Accounting Principles: Financial Data, Analysis, and Reporting 2022-23

VerifiedAdded on 2023/06/16

|26

|5260

|111

Report

AI Summary

This report provides a comprehensive overview of accounting principles, covering both management and financial accounting. It details the role of accounting in gathering, processing, and presenting financial data for internal and external users. Management accounting is explained as a tool for decision-making, planning, and analyzing financial data, while financial accounting focuses on creating financial statements like income statements, balance sheets, and cash flow statements. The report also discusses budgeting, accounts receivable, and accounts payable, highlighting their purpose in financial management. Furthermore, the skills and competencies required for accounting roles are explored, using JPMorgan Chase & Co. as an example. The report includes practical examples with trading, profit and loss accounting, and balance sheets for sole proprietorships, partnerships, and not-for-profit organizations, illustrating the application of accounting principles in various business contexts. Desklib provides this document and many more to aid students in their studies.

Student Name/ID Number

Unit Number and Title 05: Accounting Principles

Academic Year 2022-23

Unit Tutor

Assignment Title Understanding aspects of Accounting Principles

Issue Date

Submission Date

Unit Number and Title 05: Accounting Principles

Academic Year 2022-23

Unit Tutor

Assignment Title Understanding aspects of Accounting Principles

Issue Date

Submission Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO1

ACCOUNTING

Accounting is the orderly gathering, processing, interpreting, and presenting of

financial data. One person in a small business or various teams in a large corporation can

handle bookkeeping. A firm keeps track of its operations through accounting.

Business accounting's objectives include giving you a thorough view of the dynamics

of the organization's operations and information on the state of its assets. Due to their

potential for use in making future projections, these data are required for more than just

factual reporting and tax preparation.

Calculating the reserves of the company's various property assets to preserve its sound

financial state;

Presentation of objective, systematic, and in-person economic data to management on

a regular and up-to-date basis;

Reduction of dangers that can have a bad impact on business operations;

Putting the controlling function into practice (both on the part of the state and on the

part of other external counterparties).

Accounting for internal users is done to provide management with a complete picture

that will aid them in making the best decisions possible. Additionally, the organization's

administration is really interested in sharing information with outside users for monitoring,

analysis, and effective planning. In other words, information for internal users on the

organization's financial performance, financial position, and changes to that position is used

to produce information for external users.

MANAGEMENT ACCOUNTING

The process of maintaining, extracting reporting, and analyzing an organization's

financial data for decision-making is known as management accounting. Based on the study

and interpretation of financial information pertaining to the internal operations of the

organization, management accounting aids managers in developing plans, changing course,

and making knowledgeable decisions. A virtual tool called management accounting assists an

organization's leaders in directing it toward accomplishing its objectives. Accounting for

management involves analyzing, interpreting, and providing management with information. It

aids non-accounting employees in comprehending and comprehending financial information

within an organization.

ACCOUNTING

Accounting is the orderly gathering, processing, interpreting, and presenting of

financial data. One person in a small business or various teams in a large corporation can

handle bookkeeping. A firm keeps track of its operations through accounting.

Business accounting's objectives include giving you a thorough view of the dynamics

of the organization's operations and information on the state of its assets. Due to their

potential for use in making future projections, these data are required for more than just

factual reporting and tax preparation.

Calculating the reserves of the company's various property assets to preserve its sound

financial state;

Presentation of objective, systematic, and in-person economic data to management on

a regular and up-to-date basis;

Reduction of dangers that can have a bad impact on business operations;

Putting the controlling function into practice (both on the part of the state and on the

part of other external counterparties).

Accounting for internal users is done to provide management with a complete picture

that will aid them in making the best decisions possible. Additionally, the organization's

administration is really interested in sharing information with outside users for monitoring,

analysis, and effective planning. In other words, information for internal users on the

organization's financial performance, financial position, and changes to that position is used

to produce information for external users.

MANAGEMENT ACCOUNTING

The process of maintaining, extracting reporting, and analyzing an organization's

financial data for decision-making is known as management accounting. Based on the study

and interpretation of financial information pertaining to the internal operations of the

organization, management accounting aids managers in developing plans, changing course,

and making knowledgeable decisions. A virtual tool called management accounting assists an

organization's leaders in directing it toward accomplishing its objectives. Accounting for

management involves analyzing, interpreting, and providing management with information. It

aids non-accounting employees in comprehending and comprehending financial information

within an organization.

Business decisions ought to be supported by data and facts. A lot of the day-to-day

transaction information for a business is too little and intricate to be understood at a glance.

In order to provide critical answers, management accounting derives reports and insights

from actual data. Therefore, managerial accounting facilitates decision-making based on

actual accounting facts. Examining historical patterns and the effects of prior choices is also

beneficial.

Management accounting allows you to:

Set and achieve your business goals, see what real results the company has achieved

Predict company profits, prevent cash gaps, plan payments

Find growth points for the company, detail profit and loss and find out where you can

save

Save time getting financial data in any context with automation

Get convenient and understandable business reporting in real time

MANAGEMENT ACCOUNTING SYSTEM:

Cost system. It is used by manufacturers to record production activities and track

inventory movements before it can be used to produce finished goods.

The main purpose of such systems is to use them within the company to make

decisions to reduce costs, compare actual costs with planned ones in order to control, create

strategic and tactical plans for the future, and work in such a way as to get higher profits. . .

An inventory management system is the process of tracking items from purchase to

final sale, and how you approach inventory management for your business.

The main purpose of this system is to ensure sufficient demand for goods or materials

without excess inventory and save money for the business.

Job system is a process of obtaining information about the costs associated with a

particular production or service, which includes an analysis of direct and indirect costs and is

further broken down into labor and overhead costs.

The main goal is to establish the profit and loss incurred on each job and find out

which jobs are more profitable and which are less, controls the actual costs with the estimated

costs to ensure that the costs are not excessive or incorrect.

transaction information for a business is too little and intricate to be understood at a glance.

In order to provide critical answers, management accounting derives reports and insights

from actual data. Therefore, managerial accounting facilitates decision-making based on

actual accounting facts. Examining historical patterns and the effects of prior choices is also

beneficial.

