Financial Reporting: IFRS, Stakeholders, and Performance Analysis

VerifiedAdded on 2020/06/06

|18

|4548

|201

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with an introduction to the conceptual and regulatory framework, emphasizing the importance of financial information to stakeholders. It identifies both internal and external stakeholders and details the significance of financial reports for an organization. The report includes the preparation and analysis of financial statements, specifically an income statement, for Rita plc. It delves into the interpretation of financial performance, differentiating between IAS and IFRS, and highlighting the advantages of IFRS. The report also provides a case study on Sainsbury's financial performance and concludes with a summary of the key concepts discussed. The report covers essential aspects of financial reporting, including the objectives of financial reporting, the regulatory framework, qualitative characteristics, and the role of stakeholders. It also contains a detailed analysis of Rita plc's financial performance through its income statement, showcasing the application of financial reporting principles.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Conceptual and regulatory framework of financial reporting.....................................................1

Stakeholder and the importance of financial information to stakeholders..................................3

Importance of financial reports to the organisation....................................................................5

Income Statement........................................................................................................................7

Statement of changes in shareholders equity..............................................................................8

Balance sheet...............................................................................................................................8

Interpretation of financial performance......................................................................................9

Difference between IAS and IFRS............................................................................................11

Advantages of IFRS..................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

Conceptual and regulatory framework of financial reporting.....................................................1

Stakeholder and the importance of financial information to stakeholders..................................3

Importance of financial reports to the organisation....................................................................5

Income Statement........................................................................................................................7

Statement of changes in shareholders equity..............................................................................8

Balance sheet...............................................................................................................................8

Interpretation of financial performance......................................................................................9

Difference between IAS and IFRS............................................................................................11

Advantages of IFRS..................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial reporting is an essential part of any organisation whether it is from service

industry or manufacturing industry. Financial reporting is the process of preparing statements

that are used to disclose the financial status of any organisation to its internal as well as external

users. The basic reports of financial reporting are statement of financial position, statement of

profit and loss(also known as income statement), shareholders equity statement and statement of

cash flow. All the listed companies are subjected to preparation of these financial statements for

all their financial years. For the preparation of financial reports, various boards have issued the

standards like International Accounting standards, International Financial Reporting system and

Generally Accepted Accounting Standards. These reports provide the useful information to its

users which are then able to make economic decisions.

The present report will throw some light on conceptual and regulatory framework,

qualitative characteristics and objectives of financial reporting. This report will also show the

importance of financial information to the stake holders of any organisation. The report clearly

identifies internal and external stakeholders of any organisation. In the present report, financial

statements including balance sheet, income statement and statement of changes in equity has

been prepared for Rita plc. And the interpretation of its financial statements has also been

provided. The present report also provides the interpretation of the financial performance of

Sainsbury that is UK based supermarket chain, has been provided. This also includes the

difference between International Financial Reporting System and International Accounting

Standards and the benefits of IFRS.

Conceptual and regulatory framework of financial reporting

Conceptual and regulatory framework of financial reporting has been provided to define

the purpose and nature of accounting. It must consider the conceptual issues and theoretical

issues surrounded the financial reporting. In accordance to the financial reporting, conceptual

framework can be referred as a Statement of Generally Accepted Accounting Principles

(GAAP).

1

Financial reporting is an essential part of any organisation whether it is from service

industry or manufacturing industry. Financial reporting is the process of preparing statements

that are used to disclose the financial status of any organisation to its internal as well as external

users. The basic reports of financial reporting are statement of financial position, statement of

profit and loss(also known as income statement), shareholders equity statement and statement of

cash flow. All the listed companies are subjected to preparation of these financial statements for

all their financial years. For the preparation of financial reports, various boards have issued the

standards like International Accounting standards, International Financial Reporting system and

Generally Accepted Accounting Standards. These reports provide the useful information to its

users which are then able to make economic decisions.

The present report will throw some light on conceptual and regulatory framework,

qualitative characteristics and objectives of financial reporting. This report will also show the

importance of financial information to the stake holders of any organisation. The report clearly

identifies internal and external stakeholders of any organisation. In the present report, financial

statements including balance sheet, income statement and statement of changes in equity has

been prepared for Rita plc. And the interpretation of its financial statements has also been

provided. The present report also provides the interpretation of the financial performance of

Sainsbury that is UK based supermarket chain, has been provided. This also includes the

difference between International Financial Reporting System and International Accounting

Standards and the benefits of IFRS.

