International Financial Reporting: Purpose, Framework, and Analysis

VerifiedAdded on 2020/06/04

|14

|4783

|58

Report

AI Summary

This report provides a comprehensive overview of international financial reporting (IFRS). It begins by outlining the purpose of financial reporting, emphasizing its importance for stakeholders and companies in providing clear financial information for decision-making. The report then delves into the regulatory framework established by the IASB, discussing the characteristics of financial information, such as relevance, materiality, understandability, reliability, and comparability. Various types of stakeholders, including managers, investors, and creditors, are identified and their reliance on financial statements is explained. The report further explores the benefits of financial reporting to the company, the production and interpretation of financial statements, and the differentiation between IAS and IFRS bodies. It also discusses the degrees of compliance with IFRS by organizations and concludes with a summary of the key findings. The report highlights how financial reports are used by investors, lenders, and auditors for decision-making and ensuring financial transparency.

INTERNATIONAL

FINANCIAL REPORTING

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Regulatory framework of financial reporting and characteristics of financial information3

3. Outlining various types of stakeholders in the organisation..............................................5

4. Discussing value of financial reporting to the company....................................................5

5. Producing various financial statements of the organisation...............................................6

6. Interpretation of financial ratios.........................................................................................8

7. Differentiating IAS and IFRS bodies.................................................................................9

8. Outline the benefits of IFRS body......................................................................................9

9. Degrees of compliance of IFRS by the organisations......................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Regulatory framework of financial reporting and characteristics of financial information3

3. Outlining various types of stakeholders in the organisation..............................................5

4. Discussing value of financial reporting to the company....................................................5

5. Producing various financial statements of the organisation...............................................6

6. Interpretation of financial ratios.........................................................................................8

7. Differentiating IAS and IFRS bodies.................................................................................9

8. Outline the benefits of IFRS body......................................................................................9

9. Degrees of compliance of IFRS by the organisations......................................................10

CONCLUSION..............................................................................................................................11

REFERNCES.................................................................................................................................11

INTRODUCTION

International financial reporting is quite helpful for stakeholders as well as company as

proper information is available to them regarding financial viability of the business. The present

report deals with importance of financial reporting to business as well as to users of financial

information. This provides clarity to stakeholders to take effective decisions with much ease. It is

useful for investors, lenders that provide funds to organisation for functioning effectively. As

such, financial information as provided financial reports are useful for them.

TASK 1

1. Purpose of financial reporting

Financial reporting is required to get prepare reports by the organisation. It is required so

that each and every transaction is being recorded perfectly in the books of accounts with much

ease by the company. This is not an simple task as it requires effective accounting professionals

so that transaction is properly recorded in the books of accounts and as such, financial reports

may be prepared and provided to users of financial information. Financial reporting is used for

many purpose and as such it is required that accountants should prepare such reports with full

effectiveness so that proper results about the financial health of the company may be reflected to

users of financial information so that they may take better and effective decisions by relying in

such information (Biddle and et.al, 2016 ).

Financial reports conveys about the business whether it is making profit or loss in the

current period and as such, clarity related to financial health of the organisation may be imparted

to all users in the best possible and productive way. This is used for the purpose for imparting

financial performance of the company to various stakeholders be it internal or external. The

investors uses financial reports so that funds are perfectly utilised by the firm. They keep close

watch towards company as whether it is using funds effectively or not. In addition to this,

company should perform well so that it may generate large profits with much ease.

In current scenario, scandals are prevailing not locally but internationally as well. As

such, to remove such defects, it is required to prepare financial reports as it provides clarity to

shareholders and other stakeholders as well (Rahman, 2018). Furthermore, adequate records are

maintained regarding day to day activities of the business. As such, financial reports are quite

1

International financial reporting is quite helpful for stakeholders as well as company as

proper information is available to them regarding financial viability of the business. The present

report deals with importance of financial reporting to business as well as to users of financial

information. This provides clarity to stakeholders to take effective decisions with much ease. It is

useful for investors, lenders that provide funds to organisation for functioning effectively. As

such, financial information as provided financial reports are useful for them.

TASK 1

1. Purpose of financial reporting

Financial reporting is required to get prepare reports by the organisation. It is required so

that each and every transaction is being recorded perfectly in the books of accounts with much

ease by the company. This is not an simple task as it requires effective accounting professionals

so that transaction is properly recorded in the books of accounts and as such, financial reports

may be prepared and provided to users of financial information. Financial reporting is used for

many purpose and as such it is required that accountants should prepare such reports with full

effectiveness so that proper results about the financial health of the company may be reflected to

users of financial information so that they may take better and effective decisions by relying in

such information (Biddle and et.al, 2016 ).

Financial reports conveys about the business whether it is making profit or loss in the

current period and as such, clarity related to financial health of the organisation may be imparted

to all users in the best possible and productive way. This is used for the purpose for imparting

financial performance of the company to various stakeholders be it internal or external. The

investors uses financial reports so that funds are perfectly utilised by the firm. They keep close

watch towards company as whether it is using funds effectively or not. In addition to this,

company should perform well so that it may generate large profits with much ease.