Management accounting allows you to:

Set and achieve your business goals, see what real results the company has achieved

Predict company profits, prevent cash gaps, plan payments

Find growth points for the company, detail profit and loss and find out where you can

save

Save time getting financial data in any context with automation

Get convenient and understandable business reporting in real time

MANAGEMENT ACCOUNTING SYSTEM:

Cost system. It is used by manufacturers to record production activities and track

inventory movements before it can be used to produce finished goods.

The main purpose of such systems is to use them within the company to make

decisions to reduce costs, compare actual costs with planned ones in order to control, create

strategic and tactical plans for the future, and work in such a way as to get higher profits. . .

An inventory management system is the process of tracking items from purchase to

final sale, and how you approach inventory management for your business.

The main purpose of this system is to ensure sufficient demand for goods or materials

without excess inventory and save money for the business.

Job system is a process of obtaining information about the costs associated with a

particular production or service, which includes an analysis of direct and indirect costs and is

further broken down into labor and overhead costs.

The main goal is to establish the profit and loss incurred on each job and find out

which jobs are more profitable and which are less, controls the actual costs with the estimated

costs to ensure that the costs are not excessive or incorrect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING:

Journal and its purpose. A journal is a diary in which the financial transactions

associated with the records are recorded to create the financial statements of the business. It

includes all kinds of registries.

The goal is to track transactions and maintain them on a regular basis in the general

ledger, which then feeds the information into financial statements on which business decision

makers depend.

Ledger and its purpose. A general ledger is a book or collection in which account

transactions are recorded as balance sheet and income statement entries that include assets,

liabilities, capital, income, and expenses.

The goal is to record all the transactions of the company and keep track of all

individual events, recording the credits and debits of the accounts and systematizing the data

so that you know the end of the balance sheet after the end of each accounting year.

Trial balance and its purpose. The trial balance is a list of all registers created for

debit and credit accounts so that the total amounts are equal, which ensures the mathematical

correctness of entries in the accounting system.

The purpose of the trial balance is to assist in compiling the balance sheet at the end of

the year, accurately accounting for all transactions at the end of the reporting year, and

identifying errors made when posting the relevant entries.

FINANCIAL STATEMENT AND ITS PURPORSE

Income statement and its purpose. An income statement, also known as a profit and

loss statement, is a financial statement that shows a company's income and expenses for a

period and how the income is converted into net income or net income.

The purpose of preparing an income statement is to show the financial results of a

company for a period.

Balance sheet and its purpose. This is a statement of the assets, liabilities and equity

of an enterprise that details the balance of income and expenses for a period and provides a

brief overview of the company's finances.

The purpose of a balance sheet is to provide business owners with the financial

position of their company and how much assets the business owns, how many liabilities it

owes, and how much capital is invested in the business.

Cash flow statements and their purpose. This is a financial statement that shows how

changes in balance sheets and earnings affect cash and breaks down the analysis into

Journal and its purpose. A journal is a diary in which the financial transactions

associated with the records are recorded to create the financial statements of the business. It

includes all kinds of registries.

The goal is to track transactions and maintain them on a regular basis in the general

ledger, which then feeds the information into financial statements on which business decision

makers depend.

Ledger and its purpose. A general ledger is a book or collection in which account

transactions are recorded as balance sheet and income statement entries that include assets,

liabilities, capital, income, and expenses.

The goal is to record all the transactions of the company and keep track of all

individual events, recording the credits and debits of the accounts and systematizing the data

so that you know the end of the balance sheet after the end of each accounting year.

Trial balance and its purpose. The trial balance is a list of all registers created for

debit and credit accounts so that the total amounts are equal, which ensures the mathematical

correctness of entries in the accounting system.

The purpose of the trial balance is to assist in compiling the balance sheet at the end of

the year, accurately accounting for all transactions at the end of the reporting year, and

identifying errors made when posting the relevant entries.

FINANCIAL STATEMENT AND ITS PURPORSE

Income statement and its purpose. An income statement, also known as a profit and

loss statement, is a financial statement that shows a company's income and expenses for a

period and how the income is converted into net income or net income.

The purpose of preparing an income statement is to show the financial results of a

company for a period.

Balance sheet and its purpose. This is a statement of the assets, liabilities and equity

of an enterprise that details the balance of income and expenses for a period and provides a

brief overview of the company's finances.

The purpose of a balance sheet is to provide business owners with the financial

position of their company and how much assets the business owns, how many liabilities it

owes, and how much capital is invested in the business.

Cash flow statements and their purpose. This is a financial statement that shows how

changes in balance sheets and earnings affect cash and breaks down the analysis into

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

operating, investing and financing activities. Particular attention is paid to the flow of cash in

and out of the business.

The main goal is to provide a detailed picture of what happened to the cash flow of

businesses during the reporting period and the ability of the organization to operate in the

short or long term depending on how much cash flows in or out of the business.

Budgeting and its purpose. Budgeting is the process of developing, implementing and

implementing budgets. Which determines the current available capital, provides cost

estimates, and forecasts revenue streams. With a budget in mind, businesses can measure

efficiency against costs and ensure that resources are available for initiatives that support

business and growth.

Accounts receivable and its purpose. These are the funds that customers owe your

company for invoiced products or services. The total value of all receivables is shown on the

balance sheet as working capital and includes invoices due from buyers for goods or work

performed for them on credit.

Accounts payable and its purpose. The accounts payable department is responsible

for keeping track of exactly what is owned by vendors, ensuring that payments are properly

approved, and processing payments. Accurate accounts payable information is essential for

an accurate balance sheet.