Conceptual and regulatory framework of financial reporting

Conceptual and regulatory framework of financial reporting has been provided to define

the purpose and nature of accounting. It must consider the conceptual issues and theoretical

issues surrounded the financial reporting. In accordance to the financial reporting, conceptual

framework can be referred as a Statement of Generally Accepted Accounting Principles

(GAAP).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conceptual framework provides the theoretical basis as how the financial information is to be

presented and communicated to the users (Conceptual Framework for Financial Reporting,

2017).

To provide useful information related to economic decisions to its users is the main

motive of financial reporting. The regulatory framework of IFRS addresses the following:

The objectives of financial reporting:

The primary users of the information of financial reporting are investors, lenders and

creditors. The information is used to take some decisions regarding selling, buying or

holding equity or debt instruments.

The information is also used by the primary users to not only assess the future net cash

inflow of the entity but to also identify the responsibility of the management towards the

effective and efficient utilisation of entity's existing resources.

Reporting Entity:

The reporting entity is an entity where the users exist who depend on the information of

financial statement to make economic decisions.

An entity to be a reporting entity need not to be a legal entity. It could be a part of an

entity. A parent entity having subsidiary entities should present its financial statements in

consolidated form.

Useful Financial Information and its Qualitative features:

This includes the type of financial information that could be the most useful information

to the users for taking their decisions (Ahmed, Neel and Wang, 2013). The decisions are based

on the reporting entity and the information of its financial reports. Financial information should

contain following qualitative features: Relevance: The information presented in the financial reports must be relevant to the

reporting entity. A financial information to be relevant must contain predictive value,

2

presented and communicated to the users (Conceptual Framework for Financial Reporting,

2017).

To provide useful information related to economic decisions to its users is the main

motive of financial reporting. The regulatory framework of IFRS addresses the following:

The objectives of financial reporting:

The primary users of the information of financial reporting are investors, lenders and

creditors. The information is used to take some decisions regarding selling, buying or

holding equity or debt instruments.

The information is also used by the primary users to not only assess the future net cash

inflow of the entity but to also identify the responsibility of the management towards the

effective and efficient utilisation of entity's existing resources.

Reporting Entity:

The reporting entity is an entity where the users exist who depend on the information of

financial statement to make economic decisions.

An entity to be a reporting entity need not to be a legal entity. It could be a part of an

entity. A parent entity having subsidiary entities should present its financial statements in

consolidated form.

Useful Financial Information and its Qualitative features:

This includes the type of financial information that could be the most useful information

to the users for taking their decisions (Ahmed, Neel and Wang, 2013). The decisions are based

on the reporting entity and the information of its financial reports. Financial information should

contain following qualitative features: Relevance: The information presented in the financial reports must be relevant to the

reporting entity. A financial information to be relevant must contain predictive value,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

confirmatory value or both, these values are capable to make a difference in the decisions

of users. Materiality: It is an entity specific information. For an information to be material,

auditors and accountants need to focus on that aspects of the company that can

significantly affect the decisions of users. Faithful Representation: Financial reports represents economic phenomena in numbers

and words. Therefore, the numbers and words should present a true and fair view and

should be free from misstatements. Comparability: Financial reports will be useful only if the reports can be compared

across the periods and the companies. Verifiability: Financial reports must have the characteristic of communicating underlying

economics of the company's business.

Understandability: Characterising, classifying and presenting the financial information

concisely and clearly makes the financial information Understandable.

Other contents of IFRS framework are:

The measurement criteria and recognition criteria of the information of financial

statements (Bonetti, Magnan and Parbonetti, 2016).

Definition of financial statements

Concepts of capital and capital framework.

From all the above qualitative characteristics, the financial information becomes more

reliable.

Stakeholder and the importance of financial information to stakeholders.

In general term stakeholders of any organisation is a member of a group without whose

support, the organisation would cease to exist. Stakeholders can be termed as any organisation,

group or person who has an interest in the affairs and the activities of the organisation.

Internal Stakeholders

3

of users. Materiality: It is an entity specific information. For an information to be material,

auditors and accountants need to focus on that aspects of the company that can

significantly affect the decisions of users. Faithful Representation: Financial reports represents economic phenomena in numbers

and words. Therefore, the numbers and words should present a true and fair view and

should be free from misstatements. Comparability: Financial reports will be useful only if the reports can be compared

across the periods and the companies. Verifiability: Financial reports must have the characteristic of communicating underlying

economics of the company's business.

Understandability: Characterising, classifying and presenting the financial information

concisely and clearly makes the financial information Understandable.

Other contents of IFRS framework are:

The measurement criteria and recognition criteria of the information of financial

statements (Bonetti, Magnan and Parbonetti, 2016).

