Financial Reporting Analysis: Deferred Tax Impact on Stakeholders

VerifiedAdded on 2020/05/28

|15

|2727

|102

Report

AI Summary

This report undertakes a comprehensive analysis of the financial statements of Blackmores Ltd and Bega Cheese Ltd, with a specific focus on their deferred tax assets and liabilities. The analysis explores the objectives of accounting for income tax, examining how deferred tax assets and liabilities are identified and presented according to AASB 112 and IAS 12. The report delves into the financial statements of both companies, highlighting the current and deferred tax expenses, and assesses the impact of these items on stakeholder decision-making processes, including investment decisions. The report also considers the potential consequences of omitting or misrepresenting deferred tax information in annual reports. The report also includes charts and figures to support the analysis, providing a clear understanding of the financial data presented.

Running head: FINANCIAL REPORTING

FINANCIAL REPORTING

Name of the Student:

Name of the University:

Author’s Note:

FINANCIAL REPORTING

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING

Executive Summary

The main purpose of this assignment is to analyze the financial statements of two company which are

Blackmores ltd and Bega Cheese Ltd. The report aims to provide analysis of the tax and objectives of the

accounting for tax. The report will be focusing on the deferred tax assets and liabilities of the both the

companies. The report will be concluding with the impact on decision making process of the

stakeholders if such deferred tax assets and liabilities of the company are not shown in the annual

reports.

Executive Summary

The main purpose of this assignment is to analyze the financial statements of two company which are

Blackmores ltd and Bega Cheese Ltd. The report aims to provide analysis of the tax and objectives of the

accounting for tax. The report will be focusing on the deferred tax assets and liabilities of the both the

companies. The report will be concluding with the impact on decision making process of the

stakeholders if such deferred tax assets and liabilities of the company are not shown in the annual

reports.

2FINANCIAL REPORTING

Table of Contents

Executive Summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Objectives for Accounting for Income Tax...................................................................................................3

Deferred Tax Assets and Liabilities..............................................................................................................5

Analysis of financial Statement...................................................................................................................7

Impact of Decision Making of Stakeholders................................................................................................8

Conclusions..................................................................................................................................................9

Reference..................................................................................................................................................10

Appendix...................................................................................................................................................11

Table of Contents

Executive Summary.....................................................................................................................................1

Introduction.................................................................................................................................................3

Objectives for Accounting for Income Tax...................................................................................................3

Deferred Tax Assets and Liabilities..............................................................................................................5

Analysis of financial Statement...................................................................................................................7

Impact of Decision Making of Stakeholders................................................................................................8

Conclusions..................................................................................................................................................9

Reference..................................................................................................................................................10

Appendix...................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING

Introduction

The main purpose of the report is to analyze the deferred tax assets and liabilities. The report will be

analyzing the financial statements of both the companies which are Blackmores ltd and Bega Cheese ltd.

The report will be analyzing whether both the companies have any deferred tax assets and deferred tax

liabilities and whether such are properly disclosed in the financial reports of 2017 (Laux, 2013). The

report will be concluding how omission of Items of deferred tax assets and deferred tax liabilities will

impact decision making process of stakeholders and such will be impacting the investing decisions of the

stakeholders.

Overview of the Companies

Blackmores is an Australian company which is engaged in health supplements which was

founded in 1930. The company first opened its first health shop in Brisbane in Australia. The company

was founded by Maurice Blackmore and its headquarter is situated in Sydney, Australia. The company

has a market specialization of $2 billion as per recent estimates (Company information., 2018).

Bega Cheese is an Australian Based Dairy company which is engaged in the manufacture of dairy

products. As per the current estimates the company is the largest dairy company in Australia with a

market valuation of around $775 million. The company was founded in 1899 and its headquarter is

situated in Bega, New South Wales, Australia (Accc.gov.au., 2018).

Objectives for Accounting for Income Tax

Income tax is shown in the consolidated balance sheet of the company and also in income

statement of the company. The current income tax paid is shown in the income statement and the same

is also recorded in the cash flow statement. However in certain situations the figures which are shown in

the profit and loss account differs from the actual cash flow as shown in cash flow statements

(Harrington, Smith & Trippeer, 2012). The reasons for such can be the presences of deferred tax assets

and liabilities which can be set off or set on. The consolidated profit and loss statement of Blackmores

ltd shows that the company has an income tax expenses of $24023000 in 2017 which has significantly

decreased from the previous year which was $43391000 in 2016. The notes to account of the company

shows that the company has a deferred tax benefit $3092000 and also adjustments which are

recognized in the current year is $844000. On the other hand the income tax expenses as shown in the

annual reports for Bega Cheese ltd for 2016 is shown at $59290000 which is more than what was the

Introduction

The main purpose of the report is to analyze the deferred tax assets and liabilities. The report will be

analyzing the financial statements of both the companies which are Blackmores ltd and Bega Cheese ltd.

The report will be analyzing whether both the companies have any deferred tax assets and deferred tax

liabilities and whether such are properly disclosed in the financial reports of 2017 (Laux, 2013). The

report will be concluding how omission of Items of deferred tax assets and deferred tax liabilities will

impact decision making process of stakeholders and such will be impacting the investing decisions of the

stakeholders.

Overview of the Companies

Blackmores is an Australian company which is engaged in health supplements which was

founded in 1930. The company first opened its first health shop in Brisbane in Australia. The company

was founded by Maurice Blackmore and its headquarter is situated in Sydney, Australia. The company

has a market specialization of $2 billion as per recent estimates (Company information., 2018).

