Financial Accounting and Reporting: Revaluation and Shareholders

VerifiedAdded on 2020/03/23

|8

|2332

|112

Report

AI Summary

This report delves into the intricacies of financial accounting and reporting, focusing on the critical aspect of asset revaluation. It explores the motivations behind directors' decisions regarding non-revaluation of equipment, plant, and property, examining the potential impacts on financial statements. The report further investigates the adverse consequences of non-revaluation on shareholder wealth, emphasizing the importance of fair value representation. An in-depth analysis of Amcor Limited's approach to equipment, property, and plant valuation is provided, referencing relevant accounting standards like AASB and IFRS. The report highlights the significance of revaluation in presenting a true and fair view of a company's financial position, offering valuable insights for students and professionals alike. The report also emphasizes the importance of accurate asset valuation for informed decision-making by investors and stakeholders, underscoring the potential for misguidance when assets are not revalued to reflect market values.

Running head: FINANCIAL ACCOUNTING AND REPORTING

Financial accounting and reporting

Name of the student

Name of the student

Author note

Financial accounting and reporting

Name of the student

Name of the student

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING AND REPORTING

Table of Contents

(a) Director’s motivation behind behind the decision of not revaluating the equipment, plant

and property......................................................................................................................................2

(a) Impact of non-revaluation on the financial statement..........................................................3

(b) Adverse impact of non-revaluation on the wealth of shareholder........................................3

(c) Analysis of equipment, property and plant – Amcor Limited................................................5

References.............................................................................................................................................6

Table of Contents

(a) Director’s motivation behind behind the decision of not revaluating the equipment, plant

and property......................................................................................................................................2

(a) Impact of non-revaluation on the financial statement..........................................................3

(b) Adverse impact of non-revaluation on the wealth of shareholder........................................3

(c) Analysis of equipment, property and plant – Amcor Limited................................................5

References.............................................................................................................................................6

2FINANCIAL ACCOUNTING AND REPORTING

Revaluation of the fixed asset is required for stating the actual value of the capital assets

that are owned by the company. The revaluation is different from providing the depreciation on

assets where the asset value is declined based on the useful life of the asset. The main objective of

revaluation is to reveal the asset in the financial report of the company at the fair value of the

market. This assists the company regarding the decision of whether to invest the fund in any other

business or not. Further, at the time of sell the negotiation for sell is based on the revalued amount

only (Christensen & Nikolaev, 2013).

(a) Director’s motivation behind behind the decision of not revaluating the

equipment, plant and property

Finding out the motivation of the directors behind non-revaluating the assets is a tough job.

One reason may be that the sale of asset under various market conditions may results into lower

amount as compared to the value suggested by revaluation aspect. Further, the directors may be in

the view that for the purpose of accounting, retaining the cost model will be more efficient. If the

assets are not revalued, the value of the assets will be understated in the balance sheet as compared

to the actual values and therefore, the expenses related to depreciation will also be lower that will

lead to higher amount of profits. Further, the profit on sale will also be higher. Therefore, possible

motivation may also be that non-revaluation will lead to higher amount of profits. Further, the lower

base of asset and higher amount of profit will lead to improvement in return to asset ratio of the

company (Goh et al., 2015). Moreover, the reasons behind non-revaluation of assets by the directors

may be as follows –

Simplicity – as per the director’s view it may be more efficient and simple with respect to the

financial measurement to evaluate the asset as per cost model rather than changing the

value of the asset as per regular market change. Further, the calculation of depreciation

under cost model will be simpler as compared to revaluation as there will be no continuous

alterations in the value.

Consistency – as per some directors the cost model is more relevant with respect to reveal

and records the assets in the financial report of the company. The financial report are

important to the directors, partners and executives of the business in the way that it analyse

financial performance of the company and based on the performance, it forecasts the future

growth of the company.

Objectivity – the historical cost of the asset shown under the financial statement can be

verified with the related documents like receipt, voucher, statement and invoice.

Revaluation of the fixed asset is required for stating the actual value of the capital assets

that are owned by the company. The revaluation is different from providing the depreciation on

assets where the asset value is declined based on the useful life of the asset. The main objective of

revaluation is to reveal the asset in the financial report of the company at the fair value of the

market. This assists the company regarding the decision of whether to invest the fund in any other

business or not. Further, at the time of sell the negotiation for sell is based on the revalued amount

only (Christensen & Nikolaev, 2013).

