Comprehensive Analysis of Financial Reporting in the UK Context

VerifiedAdded on 2020/12/18

|14

|4011

|344

Report

AI Summary

This report provides a comprehensive analysis of financial reporting in the UK context. It begins by examining the purpose and context of financial reporting, followed by an exploration of the conceptual and regulatory frameworks, including governance aspects. The report identifies and assesses the needs of various organizational stakeholders regarding financial reports. It then analyzes the value of financial reporting for achieving organizational growth and objectives. The report also explains International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), evaluating their benefits and critically assessing financial reporting within organizations using models and theories. Furthermore, it identifies differences in financial reporting globally and evaluates factors influencing these differences, concluding with a discussion on the degree of compliance with IFRS worldwide.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Analyzing the context and purpose of financial reporting in UK...........................................1

2. Examining conceptual and regulatory framework and governance of financial reporting

with key principles and assessing requirement and purpose.......................................................2

3. Determining stakeholders of organizations along with critical assess about need of financial

reports..........................................................................................................................................3

4. Analyzing value of financial reporting for attaining organizational growth and objectives...6

5. Explaining International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS) along with evaluation of benefits...................................................................7

6. Critical evaluation of financial reporting in organization with application of models and

theories for supporting conclusions and judgments....................................................................8

7. Identifying differences in financial reporting throughout world and evaluating factors

which influence these differences.............................................................................................10

8. Degree of compliance of International Financial Reporting Standards................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

1. Analyzing the context and purpose of financial reporting in UK...........................................1

2. Examining conceptual and regulatory framework and governance of financial reporting

with key principles and assessing requirement and purpose.......................................................2

3. Determining stakeholders of organizations along with critical assess about need of financial

reports..........................................................................................................................................3

4. Analyzing value of financial reporting for attaining organizational growth and objectives...6

5. Explaining International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS) along with evaluation of benefits...................................................................7

6. Critical evaluation of financial reporting in organization with application of models and

theories for supporting conclusions and judgments....................................................................8

7. Identifying differences in financial reporting throughout world and evaluating factors

which influence these differences.............................................................................................10

8. Degree of compliance of International Financial Reporting Standards................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial reporting is referred as disclosure of financial outcome and related information

to external stakeholders and management on basis of company which is performing over specific

duration. The present report will discuss about context and purpose of financial reporting in UK

and then conceptual and regulatory framework along with governance. In the same series, it will

articulate key stakeholders of organization with their need for financial reporting. Furthermore, it

will analyse value of financial reporting for attaining organizational growth and objectives. This

report will state International Accounting Standards and International financial reporting

standards with its benefits. It will critically evaluate about financial reporting in organization

with application of various models and theories for supporting conclusions and judgements.

Henceforth, it will state variations in financial reporting throughout world and evaluation of

factors which influence these variations. Thus, it will reflect about degree of compliance with

IFRS throughout the world.

1. Analyzing the context and purpose of financial reporting in UK

Financial reporting has very crucial role throughout the world economies its main

purpose is to give useful and relevant information to company owners where is presence of

division among control and ownership of that particular company. Usually, it occurs in public

limited companies where share capital is sold to public via stock market or exchange system. The

potentially and diverse geographically shareholders does not engage in company's management

as they appoint directors with this behalf (Financial Reporting, 2019). The owners retain annual

statement which briefs about position and performance of organization so that it could assess

about investment performance in this reporting period. With absence of reporting system,

investors would be less inclined as contributing to capital without monitoring effectively that

how organization is operated through directors along with company's stewards who are supposed

for operating in shareholder's best interests.

The United Kingdom is an EU member stated as UK companies are listed ion EEA and

EU securities market follow IFRS and periodically issue document which briefs about use of

options of IAS regulation through EU member states. The key aim of corporate governance is for

safeguarding integrity of process of financial reporting to give reasonable assurance about

financial statements provide true and fair aspect of operations and finances of companies. The

good corporate governance protects interest of key stakeholders and corporate performance is

1

Financial reporting is referred as disclosure of financial outcome and related information

to external stakeholders and management on basis of company which is performing over specific

duration. The present report will discuss about context and purpose of financial reporting in UK

and then conceptual and regulatory framework along with governance. In the same series, it will

articulate key stakeholders of organization with their need for financial reporting. Furthermore, it

will analyse value of financial reporting for attaining organizational growth and objectives. This

report will state International Accounting Standards and International financial reporting

standards with its benefits. It will critically evaluate about financial reporting in organization

with application of various models and theories for supporting conclusions and judgements.

Henceforth, it will state variations in financial reporting throughout world and evaluation of

factors which influence these variations. Thus, it will reflect about degree of compliance with

IFRS throughout the world.

1. Analyzing the context and purpose of financial reporting in UK

Financial reporting has very crucial role throughout the world economies its main

purpose is to give useful and relevant information to company owners where is presence of

division among control and ownership of that particular company. Usually, it occurs in public

limited companies where share capital is sold to public via stock market or exchange system. The

potentially and diverse geographically shareholders does not engage in company's management

as they appoint directors with this behalf (Financial Reporting, 2019). The owners retain annual

statement which briefs about position and performance of organization so that it could assess

about investment performance in this reporting period. With absence of reporting system,

investors would be less inclined as contributing to capital without monitoring effectively that

how organization is operated through directors along with company's stewards who are supposed

for operating in shareholder's best interests.

