International Financial Reporting: Analysis of Financial Statements

VerifiedAdded on 2020/07/23

|15

|3823

|106

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, starting with its purpose and objectives, and progressing to its regulatory framework and governance aspects. It identifies key stakeholders and examines how they benefit from financial information. The report delves into the value of financial reporting in achieving organizational objectives, development, and growth, offering insights into the interpretation of profit & loss statements, statements of changes in equity, and balance sheets. Furthermore, it includes a practical application of financial ratios for assessing organizational performance and investment potential. A comparative assessment between IFRS and IAS is presented, emphasizing the benefits of international accounting standards. The report concludes by highlighting the importance and differences of financial reporting across various countries, providing a well-rounded perspective on the subject.

International Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

1 Analyzing the purpose of financial reporting......................................................................1

2. Presenting the context of financial reporting along with regulatory framework and

governance.............................................................................................................................1

3. Identifying main stakeholders of an organization and manner in which they benefited

from financial information.....................................................................................................1

4. Examining the value of financial reporting in the context of organizational objectives,

development and growth........................................................................................................2

5. Interpreting profit & loss, statement of changes in equity and balance sheet....................3

6 Calculating and presenting financial ratios for organizational performance & investment5

7. Assessing difference between IFRS and IAS.....................................................................7

8. Explaining the benefits of international accounting standard and IFRS............................7

9. Stating differences and importance of financial reporting across different countries.......8

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................1

1 Analyzing the purpose of financial reporting......................................................................1

2. Presenting the context of financial reporting along with regulatory framework and

governance.............................................................................................................................1

3. Identifying main stakeholders of an organization and manner in which they benefited

from financial information.....................................................................................................1

4. Examining the value of financial reporting in the context of organizational objectives,

development and growth........................................................................................................2

5. Interpreting profit & loss, statement of changes in equity and balance sheet....................3

6 Calculating and presenting financial ratios for organizational performance & investment5

7. Assessing difference between IFRS and IAS.....................................................................7

8. Explaining the benefits of international accounting standard and IFRS............................7

9. Stating differences and importance of financial reporting across different countries.......8

CONCLUSION..........................................................................................................................9

REFERENCES.........................................................................................................................11

INTRODUCTION

Financial reporting is the process that is undertaken by business organization to

measure performance and providing stakeholders with suitable information for decision

making. In the recent era, every business unit lays high level of emphasis on preparing

financial reports at the end of accounting year. This in turn helps them in communicating

monetary information and thereby attracts more investors. In this, present report will shed

light on the manner in which regulatory and governance aspects is highly associated with

financial reporting. Besides this, it will also provide deeper insight about the motives that are

considered by business unit while preparing financial reporting. Report also depicts the extent

to which profitability, liquidity and solvency position of ROB Plc is sound. Further, it also

entails the significance of financial reports in the context of international market.

1 Analyzing the purpose of financial reporting

Financial reporting lays focus on disclosing monetary information to various

stakeholders such as management, investors etc about monetary position and performance

over the specified period of time. Main purposes and objectives of financial reporting are as

follows:

Provides information to the management and helps in devising appropriate plan.

Financial reports help firm in tracking cash flow

With the motive to analyze assets, liabilities and owner’s equity firm lays emphasis on

preparing financial reports (What is the objective of financial reporting, 2017).

Along with this, another main purpose of firm behind the preparation of financial

reports is to build and maintain faith of investors.

Financial reports also enable firm to meet the information need of several

stakeholders concerning with its performance.

Financial reporting is the process that is undertaken by business organization to

measure performance and providing stakeholders with suitable information for decision

making. In the recent era, every business unit lays high level of emphasis on preparing

financial reports at the end of accounting year. This in turn helps them in communicating

monetary information and thereby attracts more investors. In this, present report will shed

light on the manner in which regulatory and governance aspects is highly associated with

financial reporting. Besides this, it will also provide deeper insight about the motives that are

considered by business unit while preparing financial reporting. Report also depicts the extent

to which profitability, liquidity and solvency position of ROB Plc is sound. Further, it also

entails the significance of financial reports in the context of international market.

1 Analyzing the purpose of financial reporting

Financial reporting lays focus on disclosing monetary information to various

stakeholders such as management, investors etc about monetary position and performance

over the specified period of time. Main purposes and objectives of financial reporting are as

follows:

Provides information to the management and helps in devising appropriate plan.

Financial reports help firm in tracking cash flow

With the motive to analyze assets, liabilities and owner’s equity firm lays emphasis on

preparing financial reports (What is the objective of financial reporting, 2017).

Along with this, another main purpose of firm behind the preparation of financial

reports is to build and maintain faith of investors.

Financial reports also enable firm to meet the information need of several

stakeholders concerning with its performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

