Financial Reporting: An Analysis of Standards and Stakeholders

VerifiedAdded on 2023/06/17

|21

|4370

|303

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, covering its context, purpose, and key principles within conceptual and regulatory frameworks. It examines the roles and benefits for main stakeholders, such as shareholders, professionals, investors, and suppliers, highlighting how financial reporting supports organizational objectives and growth. The report also differentiates between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), discussing degrees of compliance and factors influencing it across global organizations. Furthermore, it delves into the interpretation of financial statements, emphasizing the importance of relevance, materiality, and faithful representation in ensuring the reliability and applicability of accounting records for informed decision-making. This document is available on Desklib, a platform offering a wide range of study tools for students.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Outline the context and purpose of financial reporting..........................................................................3

Key principles of conceptual and regulatory frameworks, their purpose................................................4

Main stakeholders of an organisation and analyse how they benefit from financial information..........6

Value of financial reporting for meeting organizational objectives and growth......................................7

Difference between International Accounting Standards (IAS) and International Financial Reporting

Standards.................................................................................................................................................8

Degrees of compliance with IFRS by organisations across the world and the factors.............................9

Interpretation of Financial statements..................................................................................................11

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION...........................................................................................................................................3

MAIN BODY.................................................................................................................................................3

Outline the context and purpose of financial reporting..........................................................................3

Key principles of conceptual and regulatory frameworks, their purpose................................................4

Main stakeholders of an organisation and analyse how they benefit from financial information..........6

Value of financial reporting for meeting organizational objectives and growth......................................7

Difference between International Accounting Standards (IAS) and International Financial Reporting

Standards.................................................................................................................................................8

Degrees of compliance with IFRS by organisations across the world and the factors.............................9

Interpretation of Financial statements..................................................................................................11

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting is a discipline of bookkeeping that deals with the actions of documenting

financial events, bookkeeping and preparing and presenting income reports. The income

statement shows a company's current financial situation, as well as the results of various

activities, functional and work engagement, future revenues, comparisons, and other data.

Financial statements include a cash position, a statement of comprehensive income, a net

income, a statement of retained earnings, a statement of cash flow, and other pertinent

comments. Financial reporting's major goal is to provide necessary details about an individual's

statement of financial position, as well as important effect on financial circumstances, to a

variety of users to aid in great decision (Baker and Persson, 2021). Such a study analyzes the

description and intention of financial reporting, the abstract and regulatory framework for

financial reporting, the leadership of financial statements, important accounting fundamentals

and their intention and requirements, relevant parties and their necessity accounting information,

the statement of assets reportage for organizational growth and success and development and the

discrepancies between IAS and IFRS.

MAIN BODY

Outline the context and purpose of financial reporting.

Financial reporting is the structured reporting or appearance of financial results,

consequences, and associated documents to upper executives and internally or externally

interested parties (equity holders, distributors, shareholders, clients, regulatory authorities, and

others) about how a company organisation works over time. Adopting proper reporting methods

that aid in the achievement of corporate goals and targets is critical for a commercial entity. The

financial reporting of British American Tobacco informs investors, owners, as well as other

industry professionals well about firm's earnings, authenticity, feasibility of various ongoing

initiatives, and overall value. The firm may establish a basis for effective judgment and examine

its own performance indicators, liquidity situation, leveraging, and possible or current lifestyle

factors based on the outcomes of the financial reporting system (Mohamadi, 2020).

Financial reporting is a discipline of bookkeeping that deals with the actions of documenting

financial events, bookkeeping and preparing and presenting income reports. The income

statement shows a company's current financial situation, as well as the results of various

activities, functional and work engagement, future revenues, comparisons, and other data.

Financial statements include a cash position, a statement of comprehensive income, a net

income, a statement of retained earnings, a statement of cash flow, and other pertinent

comments. Financial reporting's major goal is to provide necessary details about an individual's

statement of financial position, as well as important effect on financial circumstances, to a

variety of users to aid in great decision (Baker and Persson, 2021). Such a study analyzes the

description and intention of financial reporting, the abstract and regulatory framework for

financial reporting, the leadership of financial statements, important accounting fundamentals

and their intention and requirements, relevant parties and their necessity accounting information,

the statement of assets reportage for organizational growth and success and development and the

discrepancies between IAS and IFRS.

MAIN BODY

Outline the context and purpose of financial reporting.