The United Kingdom is an EU member stated as UK companies are listed ion EEA and

EU securities market follow IFRS and periodically issue document which briefs about use of

options of IAS regulation through EU member states. The key aim of corporate governance is for

safeguarding integrity of process of financial reporting to give reasonable assurance about

financial statements provide true and fair aspect of operations and finances of companies. The

good corporate governance protects interest of key stakeholders and corporate performance is

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

enhanced and its important pillar is board of directors where they have fiduciary and legal

responsibility for purpose of managing governance risks. In nutshell, purpose of financial

reporting is to meet user legislation and expectations and ensuring about organizations to comply

with similar standards and rules and to seek investment and funding (Mao and Wu, 2019). It

helps in predicting future financial positions along with cash flow.

2. Examining conceptual and regulatory framework and governance of financial reporting with

key principles and assessing requirement and purpose

The conceptual framework of financial reporting is referred as theory of accounting

prepared through standard setting body against where practical problems could be tested

objectively. It deals with fundamental issues of financial reporting like users and objectives of

financial statements along with features which create accounting information very useful along

with basic elements of financial statements like assets, equity, liabilities, expenses and income

along with concepts for measuring and recognizing elements in financial statements. In simple

words, conceptual framework is coherent system related to interrelated objectives along with

fundamental principles and framework prescribes about nature, limits and functions of financial

statements and accounting (Dou, Wong and Xin, 2019).

Conceptual framework helps in enabling accounting standards and generally accepted

accounting practice must be developed as per agreed principles. This will avoid fire fighting

where is development of accounting standards in piecemeal aspect for responding about specific

abuses and problems. Fire fighting could lead to inconsistency among different standards among

accounting legislation and standards. There is lack of conceptual framework might mean certain

critical problems were not addressed. In this aspect, transactions are more complex and

businesses are highly sophisticated and helps in auditors for dealing with transaction as they are

not subjected to accounting standard.

With context to attain requirements of financial statement's users the organization has to

implement accounting systems which give need information. It is significant system which is

regulated for ensuring about information given to users in proper format which is useful with

context of informational requirement which is attained via framework of financial reporting on

basis of conceptual framework. The European Union has adopted regulation of IAS with

requirement of listed European companies in EU securities market which considers about

insurance and bank companies for preparing consolidated financial statements as per IFRS

2

responsibility for purpose of managing governance risks. In nutshell, purpose of financial

reporting is to meet user legislation and expectations and ensuring about organizations to comply

with similar standards and rules and to seek investment and funding (Mao and Wu, 2019). It

helps in predicting future financial positions along with cash flow.

2. Examining conceptual and regulatory framework and governance of financial reporting with

key principles and assessing requirement and purpose

The conceptual framework of financial reporting is referred as theory of accounting

prepared through standard setting body against where practical problems could be tested

objectively. It deals with fundamental issues of financial reporting like users and objectives of

financial statements along with features which create accounting information very useful along

with basic elements of financial statements like assets, equity, liabilities, expenses and income

along with concepts for measuring and recognizing elements in financial statements. In simple

words, conceptual framework is coherent system related to interrelated objectives along with

fundamental principles and framework prescribes about nature, limits and functions of financial

statements and accounting (Dou, Wong and Xin, 2019).

Conceptual framework helps in enabling accounting standards and generally accepted

accounting practice must be developed as per agreed principles. This will avoid fire fighting

where is development of accounting standards in piecemeal aspect for responding about specific

abuses and problems. Fire fighting could lead to inconsistency among different standards among

accounting legislation and standards. There is lack of conceptual framework might mean certain

critical problems were not addressed. In this aspect, transactions are more complex and

businesses are highly sophisticated and helps in auditors for dealing with transaction as they are

not subjected to accounting standard.

With context to attain requirements of financial statement's users the organization has to

implement accounting systems which give need information. It is significant system which is

regulated for ensuring about information given to users in proper format which is useful with

context of informational requirement which is attained via framework of financial reporting on

basis of conceptual framework. The European Union has adopted regulation of IAS with

requirement of listed European companies in EU securities market which considers about

insurance and bank companies for preparing consolidated financial statements as per IFRS

