Financial Reporting: Framework, Analysis, and Benefits Report

VerifiedAdded on 2021/02/20

|16

|4950

|32

Report

AI Summary

This report provides a detailed overview of financial reporting, starting with its definition and purposes, including providing information to stakeholders, evaluating data, and supporting decision-making. It explores both regulatory and conceptual frameworks, emphasizing qualitative characteristics such as relevance, faithfulness, verifiability, comparability, and understandability. The report identifies various stakeholders like managers, employees, lenders, customers, government, and suppliers, detailing their interests in financial information. It further discusses how financial reporting meets organizational objectives through the use of balance sheets, income statements, and cash flow statements. Additionally, it delves into the interpretation of financial information, using an example of a profit and loss account. The report also covers the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), along with models of financial reporting and auditing, and the overall variation and importance of financial reporting across different countries and organizations. This report highlights the importance of financial reporting in providing accurate and reliable information for effective decision-making by various stakeholders.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Meaning of financial reporting with the various purposes and regulatory and conceptual

framework...................................................................................................................................1

P 2 Purpose of financial reporting meeting the organization objective and goals......................5

LO 2.................................................................................................................................................6

P 3 Interpretation of financial information..................................................................................6

P 4 Evaluation of organization performance with different ratios..............................................6

LO 3 ................................................................................................................................................9

P 5 Benefits of International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) .......................................................................................................9

P 6 Models of financial reporting and auditing ........................................................................10

LO 4...............................................................................................................................................11

P 7 Variation and importance of financial reporting.................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Meaning of financial reporting with the various purposes and regulatory and conceptual

framework...................................................................................................................................1

P 2 Purpose of financial reporting meeting the organization objective and goals......................5

LO 2.................................................................................................................................................6

P 3 Interpretation of financial information..................................................................................6

P 4 Evaluation of organization performance with different ratios..............................................6

LO 3 ................................................................................................................................................9

P 5 Benefits of International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) .......................................................................................................9

P 6 Models of financial reporting and auditing ........................................................................10

LO 4...............................................................................................................................................11

P 7 Variation and importance of financial reporting.................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial reporting refers to disclose the financial data and results related to the company

performance to the different stakeholders such as investors, customers, creditors, employees etc.

in the company. Financial reporting provides the various monetary and non-monetary

information to the organization to evaluate the financial result and help the different stakeholders

to make effective decision regarding the investment and improving productivity and profitability

of the company. It helps the company to get the results of the company in particular time period.

The report highlights the various purpose of financial reporting ion the organization and different

regulatory and conceptual framework to present the data and information in prescribed formate.

The report explains the use of different financial statements such as balance sheet, profit and loss

account, trading account and cash flow to evaluate the performance of the company.

It provides the importance of ratios in the organization to evaluate performance with the

other companies. The ratio analyse help the company to find the performance and productivity of

the company by comparing the results to different year results. The report also highlights the

benefits of IAS ans IFRS in the company and importance of financial reporting across the

different countries. The accounting standard provide general guidelines to the company to

present the data ion more precise form to improve the understandability of the data.

LO 1

P 1 Meaning of financial reporting with the various purposes and regulatory and conceptual

framework

Meaning : Financial reporting refers to present and disclose all the data related to finance

of the company in more precise format under the guidance of accounting concept and principle

to the different users who have interest in financial information (Mazur, and Pisarski, 2015). It

includes the various statements such as balance sheet, profit and loss account, income statements,

cash flow etc. to present the data and evaluate them to get the effective and efficient financial

result.

Purpose of financial reporting

Providing information : The aim of preparing financial report in the organization to

provide the different kinds of information to the different users and stakeholders so they can get

1

Financial reporting refers to disclose the financial data and results related to the company

performance to the different stakeholders such as investors, customers, creditors, employees etc.

in the company. Financial reporting provides the various monetary and non-monetary

information to the organization to evaluate the financial result and help the different stakeholders

to make effective decision regarding the investment and improving productivity and profitability

of the company. It helps the company to get the results of the company in particular time period.

The report highlights the various purpose of financial reporting ion the organization and different

regulatory and conceptual framework to present the data and information in prescribed formate.

The report explains the use of different financial statements such as balance sheet, profit and loss

account, trading account and cash flow to evaluate the performance of the company.

It provides the importance of ratios in the organization to evaluate performance with the

other companies. The ratio analyse help the company to find the performance and productivity of

the company by comparing the results to different year results. The report also highlights the

benefits of IAS ans IFRS in the company and importance of financial reporting across the

different countries. The accounting standard provide general guidelines to the company to

present the data ion more precise form to improve the understandability of the data.

LO 1

P 1 Meaning of financial reporting with the various purposes and regulatory and conceptual

framework

Meaning : Financial reporting refers to present and disclose all the data related to finance

of the company in more precise format under the guidance of accounting concept and principle

to the different users who have interest in financial information (Mazur, and Pisarski, 2015). It

includes the various statements such as balance sheet, profit and loss account, income statements,

cash flow etc. to present the data and evaluate them to get the effective and efficient financial

result.

Purpose of financial reporting

Providing information : The aim of preparing financial report in the organization to

provide the different kinds of information to the different users and stakeholders so they can get

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the benefits from the information. The various financial report provide t eh different information.

For example cash flow statements help the company to evaluate the total inflow and outflow of

cash in particular accounting period to meet the requirement of the company and balance sheet

statement are prepared to provide the information related to the financial position such as total

debtor and creditor, assets, liability etc. to help the investor to take the investment decision. The

presentation of financial information is also required by the firm to attract the customer and pool

the investor toward the company outputs.