Financial reporting is the structured reporting or appearance of financial results,

consequences, and associated documents to upper executives and internally or externally

interested parties (equity holders, distributors, shareholders, clients, regulatory authorities, and

others) about how a company organisation works over time. Adopting proper reporting methods

that aid in the achievement of corporate goals and targets is critical for a commercial entity. The

financial reporting of British American Tobacco informs investors, owners, as well as other

industry professionals well about firm's earnings, authenticity, feasibility of various ongoing

initiatives, and overall value. The firm may establish a basis for effective judgment and examine

its own performance indicators, liquidity situation, leveraging, and possible or current lifestyle

factors based on the outcomes of the financial reporting system (Mohamadi, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Organizations like British American Tobacco are mandated by the International

Accounting Standard Board to follow all IAS and IFRS for compliance with accounting reasons

in order to achieve consistency and improve financial statement reliability. Financial reporting

guarantees that all required disclosures are made in order for final accounting to be transparent. It

also aids in the avoidance of financial statement window dressing and offers a genuine and

honest picture of the firm.

Purpose of financial reporting: The following are the major goals of financial reporting in the

United Kingdom:

• The primary objective of financial reporting is to review financial info about a disclosure

corporation that is important to prospective and current shareholders, depositors or lending

institutions, as well as other parties with a considerable interest in the reporting company in order

to make important financing and commodity judgments.

• It aids in identifying if numerous rules, rules, and guidelines are being followed.

• It holds shareholders, contributors, shareholders, and other users accountable.

• It aids in the development of an approach for evaluating an institution's real results and

compare it to its budget (Dameri, Garelli and Resta, 2020).

• Assisting British American Tobacco management in developing an adequate new strategy so

that the firm may accomplish desired revenues and profits and successfully compete in the

market edge.

Financial reporting aids in the budgeting process, which are necessary in order to determine

differences in achievement and allowing British American Tobacco to make decisions and

propose recommendations that will help decrease deviations in effectiveness in effort to match

the firm's goals and success objectives. The primary goal of financial reporting is to offer

accurate info about a company's operations and strategy so that users may make informed

decisions about the company for various purposes. On the influence of economic accounting,

investors make a variety of judgments, including lending, investment, taxation, and so on. The

financial report of Bruitish American Tobacco includes information on the company's activities,

financial status, and profitability.

Accounting Standard Board to follow all IAS and IFRS for compliance with accounting reasons

in order to achieve consistency and improve financial statement reliability. Financial reporting

guarantees that all required disclosures are made in order for final accounting to be transparent. It

also aids in the avoidance of financial statement window dressing and offers a genuine and

honest picture of the firm.

Purpose of financial reporting: The following are the major goals of financial reporting in the

United Kingdom:

• The primary objective of financial reporting is to review financial info about a disclosure

corporation that is important to prospective and current shareholders, depositors or lending

institutions, as well as other parties with a considerable interest in the reporting company in order

to make important financing and commodity judgments.

• It aids in identifying if numerous rules, rules, and guidelines are being followed.

• It holds shareholders, contributors, shareholders, and other users accountable.

• It aids in the development of an approach for evaluating an institution's real results and

compare it to its budget (Dameri, Garelli and Resta, 2020).

• Assisting British American Tobacco management in developing an adequate new strategy so

that the firm may accomplish desired revenues and profits and successfully compete in the

market edge.

Financial reporting aids in the budgeting process, which are necessary in order to determine

differences in achievement and allowing British American Tobacco to make decisions and

propose recommendations that will help decrease deviations in effectiveness in effort to match

the firm's goals and success objectives. The primary goal of financial reporting is to offer

accurate info about a company's operations and strategy so that users may make informed

decisions about the company for various purposes. On the influence of economic accounting,

investors make a variety of judgments, including lending, investment, taxation, and so on. The

financial report of Bruitish American Tobacco includes information on the company's activities,

financial status, and profitability.

Key principles of conceptual and regulatory frameworks, their purpose

The term "accounting regulatory framework" refers to a collection of regulations,

regulations, and procedures that must be followed while preparing financial statements. The use

of these principles and guidelines by commercial organizations facilitates the comparison of

accounting records. Accounting policies and generally accepted accounting principles are

essentially included in the Regulatory Framework of Accounting for Financial Reporting.

Various frameworks have been established to give a basis for creating accurate financial reports.

The Summaries of Standardized Accounting Practice (SSAP) and Financial Reporting

Requirements are the two fundamental regulations in the United Kingdom (IFRSs). These two

guidelines stress uniformity in the preparation of various statements for limited public businesses

(McVay and Szerwo, 2021). Worldwide Accounting Standards (IASs) and International

Financial Reporting Standards (IFRSs) have been established to ensure that big global

corporations' financial statements are consistent.

A conceptual framework is a collection of concepts that provide uniform or widely

recognized advice for launching innovative reporting methods in response to new and emerging

difficulties, as well as evaluating current practices. In 1989, the Worldwide Accounting

Standards Board presented its conceptual framework with the goal of regulating or governing

nationally and internationally requirements, as well as assisting accountants in understanding

requirements and providing solutions to difficulties that the benchmarks do not address. The

purpose of the conceptual framework is to assure global accounting equity and to make corporate

data more critical and accessible (Yeboah and Pais, 2021).