Bega Cheese is an Australian Based Dairy company which is engaged in the manufacture of dairy

products. As per the current estimates the company is the largest dairy company in Australia with a

market valuation of around $775 million. The company was founded in 1899 and its headquarter is

situated in Bega, New South Wales, Australia (Accc.gov.au., 2018).

Objectives for Accounting for Income Tax

Income tax is shown in the consolidated balance sheet of the company and also in income

statement of the company. The current income tax paid is shown in the income statement and the same

is also recorded in the cash flow statement. However in certain situations the figures which are shown in

the profit and loss account differs from the actual cash flow as shown in cash flow statements

(Harrington, Smith & Trippeer, 2012). The reasons for such can be the presences of deferred tax assets

and liabilities which can be set off or set on. The consolidated profit and loss statement of Blackmores

ltd shows that the company has an income tax expenses of $24023000 in 2017 which has significantly

decreased from the previous year which was $43391000 in 2016. The notes to account of the company

shows that the company has a deferred tax benefit $3092000 and also adjustments which are

recognized in the current year is $844000. On the other hand the income tax expenses as shown in the

annual reports for Bega Cheese ltd for 2016 is shown at $59290000 which is more than what was the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING

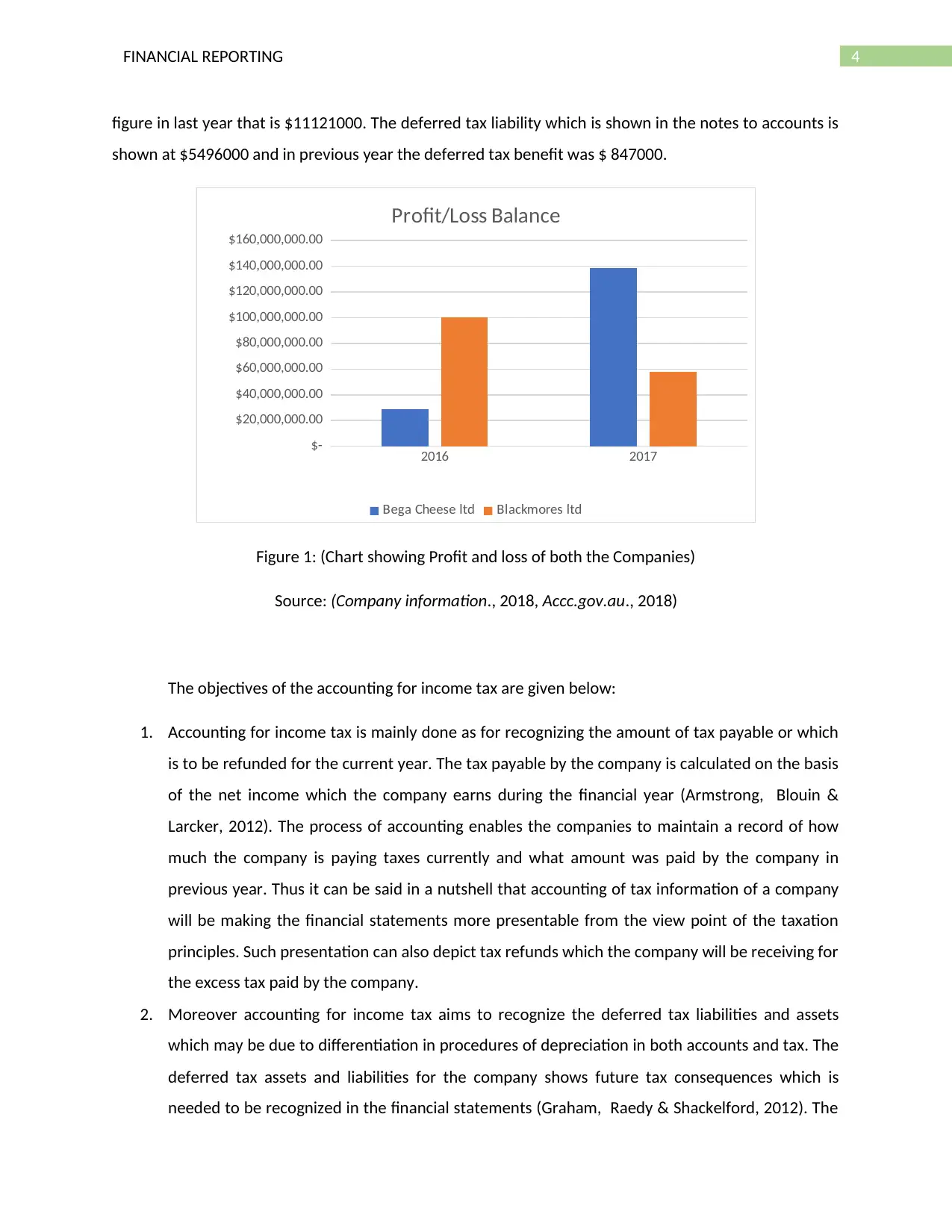

figure in last year that is $11121000. The deferred tax liability which is shown in the notes to accounts is

shown at $5496000 and in previous year the deferred tax benefit was $ 847000.

2016 2017

$-

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

$120,000,000.00

$140,000,000.00

$160,000,000.00

Profit/Loss Balance

Bega Cheese ltd Blackmores ltd

Figure 1: (Chart showing Profit and loss of both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

The objectives of the accounting for income tax are given below:

1. Accounting for income tax is mainly done as for recognizing the amount of tax payable or which

is to be refunded for the current year. The tax payable by the company is calculated on the basis

of the net income which the company earns during the financial year (Armstrong, Blouin &

Larcker, 2012). The process of accounting enables the companies to maintain a record of how

much the company is paying taxes currently and what amount was paid by the company in

previous year. Thus it can be said in a nutshell that accounting of tax information of a company

will be making the financial statements more presentable from the view point of the taxation

principles. Such presentation can also depict tax refunds which the company will be receiving for

the excess tax paid by the company.