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

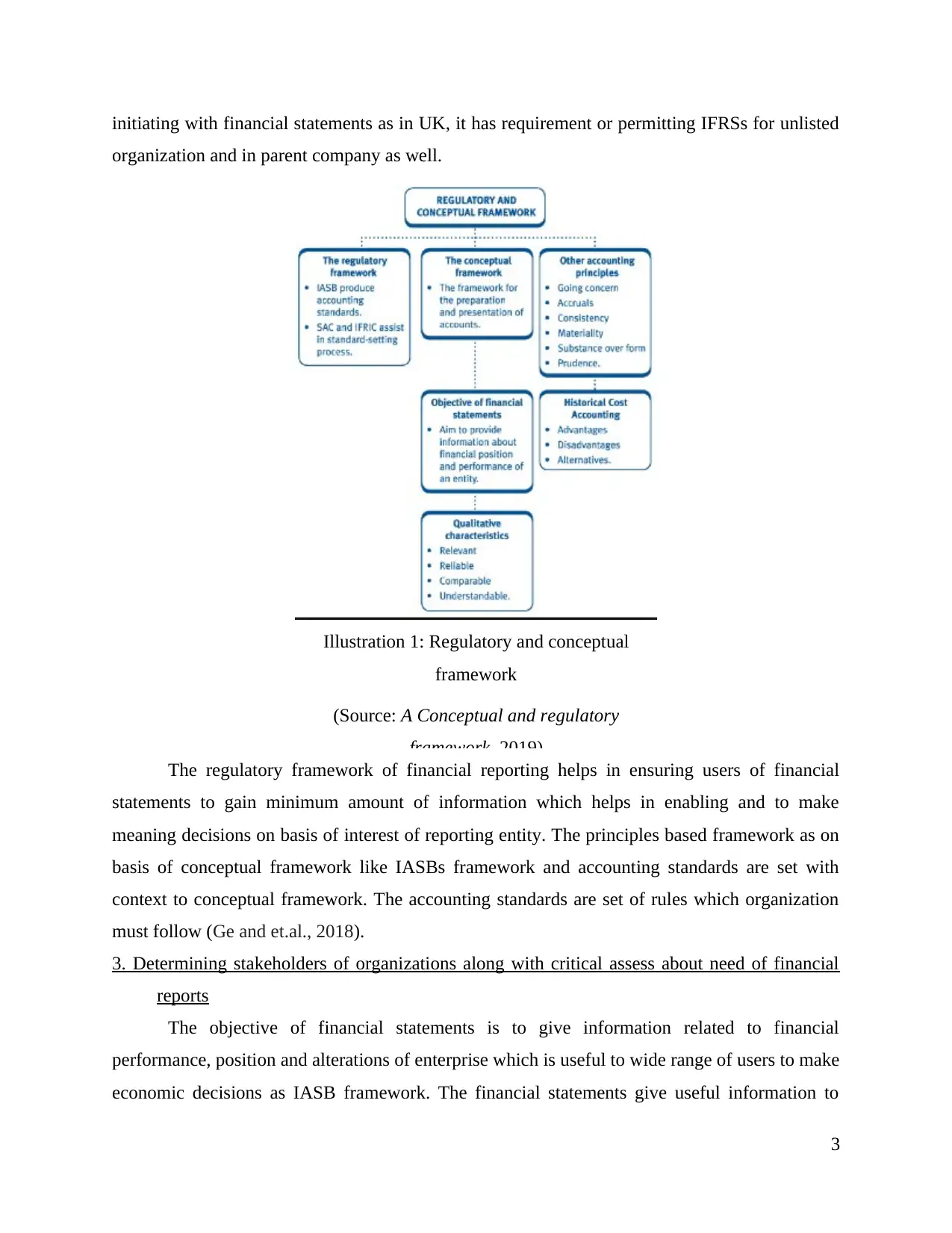

initiating with financial statements as in UK, it has requirement or permitting IFRSs for unlisted

organization and in parent company as well.

Illustration 1: Regulatory and conceptual

framework

(Source: A Conceptual and regulatory

framework, 2019)

The regulatory framework of financial reporting helps in ensuring users of financial

statements to gain minimum amount of information which helps in enabling and to make

meaning decisions on basis of interest of reporting entity. The principles based framework as on

basis of conceptual framework like IASBs framework and accounting standards are set with

context to conceptual framework. The accounting standards are set of rules which organization

must follow (Ge and et.al., 2018).

3. Determining stakeholders of organizations along with critical assess about need of financial

reports

The objective of financial statements is to give information related to financial

performance, position and alterations of enterprise which is useful to wide range of users to make

economic decisions as IASB framework. The financial statements give useful information to

3

organization and in parent company as well.

Illustration 1: Regulatory and conceptual

framework

(Source: A Conceptual and regulatory

framework, 2019)

The regulatory framework of financial reporting helps in ensuring users of financial

statements to gain minimum amount of information which helps in enabling and to make

meaning decisions on basis of interest of reporting entity. The principles based framework as on

basis of conceptual framework like IASBs framework and accounting standards are set with

context to conceptual framework. The accounting standards are set of rules which organization

must follow (Ge and et.al., 2018).

