ACC00145 Financial Reporting and Analysis Report - Semester 2

VerifiedAdded on 2023/06/10

|13

|2189

|265

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on the application of Australian Accounting Standards (AASB) within the context of General Purpose Financial Reports (GPFR). The report begins by examining the role of social accountability within the AASB conceptual framework, followed by a discussion on the development and establishment of AASBs for business practices in Australia. The core of the report involves an in-depth examination of the annual report of Coca-Cola Amatil, extracting key information and highlighting the company's compliance with AAS and IFRS. The report also details the disclosure requirements for executive remuneration, including the components and conditions of such remuneration. Finally, the report considers the reactions of investors to the information disclosed in annual reports, drawing conclusions about the impact of financial reporting on investment decisions. The report utilizes the provided annual report data to provide a real-world example of financial reporting analysis.

Running head: FINANCIAL REPORTING AND ANALYSIS

Financial reporting and analysis

Name of the student

Name of the university

Student ID

Author note

Financial reporting and analysis

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING AND ANALYSIS

Executive summary

The main objective of the report is to comment on the statement that whether social

accountability will be considered as part of the objective of GPFR. The report will further

focus on the importance of developing and establishing the AASBs for the business practices

carried in Australia. The report will take into consideration the annual report of Coca Cola

Amatil and will highlight the information provided by the company in its annual report.

Moreover the report will explain the disclosure requirement for manager’s benefit. Finally,

the report will focus on the reaction of investors regarding the information disclosed in

annual report.

Executive summary

The main objective of the report is to comment on the statement that whether social

accountability will be considered as part of the objective of GPFR. The report will further

focus on the importance of developing and establishing the AASBs for the business practices

carried in Australia. The report will take into consideration the annual report of Coca Cola

Amatil and will highlight the information provided by the company in its annual report.

Moreover the report will explain the disclosure requirement for manager’s benefit. Finally,

the report will focus on the reaction of investors regarding the information disclosed in

annual report.

2FINANCIAL REPORTING AND ANALYSIS

Table of Contents

Body of contents........................................................................................................................3

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................6

Answer 5....................................................................................................................................8

Reference....................................................................................................................................9

Appendix..................................................................................................................................11

Table of Contents

Body of contents........................................................................................................................3

Answer 1....................................................................................................................................3

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................5

Answer 4....................................................................................................................................6

Answer 5....................................................................................................................................8

Reference....................................................................................................................................9

Appendix..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING AND ANALYSIS

Body of contents

Answer 1

“Social accountability is considered in the (AASB Conceptual) Framework as part

of the objectives of general purpose financial reports (GPFR)” – comments

Accountability is considered as the imprecise notion. Hence, it it is recognised as

separate objective, it may open up the GPFR (general purpose financial reports) to deliver all

types of information like reporting for social responsibility unintentionally like reporting for

social responsibility (Luke 2017). While it is acknowledged by AASB regarding the

interrelations among scope and objectives, intended scope for GPFR shall be addressed

directly and not defining the term inadvertently through articulating the objectives

(Aasb.gov.au 2018). Based on this AASB suggests that the conceptual framework as part of

GPFR objectives shall –

Explain the decision of the users regarding the allocation of the scarce resources that

includes the decision for influencing the decision making by the management of

reporting company. The decision further includes the management’s decision

regarding the company’s scarce resource allocation basis through lobbying or voting

(Yong, Lim and Tan 2016).