2. Moreover accounting for income tax aims to recognize the deferred tax liabilities and assets

which may be due to differentiation in procedures of depreciation in both accounts and tax. The

deferred tax assets and liabilities for the company shows future tax consequences which is

needed to be recognized in the financial statements (Graham, Raedy & Shackelford, 2012). The

figure in last year that is $11121000. The deferred tax liability which is shown in the notes to accounts is

shown at $5496000 and in previous year the deferred tax benefit was $ 847000.

2016 2017

$-

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

$120,000,000.00

$140,000,000.00

$160,000,000.00

Profit/Loss Balance

Bega Cheese ltd Blackmores ltd

Figure 1: (Chart showing Profit and loss of both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

The objectives of the accounting for income tax are given below:

1. Accounting for income tax is mainly done as for recognizing the amount of tax payable or which

is to be refunded for the current year. The tax payable by the company is calculated on the basis

of the net income which the company earns during the financial year (Armstrong, Blouin &

Larcker, 2012). The process of accounting enables the companies to maintain a record of how

much the company is paying taxes currently and what amount was paid by the company in

previous year. Thus it can be said in a nutshell that accounting of tax information of a company

will be making the financial statements more presentable from the view point of the taxation

principles. Such presentation can also depict tax refunds which the company will be receiving for

the excess tax paid by the company.

2. Moreover accounting for income tax aims to recognize the deferred tax liabilities and assets

which may be due to differentiation in procedures of depreciation in both accounts and tax. The

deferred tax assets and liabilities for the company shows future tax consequences which is

needed to be recognized in the financial statements (Graham, Raedy & Shackelford, 2012). The

5FINANCIAL REPORTING

income tax assets or deferred incomes taxes are recognized and presented in the balance sheet

in the noncurrent assets and noncurrent liabilities respectively. However as per the new

guidance on deferred tax assets and liabilities there will be only one net figure of either deferred

tax assets or deferred tax liability (Stice & Stice, 2013).

3. Another objective of recording deferred tax liabilities and deferred asset is that in recent times

the companies have started using these as source of manipulations in business, if proper

accounts are maintained then such risks of manipulations are more or less mitigated.