3. Determining stakeholders of organizations along with critical assess about need of financial

reports

The objective of financial statements is to give information related to financial

performance, position and alterations of enterprise which is useful to wide range of users to make

economic decisions as IASB framework. The financial statements give useful information to

3

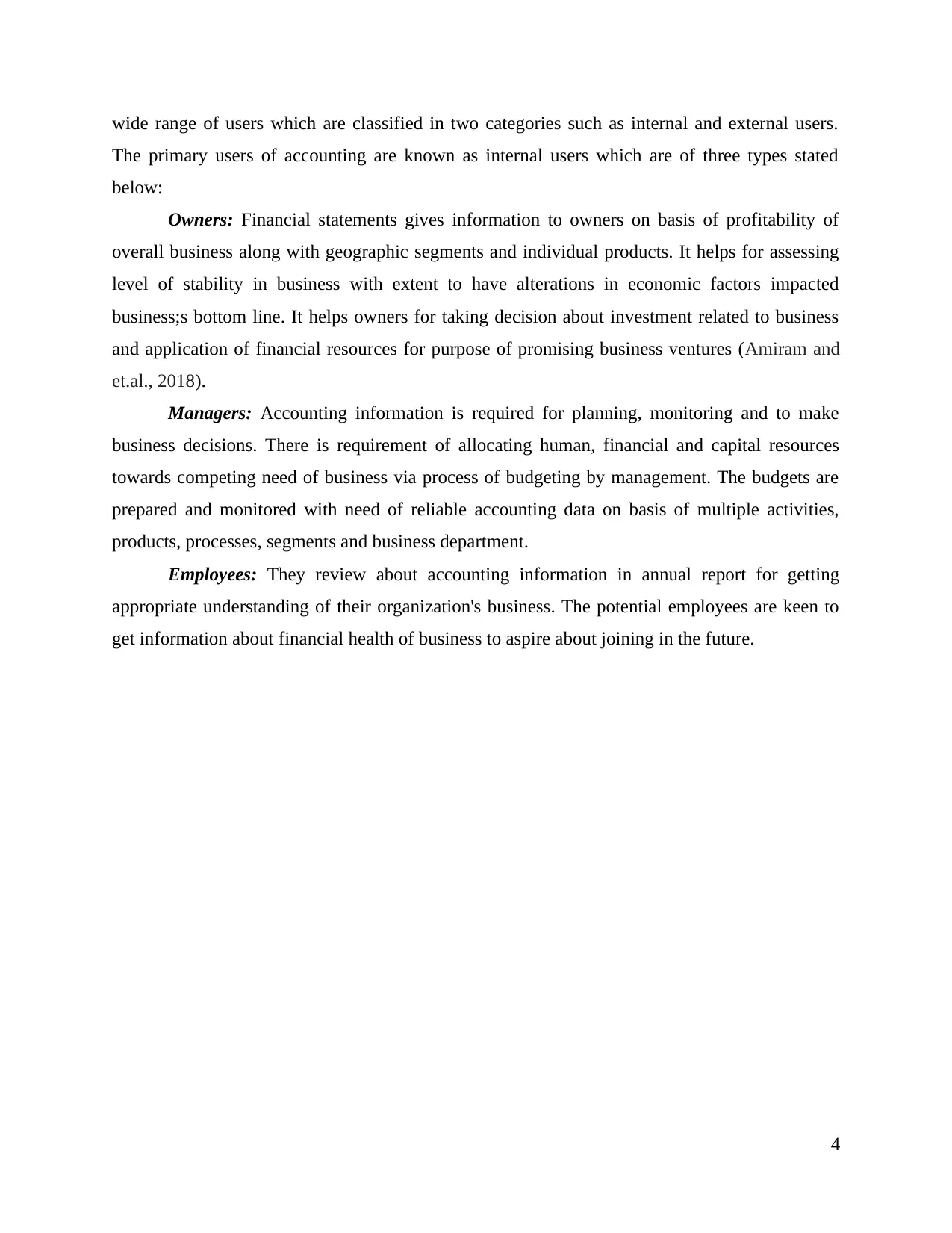

wide range of users which are classified in two categories such as internal and external users.

The primary users of accounting are known as internal users which are of three types stated

below:

Owners: Financial statements gives information to owners on basis of profitability of

overall business along with geographic segments and individual products. It helps for assessing

level of stability in business with extent to have alterations in economic factors impacted

business;s bottom line. It helps owners for taking decision about investment related to business

and application of financial resources for purpose of promising business ventures (Amiram and

et.al., 2018).

Managers: Accounting information is required for planning, monitoring and to make

business decisions. There is requirement of allocating human, financial and capital resources

towards competing need of business via process of budgeting by management. The budgets are

prepared and monitored with need of reliable accounting data on basis of multiple activities,

products, processes, segments and business department.

Employees: They review about accounting information in annual report for getting

appropriate understanding of their organization's business. The potential employees are keen to

get information about financial health of business to aspire about joining in the future.

4

The primary users of accounting are known as internal users which are of three types stated

below:

Owners: Financial statements gives information to owners on basis of profitability of

overall business along with geographic segments and individual products. It helps for assessing

level of stability in business with extent to have alterations in economic factors impacted

business;s bottom line. It helps owners for taking decision about investment related to business

and application of financial resources for purpose of promising business ventures (Amiram and

et.al., 2018).

Managers: Accounting information is required for planning, monitoring and to make

business decisions. There is requirement of allocating human, financial and capital resources

towards competing need of business via process of budgeting by management. The budgets are

prepared and monitored with need of reliable accounting data on basis of multiple activities,

products, processes, segments and business department.