Key principles: The below are the essential principles of the conceptual and regulatory regime,

as well as financial reporting leadership:

• Relevance: IFRS and IAS compliance guarantees that investors and other judgement have

access to the right information. Significance in knowledge also aids in the development of

stakeholder trust.

• Materiality: The IASB adheres to the quantification principle since the absence or

misunderstanding of any important information might impact an investor's choice.

The term "accounting regulatory framework" refers to a collection of regulations,

regulations, and procedures that must be followed while preparing financial statements. The use

of these principles and guidelines by commercial organizations facilitates the comparison of

accounting records. Accounting policies and generally accepted accounting principles are

essentially included in the Regulatory Framework of Accounting for Financial Reporting.

Various frameworks have been established to give a basis for creating accurate financial reports.

The Summaries of Standardized Accounting Practice (SSAP) and Financial Reporting

Requirements are the two fundamental regulations in the United Kingdom (IFRSs). These two

guidelines stress uniformity in the preparation of various statements for limited public businesses

(McVay and Szerwo, 2021). Worldwide Accounting Standards (IASs) and International

Financial Reporting Standards (IFRSs) have been established to ensure that big global

corporations' financial statements are consistent.

A conceptual framework is a collection of concepts that provide uniform or widely

recognized advice for launching innovative reporting methods in response to new and emerging

difficulties, as well as evaluating current practices. In 1989, the Worldwide Accounting

Standards Board presented its conceptual framework with the goal of regulating or governing

nationally and internationally requirements, as well as assisting accountants in understanding

requirements and providing solutions to difficulties that the benchmarks do not address. The

purpose of the conceptual framework is to assure global accounting equity and to make corporate

data more critical and accessible (Yeboah and Pais, 2021).

Key principles: The below are the essential principles of the conceptual and regulatory regime,

as well as financial reporting leadership:

• Relevance: IFRS and IAS compliance guarantees that investors and other judgement have

access to the right information. Significance in knowledge also aids in the development of

stakeholder trust.

• Materiality: The IASB adheres to the quantification principle since the absence or

misunderstanding of any important information might impact an investor's choice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Studies to ensure in nature: it relates to the accuracy of data and disproves assumptions based

on past financial statement assessments.

• Information is substantial if removing or misconstruing it might impact user selections based

on the presented financial data.

• Predictive Value: The Board ensures that financial reports have predictive ability for judging

the company's efficiency in the near future by adopting certain criteria (Opare, Houqe and Van

Zijl, 2021).

Purpose of regulatory and conceptual framework:

The goal of regulation planning is quite particular: it is accountable for steering organizations in

the proper path, which aids in achieving British American Tobacco's mission and vision in the

long term. The basic goal of a regulatory framework is to monitor a firm's productivity so that

shareholders can make informed judgments about it. Certain objectives connected to

international rules are included in the administrative and conceptual framework so that

businesses may organise their operation smoothly.

Quality feature of financial information: There are some characteristics of financial

information that can assist businesses in making more trustworthy and productive decisions in

the future. There are a few characteristics of good financial data that are listed elsewhere here:

Relevance: It is critical for a company to keep track of real statistics so that it may be used to

evaluate its current growth and business status (Kian, Faghih and Amiri, 2021).

Faithful representation: This is one of the most important factors in gaining the trust of

participants including such debtors, lenders, and shareholders. This, on the other hand, can help

an organisation determine if it is in a favorable position and can gain lengthy benefits including a

greater interest rate on capital spending.

Main stakeholders of an organisation and analyse how they benefit from financial information

Individual people with only a major value or interest in a business corporation, such like

interests or funds, are the major interested in financial data and information. However, certain

prospective buyers are concerned well about business's forecasting activities and success.

Stakeholders are people, person, or categories of people who already are explicitly or implicitly

on past financial statement assessments.

• Information is substantial if removing or misconstruing it might impact user selections based

on the presented financial data.

• Predictive Value: The Board ensures that financial reports have predictive ability for judging

the company's efficiency in the near future by adopting certain criteria (Opare, Houqe and Van

Zijl, 2021).

Purpose of regulatory and conceptual framework:

The goal of regulation planning is quite particular: it is accountable for steering organizations in

the proper path, which aids in achieving British American Tobacco's mission and vision in the

long term. The basic goal of a regulatory framework is to monitor a firm's productivity so that

shareholders can make informed judgments about it. Certain objectives connected to

international rules are included in the administrative and conceptual framework so that

businesses may organise their operation smoothly.

Quality feature of financial information: There are some characteristics of financial

information that can assist businesses in making more trustworthy and productive decisions in

the future. There are a few characteristics of good financial data that are listed elsewhere here:

Relevance: It is critical for a company to keep track of real statistics so that it may be used to

evaluate its current growth and business status (Kian, Faghih and Amiri, 2021).

