Financial Reporting Analysis: Marks & Spencer and IFRS Compliance

VerifiedAdded on 2020/12/29

|21

|4358

|366

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with its context and purpose, emphasizing its role in providing stakeholders with insights into a business's financial performance and position. It delves into the conceptual and regulatory frameworks, including key principles such as understandability, relevance, reliability, and comparability. The report identifies both internal and external stakeholders, detailing how they benefit from financial information. It then examines the value of financial reporting in meeting organizational objectives, such as maximizing profits and attracting investors. The main financial statements as per IAS 1 are discussed, including the statement of profit and loss, statement of changes in equity, and the balance sheet, and the importance of the cash flow statement. A case study of Marks and Spencer's financial statements is included, along with a comparison between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS). The report concludes with a discussion of the benefits of IFRS and the varying degrees of compliance with IFRS across organizations globally.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY ..................................................................................................................................3

1. Context and purpose of financial reporting........................................................................3

2. Conceptual and regulatory framework and their key principles........................................4

3. The Main stakeholder of organisation and benefit of financial information to them ........5

4. The value of financial reporting for meeting organisational objectives ............................7

5. The main financial statements as per IAS 1.......................................................................7

6) The last two years’ financial statements of Marks and Spencer......................................11

7) Difference between International Accounting standards and International financial

reporting standards ..............................................................................................................13

8) Benefits of IFRS ..............................................................................................................14

9) The varying degree of Compliance with IFRS by organisation across the world .........15

CONCLUSION ............................................................................................................................15

REFERENCES .............................................................................................................................17

Appendix .............................................................................................................................18

INTRODUCTION ..........................................................................................................................3

MAIN BODY ..................................................................................................................................3

1. Context and purpose of financial reporting........................................................................3

2. Conceptual and regulatory framework and their key principles........................................4

3. The Main stakeholder of organisation and benefit of financial information to them ........5

4. The value of financial reporting for meeting organisational objectives ............................7

5. The main financial statements as per IAS 1.......................................................................7

6) The last two years’ financial statements of Marks and Spencer......................................11

7) Difference between International Accounting standards and International financial

reporting standards ..............................................................................................................13

8) Benefits of IFRS ..............................................................................................................14

9) The varying degree of Compliance with IFRS by organisation across the world .........15

CONCLUSION ............................................................................................................................15

REFERENCES .............................................................................................................................17

Appendix .............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting is the method of presenting accounting information in the reporting

form which assist in providing brief understanding about business profitability and position to

various stakeholders of firm. This study will provide understanding of context and purpose of

financial reporting. This study will include Marks and Spencer for determining the financial

performance of firm. This company is involved in retail industry and providing products such as

clothing for men, women and kids, home appliances etc. Moreover, it will consist information

regarding the conceptual and regulatory framework of financial reporting. Furthermore, this

assignment will provide main stakeholder of an organisation. Also, it will provide with

differentiation between IFRS and IAS. In addition to this, it will include the financial statement

as per IAS 1 for Godwin Plc which will consist of profit and loss statement, statement of changes

in equity and balance sheet. This study will explain the information provided by cash flow

statement.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is a method of presenting information in the statement which provide

understanding to stakeholder about performance and profitability of business. The main purpose

of financial reporting is to provide accurate information to stakeholders (Leuz and Wysocki,

2016). Financial reports are the source of information through which investors, creditors, lenders

etc. are provided with information about organisation position and performance. Moreover, it

provides information about credit worth of firm and their ability to pay its obligation.

Financial reporting includes profit and loss statement, balance sheet, cash flow statement

etc. Profit and loss statement contains information regarding income and expenses which assist

in identifying profit earned by organisation in the particular period (Purpose of Financial

Statements, 2017). The purpose of this statement is to provide information to stakeholders about

the ability of enterprise to generate profits. Balance sheet is the statement that contains assets and

liabilities which is prepared to provide understanding to its users about the current status of the

business. Moreover, cash flow statement includes information of cash inflow and outflow for a

period.