Employees: They review about accounting information in annual report for getting

appropriate understanding of their organization's business. The potential employees are keen to

get information about financial health of business to aspire about joining in the future.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration 2: Users of accounting information

(Source: Users of Accounting Information, 2017)

External users of accounting

The secondary users of accounting are known as external users which are stated below:

Investors: They primarily rely on financial statements for investment perspective as it

helps in assessing profitability, risk and valuation of investment.

Lenders: The accounting information is used for assessing credit worthiness of borrowers

such as ability for repaying any loan. Usually, they offer loans along with facilities of credits on

basis of assessing financial health of borrowers.

Suppliers: Similarly to lenders, suppliers requires accounting information for purpose of

assessing credit worthiness of customers prior to offering services and goods on credit (Chen,

Zhang and Zhou, 2018).

Customers: Not every customer is in need of financial information of its suppliers but

industrial consumers require accounting information related to suppliers for assessing that

5

(Source: Users of Accounting Information, 2017)

External users of accounting

The secondary users of accounting are known as external users which are stated below:

Investors: They primarily rely on financial statements for investment perspective as it

helps in assessing profitability, risk and valuation of investment.

Lenders: The accounting information is used for assessing credit worthiness of borrowers

such as ability for repaying any loan. Usually, they offer loans along with facilities of credits on

basis of assessing financial health of borrowers.

Suppliers: Similarly to lenders, suppliers requires accounting information for purpose of

assessing credit worthiness of customers prior to offering services and goods on credit (Chen,

Zhang and Zhou, 2018).

Customers: Not every customer is in need of financial information of its suppliers but

industrial consumers require accounting information related to suppliers for assessing that

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

required resources are necessary with context of steady supply of services and goods in the

future.

Auditors: External auditors examines the financial statement along with underlying

accounting record of business with context to audit opinion. In the similar aspect, investors along

with other stakeholders highly rely on independent opinion related to these auditors on basis of

accuracy of financial statements.

4. Analyzing value of financial reporting for attaining organizational growth and objectives

Financial reporting has high involvement of disclosure of financial information to its

multiple stakeholders on basis of financial position and performance of organization over

specified duration. As per International accounting standards board, it gives information relate to

financial performance, position and alterations in business's financial position which is useful for

broad range of users with perspective of making economic decisions (Wang, Cao and Ye, 2018).

It helps and business for complying with different statues and regulatory requirements as they are

need of filing financial statements to government agencies. With context to listed organizations,

there is requirement of filing stock exchanges and published on quarterly and annual outcomes.

In the similar aspect, this facilitates statutory audit where these statutory auditors were required

for auditing company's financial statements with context to express opinion.

The backbone of financial planning, bench marking, analysis and decision making are

formed through financial reports. These are applicable with above purposes through multiple

stakeholders and capital could be raised both overseas and domestic as well. While considering

financial, public in large could analyze the company's performance along with management as

well. The most important is with objective of biding, government supplies, labor contracts etc.

business are in need or furnishing financial statements and reports.

Simultaneously, published accounting data in financial reports might have economic

effects via impact on manager's behavior of corporate enterprises. The consideration of

accounting numbers on compensation of management schemes of fear or market along with

misinterpretation of accounting reports would directly influence of operating and financing

decisions of managers. The accounting procedures are preferred through shareholders which

mirror the micro economic events in detailed aspect. On the other hand, they must be fully

concerned that managers might be able for reporting and manipulating data to raise their

6

future.

Auditors: External auditors examines the financial statement along with underlying

accounting record of business with context to audit opinion. In the similar aspect, investors along

with other stakeholders highly rely on independent opinion related to these auditors on basis of

accuracy of financial statements.

4. Analyzing value of financial reporting for attaining organizational growth and objectives

Financial reporting has high involvement of disclosure of financial information to its

multiple stakeholders on basis of financial position and performance of organization over

specified duration. As per International accounting standards board, it gives information relate to

financial performance, position and alterations in business's financial position which is useful for

broad range of users with perspective of making economic decisions (Wang, Cao and Ye, 2018).

It helps and business for complying with different statues and regulatory requirements as they are

need of filing financial statements to government agencies. With context to listed organizations,

there is requirement of filing stock exchanges and published on quarterly and annual outcomes.

In the similar aspect, this facilitates statutory audit where these statutory auditors were required

for auditing company's financial statements with context to express opinion.

The backbone of financial planning, bench marking, analysis and decision making are

formed through financial reports. These are applicable with above purposes through multiple

stakeholders and capital could be raised both overseas and domestic as well. While considering

financial, public in large could analyze the company's performance along with management as

well. The most important is with objective of biding, government supplies, labor contracts etc.

business are in need or furnishing financial statements and reports.

Simultaneously, published accounting data in financial reports might have economic

effects via impact on manager's behavior of corporate enterprises. The consideration of

accounting numbers on compensation of management schemes of fear or market along with

misinterpretation of accounting reports would directly influence of operating and financing

decisions of managers. The accounting procedures are preferred through shareholders which

mirror the micro economic events in detailed aspect. On the other hand, they must be fully

concerned that managers might be able for reporting and manipulating data to raise their

6

compensation. The information contributed towards better decision making related to investment

and for promoting understanding along with creating environment for cooperating perspective.

