Financial Reporting Analysis: IAS, IFRS, and Stakeholder Impact

VerifiedAdded on 2020/12/10

|17

|3834

|440

Report

AI Summary

This report delves into the core concepts of financial reporting, examining its purpose, benefits, and the preparation of financial statements in accordance with IAS 1. It explores the conceptual and regulatory frameworks, including GAAP, IFRS, and IAS, and identifies the main stakeholders and how they benefit from financial reporting. The report evaluates the value of financial reporting in meeting business goals and objectives. It includes a comparative analysis of financial performance metrics for Marks and Spencer, and differentiates between IAS and IFRS, while assessing the benefits and compliance of IFRS. The report provides a comprehensive overview of financial reporting's role in providing crucial information for internal and external stakeholders, supporting decision-making, and ensuring regulatory compliance. The report concludes by summarizing the importance of financial reporting for all stakeholders.

Financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Defining the purpose and concept of Financial reporting.....................................................1

QUESTION 2..................................................................................................................................2

Examination of the conceptual and regulatory framework....................................................2

QUESTION 3...................................................................................................................................3

Identification of the main stakeholder of the organisation and how they are benefited from the

financial reporting..................................................................................................................3

QUESTION 4...................................................................................................................................4

Determination of the values of financial reporting for meeting the goals and objectives of the

business...................................................................................................................................4

QUESTION 5...................................................................................................................................5

Presentation of the financial statement as per IAS 1..............................................................5

QUESTION 6...................................................................................................................................8

Evaluation of the financial performance of Marks and Spencer...........................................8

QUESTION 7 ..................................................................................................................................9

Presetting the difference between IAS and IFRS...................................................................9

QUESTION 8.................................................................................................................................10

Evaluation of benefits of IFRS.............................................................................................10

QUESTION 9.................................................................................................................................11

Presenting the degree of compliance of IFRS.....................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Defining the purpose and concept of Financial reporting.....................................................1

QUESTION 2..................................................................................................................................2

Examination of the conceptual and regulatory framework....................................................2

QUESTION 3...................................................................................................................................3

Identification of the main stakeholder of the organisation and how they are benefited from the

financial reporting..................................................................................................................3

QUESTION 4...................................................................................................................................4

Determination of the values of financial reporting for meeting the goals and objectives of the

business...................................................................................................................................4

QUESTION 5...................................................................................................................................5

Presentation of the financial statement as per IAS 1..............................................................5

QUESTION 6...................................................................................................................................8

Evaluation of the financial performance of Marks and Spencer...........................................8

QUESTION 7 ..................................................................................................................................9

Presetting the difference between IAS and IFRS...................................................................9

QUESTION 8.................................................................................................................................10

Evaluation of benefits of IFRS.............................................................................................10

QUESTION 9.................................................................................................................................11

Presenting the degree of compliance of IFRS.....................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial reporting is a system that disclose all the financial information related with an

organization to its members and external stakeholder such as investors, shareholders, consumers

etc. Under reporting the documents that are displayed as reflective of the performance of the

business are financial statements and information related with the firm. In the preset report

concepts, benefits and manners of financial reporting are defined. The concept of presenting the

financial statement in accordance with international standard of accounting and reporting is

done. Importance and difference of various account standard are also presented in the report.

QUESTION 1

Defining the purpose and concept of Financial reporting

Financial reporting us a process of preparation and production of various statements that

present the and disclose the financial status and performance on an organisation. It plays a vital

role in the economic world. The main purpose of this is to provide the owners and management

of the organisation with useful, significant and relevant information related with financial

matters of the business. The financial reporting includes presentation of the financial statements

reflecting the overall performance of the firm to its directors and the owners in annual meeting

(Leuz and Wysocki, 2016). This is where all the stakeholders related with entity are addressed

and presented with the reporting. With this it is assessed by the directors and other effecting

parties as how well the investments has performed, what are the level of profitability and up to

what extent the organizational goals and objectives have achieved. The main purpose of the

reporting system to provide the all with classified data and information, those who are related

with the operations and performance of the business directly or indirectly.

Without reporting system the investors of the firm would show less interest in managing

investment in the business as they do not have a measure or way to monitors the efficiency in

the performance and determination of the fact that how the organisation is being run by the

directors. Financial reporting system works in the best interest of the company with providing

the significant information. In order to meet the requirements of those who uses the financial

statements the accounting system is needed to be applied which provide the information needed.

This system is needed to be monitored and regulated on the regulate basis into present

appropriate information to users. And this is achieved through a financial reporting system

framework. With this it can be stated that with financial reporting stem the organizations is

1

Financial reporting is a system that disclose all the financial information related with an

organization to its members and external stakeholder such as investors, shareholders, consumers

etc. Under reporting the documents that are displayed as reflective of the performance of the

business are financial statements and information related with the firm. In the preset report

concepts, benefits and manners of financial reporting are defined. The concept of presenting the

financial statement in accordance with international standard of accounting and reporting is

done. Importance and difference of various account standard are also presented in the report.

QUESTION 1

Defining the purpose and concept of Financial reporting

Financial reporting us a process of preparation and production of various statements that

present the and disclose the financial status and performance on an organisation. It plays a vital

role in the economic world. The main purpose of this is to provide the owners and management

of the organisation with useful, significant and relevant information related with financial

matters of the business. The financial reporting includes presentation of the financial statements

reflecting the overall performance of the firm to its directors and the owners in annual meeting

(Leuz and Wysocki, 2016). This is where all the stakeholders related with entity are addressed

and presented with the reporting. With this it is assessed by the directors and other effecting

parties as how well the investments has performed, what are the level of profitability and up to

what extent the organizational goals and objectives have achieved. The main purpose of the

reporting system to provide the all with classified data and information, those who are related

with the operations and performance of the business directly or indirectly.