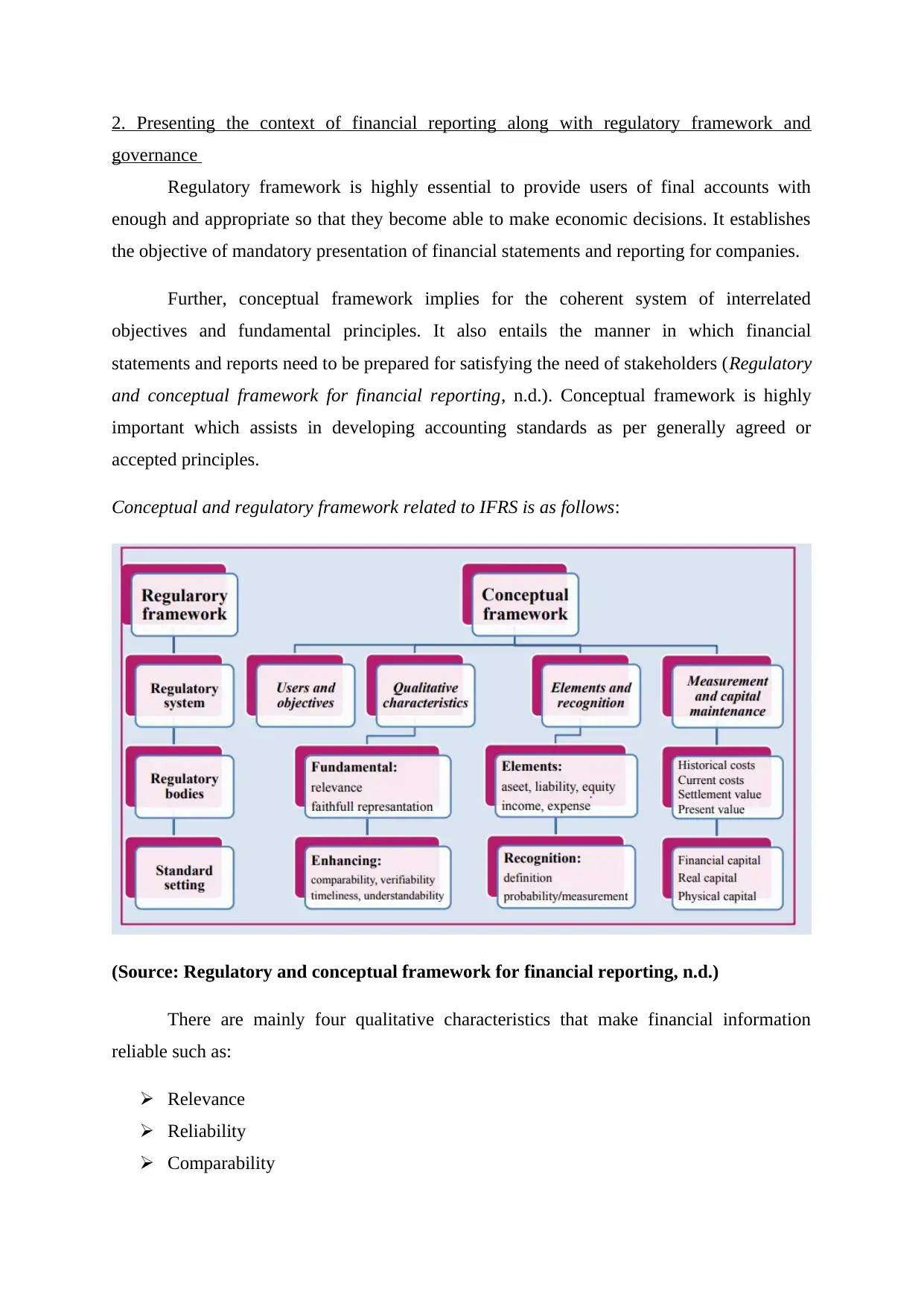

2. Presenting the context of financial reporting along with regulatory framework and

governance

Regulatory framework is highly essential to provide users of final accounts with

enough and appropriate so that they become able to make economic decisions. It establishes

the objective of mandatory presentation of financial statements and reporting for companies.

Further, conceptual framework implies for the coherent system of interrelated

objectives and fundamental principles. It also entails the manner in which financial

statements and reports need to be prepared for satisfying the need of stakeholders (Regulatory

and conceptual framework for financial reporting, n.d.). Conceptual framework is highly

important which assists in developing accounting standards as per generally agreed or

accepted principles.

Conceptual and regulatory framework related to IFRS is as follows:

(Source: Regulatory and conceptual framework for financial reporting, n.d.)

There are mainly four qualitative characteristics that make financial information

reliable such as:

Relevance

Reliability

Comparability

governance

Regulatory framework is highly essential to provide users of final accounts with

enough and appropriate so that they become able to make economic decisions. It establishes

the objective of mandatory presentation of financial statements and reporting for companies.

Further, conceptual framework implies for the coherent system of interrelated

objectives and fundamental principles. It also entails the manner in which financial

statements and reports need to be prepared for satisfying the need of stakeholders (Regulatory

and conceptual framework for financial reporting, n.d.). Conceptual framework is highly

important which assists in developing accounting standards as per generally agreed or

accepted principles.

Conceptual and regulatory framework related to IFRS is as follows:

(Source: Regulatory and conceptual framework for financial reporting, n.d.)

There are mainly four qualitative characteristics that make financial information

reliable such as:

Relevance

Reliability

Comparability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Understandability

On the basis of all the above aspects, financial statements and reports must contain

information that aid in the decision making of stakeholders. Further, financial reports must

free from false information and error (Stent, Bradbury and Hooks, 2017). To make the

information reliable firm needs to present information in such a manner that one can easily

understands the same and become able to make comparison with others.

3. Identifying main stakeholders of an organization and manner in which they benefited from

financial information

There are several stakeholders who have an interest in the performance of business

unit such as employees, investors, supplier and financial institution etc. Hence, by

undertaking and evaluating financial reports all such stakeholders are become able to satisfy

their information need (Warren and Jones, 2018). For instance: Financial reports contain

information about the level to which business unit is in position to meet debt or liabilities

from assets. In this, monetary reports serve valuable information to investors, promoters, debt

provider and creditors in making effectual decision regarding investment, credit etc. In

addition to this, financial reports help employees in making estimation about company’s

performance and growth. This in turn helps them in assessing the level of incentives and

salary enhancement. In this way, financial reports assist such stakeholders in taking suitable

decision associated with concerned unit.

4. Examining the value of financial reporting in the context of organizational objectives,

development and growth

Value of financial reporting can be assessed or determined on the basis of following

aspects:

Financial reports serve monetary information to the management team of firm and

assists in planning, analysis, benchmarking & decision making. By making evaluation

of monetary reports business unit can assess the extent to which it is performing well

and become able to take strategic measure for improvement (Janowicz, 2017). Hence,

it can be stated that aspects of financial reporting assists management team who is

engaged in decision making aspect pertaining to organizational objectives and

strategic framework.

On the basis of all the above aspects, financial statements and reports must contain

information that aid in the decision making of stakeholders. Further, financial reports must

free from false information and error (Stent, Bradbury and Hooks, 2017). To make the

information reliable firm needs to present information in such a manner that one can easily

understands the same and become able to make comparison with others.