2016 2017

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

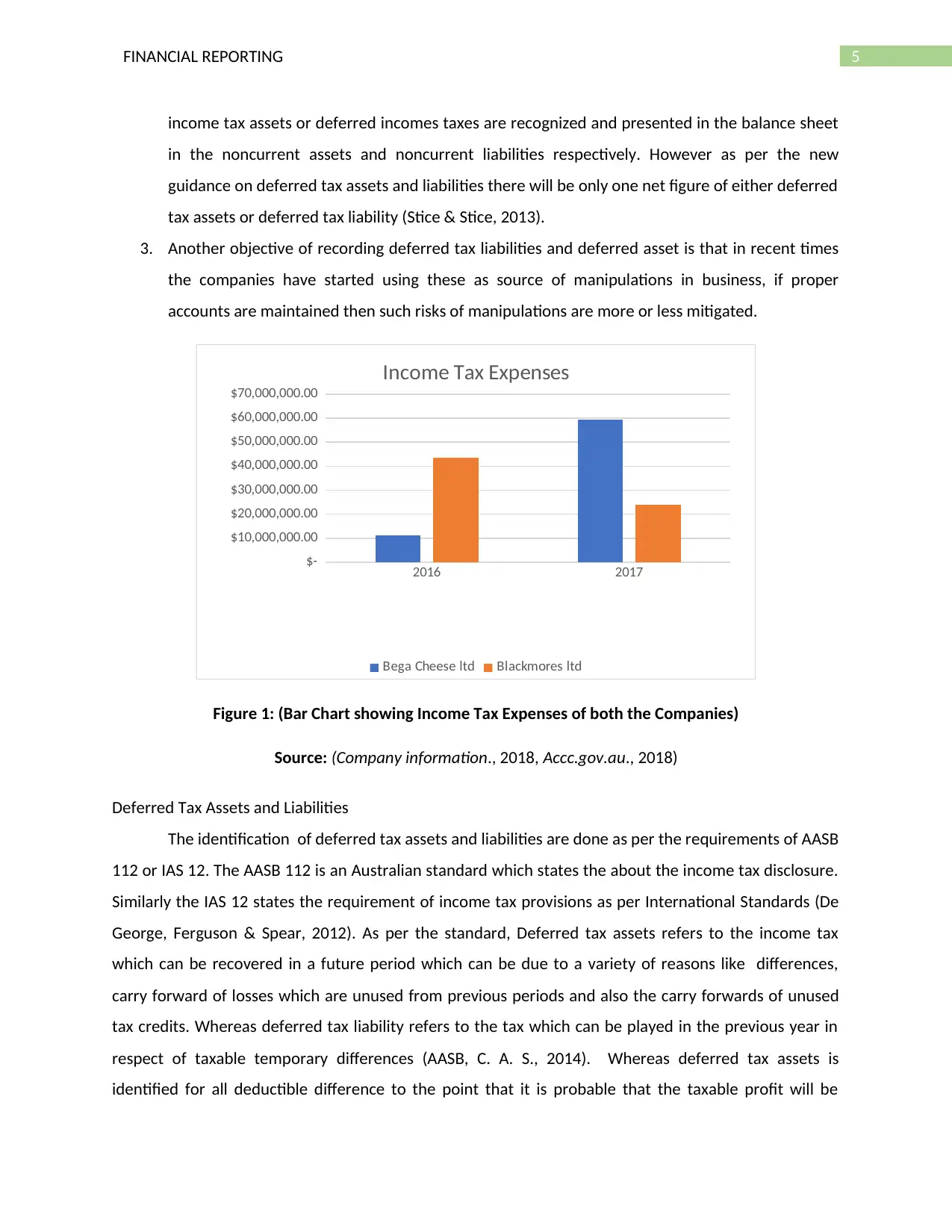

Income Tax Expenses

Bega Cheese ltd Blackmores ltd

Figure 1: (Bar Chart showing Income Tax Expenses of both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

Deferred Tax Assets and Liabilities

The identification of deferred tax assets and liabilities are done as per the requirements of AASB

112 or IAS 12. The AASB 112 is an Australian standard which states the about the income tax disclosure.

Similarly the IAS 12 states the requirement of income tax provisions as per International Standards (De

George, Ferguson & Spear, 2012). As per the standard, Deferred tax assets refers to the income tax

which can be recovered in a future period which can be due to a variety of reasons like differences,

carry forward of losses which are unused from previous periods and also the carry forwards of unused

tax credits. Whereas deferred tax liability refers to the tax which can be played in the previous year in

respect of taxable temporary differences (AASB, C. A. S., 2014). Whereas deferred tax assets is

identified for all deductible difference to the point that it is probable that the taxable profit will be

income tax assets or deferred incomes taxes are recognized and presented in the balance sheet

in the noncurrent assets and noncurrent liabilities respectively. However as per the new

guidance on deferred tax assets and liabilities there will be only one net figure of either deferred

tax assets or deferred tax liability (Stice & Stice, 2013).

3. Another objective of recording deferred tax liabilities and deferred asset is that in recent times

the companies have started using these as source of manipulations in business, if proper

accounts are maintained then such risks of manipulations are more or less mitigated.

2016 2017

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Income Tax Expenses

Bega Cheese ltd Blackmores ltd

Figure 1: (Bar Chart showing Income Tax Expenses of both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

Deferred Tax Assets and Liabilities

The identification of deferred tax assets and liabilities are done as per the requirements of AASB

112 or IAS 12. The AASB 112 is an Australian standard which states the about the income tax disclosure.

Similarly the IAS 12 states the requirement of income tax provisions as per International Standards (De

George, Ferguson & Spear, 2012). As per the standard, Deferred tax assets refers to the income tax

which can be recovered in a future period which can be due to a variety of reasons like differences,

carry forward of losses which are unused from previous periods and also the carry forwards of unused

tax credits. Whereas deferred tax liability refers to the tax which can be played in the previous year in

respect of taxable temporary differences (AASB, C. A. S., 2014). Whereas deferred tax assets is

identified for all deductible difference to the point that it is probable that the taxable profit will be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING

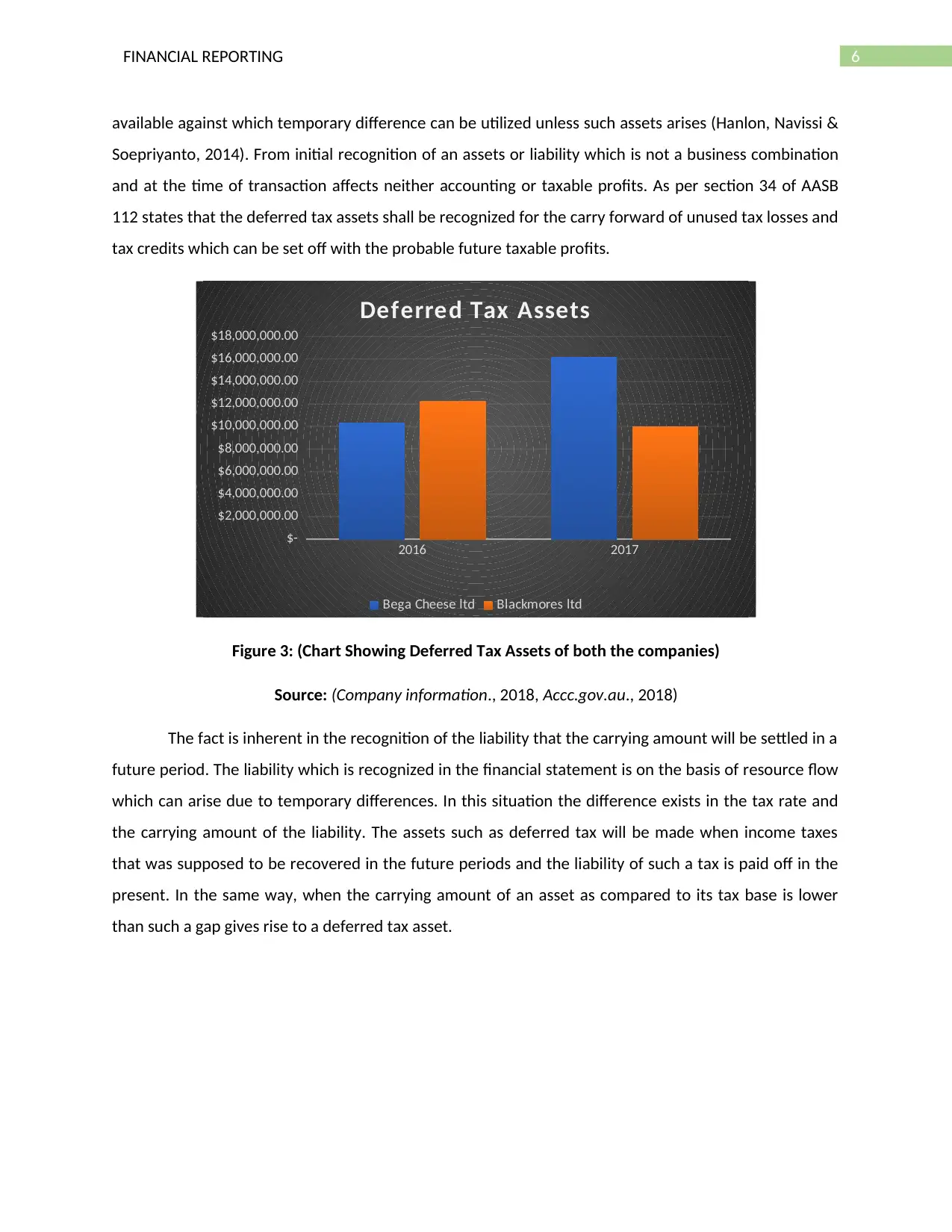

available against which temporary difference can be utilized unless such assets arises (Hanlon, Navissi &

Soepriyanto, 2014). From initial recognition of an assets or liability which is not a business combination

and at the time of transaction affects neither accounting or taxable profits. As per section 34 of AASB

112 states that the deferred tax assets shall be recognized for the carry forward of unused tax losses and

tax credits which can be set off with the probable future taxable profits.

2016 2017

$-

$2,000,000.00

$4,000,000.00

$6,000,000.00

$8,000,000.00

$10,000,000.00

$12,000,000.00

$14,000,000.00

$16,000,000.00

$18,000,000.00

Deferred Tax Assets

Bega Cheese ltd Blackmores ltd

Figure 3: (Chart Showing Deferred Tax Assets of both the companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

The fact is inherent in the recognition of the liability that the carrying amount will be settled in a

future period. The liability which is recognized in the financial statement is on the basis of resource flow

which can arise due to temporary differences. In this situation the difference exists in the tax rate and

the carrying amount of the liability. The assets such as deferred tax will be made when income taxes

that was supposed to be recovered in the future periods and the liability of such a tax is paid off in the

present. In the same way, when the carrying amount of an asset as compared to its tax base is lower

than such a gap gives rise to a deferred tax asset.

available against which temporary difference can be utilized unless such assets arises (Hanlon, Navissi &

Soepriyanto, 2014). From initial recognition of an assets or liability which is not a business combination

and at the time of transaction affects neither accounting or taxable profits. As per section 34 of AASB

112 states that the deferred tax assets shall be recognized for the carry forward of unused tax losses and

tax credits which can be set off with the probable future taxable profits.

2016 2017

$-

$2,000,000.00

$4,000,000.00

$6,000,000.00

$8,000,000.00

$10,000,000.00

$12,000,000.00

$14,000,000.00

$16,000,000.00

$18,000,000.00

Deferred Tax Assets

Bega Cheese ltd Blackmores ltd

Figure 3: (Chart Showing Deferred Tax Assets of both the companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

The fact is inherent in the recognition of the liability that the carrying amount will be settled in a

future period. The liability which is recognized in the financial statement is on the basis of resource flow

which can arise due to temporary differences. In this situation the difference exists in the tax rate and

the carrying amount of the liability. The assets such as deferred tax will be made when income taxes

that was supposed to be recovered in the future periods and the liability of such a tax is paid off in the

present. In the same way, when the carrying amount of an asset as compared to its tax base is lower

than such a gap gives rise to a deferred tax asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING