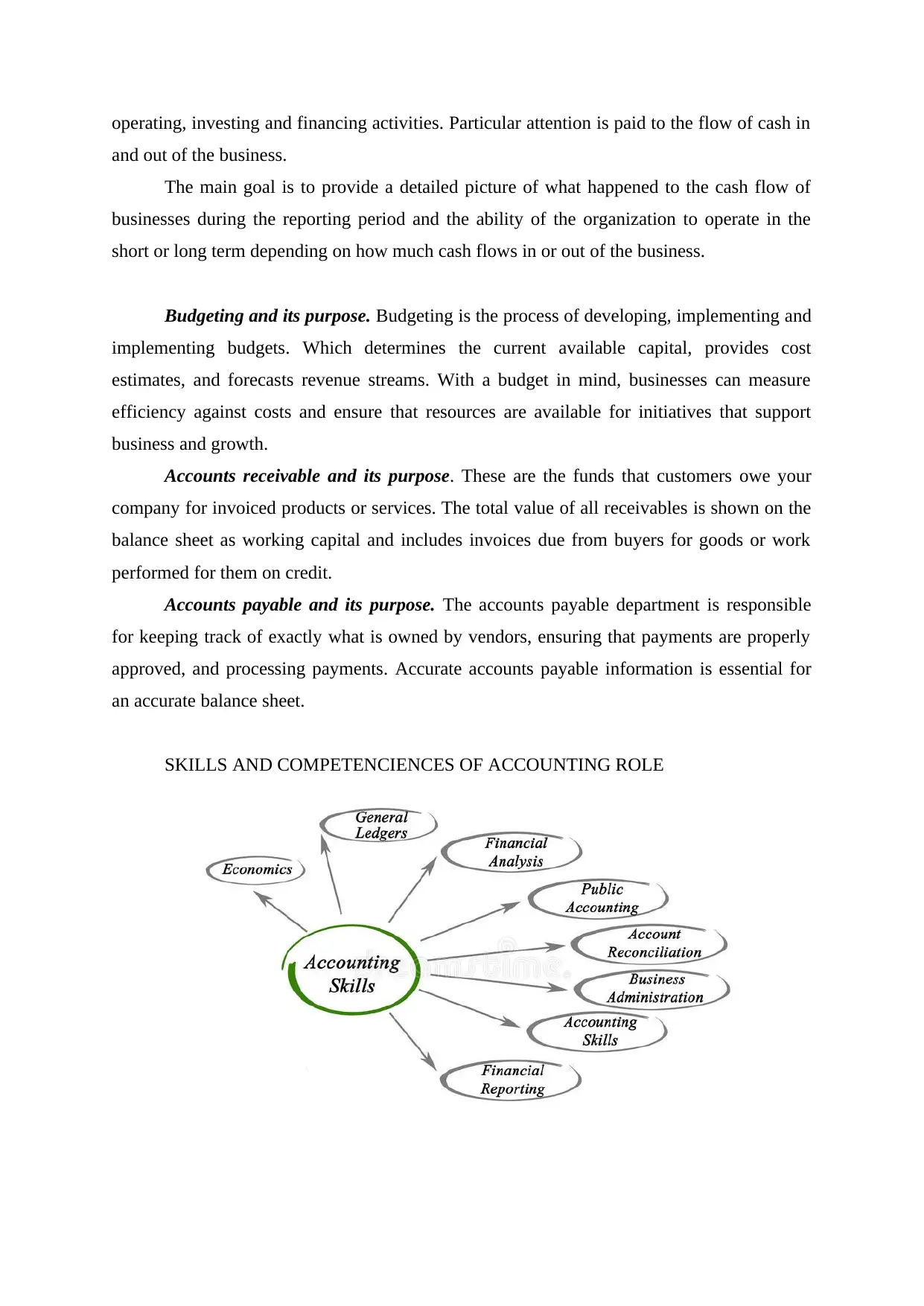

SKILLS AND COMPETENCIENCES OF ACCOUNTING ROLE

and out of the business.

The main goal is to provide a detailed picture of what happened to the cash flow of

businesses during the reporting period and the ability of the organization to operate in the

short or long term depending on how much cash flows in or out of the business.

Budgeting and its purpose. Budgeting is the process of developing, implementing and

implementing budgets. Which determines the current available capital, provides cost

estimates, and forecasts revenue streams. With a budget in mind, businesses can measure

efficiency against costs and ensure that resources are available for initiatives that support

business and growth.

Accounts receivable and its purpose. These are the funds that customers owe your

company for invoiced products or services. The total value of all receivables is shown on the

balance sheet as working capital and includes invoices due from buyers for goods or work

performed for them on credit.

Accounts payable and its purpose. The accounts payable department is responsible

for keeping track of exactly what is owned by vendors, ensuring that payments are properly

approved, and processing payments. Accurate accounts payable information is essential for

an accurate balance sheet.

SKILLS AND COMPETENCIENCES OF ACCOUNTING ROLE

JPMorgan Chase & Co. is the name of the holding company, and the firm serves its

customers and clients under the Chase and JPMorgan brands.

JPMorgan Chase (NYSE: JPM) is one of the oldest US financial institutions. With a history

spanning over 200 years, here is where they are today:

Their influence: We combine our business and policy expertise, sustainable business

practices, data, capital and global presence to advance solutions that drive inclusive economic

growth.

What they do: They are committed to working for the benefit of all communities.

Through continuous investment, business initiatives and philanthropic commitments, we are

committed to helping employees, customers, customers and communities grow and prosper

sustainably – with opportunities for all. Through investments and initiatives to support and

advance the Black, Hispanic, and Latino communities, we make economic opportunity more

equitable and affordable.

Their ideas: They invest in research and ideas that help inform and advance political

solutions that support the path to racial justice.

customers and clients under the Chase and JPMorgan brands.

JPMorgan Chase (NYSE: JPM) is one of the oldest US financial institutions. With a history

spanning over 200 years, here is where they are today:

Their influence: We combine our business and policy expertise, sustainable business

practices, data, capital and global presence to advance solutions that drive inclusive economic

growth.

What they do: They are committed to working for the benefit of all communities.

Through continuous investment, business initiatives and philanthropic commitments, we are

committed to helping employees, customers, customers and communities grow and prosper

sustainably – with opportunities for all. Through investments and initiatives to support and

advance the Black, Hispanic, and Latino communities, we make economic opportunity more

equitable and affordable.

