Financial Reporting & Corporate Regulations: HA2032 Accounting Report

VerifiedAdded on 2023/06/04

|15

|2721

|480

Report

AI Summary

This report delves into various corporate accounting aspects, emphasizing corporate regulations and their impact on financial reporting. It explores accounting standards, including Australian Accounting Standards and IFRS, and evaluates the roles of the Australian Accounting Standards Board and the International Accounting Standards Board. The report also examines owner's equity, listing equity items and changes, and provides a comparative analysis of the debt and equity positions of four firms: ARDENT LEISURE Group, AQUIS Entertainment Limited, Corporate Travel Management Limited, and Ainsworth Game Technology Limited. The analysis focuses on the debt-to-equity ratio and its implications for each company's financial health, concluding that understanding these elements is crucial for achieving profitability. Desklib provides a platform to explore similar solved assignments.

Corporate Accounting 1

Corporate Accounting

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 2

Executive Summary

The report had explained about the various corporate accounting aspects within the organization.

With the regulations of the corporate within the organization has also explained with respect of

these organizations. The different accounting standards used by the organization for the effective

financial reporting. The items that had been listed in the owners’ equity includes the retained

profits, reserves and surplus and the issued capital as it has enabled to main the certain amount

with the organization. Total four organizations have been chosen for the practical

implementation of financial analysis in the business operations. These organizations are

ARDENT LEISURE Group, AQUIS Entertainment Limited, Corporate Travel Management

Limited and Ainsworth Game Technology Limited. It has been found in the last part of the report

that these all items are necessary to analyze as they will enable in achieving profitability.

Executive Summary

The report had explained about the various corporate accounting aspects within the organization.

With the regulations of the corporate within the organization has also explained with respect of

these organizations. The different accounting standards used by the organization for the effective

financial reporting. The items that had been listed in the owners’ equity includes the retained

profits, reserves and surplus and the issued capital as it has enabled to main the certain amount

with the organization. Total four organizations have been chosen for the practical

implementation of financial analysis in the business operations. These organizations are

ARDENT LEISURE Group, AQUIS Entertainment Limited, Corporate Travel Management

Limited and Ainsworth Game Technology Limited. It has been found in the last part of the report

that these all items are necessary to analyze as they will enable in achieving profitability.

Corporate Accounting 3

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Corporate Regulations.....................................................................................................................5

Analysis of financial accounting and reporting...........................................................................5

Accounting Standards and Setting...................................................................................................7

Evaluation of how the Australian accounting standards board and IFRS....................................7

Owner’s Equity................................................................................................................................8

From the financial statements, list each item of equity and changes in equity............................8

Comparative analysis of the debt and equity position of all four firms.....................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Corporate Regulations.....................................................................................................................5

Analysis of financial accounting and reporting...........................................................................5

Accounting Standards and Setting...................................................................................................7

Evaluation of how the Australian accounting standards board and IFRS....................................7

Owner’s Equity................................................................................................................................8

From the financial statements, list each item of equity and changes in equity............................8

Comparative analysis of the debt and equity position of all four firms.....................................10

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 4

Introduction

The report basically will depict the various corporate regulations so as to analyze the disclosure

of this financial information in the financial reports by the top level authorities of the

organization. This report will highlight the Australian Accounting standards, IFRS and give

necessary information about International accounting standard board. The comparison of the 4

organizations will be done irrespective of their nature and in various financial aspects.

Introduction

The report basically will depict the various corporate regulations so as to analyze the disclosure

of this financial information in the financial reports by the top level authorities of the

organization. This report will highlight the Australian Accounting standards, IFRS and give

necessary information about International accounting standard board. The comparison of the 4

organizations will be done irrespective of their nature and in various financial aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 5

Corporate Regulations

Analysis of financial accounting and reporting

The financial statements of the organization are considered as the important resource which

contains the important information in order to disclosure in financial statements. in a proper and

appropriate manner. It will provide appropriate information to detect fraudulent activity (Leuz

and Wysocki, 2016). The financial statements of the organization are basically presented and

also released during the general annual meetings of the organization in front of the shareholders,

officials and employees.

