ACCT20074 Contemporary Accounting: Financial Reporting & Analysis

VerifiedAdded on 2023/03/31

|25

|4251

|407

Report

AI Summary

This report provides a detailed analysis of contemporary accounting theory, focusing on the conceptual framework for financial reporting and sustainability reporting practices. It includes a literature review of the history and development of the conceptual framework, addressing concerns within the Australian accounting profession regarding the application of IFRSs and IASs. The report also examines the practical application of the conceptual framework within Santos Limited, an Australian energy company, assessing its compliance with accounting standards and integrated reporting practices. Furthermore, it compares sustainability reporting under different frameworks and appraises a practical entity’s integrated reporting, concluding with insights on improving financial reporting quality and comparability. Desklib provides students access to this assignment and a wealth of other resources including past papers and solved assignments.

Running head: CORPORATE ACCOUNTING

Contemporary Accounting

Name of the Student:

Name of the University:

Authors Note:

Contemporary Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary:

In order to improve the quality of financial reporting and improve comparability of financial

reports of different entities in all across the globe International Accounting Standards Board

(IASB) has issued accounting standards (IFRSs and IASs). Complying with these standards

helps in improving the quality of financial reporting of entities. A detailed discussion here shows

that how the financial reports of Santos Limited, an Australian energy company and Vivo Energy

Plc., a South African company are prepared. Whether the financial statements including

integrated reports are in compliance with applicable accounting standards shall be verified to

state the financial performance and position of these entities fairly and truthfully.

CORPORATE ACCOUNTING

Executive summary:

In order to improve the quality of financial reporting and improve comparability of financial

reports of different entities in all across the globe International Accounting Standards Board

(IASB) has issued accounting standards (IFRSs and IASs). Complying with these standards

helps in improving the quality of financial reporting of entities. A detailed discussion here shows

that how the financial reports of Santos Limited, an Australian energy company and Vivo Energy

Plc., a South African company are prepared. Whether the financial statements including

integrated reports are in compliance with applicable accounting standards shall be verified to

state the financial performance and position of these entities fairly and truthfully.

2

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Part A:..............................................................................................................................................3

Literature Review:.......................................................................................................................3

Concerns of Australian Accounting profession in respect of application of IFRSs and IASs:...4

Academic concerns:.....................................................................................................................5

Practical application of conceptual framework in an entity:.......................................................6

Part B – Integrated and Sustainability Reporting:.........................................................................16

Comparison of sustainability reporting under different frameworks:.......................................16

Rigour of conventional accounting:...........................................................................................17

Applicability of theory:..............................................................................................................18

Index of various components of an integrated reporting:..........................................................18

Appraisal of practical entity’s integrated reporting:..................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................22

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Part A:..............................................................................................................................................3

Literature Review:.......................................................................................................................3

Concerns of Australian Accounting profession in respect of application of IFRSs and IASs:...4

Academic concerns:.....................................................................................................................5

Practical application of conceptual framework in an entity:.......................................................6

Part B – Integrated and Sustainability Reporting:.........................................................................16

Comparison of sustainability reporting under different frameworks:.......................................16

Rigour of conventional accounting:...........................................................................................17

Applicability of theory:..............................................................................................................18

Index of various components of an integrated reporting:..........................................................18

Appraisal of practical entity’s integrated reporting:..................................................................20

Conclusion:....................................................................................................................................20

References:....................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction:

IASB is the highest accounting standards board internationally responsible to formulate and issue

accounting standards globally. The national accounting standards boards of different nations are

members of IASB. The objective of issuing globally acceptable accounting standards is to reduce

alternative accounting principles and policies to record financial transactions and in preparing

financial statements from such accounting records. This will help in increasing the qualitative

characteristics of financial reports such as comparability, completeness and objectivity of

financial statements. A detailed discussion in respect to the development and application of

IASB and IFRSs is provided below.