Evaluating data : Financial reports provide the information to the company to evaluate

the performance to take effective decisions. The comparison of financial report to the different

accounting year and to compare the performance of one company to the other company. It helps

them to find position in the market in compare to other company in same industry and

understood the trend in the market to improve the performance and productivity of the company.

Decision making : Financial report provides the relevant data to the different

stakeholders such as investor, customer, creditors, employees, manager and owner to get the

result of the company and take the decision of investment, purchase and lend money to the

organization (Cardwell,, Williams, and Pyle,, 2017). It increases the productivity of company

with the profitability. The financial information such as revenue, profit and expenses of the

accounting period help the investor to make the decision regarding whether to invest in the

company or not. A sound financial growth pool the investor towards the company.

Conceptual framework and regulatory framework

Regulatory framework : The regulatory framework provides the set of rules and

regulation for treatment of accounting data and values. The framework provides various standard

to measure the performance and provide a fixed set of standard for the valuation of company data

to take the important decisions.

The purpose of regulatory framework is help the company in preparation of financial

statement because they are used by the different users. It strengthens the accountability and

creditability of the organization by using different accounting standard such as IFRS, IAS etc.

Conceptual framework : It is used by the organization to describe the nature and

objective of financial statement and accounting and set the limit of accounting to present the

information accurately and correctly (What is Conceptual Framework?, 2019). It explains the

fundamental principles and interrelated objectives.

2

For example cash flow statements help the company to evaluate the total inflow and outflow of

cash in particular accounting period to meet the requirement of the company and balance sheet

statement are prepared to provide the information related to the financial position such as total

debtor and creditor, assets, liability etc. to help the investor to take the investment decision. The

presentation of financial information is also required by the firm to attract the customer and pool

the investor toward the company outputs.

Evaluating data : Financial reports provide the information to the company to evaluate

the performance to take effective decisions. The comparison of financial report to the different

accounting year and to compare the performance of one company to the other company. It helps

them to find position in the market in compare to other company in same industry and

understood the trend in the market to improve the performance and productivity of the company.

Decision making : Financial report provides the relevant data to the different

stakeholders such as investor, customer, creditors, employees, manager and owner to get the

result of the company and take the decision of investment, purchase and lend money to the

organization (Cardwell,, Williams, and Pyle,, 2017). It increases the productivity of company

with the profitability. The financial information such as revenue, profit and expenses of the

accounting period help the investor to make the decision regarding whether to invest in the

company or not. A sound financial growth pool the investor towards the company.

Conceptual framework and regulatory framework

Regulatory framework : The regulatory framework provides the set of rules and

regulation for treatment of accounting data and values. The framework provides various standard

to measure the performance and provide a fixed set of standard for the valuation of company data

to take the important decisions.

The purpose of regulatory framework is help the company in preparation of financial

statement because they are used by the different users. It strengthens the accountability and

creditability of the organization by using different accounting standard such as IFRS, IAS etc.

Conceptual framework : It is used by the organization to describe the nature and

objective of financial statement and accounting and set the limit of accounting to present the

information accurately and correctly (What is Conceptual Framework?, 2019). It explains the

fundamental principles and interrelated objectives.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The purpose of conceptual framework is to use the accounting standard and GAAP

(General accepted accounting principle) to attain the organization objective and goal. Company

use the accounting principles to solve the major issues in the organization. It helps the

accountancy firm to prepare the accounts for audit and suggest them for valuable improvement.

Qualitative characteristics

Fundamental qualitative characteristics

Relevance : It refers to provide the relevant information to the users to minimize the

errors in decision making. The relevant information influence the investor and lenders to invest

in the organization. It also helps to the customer by provide the more accurate and predictive

value. Predictive value help the users to evaluate the past, present and future information.

Faithfulness : The faithfulness of information help the customer to evaluate the data and

make them more reliable on the information. Faithful information present the accurate financial

data in different reports and make them more comparable. The accountancy firm consider

providing faithful information to gain the trust of stakeholders.

Enhancing Qualitative characteristics

Verifiability : verifiability of data can be direct of indirect. Direct verifiability of data

refers to verify the data by direct observation and control them on regular basis. On the other

hand indirect verifiability of refers to evaluate and measure the data by using same methodology.

It helps the organization to provide the accurate data to the users (Otley , 2016).

Comparability : It helps the company to compare the financial statements such as

balance sheet, profit and loss account etc. organization can compare the one year financial data

to the other year financial data and help them to evaluate the financial position of the

organization in respect to other organization in same industry. The evaluation elaborate the

position of company in market.

Understandability : It refers to present the data in more precise form. It helps the user to

understand the meaning of the data and get information from the data for different purpose. It

depends upon the way of presentation and the capability of the users to understand them

properly. The aim of the concept is to present the financial reports in more simple form so the

user can evaluate the real meaning of the information and decide whether to invest in the

company or not.

3

(General accepted accounting principle) to attain the organization objective and goal. Company

use the accounting principles to solve the major issues in the organization. It helps the

accountancy firm to prepare the accounts for audit and suggest them for valuable improvement.

Qualitative characteristics

Fundamental qualitative characteristics

Relevance : It refers to provide the relevant information to the users to minimize the

errors in decision making. The relevant information influence the investor and lenders to invest

in the organization. It also helps to the customer by provide the more accurate and predictive

value. Predictive value help the users to evaluate the past, present and future information.

Faithfulness : The faithfulness of information help the customer to evaluate the data and

make them more reliable on the information. Faithful information present the accurate financial

data in different reports and make them more comparable. The accountancy firm consider

providing faithful information to gain the trust of stakeholders.