Regulation of financial accounting and reporting

These regulations which are set as financial accounting and reporting, can consist various sets of

guidelines which are needed to be followed by the organization before disclosing any of the

information (Leuz and Wysocki, 2016). The financial information which is reported consists of

the information regarding the share prices and other related information regarding the procedures

and policies and also the information related to the stakeholders. It also suggests that the

accounting information needs to be kept in two formats which are regulated and non- regulated.

This information should also ensure that they are reported without the conflict of interest in the

group. The proper financial analysis and evaluation should be done by the organization in order

to make annual reports & financial statements by using information in the financial accounts. It

would disclose all clauses and essential facts in relation to detect future threats at the particular

time period at the end of the financial year (Leuz and Wysocki, 2016).

Voluntary disclosure by manager

Corporate Regulations

Analysis of financial accounting and reporting

The financial statements of the organization are considered as the important resource which

contains the important information in order to disclosure in financial statements. in a proper and

appropriate manner. It will provide appropriate information to detect fraudulent activity (Leuz

and Wysocki, 2016). The financial statements of the organization are basically presented and

also released during the general annual meetings of the organization in front of the shareholders,

officials and employees.

Regulation of financial accounting and reporting

These regulations which are set as financial accounting and reporting, can consist various sets of

guidelines which are needed to be followed by the organization before disclosing any of the

information (Leuz and Wysocki, 2016). The financial information which is reported consists of

the information regarding the share prices and other related information regarding the procedures

and policies and also the information related to the stakeholders. It also suggests that the

accounting information needs to be kept in two formats which are regulated and non- regulated.

This information should also ensure that they are reported without the conflict of interest in the

group. The proper financial analysis and evaluation should be done by the organization in order

to make annual reports & financial statements by using information in the financial accounts. It

would disclose all clauses and essential facts in relation to detect future threats at the particular

time period at the end of the financial year (Leuz and Wysocki, 2016).

Voluntary disclosure by manager

Corporate Accounting 6

The willful divulgence of budgetary explanation by trough alludes to a circumstance wherein the

monetary instruments are displayed openly as and when requested without the authorization of

higher specialists (Leuz and Wysocki, 2016). This occasionally prompts wrong outcomes and

impact on the partners consequently pulling back their enthusiasm from the organization. The

exposure of money related data likewise influences the imperative choices of the organization by

releasing the private data that are a basic part and value touchy data. The chief may unveil

significant value delicate data to people along these lines influencing their benefits and offer

costs (Leuz and Wysocki, 2016).

Regulated reporting Vs disclosure by manager

It has to be ensured that the organization must follow the properly regulated reporting so that the

price related information is not affected and the organization is liable for the maintaining the

reliable balance between the authenticity as well as the accuracy of data (Leuz and Wysocki,

2016). This is done with the reason that it helps in reducing the scope of partiality as the

appropriate data is published once a year in accordance with that of the guidelines and policies

provided (Khan, 2015). The disclosure which is voluntary leads to the biases as well as the

feedbacks of the stakeholders since the disclosure is only done according to the requirements of

customer’s. The obligation which is used for reporting for the financial transactions has currently

been eliminated and the organizations have chosen the regulated disclosure method which will

enable in providing the positive impact on managers, business operations, investors and external

management (Khan, 2015).

The willful divulgence of budgetary explanation by trough alludes to a circumstance wherein the

monetary instruments are displayed openly as and when requested without the authorization of

higher specialists (Leuz and Wysocki, 2016). This occasionally prompts wrong outcomes and

impact on the partners consequently pulling back their enthusiasm from the organization. The

exposure of money related data likewise influences the imperative choices of the organization by

releasing the private data that are a basic part and value touchy data. The chief may unveil

significant value delicate data to people along these lines influencing their benefits and offer

costs (Leuz and Wysocki, 2016).