Financial reporting is the method of presenting accounting information in the reporting

form which assist in providing brief understanding about business profitability and position to

various stakeholders of firm. This study will provide understanding of context and purpose of

financial reporting. This study will include Marks and Spencer for determining the financial

performance of firm. This company is involved in retail industry and providing products such as

clothing for men, women and kids, home appliances etc. Moreover, it will consist information

regarding the conceptual and regulatory framework of financial reporting. Furthermore, this

assignment will provide main stakeholder of an organisation. Also, it will provide with

differentiation between IFRS and IAS. In addition to this, it will include the financial statement

as per IAS 1 for Godwin Plc which will consist of profit and loss statement, statement of changes

in equity and balance sheet. This study will explain the information provided by cash flow

statement.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is a method of presenting information in the statement which provide

understanding to stakeholder about performance and profitability of business. The main purpose

of financial reporting is to provide accurate information to stakeholders (Leuz and Wysocki,

2016). Financial reports are the source of information through which investors, creditors, lenders

etc. are provided with information about organisation position and performance. Moreover, it

provides information about credit worth of firm and their ability to pay its obligation.

Financial reporting includes profit and loss statement, balance sheet, cash flow statement

etc. Profit and loss statement contains information regarding income and expenses which assist

in identifying profit earned by organisation in the particular period (Purpose of Financial

Statements, 2017). The purpose of this statement is to provide information to stakeholders about

the ability of enterprise to generate profits. Balance sheet is the statement that contains assets and

liabilities which is prepared to provide understanding to its users about the current status of the

business. Moreover, cash flow statement includes information of cash inflow and outflow for a

period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It assists in identifying the cash requirement of business to conduct various business

operations. Moreover, the financial statements are used by management for taking various

decisions. This decision consists of credit decision, Investment decision etc. Management for

making effective decision in order to improve future performance and profitability of

organisation uses the financial statements (Acharya and Ryan, 2016). Financial reporting assist

investors in identifying the ability of organisation to generate returns for increasing their

shareholder’s wealth. This statement contains the accurate and reliable information for providing

true and fair information to its users. The main purpose of financial reporting is to provide

reliable information to stakeholders which assist them in making decision for allocating

resources. So, it is identified that financial reporting is used by various people which are having

interest in company's operations for making various decisions.

2. Conceptual and regulatory framework and their key principles

Conceptual framework of financial reporting consists of objective of preparing and

presenting the financial information in the financial reporting. Moreover, the conceptual

framework includes the qualitative characteristics of useful financial information. Also, it

provides understanding of reporting entity and its boundary (Weetman, 2018). The conceptual

framework of financial statement defines and assets, liabilities, incomes and expenses, equity. It

contains criteria for recording the assets and vice versa. This framework gives information about

concepts and guidance for presenting the information in report form. The regulatory framework

provides set of rules and regulation for presenting information in financial reporting. The

purpose of conceptual framework is to provide understanding about various concepts of financial

repiorting.

The regulatory body that govern the financial reporting is International accounting

standard board which has provided International accounting standards to record the transaction

in financial statements. The IFRS (international financial reporting board) is the one that makes

standards for preparing and presenting the financial reporting. The key principles for financial

reporting includes full disclosure of accounting information for providing reliable and accurate

information which is easily understandable to readers (Abbott and et.al., 2016). The conceptual

framework of financial reporting includes principles for reporting the transaction relating to

assets, liabilities, incomes and expenses. It consists of measurement principles, historical cost

operations. Moreover, the financial statements are used by management for taking various

decisions. This decision consists of credit decision, Investment decision etc. Management for

making effective decision in order to improve future performance and profitability of

organisation uses the financial statements (Acharya and Ryan, 2016). Financial reporting assist

investors in identifying the ability of organisation to generate returns for increasing their

shareholder’s wealth. This statement contains the accurate and reliable information for providing

true and fair information to its users. The main purpose of financial reporting is to provide

reliable information to stakeholders which assist them in making decision for allocating

resources. So, it is identified that financial reporting is used by various people which are having

interest in company's operations for making various decisions.

2. Conceptual and regulatory framework and their key principles

Conceptual framework of financial reporting consists of objective of preparing and

presenting the financial information in the financial reporting. Moreover, the conceptual

framework includes the qualitative characteristics of useful financial information. Also, it

provides understanding of reporting entity and its boundary (Weetman, 2018). The conceptual

framework of financial statement defines and assets, liabilities, incomes and expenses, equity. It

contains criteria for recording the assets and vice versa. This framework gives information about

concepts and guidance for presenting the information in report form. The regulatory framework

provides set of rules and regulation for presenting information in financial reporting. The

purpose of conceptual framework is to provide understanding about various concepts of financial

repiorting.