Faithful representation: This is one of the most important factors in gaining the trust of

participants including such debtors, lenders, and shareholders. This, on the other hand, can help

an organisation determine if it is in a favorable position and can gain lengthy benefits including a

greater interest rate on capital spending.

Main stakeholders of an organisation and analyse how they benefit from financial information

Individual people with only a major value or interest in a business corporation, such like

interests or funds, are the major interested in financial data and information. However, certain

prospective buyers are concerned well about business's forecasting activities and success.

Stakeholders are people, person, or categories of people who already are explicitly or implicitly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

concerned in a company's accomplishments, success, economic standing, or ongoing or possible

future. Ownership, board and senior, contractors, users, and investors are all main persons in

British American Tobacco. As mentioned, accounting reporting has a lot of key benefit for many

participants (Sonnerfeldt and Pontoppidan, 2020).

Internal stakeholder is any person or classes of people who are firm specific and so far have

promised to assist it, including senior executives, staff members, activists, and other workers.

The following is with these internal stakeholders and their advantages:

• Shareholders: Equity holders are the most significant people in British American Tobacco, with

a stake in the company represented by ordinary shares. Investor actions have a significant impact

on a firm's net value. Shares own a piece of the company's earnings or net earnings in the shape

of dividends and stock valuation.

• Professionals: Professionals at British American Tobacco can help the students to learn the

company's business accounting reports although it will encourage people in estimating their

upcoming results of the company and appraising their individual effectiveness.

External stakeholders: Different parties comprises buyers, financiers and contractors,

distributors, politicians and agencies, some of whom are not deeply associated with British

American Tobacco but are invested in or disturbed about just the organization's business,

accomplishments, statements, and financial circumstances. Below foregoing are just some of

them:

• Investors: Buyers buy securities focus on financial details offered by the business and acquire

an interest in the firm’s profitability as a condition of their contribution. Workers are indeed

interested in helping a corporation generate profits (Sentuti and et.al, 2020).

• Supplies: Sellers are a body of individuals who want effects on price and quantity estimates and

predictions. Competitive advantage arise supplier by delivering large volumes of their stock

items.

Value of financial reporting for meeting organizational objectives and growth

Financial reporting aids corporate companies in managing their total accounting and

financial processes in order to reach their goals and strategies. It establishes the basis for British

future. Ownership, board and senior, contractors, users, and investors are all main persons in

British American Tobacco. As mentioned, accounting reporting has a lot of key benefit for many

participants (Sonnerfeldt and Pontoppidan, 2020).

Internal stakeholder is any person or classes of people who are firm specific and so far have

promised to assist it, including senior executives, staff members, activists, and other workers.

The following is with these internal stakeholders and their advantages:

• Shareholders: Equity holders are the most significant people in British American Tobacco, with

a stake in the company represented by ordinary shares. Investor actions have a significant impact

on a firm's net value. Shares own a piece of the company's earnings or net earnings in the shape

of dividends and stock valuation.

• Professionals: Professionals at British American Tobacco can help the students to learn the

company's business accounting reports although it will encourage people in estimating their

upcoming results of the company and appraising their individual effectiveness.

External stakeholders: Different parties comprises buyers, financiers and contractors,

distributors, politicians and agencies, some of whom are not deeply associated with British

American Tobacco but are invested in or disturbed about just the organization's business,

accomplishments, statements, and financial circumstances. Below foregoing are just some of

them:

• Investors: Buyers buy securities focus on financial details offered by the business and acquire

an interest in the firm’s profitability as a condition of their contribution. Workers are indeed

interested in helping a corporation generate profits (Sentuti and et.al, 2020).

• Supplies: Sellers are a body of individuals who want effects on price and quantity estimates and

predictions. Competitive advantage arise supplier by delivering large volumes of their stock

items.

Value of financial reporting for meeting organizational objectives and growth

Financial reporting aids corporate companies in managing their total accounting and

financial processes in order to reach their goals and strategies. It establishes the basis for British

American Tobacco leadership to determine sound economic and financial decisions. By giving a

genuine image of the firm, financial reporting helps to create and maintain shareholder

confidence. Financial statements are used in the financial reporting to evaluate an organization's

overall profitability and market share. IAS and IFRS conformance is required for financial

statements, which improves the reliability and applicability of accounting records (Kartadjumena

and et.al, 2021). Businesses and consumers are critical to a corporation's growth and progress,

and the credibility of its financial statements entices them to contribute or pick it. British

American Tobacco's main aim is to persuade shareholders and consumers, as well as to increase

profit with enhancing productivity. Although all different stakeholders examine monetary data to

create choices, the accounting reporting offered by the company balance sheet serves to boost the

global brand prices and market share. BRITISH AMERICAN TOBACCO provides financial

statements for each income statement, allowing the company to compare one or even more

seasons' system and evaluate patterns.