Regulated reporting Vs disclosure by manager

It has to be ensured that the organization must follow the properly regulated reporting so that the

price related information is not affected and the organization is liable for the maintaining the

reliable balance between the authenticity as well as the accuracy of data (Leuz and Wysocki,

2016). This is done with the reason that it helps in reducing the scope of partiality as the

appropriate data is published once a year in accordance with that of the guidelines and policies

provided (Khan, 2015). The disclosure which is voluntary leads to the biases as well as the

feedbacks of the stakeholders since the disclosure is only done according to the requirements of

customer’s. The obligation which is used for reporting for the financial transactions has currently

been eliminated and the organizations have chosen the regulated disclosure method which will

enable in providing the positive impact on managers, business operations, investors and external

management (Khan, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 7

Accounting Standards and Setting

Evaluation of how the Australian accounting standards board and IFRS

Australian Accounting Standards

The Australian Accounting Standard board is the government agency which is responsible for

maintaining and formulating the financial reporting standards and these standards are applicable

to the organizations whether public or of the private sector (Khan, 2015). AASB is the board

which helps in contributing to the development of IFRS in the global standard setting.

IFRS

International Financial Reporting Standards aides in giving a typical worldwide business dialect

with the goal that the books of records of organization everywhere throughout the globe can be

thought about (Guay, et. al., 2016). This gives a typical business dialect along these lines making

correlation less demanding crosswise over global limits (Guay, et. al., 2016). The expanding

universal exchange and bookkeeping have prompted the development of IFRS.

International accounting standard board

The International Accounting standard board is an autonomous association working for the

accomplishment of IFRS. It was established on on1st April 2001 for creating universal

benchmarks to be taken after around the world (Guay, et. al., 2016). The fundamental thought

process of this board is to create guidelines that are reasonable, high calibre, enforceable and

acknowledged by all.

Role of AASB in context of the formulation of IFRS

The AASB aids the plan of global norms to the IFR by following the Australian securities and

speculation commission Act 2001. It aids the improvement of a structure with specific norms, the

Accounting Standards and Setting

Evaluation of how the Australian accounting standards board and IFRS

Australian Accounting Standards

The Australian Accounting Standard board is the government agency which is responsible for

maintaining and formulating the financial reporting standards and these standards are applicable

to the organizations whether public or of the private sector (Khan, 2015). AASB is the board

which helps in contributing to the development of IFRS in the global standard setting.

IFRS

International Financial Reporting Standards aides in giving a typical worldwide business dialect

with the goal that the books of records of organization everywhere throughout the globe can be

thought about (Guay, et. al., 2016). This gives a typical business dialect along these lines making

correlation less demanding crosswise over global limits (Guay, et. al., 2016). The expanding

universal exchange and bookkeeping have prompted the development of IFRS.

International accounting standard board

The International Accounting standard board is an autonomous association working for the

accomplishment of IFRS. It was established on on1st April 2001 for creating universal

benchmarks to be taken after around the world (Guay, et. al., 2016). The fundamental thought

process of this board is to create guidelines that are reasonable, high calibre, enforceable and

acknowledged by all.

Role of AASB in context of the formulation of IFRS

The AASB aids the plan of global norms to the IFR by following the Australian securities and

speculation commission Act 2001. It aids the improvement of a structure with specific norms, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 8

setting of bookkeeping guidelines to be trailed by around the world, so a typical business dialect

can be embraced globally (Guay, et. al., 2016). It likewise takes an interest in contributing to the

advancement of the single arrangement of bookkeeping gauges that will be utilized everywhere

throughout the world.

Members of IASB

The part nations of IASB are not compelled to take after the enactments but rather in the event

that they do it will profit the bookkeeping structure and enhance the introduction of monetary

articulation. Monetary emergency demonstrates that there is a dissimilarity of market cost from

central qualities (Gitman, et. al., 2015). The IFRS does not represent legitimate standards and

subsequently, bookkeeping is utilized by the organization according to their wish. Exchanges are

deciphered diversely by each organization and offer ascend to window dressing. The part nations

of IASB henceforth are not required to obligatory take after the IFRS as their own particular

arrangement of bookkeeping benchmarks are according to the principles and approaches defined

in the worldwide board (Gitman, et. al., 2015).