Without reporting system the investors of the firm would show less interest in managing

investment in the business as they do not have a measure or way to monitors the efficiency in

the performance and determination of the fact that how the organisation is being run by the

directors. Financial reporting system works in the best interest of the company with providing

the significant information. In order to meet the requirements of those who uses the financial

statements the accounting system is needed to be applied which provide the information needed.

This system is needed to be monitored and regulated on the regulate basis into present

appropriate information to users. And this is achieved through a financial reporting system

framework. With this it can be stated that with financial reporting stem the organizations is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

presented with accurate facts, figures and evident proves regarding the performance of

organisation for a given time frame.

QUESTION 2

Examination of the conceptual and regulatory framework

It can be defined as the regulations and other principles that are mandatory to be

followed by a business while preparation of the financial statement and recording of the

monitory transactions relevant for a time period (Francis and et.al., 2015). The standards are

defined as GAAP, IFRS and IAS which are published by the regulatory authorities at

international level and organisation all over the globe are needed to be abide by these standards.

These are mandatory to be followed in order to bring a single regulatory framework and assisting

in easy comparison mechanism for evaluation of the performance. Some of the principles that are

need to be followed for recording of transaction as defines in GAAP, IFRS and IAS are:

Accrual basis: this principle states that all the organisation books a transaction in accrual

basis which means as and when it had been occurred. Not at the time when money is

either received or paid.

Monetary data: in this principle it is defined that only those transactions which have

some money value must be recorded in financial statement. All other activities and acts

of the firm are recorded in other reports related with the business.

Going concern: this principle states that a company continues to exit, long enough to

carry out its objective and commitments and will not liquidate in the foreseeable future.

Matching principle: these principles requires that for all the transaction books two

entries must be made one related with income and other related with expense. The

expenditure must match with the revenues of the firm for an accounting period.

Some of the basic principle of financial reporting are:

It shall set aims, objectives policy constrain and guidelines and strategy for the business

to attain the goals.

Defines significant indicators of the performance evaluation.

Periodically review the information receive to ensure that what it need has been received

and all the members of board understand it.

To ensure that the performance reporting process links objectives, principles and

practices.

2

organisation for a given time frame.

QUESTION 2

Examination of the conceptual and regulatory framework

It can be defined as the regulations and other principles that are mandatory to be

followed by a business while preparation of the financial statement and recording of the

monitory transactions relevant for a time period (Francis and et.al., 2015). The standards are

defined as GAAP, IFRS and IAS which are published by the regulatory authorities at

international level and organisation all over the globe are needed to be abide by these standards.

These are mandatory to be followed in order to bring a single regulatory framework and assisting

in easy comparison mechanism for evaluation of the performance. Some of the principles that are

need to be followed for recording of transaction as defines in GAAP, IFRS and IAS are:

Accrual basis: this principle states that all the organisation books a transaction in accrual

basis which means as and when it had been occurred. Not at the time when money is

either received or paid.

Monetary data: in this principle it is defined that only those transactions which have

some money value must be recorded in financial statement. All other activities and acts

of the firm are recorded in other reports related with the business.

Going concern: this principle states that a company continues to exit, long enough to

carry out its objective and commitments and will not liquidate in the foreseeable future.

Matching principle: these principles requires that for all the transaction books two

entries must be made one related with income and other related with expense. The

expenditure must match with the revenues of the firm for an accounting period.

Some of the basic principle of financial reporting are:

It shall set aims, objectives policy constrain and guidelines and strategy for the business

to attain the goals.

Defines significant indicators of the performance evaluation.

Periodically review the information receive to ensure that what it need has been received

and all the members of board understand it.

To ensure that the performance reporting process links objectives, principles and

practices.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qualitative characteristic of the financial information: It can be defined as the

reliability and authenticity of the information presented in the financial statements (Christensen

and et.al., 2015). In case a choice has to be made between relevant and reliable information it has

to be relevant one. The reliability of the information is determined, if:

It can be depended by the user to represent faithfully what is either significant to

symbolize or could reasonably expected to denote.

It is free from any deliberate partiality and material errors and it is complete in all

senses.

In case of its preparation under uncertainty a significant degree of caution have been

applied in exercising the required judgment.

QUESTION 3

Identification of the main stakeholder of the organisation and how they are benefited from the

financial reporting

Stakeholder of the organisation can be identified as internal and external. Internal one

includes those which are directly affected by the organizational operations that employees,

managers and owners of the firm. External stakeholders are one who are not linked with

operation of business but get affected by the business indirectly (Gordon and et.al., 2017). This

includes consumers, suppliers, local communities and government.

Impact on internal stakeholders: these are the ones who are in direct connection with

the operations and activities of the firm. With the financial reporting the exact performance of

the organisation is determined and these help in the planning and controlling of the future

activities of the firm. The managers are assisted in the decision making process as they are given

with exact assessment of the firm's position and performance. For the employees targets and

goals are set for better and effective achievement of the objective of business. the owners of the

firm knows that at what level their business is standing and what are the area that needs a

expansion or growth or the fields to cut short for attainment of the goals of the company.

Impact on external stakeholders: this is group of those individuals and organisation

that rely mostly on financial reports of a business to make their decision regarding the

investments or sales to the firm. The supplier evaluate the liquidity and solvency level of the

business to determine the ability of the firm from the financial report to pay the supplier for the

credit purchases from the suppliers. Stakeholders and other investor see the potential of the

3

reliability and authenticity of the information presented in the financial statements (Christensen

and et.al., 2015). In case a choice has to be made between relevant and reliable information it has

to be relevant one. The reliability of the information is determined, if:

It can be depended by the user to represent faithfully what is either significant to

symbolize or could reasonably expected to denote.