Enhancing Qualitative characteristics

Verifiability : verifiability of data can be direct of indirect. Direct verifiability of data

refers to verify the data by direct observation and control them on regular basis. On the other

hand indirect verifiability of refers to evaluate and measure the data by using same methodology.

It helps the organization to provide the accurate data to the users (Otley , 2016).

Comparability : It helps the company to compare the financial statements such as

balance sheet, profit and loss account etc. organization can compare the one year financial data

to the other year financial data and help them to evaluate the financial position of the

organization in respect to other organization in same industry. The evaluation elaborate the

position of company in market.

Understandability : It refers to present the data in more precise form. It helps the user to

understand the meaning of the data and get information from the data for different purpose. It

depends upon the way of presentation and the capability of the users to understand them

properly. The aim of the concept is to present the financial reports in more simple form so the

user can evaluate the real meaning of the information and decide whether to invest in the

company or not.

3

Reliability : Reliability refers to present the data in more accurate way by using the

various accounting standard such as GAAP, IFRS and IAS. The accounting principle and

standard make the data more reliable and help the users to take the useful decisions. The

reliability if the data and information attract the customer and investor.

Different stakeholders in the company

Internal stakeholder

Manager : Manager use the financial information to prepare the financial statements

such as balance sheet, income statements, cash flow etc. to evaluate the data and present them in

more precise and understandable form (Schaltegger, and Burritt, ., 2017). The presentation of

data help the user to comes on the conclusion of investment, purchase of material etc. Further

they require the financial information to evaluate the data and make the decisions to improve the

productivity and profitability of the company.

Employees : Employees have mush interest in the financial position of the company.

They are responsible and accountable for the organisation performance and productivity. They

require the financial information to regulate the performance of the company on different

interval. The different report such as balance sheet, cash budget and capital budget help them to

evaluate the revenue and profit of the company.

External users/stakeholders

Lender : Lender provide finance to the company on specific interest rate. They are

interested in the financial information of the company to evaluate the credit worthiness and

reliability of the company data (Quattrone,, 2016). The good financial position and growth of the

organization pool the lenders toward the company to lend money for improving the performance

and productivity.

Customer : customer are the most influencing stakeholders in the organization. They

influence the manager to minimize the price of the goods and services and provide the qualified

good on reasonable price. Customer are interested in the financial information to evaluate

financial position and make the decision of purchase of goods and services.

Government : Government are more interested in the financial information of the

organization to evaluate the profit and revenue of the company to check the ability of company

to pay the taxes and duties on the goods and services. Government requires the financial

4

various accounting standard such as GAAP, IFRS and IAS. The accounting principle and

standard make the data more reliable and help the users to take the useful decisions. The

reliability if the data and information attract the customer and investor.

Different stakeholders in the company

Internal stakeholder

Manager : Manager use the financial information to prepare the financial statements

such as balance sheet, income statements, cash flow etc. to evaluate the data and present them in

more precise and understandable form (Schaltegger, and Burritt, ., 2017). The presentation of

data help the user to comes on the conclusion of investment, purchase of material etc. Further

they require the financial information to evaluate the data and make the decisions to improve the

productivity and profitability of the company.

Employees : Employees have mush interest in the financial position of the company.

They are responsible and accountable for the organisation performance and productivity. They

require the financial information to regulate the performance of the company on different

interval. The different report such as balance sheet, cash budget and capital budget help them to

evaluate the revenue and profit of the company.

External users/stakeholders

Lender : Lender provide finance to the company on specific interest rate. They are

interested in the financial information of the company to evaluate the credit worthiness and

reliability of the company data (Quattrone,, 2016). The good financial position and growth of the

organization pool the lenders toward the company to lend money for improving the performance

and productivity.

Customer : customer are the most influencing stakeholders in the organization. They

influence the manager to minimize the price of the goods and services and provide the qualified

good on reasonable price. Customer are interested in the financial information to evaluate

financial position and make the decision of purchase of goods and services.

Government : Government are more interested in the financial information of the

organization to evaluate the profit and revenue of the company to check the ability of company

to pay the taxes and duties on the goods and services. Government requires the financial

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

information to collect the tax and interest from the different organization and also help them to

run their business by providing subsidies and rebates.

Suppliers : They supply the raw material and information to the company on credit and

cash. They are interested in the financial position and information of the company to regulate the

performance and take the decision of providing goods and services on credit (Öztürk, 2017).

They use the information regarding the sales and profit of the organization to evaluate the

financial position.

P 2 Purpose of financial reporting meeting the organization objective and goals

Financial reporting are used by the company to meet the organization objectives and

growth. The various report such as balance sheet, income statements, cash flow, profit and loss

account, ledger, trail balance and budget report are used for different purpose. They help to gain

the profit of the organization and improve the growth. Balance sheet are prepared to present the

assets and liability and the profitability of the company (Ellwood, and Newberry, 2016). The

creditors and debtor are help to evaluate the financial position in particular accounting period.

Cash flow are prepared to regulate the inflow and outflow of the cash. It helps the company to

present the cash and cash equivalent in balance sheet. The purpose of formulating cash flow is to

provide the information regarding the cash receipts, net change in cash and cash payment.

Preparation of financial statement help the company to find the area of rectification.

Financial report provide a base to evaluate the financial data and information and prepare the

more effective and efficient plan for the growth of the business in the market. It attracts the

customer toward the organization by providing better services. The presentation of financial data

reflect the reliability and profitability of the company.

Balance sheet and income statements are used to present the profit, income, revenue, cash

inflow and outflow, assets and liability of the organization. They use the various qualitative

characteristic to prepare the data which make them more reliable and understandable. It helps t

eh stakeholders to relay on the information and take the valuable decisions to improve the

organization performance, productivity and profitability.