Their ideas: They invest in research and ideas that help inform and advance political

solutions that support the path to racial justice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

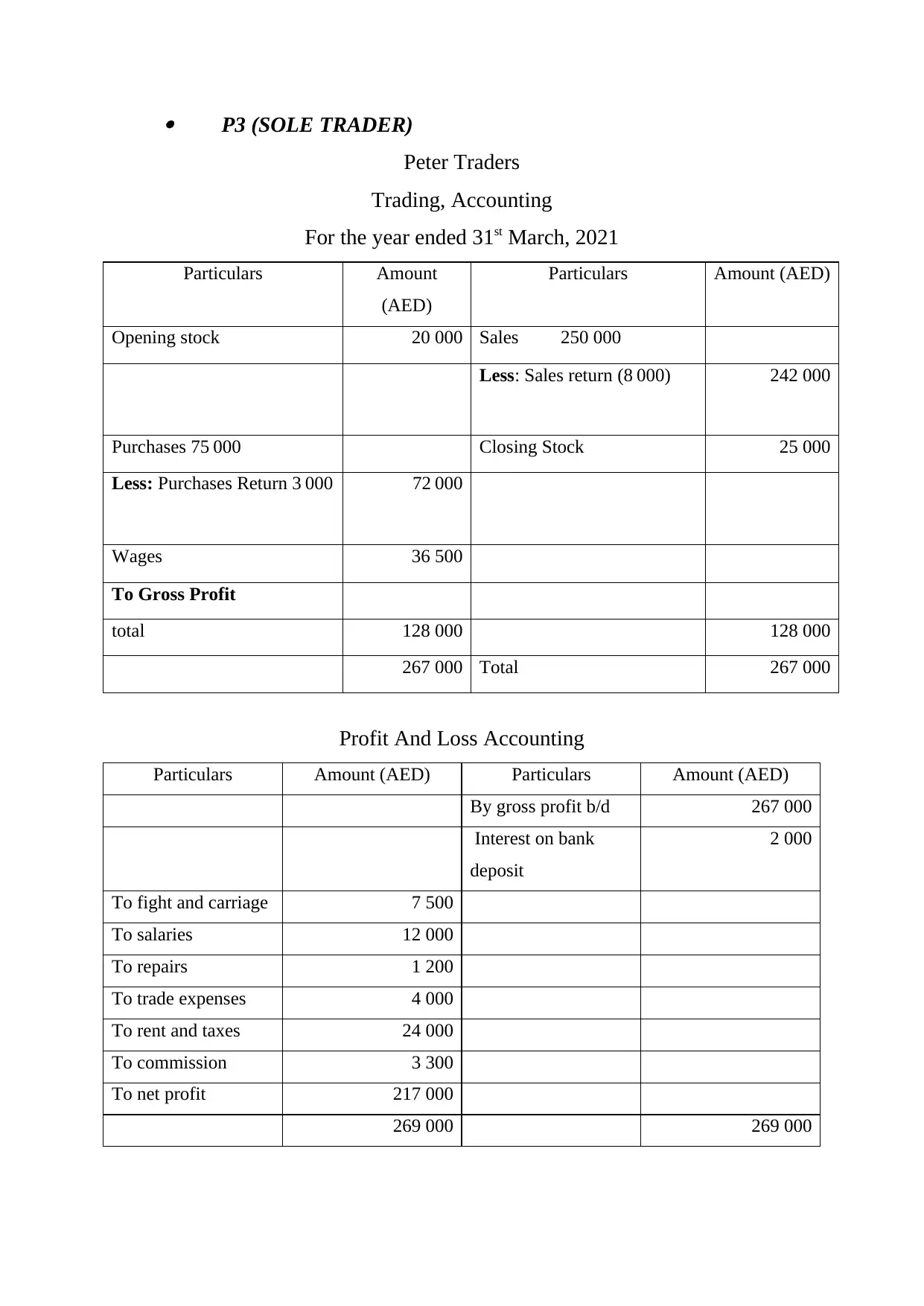

P3 (SOLE TRADER)

Peter Traders

Trading, Accounting

For the year ended 31st March, 2021

Particulars Amount

(AED)

Particulars Amount (AED)

Opening stock 20 000 Sales 250 000

Less: Sales return (8 000) 242 000

Purchases 75 000 Closing Stock 25 000

Less: Purchases Return 3 000 72 000

Wages 36 500

To Gross Profit

total 128 000 128 000

267 000 Total 267 000

Profit And Loss Accounting

Particulars Amount (AED) Particulars Amount (AED)

By gross profit b/d 267 000

Interest on bank

deposit

2 000

To fight and carriage 7 500

To salaries 12 000

To repairs 1 200

To trade expenses 4 000

To rent and taxes 24 000

To commission 3 300

To net profit 217 000

269 000 269 000

Peter Traders

Trading, Accounting

For the year ended 31st March, 2021

Particulars Amount

(AED)

Particulars Amount (AED)

Opening stock 20 000 Sales 250 000

Less: Sales return (8 000) 242 000

Purchases 75 000 Closing Stock 25 000

Less: Purchases Return 3 000 72 000

Wages 36 500

To Gross Profit

total 128 000 128 000

267 000 Total 267 000

Profit And Loss Accounting

Particulars Amount (AED) Particulars Amount (AED)