Financial reporting produces confidence along with favorable impact on cost of capital of

organization. This helps in retaining credibility and provide society with reliable and relevant

information with economic transactions and events and with absence of attempt for move

economy in single direction instead of another (Liu and et.al., 2018).

5. Explaining International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS) along with evaluation of benefits

International Accounting standards were issued through antecedent International

Accounting Standards Council and amended and endorsed through International Accounting

Standard Board. This set of accounting standards developed and supervised through UK-based

International Accounting Standards Board where it has no authority with need of countries for

complying with standards along with jurisdictions through world (Satsuk and et.al., 2018). The

globally comparable accounting standards promotes accountability, transparency along with

efficiency in financial markets throughout the world. It helps in enabling investors other than

other participants of market to make informed about economic decisions related to opportunities

of investment along with risk. Universal standards significantly decreases reporting and

regulatory cost, especially with context to companies through international operations with

subsidiaries in various countries.

The different regions and countries throughout world boast with various norms and

cultures as they manifest themselves with prevailing business culture in country. The major

benefit of these standards is consideration of input through professionals along with legal

authorities throughout the world. This could create set of ethical guidelines which does not favor

single culture where foreign company adheres its own domestic ethical values.

International financial accounting standards are set of international accounting standards

which states about specific type of transactions along with other events must be reported in

financial statements. These standards are issued through International Accounting standards

board and specify exactly that accountants should maintain and report its accounts. IFRS was

established for having common accounting language so accounts and business could understand

through country to country and company to company. It allows business for great comparability

with application of similar standards for preparing financial statements could be very accurate

7

and for promoting understanding along with creating environment for cooperating perspective.

Financial reporting produces confidence along with favorable impact on cost of capital of

organization. This helps in retaining credibility and provide society with reliable and relevant

information with economic transactions and events and with absence of attempt for move

economy in single direction instead of another (Liu and et.al., 2018).

5. Explaining International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS) along with evaluation of benefits

International Accounting standards were issued through antecedent International

Accounting Standards Council and amended and endorsed through International Accounting

Standard Board. This set of accounting standards developed and supervised through UK-based

International Accounting Standards Board where it has no authority with need of countries for

complying with standards along with jurisdictions through world (Satsuk and et.al., 2018). The

globally comparable accounting standards promotes accountability, transparency along with

efficiency in financial markets throughout the world. It helps in enabling investors other than

other participants of market to make informed about economic decisions related to opportunities

of investment along with risk. Universal standards significantly decreases reporting and

regulatory cost, especially with context to companies through international operations with

subsidiaries in various countries.

The different regions and countries throughout world boast with various norms and

cultures as they manifest themselves with prevailing business culture in country. The major

benefit of these standards is consideration of input through professionals along with legal

authorities throughout the world. This could create set of ethical guidelines which does not favor

single culture where foreign company adheres its own domestic ethical values.

International financial accounting standards are set of international accounting standards

which states about specific type of transactions along with other events must be reported in

financial statements. These standards are issued through International Accounting standards

board and specify exactly that accountants should maintain and report its accounts. IFRS was

established for having common accounting language so accounts and business could understand

through country to country and company to company. It allows business for great comparability

with application of similar standards for preparing financial statements could be very accurate

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for comparison perspective. It is on basis of principles instead of philosophy of rules based

(Bassemir and Novotny‐Farkas, 2018). The principles based philosophy signifies that objective

of every standard is to reach reasonable valuation. In the similar aspect, it provides freedom for

adapting IFRS at specific situation which leads to useful statements and easily read. This

standard is highly beneficial to small and new investors by making reporting standards with

better quality and simpler and putting investors at same position with context to professional

investors as they are not feasible through previous standards. It helps in entailing decreased risk

for investors with context to trade and professionals would be not able for undertaking advantage

due to nature of financial statements.

6. Critical evaluation of financial reporting in organization with application of models and

theories for supporting conclusions and judgments

The basic theories of accounting are held through conceptual framework of accounting as

in this context, there are basic accounting theories which directly fits in this conceptual

framework which are stated below: Equity theory: It is also referred as Residuals equity theory with objective of striking

balance among input and output of employee in a workplace. In case any employee is

capable to extract right balance then it would lead for highly productive relationship

within management. In this aspect, residual equity theory is concept which is in between

entity and proprietary theory. In this aspect, equation is specified as Assets minus specific

equities is equals to residual equity. The specific equities consider claims of creditors

along with equities of preferred shareholders. On the contrary, in various cases with large

losses along with proceedings in bankruptcy along with equity of common shareholders

might disappear along with preferred shareholders or bondholders might become residual

equity holders.

Legitimacy theory: Legitimacy is referred as generalized perception and assumption

which action of any entity is desirable, appropriate and proper within socially constructed

system of values, norms and beliefs. This theory posits organization which continually

seek for ensuring about operations within norms and bounds with their respective

societies. With adoption of legitimacy theory, organization would voluntarily report on

its activities when management perceived amount activities expected through

communities where it operates. Generally, this theory is used for explaining disclosure of

8

(Bassemir and Novotny‐Farkas, 2018). The principles based philosophy signifies that objective

of every standard is to reach reasonable valuation. In the similar aspect, it provides freedom for

adapting IFRS at specific situation which leads to useful statements and easily read. This

standard is highly beneficial to small and new investors by making reporting standards with

better quality and simpler and putting investors at same position with context to professional

investors as they are not feasible through previous standards. It helps in entailing decreased risk

for investors with context to trade and professionals would be not able for undertaking advantage

due to nature of financial statements.