Unambiguously includes the accountability for the objectives of decision making

through defining the term accountability as responsibility for proving the information

that will enable the users in making informed judgements. The judgements are made

with regard to the company’s performance, its financial position and the compliance

with the objective of evaluating and making the decisions regarding scarce resources

allocation. These will further include the judgements regarding whether the

Body of contents

Answer 1

“Social accountability is considered in the (AASB Conceptual) Framework as part

of the objectives of general purpose financial reports (GPFR)” – comments

Accountability is considered as the imprecise notion. Hence, it it is recognised as

separate objective, it may open up the GPFR (general purpose financial reports) to deliver all

types of information like reporting for social responsibility unintentionally like reporting for

social responsibility (Luke 2017). While it is acknowledged by AASB regarding the

interrelations among scope and objectives, intended scope for GPFR shall be addressed

directly and not defining the term inadvertently through articulating the objectives

(Aasb.gov.au 2018). Based on this AASB suggests that the conceptual framework as part of

GPFR objectives shall –

Explain the decision of the users regarding the allocation of the scarce resources that

includes the decision for influencing the decision making by the management of

reporting company. The decision further includes the management’s decision

regarding the company’s scarce resource allocation basis through lobbying or voting

(Yong, Lim and Tan 2016).

Unambiguously includes the accountability for the objectives of decision making

through defining the term accountability as responsibility for proving the information

that will enable the users in making informed judgements. The judgements are made

with regard to the company’s performance, its financial position and the compliance

with the objective of evaluating and making the decisions regarding scarce resources

allocation. These will further include the judgements regarding whether the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING AND ANALYSIS

management of the company has made effective and efficient use of company’s

resources (Barth 2013).

Therefore, it can be stated that social accountability is taken into consideration under

the AASB conceptual framework as an important part of GPFR.

Answer 2

Requirement for establishing and developing AASBs for the business practices in Australia

Accounting standard those are used by the business entities in Australia for preparing

and presenting their financial reports as per the Corporation law those are commonly referred

as AASBs are prepared by AASB. Development of AASB in Australia is multi-step

procedure that includes the process of public consultation and supplementary discussions,

wherever appropriate. Australia has differential disclosure requirement under which

requirement for financial reporting are set on the basis of type of the company, specifically

based on public interest level in the company. Companies are classified as –

Disclosing entities that mainly includes listed organizations and registered managed

undertakings. These companies have issued the share or have listed and other

securities owing to prospectus circulation (Luke 2016).

Large proprietary and unlisted public companies those have at least 2 criteria among 3

– (i) gross operating revenue amounting to $ 10 million or more (ii) gross assets

amounting to $ 5 million or more (iii) employee number 50 or more.

Small proprietary entities

However, as per AASB all the above mentioned companies are required to maintain

the records that record their accounting and financial transactions accurately. It shall further

enable preparing the financial reports and auditing of these financial reports. Further, all the

management of the company has made effective and efficient use of company’s

resources (Barth 2013).

Therefore, it can be stated that social accountability is taken into consideration under

the AASB conceptual framework as an important part of GPFR.

Answer 2

Requirement for establishing and developing AASBs for the business practices in Australia

Accounting standard those are used by the business entities in Australia for preparing

and presenting their financial reports as per the Corporation law those are commonly referred

as AASBs are prepared by AASB. Development of AASB in Australia is multi-step

procedure that includes the process of public consultation and supplementary discussions,

wherever appropriate. Australia has differential disclosure requirement under which

requirement for financial reporting are set on the basis of type of the company, specifically

based on public interest level in the company. Companies are classified as –

Disclosing entities that mainly includes listed organizations and registered managed

undertakings. These companies have issued the share or have listed and other

securities owing to prospectus circulation (Luke 2016).

Large proprietary and unlisted public companies those have at least 2 criteria among 3

– (i) gross operating revenue amounting to $ 10 million or more (ii) gross assets

amounting to $ 5 million or more (iii) employee number 50 or more.

Small proprietary entities

However, as per AASB all the above mentioned companies are required to maintain

the records that record their accounting and financial transactions accurately. It shall further

enable preparing the financial reports and auditing of these financial reports. Further, all the

5FINANCIAL REPORTING AND ANALYSIS

entities except the small proprietary entities shall prepare the financial statement on annual

basis. These financial reports include profit and loss statement, balance sheet and Cash flow

statement. Matters those are needed to be disclosed under financial reports are stated in the

accounting standards that are issued by the AASBs. Further it has force of law as per the

corporation law. Corporation law further stated that the consolidated financial report shall be

prepared where preparation of these statements are required by the by accounting standard.