LO 2

P 3 Interpretation of financial information

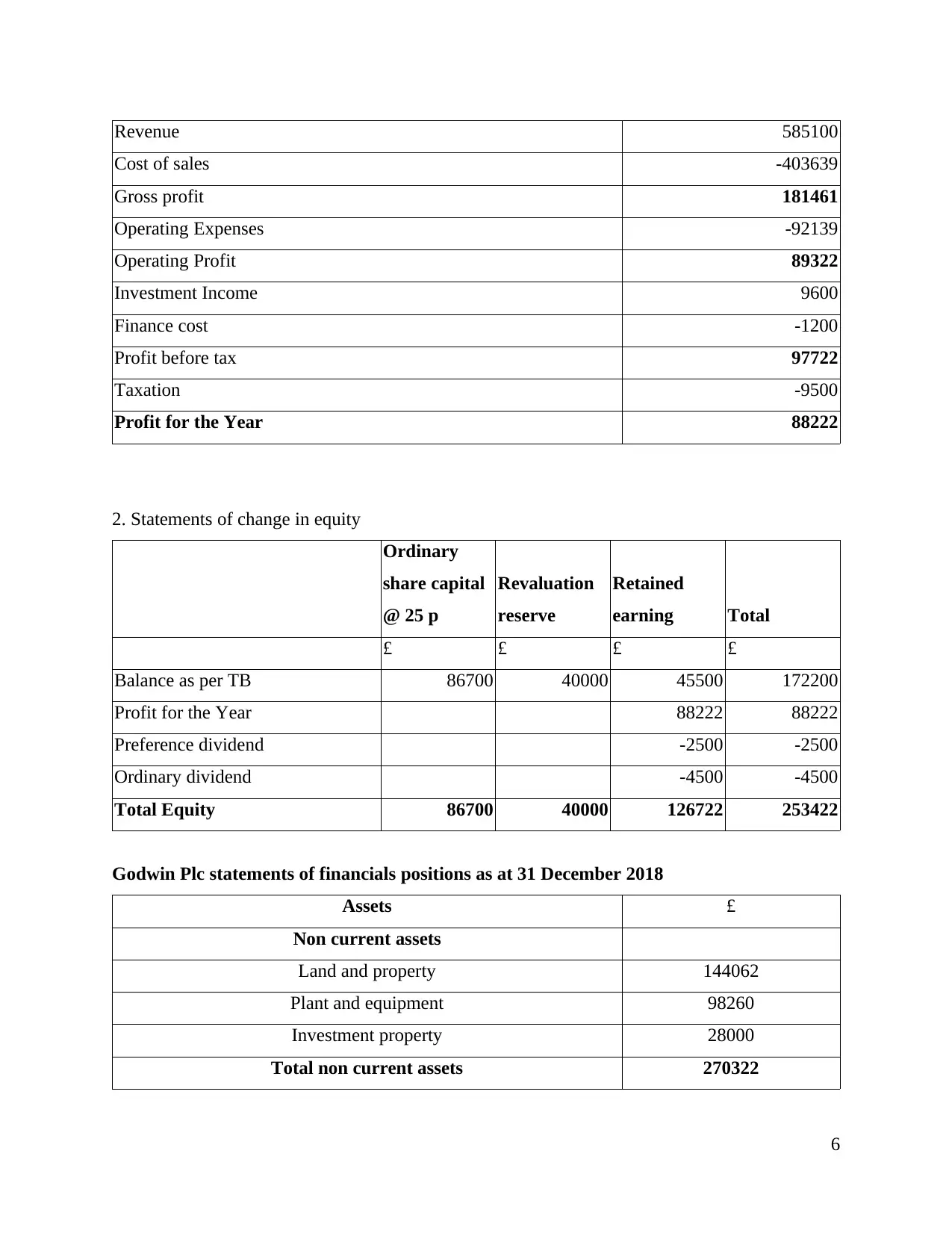

Profit and loss account of Godwin plc company as per 31 December 2018

5

run their business by providing subsidies and rebates.

Suppliers : They supply the raw material and information to the company on credit and

cash. They are interested in the financial position and information of the company to regulate the

performance and take the decision of providing goods and services on credit (Öztürk, 2017).

They use the information regarding the sales and profit of the organization to evaluate the

financial position.

P 2 Purpose of financial reporting meeting the organization objective and goals

Financial reporting are used by the company to meet the organization objectives and

growth. The various report such as balance sheet, income statements, cash flow, profit and loss

account, ledger, trail balance and budget report are used for different purpose. They help to gain

the profit of the organization and improve the growth. Balance sheet are prepared to present the

assets and liability and the profitability of the company (Ellwood, and Newberry, 2016). The

creditors and debtor are help to evaluate the financial position in particular accounting period.

Cash flow are prepared to regulate the inflow and outflow of the cash. It helps the company to

present the cash and cash equivalent in balance sheet. The purpose of formulating cash flow is to

provide the information regarding the cash receipts, net change in cash and cash payment.

Preparation of financial statement help the company to find the area of rectification.

Financial report provide a base to evaluate the financial data and information and prepare the

more effective and efficient plan for the growth of the business in the market. It attracts the

customer toward the organization by providing better services. The presentation of financial data

reflect the reliability and profitability of the company.

Balance sheet and income statements are used to present the profit, income, revenue, cash

inflow and outflow, assets and liability of the organization. They use the various qualitative

characteristic to prepare the data which make them more reliable and understandable. It helps t

eh stakeholders to relay on the information and take the valuable decisions to improve the

organization performance, productivity and profitability.