By gross profit b/d 267 000

Interest on bank

deposit

2 000

To fight and carriage 7 500

To salaries 12 000

To repairs 1 200

To trade expenses 4 000

To rent and taxes 24 000

To commission 3 300

To net profit 217 000

269 000 269 000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

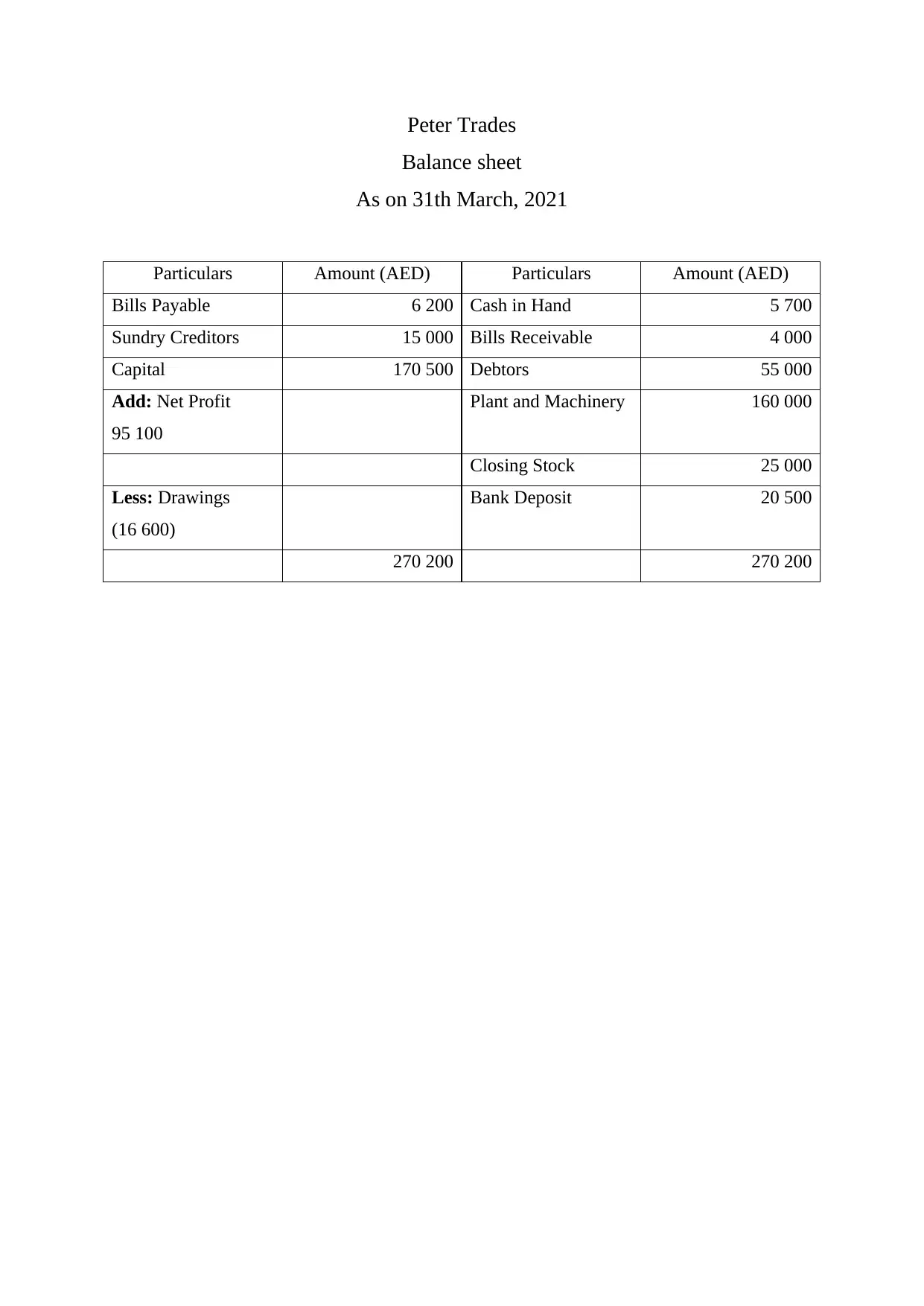

Peter Trades

Balance sheet

As on 31th March, 2021

Particulars Amount (AED) Particulars Amount (AED)

Bills Payable 6 200 Cash in Hand 5 700

Sundry Creditors 15 000 Bills Receivable 4 000

Capital 170 500 Debtors 55 000

Add: Net Profit

95 100

Plant and Machinery 160 000

Closing Stock 25 000

Less: Drawings

(16 600)

Bank Deposit 20 500

270 200 270 200

Balance sheet

As on 31th March, 2021

Particulars Amount (AED) Particulars Amount (AED)

Bills Payable 6 200 Cash in Hand 5 700

Sundry Creditors 15 000 Bills Receivable 4 000

Capital 170 500 Debtors 55 000

Add: Net Profit

95 100

Plant and Machinery 160 000

Closing Stock 25 000

Less: Drawings

(16 600)