(a) Director’s motivation behind behind the decision of not revaluating the

equipment, plant and property

Finding out the motivation of the directors behind non-revaluating the assets is a tough job.

One reason may be that the sale of asset under various market conditions may results into lower

amount as compared to the value suggested by revaluation aspect. Further, the directors may be in

the view that for the purpose of accounting, retaining the cost model will be more efficient. If the

assets are not revalued, the value of the assets will be understated in the balance sheet as compared

to the actual values and therefore, the expenses related to depreciation will also be lower that will

lead to higher amount of profits. Further, the profit on sale will also be higher. Therefore, possible

motivation may also be that non-revaluation will lead to higher amount of profits. Further, the lower

base of asset and higher amount of profit will lead to improvement in return to asset ratio of the

company (Goh et al., 2015). Moreover, the reasons behind non-revaluation of assets by the directors

may be as follows –

Simplicity – as per the director’s view it may be more efficient and simple with respect to the

financial measurement to evaluate the asset as per cost model rather than changing the

value of the asset as per regular market change. Further, the calculation of depreciation

under cost model will be simpler as compared to revaluation as there will be no continuous

alterations in the value.

Consistency – as per some directors the cost model is more relevant with respect to reveal

and records the assets in the financial report of the company. The financial report are

important to the directors, partners and executives of the business in the way that it analyse

financial performance of the company and based on the performance, it forecasts the future

growth of the company.

Objectivity – the historical cost of the asset shown under the financial statement can be

verified with the related documents like receipt, voucher, statement and invoice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING AND REPORTING

Further, where the directors are required to manipulate the amount of profit and reveal it at

higher amount, the revaluation method sometimes do not allow the company to manipulate the

figures. Due to all these reasons the directors may not be motivated to revalue the amount of

property, equipment and plant (Jack, 2015).

(b) Impact of non-revaluation on the financial statement

The main objective of revaluation method is to present the assets in the financial statement

at the value that is influenced by market condition and valuation. Therefore, the asset that is valued

as per the revaluation method presents the asset more fairly. Further, as the revaluation is involved

more with presenting the true value of the asset and less with the earning capacity, not considering

the revalued figures will misrepresent the statement. Further, under the cost approach the real

value of the asset will not be revealed and the company will not take into consideration the market

value changes of the asset (Liang & Riedl, 2013). Moreover, the actual profit under income

statement will not be revealed as the asset in the balance sheet will be recorded as per the historical

value whereas the sale will be carried out as per the revalued amount ( Small, Yaseen & Schmidt,

2016).

The additional amount or the surplus amount generated from revaluation may be added up

to the value of retained earnings while the asset is derecognized. Further, the difference between

the depreciation amount on historical cost of the asset and the depreciation amount of revalued

amount of asset may charge against the retained earnings during the useful life of the asset. As per

AASB 116, the amount arise from the revaluation may be distributed among the investors. However,

there is no clear indication that whether the surpluses is to be allocate or not but if the company

wants to distribute this profit, it may do that on its own discretion. In the same way, if the company

wants, it may poses restriction on allocation of surplus amount (Hu, Percy & Yao, 2015). To resolve

this issue, as per the accounting standards, the company can shift the difference between the

depreciation amount on historical cost of the asset and the depreciation amount of revalued amount

of asset may charge against the retained earnings for each accounting period during the useful life of

the asset. Therefore, non-revaluation of the asset or recording the asset as per the cost model under

the financial statement will have large impact on the financial statement f any company.

(c) Adverse impact of non-revaluation on the wealth of shareholder

The main reason behind the adoption of valuation for the assets is to assure that the assets

are shown under the financial statement at the market values that is the fair values. Various reasons

are there to revalue the asset. These reasons may be to increase the company’s borrowing capacity,

increasing the company’s growth opportunities, bonus share issue and liquidity maintenance. The

Further, where the directors are required to manipulate the amount of profit and reveal it at

higher amount, the revaluation method sometimes do not allow the company to manipulate the

figures. Due to all these reasons the directors may not be motivated to revalue the amount of

property, equipment and plant (Jack, 2015).