2016 2017

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

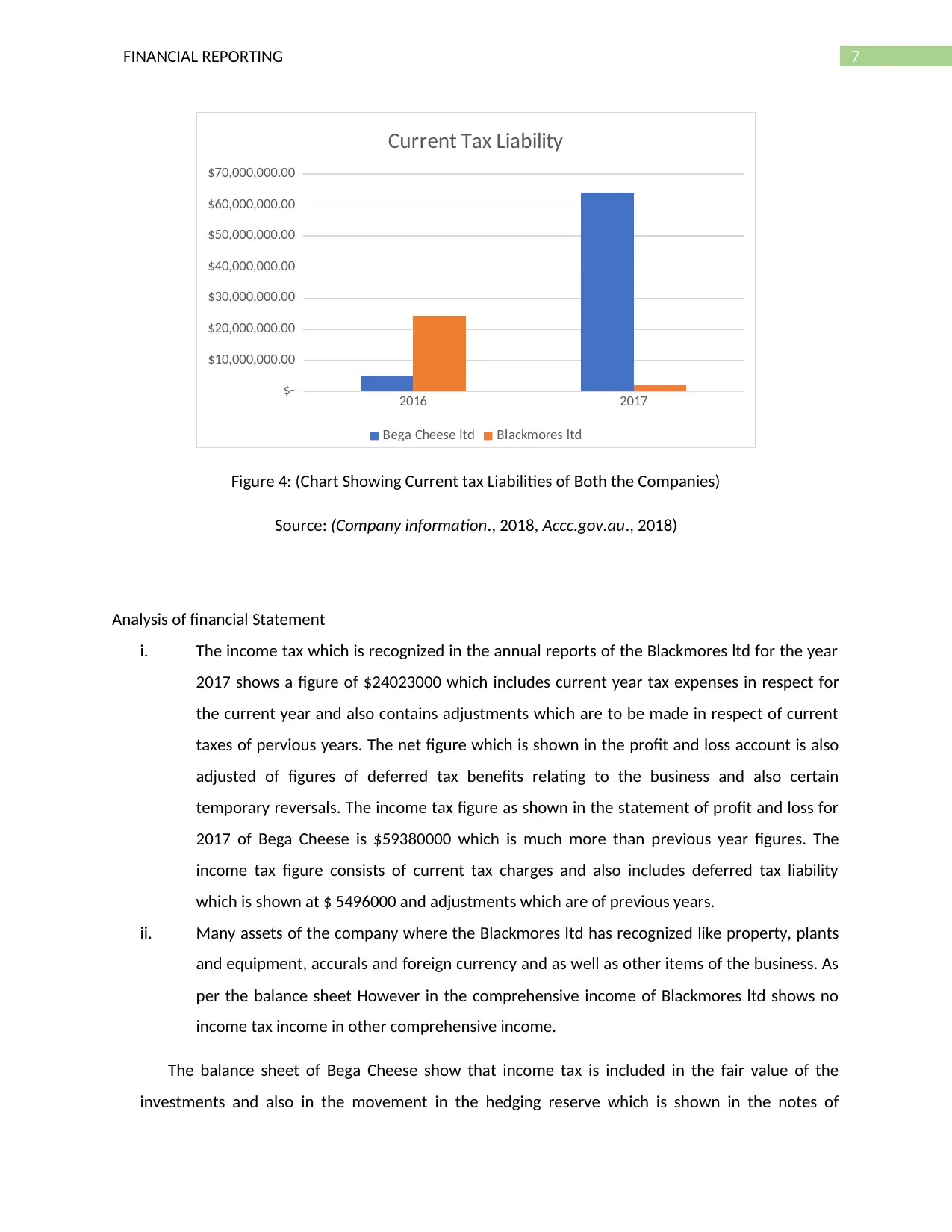

Current Tax Liability

Bega Cheese ltd Blackmores ltd

Figure 4: (Chart Showing Current tax Liabilities of Both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

Analysis of financial Statement

i. The income tax which is recognized in the annual reports of the Blackmores ltd for the year

2017 shows a figure of $24023000 which includes current year tax expenses in respect for

the current year and also contains adjustments which are to be made in respect of current

taxes of pervious years. The net figure which is shown in the profit and loss account is also

adjusted of figures of deferred tax benefits relating to the business and also certain

temporary reversals. The income tax figure as shown in the statement of profit and loss for

2017 of Bega Cheese is $59380000 which is much more than previous year figures. The

income tax figure consists of current tax charges and also includes deferred tax liability

which is shown at $ 5496000 and adjustments which are of previous years.

ii. Many assets of the company where the Blackmores ltd has recognized like property, plants

and equipment, accurals and foreign currency and as well as other items of the business. As

per the balance sheet However in the comprehensive income of Blackmores ltd shows no

income tax income in other comprehensive income.

The balance sheet of Bega Cheese show that income tax is included in the fair value of the

investments and also in the movement in the hedging reserve which is shown in the notes of

2016 2017

$-

$10,000,000.00

$20,000,000.00

$30,000,000.00

$40,000,000.00

$50,000,000.00

$60,000,000.00

$70,000,000.00

Current Tax Liability

Bega Cheese ltd Blackmores ltd

Figure 4: (Chart Showing Current tax Liabilities of Both the Companies)

Source: (Company information., 2018, Accc.gov.au., 2018)

Analysis of financial Statement

i. The income tax which is recognized in the annual reports of the Blackmores ltd for the year

2017 shows a figure of $24023000 which includes current year tax expenses in respect for

the current year and also contains adjustments which are to be made in respect of current

taxes of pervious years. The net figure which is shown in the profit and loss account is also

adjusted of figures of deferred tax benefits relating to the business and also certain

temporary reversals. The income tax figure as shown in the statement of profit and loss for

2017 of Bega Cheese is $59380000 which is much more than previous year figures. The

income tax figure consists of current tax charges and also includes deferred tax liability

which is shown at $ 5496000 and adjustments which are of previous years.

ii. Many assets of the company where the Blackmores ltd has recognized like property, plants

and equipment, accurals and foreign currency and as well as other items of the business. As

per the balance sheet However in the comprehensive income of Blackmores ltd shows no

income tax income in other comprehensive income.

The balance sheet of Bega Cheese show that income tax is included in the fair value of the

investments and also in the movement in the hedging reserve which is shown in the notes of

8FINANCIAL REPORTING

accounts of the company. The company has income tax figure of $45000 in 2017 of fair value

movement in investments and movement in hedging reserve shows a figure of $ 161000 which is

negative.

iii. The current tax expenses of the Blackmores ltd as shown in the balance sheet of the

company is shown at $27239000 and the deferred tax of the company is shown at

$3092000. The net figure which is shown in the profit and loss account is also adjusted of

figures of deferred tax benefits relating to the business and also certain temporary reversals.

On the other hand Bega Cheese ltd shows deferred tax liability in the notes to accounts is

shown at $5496000 and in previous year the deferred tax benefit was $847000. The current

tax expense is $65152000 of the company which is more than the previous year figures.

iv. In both the annual reports of the both the companies that is Blackmores ltd and Bega

Cheese ltd show both current and deferred tax expenses in the balance sheet of the

company. The significance of the current tax expenses and deferred tax items in the

Blackmores is more than that of Bega Cheese of the company.