In current scenario, scandals are prevailing not locally but internationally as well. As

such, to remove such defects, it is required to prepare financial reports as it provides clarity to

shareholders and other stakeholders as well (Rahman, 2018). Furthermore, adequate records are

maintained regarding day to day activities of the business. As such, financial reports are quite

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

useful so that scandals may be completely vanished and as a result, organisation is able to make

proper records which are then reflected or listed in financial reports. Liabilities and assets are

also listed in the separate in the financial reports. Moreover, it also reflects how efficiently

business is using capital and how it is producing profits by using such, capital provided by the

shareholders (Nobes, 2014).

In addition to this, financial reports also used for the purpose for providing information to

stakeholders whether may lead in future or not. It provides clarity whether capital given by the

stakeholders’ are adequate to carry out the future activities or not. Lenders and investors also

uses financial reports to come at conclusion whether funds to be provided to company or not and

whether it will repay loans within stipulated time or not. This report provide good summary of

all financial statements such as balance sheet, cash flow statement, income statement, changes in

stockholder’s' equity in quite effective manner to all users to take better and effective decisions

with much ease. Moreover, it also has notes to accounts or workings which supports financial

statements to provide clarity to information seekers in the best possible way. Annual reports are

described in it as well in the most productive way.

Statutory auditors are also benefited by such information as it provided them clarity

whether financial reports give true and fair information or not. As a result, this is used not only

for stakeholders but also by auditors so that true financial information may be exhibit by

financial reports. Thus, all the parties which requires much needed information of the company

are relaxed by seeking financial reports as it represents true and fair information about the

financial health and position of the company in effective way. The information related to

economic resources utilised in the organisation are also listed in the reports which is essential as

it provides information related to money being spent of the shareholders.

The financial reports exhibit each and every aspect of the company which is quite

effectively been utilised by the stakeholders to take vibrant and better decisions for them. In

addition to this, auditors are supported by such reports and it eases for them to check accuracy o

the financial statements in the easiest way (Lang and Stice-Lawrence, 2015). The authorities of

tax department is also benefited by financial reports as it highlights whether firm is paying tax

wisely or not. As such, financial reports are being utilised by every authority to check and test

the accuracy of the financial statements so prepared by the firm. The financial reports are being

utilised for numerous stakeholders and by taxation authorities as well.

2

proper records which are then reflected or listed in financial reports. Liabilities and assets are

also listed in the separate in the financial reports. Moreover, it also reflects how efficiently

business is using capital and how it is producing profits by using such, capital provided by the

shareholders (Nobes, 2014).

In addition to this, financial reports also used for the purpose for providing information to

stakeholders whether may lead in future or not. It provides clarity whether capital given by the

stakeholders’ are adequate to carry out the future activities or not. Lenders and investors also

uses financial reports to come at conclusion whether funds to be provided to company or not and

whether it will repay loans within stipulated time or not. This report provide good summary of

all financial statements such as balance sheet, cash flow statement, income statement, changes in

stockholder’s' equity in quite effective manner to all users to take better and effective decisions

with much ease. Moreover, it also has notes to accounts or workings which supports financial

statements to provide clarity to information seekers in the best possible way. Annual reports are

described in it as well in the most productive way.

Statutory auditors are also benefited by such information as it provided them clarity

whether financial reports give true and fair information or not. As a result, this is used not only

for stakeholders but also by auditors so that true financial information may be exhibit by

financial reports. Thus, all the parties which requires much needed information of the company

are relaxed by seeking financial reports as it represents true and fair information about the

financial health and position of the company in effective way. The information related to

economic resources utilised in the organisation are also listed in the reports which is essential as

it provides information related to money being spent of the shareholders.

The financial reports exhibit each and every aspect of the company which is quite

effectively been utilised by the stakeholders to take vibrant and better decisions for them. In

addition to this, auditors are supported by such reports and it eases for them to check accuracy o

the financial statements in the easiest way (Lang and Stice-Lawrence, 2015). The authorities of

tax department is also benefited by financial reports as it highlights whether firm is paying tax

wisely or not. As such, financial reports are being utilised by every authority to check and test

the accuracy of the financial statements so prepared by the firm. The financial reports are being

utilised for numerous stakeholders and by taxation authorities as well.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial reporting is used by the shareholders and as such, if the performances of the

company is better, then more and more of shareholders’ subscribe shares which is quite

beneficial for the company as it has abundant capital to function effectively in the best possible

way.

2. Regulatory framework of financial reporting and characteristics of financial information

The legal framework is used by the professional bodies so that firm may prepare adequate

reports which is utilised by users of financial information to make certain specific and better

decisions (Kim, Shi and Zhou, 2014). IASB (International Accounting Standards Board) has

given guidelines and framework within which financial reports are to be prepared by the

company so that true and fair information may be imparted to various stakeholders with much

ease. The guidelines are required to be followed by accountants so that proper financial

information may be provided to the shareholders as well. In respect to this, financial guidelines

are numerous which is provided by the professional body.