LO 2

P 3 Interpretation of financial information

Profit and loss account of Godwin plc company as per 31 December 2018

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue 585100

Cost of sales -403639

Gross profit 181461

Operating Expenses -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit before tax 97722

Taxation -9500

Profit for the Year 88222

2. Statements of change in equity

Ordinary

share capital

@ 25 p

Revaluation

reserve

Retained

earning Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the Year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

Godwin Plc statements of financials positions as at 31 December 2018

Assets £

Non current assets

Land and property 144062

Plant and equipment 98260

Investment property 28000

Total non current assets 270322

6

Cost of sales -403639

Gross profit 181461

Operating Expenses -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit before tax 97722

Taxation -9500

Profit for the Year 88222

2. Statements of change in equity

Ordinary

share capital

@ 25 p

Revaluation

reserve

Retained

earning Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the Year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

Godwin Plc statements of financials positions as at 31 December 2018

Assets £

Non current assets

Land and property 144062

Plant and equipment 98260

Investment property 28000

Total non current assets 270322

6

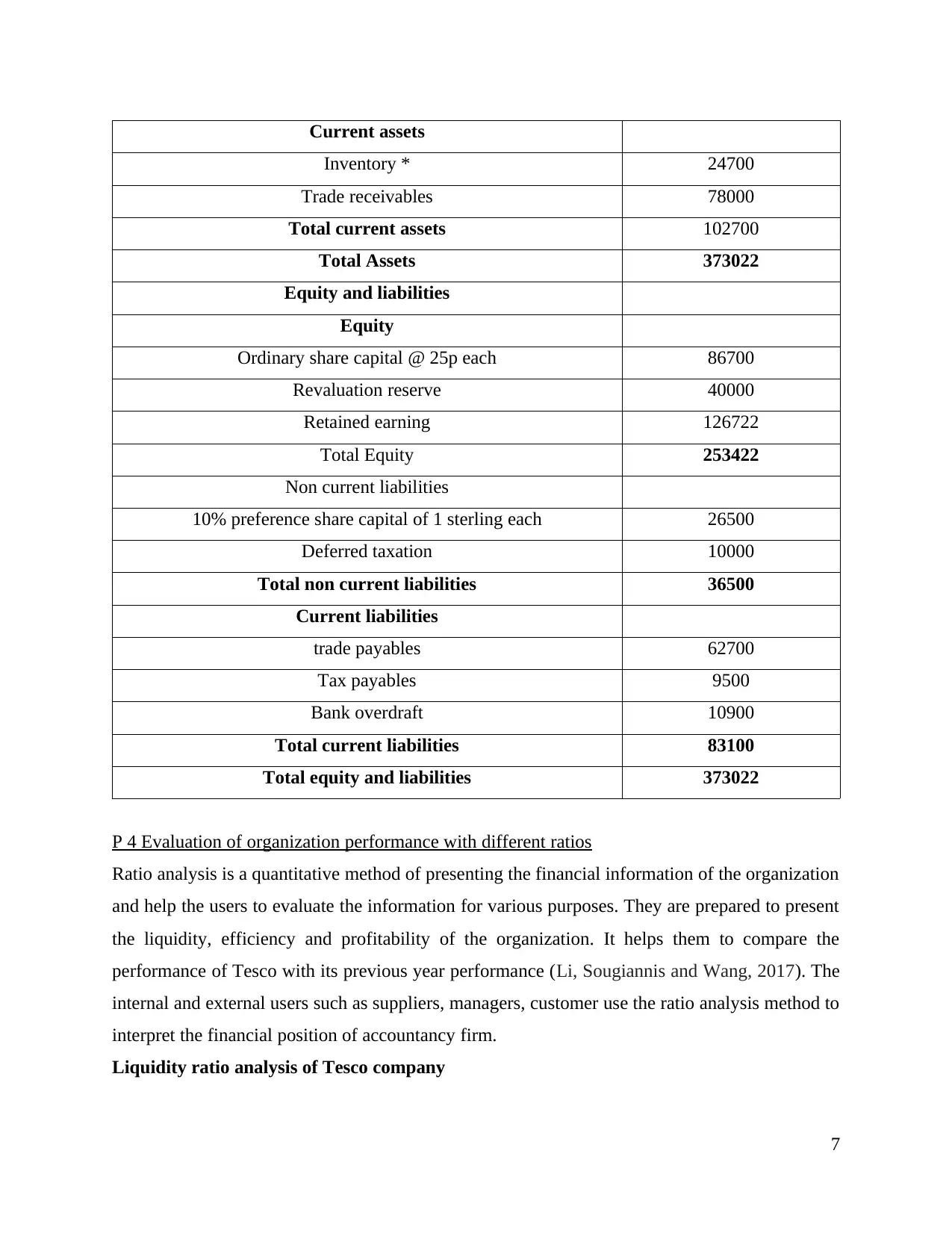

Current assets

Inventory * 24700

Trade receivables 78000

Total current assets 102700

Total Assets 373022

Equity and liabilities

Equity

Ordinary share capital @ 25p each 86700

Revaluation reserve 40000

Retained earning 126722

Total Equity 253422

Non current liabilities

10% preference share capital of 1 sterling each 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities

trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

P 4 Evaluation of organization performance with different ratios

Ratio analysis is a quantitative method of presenting the financial information of the organization

and help the users to evaluate the information for various purposes. They are prepared to present

the liquidity, efficiency and profitability of the organization. It helps them to compare the

performance of Tesco with its previous year performance (Li, Sougiannis and Wang, 2017). The

internal and external users such as suppliers, managers, customer use the ratio analysis method to

interpret the financial position of accountancy firm.