Impact of Decision Making of Stakeholders

Nowadays the figure of deferred tax is gaining importance more and more these days as the

business may try to manipulate such entries so that the business can gain advantage in business. The

investor and the stakeholder’s decisions can be altered as changes or omission of the deferred tax

amounts can significantly impact business valuations (Trugman, 2016). Moreover companies utilizes

such deferred tax items using the tax rates which are prevalent in the current year. If there are

significant changes in the tax rates than that will consequently change all the values of the financial

report of the company. If corporate rates of the company change then so will the deferred tax assets

and liabilities. In addition to this the deferred tax assets and liabilities have direct impacts on the cash

flow of the company and so the stakeholder’s decisions may also be impacted by such a reason (Collier,

2015). Any rational investor or lender who is reviewing a financial report of the company would want to

know more about the deferred tax expenses if such appear in the annual reports. The investors would

be keen to know the break ups and what consists of the deferred tax assets and liabilities. The investor

or the lender will also like to know what are the situations which caused the deferred tax assets and

liabilities of the company in the first place. Thus from the above discussion it is clear that the investor

will be definitely considering the deferred tax assets and liabilities while taking a decisions (Wahab &

Holland, 2012).

accounts of the company. The company has income tax figure of $45000 in 2017 of fair value

movement in investments and movement in hedging reserve shows a figure of $ 161000 which is

negative.

iii. The current tax expenses of the Blackmores ltd as shown in the balance sheet of the

company is shown at $27239000 and the deferred tax of the company is shown at

$3092000. The net figure which is shown in the profit and loss account is also adjusted of

figures of deferred tax benefits relating to the business and also certain temporary reversals.

On the other hand Bega Cheese ltd shows deferred tax liability in the notes to accounts is

shown at $5496000 and in previous year the deferred tax benefit was $847000. The current

tax expense is $65152000 of the company which is more than the previous year figures.

iv. In both the annual reports of the both the companies that is Blackmores ltd and Bega

Cheese ltd show both current and deferred tax expenses in the balance sheet of the

company. The significance of the current tax expenses and deferred tax items in the

Blackmores is more than that of Bega Cheese of the company.

Impact of Decision Making of Stakeholders

Nowadays the figure of deferred tax is gaining importance more and more these days as the

business may try to manipulate such entries so that the business can gain advantage in business. The

investor and the stakeholder’s decisions can be altered as changes or omission of the deferred tax

amounts can significantly impact business valuations (Trugman, 2016). Moreover companies utilizes

such deferred tax items using the tax rates which are prevalent in the current year. If there are

significant changes in the tax rates than that will consequently change all the values of the financial

report of the company. If corporate rates of the company change then so will the deferred tax assets

and liabilities. In addition to this the deferred tax assets and liabilities have direct impacts on the cash

flow of the company and so the stakeholder’s decisions may also be impacted by such a reason (Collier,

2015). Any rational investor or lender who is reviewing a financial report of the company would want to

know more about the deferred tax expenses if such appear in the annual reports. The investors would

be keen to know the break ups and what consists of the deferred tax assets and liabilities. The investor

or the lender will also like to know what are the situations which caused the deferred tax assets and

liabilities of the company in the first place. Thus from the above discussion it is clear that the investor

will be definitely considering the deferred tax assets and liabilities while taking a decisions (Wahab &

Holland, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING

Conclusions

Thus from the above discussions it is clear that the decision making of the investors will be affected by

the deferred tax assets and liabilities. The above discussions also stresses and evaluates the tax

treatments of Blackmores ltd and Bega Cheese ltd. The above discussions also shows the breakup of

deferred tax assets and liabilities which includes current taxes, adjustments.

Conclusions

Thus from the above discussions it is clear that the decision making of the investors will be affected by

the deferred tax assets and liabilities. The above discussions also stresses and evaluates the tax

treatments of Blackmores ltd and Bega Cheese ltd. The above discussions also shows the breakup of

deferred tax assets and liabilities which includes current taxes, adjustments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING

Reference

Company information. (2018). Blackmores.com.au. Retrieved 22 January 2018, from

https://www.blackmores.com.au/about-us/company-information

Laux, R. C. (2013). The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Harrington, C., Smith, W., & Trippeer, D. (2012). Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, 1.

Armstrong, C. S., Blouin, J. L., & Larcker, D. F. (2012). The incentives for tax planning. Journal of

Accounting and Economics, 53(1), 391-411.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for income taxes. Journal

of Accounting and Economics, 53(1), 412-434.

Stice, E. K., & Stice, J. D. (2013). Intermediate accounting. Cengage Learning.

De George, E. T., Ferguson, C. B., & Spear, N. A. (2012). How much does IFRS cost? IFRS adoption and

audit fees. The Accounting Review, 88(2), 429-462.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax attributed to asset

revaluations. Journal of Contemporary Accounting & Economics, 10(2), 87-99.

AASB, C. A. S. (2014). Business Combinations. Disclosure, 66, 77.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for decision making.

John Wiley & Sons.

Wahab, N. S. A., & Holland, K. (2012). Tax planning, corporate governance and equity value. The British

Accounting Review, 44(2), 111-124.

Trugman. (2016). Understanding business valuation: A practical guide to valuing small to medium sized

businesses. John Wiley & Sons.