Definition of financial statements

Concepts of capital and capital framework.

From all the above qualitative characteristics, the financial information becomes more

reliable.

Stakeholder and the importance of financial information to stakeholders.

In general term stakeholders of any organisation is a member of a group without whose

support, the organisation would cease to exist. Stakeholders can be termed as any organisation,

group or person who has an interest in the affairs and the activities of the organisation.

Internal Stakeholders

3

Employees: Employees of any organisation are the one who create the companies products and

services that are consumed by the customers. If, the best employees of the organisation are

antagonized then the company's customer service will suffer.

Shareholder: These are considered the owners of the company. Shareholders invests the capital

in the company in order to bring the company in a running position, therefore their needs are

important. The board acts on the behalf of shareholders, so they have the capability to replace the

CEO and the executive team. They will act only when the things are going badly wrong.

External Stakeholders

Customers: Every company's purpose is to create more and more customers. A company cannot

survive without customers, therefore the need of the customers comes first (Brigham, 2014). The

customer is the only one that can make the business or can drop the business if shifted to the

competitor. Therefore, in order to retain customers it is essential for the company to innovate its

products on continue basis and offer the products at a rate that gives a good value of money.

Suppliers, other business partners: The company need to maintain relation with their partners to

run the business. Companies, having good long- term relationships with their suppliers can

succeed in long term. Good relationship with suppliers enables the business to develop

strategies, objectives and vision. Distributors and other business partners. In 21st century,

Suppliers have become more critical stakeholders.

Creditors: Lenders to the business are key stakeholders as they provide finance business

ventures, asset and building purchases and supply purchases. Banks provides loans for the

purpose of major purchases of assets like land and building and suppliers provide inventory on

credit. The only expectation of the creditors from business is that the business meets its payment

deadlines consistently and responsibly.

The Local Community: A business to become successful need to be a good citizen. Business

should fulfil its corporate social responsibility towards the community. An organisation should

be seen as a good employer that can provide a good work place (Ongore and Kusa, 2013). The

local community is important for any business but at a lower priority than the other stakeholders.

4

services that are consumed by the customers. If, the best employees of the organisation are

antagonized then the company's customer service will suffer.

Shareholder: These are considered the owners of the company. Shareholders invests the capital

in the company in order to bring the company in a running position, therefore their needs are

important. The board acts on the behalf of shareholders, so they have the capability to replace the

CEO and the executive team. They will act only when the things are going badly wrong.

External Stakeholders

Customers: Every company's purpose is to create more and more customers. A company cannot

survive without customers, therefore the need of the customers comes first (Brigham, 2014). The

customer is the only one that can make the business or can drop the business if shifted to the

competitor. Therefore, in order to retain customers it is essential for the company to innovate its

products on continue basis and offer the products at a rate that gives a good value of money.

Suppliers, other business partners: The company need to maintain relation with their partners to

run the business. Companies, having good long- term relationships with their suppliers can

succeed in long term. Good relationship with suppliers enables the business to develop

strategies, objectives and vision. Distributors and other business partners. In 21st century,

Suppliers have become more critical stakeholders.

Creditors: Lenders to the business are key stakeholders as they provide finance business

ventures, asset and building purchases and supply purchases. Banks provides loans for the

purpose of major purchases of assets like land and building and suppliers provide inventory on

credit. The only expectation of the creditors from business is that the business meets its payment

deadlines consistently and responsibly.

The Local Community: A business to become successful need to be a good citizen. Business

should fulfil its corporate social responsibility towards the community. An organisation should

be seen as a good employer that can provide a good work place (Ongore and Kusa, 2013). The

local community is important for any business but at a lower priority than the other stakeholders.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Government and Regulatory Authorities: every business need to comply with the regulations in

order to avoid disputes and prosecution. Decisions of government entities may have a significant

impact to the operational activities of the business. Therefore, company managers should focus

on maintaining good relationships with the government and local authority.

Importance of financial information to stakeholders

Financial information of the company can have significant impact on the decisions of

stakeholders (Brüggemann, Hitz and Sellhorn, 2013). All the stakeholders want to see the use of

their investments in the company and also to assess the management through the financial

statement. They require the financial information for the following purposes:

To determine how well the company is operating.

To find out the ratio of the company's revenues and expenditure.

To get idea about the company's future strategies, plans and tactics.

To know whether the company is earning profits or is suffering from loss.

To know hoe the assets of the company stacks up against the liabilities of the company.

To determine whether the business have enough capital for its future growth.