The principles provided by IASB are related to economic resources and claims must be

provided to users of such information that automatically reflects liquidity and profitability

position of the company to its shareholders to figure out financial health of the organisation in

the best possible way. The shareholders are able to assess and determine strengths and

weaknesses of the organisation in the easiest way. Accrual accounting must be described or

listed in the financial reports as per the guidelines of the professional body. This is essential as it

provides information related to cash flow generated in a particular period.

The body also requires that changes of economic resources may be reflected in statement

of income or profit and loss statement. Whereas, cash flows related information must be

furnished in the cash flow statement. This provides separate sections of certain adjustments

which is being separately shown in the income statement and provides meaningful information to

various stakeholders in the best possible way so that they may assess liquidity and efficiency of

the firm quite effectively (Chen and Li, 2015).

Moreover, information furnished in the financial reports must be by listing elements of

financial statements. In simple words, element so listed in the financial statements must be

directly linked to assets, liabilities and equity as well. In addition to this, income statement

should reflect revenues and expenditures so incurred in the current period as well. These various

elements are quite useful for stakeholders to easily ascertain financial information of the firm in

3

company is better, then more and more of shareholders’ subscribe shares which is quite

beneficial for the company as it has abundant capital to function effectively in the best possible

way.

2. Regulatory framework of financial reporting and characteristics of financial information

The legal framework is used by the professional bodies so that firm may prepare adequate

reports which is utilised by users of financial information to make certain specific and better

decisions (Kim, Shi and Zhou, 2014). IASB (International Accounting Standards Board) has

given guidelines and framework within which financial reports are to be prepared by the

company so that true and fair information may be imparted to various stakeholders with much

ease. The guidelines are required to be followed by accountants so that proper financial

information may be provided to the shareholders as well. In respect to this, financial guidelines

are numerous which is provided by the professional body.

The principles provided by IASB are related to economic resources and claims must be

provided to users of such information that automatically reflects liquidity and profitability

position of the company to its shareholders to figure out financial health of the organisation in

the best possible way. The shareholders are able to assess and determine strengths and

weaknesses of the organisation in the easiest way. Accrual accounting must be described or

listed in the financial reports as per the guidelines of the professional body. This is essential as it

provides information related to cash flow generated in a particular period.

The body also requires that changes of economic resources may be reflected in statement

of income or profit and loss statement. Whereas, cash flows related information must be

furnished in the cash flow statement. This provides separate sections of certain adjustments

which is being separately shown in the income statement and provides meaningful information to

various stakeholders in the best possible way so that they may assess liquidity and efficiency of

the firm quite effectively (Chen and Li, 2015).

Moreover, information furnished in the financial reports must be by listing elements of

financial statements. In simple words, element so listed in the financial statements must be

directly linked to assets, liabilities and equity as well. In addition to this, income statement

should reflect revenues and expenditures so incurred in the current period as well. These various

elements are quite useful for stakeholders to easily ascertain financial information of the firm in

3

the best possible way. Furthermore, legal framework provided by professional bodies must be

fulfilled by the company so that accurate financial reports are prepared and provided to the

stakeholders for making decisions with much ease.

The attributes of financial information are listed below :

1. Relevance –

The underlying concept states that only that information may be recorded which might

affect shareholders perspective. In simple words, relevance concept makes clear that only that

financial information must be recorded which is relevant to users of accounting information to

take better and effective decisions (Ali, Akbar and Ormrod, 2016). Only that financial

information must be recorded which ultimately helps various stakeholders of the company.

2. Materiality -

This principle of financial information states that material information should be recorded

in the accounting books of the company. It simply means that immaterial information must be

ignored while recording information in the books of accounts. Accountants are abide by

professional bodies so that proper and meaningful information is recorded which might affect

decisions of stakeholders.

3. Understandability –

The understandability principle states that financial information presented to users of

accounting information must be easily understandable by them so that they may be able to take

better and effective decisions by relying on such financial information. Thus, to completely

assess organisation’s viability and efficiency position, it is required that information must be

presented in the easiest way which is understandable by various stakeholders.

4. Reliability –

Reliable information must be furnished which is helpful for various stakeholders’ to take

better and effective decisions with much ease. Reliable information means that company should

present financial information with accuracy and with no errors and mistakes related to omissions

of some records which hampers entire financial information (Dudin and et.al, 2015). As such,

this information is quite helpful to users of financial information to take better decisions.

5. Comparability –

The comparability principle states that information may be compared with one another

firm so that liquidity and profitability aspect of the companies may be attained quite easily. This

4

fulfilled by the company so that accurate financial reports are prepared and provided to the

stakeholders for making decisions with much ease.

The attributes of financial information are listed below :

1. Relevance –

The underlying concept states that only that information may be recorded which might

affect shareholders perspective. In simple words, relevance concept makes clear that only that

financial information must be recorded which is relevant to users of accounting information to

take better and effective decisions (Ali, Akbar and Ormrod, 2016). Only that financial

information must be recorded which ultimately helps various stakeholders of the company.

2. Materiality -

This principle of financial information states that material information should be recorded

in the accounting books of the company. It simply means that immaterial information must be

ignored while recording information in the books of accounts. Accountants are abide by

professional bodies so that proper and meaningful information is recorded which might affect

decisions of stakeholders.