It is free from any deliberate partiality and material errors and it is complete in all

senses.

In case of its preparation under uncertainty a significant degree of caution have been

applied in exercising the required judgment.

QUESTION 3

Identification of the main stakeholder of the organisation and how they are benefited from the

financial reporting

Stakeholder of the organisation can be identified as internal and external. Internal one

includes those which are directly affected by the organizational operations that employees,

managers and owners of the firm. External stakeholders are one who are not linked with

operation of business but get affected by the business indirectly (Gordon and et.al., 2017). This

includes consumers, suppliers, local communities and government.

Impact on internal stakeholders: these are the ones who are in direct connection with

the operations and activities of the firm. With the financial reporting the exact performance of

the organisation is determined and these help in the planning and controlling of the future

activities of the firm. The managers are assisted in the decision making process as they are given

with exact assessment of the firm's position and performance. For the employees targets and

goals are set for better and effective achievement of the objective of business. the owners of the

firm knows that at what level their business is standing and what are the area that needs a

expansion or growth or the fields to cut short for attainment of the goals of the company.

Impact on external stakeholders: this is group of those individuals and organisation

that rely mostly on financial reports of a business to make their decision regarding the

investments or sales to the firm. The supplier evaluate the liquidity and solvency level of the

business to determine the ability of the firm from the financial report to pay the supplier for the

credit purchases from the suppliers. Stakeholders and other investor see the potential of the

3

company’s growth and value of the shares as they have made investment and the level of the

return that can be given by the business. Government and other agencies look into the matters

related with adherence with all the legal regulations and legislation that a firm is required to

follow.

QUESTION 4

Determination of the values of financial reporting for meeting the goals and objectives of the

business

The value of the financial reporting is of immense level for every organisation as it aids

the management of the business in meeting the goals and objectives of the firm effectively,

efficiently and timely. The value of this can be defined with following:

This reporting system provide information to the management that is useful in planning,

analyzing, bench marking and decision making process and with this organizational

operation are carried out precisely and this helps in attainment of the goals and

objectives.

With this the business process is monitored on a regular basis and this determined any

slowdown in the performance. Effective control system is applied for achievement of

the mission of firm.

Provide significant information to the outside stakeholders such as investors, consumers,

shareholders, government etc, and present the information related with the performance

of the business (Capkun, Collins and Jeanjean, 2016). This information assist them in

taking decision related with their interest in the organisation which result in increasing

reputation and involvement of stakeholders in the entity.

Provide information on how business procure and use the various financial and other

resources which helps the management to carry off this activaty in order to cut the cost

and expenses. Thus reducing cost of production and increasing the profitability which is

one of the primary goal of every organisation.

Provide information to the statutory auditors which facilitate audit this helps in

identification of any fraudulent activity or misrepresentation in the business operations.

Hence, assist the organisation to abide withal statutory legislation and regulation.

4

return that can be given by the business. Government and other agencies look into the matters

related with adherence with all the legal regulations and legislation that a firm is required to

follow.

QUESTION 4

Determination of the values of financial reporting for meeting the goals and objectives of the

business

The value of the financial reporting is of immense level for every organisation as it aids

the management of the business in meeting the goals and objectives of the firm effectively,

efficiently and timely. The value of this can be defined with following:

This reporting system provide information to the management that is useful in planning,

analyzing, bench marking and decision making process and with this organizational

operation are carried out precisely and this helps in attainment of the goals and

objectives.

With this the business process is monitored on a regular basis and this determined any

slowdown in the performance. Effective control system is applied for achievement of

the mission of firm.

Provide significant information to the outside stakeholders such as investors, consumers,

shareholders, government etc, and present the information related with the performance

of the business (Capkun, Collins and Jeanjean, 2016). This information assist them in

taking decision related with their interest in the organisation which result in increasing

reputation and involvement of stakeholders in the entity.

Provide information on how business procure and use the various financial and other

resources which helps the management to carry off this activaty in order to cut the cost

and expenses. Thus reducing cost of production and increasing the profitability which is

one of the primary goal of every organisation.

Provide information to the statutory auditors which facilitate audit this helps in

identification of any fraudulent activity or misrepresentation in the business operations.

Hence, assist the organisation to abide withal statutory legislation and regulation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