Importance of financial reports to the organisation

In all kinds of industries whether service or manufacturing, there are multiple

departments, which functions to achieve organisational goals and objectives. The functions of all

these departments may be dependent or independent. However, at the end of the day all these

departments are linked together with accountancy and finance department (Daske and et.al.,

2013). The various accounting aspects of all these departments are then reported to the

stakeholders, internal stakeholders as well as external stakeholders. For external stakeholders,

there is financial reporting and for internal stakeholders there is management reporting.

Financial reporting objectives:

Financial reporting is done with an objective to identify financial position and the

financial performance of the company. Its objective is also to provide information to the users of

that company so that they can make better economic decisions.

5

order to avoid disputes and prosecution. Decisions of government entities may have a significant

impact to the operational activities of the business. Therefore, company managers should focus

on maintaining good relationships with the government and local authority.

Importance of financial information to stakeholders

Financial information of the company can have significant impact on the decisions of

stakeholders (Brüggemann, Hitz and Sellhorn, 2013). All the stakeholders want to see the use of

their investments in the company and also to assess the management through the financial

statement. They require the financial information for the following purposes:

To determine how well the company is operating.

To find out the ratio of the company's revenues and expenditure.

To get idea about the company's future strategies, plans and tactics.

To know whether the company is earning profits or is suffering from loss.

To know hoe the assets of the company stacks up against the liabilities of the company.

To determine whether the business have enough capital for its future growth.

Importance of financial reports to the organisation

In all kinds of industries whether service or manufacturing, there are multiple

departments, which functions to achieve organisational goals and objectives. The functions of all

these departments may be dependent or independent. However, at the end of the day all these

departments are linked together with accountancy and finance department (Daske and et.al.,

2013). The various accounting aspects of all these departments are then reported to the

stakeholders, internal stakeholders as well as external stakeholders. For external stakeholders,

there is financial reporting and for internal stakeholders there is management reporting.

Financial reporting objectives:

Financial reporting is done with an objective to identify financial position and the

financial performance of the company. Its objective is also to provide information to the users of

that company so that they can make better economic decisions.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 1: Financial Reports

(Leuz and Wysocki, 2016)

Following is the summary of objectives and purpose of financial reporting:

It provides information to the organisation's management which is then used for the

purpose of benchmarking, decision making, planning and analysing.

It provides information to the external users including investors, promoters, creditors and

debt providers which enables them to make prudent and rational decisions regarding

credit, investments, etc.

It provides the information about the various aspects of the organisation to the

shareholders and external users.

Information about the procurement and the utilisation of resources of the company.

With the help of financial reporting, management enhances social welfare by looking

towards the interest of employees, government and trade union.

All the objectives of financial reporting creates base for the organisation to meet their

organisational goals and objectives (Flower, 2016). Through all the above information that is

provided in financial reporting:

6

(Leuz and Wysocki, 2016)

Following is the summary of objectives and purpose of financial reporting:

It provides information to the organisation's management which is then used for the

purpose of benchmarking, decision making, planning and analysing.

It provides information to the external users including investors, promoters, creditors and

debt providers which enables them to make prudent and rational decisions regarding

credit, investments, etc.

It provides the information about the various aspects of the organisation to the

shareholders and external users.

Information about the procurement and the utilisation of resources of the company.

With the help of financial reporting, management enhances social welfare by looking

towards the interest of employees, government and trade union.

All the objectives of financial reporting creates base for the organisation to meet their

organisational goals and objectives (Flower, 2016). Through all the above information that is

provided in financial reporting:

6

More investors will get attracted towards the organisation if the reports show good

percentage of earnings to the customers.

More investor's means more expansion of the business.

With the help of the reports, management is able to make better future decisions

regarding investments, production, and about all other operational activities.

Financial reporting provides the information that the operations of the business are going

in the way to accomplish the missions and visions of the organisation or not.

It helps in identifying the loopholes of the organisation to the management, which can be

rectified at the right time.

A sound financial position of the organisation will attract more customers which in turn

increase the profitability and the performance of the business.