(b) Impact of non-revaluation on the financial statement

The main objective of revaluation method is to present the assets in the financial statement

at the value that is influenced by market condition and valuation. Therefore, the asset that is valued

as per the revaluation method presents the asset more fairly. Further, as the revaluation is involved

more with presenting the true value of the asset and less with the earning capacity, not considering

the revalued figures will misrepresent the statement. Further, under the cost approach the real

value of the asset will not be revealed and the company will not take into consideration the market

value changes of the asset (Liang & Riedl, 2013). Moreover, the actual profit under income

statement will not be revealed as the asset in the balance sheet will be recorded as per the historical

value whereas the sale will be carried out as per the revalued amount ( Small, Yaseen & Schmidt,

2016).

The additional amount or the surplus amount generated from revaluation may be added up

to the value of retained earnings while the asset is derecognized. Further, the difference between

the depreciation amount on historical cost of the asset and the depreciation amount of revalued

amount of asset may charge against the retained earnings during the useful life of the asset. As per

AASB 116, the amount arise from the revaluation may be distributed among the investors. However,

there is no clear indication that whether the surpluses is to be allocate or not but if the company

wants to distribute this profit, it may do that on its own discretion. In the same way, if the company

wants, it may poses restriction on allocation of surplus amount (Hu, Percy & Yao, 2015). To resolve

this issue, as per the accounting standards, the company can shift the difference between the

depreciation amount on historical cost of the asset and the depreciation amount of revalued amount

of asset may charge against the retained earnings for each accounting period during the useful life of

the asset. Therefore, non-revaluation of the asset or recording the asset as per the cost model under

the financial statement will have large impact on the financial statement f any company.

(c) Adverse impact of non-revaluation on the wealth of shareholder

The main reason behind the adoption of valuation for the assets is to assure that the assets

are shown under the financial statement at the market values that is the fair values. Various reasons

are there to revalue the asset. These reasons may be to increase the company’s borrowing capacity,

increasing the company’s growth opportunities, bonus share issue and liquidity maintenance. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING AND REPORTING

stakeholders of the company make important decisions for the investment based on the

performance and the amount of various items in the balance sheet through analysing the company’s

future growth prospect. Therefore, to present the assets with its actual value as per the market

value, it shall be revalued on regular periodic basis otherwise the figures will misguide the investors

as well as the other users of the financial statement (Amcor.com, 2017). Other reasons behind the

revaluation may b expressed as follows –

Appropriate assessment for internal and external reconstruction

It states actual amount of employed capital and return rate

Te company y will be able to analyse the actual amount for bargaining under the acquisition

by any other organization or merger with any other organization

It will assist in assessing the market value of the available asset under sales and leaseback

contracts.

The depreciation is generally provided on the asset to accumulate the fund to replace the

asset after the useful life of the asset gets over. Therefore, if the depreciation is provided on

the historical value of the asset, it may not be sufficient to replace the asset as the

replacement will be on market value of the asset and thereby it will put extra burden on the

shareholder for replacement

If the depreciation is provided at lesser amount, it will lead to higher amount of profit and

thereby higher amount of dividend. This will lead to adverse effect on the shareholders as

the profit will be wrongly stated.

Further, it is implied condition of AASB 136 that the users of the financial statement shall be

assured for true figures of the items included in the statement as various important decisions based

on the financial statement information. Thus, the revalued figure of plant, equipment and property

will show more accurate and appropriate information which in turn will have a significant impact on

the share value of the company. On the contrary, the share value measured on the historical value

will definitely mislead the investors as the true value will not be revealed (Zakaria et al., 2014).

Thus, if the directors decide not to revalue the assets will adversely affect the shareholder’s

wealth as they will invest without knowing the asset’s true value and company’s actual performance.