Accc.gov.au. (2018) Retrieved 22 January 2018, from https://www.accc.gov.au/system/files/Bega

%2520Cheese%2520Limited.pdf

Reference

Company information. (2018). Blackmores.com.au. Retrieved 22 January 2018, from

https://www.blackmores.com.au/about-us/company-information

Laux, R. C. (2013). The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Harrington, C., Smith, W., & Trippeer, D. (2012). Deferred tax assets and liabilities: tax benefits,

obligations and corporate debt policy. Journal of Finance and Accountancy, 11, 1.

Armstrong, C. S., Blouin, J. L., & Larcker, D. F. (2012). The incentives for tax planning. Journal of

Accounting and Economics, 53(1), 391-411.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for income taxes. Journal

of Accounting and Economics, 53(1), 412-434.

Stice, E. K., & Stice, J. D. (2013). Intermediate accounting. Cengage Learning.

De George, E. T., Ferguson, C. B., & Spear, N. A. (2012). How much does IFRS cost? IFRS adoption and

audit fees. The Accounting Review, 88(2), 429-462.

Hanlon, D., Navissi, F., & Soepriyanto, G. (2014). The value relevance of deferred tax attributed to asset

revaluations. Journal of Contemporary Accounting & Economics, 10(2), 87-99.

AASB, C. A. S. (2014). Business Combinations. Disclosure, 66, 77.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for decision making.

John Wiley & Sons.

Wahab, N. S. A., & Holland, K. (2012). Tax planning, corporate governance and equity value. The British

Accounting Review, 44(2), 111-124.

Trugman. (2016). Understanding business valuation: A practical guide to valuing small to medium sized

businesses. John Wiley & Sons.

Accc.gov.au. (2018) Retrieved 22 January 2018, from https://www.accc.gov.au/system/files/Bega

%2520Cheese%2520Limited.pdf

11FINANCIAL REPORTING

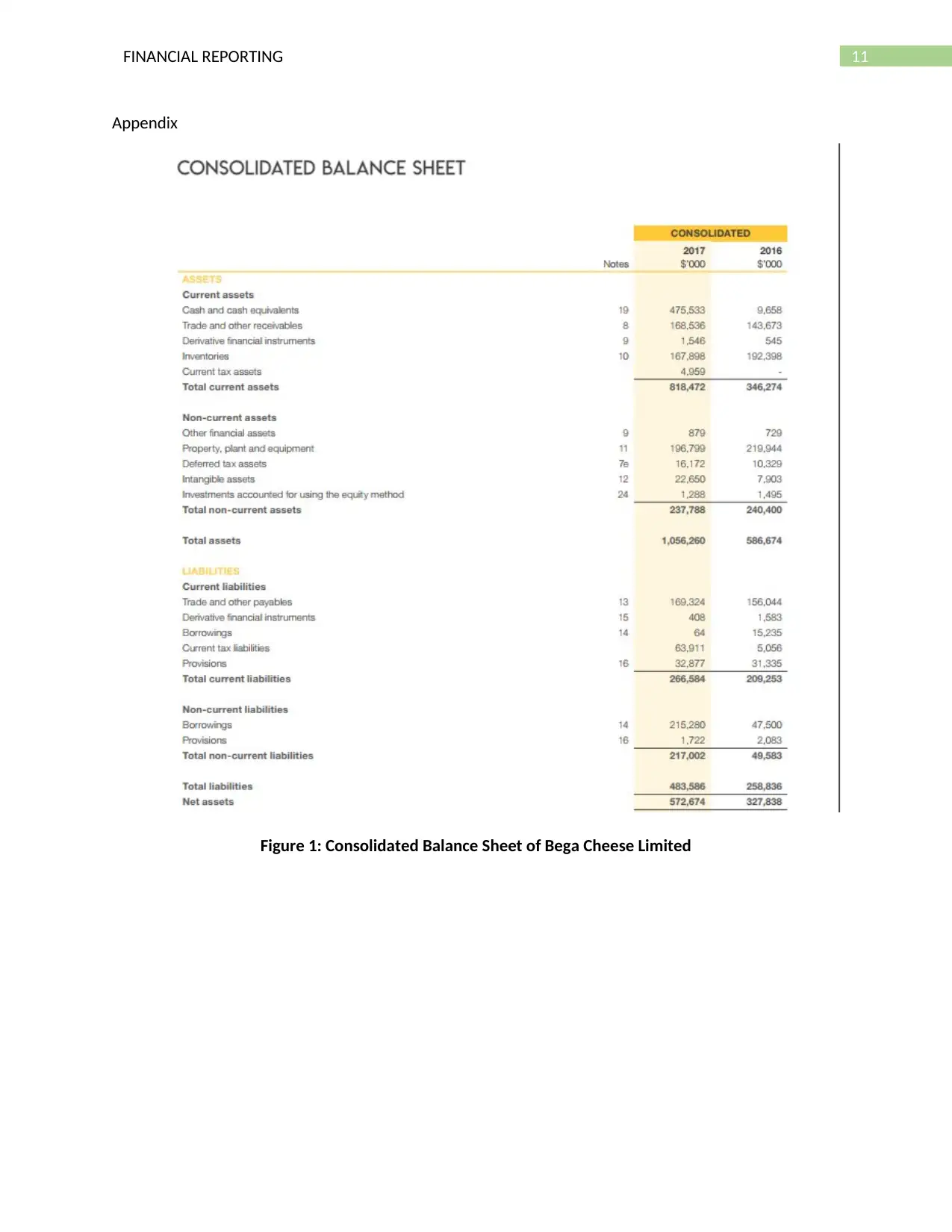

Appendix

Figure 1: Consolidated Balance Sheet of Bega Cheese Limited

Appendix

Figure 1: Consolidated Balance Sheet of Bega Cheese Limited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.