3. Identifying main stakeholders of an organization and manner in which they benefited from

financial information

There are several stakeholders who have an interest in the performance of business

unit such as employees, investors, supplier and financial institution etc. Hence, by

undertaking and evaluating financial reports all such stakeholders are become able to satisfy

their information need (Warren and Jones, 2018). For instance: Financial reports contain

information about the level to which business unit is in position to meet debt or liabilities

from assets. In this, monetary reports serve valuable information to investors, promoters, debt

provider and creditors in making effectual decision regarding investment, credit etc. In

addition to this, financial reports help employees in making estimation about company’s

performance and growth. This in turn helps them in assessing the level of incentives and

salary enhancement. In this way, financial reports assist such stakeholders in taking suitable

decision associated with concerned unit.

4. Examining the value of financial reporting in the context of organizational objectives,

development and growth

Value of financial reporting can be assessed or determined on the basis of following

aspects:

Financial reports serve monetary information to the management team of firm and

assists in planning, analysis, benchmarking & decision making. By making evaluation

of monetary reports business unit can assess the extent to which it is performing well

and become able to take strategic measure for improvement (Janowicz, 2017). Hence,

it can be stated that aspects of financial reporting assists management team who is

engaged in decision making aspect pertaining to organizational objectives and

strategic framework.

In the competitive business arena, firm can maintain and attract investors only when it

serves suitable information to them on time. In this regard, financial reports are highly

significant which in turn helps investors in making evaluation of financial position

and performance (Ward and Lowe, 2017). Hence, through the means of financial

reports by providing accurate and timely information to investor’s business

organization can maintain their faith. This in turn offers benefits and makes

significant contribution in the attainment of organizational goals and objectives. For

instance: Whenever growing firm will issue shares to public then on the basis of

financial reports it would become able to attract more investors and helps in fulfilling

monetary requirements.

Company also prepares report with the motive to ascertain manner in which various

resources are procured and used (Stent, Bradbury and Hooks, 2017). By this, firm can

evaluate its efficiency level and take competent decisions for the growth as well as

development in relation to the near future.

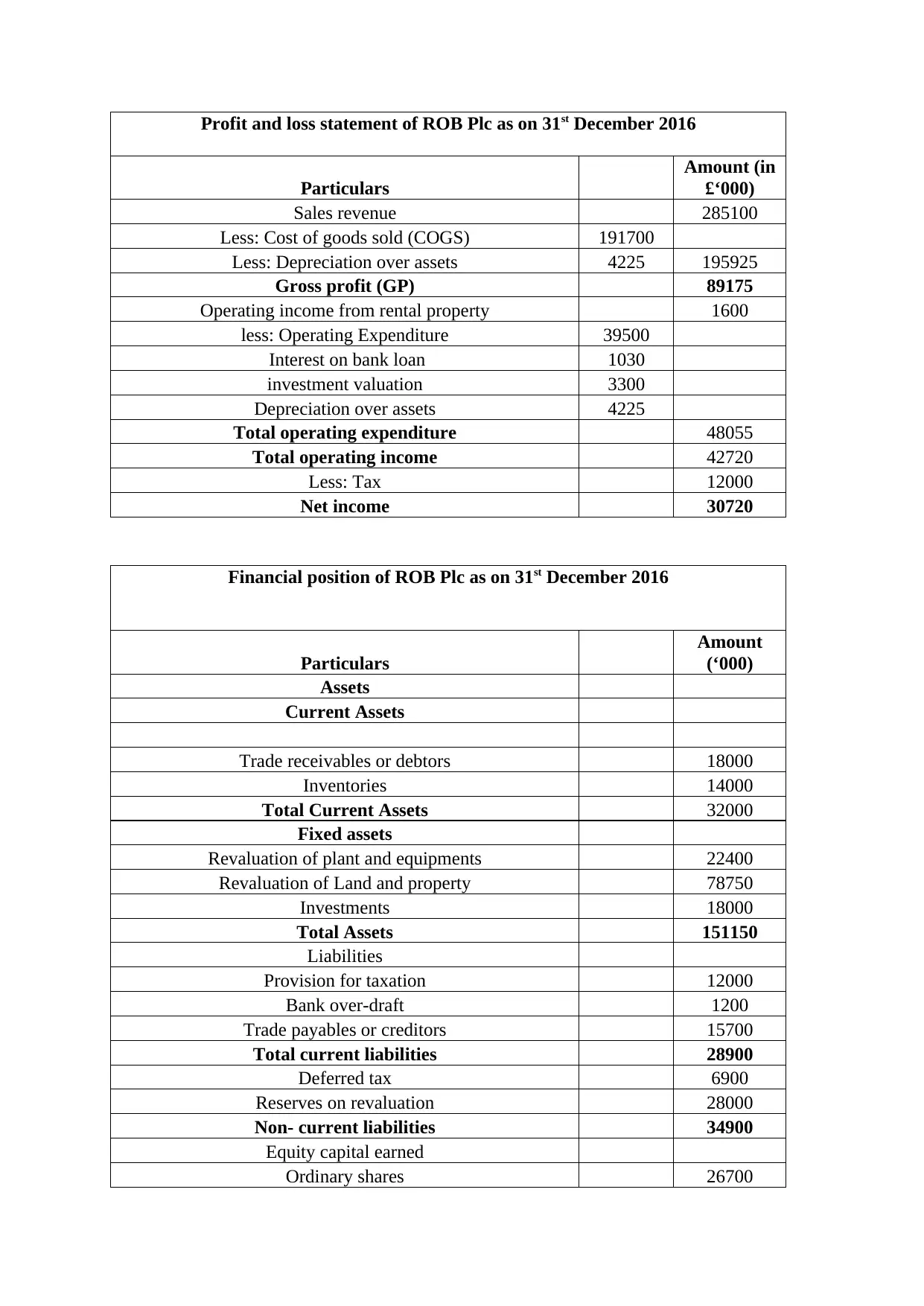

5. Interpreting profit & loss, statement of changes in equity and balance sheet

Business unit prepares financial statements at the end of accounting year with the

motive to ascertain and evaluate performance.

