Financial Reporting Report: AASB Amendments and Financials

VerifiedAdded on 2020/03/02

|10

|952

|47

Report

AI Summary

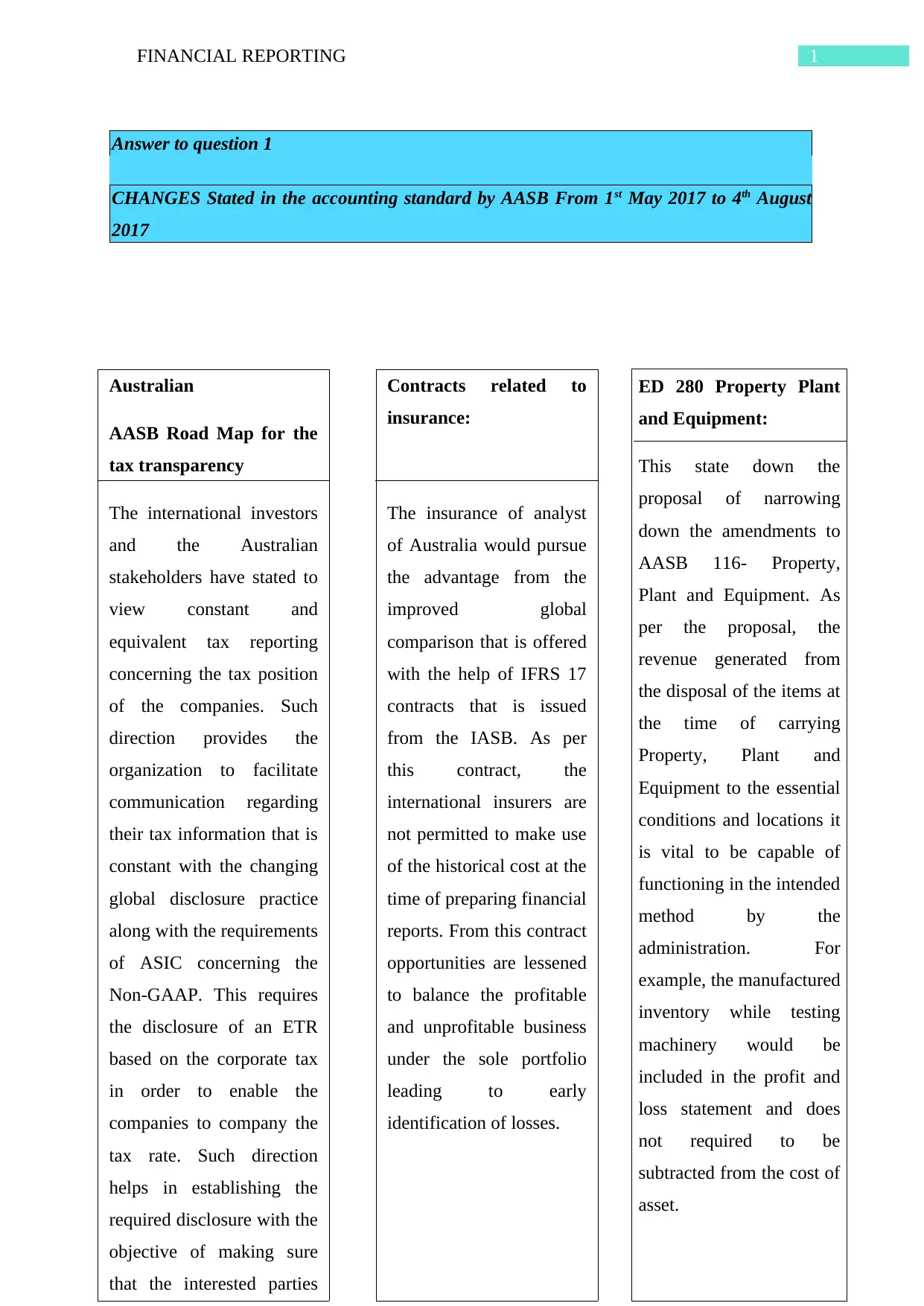