Financial statements prepared annually shall be circulated to the members of company and

shall be lodged with ASIC (Australian securities and investment commission). Apart from

meeting the requirements for annual disclosures, the disclosing companies shall prepare

financial statement on half-yearly basis. This half-yearly statement is the abridged version of

the financial statements prepared annually. It shall be lodged with the ASIC but is not

required to be distributed to the members (Palmer 2013).

Therefore, for Australian business practices it is necessary to develop and establish

the AASBs to provide transparency, removing true and fair override and enhancing the

disclosure requirement.

Answer 3

Information given in annual report of Coca – Cola Amatil

Major information provided in the annual report of Coca Cola Amatil for the year

ended 2017 are as follows –

Remuneration report

Director’s report

Corporate governance

Financial and operating review

entities except the small proprietary entities shall prepare the financial statement on annual

basis. These financial reports include profit and loss statement, balance sheet and Cash flow

statement. Matters those are needed to be disclosed under financial reports are stated in the

accounting standards that are issued by the AASBs. Further it has force of law as per the

corporation law. Corporation law further stated that the consolidated financial report shall be

prepared where preparation of these statements are required by the by accounting standard.

Financial statements prepared annually shall be circulated to the members of company and

shall be lodged with ASIC (Australian securities and investment commission). Apart from

meeting the requirements for annual disclosures, the disclosing companies shall prepare

financial statement on half-yearly basis. This half-yearly statement is the abridged version of

the financial statements prepared annually. It shall be lodged with the ASIC but is not

required to be distributed to the members (Palmer 2013).

Therefore, for Australian business practices it is necessary to develop and establish

the AASBs to provide transparency, removing true and fair override and enhancing the

disclosure requirement.

Answer 3

Information given in annual report of Coca – Cola Amatil

Major information provided in the annual report of Coca Cola Amatil for the year

ended 2017 are as follows –

Remuneration report

Director’s report

Corporate governance

Financial and operating review

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING AND ANALYSIS

Shareholder information

5 year financial summary

Independence auditor’s report

Financial reports including consolidated income statements, consolidated

comprehensive income statement, consolidated statement for changes in the equity,

consolidated balance sheet and consolidated statement for cash flows

Notes to the financial statements (Ccamatil.com 2018).

Further it has been stated in the company’s annual report that the general purpose

financial report of the company has been prepared in compliance with the AAS (Australian

accounting standards) and various other authoritative pronouncements of AASB and

Corporation Act 2001. The financial reports of the company further complied with the IFRS

issued by IASB.

Answer 4

With regard to each specified executive and specified director below mentioned

details shall be disclosed –

Total amount of remuneration covering the reporting period. Remuneration includes

bonuses, salaries, fees, expenses allowance, personal benefits, perquisites, post

employment benefits and equity investment. However, it excludes the reimbursement

with regard to the expenses incurred for entity’s benefit or the benefit of its

subsidiary. The remuneration shall be measured as per the requirement of AASB 1028

on employee benefits. However, if the standard does not prescribe any requirement

for measurement for any particular amount of remuneration, it shall be measured

depending on the cost to the company for providing the item (Pwc.com.au 2018).

Shareholder information

5 year financial summary

Independence auditor’s report

Financial reports including consolidated income statements, consolidated

comprehensive income statement, consolidated statement for changes in the equity,

consolidated balance sheet and consolidated statement for cash flows

Notes to the financial statements (Ccamatil.com 2018).

Further it has been stated in the company’s annual report that the general purpose

financial report of the company has been prepared in compliance with the AAS (Australian

accounting standards) and various other authoritative pronouncements of AASB and

Corporation Act 2001. The financial reports of the company further complied with the IFRS

issued by IASB.