The regulatory body that govern the financial reporting is International accounting

standard board which has provided International accounting standards to record the transaction

in financial statements. The IFRS (international financial reporting board) is the one that makes

standards for preparing and presenting the financial reporting. The key principles for financial

reporting includes full disclosure of accounting information for providing reliable and accurate

information which is easily understandable to readers (Abbott and et.al., 2016). The conceptual

framework of financial reporting includes principles for reporting the transaction relating to

assets, liabilities, incomes and expenses. It consists of measurement principles, historical cost

principle, fair value principle, full disclosure principle etc. The purpose of regulatory framework

is to ensure that proper standards are followed in reporting the financial information.

The qualitative characteristics of financial reporting consist of following:

Understandability: The financial information presented in the statement must be

clearly understandable to users of financial reporting. The information contained in

the statement must be simple and must provide supporting information in footnotes to

give the readers clear understanding about the profitability and position of the

organisation.

Relevance: It means that the information included in the financial reporting must be

useful for the users in order to make the economic decisions (Call and et.al., 2017).

The financial statement must present relevant information which will helps the

stakeholders in making effective decisions about the organisation.

Reliability: The information presented in the financial information must be reliable

that is they must be free from material errors. Moreover, the information must be

faithfully presented to provide clear understanding about the business operation and

the information must not be misappropriated as it will not provide accurate

information to investors for making decisions.

Comparability: The information about the transaction presented in financial

reporting must be comparable which will help in identifying the trend of profitability

and position of the business. The financial statement must be comparable with the

past record.

3. The Main stakeholder of organisation and benefit of financial information to them

The stakeholders of organisation are divided into internal and external. Internal

stakeholders consist of Owners, managers and employees. Whereas external stakeholder consists

of lenders, investors, suppliers, tax authorities, customers etc.

Internal stakeholders: They are the primary users of financial information and are

present in the organisation. The following are internal users of financial information.

Owners: They use the financial information in order to identify the business

performance and the risk associated with it. Financial reporting assist in providing the

owners with accurate information about the overall business which provide

understanding to them while formulating various business policies.

is to ensure that proper standards are followed in reporting the financial information.

The qualitative characteristics of financial reporting consist of following:

Understandability: The financial information presented in the statement must be

clearly understandable to users of financial reporting. The information contained in

the statement must be simple and must provide supporting information in footnotes to

give the readers clear understanding about the profitability and position of the

organisation.

Relevance: It means that the information included in the financial reporting must be

useful for the users in order to make the economic decisions (Call and et.al., 2017).

The financial statement must present relevant information which will helps the

stakeholders in making effective decisions about the organisation.

Reliability: The information presented in the financial information must be reliable

that is they must be free from material errors. Moreover, the information must be

faithfully presented to provide clear understanding about the business operation and

the information must not be misappropriated as it will not provide accurate

information to investors for making decisions.

Comparability: The information about the transaction presented in financial

reporting must be comparable which will help in identifying the trend of profitability

and position of the business. The financial statement must be comparable with the

past record.

3. The Main stakeholder of organisation and benefit of financial information to them

The stakeholders of organisation are divided into internal and external. Internal

stakeholders consist of Owners, managers and employees. Whereas external stakeholder consists

of lenders, investors, suppliers, tax authorities, customers etc.

Internal stakeholders: They are the primary users of financial information and are

present in the organisation. The following are internal users of financial information.

Owners: They use the financial information in order to identify the business

performance and the risk associated with it. Financial reporting assist in providing the

owners with accurate information about the overall business which provide

understanding to them while formulating various business policies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managers: It uses accounting information to plan, monitor and make business

decisions. Financial reporting assist in providing information to managers about the

performance of organisation which helps them in making decisions and strategies for

improving the future performance of firm (11 Users of Accounting Information,

2017).

Employees: They use the financial information in order to determine the performance

of firm for their job security. Employees are internal stakeholders of organisation as

they use the financial information to identify the profit earned by their company to

measure their performance and future concerns about their jobs.

External stakeholders: They are the secondary users of financial information which are

present outside the organisation. It consists of following:

Investors: They are provided with financial statement to give them understanding

about their returns on invested capital. It helps them in assessing the profitability and

risk associated with the investment. For example, Investors are provided with

understanding of their return through help of ratio analysis.

Suppliers: They use the financial information in order to identify the

creditworthiness of company in order to identify the ability of company to pay back

its obligation.

Customers: They use the financial information in order to determine the resource

which they need are available with the business or not (Naranjo, Saavedra and Verdi,

2018). It assists in making decision for future supply of goods by the same supplier

Lenders: It includes banks and financial institutions which are interested in

determining the company's ability to pay its debt on maturity. They use financial

information to determine the liquidity position of organisation.