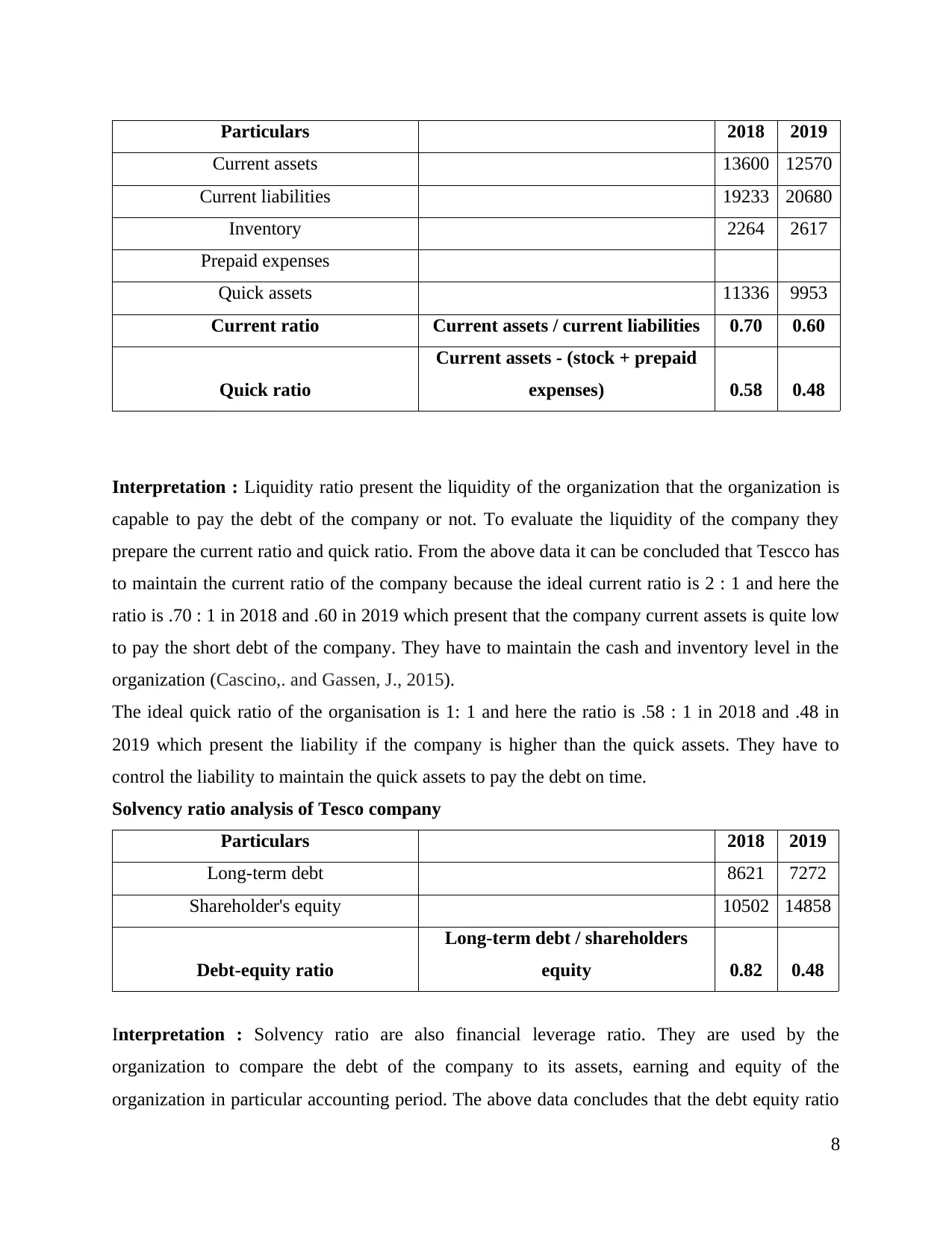

Liquidity ratio analysis of Tesco company

7

Inventory * 24700

Trade receivables 78000

Total current assets 102700

Total Assets 373022

Equity and liabilities

Equity

Ordinary share capital @ 25p each 86700

Revaluation reserve 40000

Retained earning 126722

Total Equity 253422

Non current liabilities

10% preference share capital of 1 sterling each 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities

trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

P 4 Evaluation of organization performance with different ratios

Ratio analysis is a quantitative method of presenting the financial information of the organization

and help the users to evaluate the information for various purposes. They are prepared to present

the liquidity, efficiency and profitability of the organization. It helps them to compare the

performance of Tesco with its previous year performance (Li, Sougiannis and Wang, 2017). The

internal and external users such as suppliers, managers, customer use the ratio analysis method to

interpret the financial position of accountancy firm.

Liquidity ratio analysis of Tesco company

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars 2018 2019

Current assets 13600 12570

Current liabilities 19233 20680

Inventory 2264 2617

Prepaid expenses

Quick assets 11336 9953

Current ratio Current assets / current liabilities 0.70 0.60

Quick ratio

Current assets - (stock + prepaid

expenses) 0.58 0.48

Interpretation : Liquidity ratio present the liquidity of the organization that the organization is

capable to pay the debt of the company or not. To evaluate the liquidity of the company they

prepare the current ratio and quick ratio. From the above data it can be concluded that Tescco has

to maintain the current ratio of the company because the ideal current ratio is 2 : 1 and here the

ratio is .70 : 1 in 2018 and .60 in 2019 which present that the company current assets is quite low

to pay the short debt of the company. They have to maintain the cash and inventory level in the

organization (Cascino,. and Gassen, J., 2015).

The ideal quick ratio of the organisation is 1: 1 and here the ratio is .58 : 1 in 2018 and .48 in

2019 which present the liability if the company is higher than the quick assets. They have to

control the liability to maintain the quick assets to pay the debt on time.

