Comprehensive Analysis of Financial Reporting: Standards and Practices

VerifiedAdded on 2020/12/09

|17

|3775

|188

Report

AI Summary

This report provides a detailed overview of financial reporting, encompassing its purpose, the context within which it operates, and the regulatory and conceptual frameworks that underpin it. It identifies key stakeholders and elucidates the advantages of financial information for each group, emphasizing its role in achieving organizational growth and objectives. The report delves into the presentation of financial statements, adhering to IAS 1, and offers insights into the information conveyed by cash flow statements and balance sheets. It further explores the interpretation and calculation of financial ratios to assess financial performance, differentiates between International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS), and evaluates the advantages of IFRS. Additionally, the report examines the degree of IFRS compliance globally, considering factors that impact compliance. The report concludes with a comprehensive analysis of financial reporting principles and practices.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................1

1. Purpose and context of financial reporting..............................................................................1

2. Regulatory and conceptual framework with its qualitative characteristics.............................2

3. Determining stakeholders of organization with its advantages through financial information.

.....................................................................................................................................................3

4. Examining importance of financial reporting for accomplishing organizational growth and

objectives.....................................................................................................................................5

5. Presenting financial statements according to IAS 1................................................................5

(d) explaining the information that cash flow and balance sheet is providing............................7

6. Explaining and interpreting financial performance.................................................................7

7. Explaining differences among International financial Reporting standards and International

Accounting Standards................................................................................................................10

8. Evaluating advantages of IFRS.............................................................................................11

9. Determining degrees of compliance with IFRS across world along with factors which gives

direct impact to compliance.......................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

TABLE OF CONTENTS..............................................................................................................2

INTRODUCTION...........................................................................................................................1

1. Purpose and context of financial reporting..............................................................................1

2. Regulatory and conceptual framework with its qualitative characteristics.............................2

3. Determining stakeholders of organization with its advantages through financial information.

.....................................................................................................................................................3

4. Examining importance of financial reporting for accomplishing organizational growth and

objectives.....................................................................................................................................5

5. Presenting financial statements according to IAS 1................................................................5

(d) explaining the information that cash flow and balance sheet is providing............................7

6. Explaining and interpreting financial performance.................................................................7

7. Explaining differences among International financial Reporting standards and International

Accounting Standards................................................................................................................10

8. Evaluating advantages of IFRS.............................................................................................11

9. Determining degrees of compliance with IFRS across world along with factors which gives

direct impact to compliance.......................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial reporting is considered as process of framing statements which directly

discloses about financial status to investors, government and management about business entity.

The present report will discuss about context and purpose of financial reporting along with

conceptual and regulatory framework along with qualitative characteristics. There will be

determination of main stakeholders of business organization with importance of financial

reporting to growth and organizational objectives. In the similar aspect, it will articulate

statements of profit and loss, changes in equity and financial statements. There will be

interpretation and calculation of financial ratios along with benefits to International financial

reporting standards.

1. Purpose and context of financial reporting

Financial reporting engages appropriate disclosure of financial information to public and

management where business entity id directly performing over specific duration. In the similar

aspect, financial reporting is directly issued on yearly or quarterly aspect as it is not similar to

management reporting where disclosure of financial information inside the business entity for

creating decisions with reference to business entity. The financial reports are directly considered

in annual report of public company. The financial reporting has served for two initial objective as

it helps management for involving in effective decision making which directly concerns with

objective of company along with overall strategies. The disclosure of data in reports helps

management to directly discern with weaknesses and strengths of business entity with its overall

financial health. In the same series, it gives vital information on basis of financial activities and

health of organization to its stakeholders as it comprises shareholders, consumers, government

regulators and potential investors (Stubbs and Higgins, 2018).

It is considered as mean for ensuring that company is operating in appropriate aspect. The

absence of reporting system the investors must be less inclined to contribute with its capital and

no method for monitoring that how effective company performs with directors, the appointed

steward of business are directly supposed to operate with the best interests and stakeholders as

well. The requirements of accomplishing users of financial statements the organization has to

directly implement accounting systems for giving required information. Furthermore, it is very

important that regulations of systems helps for ensuring about provided information to users in

Financial reporting is considered as process of framing statements which directly

discloses about financial status to investors, government and management about business entity.

The present report will discuss about context and purpose of financial reporting along with

conceptual and regulatory framework along with qualitative characteristics. There will be

determination of main stakeholders of business organization with importance of financial

reporting to growth and organizational objectives. In the similar aspect, it will articulate

statements of profit and loss, changes in equity and financial statements. There will be

interpretation and calculation of financial ratios along with benefits to International financial

reporting standards.

1. Purpose and context of financial reporting

Financial reporting engages appropriate disclosure of financial information to public and

management where business entity id directly performing over specific duration. In the similar

aspect, financial reporting is directly issued on yearly or quarterly aspect as it is not similar to

management reporting where disclosure of financial information inside the business entity for

creating decisions with reference to business entity. The financial reports are directly considered

in annual report of public company. The financial reporting has served for two initial objective as

it helps management for involving in effective decision making which directly concerns with

objective of company along with overall strategies. The disclosure of data in reports helps

management to directly discern with weaknesses and strengths of business entity with its overall

financial health. In the same series, it gives vital information on basis of financial activities and

health of organization to its stakeholders as it comprises shareholders, consumers, government

regulators and potential investors (Stubbs and Higgins, 2018).