Owner’s Equity

From the financial statements, list each item of equity and changes in equity

Contributed equity: The contributed capital is also known as the paid-up capital. It can be

defined as the assets which have been contributed by the investors in the organization in return of

stocks (Fourie, et. al., 2015). It is also termed as the price which has to be paid by the investors

in return for the stake in the organization.

Reserves: It is the equity of the stockholders apart from that of the share capital. It is also the

amount which has been retained in the business and this amount is not shredded to that of the

setting of bookkeeping guidelines to be trailed by around the world, so a typical business dialect

can be embraced globally (Guay, et. al., 2016). It likewise takes an interest in contributing to the

advancement of the single arrangement of bookkeeping gauges that will be utilized everywhere

throughout the world.

Members of IASB

The part nations of IASB are not compelled to take after the enactments but rather in the event

that they do it will profit the bookkeeping structure and enhance the introduction of monetary

articulation. Monetary emergency demonstrates that there is a dissimilarity of market cost from

central qualities (Gitman, et. al., 2015). The IFRS does not represent legitimate standards and

subsequently, bookkeeping is utilized by the organization according to their wish. Exchanges are

deciphered diversely by each organization and offer ascend to window dressing. The part nations

of IASB henceforth are not required to obligatory take after the IFRS as their own particular

arrangement of bookkeeping benchmarks are according to the principles and approaches defined

in the worldwide board (Gitman, et. al., 2015).

Owner’s Equity

From the financial statements, list each item of equity and changes in equity

Contributed equity: The contributed capital is also known as the paid-up capital. It can be

defined as the assets which have been contributed by the investors in the organization in return of

stocks (Fourie, et. al., 2015). It is also termed as the price which has to be paid by the investors

in return for the stake in the organization.

Reserves: It is the equity of the stockholders apart from that of the share capital. It is also the

amount which has been retained in the business and this amount is not shredded to that of the

Corporate Accounting 9

owners and the investors (Fourie, et. al., 2015). The reserves are also called the stock equity

capital other than the share capital.