Gaining a strategic advantage is aided by the company's future and brand recognition.

Accounting information that are accurate and useful assist a company in analyzing its general

development and market possibilities, as well as promoting the successful exploitation of

chances. The feasibility and performance of decisions made by a firm based on financial

statements created as part of the financial information disclosure assures the condition and

performance of those decisions that lead to growth and advancement. Organizations may easily

identify development prospects by employing corporate accounting data (Ertimur and et.al,

2020).

Difference between International Accounting Standards (IAS) and International Financial

Reporting Standards

IFRS (International Financial Reporting Standards): This was developed by the IASB that is

a global financial reporting body that was created to offer direction to businesses on how to

report activities in their accounting records. It is critical for all businesses to adhere to all

bookkeeping rules and requirements so that reports can be generated and presented to various

stakeholders so that they can make informed choices.

IAS (International Accounting Standards): All IAS requirements are imposed by the

International Accounting Standards Committee (IASC), which directs businesses on how to use

genuine image of the firm, financial reporting helps to create and maintain shareholder

confidence. Financial statements are used in the financial reporting to evaluate an organization's

overall profitability and market share. IAS and IFRS conformance is required for financial

statements, which improves the reliability and applicability of accounting records (Kartadjumena

and et.al, 2021). Businesses and consumers are critical to a corporation's growth and progress,

and the credibility of its financial statements entices them to contribute or pick it. British

American Tobacco's main aim is to persuade shareholders and consumers, as well as to increase

profit with enhancing productivity. Although all different stakeholders examine monetary data to

create choices, the accounting reporting offered by the company balance sheet serves to boost the

global brand prices and market share. BRITISH AMERICAN TOBACCO provides financial

statements for each income statement, allowing the company to compare one or even more

seasons' system and evaluate patterns.

Gaining a strategic advantage is aided by the company's future and brand recognition.

Accounting information that are accurate and useful assist a company in analyzing its general

development and market possibilities, as well as promoting the successful exploitation of

chances. The feasibility and performance of decisions made by a firm based on financial

statements created as part of the financial information disclosure assures the condition and

performance of those decisions that lead to growth and advancement. Organizations may easily

identify development prospects by employing corporate accounting data (Ertimur and et.al,

2020).

Difference between International Accounting Standards (IAS) and International Financial

Reporting Standards

IFRS (International Financial Reporting Standards): This was developed by the IASB that is

a global financial reporting body that was created to offer direction to businesses on how to

report activities in their accounting records. It is critical for all businesses to adhere to all

bookkeeping rules and requirements so that reports can be generated and presented to various

stakeholders so that they can make informed choices.

IAS (International Accounting Standards): All IAS requirements are imposed by the

International Accounting Standards Committee (IASC), which directs businesses on how to use

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial statements in their accounting processes. As a result, it aids in the recording of needed

data in financial statements (Gamayuni, 2020).