Bank Deposit 20 500

270 200 270 200

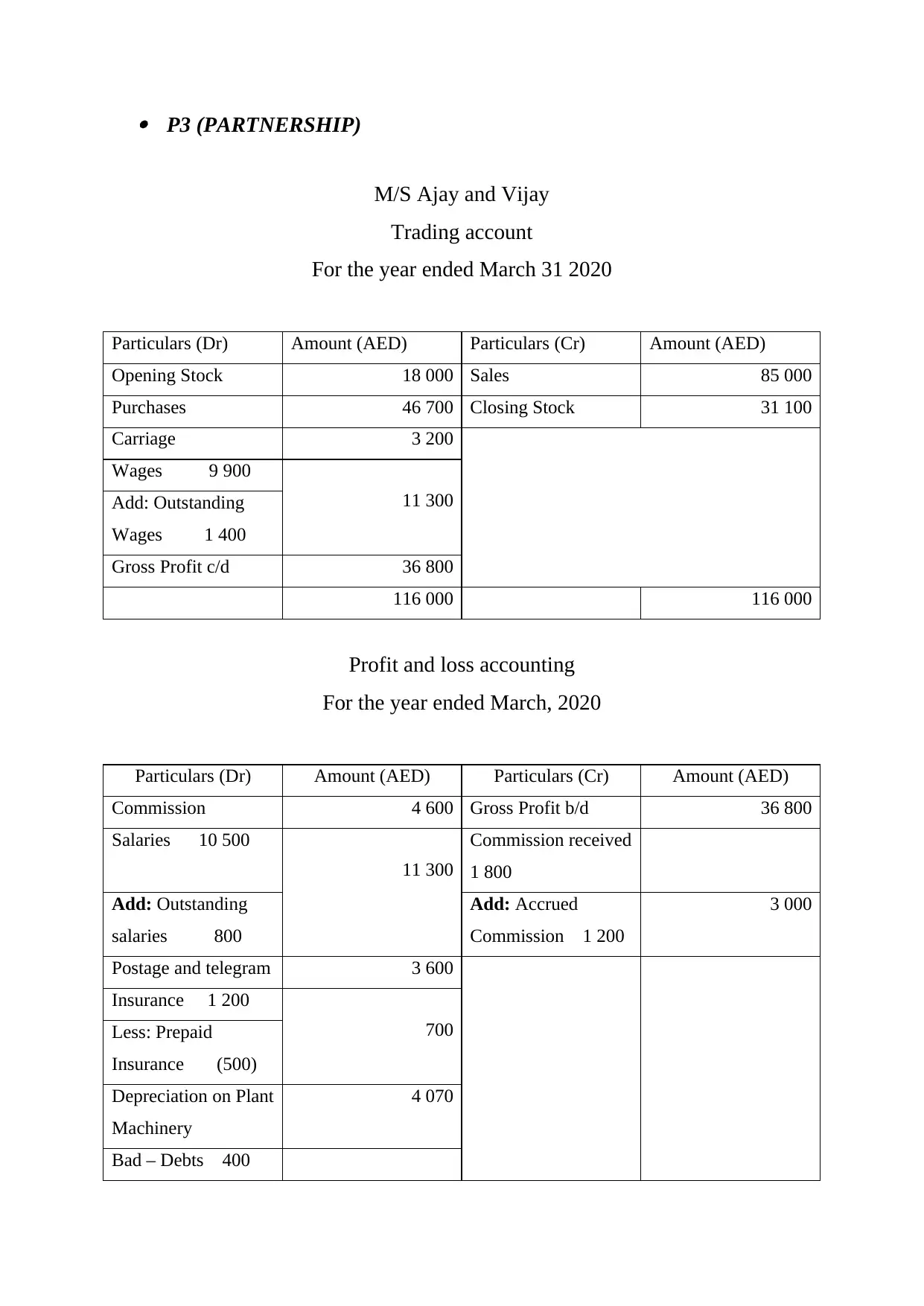

P3 (PARTNERSHIP)

M/S Ajay and Vijay

Trading account

For the year ended March 31 2020

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Opening Stock 18 000 Sales 85 000

Purchases 46 700 Closing Stock 31 100

Carriage 3 200

Wages 9 900

11 300Add: Outstanding

Wages 1 400

Gross Profit c/d 36 800

116 000 116 000

Profit and loss accounting

For the year ended March, 2020

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Commission 4 600 Gross Profit b/d 36 800

Salaries 10 500

11 300

Commission received

1 800

Add: Outstanding

salaries 800

Add: Accrued

Commission 1 200

3 000

Postage and telegram 3 600

Insurance 1 200

700Less: Prepaid

Insurance (500)

Depreciation on Plant

Machinery

4 070

Bad – Debts 400

M/S Ajay and Vijay

Trading account

For the year ended March 31 2020

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Opening Stock 18 000 Sales 85 000

Purchases 46 700 Closing Stock 31 100

Carriage 3 200

Wages 9 900

11 300Add: Outstanding

Wages 1 400

Gross Profit c/d 36 800

116 000 116 000

Profit and loss accounting

For the year ended March, 2020

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Commission 4 600 Gross Profit b/d 36 800

Salaries 10 500

11 300

Commission received

1 800

Add: Outstanding

salaries 800

Add: Accrued

Commission 1 200

3 000

Postage and telegram 3 600

Insurance 1 200

700Less: Prepaid

Insurance (500)

Depreciation on Plant

Machinery

4 070

Bad – Debts 400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

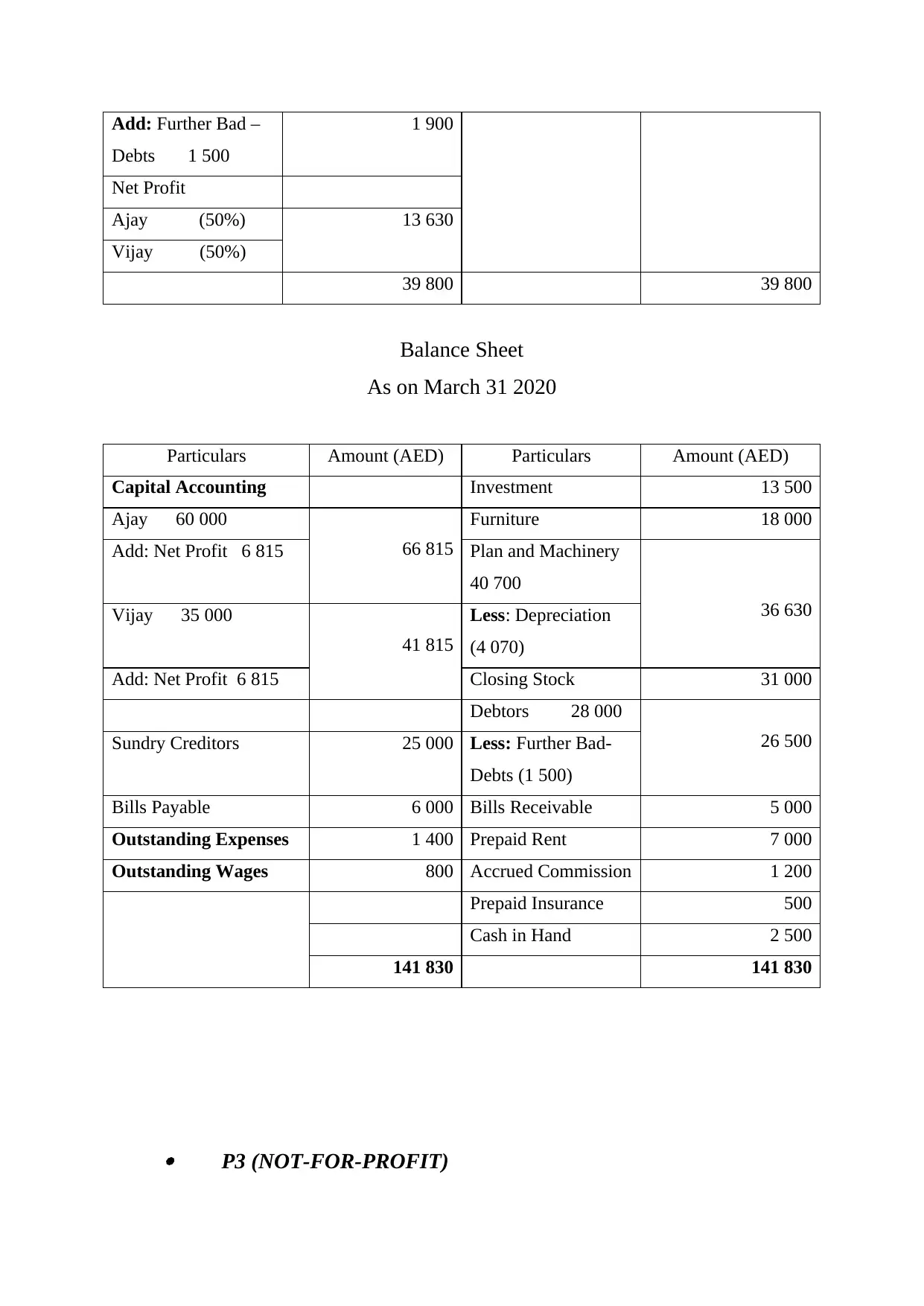

1 900Add: Further Bad –

Debts 1 500

Net Profit

Ajay (50%) 13 630

Vijay (50%)