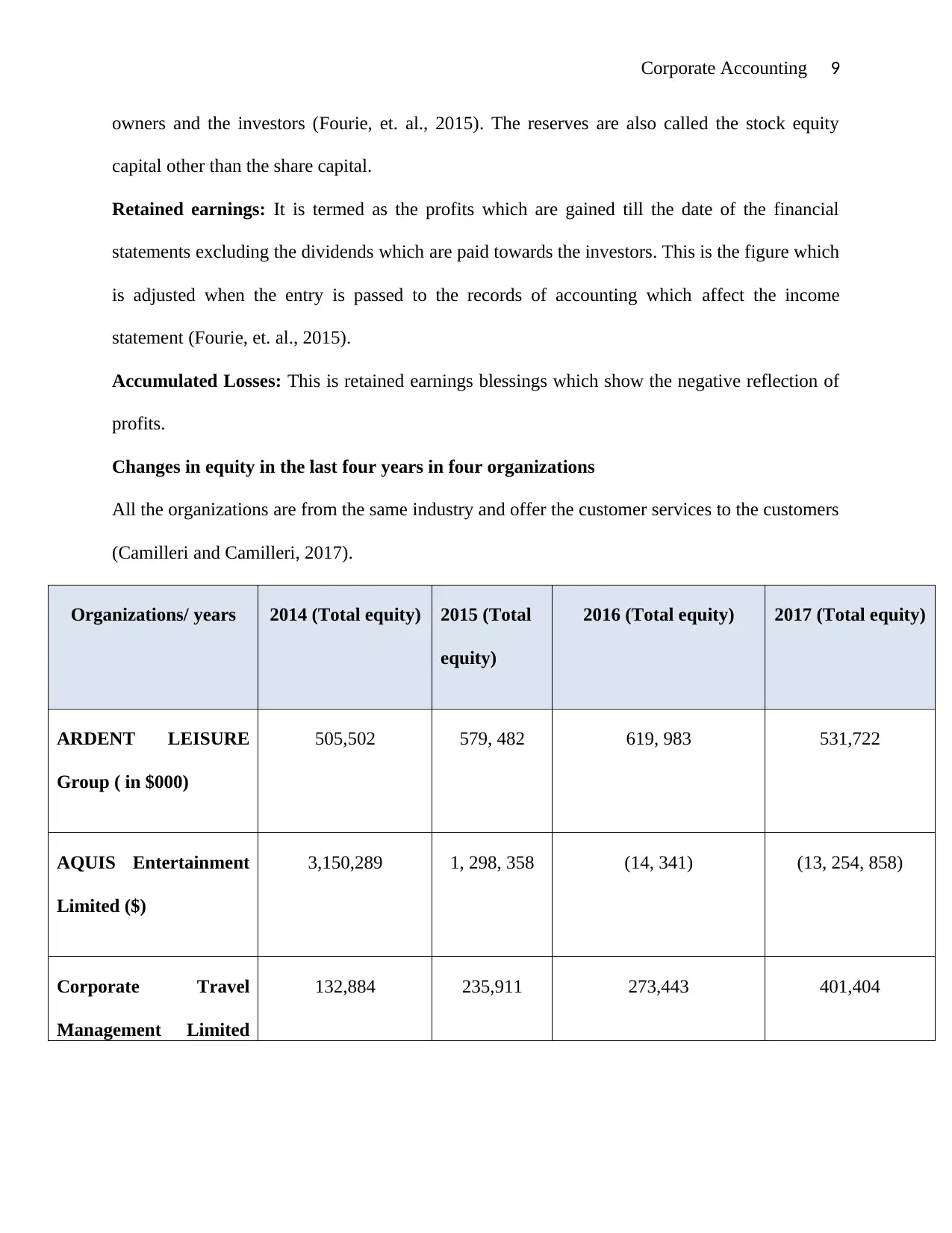

Retained earnings: It is termed as the profits which are gained till the date of the financial

statements excluding the dividends which are paid towards the investors. This is the figure which

is adjusted when the entry is passed to the records of accounting which affect the income

statement (Fourie, et. al., 2015).

Accumulated Losses: This is retained earnings blessings which show the negative reflection of

profits.

Changes in equity in the last four years in four organizations

All the organizations are from the same industry and offer the customer services to the customers

(Camilleri and Camilleri, 2017).

Organizations/ years 2014 (Total equity) 2015 (Total

equity)

2016 (Total equity) 2017 (Total equity)

ARDENT LEISURE

Group ( in $000)

505,502 579, 482 619, 983 531,722

AQUIS Entertainment

Limited ($)

3,150,289 1, 298, 358 (14, 341) (13, 254, 858)

Corporate Travel

Management Limited

132,884 235,911 273,443 401,404

owners and the investors (Fourie, et. al., 2015). The reserves are also called the stock equity

capital other than the share capital.

Retained earnings: It is termed as the profits which are gained till the date of the financial

statements excluding the dividends which are paid towards the investors. This is the figure which

is adjusted when the entry is passed to the records of accounting which affect the income

statement (Fourie, et. al., 2015).

Accumulated Losses: This is retained earnings blessings which show the negative reflection of

profits.

Changes in equity in the last four years in four organizations

All the organizations are from the same industry and offer the customer services to the customers

(Camilleri and Camilleri, 2017).

Organizations/ years 2014 (Total equity) 2015 (Total

equity)

2016 (Total equity) 2017 (Total equity)

ARDENT LEISURE

Group ( in $000)

505,502 579, 482 619, 983 531,722

AQUIS Entertainment

Limited ($)

3,150,289 1, 298, 358 (14, 341) (13, 254, 858)

Corporate Travel

Management Limited

132,884 235,911 273,443 401,404

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting 10

( in $000)