Profit & loss statement: It furnishes information about net margin generate by the

firm during accounting year over expenses.

Statement of financial position: Balance sheet presents financial performance under

two different categories such as assets and liabilities. Assets side include fixed such as land,

machinery etc, and current namely cash, debtors (Sinclair and Keller, 2017). On the other

side, liabilities are further distinguished into three aspects such as current and non-current

obligations as well as shareholder’s equity.

However, statement of cash flow provides deeper insight about cash generated

through operating, investing and financing activities. Hence, investing activities of cash flow

statement entails about fixed assets purchased and sold during the accounting year (Florou,

Kosi and Pope, 2017). Further, financing activities of cash flow statement presents

information regarding issue and redemption of debenture etc. Such aspects of financing and

investing activities make cash flow statement different from others.

serves suitable information to them on time. In this regard, financial reports are highly

significant which in turn helps investors in making evaluation of financial position

and performance (Ward and Lowe, 2017). Hence, through the means of financial

reports by providing accurate and timely information to investor’s business

organization can maintain their faith. This in turn offers benefits and makes

significant contribution in the attainment of organizational goals and objectives. For

instance: Whenever growing firm will issue shares to public then on the basis of

financial reports it would become able to attract more investors and helps in fulfilling

monetary requirements.

Company also prepares report with the motive to ascertain manner in which various

resources are procured and used (Stent, Bradbury and Hooks, 2017). By this, firm can

evaluate its efficiency level and take competent decisions for the growth as well as

development in relation to the near future.

5. Interpreting profit & loss, statement of changes in equity and balance sheet

Business unit prepares financial statements at the end of accounting year with the

motive to ascertain and evaluate performance.

Profit & loss statement: It furnishes information about net margin generate by the

firm during accounting year over expenses.

Statement of financial position: Balance sheet presents financial performance under

two different categories such as assets and liabilities. Assets side include fixed such as land,

machinery etc, and current namely cash, debtors (Sinclair and Keller, 2017). On the other

side, liabilities are further distinguished into three aspects such as current and non-current

obligations as well as shareholder’s equity.

However, statement of cash flow provides deeper insight about cash generated

through operating, investing and financing activities. Hence, investing activities of cash flow

statement entails about fixed assets purchased and sold during the accounting year (Florou,

Kosi and Pope, 2017). Further, financing activities of cash flow statement presents

information regarding issue and redemption of debenture etc. Such aspects of financing and

investing activities make cash flow statement different from others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit and loss statement of ROB Plc as on 31st December 2016

Particulars

Amount (in

£‘000)

Sales revenue 285100

Less: Cost of goods sold (COGS) 191700

Less: Depreciation over assets 4225 195925

Gross profit (GP) 89175

Operating income from rental property 1600

less: Operating Expenditure 39500

Interest on bank loan 1030

investment valuation 3300

Depreciation over assets 4225

Total operating expenditure 48055

Total operating income 42720

Less: Tax 12000

Net income 30720

Financial position of ROB Plc as on 31st December 2016

Particulars

Amount

(‘000)

Assets

Current Assets

Trade receivables or debtors 18000

Inventories 14000

Total Current Assets 32000

Fixed assets

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank over-draft 1200

Trade payables or creditors 15700

Total current liabilities 28900

Deferred tax 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital earned

Ordinary shares 26700

Particulars

Amount (in

£‘000)

Sales revenue 285100

Less: Cost of goods sold (COGS) 191700

Less: Depreciation over assets 4225 195925

Gross profit (GP) 89175

Operating income from rental property 1600

less: Operating Expenditure 39500

Interest on bank loan 1030

investment valuation 3300

Depreciation over assets 4225

Total operating expenditure 48055

Total operating income 42720

Less: Tax 12000

Net income 30720

Financial position of ROB Plc as on 31st December 2016

Particulars

Amount

(‘000)

Assets

Current Assets

Trade receivables or debtors 18000

Inventories 14000

Total Current Assets 32000

Fixed assets

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank over-draft 1200

Trade payables or creditors 15700

Total current liabilities 28900

Deferred tax 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital earned

Ordinary shares 26700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preference shares 13300