3. Understandability –

The understandability principle states that financial information presented to users of

accounting information must be easily understandable by them so that they may be able to take

better and effective decisions by relying on such financial information. Thus, to completely

assess organisation’s viability and efficiency position, it is required that information must be

presented in the easiest way which is understandable by various stakeholders.

4. Reliability –

Reliable information must be furnished which is helpful for various stakeholders’ to take

better and effective decisions with much ease. Reliable information means that company should

present financial information with accuracy and with no errors and mistakes related to omissions

of some records which hampers entire financial information (Dudin and et.al, 2015). As such,

this information is quite helpful to users of financial information to take better decisions.

5. Comparability –

The comparability principle states that information may be compared with one another

firm so that liquidity and profitability aspect of the companies may be attained quite easily. This

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is used by users of accounting information to easily compare inter firm and intra firm

performances. Moreover, interpretations are also easily done by users of accounting information

and as such, it is required that financial information must be comparable. Thus, financial

reporting is required to be legally prepared by the company so that financial information may be

easily provided to users of it and they may take economic decisions with much ease

(Ahmetshina, Vagizova and Kaspina, 2018).

3. Outlining various types of stakeholders in the organisation

There are several types of stakeholders in the company. They are described below :

1. Managers –

Managers are essential stakeholders of the company as they constantly looks at the

operational activities of the organisation so that it may perform well. They also require that

accurate accounting records are maintained by accounting professionals so that true position of

the company may be furnished quite effectively. The financial reports are then provided to users

to take effective decisions.

2. Investors –

Without capital in the company, it may not run smoothly. As such, investors invest their

savings or money in the company in return of getting some Return on Investment. Profitability

aspect is judged by them in the easiest way so that they may assess the efficiency of the firm

whether it will provide greater returns or not. As such, investors looks financial statements to

take decisions quite effectually.

3. Creditors –

The creditors are also important stakeholders of the company. They provide debt to

company for accomplishing operational activities and in return, they charge interest amount

along with the principal amount (O'Connell, AbuGhazaleh and Kintou, 2018). The creditors

ascertain financial statements to assess liquidity position of the company whether it will repay

loans on time or not. Thus, they reach at conclusion whether organisation has debt paying

capacity or not.

4. Discussing value of financial reporting to the company

The company is highly benefited by financial reporting as it helps organisation to pay

taxes and liabilities in the easiest way quite effectively. Moreover, it is essential for the company

to generate accurate financial reports to users of financial information so that better and effective

5

performances. Moreover, interpretations are also easily done by users of accounting information

and as such, it is required that financial information must be comparable. Thus, financial

reporting is required to be legally prepared by the company so that financial information may be

easily provided to users of it and they may take economic decisions with much ease

(Ahmetshina, Vagizova and Kaspina, 2018).

3. Outlining various types of stakeholders in the organisation

There are several types of stakeholders in the company. They are described below :

1. Managers –

Managers are essential stakeholders of the company as they constantly looks at the

operational activities of the organisation so that it may perform well. They also require that

accurate accounting records are maintained by accounting professionals so that true position of

the company may be furnished quite effectively. The financial reports are then provided to users

to take effective decisions.

2. Investors –

Without capital in the company, it may not run smoothly. As such, investors invest their

savings or money in the company in return of getting some Return on Investment. Profitability

aspect is judged by them in the easiest way so that they may assess the efficiency of the firm

whether it will provide greater returns or not. As such, investors looks financial statements to

take decisions quite effectually.

3. Creditors –

The creditors are also important stakeholders of the company. They provide debt to

company for accomplishing operational activities and in return, they charge interest amount

along with the principal amount (O'Connell, AbuGhazaleh and Kintou, 2018). The creditors

ascertain financial statements to assess liquidity position of the company whether it will repay

loans on time or not. Thus, they reach at conclusion whether organisation has debt paying

capacity or not.

4. Discussing value of financial reporting to the company

The company is highly benefited by financial reporting as it helps organisation to pay

taxes and liabilities in the easiest way quite effectively. Moreover, it is essential for the company

to generate accurate financial reports to users of financial information so that better and effective

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions are taken by them with much ease. The government also requires financial reports as it

assess financial position of the company quite easily. Moreover, government uses reports so that

taxes are being wisely paid by company. Thus, financial reporting creates value fot the company

as it reflects true and fair view of it in the best possible way. The financial reports creates value

for the organisation by forecasting future aspect as well. Thus, if organisation is planning to buy

stock, then looking at financial reports, plan may be made accordingly (Binnekade and et.al,

2018).

Furthermore, financial reports are used by the management to take better internal

decisions so that company may perform well with higher profitability. The strengths and

weaknesses are also highlighted by financial reports which are used by the management so that

weaknesses may be eradicated with much ease. This helps company to flourish in the market. By

going through financial reports, capital is analysed and company is able to assess how much

money is left after paying salaries to workers and other expenses.