It is considered as mean for ensuring that company is operating in appropriate aspect. The

absence of reporting system the investors must be less inclined to contribute with its capital and

no method for monitoring that how effective company performs with directors, the appointed

steward of business are directly supposed to operate with the best interests and stakeholders as

well. The requirements of accomplishing users of financial statements the organization has to

directly implement accounting systems for giving required information. Furthermore, it is very

important that regulations of systems helps for ensuring about provided information to users in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

proper format which is highly useful about required information. As, it could be attained via

framework of financial reporting on basis of conceptual framework.

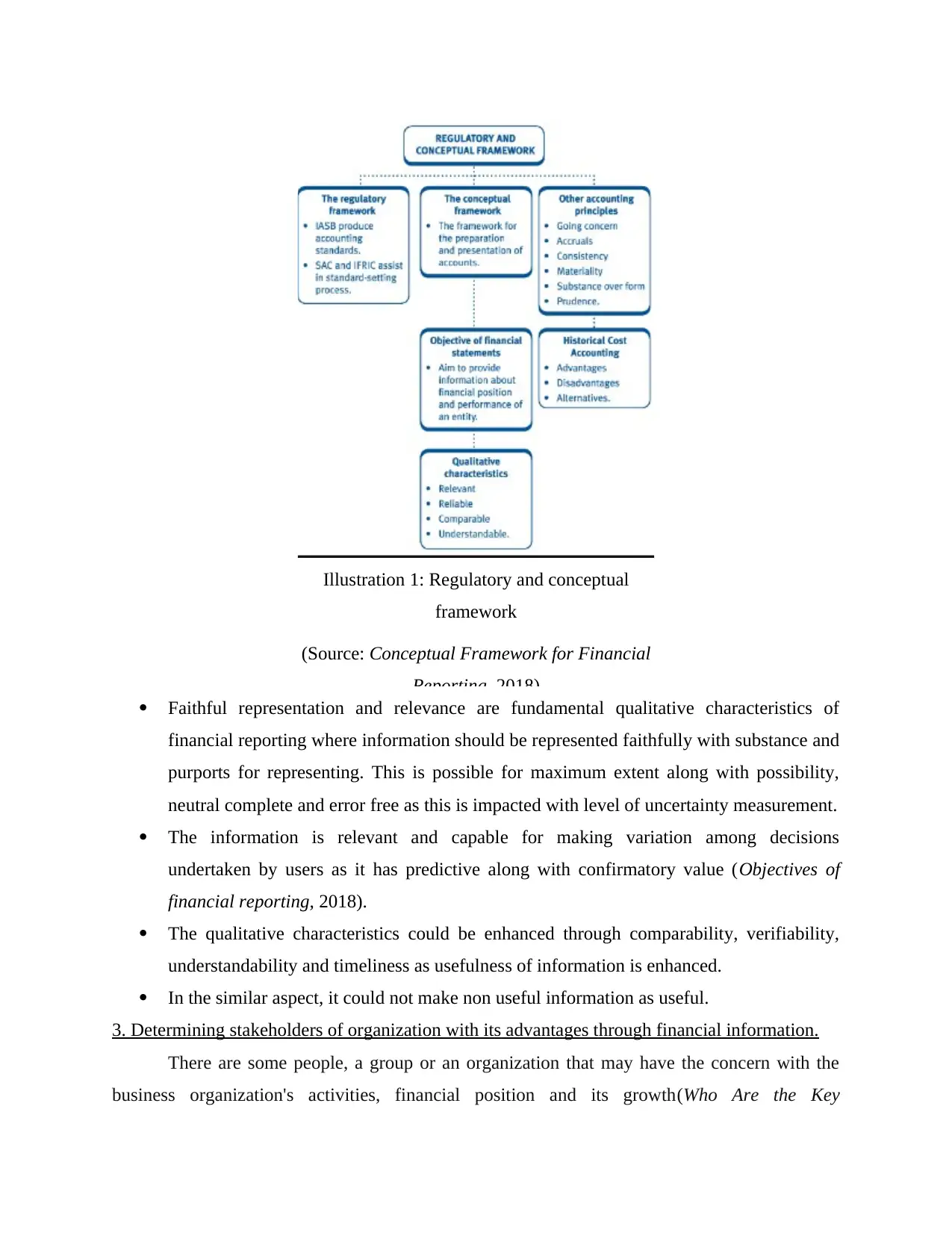

2. Regulatory and conceptual framework with its qualitative characteristics

The conceptual framework of financial reporting has been directly underpinned for

purpose of preparation of financial statements. It represented main concepts, ideas and principles

on basis of international financial reporting standards and financial statements as well. It

considers full discussion about its qualitative characteristics, objectives, accrual and going

concern concepts. In the similar aspect, it will be defining, measuring and recognising elements

with construction of financial statements and concepts of capital along with capital maintenance.

The regulatory framework for purpose of preparing financial statements which is mandatory for

numerous reasons as it ensures about needs of financial statements users for accomplishing with

the least information. It will ensure about given information in relevant economic arena which is

consistent and comparable. With context of given growth, the global investments and

multinational organizations are raising as behaviours of companies will regulate along with

directors towards investors. Further, elements of regulatory environment of accounting has

numerous elements as typical regulatory structure considers National financial reporting

standards, Market regulations, National law and Security exchange rules. The qualitative

characteristics of financial information are stated below:

framework of financial reporting on basis of conceptual framework.