Retained earnings 47350

Total shareholder's equity 87350

Total liabilities and shareholder's equity 151150

Statement of changes in equity for ROB Plc

Particulars Share capital

Retained

earnings

Balance at the beginning 23300

Net income 30720

less: Dividends paid 6670

Issue of equity share 40000

Total changes in the equity 40000 47350

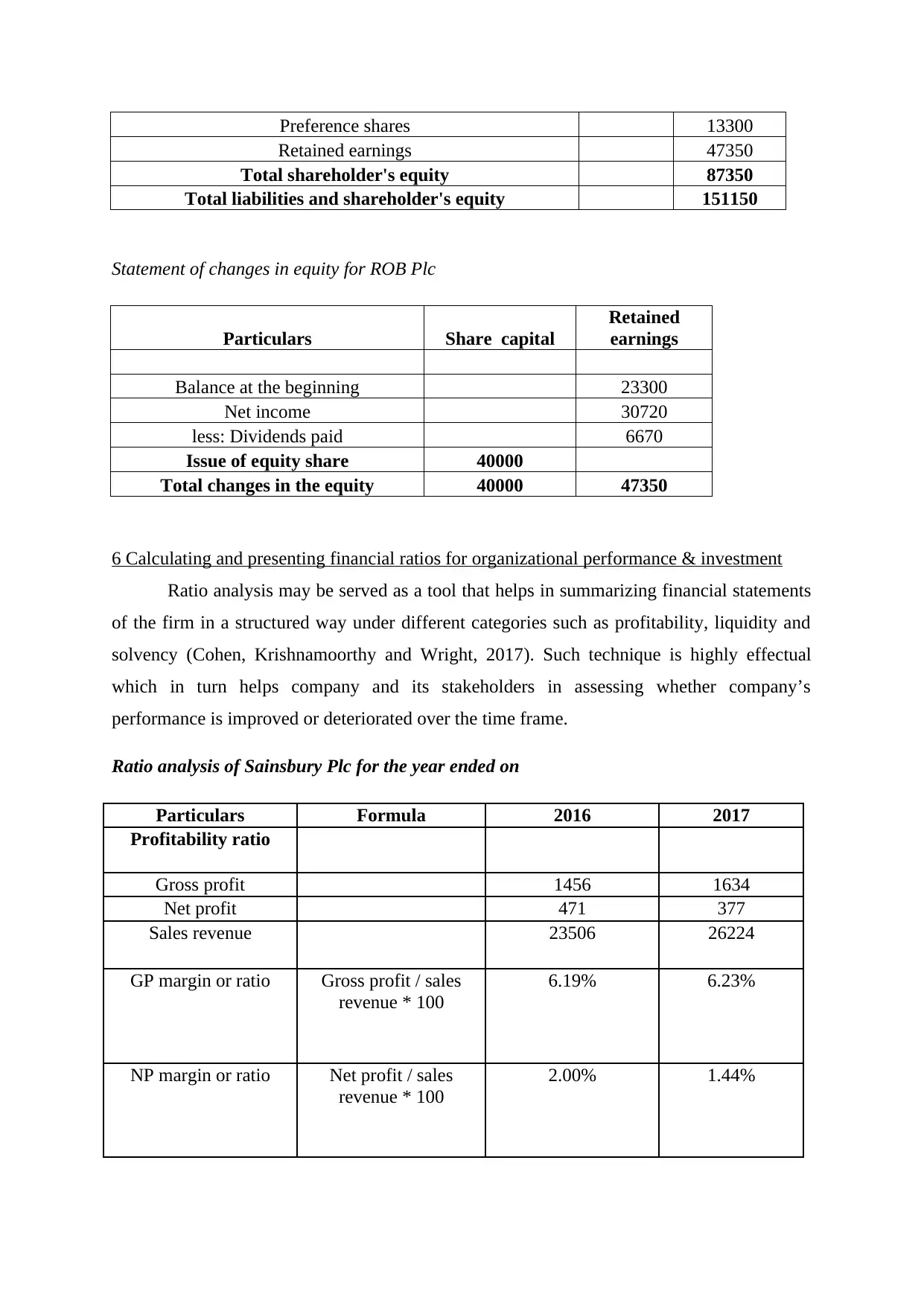

6 Calculating and presenting financial ratios for organizational performance & investment

Ratio analysis may be served as a tool that helps in summarizing financial statements

of the firm in a structured way under different categories such as profitability, liquidity and

solvency (Cohen, Krishnamoorthy and Wright, 2017). Such technique is highly effectual

which in turn helps company and its stakeholders in assessing whether company’s

performance is improved or deteriorated over the time frame.

Ratio analysis of Sainsbury Plc for the year ended on

Particulars Formula 2016 2017

Profitability ratio

Gross profit 1456 1634

Net profit 471 377

Sales revenue 23506 26224

GP margin or ratio Gross profit / sales

revenue * 100

6.19% 6.23%

NP margin or ratio Net profit / sales

revenue * 100

2.00% 1.44%

Retained earnings 47350

Total shareholder's equity 87350

Total liabilities and shareholder's equity 151150

Statement of changes in equity for ROB Plc

Particulars Share capital

Retained

earnings

Balance at the beginning 23300

Net income 30720

less: Dividends paid 6670

Issue of equity share 40000

Total changes in the equity 40000 47350

6 Calculating and presenting financial ratios for organizational performance & investment

Ratio analysis may be served as a tool that helps in summarizing financial statements

of the firm in a structured way under different categories such as profitability, liquidity and

solvency (Cohen, Krishnamoorthy and Wright, 2017). Such technique is highly effectual

which in turn helps company and its stakeholders in assessing whether company’s

performance is improved or deteriorated over the time frame.