Solvency ratio analysis of Tesco company

Particulars 2018 2019

Long-term debt 8621 7272

Shareholder's equity 10502 14858

Debt-equity ratio

Long-term debt / shareholders

equity 0.82 0.48

Interpretation : Solvency ratio are also financial leverage ratio. They are used by the

organization to compare the debt of the company to its assets, earning and equity of the

organization in particular accounting period. The above data concludes that the debt equity ratio

8

Current assets 13600 12570

Current liabilities 19233 20680

Inventory 2264 2617

Prepaid expenses

Quick assets 11336 9953

Current ratio Current assets / current liabilities 0.70 0.60

Quick ratio

Current assets - (stock + prepaid

expenses) 0.58 0.48

Interpretation : Liquidity ratio present the liquidity of the organization that the organization is

capable to pay the debt of the company or not. To evaluate the liquidity of the company they

prepare the current ratio and quick ratio. From the above data it can be concluded that Tescco has

to maintain the current ratio of the company because the ideal current ratio is 2 : 1 and here the

ratio is .70 : 1 in 2018 and .60 in 2019 which present that the company current assets is quite low

to pay the short debt of the company. They have to maintain the cash and inventory level in the

organization (Cascino,. and Gassen, J., 2015).

The ideal quick ratio of the organisation is 1: 1 and here the ratio is .58 : 1 in 2018 and .48 in

2019 which present the liability if the company is higher than the quick assets. They have to

control the liability to maintain the quick assets to pay the debt on time.

Solvency ratio analysis of Tesco company

Particulars 2018 2019

Long-term debt 8621 7272

Shareholder's equity 10502 14858

Debt-equity ratio

Long-term debt / shareholders

equity 0.82 0.48

Interpretation : Solvency ratio are also financial leverage ratio. They are used by the

organization to compare the debt of the company to its assets, earning and equity of the

organization in particular accounting period. The above data concludes that the debt equity ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of Tesco is .82 : 1 in 2018 and .48 in 2019. Here the equity of the company is greater than the

debt which represent that the company is able to pay the debt and manage the organization

performance and profitability. If the ratio is greater than 20% which means that the financial

position of Tesco is good and ready to meet the goal and objectives of the company.

