proportion. On the another side, quick ratio responding in positive direction where it

improves from 0.24:1 to 0.33:1. Considering to these both the ratios it can be interpreted that,

M&S has better performance where it able to manage cash and profits generates. Along with

this, due to using profitable alternatives of investment also able to enhance cash in the working

place. Therefore, ability for paying short debts improve at the fiscal period ending 2017.

Gearing ratio Formula 2016 2017

Total debt 1727 1663

Total equity 3445 3156

Debt equity ratio Total debt / Total equity 0.50:1 0.53:1

9

2016 2017

0.49

0.49

0.50

0.50

0.51

0.51

0.52

0.52

0.53

0.53

0.50

0.53

Illustration 5: Debt to equity ratio

Analysis: On the basis of D/E ratio, structure of the firm can be analysed properly in

form of raising fund from market. Under this, only two financing sources involved which are like

debt or bank loan as well as equity shares (Cadman, Rusticus and Sunder, 2013). Ideal

proportion of this tool is 0.5:1 where equity capital should be double then debt. In the case of

M&S enterprise, D/E ratio increases from 0.50:1 to 0.53:1 which is not beneficial for it. In the

previous year i.e. 2016, it performs at the boarder level where actual and standard both are same.

However, due to high bank overdraft the firm unable to maintain ideal level of this ratio.

Therefore, performance declines in the next year i.e. 2017 in comparison to 2016.

7. Differentiate two terms i.e. IAS and IFRS

The present terms like IFRS and IAS are related to process of FR which support to an

accountant for formulating final accounts and publish them. However, there are some differences

among these concepts along with this similarity which are explained below:

Full form of IAS is International Accounting Standard and on the another side IFRS

terms refers to International Financial Reporting Standard (Christiaens and et.al., 2015).

In relation to accounting several principles, regulations, rules and standards are

published. When these are published in between accounting period 1973 to 2001 are part

of the IAS and amended later on FY 2001 are involved in another stated term i.e. IFRS.

10

0.49

0.49

0.50

0.50

0.51

0.51

0.52

0.52

0.53

0.53

0.50

0.53

Illustration 5: Debt to equity ratio

Analysis: On the basis of D/E ratio, structure of the firm can be analysed properly in

form of raising fund from market. Under this, only two financing sources involved which are like

debt or bank loan as well as equity shares (Cadman, Rusticus and Sunder, 2013). Ideal

proportion of this tool is 0.5:1 where equity capital should be double then debt. In the case of

M&S enterprise, D/E ratio increases from 0.50:1 to 0.53:1 which is not beneficial for it. In the

previous year i.e. 2016, it performs at the boarder level where actual and standard both are same.

However, due to high bank overdraft the firm unable to maintain ideal level of this ratio.

Therefore, performance declines in the next year i.e. 2017 in comparison to 2016.

7. Differentiate two terms i.e. IAS and IFRS

The present terms like IFRS and IAS are related to process of FR which support to an

accountant for formulating final accounts and publish them. However, there are some differences

among these concepts along with this similarity which are explained below:

Full form of IAS is International Accounting Standard and on the another side IFRS

terms refers to International Financial Reporting Standard (Christiaens and et.al., 2015).

In relation to accounting several principles, regulations, rules and standards are

published. When these are published in between accounting period 1973 to 2001 are part

of the IAS and amended later on FY 2001 are involved in another stated term i.e. IFRS.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.