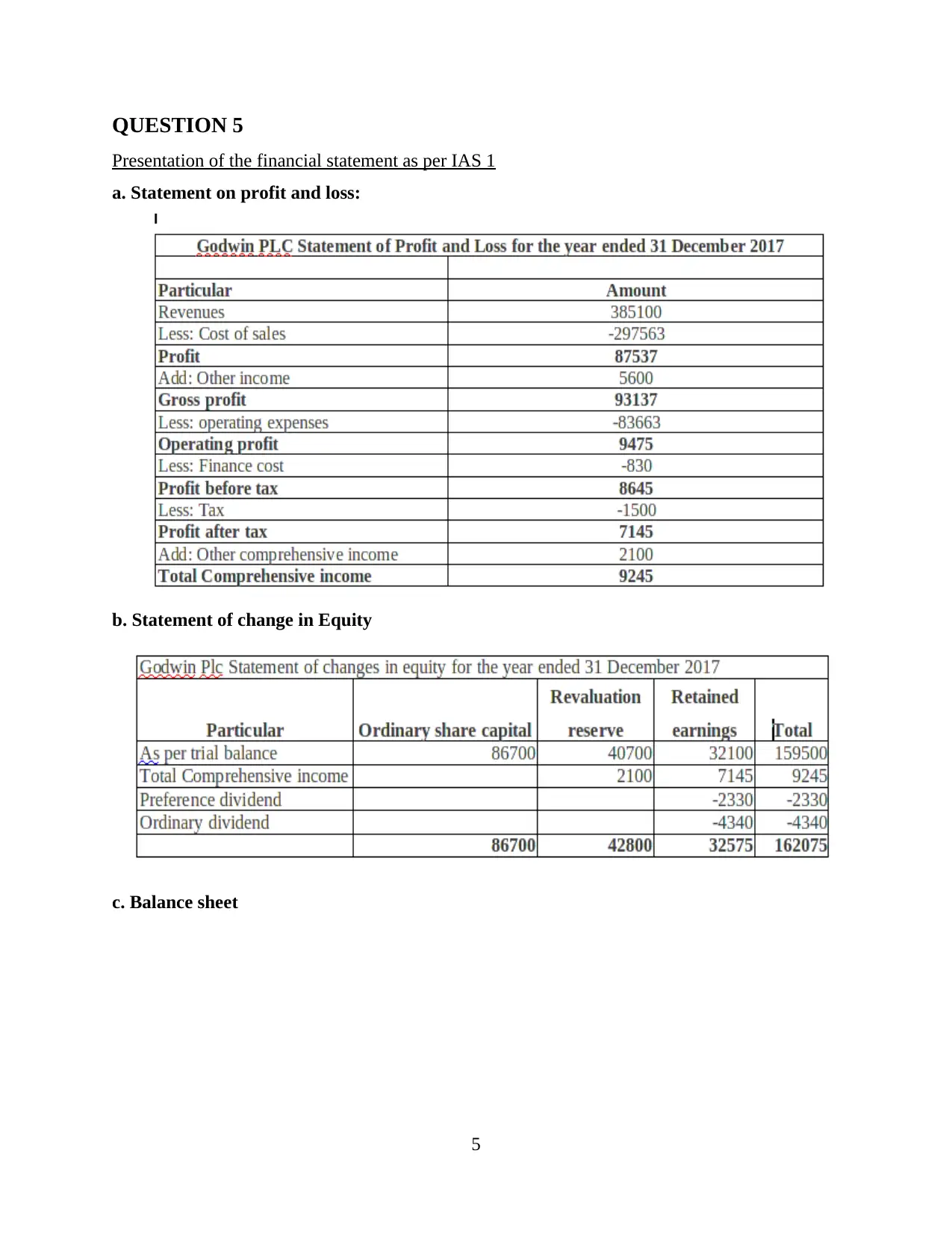

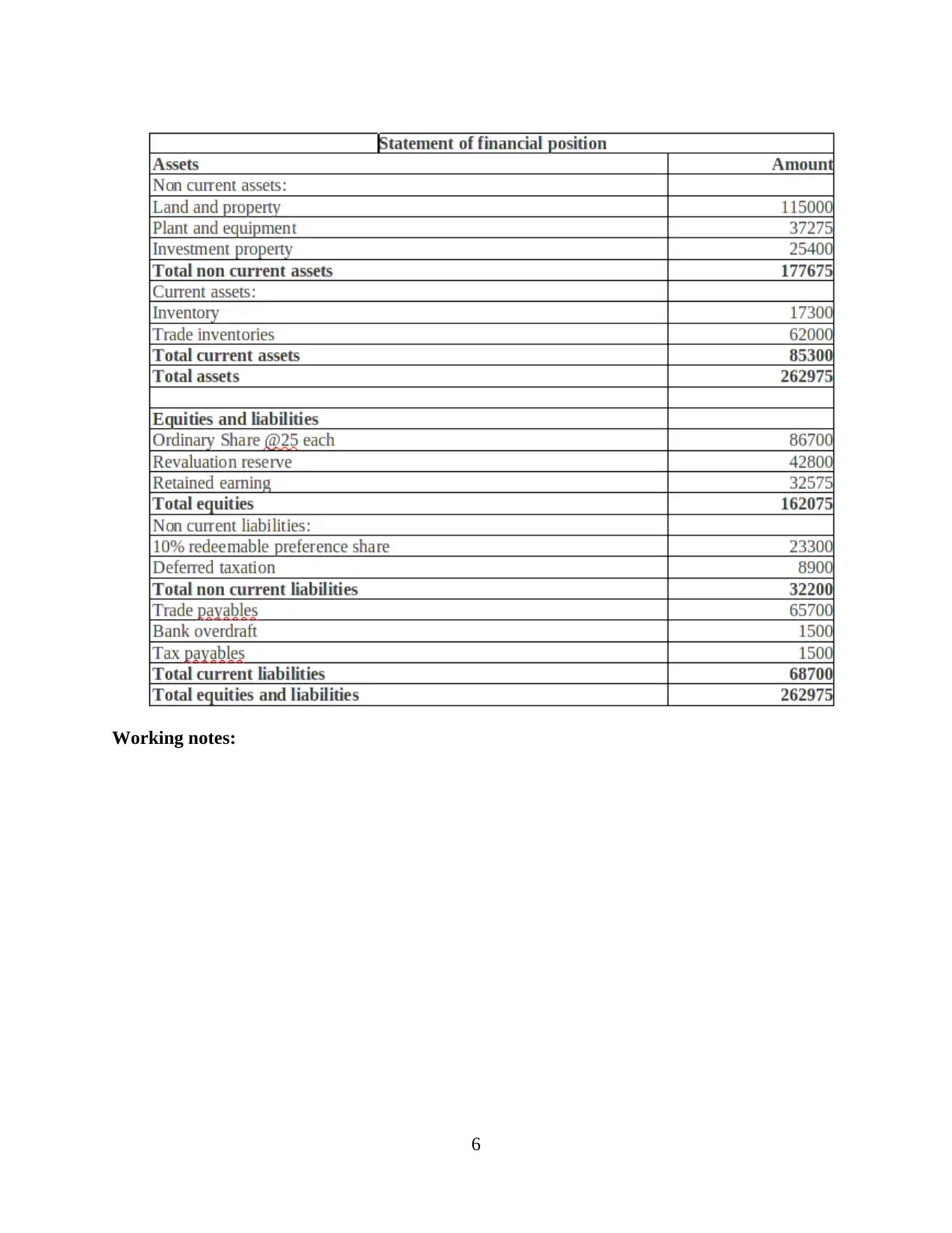

QUESTION 5

Presentation of the financial statement as per IAS 1

a. Statement on profit and loss:

b. Statement of change in Equity

c. Balance sheet

5

Presentation of the financial statement as per IAS 1

a. Statement on profit and loss:

b. Statement of change in Equity

c. Balance sheet

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

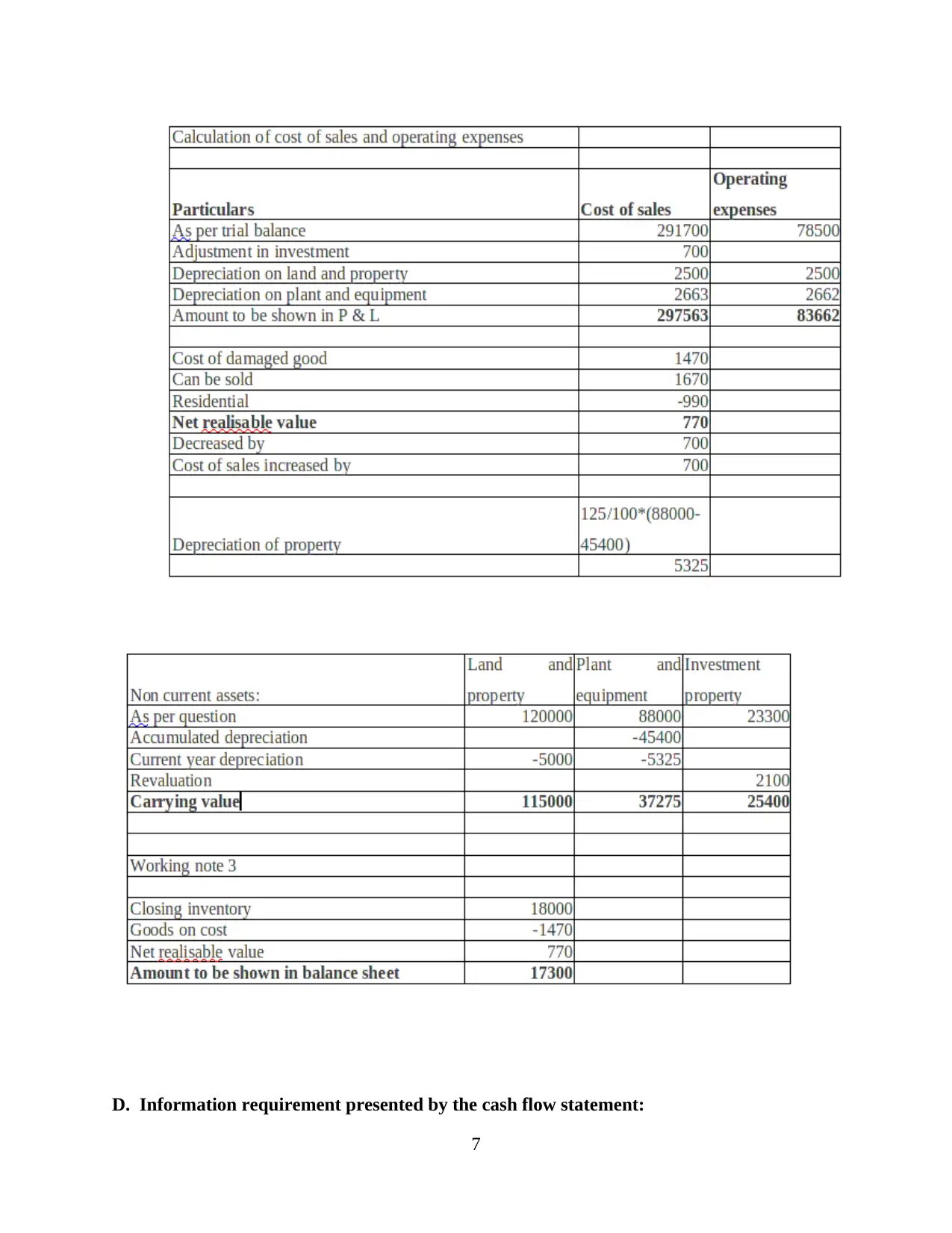

Working notes:

6

6

D. Information requirement presented by the cash flow statement:

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The profit and loss account and balance sheet present the cash flows of the organisation

in a period of 1 years. In the income statement data related with revenues generated and

expenses incurred for generating the profits are given (Edeigba and Amenkhienan, 2017). The

cash flow statement takes into consideration actual monetary translation the credit sales are not

considered in cash flow account. From the balance sheet the investment on the plant and

machinery and cash expenses are taken and the revenues in from id interest and buy back of the

share is consideration. The cash flow statement represent the actual cash outflow and inflow in

a year and at last what is amount of actual cash available with the organisation.