(d) Analysis of equipment, property and plant – Amcor Limited

Amcor Limited is engaged in providing packaging materials, paper and plastics for metals

and these products are used for bags, plastic tubes, solid fibre containers, wrapping of the papers,

cans and plastic rigid containers.

stakeholders of the company make important decisions for the investment based on the

performance and the amount of various items in the balance sheet through analysing the company’s

future growth prospect. Therefore, to present the assets with its actual value as per the market

value, it shall be revalued on regular periodic basis otherwise the figures will misguide the investors

as well as the other users of the financial statement (Amcor.com, 2017). Other reasons behind the

revaluation may b expressed as follows –

Appropriate assessment for internal and external reconstruction

It states actual amount of employed capital and return rate

Te company y will be able to analyse the actual amount for bargaining under the acquisition

by any other organization or merger with any other organization

It will assist in assessing the market value of the available asset under sales and leaseback

contracts.

The depreciation is generally provided on the asset to accumulate the fund to replace the

asset after the useful life of the asset gets over. Therefore, if the depreciation is provided on

the historical value of the asset, it may not be sufficient to replace the asset as the

replacement will be on market value of the asset and thereby it will put extra burden on the

shareholder for replacement

If the depreciation is provided at lesser amount, it will lead to higher amount of profit and

thereby higher amount of dividend. This will lead to adverse effect on the shareholders as

the profit will be wrongly stated.

Further, it is implied condition of AASB 136 that the users of the financial statement shall be

assured for true figures of the items included in the statement as various important decisions based

on the financial statement information. Thus, the revalued figure of plant, equipment and property

will show more accurate and appropriate information which in turn will have a significant impact on

the share value of the company. On the contrary, the share value measured on the historical value

will definitely mislead the investors as the true value will not be revealed (Zakaria et al., 2014).

Thus, if the directors decide not to revalue the assets will adversely affect the shareholder’s

wealth as they will invest without knowing the asset’s true value and company’s actual performance.

(d) Analysis of equipment, property and plant – Amcor Limited

Amcor Limited is engaged in providing packaging materials, paper and plastics for metals

and these products are used for bags, plastic tubes, solid fibre containers, wrapping of the papers,

cans and plastic rigid containers.