Tax authorities: They are the users of financial information for determining the tax

liability of the company. They are using the financial information to identify if the

correct amount of tax is included in the financial statement or not. Fore example,

They use balance sheet to identify the liabilities of the company.

4. The value of financial reporting for meeting organisational objectives

decisions. Financial reporting assist in providing information to managers about the

performance of organisation which helps them in making decisions and strategies for

improving the future performance of firm (11 Users of Accounting Information,

2017).

Employees: They use the financial information in order to determine the performance

of firm for their job security. Employees are internal stakeholders of organisation as

they use the financial information to identify the profit earned by their company to

measure their performance and future concerns about their jobs.

External stakeholders: They are the secondary users of financial information which are

present outside the organisation. It consists of following:

Investors: They are provided with financial statement to give them understanding

about their returns on invested capital. It helps them in assessing the profitability and

risk associated with the investment. For example, Investors are provided with

understanding of their return through help of ratio analysis.

Suppliers: They use the financial information in order to identify the

creditworthiness of company in order to identify the ability of company to pay back

its obligation.

Customers: They use the financial information in order to determine the resource

which they need are available with the business or not (Naranjo, Saavedra and Verdi,

2018). It assists in making decision for future supply of goods by the same supplier

Lenders: It includes banks and financial institutions which are interested in

determining the company's ability to pay its debt on maturity. They use financial

information to determine the liquidity position of organisation.

Tax authorities: They are the users of financial information for determining the tax

liability of the company. They are using the financial information to identify if the

correct amount of tax is included in the financial statement or not. Fore example,

They use balance sheet to identify the liabilities of the company.

4. The value of financial reporting for meeting organisational objectives

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The goals of the organisation consist of maximising profit , providing their investors

with higher returns , retaining customers for long term etc. Financial statement create value for

the organisation by providing them accurate information regarding the incomes and expenses,

assets and liability of organisation. It assists in providing the information regarding business

operation and performance of firm in industry. Moreover, financial information presented in

financial reporting assist in identifying the risk associated with business operation and

profitability (Reid and et.al., 2018). It provides the investors with better understanding of their

investment and their use in business operation which helps in increasing investor's attention

towards organisation. Management by using the financial reporting is able to make future

planning for increasing performance and profitability of firm.

This statement assists in preparing budget which helps in determining the future

profitability of business. With the help of this statement organisation is able to make effective

decision regarding objectives and growth of firm. By using the financial information enterprise

is able to determine its future incomes and expenses which will helps in reducing the future

expenses by making effective strategies. Financial statement creates value for the firm by

providing them information about their business operations which will helps in attracting more

investors towards the organisation. Moreover, this statement is important for determining the

profit earned by enterprise and the requirement of future improvement for achieving objectives.

Furthermore, it assists in providing the information to stakeholders regarding liquidity

position of company. This statement is valuable for organisation as it give information to

enterprise about various risk which will hamper business operations (Davidson, Dey and Smith,

2015). It is important to prepare financial reporting as they assist in providing the information

regarding the operations conducted by firm which helps in planning for future to increase the

profitability of firm in order to achieve organisation objective effectively and efficiently.