6. Critical evaluation of financial reporting in organization with application of models and

theories for supporting conclusions and judgments

The basic theories of accounting are held through conceptual framework of accounting as

in this context, there are basic accounting theories which directly fits in this conceptual

framework which are stated below: Equity theory: It is also referred as Residuals equity theory with objective of striking

balance among input and output of employee in a workplace. In case any employee is

capable to extract right balance then it would lead for highly productive relationship

within management. In this aspect, residual equity theory is concept which is in between

entity and proprietary theory. In this aspect, equation is specified as Assets minus specific

equities is equals to residual equity. The specific equities consider claims of creditors

along with equities of preferred shareholders. On the contrary, in various cases with large

losses along with proceedings in bankruptcy along with equity of common shareholders

might disappear along with preferred shareholders or bondholders might become residual

equity holders.

Legitimacy theory: Legitimacy is referred as generalized perception and assumption

which action of any entity is desirable, appropriate and proper within socially constructed

system of values, norms and beliefs. This theory posits organization which continually

seek for ensuring about operations within norms and bounds with their respective

societies. With adoption of legitimacy theory, organization would voluntarily report on

its activities when management perceived amount activities expected through

communities where it operates. Generally, this theory is used for explaining disclosure of

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

social and environmental reports with accountability reporting framework for

communicating it with stakeholders along with clarifying importance of their

relationships.

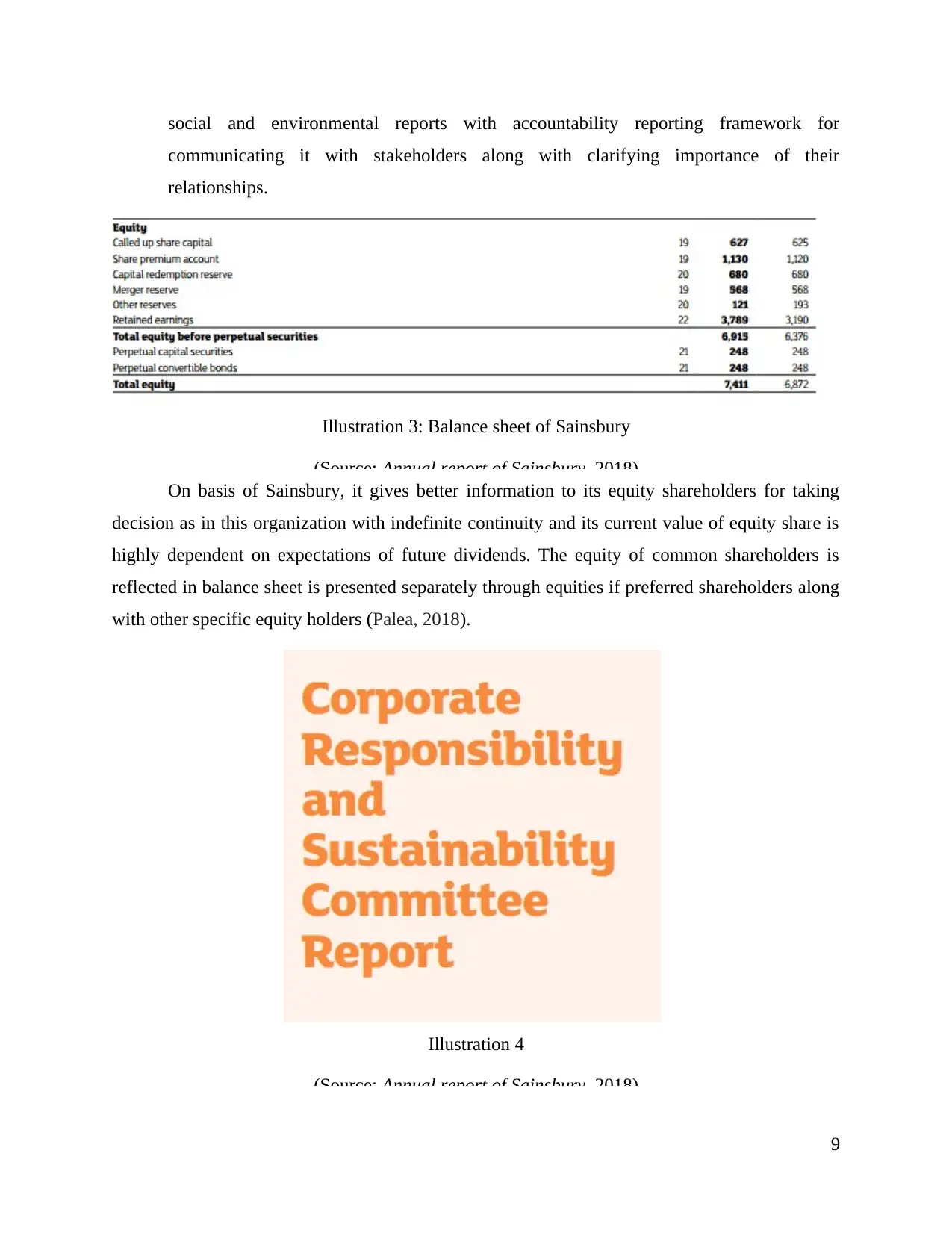

Illustration 3: Balance sheet of Sainsbury

(Source: Annual report of Sainsbury, 2018)