5FINANCIAL ACCOUNTING AND REPORTING

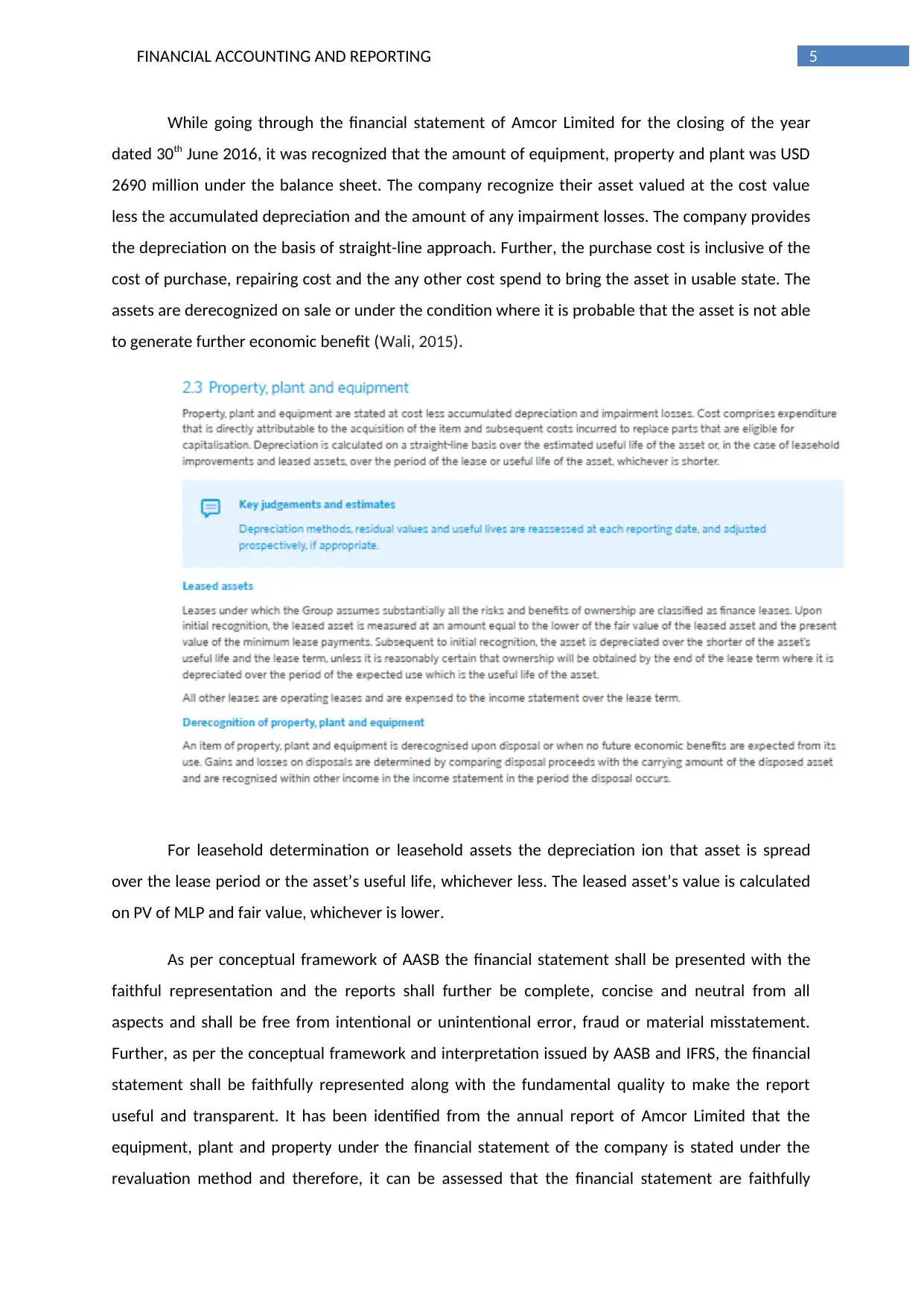

While going through the financial statement of Amcor Limited for the closing of the year

dated 30th June 2016, it was recognized that the amount of equipment, property and plant was USD

2690 million under the balance sheet. The company recognize their asset valued at the cost value

less the accumulated depreciation and the amount of any impairment losses. The company provides

the depreciation on the basis of straight-line approach. Further, the purchase cost is inclusive of the

cost of purchase, repairing cost and the any other cost spend to bring the asset in usable state. The

assets are derecognized on sale or under the condition where it is probable that the asset is not able

to generate further economic benefit (Wali, 2015).

For leasehold determination or leasehold assets the depreciation ion that asset is spread

over the lease period or the asset’s useful life, whichever less. The leased asset’s value is calculated

on PV of MLP and fair value, whichever is lower.

As per conceptual framework of AASB the financial statement shall be presented with the

faithful representation and the reports shall further be complete, concise and neutral from all

aspects and shall be free from intentional or unintentional error, fraud or material misstatement.

Further, as per the conceptual framework and interpretation issued by AASB and IFRS, the financial

statement shall be faithfully represented along with the fundamental quality to make the report

useful and transparent. It has been identified from the annual report of Amcor Limited that the

equipment, plant and property under the financial statement of the company is stated under the

revaluation method and therefore, it can be assessed that the financial statement are faithfully

While going through the financial statement of Amcor Limited for the closing of the year

dated 30th June 2016, it was recognized that the amount of equipment, property and plant was USD

2690 million under the balance sheet. The company recognize their asset valued at the cost value

less the accumulated depreciation and the amount of any impairment losses. The company provides

the depreciation on the basis of straight-line approach. Further, the purchase cost is inclusive of the

cost of purchase, repairing cost and the any other cost spend to bring the asset in usable state. The

assets are derecognized on sale or under the condition where it is probable that the asset is not able

to generate further economic benefit (Wali, 2015).

For leasehold determination or leasehold assets the depreciation ion that asset is spread

over the lease period or the asset’s useful life, whichever less. The leased asset’s value is calculated

on PV of MLP and fair value, whichever is lower.

As per conceptual framework of AASB the financial statement shall be presented with the

faithful representation and the reports shall further be complete, concise and neutral from all

aspects and shall be free from intentional or unintentional error, fraud or material misstatement.