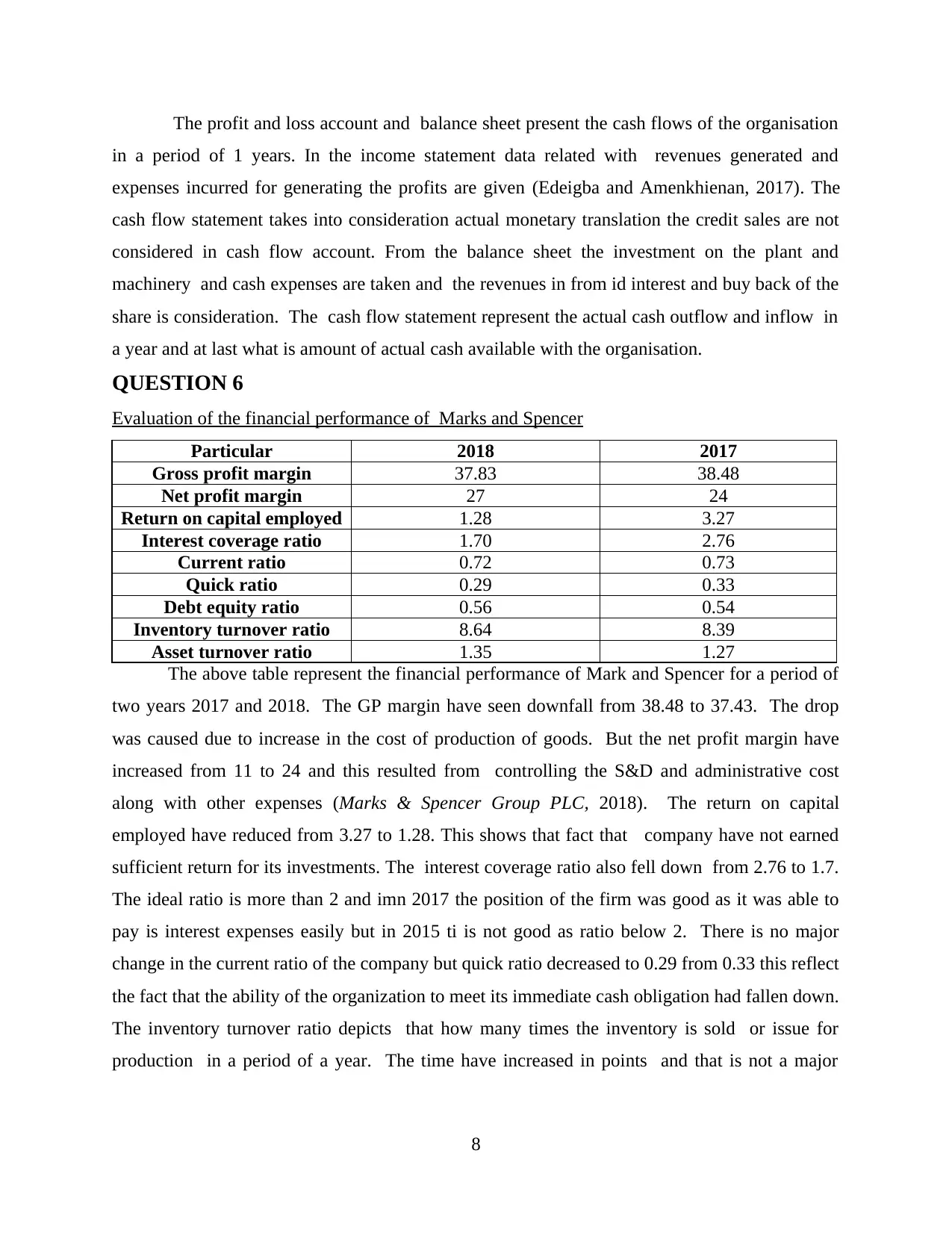

QUESTION 6

Evaluation of the financial performance of Marks and Spencer

Particular 2018 2017

Gross profit margin 37.83 38.48

Net profit margin 27 24

Return on capital employed 1.28 3.27

Interest coverage ratio 1.70 2.76

Current ratio 0.72 0.73

Quick ratio 0.29 0.33

Debt equity ratio 0.56 0.54

Inventory turnover ratio 8.64 8.39

Asset turnover ratio 1.35 1.27

The above table represent the financial performance of Mark and Spencer for a period of

two years 2017 and 2018. The GP margin have seen downfall from 38.48 to 37.43. The drop

was caused due to increase in the cost of production of goods. But the net profit margin have

increased from 11 to 24 and this resulted from controlling the S&D and administrative cost

along with other expenses (Marks & Spencer Group PLC, 2018). The return on capital

employed have reduced from 3.27 to 1.28. This shows that fact that company have not earned

sufficient return for its investments. The interest coverage ratio also fell down from 2.76 to 1.7.

The ideal ratio is more than 2 and imn 2017 the position of the firm was good as it was able to

pay is interest expenses easily but in 2015 ti is not good as ratio below 2. There is no major

change in the current ratio of the company but quick ratio decreased to 0.29 from 0.33 this reflect

the fact that the ability of the organization to meet its immediate cash obligation had fallen down.

The inventory turnover ratio depicts that how many times the inventory is sold or issue for

production in a period of a year. The time have increased in points and that is not a major

8

in a period of 1 years. In the income statement data related with revenues generated and

expenses incurred for generating the profits are given (Edeigba and Amenkhienan, 2017). The

cash flow statement takes into consideration actual monetary translation the credit sales are not

considered in cash flow account. From the balance sheet the investment on the plant and

machinery and cash expenses are taken and the revenues in from id interest and buy back of the

share is consideration. The cash flow statement represent the actual cash outflow and inflow in

a year and at last what is amount of actual cash available with the organisation.