2. Regulatory and conceptual framework with its qualitative characteristics

The conceptual framework of financial reporting has been directly underpinned for

purpose of preparation of financial statements. It represented main concepts, ideas and principles

on basis of international financial reporting standards and financial statements as well. It

considers full discussion about its qualitative characteristics, objectives, accrual and going

concern concepts. In the similar aspect, it will be defining, measuring and recognising elements

with construction of financial statements and concepts of capital along with capital maintenance.

The regulatory framework for purpose of preparing financial statements which is mandatory for

numerous reasons as it ensures about needs of financial statements users for accomplishing with

the least information. It will ensure about given information in relevant economic arena which is

consistent and comparable. With context of given growth, the global investments and

multinational organizations are raising as behaviours of companies will regulate along with

directors towards investors. Further, elements of regulatory environment of accounting has

numerous elements as typical regulatory structure considers National financial reporting

standards, Market regulations, National law and Security exchange rules. The qualitative

characteristics of financial information are stated below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 1: Regulatory and conceptual

framework

(Source: Conceptual Framework for Financial

Reporting, 2018)

Faithful representation and relevance are fundamental qualitative characteristics of

financial reporting where information should be represented faithfully with substance and

purports for representing. This is possible for maximum extent along with possibility,

neutral complete and error free as this is impacted with level of uncertainty measurement.

The information is relevant and capable for making variation among decisions

undertaken by users as it has predictive along with confirmatory value (Objectives of

financial reporting, 2018).

The qualitative characteristics could be enhanced through comparability, verifiability,

understandability and timeliness as usefulness of information is enhanced.

In the similar aspect, it could not make non useful information as useful.

3. Determining stakeholders of organization with its advantages through financial information.

There are some people, a group or an organization that may have the concern with the

business organization's activities, financial position and its growth(Who Are the Key

framework

(Source: Conceptual Framework for Financial

Reporting, 2018)

Faithful representation and relevance are fundamental qualitative characteristics of

financial reporting where information should be represented faithfully with substance and

purports for representing. This is possible for maximum extent along with possibility,

neutral complete and error free as this is impacted with level of uncertainty measurement.

The information is relevant and capable for making variation among decisions

undertaken by users as it has predictive along with confirmatory value (Objectives of

financial reporting, 2018).

The qualitative characteristics could be enhanced through comparability, verifiability,

understandability and timeliness as usefulness of information is enhanced.

In the similar aspect, it could not make non useful information as useful.

3. Determining stakeholders of organization with its advantages through financial information.

There are some people, a group or an organization that may have the concern with the

business organization's activities, financial position and its growth(Who Are the Key

Stakeholders in an Organization? ,2018). They are known as stakeholder which are connected

with the business organization. Stakeholder of an organization can be the shareholder, investors,

employees, customer and suppliers. They are an essential element of the company as they can

influence the companies activities and they can also be affected either the companies activities.

Financial information is an important source of getting about the activities of organization.

Following are some benefits of the financial information to the stakeholder:

Shareholders: They are the one who invested their money in company in order to get a

return from the company's revenue. They expect a good return of profit from the

company. Financial information is beneficial for the shareholder in getting a proper

knowledge of the company's financial postilion (Who Are the Stakeholders Relative to an

Organization? ,2018). Financial information will help the shareholder in providing the

company's stability of cash flow which are the source of their cash in form of their return

on investment.

Employees: They are the people who perform in order to enhance the company's overall

growth and increase in company's revenue. Financial information is an important source

which help the employee in knowing the company's financial performance so that they

can perform well to increase the company's financial condition. Financial reporting is

important for the employees in determining the stability, growth and progress of the

company. The growth of the company will help them in providing more opportunities of

growth in their career and in fulfilling their personal needs.

Suppliers: the are individual or the organisation which provides the raw material in order

to manufactures the goods of company. Financial information will help them to be

assured about the company's ability to pay their debts on time. It will help them in know

the company's financial condition.

Customers: in order to increase the revenue of the company, customer satisfaction is

very essential (Fassin, 2012). As the sales to the customer are the main source of

generating revenue for a company. It is beneficial for the customer to analyse the

company's profitability and the position to stay stable in providing them goods and

services. Financial information is also important for the customer in determining the price

of the product offered to customers.

with the business organization. Stakeholder of an organization can be the shareholder, investors,

employees, customer and suppliers. They are an essential element of the company as they can

influence the companies activities and they can also be affected either the companies activities.

Financial information is an important source of getting about the activities of organization.

Following are some benefits of the financial information to the stakeholder:

Shareholders: They are the one who invested their money in company in order to get a

return from the company's revenue. They expect a good return of profit from the

company. Financial information is beneficial for the shareholder in getting a proper

knowledge of the company's financial postilion (Who Are the Stakeholders Relative to an

Organization? ,2018). Financial information will help the shareholder in providing the

company's stability of cash flow which are the source of their cash in form of their return

on investment.

Employees: They are the people who perform in order to enhance the company's overall

growth and increase in company's revenue. Financial information is an important source

which help the employee in knowing the company's financial performance so that they

can perform well to increase the company's financial condition. Financial reporting is

important for the employees in determining the stability, growth and progress of the

company. The growth of the company will help them in providing more opportunities of

growth in their career and in fulfilling their personal needs.

Suppliers: the are individual or the organisation which provides the raw material in order

to manufactures the goods of company. Financial information will help them to be

assured about the company's ability to pay their debts on time. It will help them in know

the company's financial condition.