Part A:

Literature Review:

A conceptual framework in financial reporting can be defined as the summary of accounting

principles and policies developed to reduce the limitations in financial reporting to improve the

quality of financial reports. The objectives of conceptual financial reporting framework include

developing a framework for setting accounting standards, resolving disputes in accounting

related matters and strengthening fundamental accounting principles to ensure there is no

requirement to repeat the accounting standards. Most of the ASB standards issued in the United

Kingdom in last few years are based on rules rather than principles. Rule based accounting

standards increase the tick box mentality in financial reporting instead of looking to improve the

quality of financial reporting. This is because the accountants are mainly concerned with

following the rules instead of improving the quality of financial reporting under rule based

accounting standards (Alzoubi, 2012). As a result UK is moving towards a principle based

CORPORATE ACCOUNTING

Introduction:

IASB is the highest accounting standards board internationally responsible to formulate and issue

accounting standards globally. The national accounting standards boards of different nations are

members of IASB. The objective of issuing globally acceptable accounting standards is to reduce

alternative accounting principles and policies to record financial transactions and in preparing

financial statements from such accounting records. This will help in increasing the qualitative

characteristics of financial reports such as comparability, completeness and objectivity of

financial statements. A detailed discussion in respect to the development and application of

IASB and IFRSs is provided below.

Part A:

Literature Review:

A conceptual framework in financial reporting can be defined as the summary of accounting

principles and policies developed to reduce the limitations in financial reporting to improve the

quality of financial reports. The objectives of conceptual financial reporting framework include

developing a framework for setting accounting standards, resolving disputes in accounting

related matters and strengthening fundamental accounting principles to ensure there is no

requirement to repeat the accounting standards. Most of the ASB standards issued in the United

Kingdom in last few years are based on rules rather than principles. Rule based accounting

standards increase the tick box mentality in financial reporting instead of looking to improve the

quality of financial reporting. This is because the accountants are mainly concerned with

following the rules instead of improving the quality of financial reporting under rule based

accounting standards (Alzoubi, 2012). As a result UK is moving towards a principle based

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

accounting standards from rule based accounting standards to enhance the quality financial

reports.

In United States of America, the accounting standards are completely based on the accounting

rules and regulations with US GAAP as the premier accounting standards to be followed in

preparation and presentation of financial reports in the country. Thus, US based accounting

concept is more rigid as compared to the accounting standards in different countries which are

principle based. US GAAP sets out detailed and specific rules to be followed for specific

accounting problems. UK though is moving towards a principle based accounting standards US

has yet to implement the principle based IFRSs and IASs issued by the IASB to show any real

intent of moving towards principle based accounting standards (Azam, 2017).

Australian Accounting Standards Board (AASB) on the other hand has taken a middle route

where it has used both principles and rules to develop accounting standards to be followed by

business non business entities to comply with the conceptual framework of financial reporting in

the country. AASBs have the characteristics of principles and rules. Thus, the conceptual

framework of financial reporting in Australia is one which is flexible yet rigid in its own way.

The objective of AASB is to ensure that the entities operating in the country are complying with

applicable accounting standards to record, summarize and classify financial transactions properly

(Bertoni & De Rosa, 2013).

Concerns of Australian Accounting profession in respect of application of IFRSs and IASs:

Australian accounting professionals are obliged to comply with the professional and ethical

standards while discharging their attest responsibilities as professional accountants in the

country. The accountants in the country must adhere to the applicable standards in the country

CORPORATE ACCOUNTING

accounting standards from rule based accounting standards to enhance the quality financial

reports.

In United States of America, the accounting standards are completely based on the accounting

rules and regulations with US GAAP as the premier accounting standards to be followed in

preparation and presentation of financial reports in the country. Thus, US based accounting

concept is more rigid as compared to the accounting standards in different countries which are

principle based. US GAAP sets out detailed and specific rules to be followed for specific

accounting problems. UK though is moving towards a principle based accounting standards US

has yet to implement the principle based IFRSs and IASs issued by the IASB to show any real

intent of moving towards principle based accounting standards (Azam, 2017).

Australian Accounting Standards Board (AASB) on the other hand has taken a middle route

where it has used both principles and rules to develop accounting standards to be followed by

business non business entities to comply with the conceptual framework of financial reporting in

the country. AASBs have the characteristics of principles and rules. Thus, the conceptual

framework of financial reporting in Australia is one which is flexible yet rigid in its own way.

The objective of AASB is to ensure that the entities operating in the country are complying with

applicable accounting standards to record, summarize and classify financial transactions properly

(Bertoni & De Rosa, 2013).