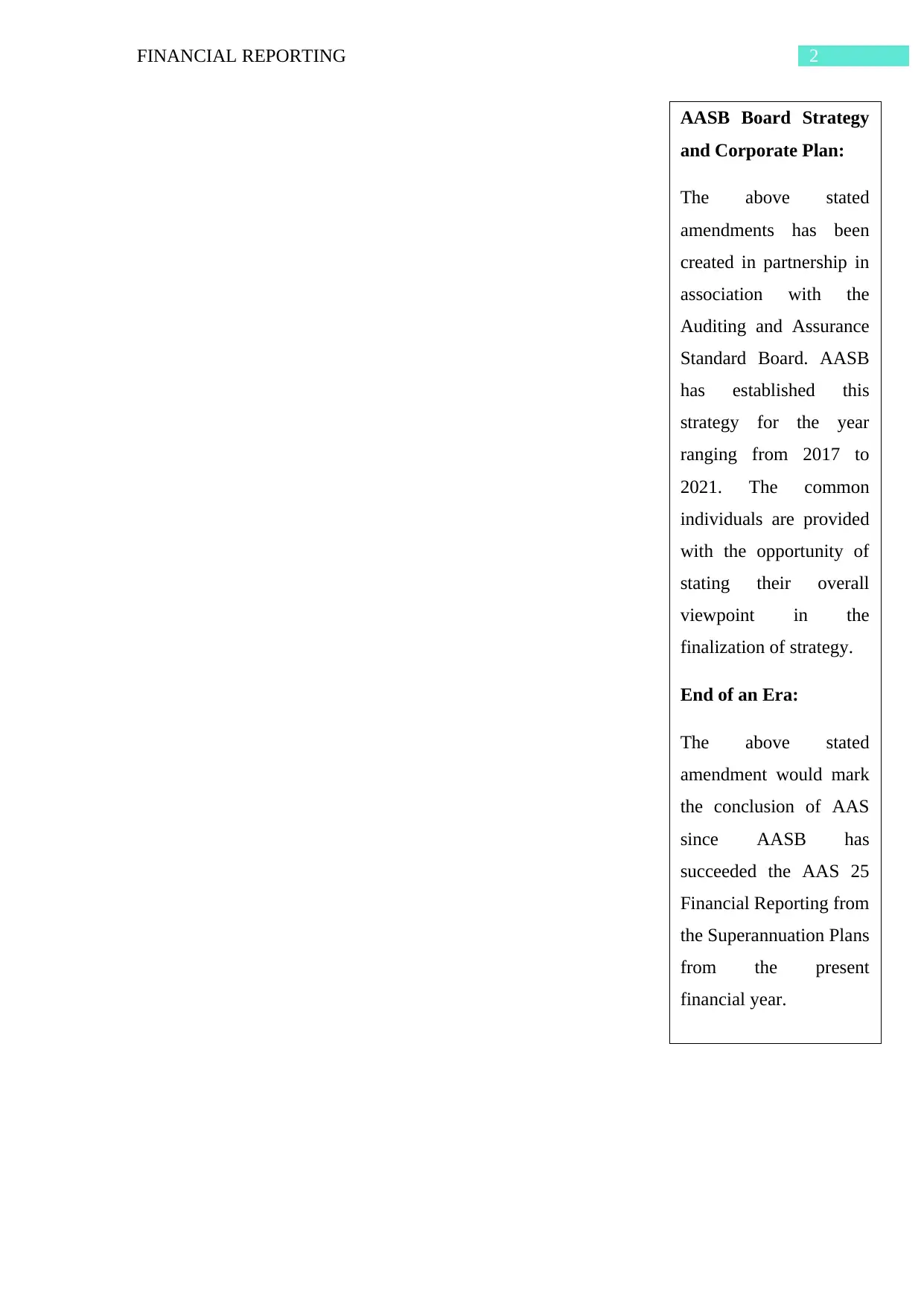

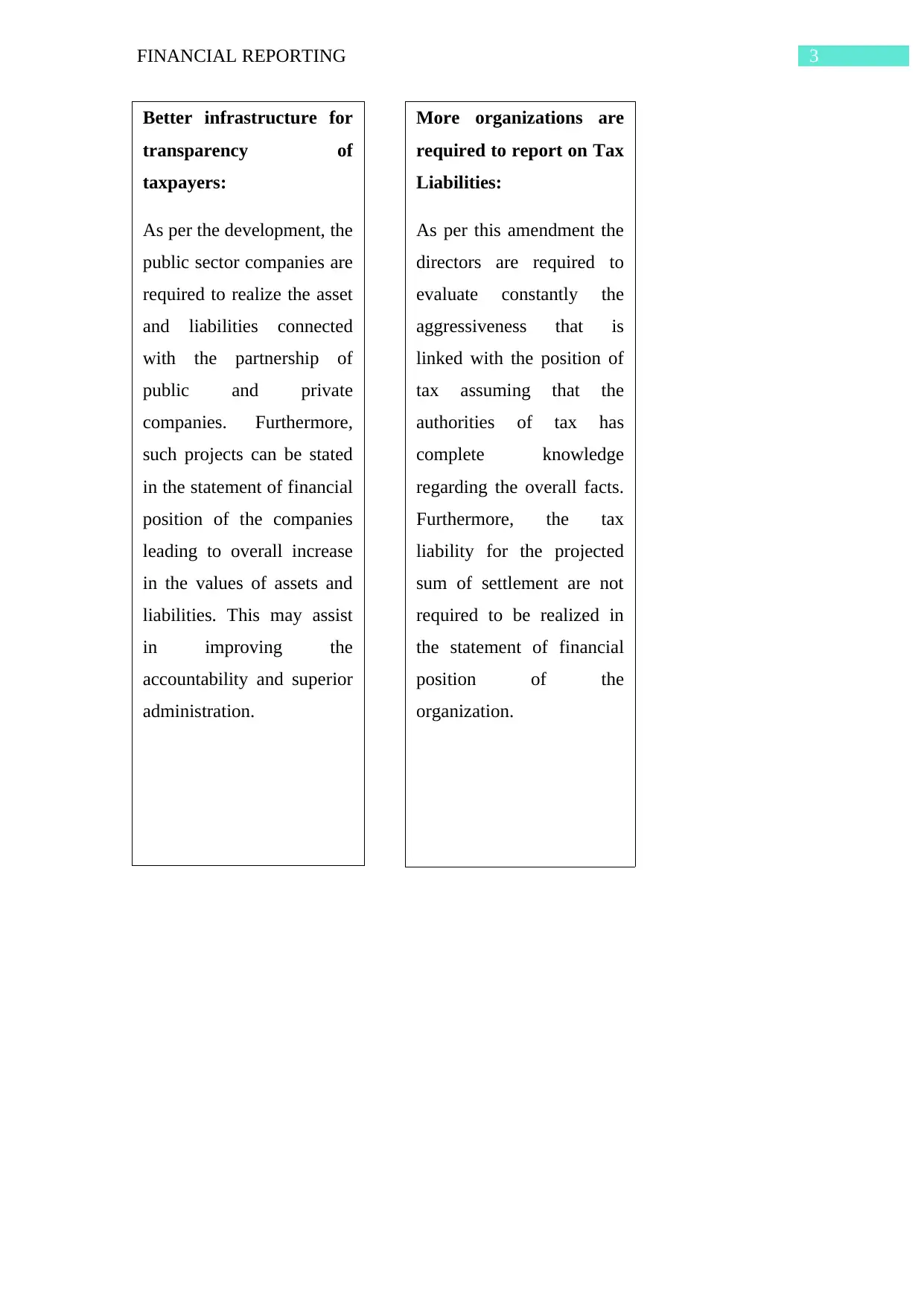

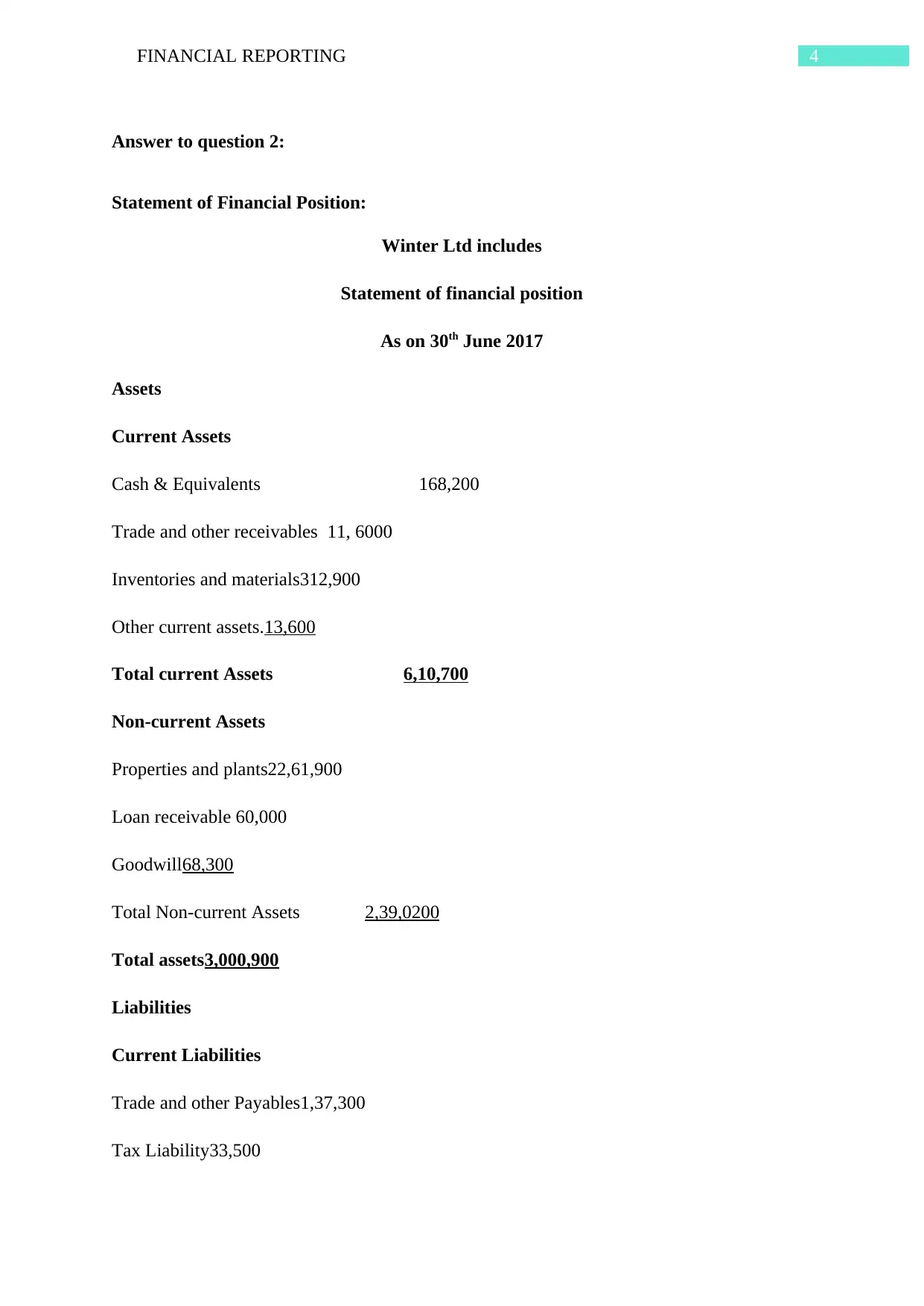

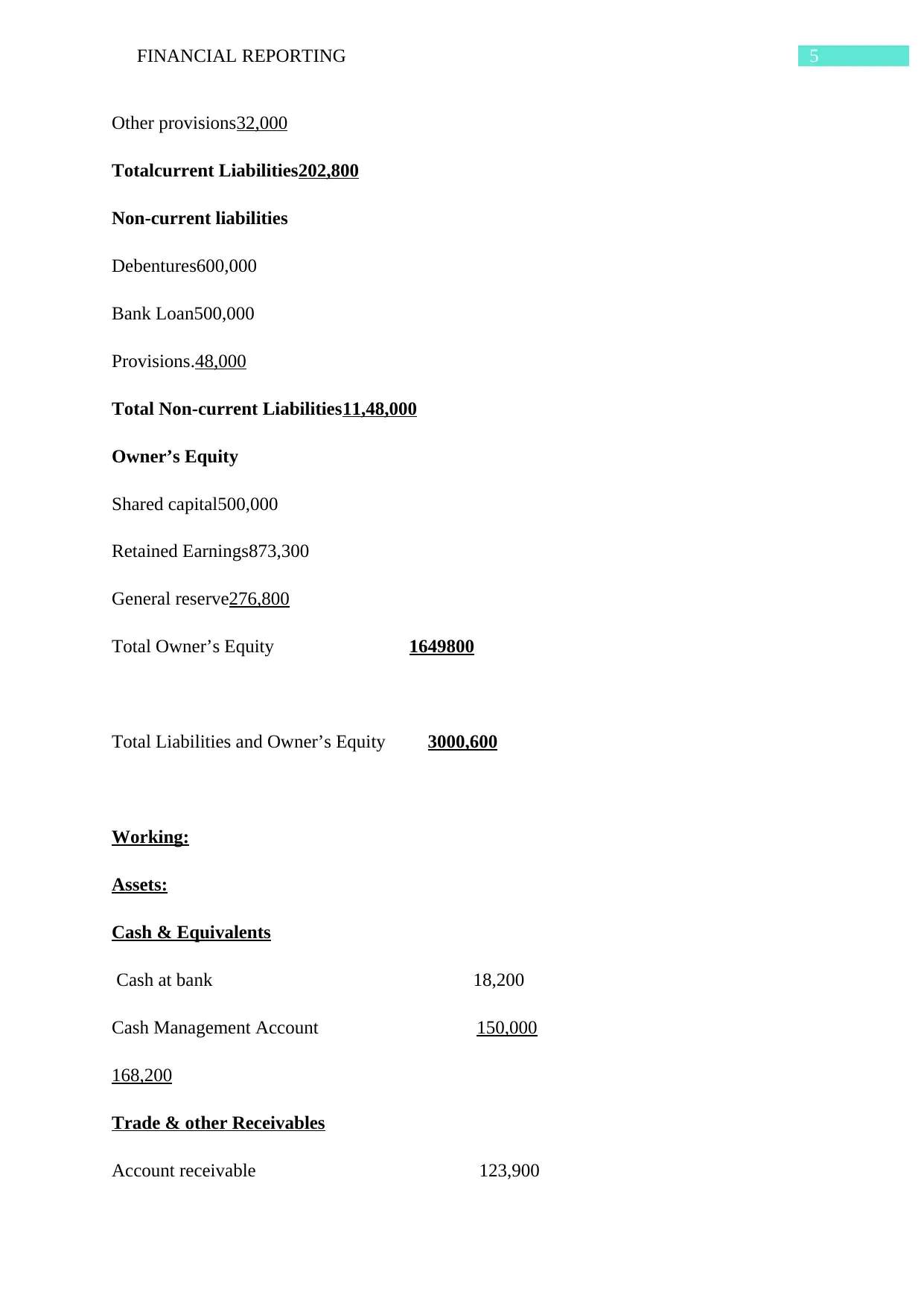