Answer 4

With regard to each specified executive and specified director below mentioned

details shall be disclosed –

Total amount of remuneration covering the reporting period. Remuneration includes

bonuses, salaries, fees, expenses allowance, personal benefits, perquisites, post

employment benefits and equity investment. However, it excludes the reimbursement

with regard to the expenses incurred for entity’s benefit or the benefit of its

subsidiary. The remuneration shall be measured as per the requirement of AASB 1028

on employee benefits. However, if the standard does not prescribe any requirement

for measurement for any particular amount of remuneration, it shall be measured

depending on the cost to the company for providing the item (Pwc.com.au 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING AND ANALYSIS

Aggregate for total remuneration of individual and aggregate for each component

shall be disclosed for each of following groups –

Specifies executives

Specified directors

Disclosure of the comparative amounts for previous reporting period is not necessary

for the individuals who were not been specified in that period. Disclosing the

comparative amounts for that period is necessary for each category of entire

remuneration and aggregate of the components.

It is not required to separate the disclosure for remuneration of specified executives

into economic entity and parent entity on the basis of which the entity employs its

employees.

Below mentioned details with regard to the remuneration shall be disclosed for

specified executive and specified directors –

Principle used for determining the amount and nature of remuneration

Whether and how relationship principle established among the remuneration and the

company’s performance

For each service contract among specified executive or specified executives and

disclosing entity explanations those are required for providing the understanding

regarding how remuneration amount in current period of reporting was determined. It

further determines the way in which the contract terms impacted the remuneration for

future period (Pwc.com.au 2018).

For each of the grant of cash bonus, share based compensation benefit payment or

bonus related to performance, conditions and terms for each grant that has an impact

on the remuneration in current or future accounting period. it includes – (i) date of

grant (ii) nature of granted remuneration (iii) Performance and service criteria used

Aggregate for total remuneration of individual and aggregate for each component

shall be disclosed for each of following groups –

Specifies executives

Specified directors

Disclosure of the comparative amounts for previous reporting period is not necessary

for the individuals who were not been specified in that period. Disclosing the

comparative amounts for that period is necessary for each category of entire

remuneration and aggregate of the components.

It is not required to separate the disclosure for remuneration of specified executives

into economic entity and parent entity on the basis of which the entity employs its

employees.

Below mentioned details with regard to the remuneration shall be disclosed for

specified executive and specified directors –

Principle used for determining the amount and nature of remuneration

Whether and how relationship principle established among the remuneration and the

company’s performance

For each service contract among specified executive or specified executives and

disclosing entity explanations those are required for providing the understanding

regarding how remuneration amount in current period of reporting was determined. It

further determines the way in which the contract terms impacted the remuneration for

future period (Pwc.com.au 2018).

For each of the grant of cash bonus, share based compensation benefit payment or

bonus related to performance, conditions and terms for each grant that has an impact

on the remuneration in current or future accounting period. it includes – (i) date of

grant (ii) nature of granted remuneration (iii) Performance and service criteria used

8FINANCIAL REPORTING AND ANALYSIS

for determining the remuneration amount (iv) in case of any alteration of conditions

and terms of grant since the date of grant, the date, effect and details of each of the

alteration.

Further the additional conditions and terms required to be disclosed are – (i) whether

approval from the shareholder required (ii) whether any other benefits are payable

during performance period on annual basis or at the end of the grant period (iii)

restrictions, if any on transfer of the equity instrument after the vesting (Mazhambe

2014).

Answer 5

Reaction of investors on annual report disclosures

Financial statement is considered as the financial information with regard to the

financial performance and position of the company. Based on the financial information the

investors take various decisions regarding the profitability, liquidity and leverage position of

the company. For instance, it can be found from the annual report of Coca Cola Amatil for