Ratio analysis of Sainsbury Plc for the year ended on

Particulars Formula 2016 2017

Profitability ratio

Gross profit 1456 1634

Net profit 471 377

Sales revenue 23506 26224

GP margin or ratio Gross profit / sales

revenue * 100

6.19% 6.23%

NP margin or ratio Net profit / sales

revenue * 100

2.00% 1.44%

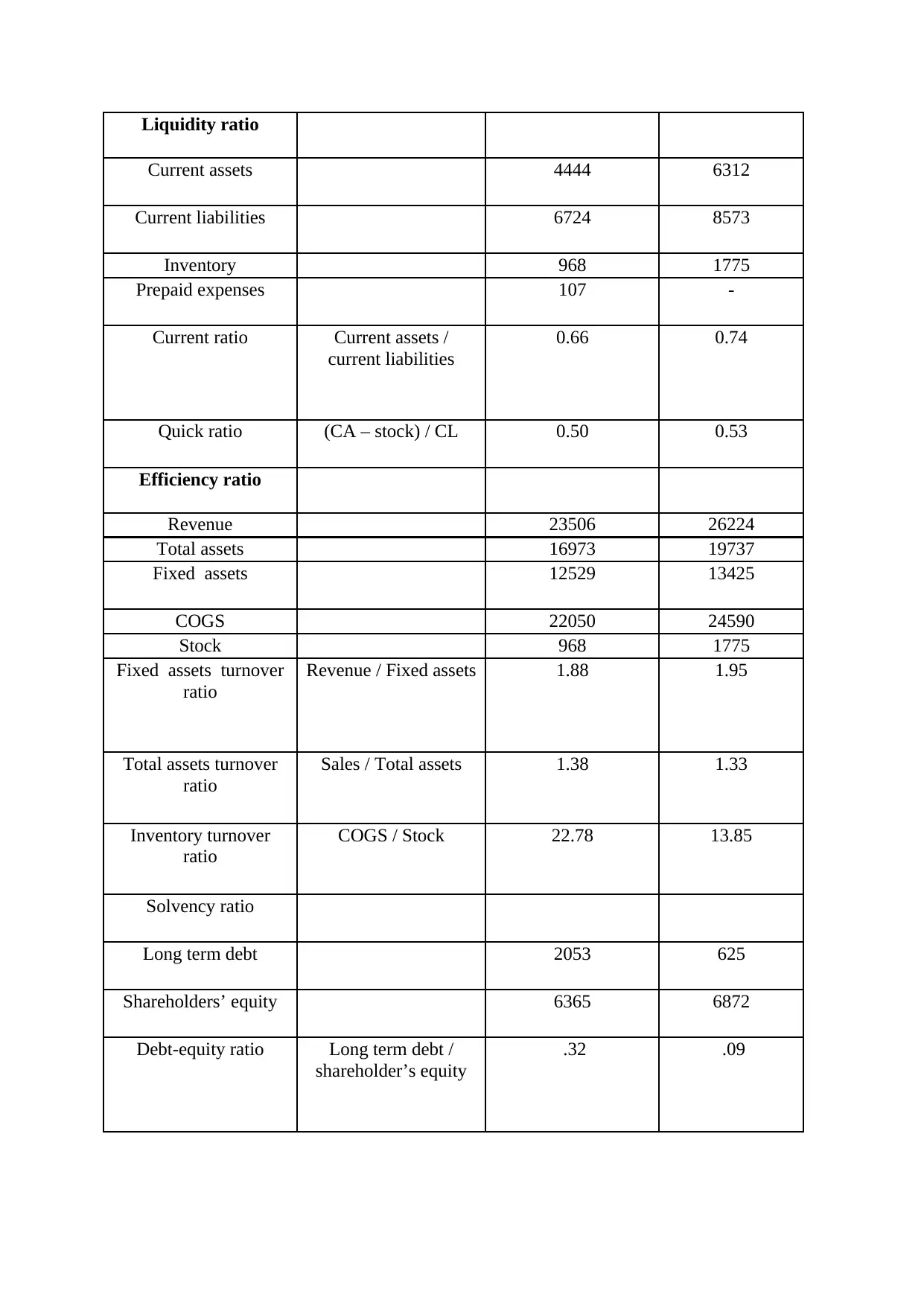

Liquidity ratio

Current assets 4444 6312

Current liabilities 6724 8573

Inventory 968 1775

Prepaid expenses 107 -

Current ratio Current assets /

current liabilities

0.66 0.74

Quick ratio (CA – stock) / CL 0.50 0.53

Efficiency ratio

Revenue 23506 26224

Total assets 16973 19737

Fixed assets 12529 13425

COGS 22050 24590

Stock 968 1775

Fixed assets turnover

ratio

Revenue / Fixed assets 1.88 1.95

Total assets turnover

ratio

Sales / Total assets 1.38 1.33

Inventory turnover

ratio

COGS / Stock 22.78 13.85

Solvency ratio

Long term debt 2053 625

Shareholders’ equity 6365 6872

Debt-equity ratio Long term debt /

shareholder’s equity

.32 .09

Current assets 4444 6312

Current liabilities 6724 8573

Inventory 968 1775

Prepaid expenses 107 -

Current ratio Current assets /

current liabilities

0.66 0.74

Quick ratio (CA – stock) / CL 0.50 0.53

Efficiency ratio

Revenue 23506 26224

Total assets 16973 19737

Fixed assets 12529 13425

COGS 22050 24590

Stock 968 1775

Fixed assets turnover

ratio

Revenue / Fixed assets 1.88 1.95

Total assets turnover

ratio

Sales / Total assets 1.38 1.33

Inventory turnover

ratio

COGS / Stock 22.78 13.85

Solvency ratio

Long term debt 2053 625

Shareholders’ equity 6365 6872

Debt-equity ratio Long term debt /

shareholder’s equity

.32 .09

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

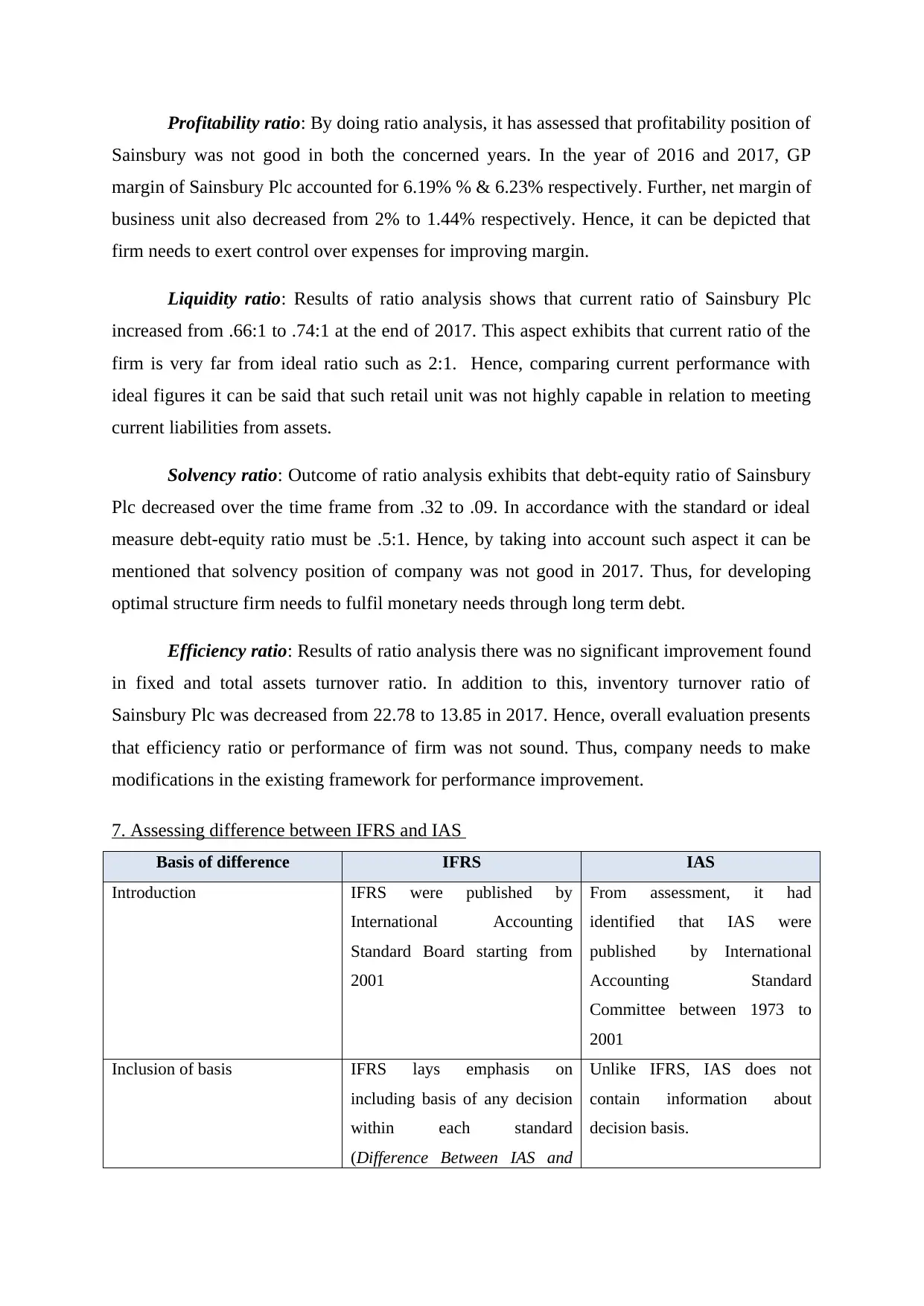

Profitability ratio: By doing ratio analysis, it has assessed that profitability position of

Sainsbury was not good in both the concerned years. In the year of 2016 and 2017, GP

margin of Sainsbury Plc accounted for 6.19% % & 6.23% respectively. Further, net margin of

business unit also decreased from 2% to 1.44% respectively. Hence, it can be depicted that

firm needs to exert control over expenses for improving margin.

Liquidity ratio: Results of ratio analysis shows that current ratio of Sainsbury Plc

increased from .66:1 to .74:1 at the end of 2017. This aspect exhibits that current ratio of the

firm is very far from ideal ratio such as 2:1. Hence, comparing current performance with

ideal figures it can be said that such retail unit was not highly capable in relation to meeting

current liabilities from assets.

Solvency ratio: Outcome of ratio analysis exhibits that debt-equity ratio of Sainsbury

Plc decreased over the time frame from .32 to .09. In accordance with the standard or ideal

measure debt-equity ratio must be .5:1. Hence, by taking into account such aspect it can be

mentioned that solvency position of company was not good in 2017. Thus, for developing

optimal structure firm needs to fulfil monetary needs through long term debt.

Efficiency ratio: Results of ratio analysis there was no significant improvement found

in fixed and total assets turnover ratio. In addition to this, inventory turnover ratio of

Sainsbury Plc was decreased from 22.78 to 13.85 in 2017. Hence, overall evaluation presents

that efficiency ratio or performance of firm was not sound. Thus, company needs to make

modifications in the existing framework for performance improvement.

7. Assessing difference between IFRS and IAS

Basis of difference IFRS IAS

Introduction IFRS were published by

International Accounting