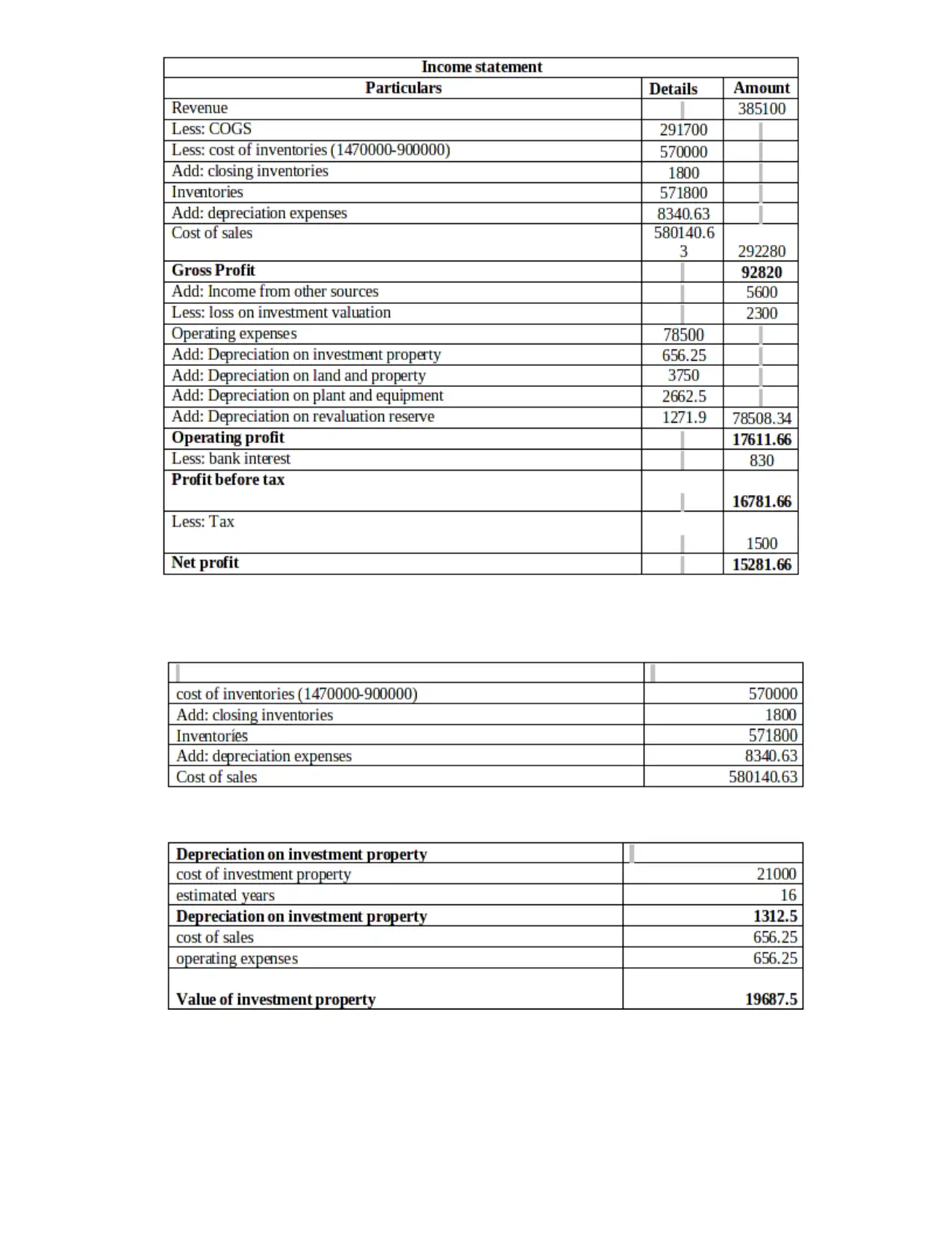

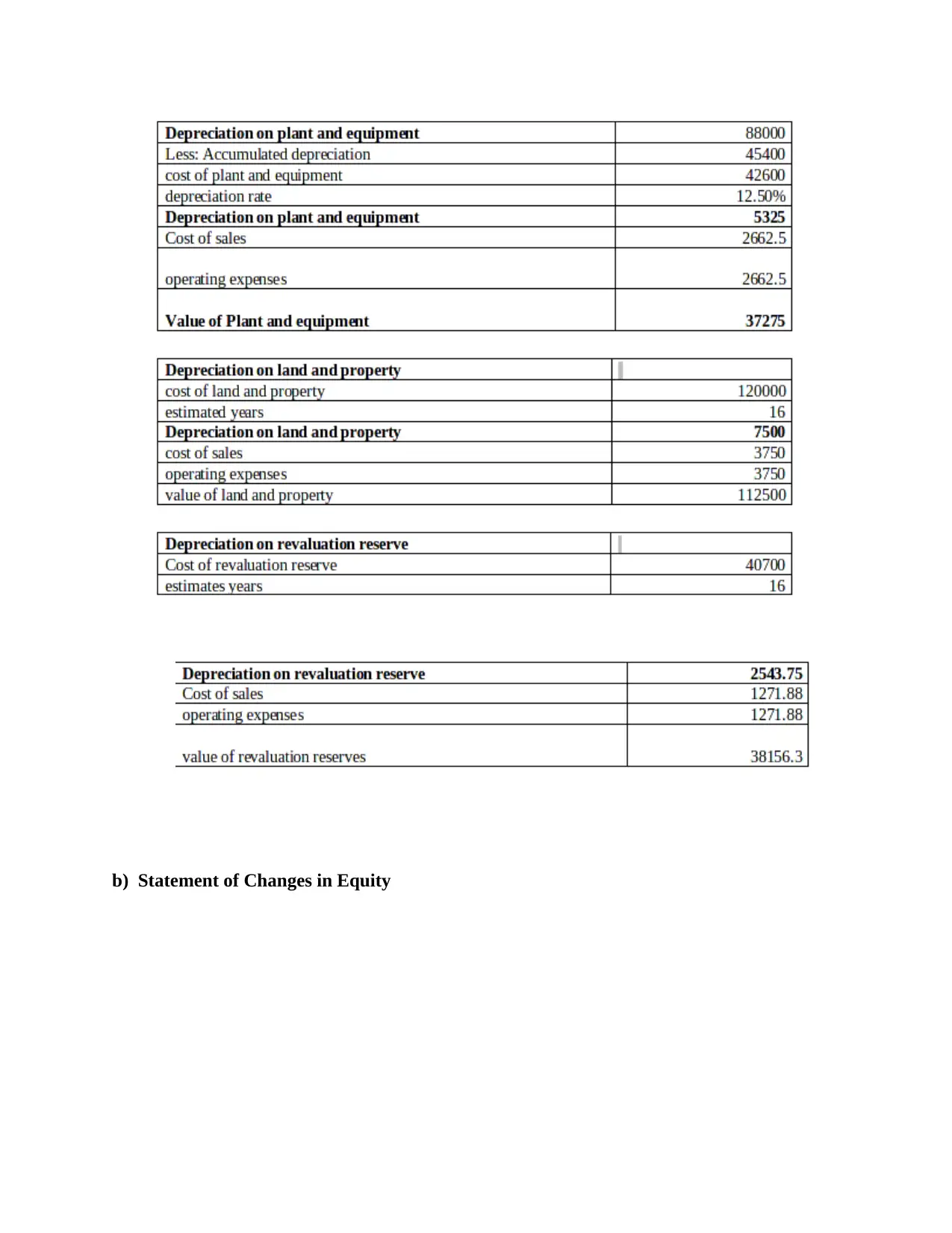

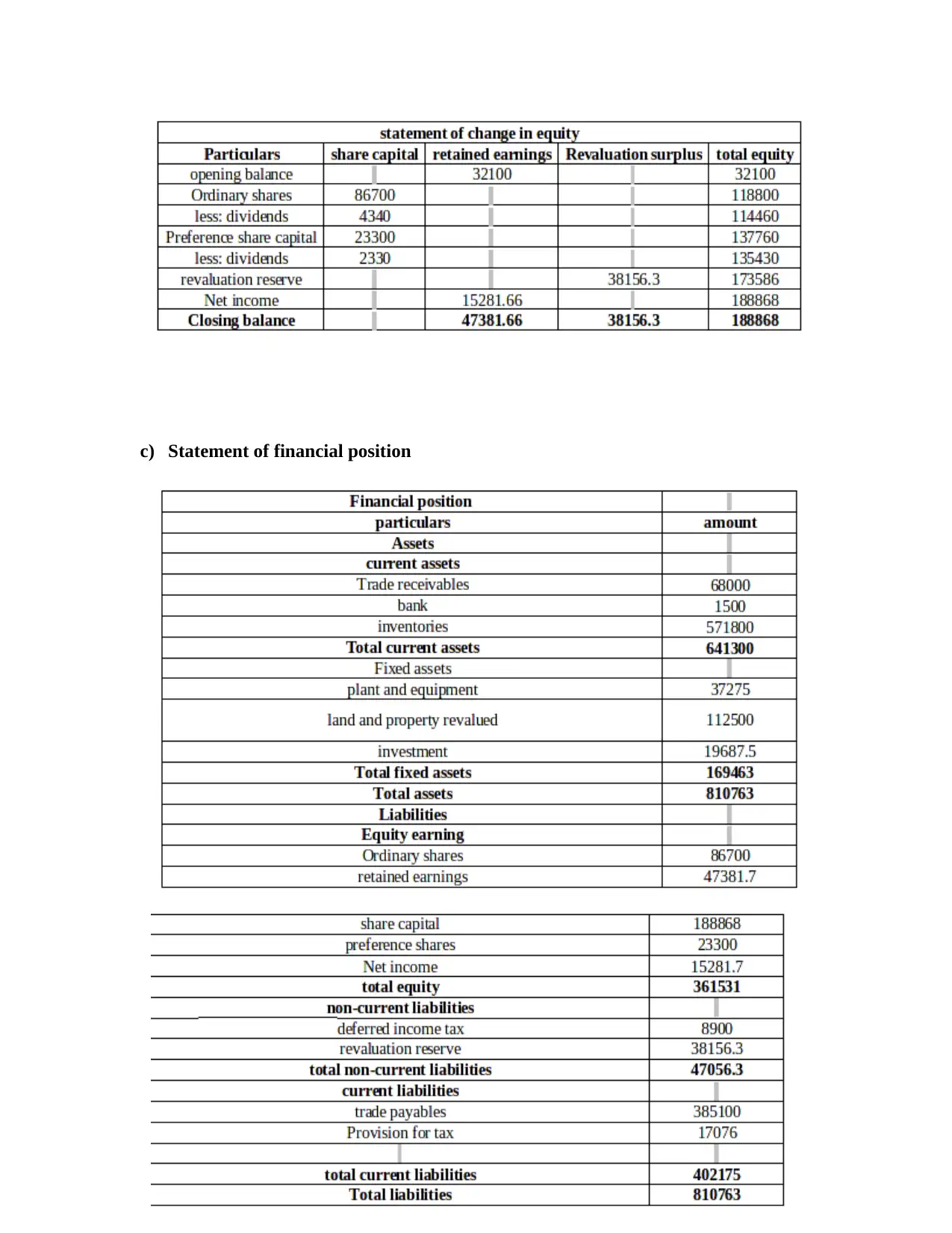

5. The main financial statements as per IAS 1

a) Statement of profit and loss and other comprehensive income

with higher returns , retaining customers for long term etc. Financial statement create value for

the organisation by providing them accurate information regarding the incomes and expenses,

assets and liability of organisation. It assists in providing the information regarding business

operation and performance of firm in industry. Moreover, financial information presented in

financial reporting assist in identifying the risk associated with business operation and

profitability (Reid and et.al., 2018). It provides the investors with better understanding of their

investment and their use in business operation which helps in increasing investor's attention

towards organisation. Management by using the financial reporting is able to make future

planning for increasing performance and profitability of firm.

This statement assists in preparing budget which helps in determining the future

profitability of business. With the help of this statement organisation is able to make effective

decision regarding objectives and growth of firm. By using the financial information enterprise

is able to determine its future incomes and expenses which will helps in reducing the future

expenses by making effective strategies. Financial statement creates value for the firm by

providing them information about their business operations which will helps in attracting more

investors towards the organisation. Moreover, this statement is important for determining the

profit earned by enterprise and the requirement of future improvement for achieving objectives.

Furthermore, it assists in providing the information to stakeholders regarding liquidity

position of company. This statement is valuable for organisation as it give information to

enterprise about various risk which will hamper business operations (Davidson, Dey and Smith,

2015). It is important to prepare financial reporting as they assist in providing the information

regarding the operations conducted by firm which helps in planning for future to increase the

profitability of firm in order to achieve organisation objective effectively and efficiently.

5. The main financial statements as per IAS 1

a) Statement of profit and loss and other comprehensive income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Statement of Changes in Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c) Statement of financial position