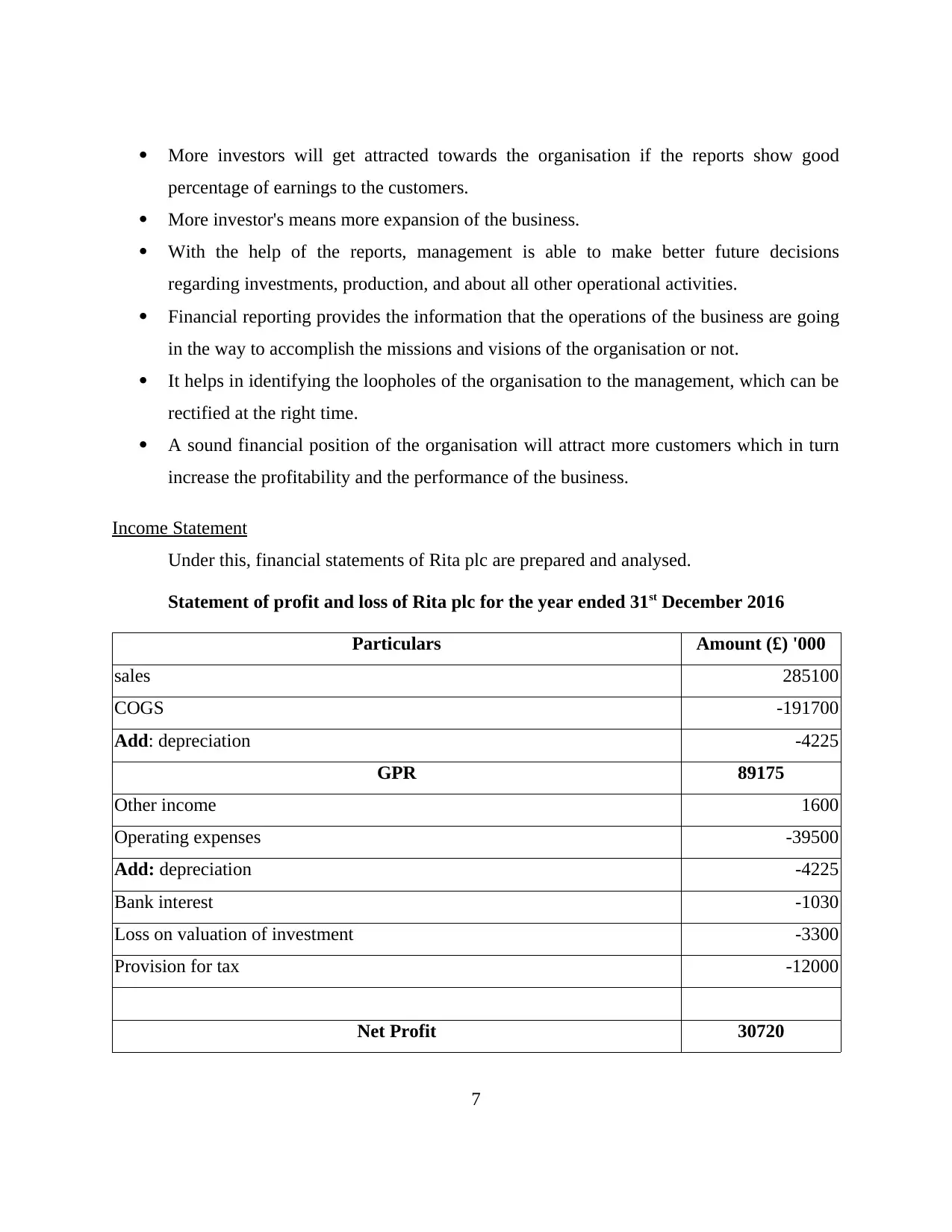

Income Statement

Under this, financial statements of Rita plc are prepared and analysed.

Statement of profit and loss of Rita plc for the year ended 31st December 2016

Particulars Amount (£) '000

sales 285100

COGS -191700

Add: depreciation -4225

GPR 89175

Other income 1600

Operating expenses -39500

Add: depreciation -4225

Bank interest -1030

Loss on valuation of investment -3300

Provision for tax -12000

Net Profit 30720

7

percentage of earnings to the customers.

More investor's means more expansion of the business.

With the help of the reports, management is able to make better future decisions

regarding investments, production, and about all other operational activities.

Financial reporting provides the information that the operations of the business are going

in the way to accomplish the missions and visions of the organisation or not.

It helps in identifying the loopholes of the organisation to the management, which can be

rectified at the right time.

A sound financial position of the organisation will attract more customers which in turn

increase the profitability and the performance of the business.

Income Statement

Under this, financial statements of Rita plc are prepared and analysed.