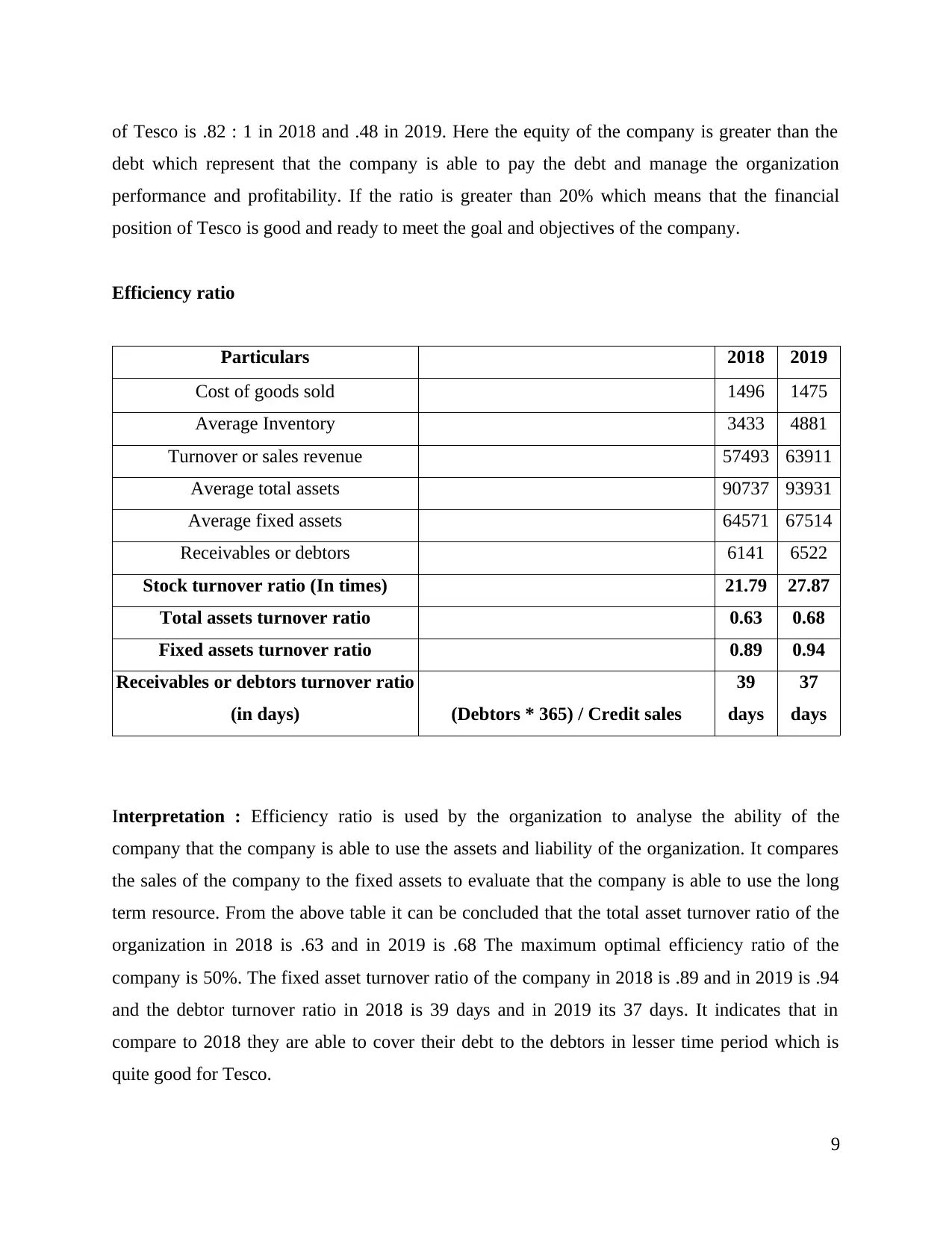

Efficiency ratio

Particulars 2018 2019

Cost of goods sold 1496 1475

Average Inventory 3433 4881

Turnover or sales revenue 57493 63911

Average total assets 90737 93931

Average fixed assets 64571 67514

Receivables or debtors 6141 6522

Stock turnover ratio (In times) 21.79 27.87

Total assets turnover ratio 0.63 0.68

Fixed assets turnover ratio 0.89 0.94

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales

39

days

37

days

Interpretation : Efficiency ratio is used by the organization to analyse the ability of the

company that the company is able to use the assets and liability of the organization. It compares

the sales of the company to the fixed assets to evaluate that the company is able to use the long

term resource. From the above table it can be concluded that the total asset turnover ratio of the

organization in 2018 is .63 and in 2019 is .68 The maximum optimal efficiency ratio of the

company is 50%. The fixed asset turnover ratio of the company in 2018 is .89 and in 2019 is .94

and the debtor turnover ratio in 2018 is 39 days and in 2019 its 37 days. It indicates that in

compare to 2018 they are able to cover their debt to the debtors in lesser time period which is

quite good for Tesco.

9

debt which represent that the company is able to pay the debt and manage the organization

performance and profitability. If the ratio is greater than 20% which means that the financial

position of Tesco is good and ready to meet the goal and objectives of the company.

Efficiency ratio

Particulars 2018 2019

Cost of goods sold 1496 1475

Average Inventory 3433 4881

Turnover or sales revenue 57493 63911

Average total assets 90737 93931

Average fixed assets 64571 67514

Receivables or debtors 6141 6522

Stock turnover ratio (In times) 21.79 27.87

Total assets turnover ratio 0.63 0.68

Fixed assets turnover ratio 0.89 0.94

Receivables or debtors turnover ratio

(in days) (Debtors * 365) / Credit sales

39

days

37

days

Interpretation : Efficiency ratio is used by the organization to analyse the ability of the

company that the company is able to use the assets and liability of the organization. It compares

the sales of the company to the fixed assets to evaluate that the company is able to use the long

term resource. From the above table it can be concluded that the total asset turnover ratio of the

organization in 2018 is .63 and in 2019 is .68 The maximum optimal efficiency ratio of the

company is 50%. The fixed asset turnover ratio of the company in 2018 is .89 and in 2019 is .94

and the debtor turnover ratio in 2018 is 39 days and in 2019 its 37 days. It indicates that in

compare to 2018 they are able to cover their debt to the debtors in lesser time period which is

quite good for Tesco.

9

LO 3

P 5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

International Accounting Standards (IAS):

These standards were first international accounting standards which were issued through

International Accounting Standards Committee made in 1973. The objective was to create it easy

to contrast businesses around the world, enhance transparency and trust in financial reporting and

adoptive international trade and investment (Flower, 2018).

International Financial Reporting Standards (IFRS):

These standards are setting up common rules, so that financial arguments can be

conformable around the world. IFRS are issued by International Accounting Standards Board in

which they clear ways of maintaining and reporting the accounts by firms. These standards are

setting up to make common accounting communication, so that companies and their financial

statements can be consistent and reliable from firm to firm and nation to nation.

Benefits of IAS Benefits of IFRS

It is beneficial for improving the international

investment in terms of review financial

documents from international firms.

It is good for increasing the larger

comparability in terms of determines the

investment by investors.

These standards serve ethics compliances

which involves standard of behaviour, code of

accounting to the firm (Al-Sartawi, Alrawahi

and Sanad, 2016).

This can provide freedom to follow IFRS to

specific condition that leads to more easily read

and helpful statement.

These standards set generalized standards

which are applicable and helpful to different

territorial circumstances and practice.

It will be decrease time, contribution and

expenditure of making many reports (Acharya

and Ryan, 2016).

IAS also modify accounting for multinational

corporation which have facilitated and

It will aid to contour the system through

10

P 5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

International Accounting Standards (IAS):

These standards were first international accounting standards which were issued through

International Accounting Standards Committee made in 1973. The objective was to create it easy

to contrast businesses around the world, enhance transparency and trust in financial reporting and

adoptive international trade and investment (Flower, 2018).

International Financial Reporting Standards (IFRS):

These standards are setting up common rules, so that financial arguments can be

conformable around the world. IFRS are issued by International Accounting Standards Board in

which they clear ways of maintaining and reporting the accounts by firms. These standards are

setting up to make common accounting communication, so that companies and their financial

statements can be consistent and reliable from firm to firm and nation to nation.

Benefits of IAS Benefits of IFRS

It is beneficial for improving the international

investment in terms of review financial

documents from international firms.

It is good for increasing the larger

comparability in terms of determines the

investment by investors.

These standards serve ethics compliances

which involves standard of behaviour, code of

accounting to the firm (Al-Sartawi, Alrawahi

and Sanad, 2016).

This can provide freedom to follow IFRS to

specific condition that leads to more easily read

and helpful statement.

These standards set generalized standards

which are applicable and helpful to different

territorial circumstances and practice.

It will be decrease time, contribution and

expenditure of making many reports (Acharya

and Ryan, 2016).

IAS also modify accounting for multinational

corporation which have facilitated and

It will aid to contour the system through

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.