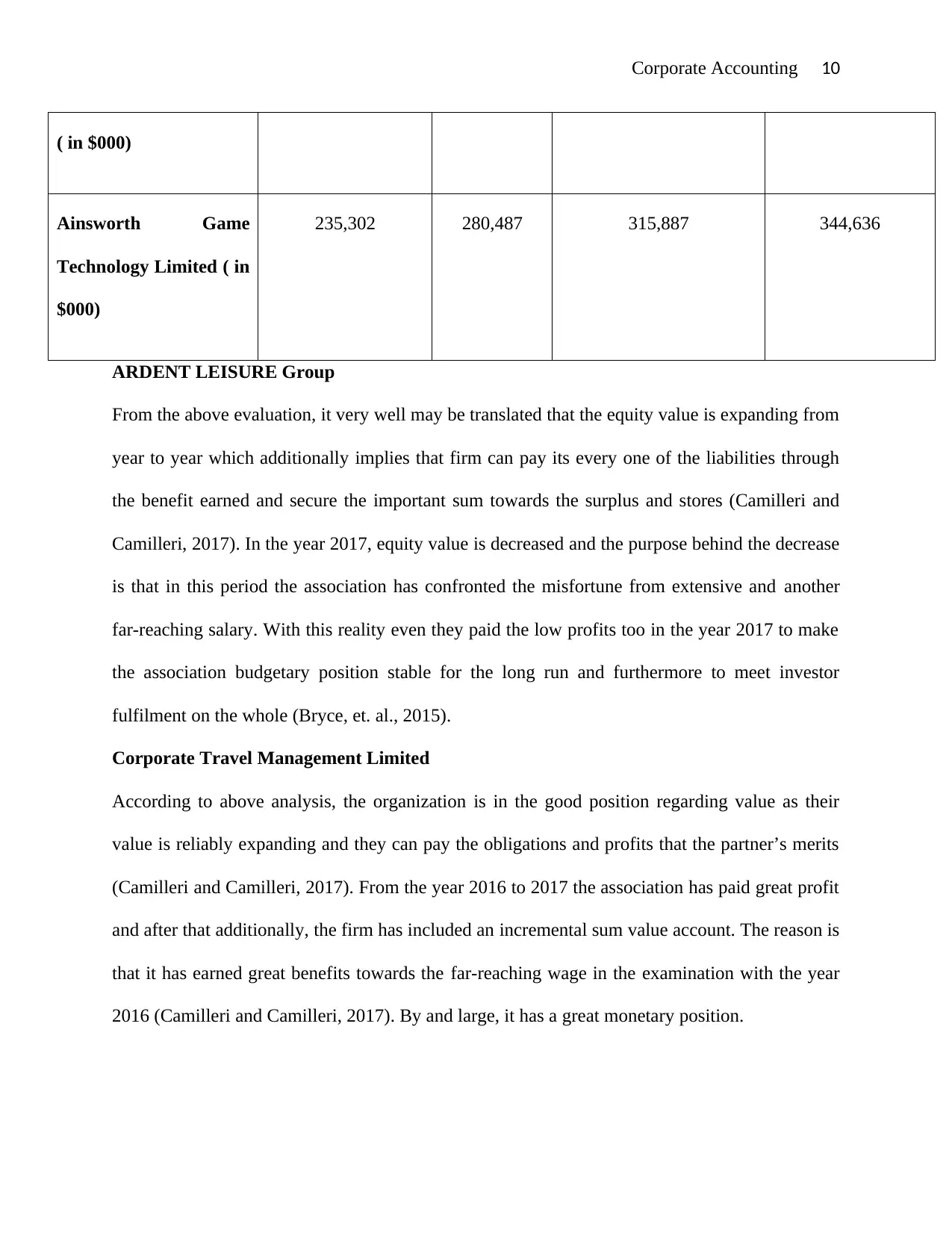

Ainsworth Game

Technology Limited ( in

$000)

235,302 280,487 315,887 344,636

ARDENT LEISURE Group

From the above evaluation, it very well may be translated that the equity value is expanding from

year to year which additionally implies that firm can pay its every one of the liabilities through

the benefit earned and secure the important sum towards the surplus and stores (Camilleri and

Camilleri, 2017). In the year 2017, equity value is decreased and the purpose behind the decrease

is that in this period the association has confronted the misfortune from extensive and another

far-reaching salary. With this reality even they paid the low profits too in the year 2017 to make

the association budgetary position stable for the long run and furthermore to meet investor

fulfilment on the whole (Bryce, et. al., 2015).