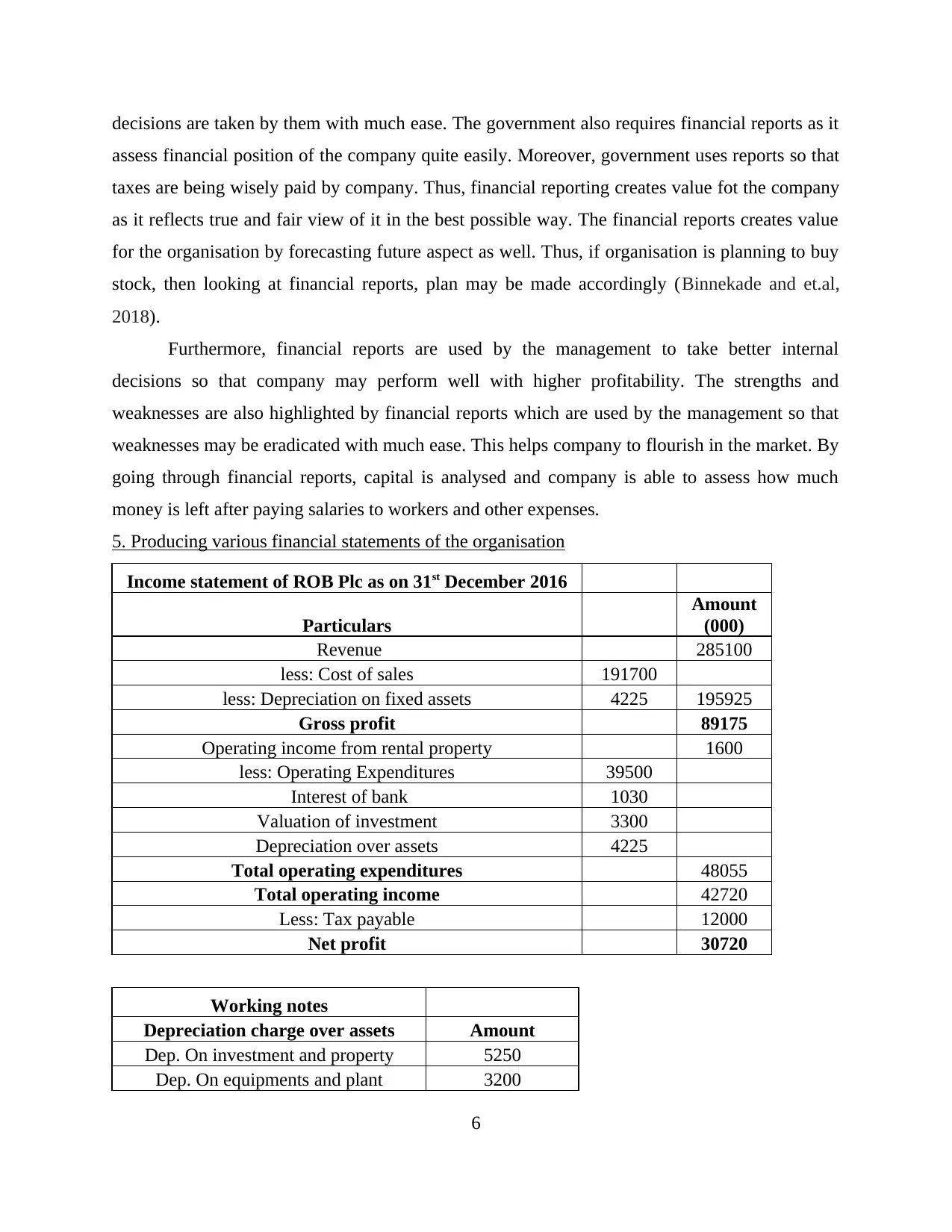

5. Producing various financial statements of the organisation

Income statement of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Revenue 285100