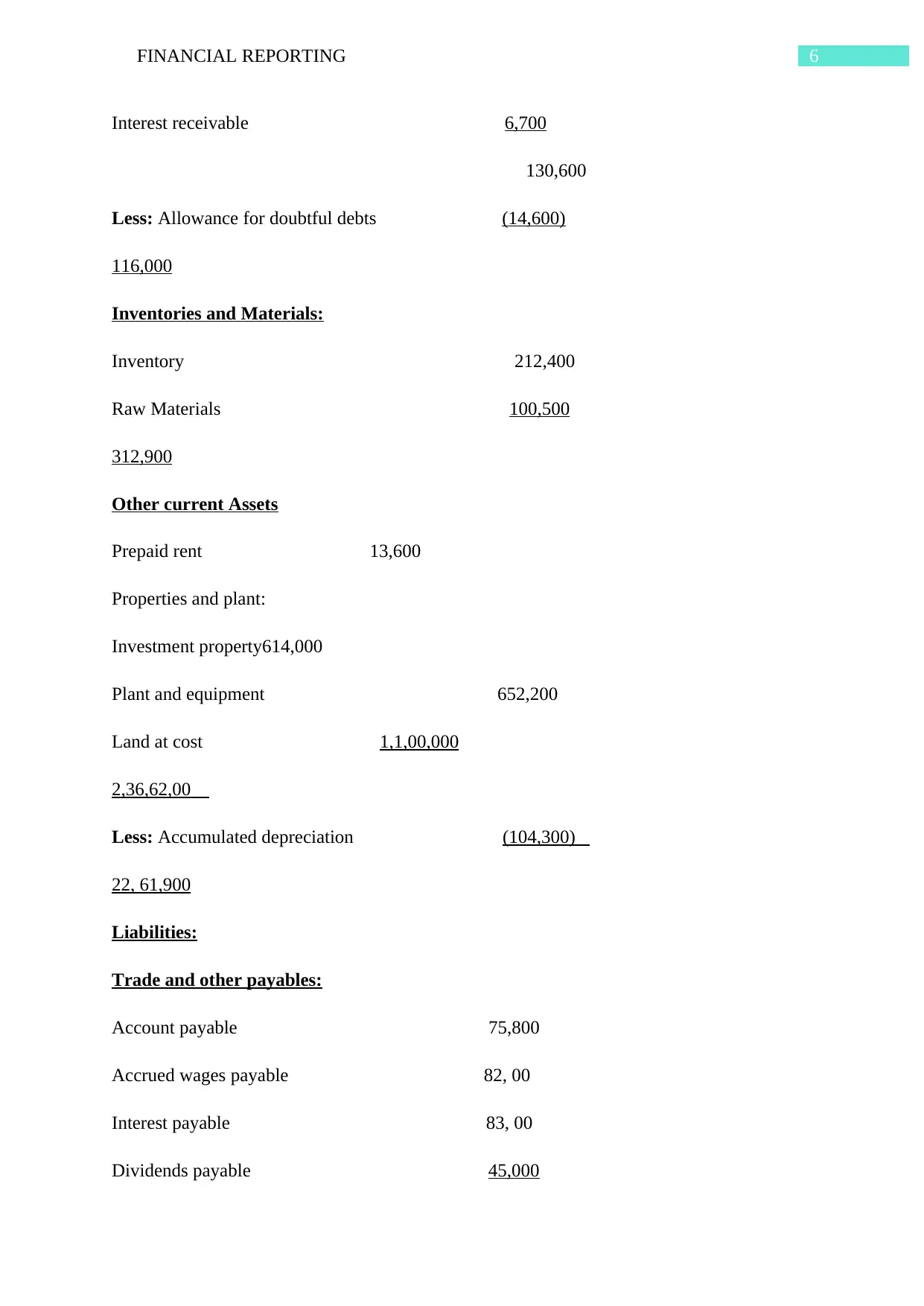

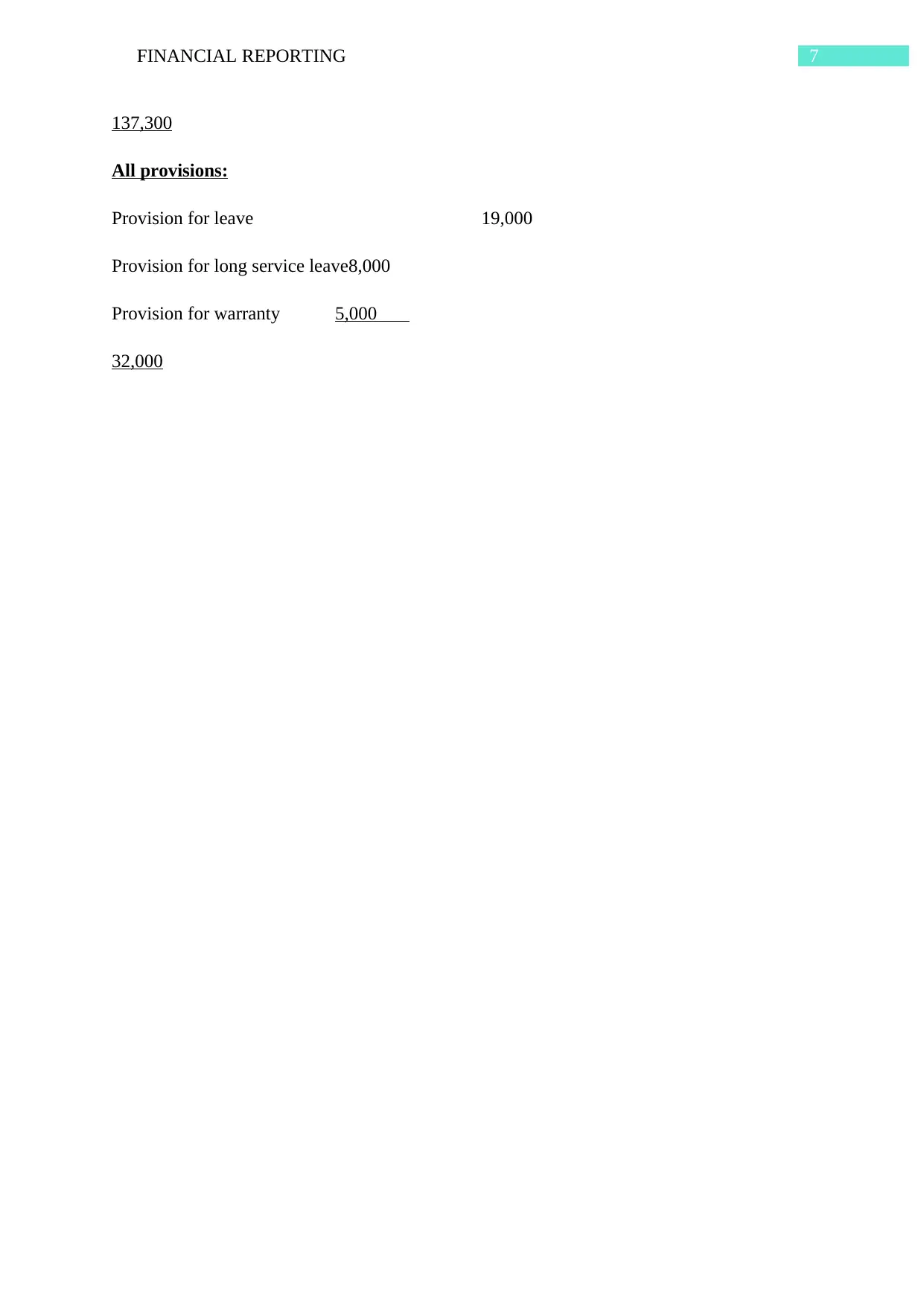

This report provides an analysis of financial reporting, focusing on recent amendments by AASB and the financial statements of Winter Ltd. The report begins by outlining key changes in accounting standards, including those related to Property, Plant, and Equipment (AASB 116), insurance contracts, and tax transparency. It also discusses the AASB Board Strategy and Corporate Plan, along with the implications of these changes. The second part of the report presents a detailed Statement of Financial Position for Winter Ltd as of June 30, 2017, including asset and liability breakdowns, along with working notes for calculations and the accounting standards applied. The report concludes with a list of relevant references to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.