Standard Board starting from

2001

From assessment, it had

identified that IAS were

published by International

Accounting Standard

Committee between 1973 to

2001

Inclusion of basis IFRS lays emphasis on

including basis of any decision

within each standard

(Difference Between IAS and

Unlike IFRS, IAS does not

contain information about

decision basis.

Sainsbury was not good in both the concerned years. In the year of 2016 and 2017, GP

margin of Sainsbury Plc accounted for 6.19% % & 6.23% respectively. Further, net margin of

business unit also decreased from 2% to 1.44% respectively. Hence, it can be depicted that

firm needs to exert control over expenses for improving margin.

Liquidity ratio: Results of ratio analysis shows that current ratio of Sainsbury Plc

increased from .66:1 to .74:1 at the end of 2017. This aspect exhibits that current ratio of the

firm is very far from ideal ratio such as 2:1. Hence, comparing current performance with

ideal figures it can be said that such retail unit was not highly capable in relation to meeting

current liabilities from assets.

Solvency ratio: Outcome of ratio analysis exhibits that debt-equity ratio of Sainsbury

Plc decreased over the time frame from .32 to .09. In accordance with the standard or ideal

measure debt-equity ratio must be .5:1. Hence, by taking into account such aspect it can be

mentioned that solvency position of company was not good in 2017. Thus, for developing

optimal structure firm needs to fulfil monetary needs through long term debt.

Efficiency ratio: Results of ratio analysis there was no significant improvement found

in fixed and total assets turnover ratio. In addition to this, inventory turnover ratio of

Sainsbury Plc was decreased from 22.78 to 13.85 in 2017. Hence, overall evaluation presents

that efficiency ratio or performance of firm was not sound. Thus, company needs to make

modifications in the existing framework for performance improvement.

7. Assessing difference between IFRS and IAS

Basis of difference IFRS IAS

Introduction IFRS were published by

International Accounting

Standard Board starting from

2001

From assessment, it had

identified that IAS were

published by International

Accounting Standard

Committee between 1973 to

2001

Inclusion of basis IFRS lays emphasis on

including basis of any decision

within each standard

(Difference Between IAS and

Unlike IFRS, IAS does not

contain information about

decision basis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IFRS, 2017).

Bold text entails Guiding principles in IFRS Compulsory elements of the

standard.

8. Explaining the benefits of international accounting standard and IFRS

From assessment, it has identified that international accounting standards and IFRS

offers benefit to both business organization as well as concerned stakeholders. Moreover,

both IAS & IFRS facilitates standardization and thereby help investors in making selection of

firm which in turn offering high returns (Hope, Thomas and Vyas, 2017). Along with this, in

the case of standardized accounting companies can evaluate its position in again to

competitors and become able to take appropriate decision. Both IAS and IFRS enhance

corporate governance and free flow of capital across the globe. Further, benefits of IFRS and

IAS are enumerated below:

IAS benefits

Investors-benefits: IAS and formats of financial statement simplify international

investment decision. Hence, companies that follow IAS and guidelines help

shareholders can make comparison of financial information regardless of company’s

origin.