less: Cost of sales 191700

less: Depreciation on fixed assets 4225 195925

Gross profit 89175

Operating income from rental property 1600

less: Operating Expenditures 39500

Interest of bank 1030

Valuation of investment 3300

Depreciation over assets 4225

Total operating expenditures 48055

Total operating income 42720

Less: Tax payable 12000

Net profit 30720

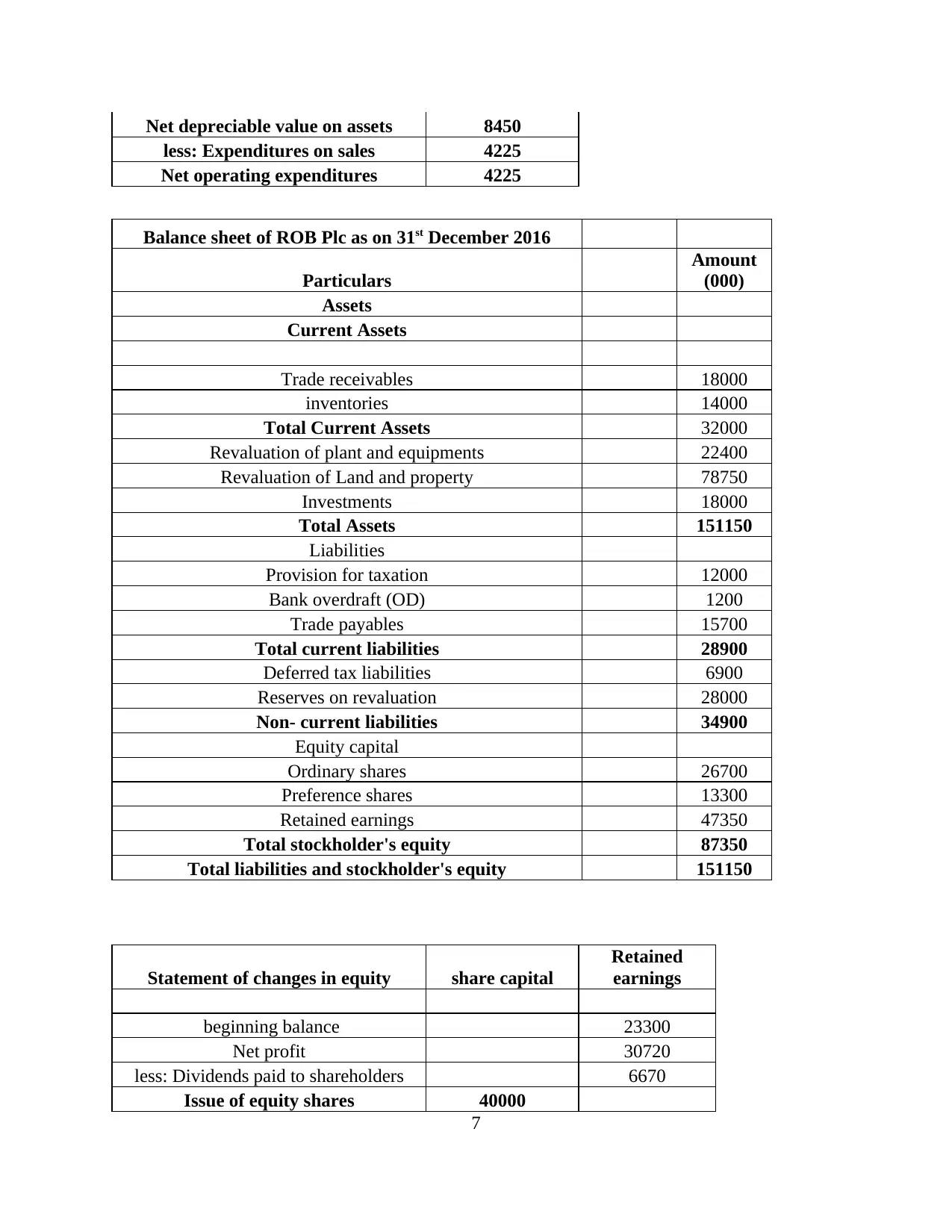

Working notes

Depreciation charge over assets Amount

Dep. On investment and property 5250

Dep. On equipments and plant 3200

6

assess financial position of the company quite easily. Moreover, government uses reports so that

taxes are being wisely paid by company. Thus, financial reporting creates value fot the company

as it reflects true and fair view of it in the best possible way. The financial reports creates value

for the organisation by forecasting future aspect as well. Thus, if organisation is planning to buy

stock, then looking at financial reports, plan may be made accordingly (Binnekade and et.al,

2018).

Furthermore, financial reports are used by the management to take better internal

decisions so that company may perform well with higher profitability. The strengths and

weaknesses are also highlighted by financial reports which are used by the management so that

weaknesses may be eradicated with much ease. This helps company to flourish in the market. By

going through financial reports, capital is analysed and company is able to assess how much

money is left after paying salaries to workers and other expenses.

5. Producing various financial statements of the organisation

Income statement of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Revenue 285100

less: Cost of sales 191700

less: Depreciation on fixed assets 4225 195925

Gross profit 89175

Operating income from rental property 1600

less: Operating Expenditures 39500

Interest of bank 1030

Valuation of investment 3300

Depreciation over assets 4225

Total operating expenditures 48055

Total operating income 42720

Less: Tax payable 12000

Net profit 30720

Working notes

Depreciation charge over assets Amount

Dep. On investment and property 5250

Dep. On equipments and plant 3200

6

Net depreciable value on assets 8450

less: Expenditures on sales 4225

Net operating expenditures 4225

Balance sheet of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Assets

Current Assets

Trade receivables 18000

inventories 14000

Total Current Assets 32000

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank overdraft (OD) 1200

Trade payables 15700

Total current liabilities 28900

Deferred tax liabilities 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital

Ordinary shares 26700

Preference shares 13300

Retained earnings 47350

Total stockholder's equity 87350

Total liabilities and stockholder's equity 151150

Statement of changes in equity share capital

Retained

earnings

beginning balance 23300

Net profit 30720

less: Dividends paid to shareholders 6670

Issue of equity shares 40000

7

less: Expenditures on sales 4225

Net operating expenditures 4225

Balance sheet of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Assets

Current Assets

Trade receivables 18000

inventories 14000

Total Current Assets 32000

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank overdraft (OD) 1200

Trade payables 15700

Total current liabilities 28900

Deferred tax liabilities 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital

Ordinary shares 26700

Preference shares 13300

Retained earnings 47350

Total stockholder's equity 87350

Total liabilities and stockholder's equity 151150

Statement of changes in equity share capital

Retained

earnings

beginning balance 23300

Net profit 30720

less: Dividends paid to shareholders 6670

Issue of equity shares 40000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total changes in the equity 40000 47350

Interpretation:

It can be interpreted that above calculations shows that ROB plc has adequate amount of

capital in the business. As it is reflected by changes in equity statement is 87350. Whereas,

current assets and liabilities are 32000, 28900 respectively. The net income is 30720, which

implies that overall financial position of the company is good.