QUESTION 6

Evaluation of the financial performance of Marks and Spencer

Particular 2018 2017

Gross profit margin 37.83 38.48

Net profit margin 27 24

Return on capital employed 1.28 3.27

Interest coverage ratio 1.70 2.76

Current ratio 0.72 0.73

Quick ratio 0.29 0.33

Debt equity ratio 0.56 0.54

Inventory turnover ratio 8.64 8.39

Asset turnover ratio 1.35 1.27

The above table represent the financial performance of Mark and Spencer for a period of

two years 2017 and 2018. The GP margin have seen downfall from 38.48 to 37.43. The drop

was caused due to increase in the cost of production of goods. But the net profit margin have

increased from 11 to 24 and this resulted from controlling the S&D and administrative cost

along with other expenses (Marks & Spencer Group PLC, 2018). The return on capital

employed have reduced from 3.27 to 1.28. This shows that fact that company have not earned

sufficient return for its investments. The interest coverage ratio also fell down from 2.76 to 1.7.

The ideal ratio is more than 2 and imn 2017 the position of the firm was good as it was able to

pay is interest expenses easily but in 2015 ti is not good as ratio below 2. There is no major

change in the current ratio of the company but quick ratio decreased to 0.29 from 0.33 this reflect

the fact that the ability of the organization to meet its immediate cash obligation had fallen down.

The inventory turnover ratio depicts that how many times the inventory is sold or issue for

production in a period of a year. The time have increased in points and that is not a major

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

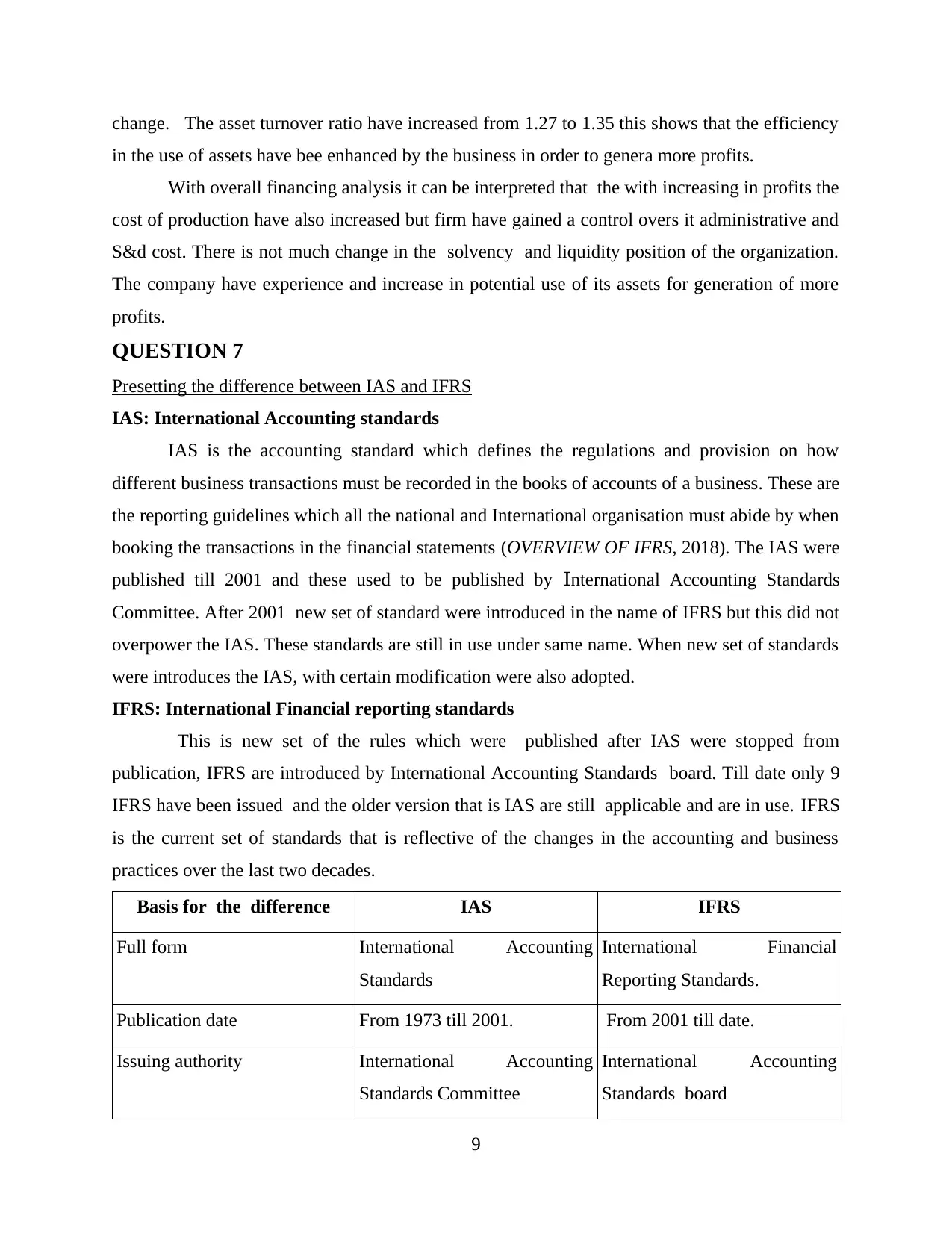

change. The asset turnover ratio have increased from 1.27 to 1.35 this shows that the efficiency

in the use of assets have bee enhanced by the business in order to genera more profits.