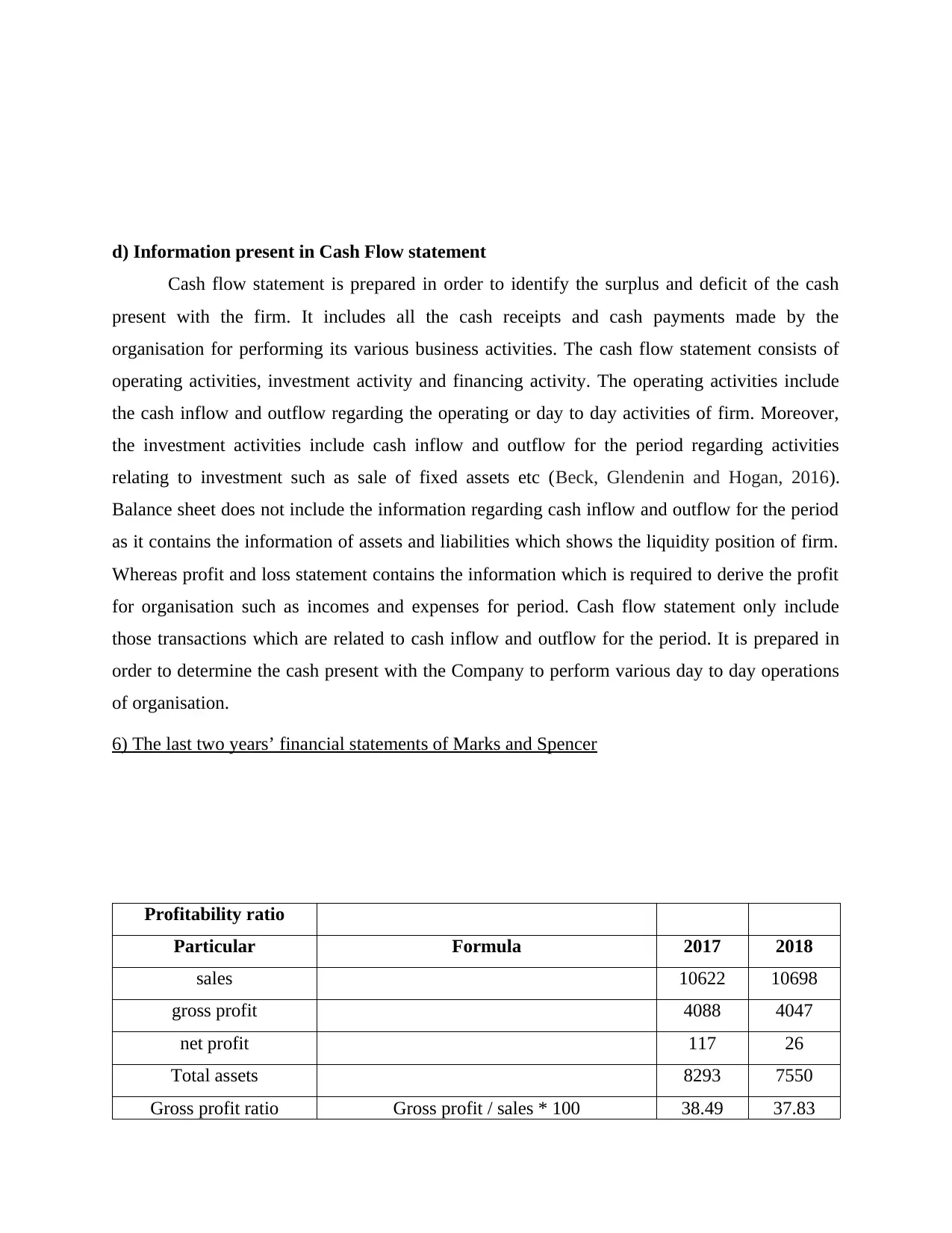

d) Information present in Cash Flow statement

Cash flow statement is prepared in order to identify the surplus and deficit of the cash

present with the firm. It includes all the cash receipts and cash payments made by the

organisation for performing its various business activities. The cash flow statement consists of

operating activities, investment activity and financing activity. The operating activities include

the cash inflow and outflow regarding the operating or day to day activities of firm. Moreover,

the investment activities include cash inflow and outflow for the period regarding activities

relating to investment such as sale of fixed assets etc (Beck, Glendenin and Hogan, 2016).

Balance sheet does not include the information regarding cash inflow and outflow for the period

as it contains the information of assets and liabilities which shows the liquidity position of firm.

Whereas profit and loss statement contains the information which is required to derive the profit

for organisation such as incomes and expenses for period. Cash flow statement only include

those transactions which are related to cash inflow and outflow for the period. It is prepared in

order to determine the cash present with the Company to perform various day to day operations

of organisation.

6) The last two years’ financial statements of Marks and Spencer

Profitability ratio

Particular Formula 2017 2018

sales 10622 10698

gross profit 4088 4047

net profit 117 26

Total assets 8293 7550

Gross profit ratio Gross profit / sales * 100 38.49 37.83

Cash flow statement is prepared in order to identify the surplus and deficit of the cash

present with the firm. It includes all the cash receipts and cash payments made by the

organisation for performing its various business activities. The cash flow statement consists of

operating activities, investment activity and financing activity. The operating activities include

the cash inflow and outflow regarding the operating or day to day activities of firm. Moreover,

the investment activities include cash inflow and outflow for the period regarding activities

relating to investment such as sale of fixed assets etc (Beck, Glendenin and Hogan, 2016).

Balance sheet does not include the information regarding cash inflow and outflow for the period

as it contains the information of assets and liabilities which shows the liquidity position of firm.

Whereas profit and loss statement contains the information which is required to derive the profit

for organisation such as incomes and expenses for period. Cash flow statement only include

those transactions which are related to cash inflow and outflow for the period. It is prepared in

order to determine the cash present with the Company to perform various day to day operations

of organisation.

6) The last two years’ financial statements of Marks and Spencer

Profitability ratio

Particular Formula 2017 2018

sales 10622 10698

gross profit 4088 4047

net profit 117 26

Total assets 8293 7550

Gross profit ratio Gross profit / sales * 100 38.49 37.83

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.