6. Interpretation of financial ratios

Marks & Spencer (M & S) Plc

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 3.85 % 4.72 %

Liquidity ratio

Current ratio Current assets / Current

Liabilities 0.69:1 0.69:1

Efficiency Ratios

Asset turnover ratio Net sales / Average total

assets 1.27 % 1.28 %

Capital structure

ratios

Gearing ratio Company debt /

Shareholders' Equity 0.52 % 0.55 %

From the calculation of financial ratios, it may be interpreted that financial position of M

& S is overall good in the market. The company is engaged in retail business and is listed on

FTSE index in UK. The financial ratios such as profitability ratio shows that company has good

net profit margin, which is reflected by ratios. However, net profit is decreased in 2016 year

which implies that company need to control on expenses so that it may earn revenue (Ombati and

Shukla, 2018).

Current ratio shows that company has not good liquidity position as it is just 0.69 : 1

which is much lower than ideal ratio of 2 : 1. This implies that it will be unable to pay off

liabilities to the creditors. M & S should improve upon liquidity so that it can make timely

payments. Asset turnover ratio is good in both the years, which shows that company is

8

Interpretation:

It can be interpreted that above calculations shows that ROB plc has adequate amount of

capital in the business. As it is reflected by changes in equity statement is 87350. Whereas,

current assets and liabilities are 32000, 28900 respectively. The net income is 30720, which

implies that overall financial position of the company is good.

6. Interpretation of financial ratios

Marks & Spencer (M & S) Plc

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 3.85 % 4.72 %

Liquidity ratio

Current ratio Current assets / Current

Liabilities 0.69:1 0.69:1

Efficiency Ratios

Asset turnover ratio Net sales / Average total

assets 1.27 % 1.28 %

Capital structure

ratios

Gearing ratio Company debt /

Shareholders' Equity 0.52 % 0.55 %

From the calculation of financial ratios, it may be interpreted that financial position of M

& S is overall good in the market. The company is engaged in retail business and is listed on

FTSE index in UK. The financial ratios such as profitability ratio shows that company has good

net profit margin, which is reflected by ratios. However, net profit is decreased in 2016 year

which implies that company need to control on expenses so that it may earn revenue (Ombati and

Shukla, 2018).

Current ratio shows that company has not good liquidity position as it is just 0.69 : 1

which is much lower than ideal ratio of 2 : 1. This implies that it will be unable to pay off

liabilities to the creditors. M & S should improve upon liquidity so that it can make timely

payments. Asset turnover ratio is good in both the years, which shows that company is

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

effectively using assets to generate sales and as such, profits are garnered by it. Coming to

gearing ratio which is 0.52 and 0.55 in both the years which is not bad as lower gearing ratio is

generally preferable. It shows that firm is using debt in adequate amount.

7. Differentiating IAS and IFRS bodies

IAS IFRS

1. IAS stands for International Accounting

Standards. This scope of this body is not much

wider than IFRS. This is because when any

contradictions is observed than IAS principles

are usually dropped which are then forwarded

to IFRS.

2. IASC (International Accounting Standards

Committee) has issued IAS principles, which

regulates entire accounting system. IASC is

replaced by IASB (International Accounting

Standards Board).

3. The guidelines provided by the body helps

accountants to carry out tasks in effective

manner. This helps them to follow such

guidelines so that accuracy may be achieved.

4. The main of IAS is to work for the internal

control of the organisation so that accurate and

proper accounting records are maintained

effectively by the firm.

1. IFRS stands for International Financial

Reporting Standards. In event of

contradictions, this body is approached to solve

problems and as such, scope of IFRS is much

wider than IAS.

2. On the other hand, principles of IFRS is

issued by IASB as well.

3. The guidelines provided by it completely

differs from IAS. The financial reporting

standards are provided which facilitates legal

framework, which are to be followed by

accountants (Lin, Wu and Lo, 2018).

4. IFRS work for providing legal framework so

that organisation may follow such rules and

laws related to accounting. This is usually done

so that proper accounting records are

maintained by the organisation.

8. Outline the benefits of IFRS body

The benefits of IFRS body is listed below :

1. IFRS usually provide legal framework, which helps company to prepare financial reports with

much ease. Moreover, companies universally accept IFRS guidelines. Various stakeholders are

9

gearing ratio which is 0.52 and 0.55 in both the years which is not bad as lower gearing ratio is

generally preferable. It shows that firm is using debt in adequate amount.