Statement of profit and loss of Rita plc for the year ended 31st December 2016

Particulars Amount (£) '000

sales 285100

COGS -191700

Add: depreciation -4225

GPR 89175

Other income 1600

Operating expenses -39500

Add: depreciation -4225

Bank interest -1030

Loss on valuation of investment -3300

Provision for tax -12000

Net Profit 30720

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

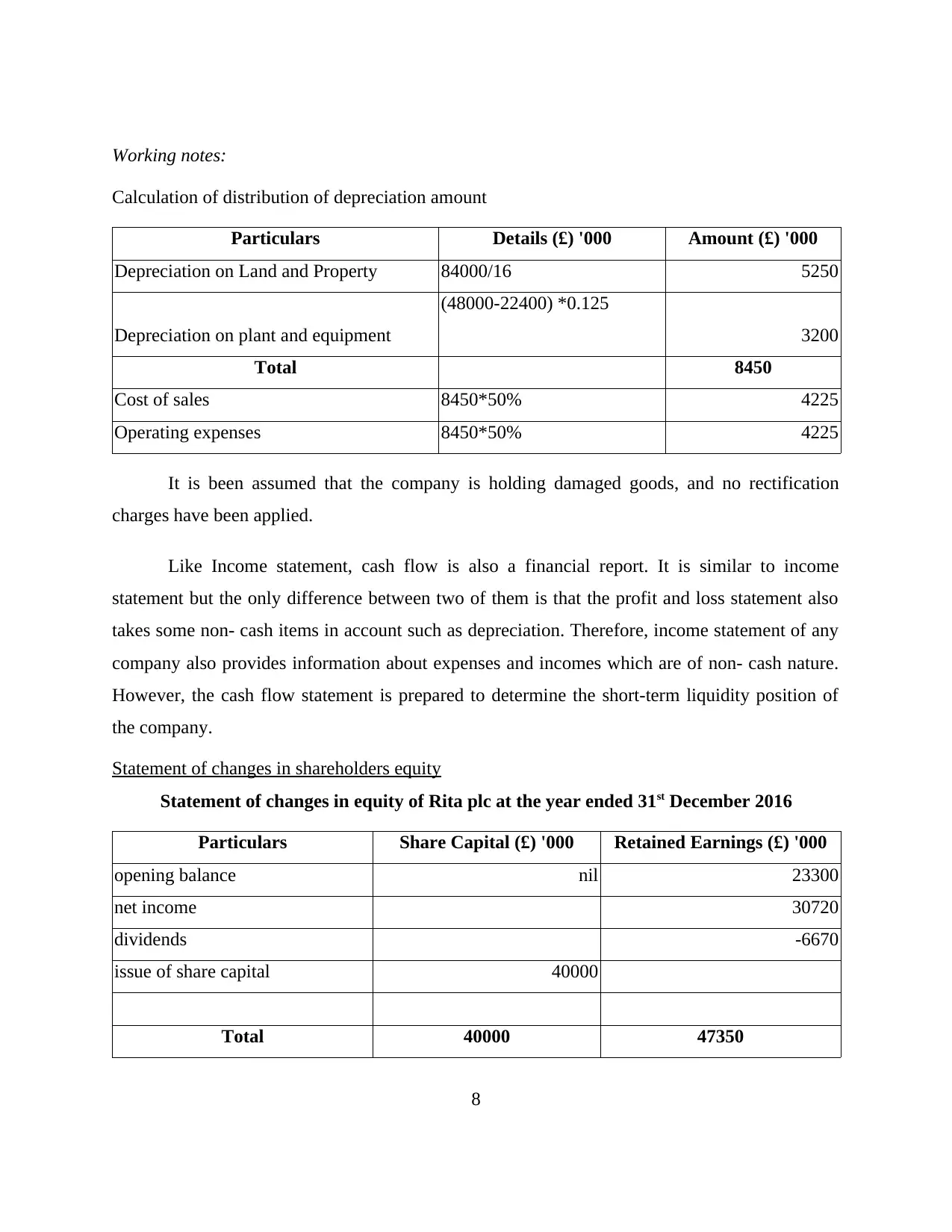

Working notes:

Calculation of distribution of depreciation amount

Particulars Details (£) '000 Amount (£) '000

Depreciation on Land and Property 84000/16 5250

Depreciation on plant and equipment

(48000-22400) *0.125

3200

Total 8450

Cost of sales 8450*50% 4225

Operating expenses 8450*50% 4225

It is been assumed that the company is holding damaged goods, and no rectification

charges have been applied.

Like Income statement, cash flow is also a financial report. It is similar to income

statement but the only difference between two of them is that the profit and loss statement also

takes some non- cash items in account such as depreciation. Therefore, income statement of any

company also provides information about expenses and incomes which are of non- cash nature.

However, the cash flow statement is prepared to determine the short-term liquidity position of

the company.