Corporate Travel Management Limited

According to above analysis, the organization is in the good position regarding value as their

value is reliably expanding and they can pay the obligations and profits that the partner’s merits

(Camilleri and Camilleri, 2017). From the year 2016 to 2017 the association has paid great profit

and after that additionally, the firm has included an incremental sum value account. The reason is

that it has earned great benefits towards the far-reaching wage in the examination with the year

2016 (Camilleri and Camilleri, 2017). By and large, it has a great monetary position.

( in $000)

Ainsworth Game

Technology Limited ( in

$000)

235,302 280,487 315,887 344,636

ARDENT LEISURE Group

From the above evaluation, it very well may be translated that the equity value is expanding from

year to year which additionally implies that firm can pay its every one of the liabilities through

the benefit earned and secure the important sum towards the surplus and stores (Camilleri and

Camilleri, 2017). In the year 2017, equity value is decreased and the purpose behind the decrease

is that in this period the association has confronted the misfortune from extensive and another

far-reaching salary. With this reality even they paid the low profits too in the year 2017 to make

the association budgetary position stable for the long run and furthermore to meet investor

fulfilment on the whole (Bryce, et. al., 2015).

Corporate Travel Management Limited

According to above analysis, the organization is in the good position regarding value as their

value is reliably expanding and they can pay the obligations and profits that the partner’s merits

(Camilleri and Camilleri, 2017). From the year 2016 to 2017 the association has paid great profit

and after that additionally, the firm has included an incremental sum value account. The reason is

that it has earned great benefits towards the far-reaching wage in the examination with the year

2016 (Camilleri and Camilleri, 2017). By and large, it has a great monetary position.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting 11