39 800 39 800

Balance Sheet

As on March 31 2020

Particulars Amount (AED) Particulars Amount (AED)

Capital Accounting Investment 13 500

Ajay 60 000

66 815

Furniture 18 000

Add: Net Profit 6 815 Plan and Machinery

40 700

36 630Vijay 35 000

41 815

Less: Depreciation

(4 070)

Add: Net Profit 6 815 Closing Stock 31 000

Debtors 28 000

26 500Sundry Creditors 25 000 Less: Further Bad-

Debts (1 500)

Bills Payable 6 000 Bills Receivable 5 000

Outstanding Expenses 1 400 Prepaid Rent 7 000

Outstanding Wages 800 Accrued Commission 1 200

Prepaid Insurance 500

Cash in Hand 2 500

141 830 141 830

P3 (NOT-FOR-PROFIT)

Debts 1 500

Net Profit

Ajay (50%) 13 630

Vijay (50%)

39 800 39 800

Balance Sheet

As on March 31 2020

Particulars Amount (AED) Particulars Amount (AED)

Capital Accounting Investment 13 500

Ajay 60 000

66 815

Furniture 18 000

Add: Net Profit 6 815 Plan and Machinery

40 700

36 630Vijay 35 000

41 815

Less: Depreciation

(4 070)

Add: Net Profit 6 815 Closing Stock 31 000

Debtors 28 000

26 500Sundry Creditors 25 000 Less: Further Bad-

Debts (1 500)

Bills Payable 6 000 Bills Receivable 5 000

Outstanding Expenses 1 400 Prepaid Rent 7 000

Outstanding Wages 800 Accrued Commission 1 200

Prepaid Insurance 500

Cash in Hand 2 500

141 830 141 830

P3 (NOT-FOR-PROFIT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

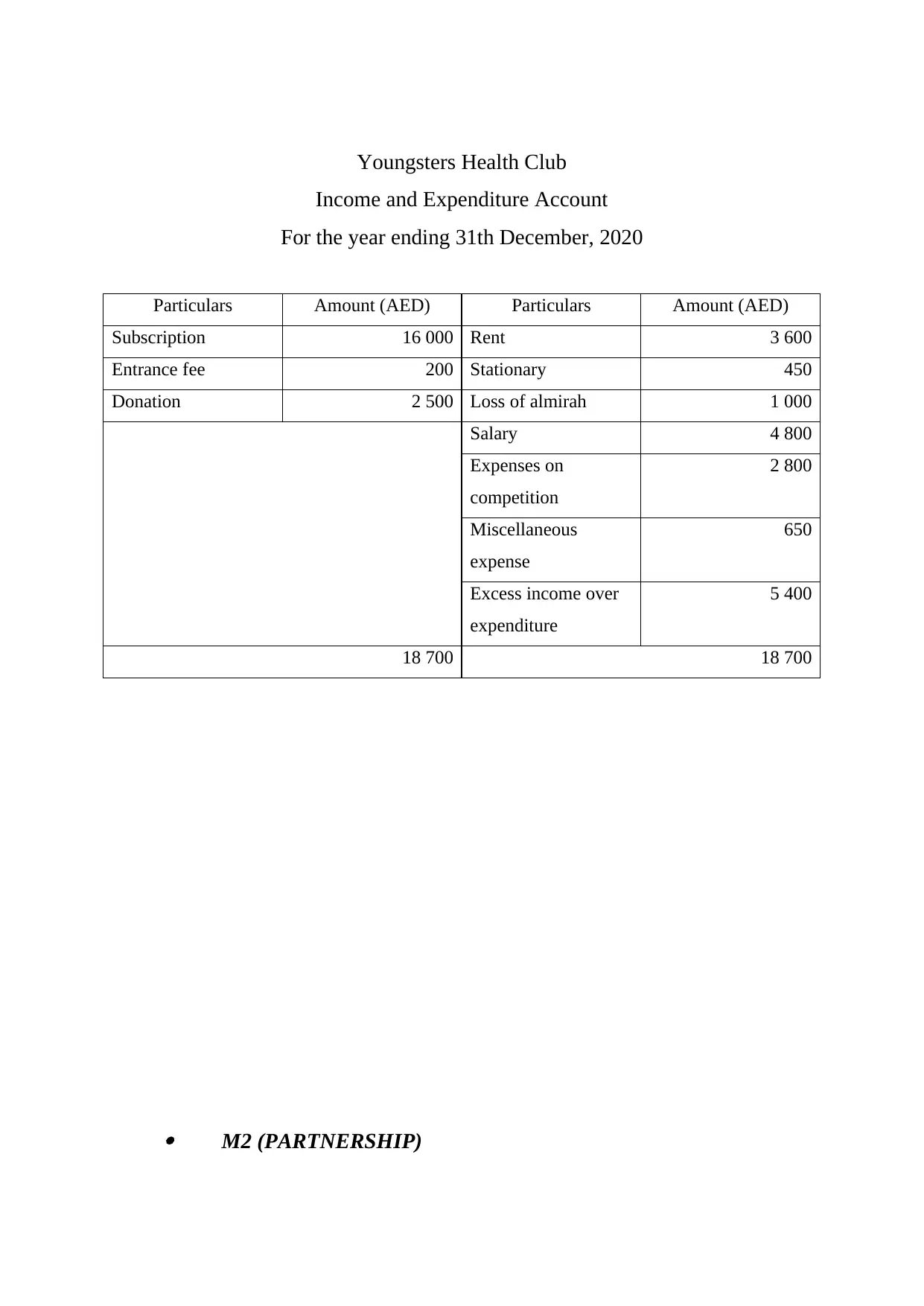

Youngsters Health Club

Income and Expenditure Account

For the year ending 31th December, 2020

Particulars Amount (AED) Particulars Amount (AED)

Subscription 16 000 Rent 3 600

Entrance fee 200 Stationary 450

Donation 2 500 Loss of almirah 1 000

Salary 4 800

Expenses on

competition

2 800

Miscellaneous

expense

650

Excess income over

expenditure

5 400

18 700 18 700

M2 (PARTNERSHIP)