7. Differentiating IAS and IFRS bodies

IAS IFRS

1. IAS stands for International Accounting

Standards. This scope of this body is not much

wider than IFRS. This is because when any

contradictions is observed than IAS principles

are usually dropped which are then forwarded

to IFRS.

2. IASC (International Accounting Standards

Committee) has issued IAS principles, which

regulates entire accounting system. IASC is

replaced by IASB (International Accounting

Standards Board).

3. The guidelines provided by the body helps

accountants to carry out tasks in effective

manner. This helps them to follow such

guidelines so that accuracy may be achieved.

4. The main of IAS is to work for the internal

control of the organisation so that accurate and

proper accounting records are maintained

effectively by the firm.

1. IFRS stands for International Financial

Reporting Standards. In event of

contradictions, this body is approached to solve

problems and as such, scope of IFRS is much

wider than IAS.

2. On the other hand, principles of IFRS is

issued by IASB as well.

3. The guidelines provided by it completely

differs from IAS. The financial reporting

standards are provided which facilitates legal

framework, which are to be followed by

accountants (Lin, Wu and Lo, 2018).

4. IFRS work for providing legal framework so

that organisation may follow such rules and

laws related to accounting. This is usually done

so that proper accounting records are

maintained by the organisation.

8. Outline the benefits of IFRS body

The benefits of IFRS body is listed below :

1. IFRS usually provide legal framework, which helps company to prepare financial reports with

much ease. Moreover, companies universally accept IFRS guidelines. Various stakeholders are

9

benefited by such guidelines and as such they are able to take effective decisions in the best

possible way.

2. The benefits are also to creditors and investors as they are able to take better decisions with

much ease (El Guindy and Basuony, 2018). IFRS provides legal framework and as such,

accurate and true financial information is imparted to investors and creditors and they rely on

such financial statements to take reliable decisions whether to provide funds to company or not.

3. Shareholders are also benefited by IRFS as dividend policies and other related information are

to be provided to them and as a result, they may assess the financial health of firm. This helps

company also as shareholders subscribe more shares and new subscribers evolve as well. As a

result, capital is being garnered by the company, which helps to perform quite well in the future.

4. Qualitative financial information is being provided to shareholders and other stakeholders,

which is used by them to take effective decisions with much ease. IFRS provides benefits to

stakeholders as company provides accurate information about the financial health. The

qualitative information is provided with elements such as comparability, understandability and

reliability.

5. Various rules are provided by IFRS which provides transparency and clarity to users of

accounting information and as a result, they are able to take enhanced decision in the best

possible way. Thus, stakeholders are provided by company and as such, proper accounting

records are maintained effectively.

9. Degrees of compliance of IFRS by the organisations

The above examples of companies such as M & S and other companies, it may be

conveyed that they are using effective framework which is provided by IFRS. As such, financial

reports are prepared in stake of guidelines provided by the professional body (Manes Rossi,

Brusca and Aversano, 2018). This is essential as true and fair view of financial position of

company is reflected which is quite useful for stakeholders to take enhanced decisions. In

accordance of IAS 38, it states that customers’ lists, published titles are restricted by such

professional body. As a result, firm has to abide by such rule and cannot do anything

contradictory to such rule.

Moreover, IAS 29 A also states that financial statements are required to be prepared by

complying legal framework so that reliable information may be provided to users of financial

information with much ease. As such, business is highly affected by such rules and regulations

10

possible way.

2. The benefits are also to creditors and investors as they are able to take better decisions with

much ease (El Guindy and Basuony, 2018). IFRS provides legal framework and as such,

accurate and true financial information is imparted to investors and creditors and they rely on

such financial statements to take reliable decisions whether to provide funds to company or not.

3. Shareholders are also benefited by IRFS as dividend policies and other related information are

to be provided to them and as a result, they may assess the financial health of firm. This helps

company also as shareholders subscribe more shares and new subscribers evolve as well. As a

result, capital is being garnered by the company, which helps to perform quite well in the future.

4. Qualitative financial information is being provided to shareholders and other stakeholders,

which is used by them to take effective decisions with much ease. IFRS provides benefits to

stakeholders as company provides accurate information about the financial health. The

qualitative information is provided with elements such as comparability, understandability and

reliability.

5. Various rules are provided by IFRS which provides transparency and clarity to users of

accounting information and as a result, they are able to take enhanced decision in the best

possible way. Thus, stakeholders are provided by company and as such, proper accounting

records are maintained effectively.

9. Degrees of compliance of IFRS by the organisations

The above examples of companies such as M & S and other companies, it may be

conveyed that they are using effective framework which is provided by IFRS. As such, financial

reports are prepared in stake of guidelines provided by the professional body (Manes Rossi,

Brusca and Aversano, 2018). This is essential as true and fair view of financial position of

company is reflected which is quite useful for stakeholders to take enhanced decisions. In

accordance of IAS 38, it states that customers’ lists, published titles are restricted by such

professional body. As a result, firm has to abide by such rule and cannot do anything

contradictory to such rule.

Moreover, IAS 29 A also states that financial statements are required to be prepared by

complying legal framework so that reliable information may be provided to users of financial

information with much ease. As such, business is highly affected by such rules and regulations

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.