Customers: in order to increase the revenue of the company, customer satisfaction is

very essential (Fassin, 2012). As the sales to the customer are the main source of

generating revenue for a company. It is beneficial for the customer to analyse the

company's profitability and the position to stay stable in providing them goods and

services. Financial information is also important for the customer in determining the price

of the product offered to customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Examining importance of financial reporting for accomplishing organizational growth and

objectives

Financial report is crucial for the growth if the business entity. It is engaged in the

preparation of the financial statement that will help in disclosure of the company's financial

performance and position to the management and stakeholders of the company.

Financial reporting plays an important role for achieving the organisational growth and

objectives (O’Riordan and Fairbrass, 2014). Financial reporting and information's main objective

is to improve the financial position and performance of the company. Management of the

company's make policies and strategies in order to increase the profitability and cash flow of the

company. Financial statements helps them in determining the possible expenses and operating

income that are generated in the year. It help the management in making policies to control the

cost of the company. One of the important role that financial reporting plays is to provide the

accurate financial information to the management on time that will help them in taking decision

for growth of organisation. Financial reporting will help ,management of company in monitoring

the business activities which help in controlling the cost and maintain proper cash flow in

business entity (Nobes, 2014). Financial reporting also help the management in attracting more

capital through the investors. Financial statements help in attracting the investors as they can

analyse the financial condition from the statement It helps the investors and shareholder in

making their decision of investing in the company. More shareholder will help in increasing in

goodwill of the company, it will help in meeting the company's objectives and growth in future.

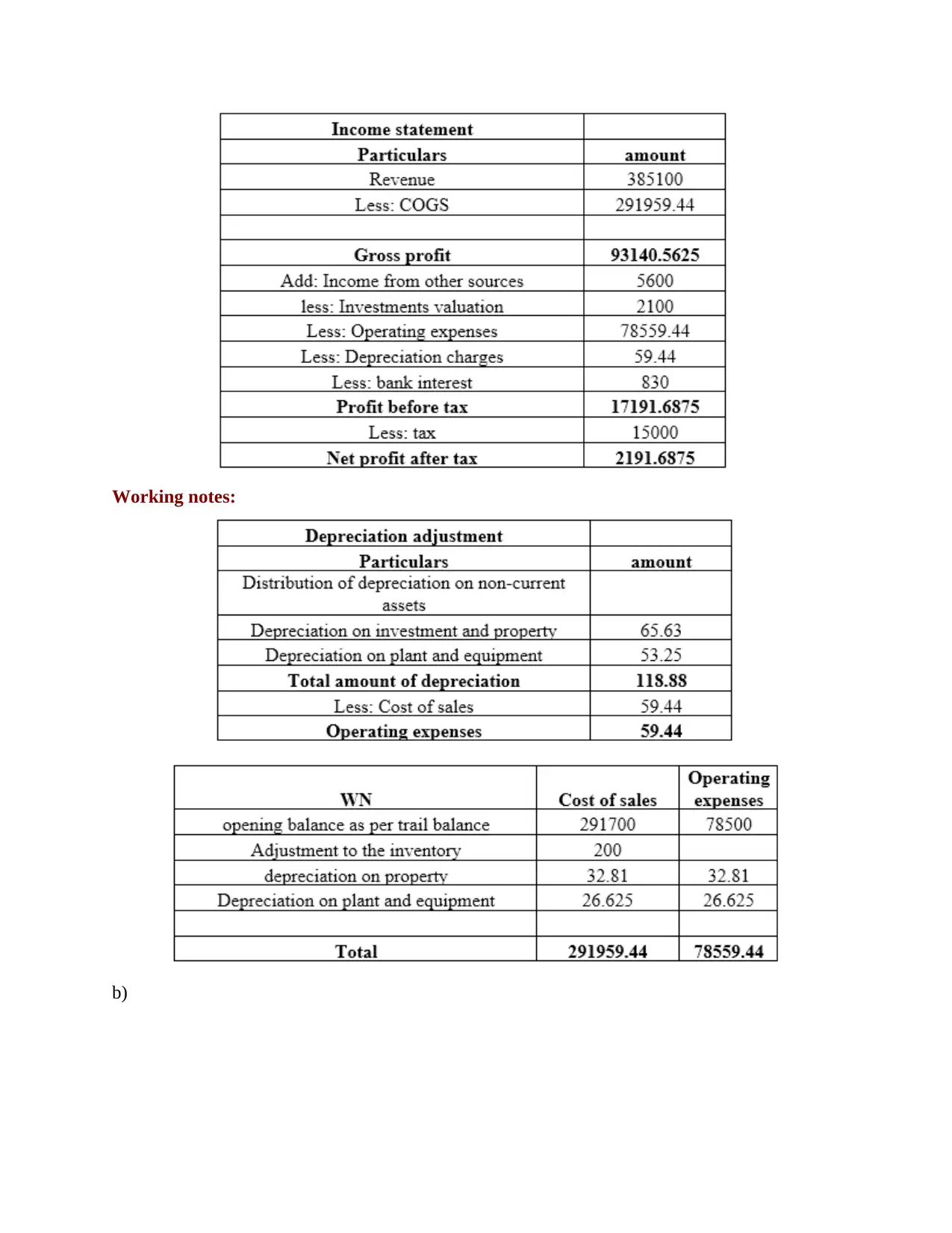

5. Presenting financial statements according to IAS 1

a)

objectives

Financial report is crucial for the growth if the business entity. It is engaged in the

preparation of the financial statement that will help in disclosure of the company's financial

performance and position to the management and stakeholders of the company.

