Accounting Policies and Estimates for PPE: Origin Energy Analysis

VerifiedAdded on 2022/10/02

|11

|1824

|65

Report

AI Summary

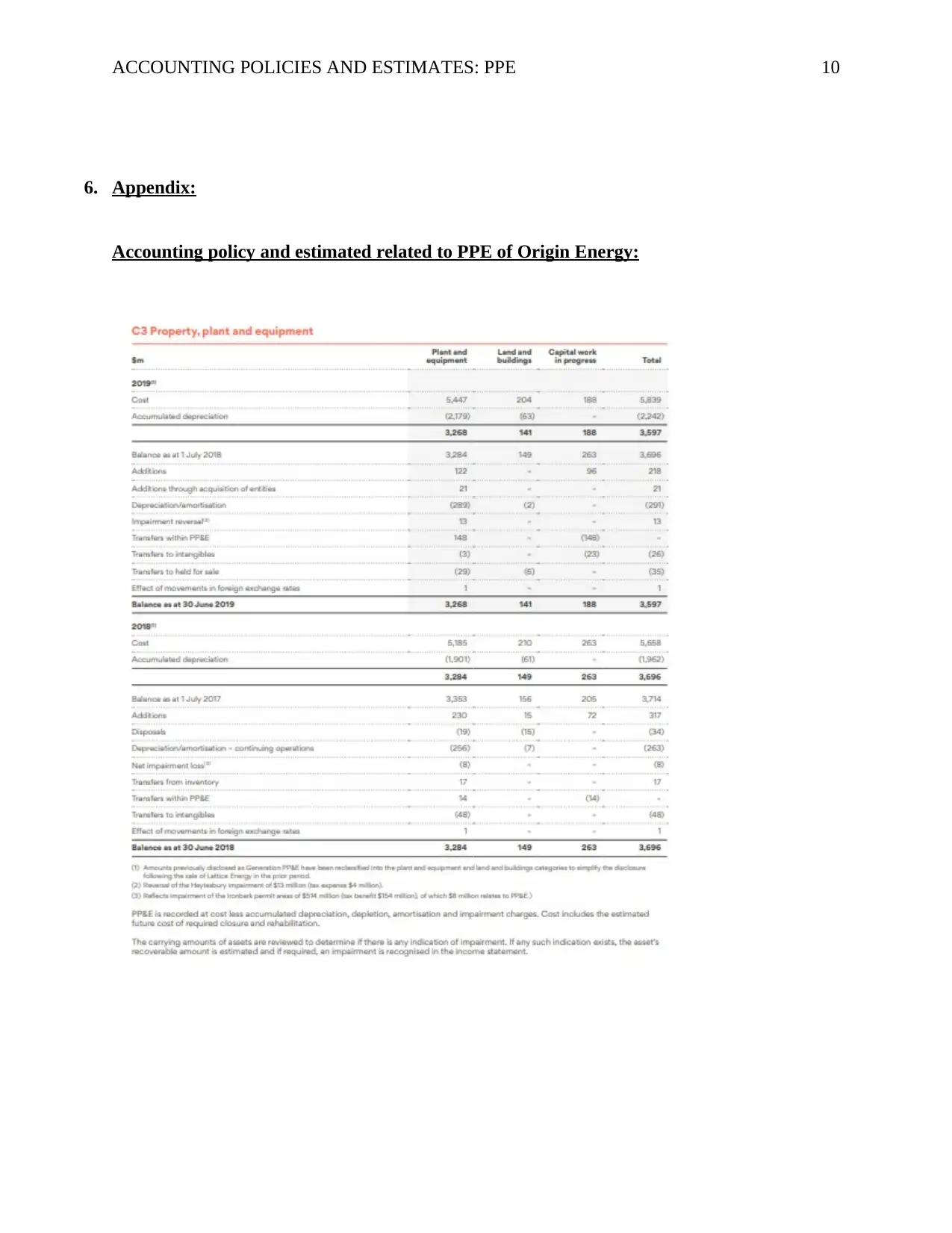

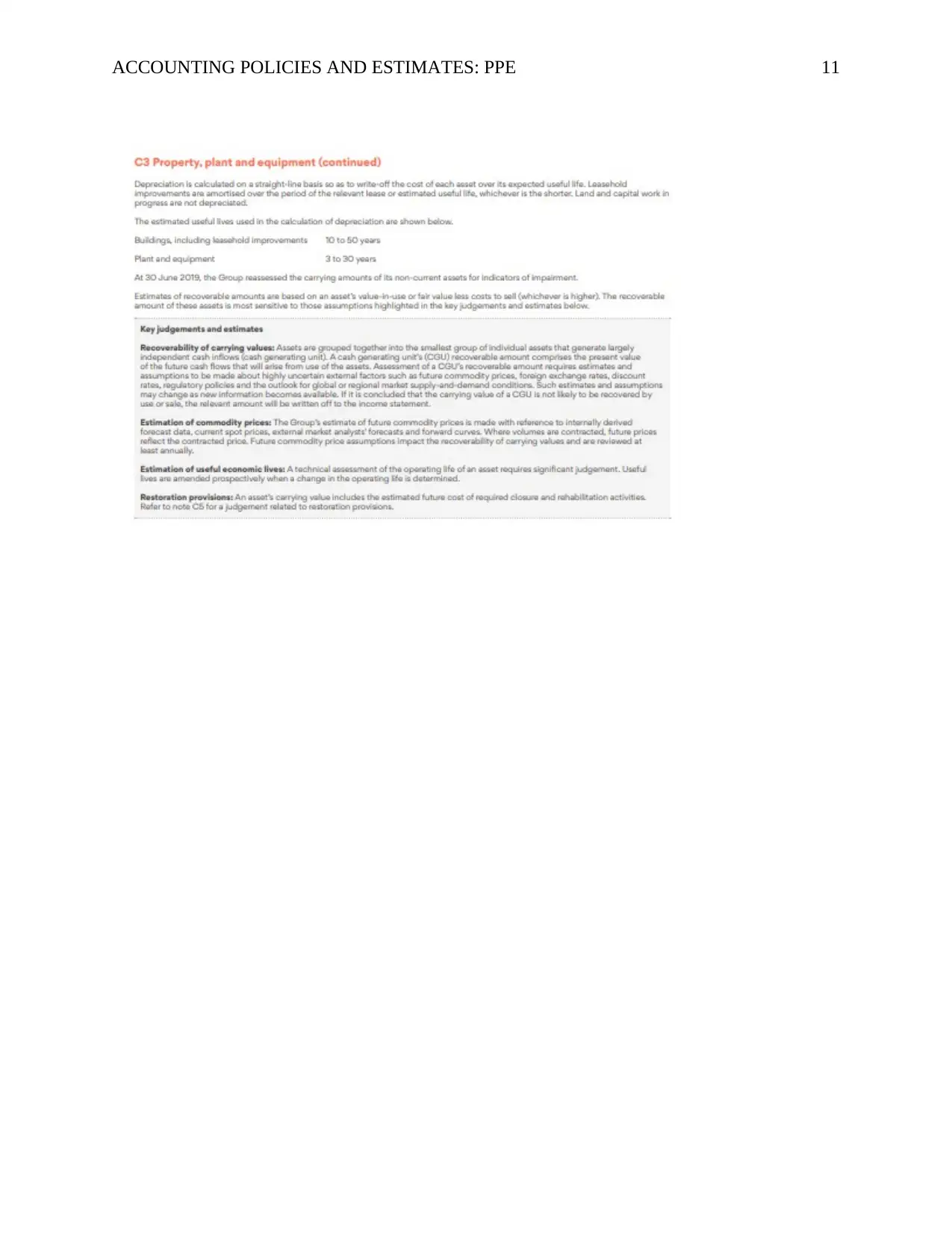

This report provides a comprehensive analysis of Origin Energy's accounting policies and estimates related to Plant, Property, and Equipment (PPE). It examines the company's application of accounting standards, including AASB 108, and its choices regarding depreciation methods, impairment assessments, and the estimation of asset useful lives. The report highlights the importance of professional judgment in selecting and applying these policies, emphasizing the need for reasonable and logical decision-making. It also evaluates the appropriateness of the professional judgments made by Origin Energy, comparing them to industry practices and competitor approaches. Furthermore, the report offers recommendations for improving the company's accounting policies, particularly regarding the use of technical analysis in calculating recoverable amounts and future cash flows for impairment analysis. The report concludes that Origin Energy has generally followed accounting standards, but suggests enhancements to ensure accurate PPE valuation.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.