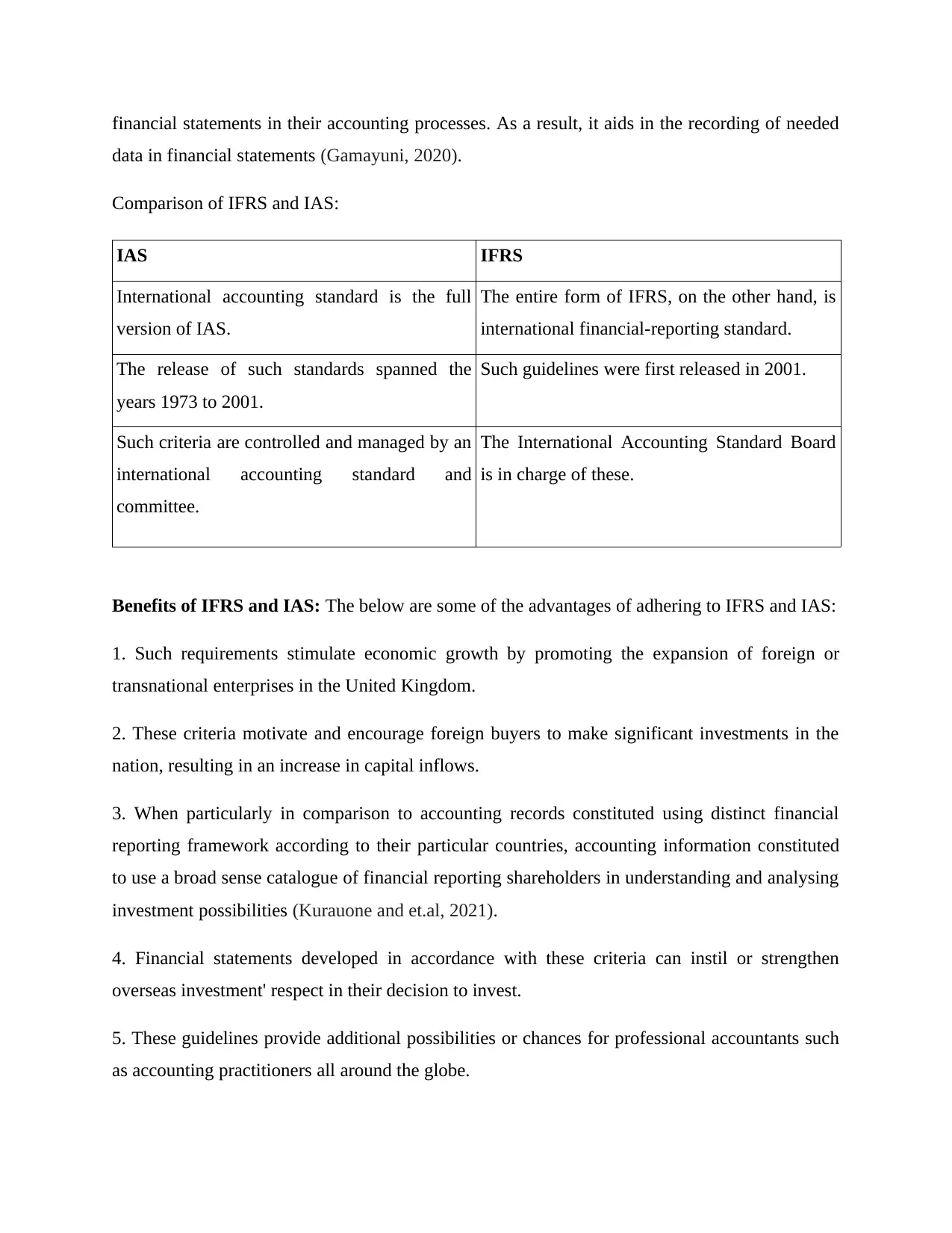

Comparison of IFRS and IAS:

IAS IFRS

International accounting standard is the full

version of IAS.

The entire form of IFRS, on the other hand, is

international financial-reporting standard.

The release of such standards spanned the

years 1973 to 2001.

Such guidelines were first released in 2001.

Such criteria are controlled and managed by an

international accounting standard and

committee.

The International Accounting Standard Board

is in charge of these.

Benefits of IFRS and IAS: The below are some of the advantages of adhering to IFRS and IAS:

1. Such requirements stimulate economic growth by promoting the expansion of foreign or

transnational enterprises in the United Kingdom.

2. These criteria motivate and encourage foreign buyers to make significant investments in the

nation, resulting in an increase in capital inflows.

3. When particularly in comparison to accounting records constituted using distinct financial

reporting framework according to their particular countries, accounting information constituted

to use a broad sense catalogue of financial reporting shareholders in understanding and analysing

investment possibilities (Kurauone and et.al, 2021).

4. Financial statements developed in accordance with these criteria can instil or strengthen

overseas investment' respect in their decision to invest.

5. These guidelines provide additional possibilities or chances for professional accountants such

as accounting practitioners all around the globe.

data in financial statements (Gamayuni, 2020).

Comparison of IFRS and IAS:

IAS IFRS

International accounting standard is the full

version of IAS.

The entire form of IFRS, on the other hand, is

international financial-reporting standard.

The release of such standards spanned the

years 1973 to 2001.

Such guidelines were first released in 2001.

Such criteria are controlled and managed by an

international accounting standard and

committee.

The International Accounting Standard Board

is in charge of these.

Benefits of IFRS and IAS: The below are some of the advantages of adhering to IFRS and IAS:

1. Such requirements stimulate economic growth by promoting the expansion of foreign or

transnational enterprises in the United Kingdom.

2. These criteria motivate and encourage foreign buyers to make significant investments in the

nation, resulting in an increase in capital inflows.

3. When particularly in comparison to accounting records constituted using distinct financial

reporting framework according to their particular countries, accounting information constituted

to use a broad sense catalogue of financial reporting shareholders in understanding and analysing

investment possibilities (Kurauone and et.al, 2021).

4. Financial statements developed in accordance with these criteria can instil or strengthen

overseas investment' respect in their decision to invest.

5. These guidelines provide additional possibilities or chances for professional accountants such

as accounting practitioners all around the globe.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Such criteria aid businesses in establishing benchmarks for themselves and gaining a success

in the international marketplace.