Statement of changes in shareholders equity

Statement of changes in equity of Rita plc at the year ended 31st December 2016

Particulars Share Capital (£) '000 Retained Earnings (£) '000

opening balance nil 23300

net income 30720

dividends -6670

issue of share capital 40000

Total 40000 47350

8

Calculation of distribution of depreciation amount

Particulars Details (£) '000 Amount (£) '000

Depreciation on Land and Property 84000/16 5250

Depreciation on plant and equipment

(48000-22400) *0.125

3200

Total 8450

Cost of sales 8450*50% 4225

Operating expenses 8450*50% 4225

It is been assumed that the company is holding damaged goods, and no rectification

charges have been applied.

Like Income statement, cash flow is also a financial report. It is similar to income

statement but the only difference between two of them is that the profit and loss statement also

takes some non- cash items in account such as depreciation. Therefore, income statement of any

company also provides information about expenses and incomes which are of non- cash nature.

However, the cash flow statement is prepared to determine the short-term liquidity position of

the company.

Statement of changes in shareholders equity

Statement of changes in equity of Rita plc at the year ended 31st December 2016

Particulars Share Capital (£) '000 Retained Earnings (£) '000

opening balance nil 23300

net income 30720

dividends -6670

issue of share capital 40000

Total 40000 47350

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balance sheet

Balance Sheet of Rita plc at the year ended 31st December 2016

Particulars Details (£) '000 Amount (£) '000

Assets

Non-current assets

Plant and equipment 25600

Less: depreciation -3200 22400

Land and property 84000

Less: depreciation -5250 78750

Investments 18000

(A) 119150

Current assets

Inventories 14000

Trade receivables 18000

(B) 32000

Total Assets (A+B) 151150

Equities and liabilities

Equity

Ordinary shares 26700

Retained earnings 47350

Preference shares 13300

(C) 87350

Non-current liabilities

Deferred income tax 6900

Revaluation reserve 28000

(D) 34900

Current Liabilities

Trade Payables 15700

9

Balance Sheet of Rita plc at the year ended 31st December 2016

Particulars Details (£) '000 Amount (£) '000

Assets

Non-current assets

Plant and equipment 25600

Less: depreciation -3200 22400

Land and property 84000

Less: depreciation -5250 78750

Investments 18000

(A) 119150

Current assets

Inventories 14000

Trade receivables 18000

(B) 32000

Total Assets (A+B) 151150

Equities and liabilities

Equity

Ordinary shares 26700

Retained earnings 47350

Preference shares 13300

(C) 87350

Non-current liabilities

Deferred income tax 6900

Revaluation reserve 28000

(D) 34900

Current Liabilities

Trade Payables 15700

9

Bank Overdraft 1200

Provision for tax 12000

(E) 28900

Total Liabilities (C+D+E) 151150

Statement of financial position is the summary of company's financial information, while

statement of cash flow is the summary of company's flow of cash. Essentially cash flow

statement of any company measures the inflow and outflow of cash, while balance sheet of the

company measures the assets, liabilities and owner's equity of the company. Cash flow statement

provides the information about how changes in the statement of financial position and profit and

loss statement affects the cash position of the company.