Globally accepted: IAS is globally acceptable which in turn reduces the need of

preparing additional statements and thereby lead reduction in expenses (What Are the

Benefits of International Accounting Standards, 2018).

Benefits of IFRS

Transparency: IFRS brings transparency in relation to financial information by

increasing the level of international comparability and quality. It enables investor and

other participants to make appropriate informed decision.

Accountability: By doing evaluation, it has found that FRS increases or strengthens

accountability to the significant level. As, it reduces gap pertaining to information

which take place between providers of capital and people to whom financial

assistance is provided (Picker and et.al., 2016). In addition to this, IFRS also helps

regulator around the world and aid in effectual decision making.

Bold text entails Guiding principles in IFRS Compulsory elements of the

standard.

8. Explaining the benefits of international accounting standard and IFRS

From assessment, it has identified that international accounting standards and IFRS

offers benefit to both business organization as well as concerned stakeholders. Moreover,

both IAS & IFRS facilitates standardization and thereby help investors in making selection of

firm which in turn offering high returns (Hope, Thomas and Vyas, 2017). Along with this, in

the case of standardized accounting companies can evaluate its position in again to

competitors and become able to take appropriate decision. Both IAS and IFRS enhance

corporate governance and free flow of capital across the globe. Further, benefits of IFRS and

IAS are enumerated below:

IAS benefits

Investors-benefits: IAS and formats of financial statement simplify international

investment decision. Hence, companies that follow IAS and guidelines help

shareholders can make comparison of financial information regardless of company’s

origin.

Globally accepted: IAS is globally acceptable which in turn reduces the need of

preparing additional statements and thereby lead reduction in expenses (What Are the

Benefits of International Accounting Standards, 2018).

Benefits of IFRS

Transparency: IFRS brings transparency in relation to financial information by

increasing the level of international comparability and quality. It enables investor and

other participants to make appropriate informed decision.

Accountability: By doing evaluation, it has found that FRS increases or strengthens

accountability to the significant level. As, it reduces gap pertaining to information

which take place between providers of capital and people to whom financial

assistance is provided (Picker and et.al., 2016). In addition to this, IFRS also helps

regulator around the world and aid in effectual decision making.

Efficiency: International financial reporting standards enhance economic efficiency

to a great extent. Hence, IFRS provides high level of assistance to investors in

identifying opportunities as well as risks take place across the world and thereby leads

capital allocation. Along with this, standardized system also offers benefit to the firm

by reducing the level of international reporting costs.

However, on the critical note, it can be said that flexibility which is offered by IFRS to

the companies lead manipulation. Moreover, IFRS flexibility allows firm to include methods

which they want. This in turn enables them to shows desired level of results in financial

statement regarding revenue, profit etc (International Financial Reporting Standards -

Advantages & Disadvantages, 2018). Along with this, requirement pertaining to compliance

with IFRS also imposes issue in front of small business units as they require trained staff for

recording transaction according to the same.

9. Stating differences and importance of financial reporting across different countries

From evaluation, it has asserted that approximately 90 countries are complying with

the international financial reporting and accounting standards while preparing statements as

well as audit (Kim, Shi and Zhou, 2014). However, still gap takes place in the accounting

practices undertaken by organization across different countries. Moreover, United States and

other countries have not yet adopted IFRS. In US, GAAP is followed by business unit while

preparing statements and disclosing reports in relation to the same.

Importance of financial reporting in the context of international market is enumerated

below:

Comparability: Financial reporting aspects in accordance with IFRS ensure greater

comparability of statements. On the basis of such aspect, companies that undertake

similar standards for the preparation of financial statements can compare their

performance in against to each other more effectually. Hence, by considering the

results of evaluation concerned business units can develop competent strategic and

policy framework.

Assists in taking decision regarding merger & acquisition: Now, companies are

seeking for strategic partners, customers and suppliers in foreign market. Financial

reports help organization in getting monetary information about leading brands

(Warren, 2016). By considering financial reports, firm can take decision about merger

to a great extent. Hence, IFRS provides high level of assistance to investors in

identifying opportunities as well as risks take place across the world and thereby leads

capital allocation. Along with this, standardized system also offers benefit to the firm

by reducing the level of international reporting costs.

However, on the critical note, it can be said that flexibility which is offered by IFRS to

the companies lead manipulation. Moreover, IFRS flexibility allows firm to include methods

which they want. This in turn enables them to shows desired level of results in financial

statement regarding revenue, profit etc (International Financial Reporting Standards -

Advantages & Disadvantages, 2018). Along with this, requirement pertaining to compliance

with IFRS also imposes issue in front of small business units as they require trained staff for

recording transaction according to the same.

9. Stating differences and importance of financial reporting across different countries

From evaluation, it has asserted that approximately 90 countries are complying with

the international financial reporting and accounting standards while preparing statements as

well as audit (Kim, Shi and Zhou, 2014). However, still gap takes place in the accounting

practices undertaken by organization across different countries. Moreover, United States and

other countries have not yet adopted IFRS. In US, GAAP is followed by business unit while

preparing statements and disclosing reports in relation to the same.

Importance of financial reporting in the context of international market is enumerated

below:

Comparability: Financial reporting aspects in accordance with IFRS ensure greater

comparability of statements. On the basis of such aspect, companies that undertake

similar standards for the preparation of financial statements can compare their

performance in against to each other more effectually. Hence, by considering the

results of evaluation concerned business units can develop competent strategic and

policy framework.

Assists in taking decision regarding merger & acquisition: Now, companies are

seeking for strategic partners, customers and suppliers in foreign market. Financial

reports help organization in getting monetary information about leading brands

(Warren, 2016). By considering financial reports, firm can take decision about merger

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.