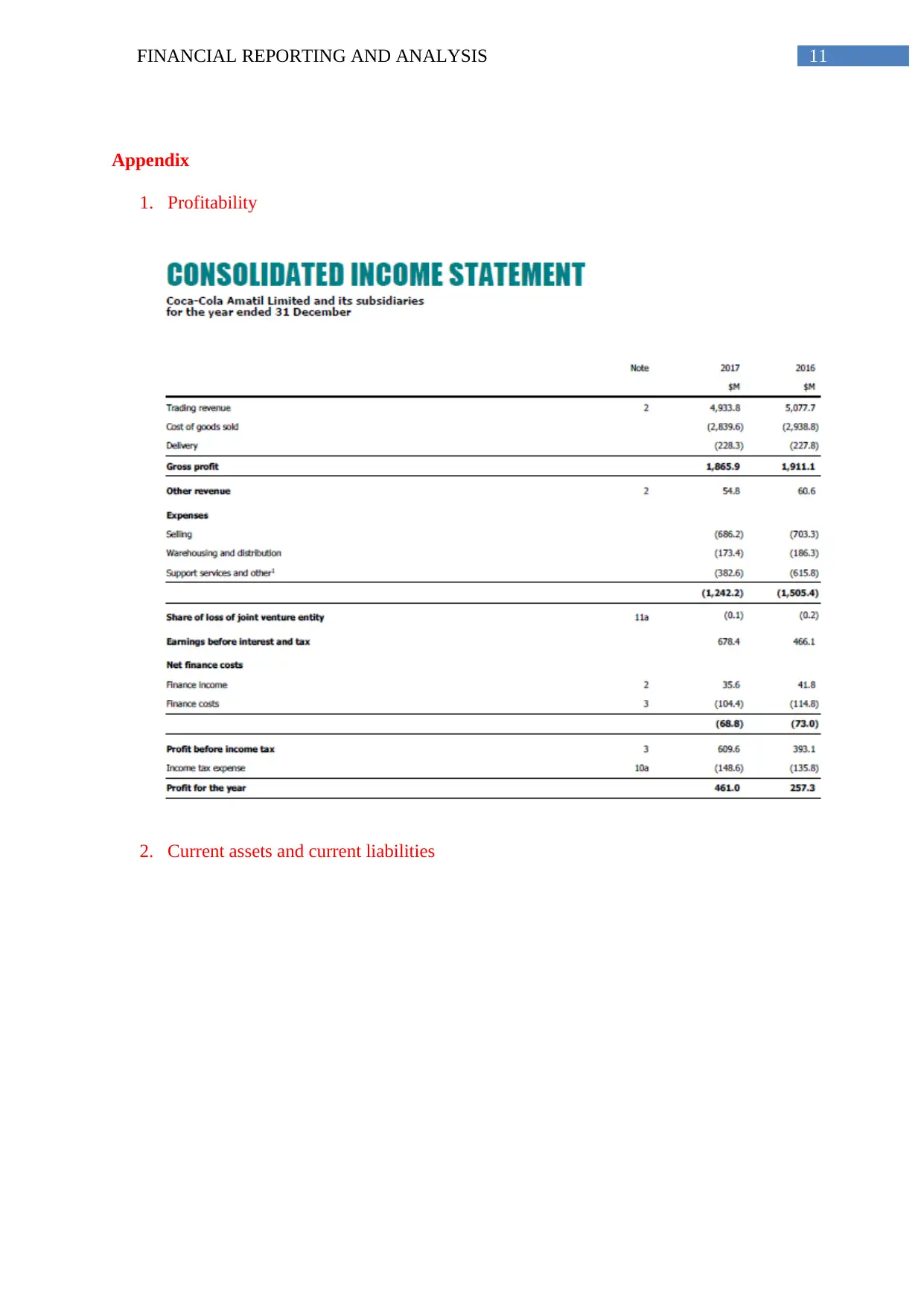

the year ended 2017 that the net profit of the company has been increased to $ 461 million as

compared to $ 257.3 million in 2016 (Appendix 1). It is indicating that the profitability

position of the company has been improved (Newberry 2015). Looking into the balance

sheet of the company for the same period it is found that amount of total current liabilities are

$ 2799.6 million whereas the amount of current liabilities was $ 1838.8 million (Appendix 2).

Therefore, the short term assets of the company are sufficient to pay off the short term

obligation of the company. It is indicating that the liquidity position of the company strong

(Ccamatil.com 2018). Therefore, it can be decided that the company is good in investment

aspect. Hence, it can be stated that investors or the securities market react on disclosure of the

information provided in annual report.

for determining the remuneration amount (iv) in case of any alteration of conditions

and terms of grant since the date of grant, the date, effect and details of each of the

alteration.