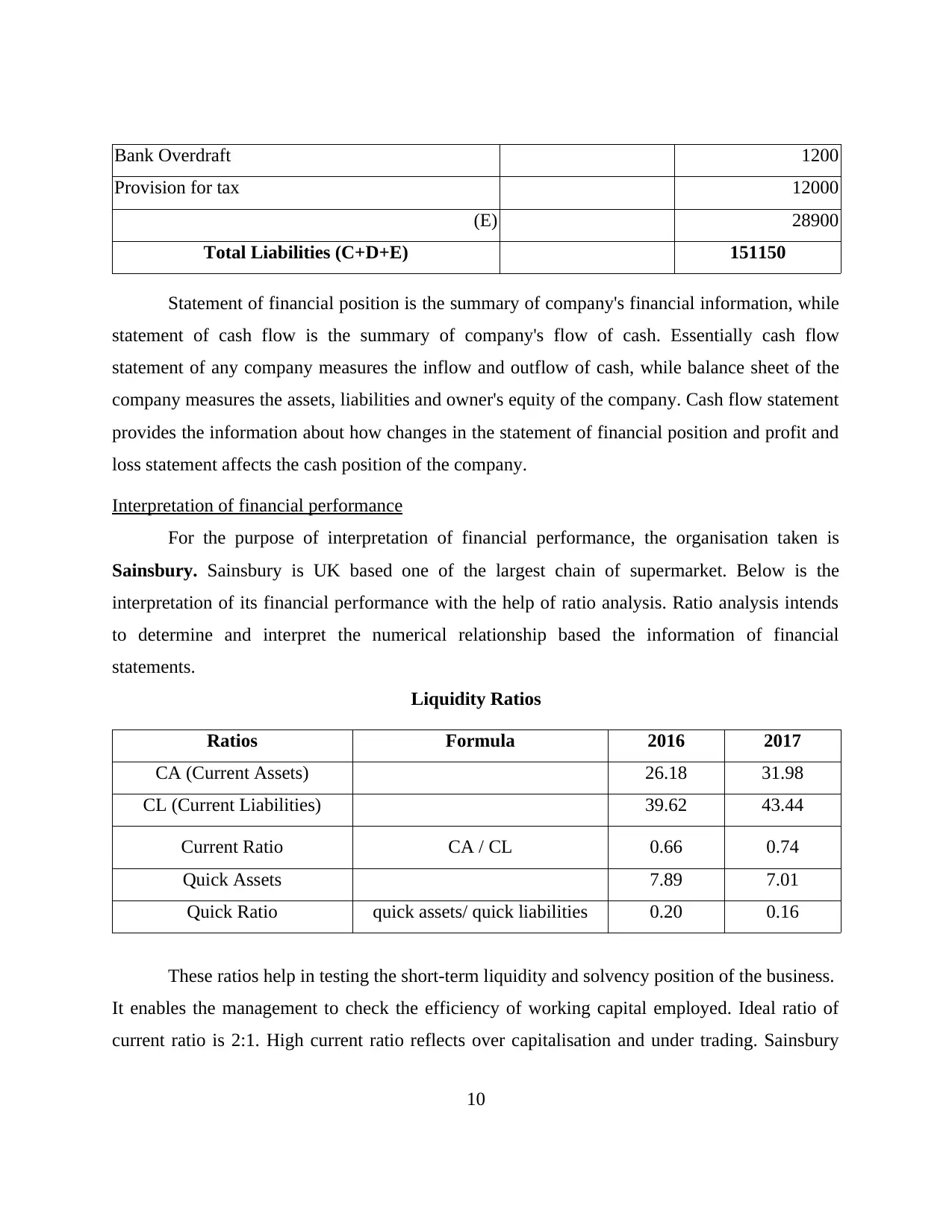

Interpretation of financial performance

For the purpose of interpretation of financial performance, the organisation taken is

Sainsbury. Sainsbury is UK based one of the largest chain of supermarket. Below is the

interpretation of its financial performance with the help of ratio analysis. Ratio analysis intends

to determine and interpret the numerical relationship based the information of financial

statements.

Liquidity Ratios

Ratios Formula 2016 2017

CA (Current Assets) 26.18 31.98

CL (Current Liabilities) 39.62 43.44

Current Ratio CA / CL 0.66 0.74

Quick Assets 7.89 7.01

Quick Ratio quick assets/ quick liabilities 0.20 0.16

These ratios help in testing the short-term liquidity and solvency position of the business.

It enables the management to check the efficiency of working capital employed. Ideal ratio of

current ratio is 2:1. High current ratio reflects over capitalisation and under trading. Sainsbury

10

Provision for tax 12000

(E) 28900

Total Liabilities (C+D+E) 151150

Statement of financial position is the summary of company's financial information, while

statement of cash flow is the summary of company's flow of cash. Essentially cash flow

statement of any company measures the inflow and outflow of cash, while balance sheet of the

company measures the assets, liabilities and owner's equity of the company. Cash flow statement

provides the information about how changes in the statement of financial position and profit and

loss statement affects the cash position of the company.

Interpretation of financial performance

For the purpose of interpretation of financial performance, the organisation taken is

Sainsbury. Sainsbury is UK based one of the largest chain of supermarket. Below is the

interpretation of its financial performance with the help of ratio analysis. Ratio analysis intends

to determine and interpret the numerical relationship based the information of financial

statements.

Liquidity Ratios

Ratios Formula 2016 2017

CA (Current Assets) 26.18 31.98

CL (Current Liabilities) 39.62 43.44

Current Ratio CA / CL 0.66 0.74

Quick Assets 7.89 7.01

Quick Ratio quick assets/ quick liabilities 0.20 0.16

These ratios help in testing the short-term liquidity and solvency position of the business.

It enables the management to check the efficiency of working capital employed. Ideal ratio of

current ratio is 2:1. High current ratio reflects over capitalisation and under trading. Sainsbury

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.