Degrees of compliance with IFRS by organisations across the world and the factors

International Financial Reporting Standards (IFRS) are developed by the Accounting

Standards Board to guarantee consistency in accounting and auditing, as well as to include a

prevalent or largely acknowledged vocabulary for commercial transactions at a world stage, so

that a company group's account holders are quickly readily available from various regions or

borders. Compliance with various IFRS is required for such industries or business organisations

that operate throughout international territories or borders. The upper and lower limits of these

standards may vary from one country to the next. Various regions have their own reporting

requirements. Because Marks & Spencer is an international corporation, adopting the accounting

norms and standards of the several countries in which it operates is difficult, hence IFRS are the

best option for consolidating its income reports. This standard also aids in attracting overseas

buyers to purchase shares (Whittington, 2020).

The main goal of the International Financial Reporting Standards (IFRS) is to provide

businesses with direction on how to frame financial statements in an effective and suitable

manner. Some of these guidelines aid in the analysis of the British American Tobacco group's

actual quality by combining financial statements from several businesses in various regions. IAS

were initially released by the IASB, however compliance with IAS has revealed a number of

complexity and challenges. So, in order to cope with all of these issues and complications, the

IASB created the International Financial Reporting Standards (IFRS). Some of the IAS are still

relevant to businesses. Businesses in the UK and other european countries employ GAAP, or

generally accepted accounting principles, whereas IFRS is used in over 110 countries across the

globe. The International Financial Reporting Standards (IFRS) are widely acknowledged by

world governments and regulatory agencies, necessitating their observance. Such rules are re-

commendatory rather than mandated in some nations; hence IFRS is used to preserve fairness in

presenting in such nations (Baidybekova and et.al, 2021).

Herein, the differences of financial reporting among some countries are mentioned below:

UK USA AUSTRALIA

in the international marketplace.

Degrees of compliance with IFRS by organisations across the world and the factors

International Financial Reporting Standards (IFRS) are developed by the Accounting

Standards Board to guarantee consistency in accounting and auditing, as well as to include a

prevalent or largely acknowledged vocabulary for commercial transactions at a world stage, so

that a company group's account holders are quickly readily available from various regions or

borders. Compliance with various IFRS is required for such industries or business organisations

that operate throughout international territories or borders. The upper and lower limits of these

standards may vary from one country to the next. Various regions have their own reporting

requirements. Because Marks & Spencer is an international corporation, adopting the accounting

norms and standards of the several countries in which it operates is difficult, hence IFRS are the

best option for consolidating its income reports. This standard also aids in attracting overseas

buyers to purchase shares (Whittington, 2020).

The main goal of the International Financial Reporting Standards (IFRS) is to provide

businesses with direction on how to frame financial statements in an effective and suitable

manner. Some of these guidelines aid in the analysis of the British American Tobacco group's

actual quality by combining financial statements from several businesses in various regions. IAS

were initially released by the IASB, however compliance with IAS has revealed a number of

complexity and challenges. So, in order to cope with all of these issues and complications, the

IASB created the International Financial Reporting Standards (IFRS). Some of the IAS are still

relevant to businesses. Businesses in the UK and other european countries employ GAAP, or

generally accepted accounting principles, whereas IFRS is used in over 110 countries across the

globe. The International Financial Reporting Standards (IFRS) are widely acknowledged by

world governments and regulatory agencies, necessitating their observance. Such rules are re-

commendatory rather than mandated in some nations; hence IFRS is used to preserve fairness in

presenting in such nations (Baidybekova and et.al, 2021).

Herein, the differences of financial reporting among some countries are mentioned below:

UK USA AUSTRALIA

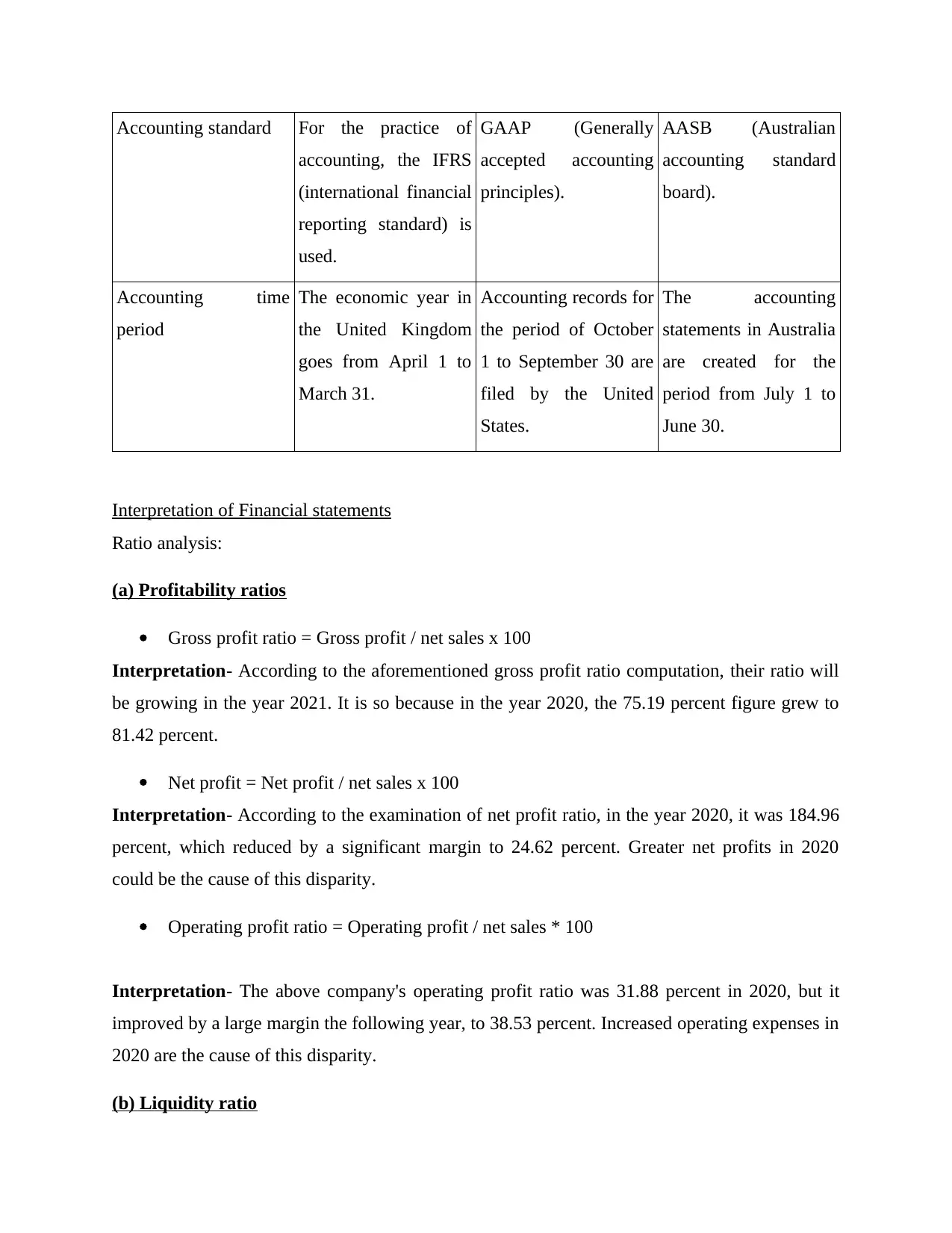

Accounting standard For the practice of

accounting, the IFRS

(international financial

reporting standard) is

used.

GAAP (Generally

accepted accounting

principles).

AASB (Australian

accounting standard

board).

Accounting time

period

The economic year in

the United Kingdom

goes from April 1 to

March 31.

Accounting records for

the period of October

1 to September 30 are

filed by the United

States.

The accounting

statements in Australia

are created for the

period from July 1 to

June 30.

Interpretation of Financial statements

Ratio analysis:

(a) Profitability ratios

Gross profit ratio = Gross profit / net sales x 100

Interpretation- According to the aforementioned gross profit ratio computation, their ratio will

be growing in the year 2021. It is so because in the year 2020, the 75.19 percent figure grew to

81.42 percent.

Net profit = Net profit / net sales x 100

Interpretation- According to the examination of net profit ratio, in the year 2020, it was 184.96

percent, which reduced by a significant margin to 24.62 percent. Greater net profits in 2020

could be the cause of this disparity.

Operating profit ratio = Operating profit / net sales * 100

Interpretation- The above company's operating profit ratio was 31.88 percent in 2020, but it

improved by a large margin the following year, to 38.53 percent. Increased operating expenses in

2020 are the cause of this disparity.

(b) Liquidity ratio

accounting, the IFRS

(international financial

reporting standard) is

used.

GAAP (Generally

accepted accounting

principles).

AASB (Australian

accounting standard

board).

Accounting time

period

The economic year in

the United Kingdom

goes from April 1 to

March 31.

Accounting records for

the period of October

1 to September 30 are

filed by the United

States.

The accounting

statements in Australia

are created for the

period from July 1 to

June 30.

Interpretation of Financial statements

Ratio analysis:

(a) Profitability ratios

Gross profit ratio = Gross profit / net sales x 100

Interpretation- According to the aforementioned gross profit ratio computation, their ratio will

be growing in the year 2021. It is so because in the year 2020, the 75.19 percent figure grew to

81.42 percent.

Net profit = Net profit / net sales x 100

Interpretation- According to the examination of net profit ratio, in the year 2020, it was 184.96

percent, which reduced by a significant margin to 24.62 percent. Greater net profits in 2020

could be the cause of this disparity.

Operating profit ratio = Operating profit / net sales * 100

Interpretation- The above company's operating profit ratio was 31.88 percent in 2020, but it

improved by a large margin the following year, to 38.53 percent. Increased operating expenses in

2020 are the cause of this disparity.

(b) Liquidity ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.