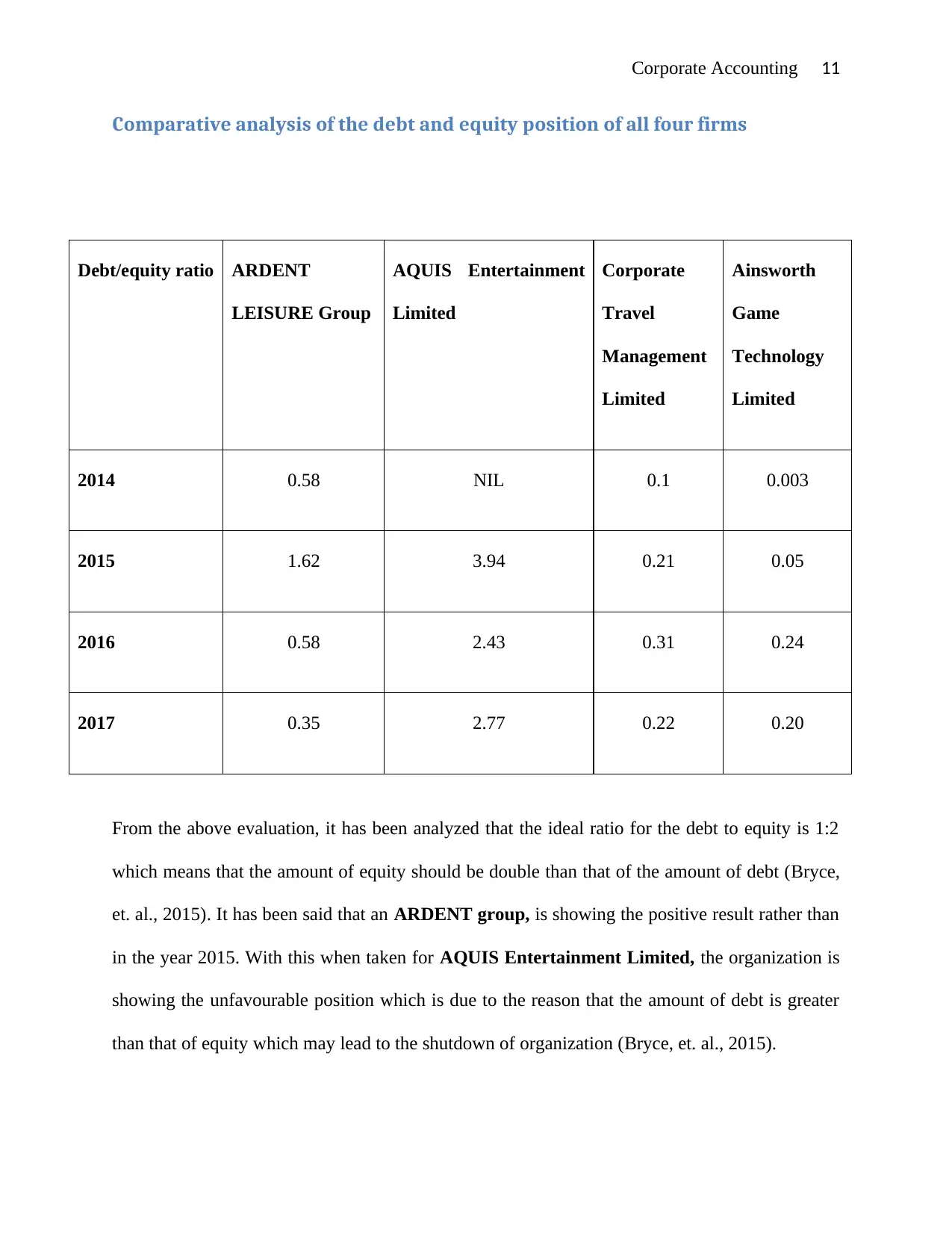

Comparative analysis of the debt and equity position of all four firms

Debt/equity ratio ARDENT

LEISURE Group

AQUIS Entertainment

Limited

Corporate

Travel

Management

Limited

Ainsworth

Game

Technology

Limited

2014 0.58 NIL 0.1 0.003

2015 1.62 3.94 0.21 0.05

2016 0.58 2.43 0.31 0.24

2017 0.35 2.77 0.22 0.20

From the above evaluation, it has been analyzed that the ideal ratio for the debt to equity is 1:2

which means that the amount of equity should be double than that of the amount of debt (Bryce,

et. al., 2015). It has been said that an ARDENT group, is showing the positive result rather than

in the year 2015. With this when taken for AQUIS Entertainment Limited, the organization is

showing the unfavourable position which is due to the reason that the amount of debt is greater

than that of equity which may lead to the shutdown of organization (Bryce, et. al., 2015).

Comparative analysis of the debt and equity position of all four firms

Debt/equity ratio ARDENT

LEISURE Group

AQUIS Entertainment

Limited

Corporate

Travel

Management

Limited

Ainsworth

Game

Technology

Limited

2014 0.58 NIL 0.1 0.003

2015 1.62 3.94 0.21 0.05

2016 0.58 2.43 0.31 0.24

2017 0.35 2.77 0.22 0.20

From the above evaluation, it has been analyzed that the ideal ratio for the debt to equity is 1:2

which means that the amount of equity should be double than that of the amount of debt (Bryce,

et. al., 2015). It has been said that an ARDENT group, is showing the positive result rather than

in the year 2015. With this when taken for AQUIS Entertainment Limited, the organization is

showing the unfavourable position which is due to the reason that the amount of debt is greater

than that of equity which may lead to the shutdown of organization (Bryce, et. al., 2015).

Corporate Accounting 12

In case of Corporate Travel Management Limited, the debt-equity ratio is in good condition

as the ratio of debt is less than 1 which can be said that the investors of the organization can

easily be paid off through the equity (Bryce, et. al., 2015). For Ainsworth Game Technology

Limited, also the debt-equity ratio is also positive and is also liable to pay all the obligations

through equity so that the situation of shut down may not occur.

In case of Corporate Travel Management Limited, the debt-equity ratio is in good condition

as the ratio of debt is less than 1 which can be said that the investors of the organization can

easily be paid off through the equity (Bryce, et. al., 2015). For Ainsworth Game Technology

Limited, also the debt-equity ratio is also positive and is also liable to pay all the obligations

through equity so that the situation of shut down may not occur.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.