On basis of Sainsbury, it gives better information to its equity shareholders for taking

decision as in this organization with indefinite continuity and its current value of equity share is

highly dependent on expectations of future dividends. The equity of common shareholders is

reflected in balance sheet is presented separately through equities if preferred shareholders along

with other specific equity holders (Palea, 2018).

Illustration 4

(Source: Annual report of Sainsbury, 2018)

9

communicating it with stakeholders along with clarifying importance of their

relationships.

Illustration 3: Balance sheet of Sainsbury

(Source: Annual report of Sainsbury, 2018)

On basis of Sainsbury, it gives better information to its equity shareholders for taking

decision as in this organization with indefinite continuity and its current value of equity share is

highly dependent on expectations of future dividends. The equity of common shareholders is

reflected in balance sheet is presented separately through equities if preferred shareholders along

with other specific equity holders (Palea, 2018).

Illustration 4

(Source: Annual report of Sainsbury, 2018)

9

In the similar aspect, Sainsbury has also disclosed its social and environmental issues in

corporate responsibility and sustainability committee report where they have reduced emissions,

water use along with waste across value chain and many more.

7. Identifying differences in financial reporting throughout world and evaluating factors which

influence these differences

The factors which has evaluated theses differences are rule and principles, inventory

methods and inventory reversal. International financial reporting standards is accounting method

which is used in various countries throughout the world as Generally Accepted Accounting

Principles implemented in United States. The first factor is methodology used for assessing

process of accounting where GAAP lays special emphasis on research and in based on rules.

However, IFRS observes overall patterns and is fully based on principle. On basis of GAAP

accounting, there are exceptions or interpretation as every transaction should abide through

specific set of rules and IFRS says about potential for various interpretations of similar tax

related situations (Liu and et.al., 2018).

With context to GAAP, organization is allowed with application of LIFO and FIFO

method for estimate of inventory. Conversely, under IFRS, the LIFO method is not allowed for

inventory. In addition to this, with different methods of tracking inventory the accounting

standards differ as GAAP specifies that there is increment in market value of asset then amount

of write down could not be reversed. In similar situation in IFRS, amount of write down could be

reversed.

8. Degree of compliance of International Financial Reporting Standards

IFRS helps different country to set out accounting system because of every country has

different culture for instance – in the south pacific reign, headquarter of company keeps close

their eyes on organization branches, therefore they imply homogeneous accounting practice as

well. Countries who have low education level are not able to meet accounting standard set out by

IFRS , so they required accounting training for novice.

Apart from these national culture also impact the implementation of international

standard. Countries of south pacific inland try to adopt accounting system of developed

countries, even when these standards not suit their business (Ge and et.al., 2018). Developing

and developed country has different accounting judgments but their accounting system has

similarity with each other. Australia and Fiji has same standards for financial report even after

10

corporate responsibility and sustainability committee report where they have reduced emissions,

water use along with waste across value chain and many more.

7. Identifying differences in financial reporting throughout world and evaluating factors which

influence these differences

The factors which has evaluated theses differences are rule and principles, inventory

methods and inventory reversal. International financial reporting standards is accounting method

which is used in various countries throughout the world as Generally Accepted Accounting

Principles implemented in United States. The first factor is methodology used for assessing

process of accounting where GAAP lays special emphasis on research and in based on rules.

However, IFRS observes overall patterns and is fully based on principle. On basis of GAAP

accounting, there are exceptions or interpretation as every transaction should abide through

specific set of rules and IFRS says about potential for various interpretations of similar tax

related situations (Liu and et.al., 2018).

With context to GAAP, organization is allowed with application of LIFO and FIFO

method for estimate of inventory. Conversely, under IFRS, the LIFO method is not allowed for

inventory. In addition to this, with different methods of tracking inventory the accounting

standards differ as GAAP specifies that there is increment in market value of asset then amount

of write down could not be reversed. In similar situation in IFRS, amount of write down could be

reversed.

8. Degree of compliance of International Financial Reporting Standards

IFRS helps different country to set out accounting system because of every country has

different culture for instance – in the south pacific reign, headquarter of company keeps close

their eyes on organization branches, therefore they imply homogeneous accounting practice as

well. Countries who have low education level are not able to meet accounting standard set out by

IFRS , so they required accounting training for novice.

Apart from these national culture also impact the implementation of international

standard. Countries of south pacific inland try to adopt accounting system of developed

countries, even when these standards not suit their business (Ge and et.al., 2018). Developing

and developed country has different accounting judgments but their accounting system has

similarity with each other. Australia and Fiji has same standards for financial report even after

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.