Further, as per the conceptual framework and interpretation issued by AASB and IFRS, the financial

statement shall be faithfully represented along with the fundamental quality to make the report

useful and transparent. It has been identified from the annual report of Amcor Limited that the

equipment, plant and property under the financial statement of the company is stated under the

revaluation method and therefore, it can be assessed that the financial statement are faithfully

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING AND REPORTING

represented. Further, the revaluation approach will reveal the real position of the company y which

in turn will enable the investors, creditors and borrowers to take important decisions. Thus, it can be

stated that the company’s revaluation approach to measure and state the value of equipment,

property and plant in the financial statement of the company, that is for Amcor Limited is

appropriate and can be regarded as per the requirement of AASB and IFRS framework.

represented. Further, the revaluation approach will reveal the real position of the company y which

in turn will enable the investors, creditors and borrowers to take important decisions. Thus, it can be

stated that the company’s revaluation approach to measure and state the value of equipment,

property and plant in the financial statement of the company, that is for Amcor Limited is

appropriate and can be regarded as per the requirement of AASB and IFRS framework.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING AND REPORTING

References

Amcor.com. (2017). Reports. [online] Available at:

http://www.amcor.com/investor-centre/company-performance-news/reports [Accessed 11

Sept. 2017].

Christensen, H. B., & Nikolaev, V. V. (2013). Does fair value accounting for non-financial assets pass

the market test?. Review of Accounting Studies, 18(3), 734-775.

Goh, B. W., Li, D., Ng, J., & Yong, K. O. (2015). Market pricing of banks’ fair value assets reported

under SFAS 157 since the 2008 financial crisis. Journal of Accounting and Public Policy, 34(2),

129-145.

Hu, F., Percy, M., & Yao, D. (2015). Asset revaluations and earnings management: Evidence from

Australian companies. Corporate Ownership and Control, 13(1), 930-939.

Jack, L. (2015). Book Review: Fair value accounting in historical perspective. Accounting

Review, 90(2), 825-828.

Liang, L., & Riedl, E. J. (2013). The effect of fair value versus historical cost reporting model on

analyst forecast accuracy. The Accounting Review, 89(3), 1151-1177.

Small, R., Yaseen, Y., & Schmidt, L. (2016). Amortisation of intangible assets: accounting

technical. Professional Accountant, 2016(28), 16-17.

Wali, S. (2015). Mechanisms of corporate governance and fixed asset revaluation. International

Journal of Accounting and Finance, 5(1), 82-97.

Zakaria, A., Edwards, D. J., Holt, G. D., & Ramachandran, V. (2014). A Review of Property, Plant and

Equipment Asset Revaluation Decision Making in Indonesia: Development of a Conceptual

Model. Mindanao Journal of Science and Technology, 12(1), 1-1.

References

Amcor.com. (2017). Reports. [online] Available at:

http://www.amcor.com/investor-centre/company-performance-news/reports [Accessed 11

Sept. 2017].

Christensen, H. B., & Nikolaev, V. V. (2013). Does fair value accounting for non-financial assets pass

the market test?. Review of Accounting Studies, 18(3), 734-775.

Goh, B. W., Li, D., Ng, J., & Yong, K. O. (2015). Market pricing of banks’ fair value assets reported

under SFAS 157 since the 2008 financial crisis. Journal of Accounting and Public Policy, 34(2),

129-145.

Hu, F., Percy, M., & Yao, D. (2015). Asset revaluations and earnings management: Evidence from

Australian companies. Corporate Ownership and Control, 13(1), 930-939.

Jack, L. (2015). Book Review: Fair value accounting in historical perspective. Accounting

Review, 90(2), 825-828.

Liang, L., & Riedl, E. J. (2013). The effect of fair value versus historical cost reporting model on

analyst forecast accuracy. The Accounting Review, 89(3), 1151-1177.

Small, R., Yaseen, Y., & Schmidt, L. (2016). Amortisation of intangible assets: accounting

technical. Professional Accountant, 2016(28), 16-17.

Wali, S. (2015). Mechanisms of corporate governance and fixed asset revaluation. International

Journal of Accounting and Finance, 5(1), 82-97.

Zakaria, A., Edwards, D. J., Holt, G. D., & Ramachandran, V. (2014). A Review of Property, Plant and

Equipment Asset Revaluation Decision Making in Indonesia: Development of a Conceptual

Model. Mindanao Journal of Science and Technology, 12(1), 1-1.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.