Financial reporting plays an important role for achieving the organisational growth and

objectives (O’Riordan and Fairbrass, 2014). Financial reporting and information's main objective

is to improve the financial position and performance of the company. Management of the

company's make policies and strategies in order to increase the profitability and cash flow of the

company. Financial statements helps them in determining the possible expenses and operating

income that are generated in the year. It help the management in making policies to control the

cost of the company. One of the important role that financial reporting plays is to provide the

accurate financial information to the management on time that will help them in taking decision

for growth of organisation. Financial reporting will help ,management of company in monitoring

the business activities which help in controlling the cost and maintain proper cash flow in

business entity (Nobes, 2014). Financial reporting also help the management in attracting more

capital through the investors. Financial statements help in attracting the investors as they can

analyse the financial condition from the statement It helps the investors and shareholder in

making their decision of investing in the company. More shareholder will help in increasing in

goodwill of the company, it will help in meeting the company's objectives and growth in future.

5. Presenting financial statements according to IAS 1

a)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working notes:

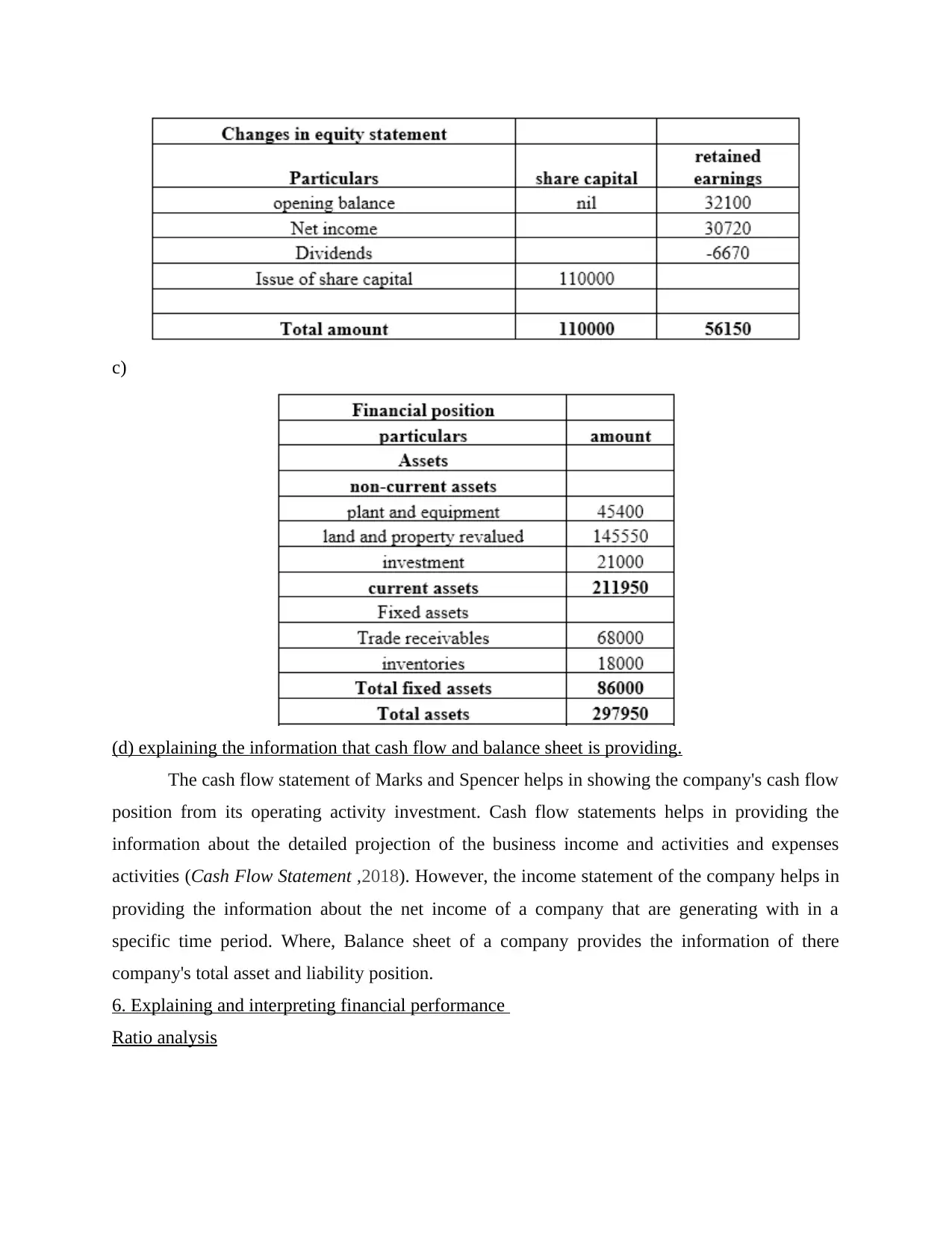

b)

b)

c)

(d) explaining the information that cash flow and balance sheet is providing.

The cash flow statement of Marks and Spencer helps in showing the company's cash flow

position from its operating activity investment. Cash flow statements helps in providing the

information about the detailed projection of the business income and activities and expenses

activities (Cash Flow Statement ,2018). However, the income statement of the company helps in

providing the information about the net income of a company that are generating with in a

specific time period. Where, Balance sheet of a company provides the information of there

company's total asset and liability position.

