Financial Accounting Process: Reporting and Decision Making Analysis

VerifiedAdded on 2023/06/08

|10

|583

|98

Report

AI Summary

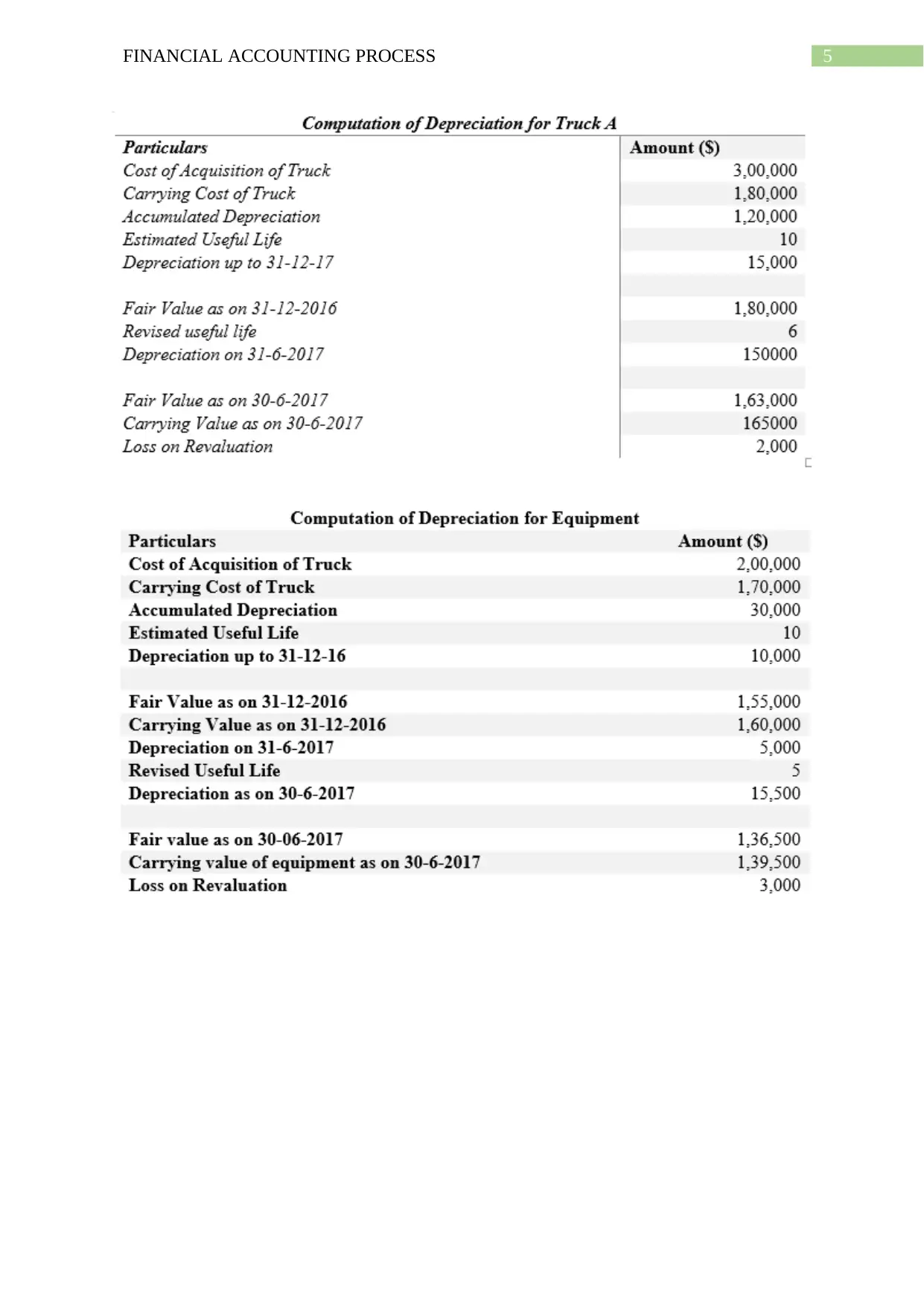

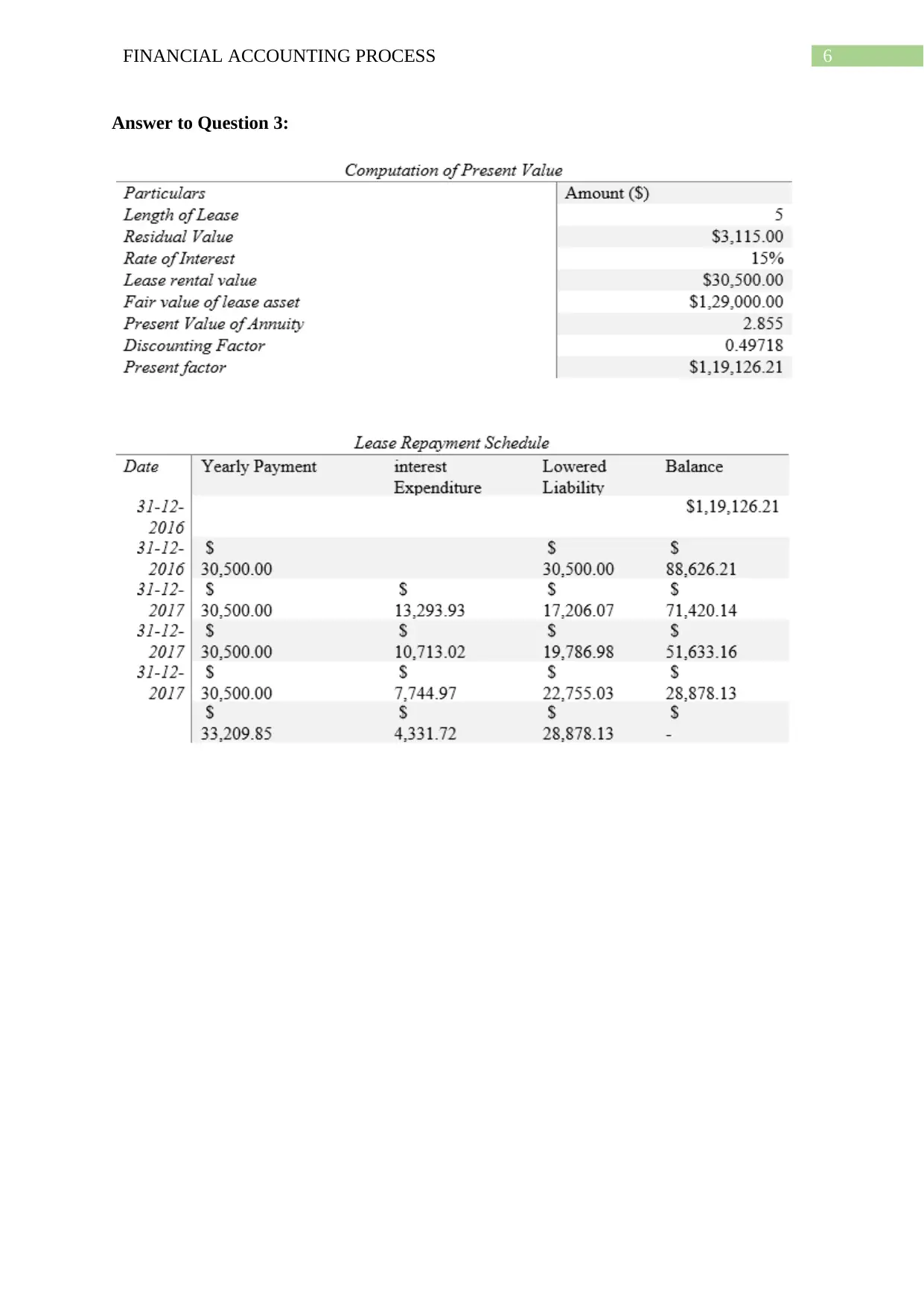

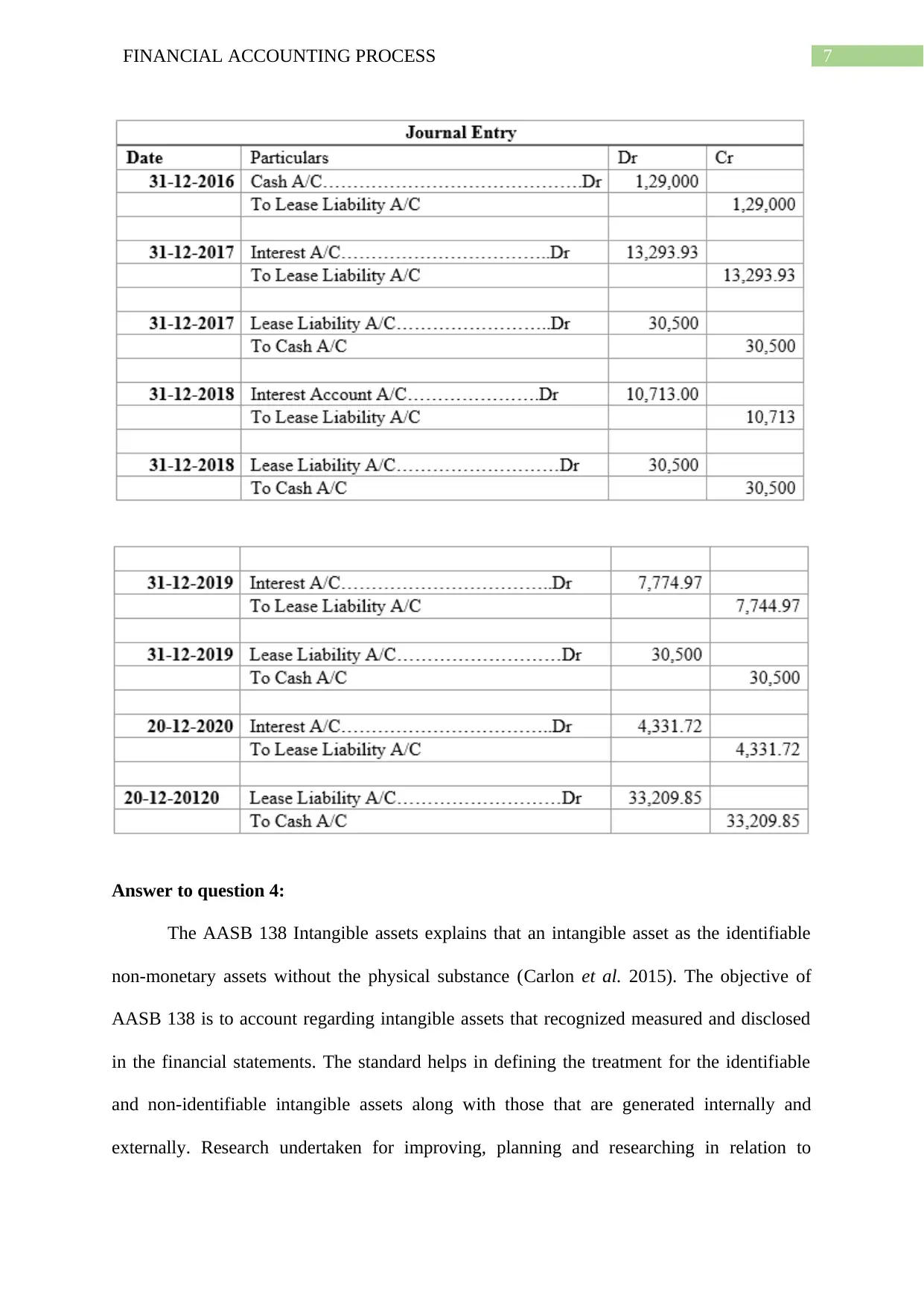

This report provides a detailed analysis of the financial accounting process, focusing on the recognition, measurement, and disclosure of intangible assets in accordance with AASB 138. It addresses two scenarios, the first examining general accounting principles and the second focusing on the treatment of research and development costs for ChiHerbal Ltd. The report explains how capitalized development costs can be considered intangible assets and should be reported in the financial statements, emphasizing the importance of identifying intangible assets that provide future economic benefits to the business. It also covers the criteria for recognizing intangible assets, including the probability of future economic benefits and the ability to reliably measure the cost of the assets. The document concludes that all expenses incurred on R&D by ChiHerbal Ltd should be recorded in the financial statement to ensure proper recognition of intangible assets.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.