With overall financing analysis it can be interpreted that the with increasing in profits the

cost of production have also increased but firm have gained a control overs it administrative and

S&d cost. There is not much change in the solvency and liquidity position of the organization.

The company have experience and increase in potential use of its assets for generation of more

profits.

QUESTION 7

Presetting the difference between IAS and IFRS

IAS: International Accounting standards

IAS is the accounting standard which defines the regulations and provision on how

different business transactions must be recorded in the books of accounts of a business. These are

the reporting guidelines which all the national and International organisation must abide by when

booking the transactions in the financial statements (OVERVIEW OF IFRS, 2018). The IAS were

published till 2001 and these used to be published by International Accounting Standards

Committee. After 2001 new set of standard were introduced in the name of IFRS but this did not

overpower the IAS. These standards are still in use under same name. When new set of standards

were introduces the IAS, with certain modification were also adopted.

IFRS: International Financial reporting standards

This is new set of the rules which were published after IAS were stopped from

publication, IFRS are introduced by International Accounting Standards board. Till date only 9

IFRS have been issued and the older version that is IAS are still applicable and are in use. IFRS

is the current set of standards that is reflective of the changes in the accounting and business

practices over the last two decades.

Basis for the difference IAS IFRS

Full form International Accounting

Standards

International Financial

Reporting Standards.

Publication date From 1973 till 2001. From 2001 till date.

Issuing authority International Accounting

Standards Committee

International Accounting

Standards board

9

in the use of assets have bee enhanced by the business in order to genera more profits.

With overall financing analysis it can be interpreted that the with increasing in profits the

cost of production have also increased but firm have gained a control overs it administrative and

S&d cost. There is not much change in the solvency and liquidity position of the organization.

The company have experience and increase in potential use of its assets for generation of more

profits.

QUESTION 7

Presetting the difference between IAS and IFRS

IAS: International Accounting standards

IAS is the accounting standard which defines the regulations and provision on how

different business transactions must be recorded in the books of accounts of a business. These are

the reporting guidelines which all the national and International organisation must abide by when

booking the transactions in the financial statements (OVERVIEW OF IFRS, 2018). The IAS were

published till 2001 and these used to be published by International Accounting Standards

Committee. After 2001 new set of standard were introduced in the name of IFRS but this did not

overpower the IAS. These standards are still in use under same name. When new set of standards

were introduces the IAS, with certain modification were also adopted.

IFRS: International Financial reporting standards

This is new set of the rules which were published after IAS were stopped from

publication, IFRS are introduced by International Accounting Standards board. Till date only 9

IFRS have been issued and the older version that is IAS are still applicable and are in use. IFRS

is the current set of standards that is reflective of the changes in the accounting and business

practices over the last two decades.

Basis for the difference IAS IFRS

Full form International Accounting

Standards

International Financial

Reporting Standards.

Publication date From 1973 till 2001. From 2001 till date.

Issuing authority International Accounting

Standards Committee

International Accounting

Standards board

9

Rules of contradiction These are suppressed over

IFRS

These are given preference in

case on contradiction with

IAS.

This can be seen from the above table and explanation that IFRS is an updated version

of the IAS. Both are same and IFRS are presented with changed names and some changes. This

can be stated that old standards are presented in a newer form with significant changes and the

issuing body have also changed.

QUESTION 8

Evaluation of benefits of IFRS

The economy gets benefited with application of the IFRS by increasing the growth of the

international business of the country.

This ensure more presentation of financial statement accurately, on time and with

comprehension.

Assist small investors to make reporting standard with better and simpler quality.

Due to harmonization and standardization of reporting standards under IFRS, the

investors do not need to pay for processing and adjusting the financial statement and this

cuts shots the expanses of the analysis.

One of the key feature of IFRS is recognition of the loss on time which benefits not only

the investors but also the stakeholder and lenders (Compliance with IAS/IFRS, 2018).

With IFRS application, transparency have increased and lenders are given with clear

information related with financial position of the company and its ability to pay the

mortgages and loans taken.

This is applicable in all over EU to all the member nation, hence provide a significant

Platform for comparing the financial performance of the organization from different

nations and regions.

This aids in standardization of the financial reporting which improve comparability

removes barriers.

This improves the constancy and transparency of the financial reporting that enhances

the relationship between investors and other members of the company.

10

IFRS

These are given preference in

case on contradiction with

IAS.

This can be seen from the above table and explanation that IFRS is an updated version

of the IAS. Both are same and IFRS are presented with changed names and some changes. This

can be stated that old standards are presented in a newer form with significant changes and the

issuing body have also changed.

QUESTION 8

Evaluation of benefits of IFRS

The economy gets benefited with application of the IFRS by increasing the growth of the

international business of the country.

This ensure more presentation of financial statement accurately, on time and with

comprehension.

Assist small investors to make reporting standard with better and simpler quality.

Due to harmonization and standardization of reporting standards under IFRS, the

investors do not need to pay for processing and adjusting the financial statement and this

cuts shots the expanses of the analysis.

One of the key feature of IFRS is recognition of the loss on time which benefits not only

the investors but also the stakeholder and lenders (Compliance with IAS/IFRS, 2018).

With IFRS application, transparency have increased and lenders are given with clear

information related with financial position of the company and its ability to pay the

mortgages and loans taken.

This is applicable in all over EU to all the member nation, hence provide a significant

Platform for comparing the financial performance of the organization from different

nations and regions.

This aids in standardization of the financial reporting which improve comparability

removes barriers.

This improves the constancy and transparency of the financial reporting that enhances

the relationship between investors and other members of the company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.