6. Explaining and interpreting financial performance

Ratio analysis

(d) explaining the information that cash flow and balance sheet is providing.

The cash flow statement of Marks and Spencer helps in showing the company's cash flow

position from its operating activity investment. Cash flow statements helps in providing the

information about the detailed projection of the business income and activities and expenses

activities (Cash Flow Statement ,2018). However, the income statement of the company helps in

providing the information about the net income of a company that are generating with in a

specific time period. Where, Balance sheet of a company provides the information of there

company's total asset and liability position.

6. Explaining and interpreting financial performance

Ratio analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

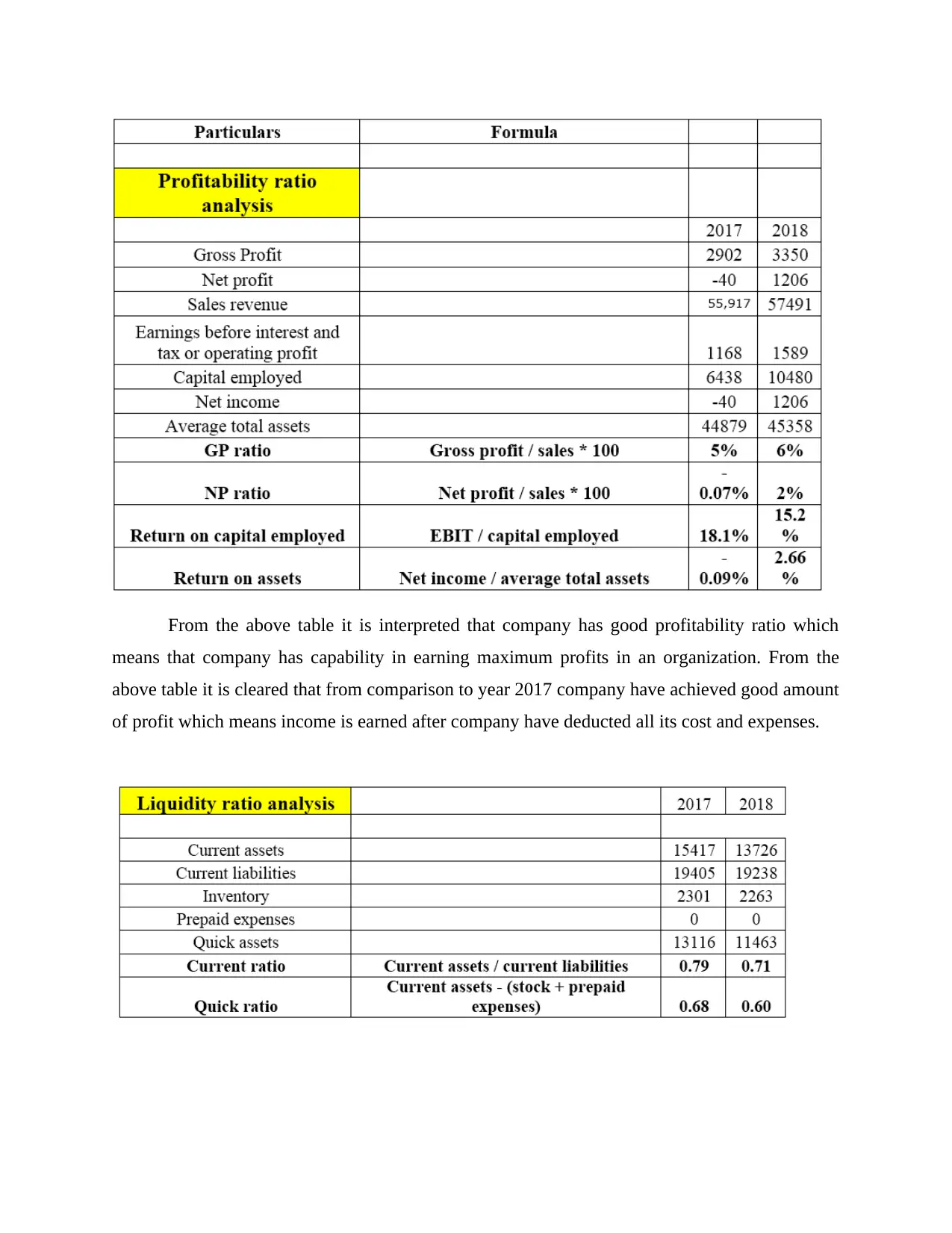

From the above table it is interpreted that company has good profitability ratio which

means that company has capability in earning maximum profits in an organization. From the

above table it is cleared that from comparison to year 2017 company have achieved good amount

of profit which means income is earned after company have deducted all its cost and expenses.

means that company has capability in earning maximum profits in an organization. From the

above table it is cleared that from comparison to year 2017 company have achieved good amount

of profit which means income is earned after company have deducted all its cost and expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