Further the additional conditions and terms required to be disclosed are – (i) whether

approval from the shareholder required (ii) whether any other benefits are payable

during performance period on annual basis or at the end of the grant period (iii)

restrictions, if any on transfer of the equity instrument after the vesting (Mazhambe

2014).

Answer 5

Reaction of investors on annual report disclosures

Financial statement is considered as the financial information with regard to the

financial performance and position of the company. Based on the financial information the

investors take various decisions regarding the profitability, liquidity and leverage position of

the company. For instance, it can be found from the annual report of Coca Cola Amatil for

the year ended 2017 that the net profit of the company has been increased to $ 461 million as

compared to $ 257.3 million in 2016 (Appendix 1). It is indicating that the profitability

position of the company has been improved (Newberry 2015). Looking into the balance

sheet of the company for the same period it is found that amount of total current liabilities are

$ 2799.6 million whereas the amount of current liabilities was $ 1838.8 million (Appendix 2).

Therefore, the short term assets of the company are sufficient to pay off the short term

obligation of the company. It is indicating that the liquidity position of the company strong

(Ccamatil.com 2018). Therefore, it can be decided that the company is good in investment

aspect. Hence, it can be stated that investors or the securities market react on disclosure of the

information provided in annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING AND ANALYSIS

Reference

Aasb.gov.au. (2018). [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB1046_01-04.pdf [Accessed 20 Sep.

2018].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Ccamatil.com. (2018). [online] Available at:

https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2018/Annual-

Report-2017.ashx [Accessed 20 Sep. 2018].

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives

to a useful reporting framework for social enterprises. Social and Environmental

Accountability Journal, 36(2), pp.103-123.

Luke, B., 2017. Statement of social performance: Opportunities and barriers to

adoption. Social and Environmental Accountability Journal, 37(2), pp.118-136.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Palmer, P.D., 2013. Exploring attitudes to financial reporting in the Australian not‐for‐profit

sector. Accounting & Finance, 53(1), pp.217-241.

Reference

Aasb.gov.au. (2018). [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/AASB1046_01-04.pdf [Accessed 20 Sep.

2018].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Ccamatil.com. (2018). [online] Available at:

https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2018/Annual-

Report-2017.ashx [Accessed 20 Sep. 2018].

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives

to a useful reporting framework for social enterprises. Social and Environmental

Accountability Journal, 36(2), pp.103-123.

Luke, B., 2017. Statement of social performance: Opportunities and barriers to

adoption. Social and Environmental Accountability Journal, 37(2), pp.118-136.

Mazhambe, Z., 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework: Discussion Paper (DP/2013/1). Journal of Modern Accounting

and Auditing, 10(8).

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

Palmer, P.D., 2013. Exploring attitudes to financial reporting in the Australian not‐for‐profit

sector. Accounting & Finance, 53(1), pp.217-241.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING AND ANALYSIS

Pwc.com.au. (2018). [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/kmp-remuneration-disclosures-apr14.pdf

[Accessed 20 Sep. 2018].

Yong, K.O., Lim, C.Y. and Tan, P., 2016. Theory and practice of the proposed conceptual

framework: Evidence from the field. Advances in accounting, 35, pp.62-74.

Pwc.com.au. (2018). [online] Available at:

https://www.pwc.com.au/assurance/ifrs/assets/kmp-remuneration-disclosures-apr14.pdf

[Accessed 20 Sep. 2018].

Yong, K.O., Lim, C.Y. and Tan, P., 2016. Theory and practice of the proposed conceptual

framework: Evidence from the field. Advances in accounting, 35, pp.62-74.

11FINANCIAL REPORTING AND ANALYSIS

Appendix

1. Profitability

2. Current assets and current liabilities

Appendix

1. Profitability

2. Current assets and current liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.