Income and Expenditure Account

For the year ending 31th December, 2020

Particulars Amount (AED) Particulars Amount (AED)

Subscription 16 000 Rent 3 600

Entrance fee 200 Stationary 450

Donation 2 500 Loss of almirah 1 000

Salary 4 800

Expenses on

competition

2 800

Miscellaneous

expense

650

Excess income over

expenditure

5 400

18 700 18 700

M2 (PARTNERSHIP)

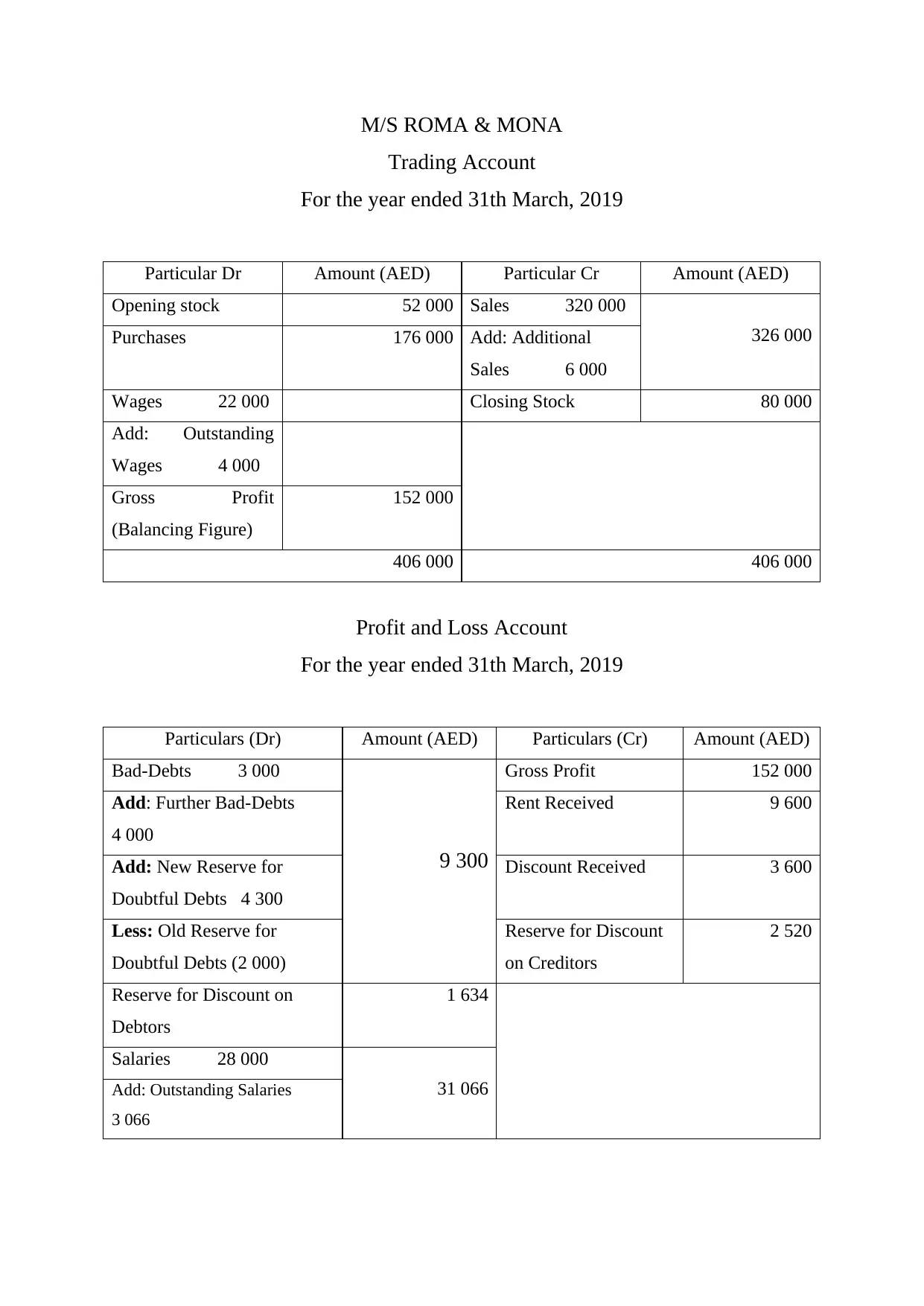

M/S ROMA & MONA

Trading Account

For the year ended 31th March, 2019

Particular Dr Amount (AED) Particular Cr Amount (AED)

Opening stock 52 000 Sales 320 000

326 000Purchases 176 000 Add: Additional

Sales 6 000

Wages 22 000 Closing Stock 80 000

Add: Outstanding

Wages 4 000

Gross Profit

(Balancing Figure)

152 000

406 000 406 000

Profit and Loss Account

For the year ended 31th March, 2019

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Bad-Debts 3 000

9 300

Gross Profit 152 000

Add: Further Bad-Debts

4 000

Rent Received 9 600

Add: New Reserve for

Doubtful Debts 4 300

Discount Received 3 600

Less: Old Reserve for

Doubtful Debts (2 000)

Reserve for Discount

on Creditors

2 520

Reserve for Discount on

Debtors

1 634

Salaries 28 000

31 066Add: Outstanding Salaries

3 066

Trading Account

For the year ended 31th March, 2019

Particular Dr Amount (AED) Particular Cr Amount (AED)

Opening stock 52 000 Sales 320 000

326 000Purchases 176 000 Add: Additional

Sales 6 000

Wages 22 000 Closing Stock 80 000

Add: Outstanding

Wages 4 000

Gross Profit

(Balancing Figure)

152 000

406 000 406 000

Profit and Loss Account

For the year ended 31th March, 2019

Particulars (Dr) Amount (AED) Particulars (Cr) Amount (AED)

Bad-Debts 3 000

9 300

Gross Profit 152 000

Add: Further Bad-Debts

4 000

Rent Received 9 600

Add: New Reserve for

Doubtful Debts 4 300

Discount Received 3 600

Less: Old Reserve for

Doubtful Debts (2 000)

Reserve for Discount

on Creditors

2 520

Reserve for Discount on

Debtors

1 634

Salaries 28 000

31 066Add: Outstanding Salaries

3 066

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.