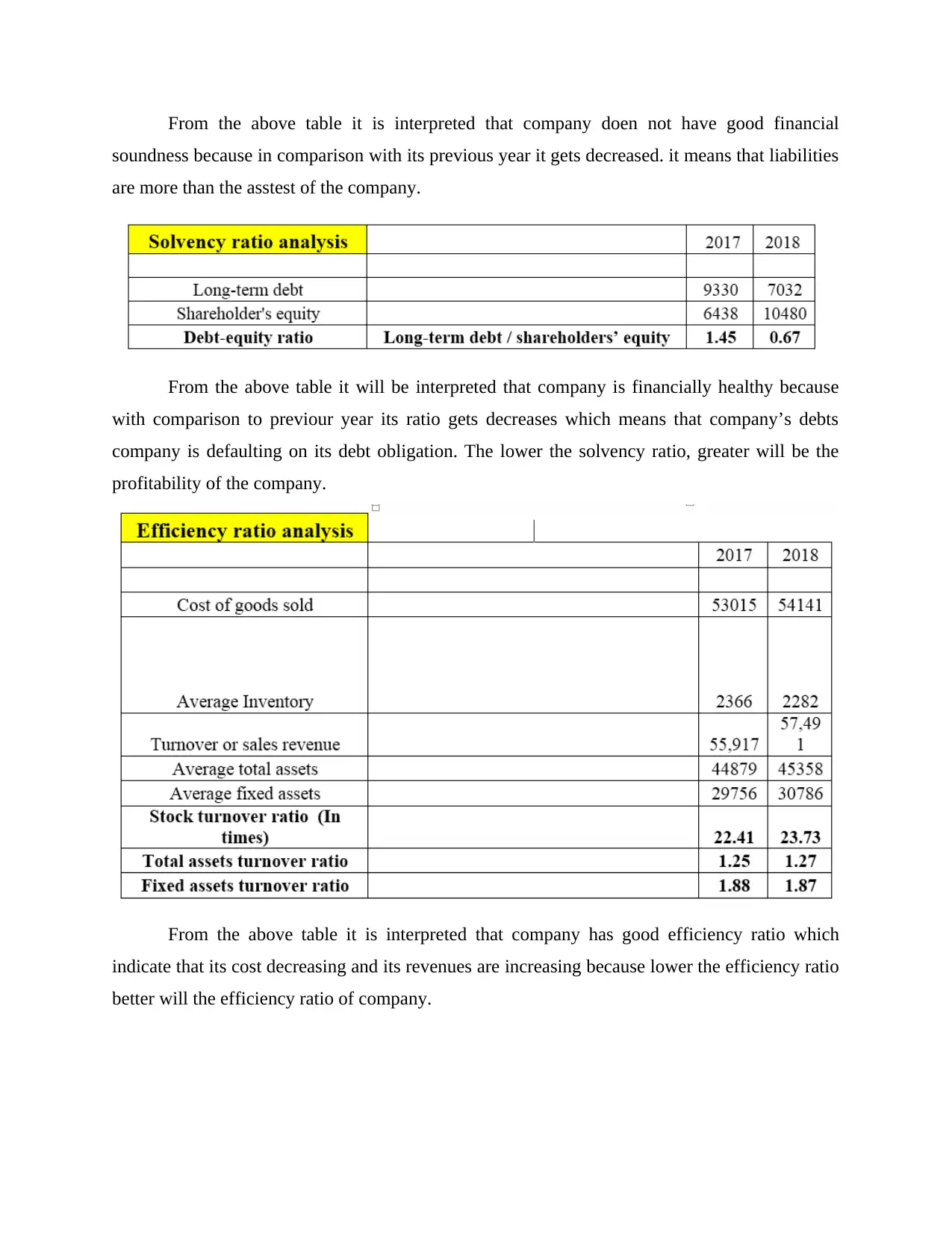

From the above table it is interpreted that company doen not have good financial

soundness because in comparison with its previous year it gets decreased. it means that liabilities

are more than the asstest of the company.

From the above table it will be interpreted that company is financially healthy because

with comparison to previour year its ratio gets decreases which means that company’s debts

company is defaulting on its debt obligation. The lower the solvency ratio, greater will be the

profitability of the company.

From the above table it is interpreted that company has good efficiency ratio which

indicate that its cost decreasing and its revenues are increasing because lower the efficiency ratio

better will the efficiency ratio of company.

soundness because in comparison with its previous year it gets decreased. it means that liabilities

are more than the asstest of the company.

From the above table it will be interpreted that company is financially healthy because

with comparison to previour year its ratio gets decreases which means that company’s debts

company is defaulting on its debt obligation. The lower the solvency ratio, greater will be the

profitability of the company.

From the above table it is interpreted that company has good efficiency ratio which

indicate that its cost decreasing and its revenues are increasing because lower the efficiency ratio

better will the efficiency ratio of company.

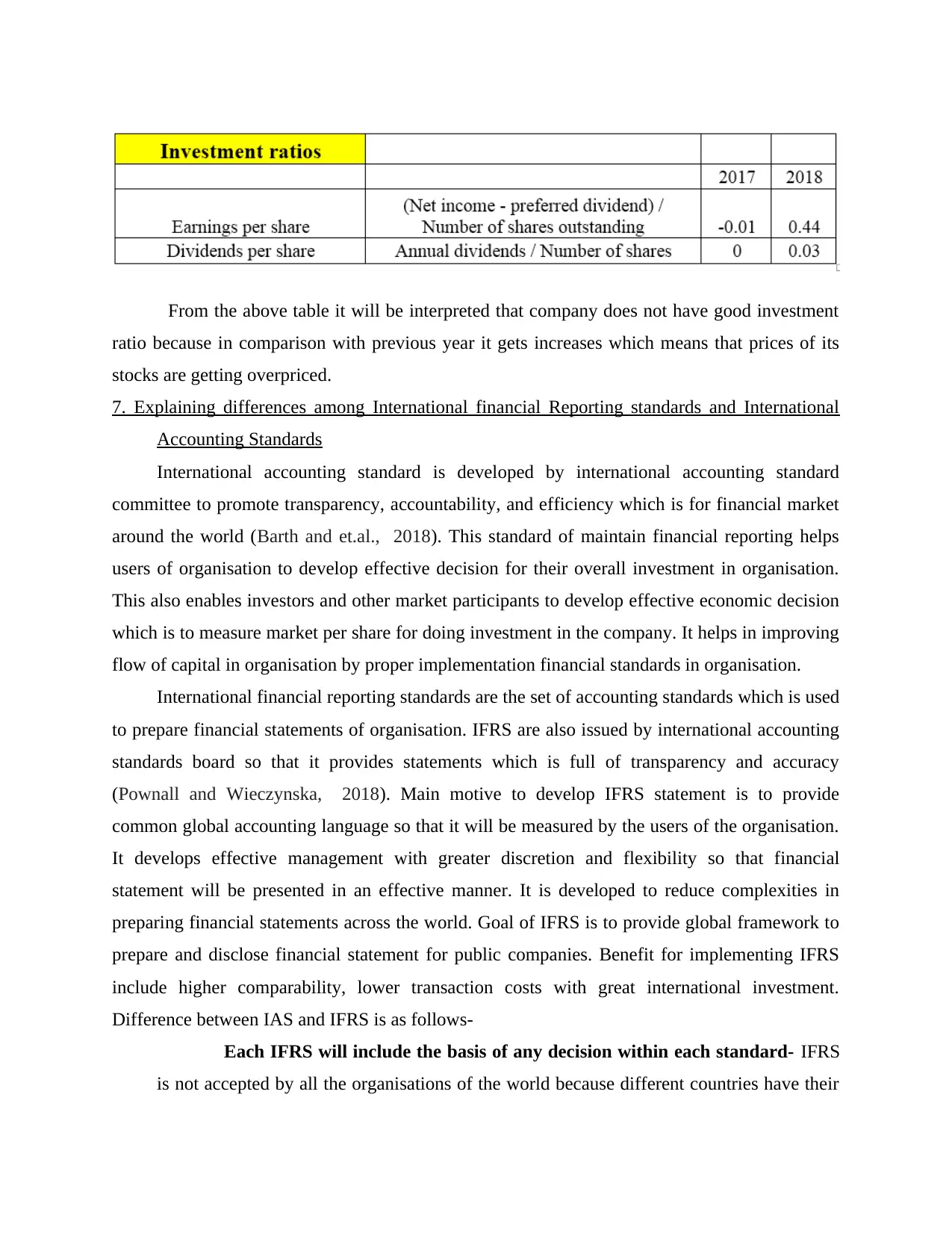

From the above table it will be interpreted that company does not have good investment

ratio because in comparison with previous year it gets increases which means that prices of its

stocks are getting overpriced.

7. Explaining differences among International financial Reporting standards and International

Accounting Standards

International accounting standard is developed by international accounting standard

committee to promote transparency, accountability, and efficiency which is for financial market

around the world (Barth and et.al., 2018). This standard of maintain financial reporting helps

users of organisation to develop effective decision for their overall investment in organisation.

This also enables investors and other market participants to develop effective economic decision

which is to measure market per share for doing investment in the company. It helps in improving

flow of capital in organisation by proper implementation financial standards in organisation.

International financial reporting standards are the set of accounting standards which is used

to prepare financial statements of organisation. IFRS are also issued by international accounting

standards board so that it provides statements which is full of transparency and accuracy

(Pownall and Wieczynska, 2018). Main motive to develop IFRS statement is to provide

common global accounting language so that it will be measured by the users of the organisation.

It develops effective management with greater discretion and flexibility so that financial

statement will be presented in an effective manner. It is developed to reduce complexities in

preparing financial statements across the world. Goal of IFRS is to provide global framework to

prepare and disclose financial statement for public companies. Benefit for implementing IFRS

include higher comparability, lower transaction costs with great international investment.

Difference between IAS and IFRS is as follows-

Each IFRS will include the basis of any decision within each standard- IFRS

is not accepted by all the organisations of the world because different countries have their

ratio because in comparison with previous year it gets increases which means that prices of its

stocks are getting overpriced.

7. Explaining differences among International financial Reporting standards and International

Accounting Standards

International accounting standard is developed by international accounting standard

committee to promote transparency, accountability, and efficiency which is for financial market

around the world (Barth and et.al., 2018). This standard of maintain financial reporting helps

users of organisation to develop effective decision for their overall investment in organisation.

This also enables investors and other market participants to develop effective economic decision

which is to measure market per share for doing investment in the company. It helps in improving

flow of capital in organisation by proper implementation financial standards in organisation.

International financial reporting standards are the set of accounting standards which is used

to prepare financial statements of organisation. IFRS are also issued by international accounting

standards board so that it provides statements which is full of transparency and accuracy

(Pownall and Wieczynska, 2018). Main motive to develop IFRS statement is to provide

common global accounting language so that it will be measured by the users of the organisation.

It develops effective management with greater discretion and flexibility so that financial

statement will be presented in an effective manner. It is developed to reduce complexities in

preparing financial statements across the world. Goal of IFRS is to provide global framework to

prepare and disclose financial statement for public companies. Benefit for implementing IFRS

include higher comparability, lower transaction costs with great international investment.

Difference between IAS and IFRS is as follows-

Each IFRS will include the basis of any decision within each standard- IFRS

is not accepted by all the organisations of the world because different countries have their

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.