Concerns of Australian Accounting profession in respect of application of IFRSs and IASs:

Australian accounting professionals are obliged to comply with the professional and ethical

standards while discharging their attest responsibilities as professional accountants in the

country. The accountants in the country must adhere to the applicable standards in the country

5

CORPORATE ACCOUNTING

issued by the AASB. The accounting information must compliment the applicable standards of

accounting in the country to ensure these are in line with the conceptual framework of financial

reporting in the country. The accounting professionals are mainly concerned with the

implications of compliance of accounting and financial reports with IFRSs and IASs issued by

the IASB. Currently the entities operating in the country are following AASBs issued by the

AASB. However, with ever increasing role of IASB in achieving global harmony in financial

reporting the AASBs are also aligning with IFRSs and IASs. This is certainly a concern for the

accounting profession in the country as the existing qualified accountants in the country are not

fully aware of all IFRSs and IASs. Thus, before the complete adoption of IFRSs and IASs to

prepare and present financial reports in the country the professional accountants in the country

must be equipped to understand the implications of different IFRSs and IASs. Providing

appropriate training to the professionals on IFRSs and IASs and keeping them informed about

new amendments and changes in these standards shall be helpful to the accounting professionals

in the country (Botez, 2014).

Academic concerns:

Marthinus C. Gerber, Aurona J. Gerber and Alta van der Merwe have discussed the importance

of a quality financial reporting framework in the article, “The conceptual framework for financial

reporting as a domain ontology.” The objective behind development of conceptual framework of

financial reporting is to provide the users and preparers of financial reports proper guidelines.

However, the accounting community in general believes that the conceptual framework has

failed to achieve that objective. This is because the alternative accounting principles and policies

despite development and issuance of number of accounting standards are still more than few in

many specific areas of accounting. As a result the confusion and lack of standardization in

CORPORATE ACCOUNTING

issued by the AASB. The accounting information must compliment the applicable standards of

accounting in the country to ensure these are in line with the conceptual framework of financial

reporting in the country. The accounting professionals are mainly concerned with the

implications of compliance of accounting and financial reports with IFRSs and IASs issued by

the IASB. Currently the entities operating in the country are following AASBs issued by the

AASB. However, with ever increasing role of IASB in achieving global harmony in financial

reporting the AASBs are also aligning with IFRSs and IASs. This is certainly a concern for the

accounting profession in the country as the existing qualified accountants in the country are not

fully aware of all IFRSs and IASs. Thus, before the complete adoption of IFRSs and IASs to

prepare and present financial reports in the country the professional accountants in the country

must be equipped to understand the implications of different IFRSs and IASs. Providing

appropriate training to the professionals on IFRSs and IASs and keeping them informed about

new amendments and changes in these standards shall be helpful to the accounting professionals

in the country (Botez, 2014).

Academic concerns:

Marthinus C. Gerber, Aurona J. Gerber and Alta van der Merwe have discussed the importance

of a quality financial reporting framework in the article, “The conceptual framework for financial

reporting as a domain ontology.” The objective behind development of conceptual framework of

financial reporting is to provide the users and preparers of financial reports proper guidelines.

However, the accounting community in general believes that the conceptual framework has

failed to achieve that objective. This is because the alternative accounting principles and policies

despite development and issuance of number of accounting standards are still more than few in

many specific areas of accounting. As a result the confusion and lack of standardization in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

accounting and financial reporting are still very much in existence. Thus, the users of financial

reports have not been fully assured with the ability of financial reports to disclose the true and

correct financial results and position of an entity. Similarly, the accountants who are responsible

to prepare and present financial statements have more than one alternative accounting principle

and policies available to disclose certain items in financial reports. The inability of accounting

standards to standardize accounting principles and policies to reduce the alternative accounting

practices to one is one of the main restricting factors in conceptual framework of financial

reporting to be effective (Ceustermans, Breesch & Branson, 2012).

Practical application of conceptual framework in an entity:

South Australia Northern Territory Oil Search (Santos) Limited is an Australian energy company

is the country’s second largest oil and gas producer. The company produces gas to supply in the

Australian states and territories only. Thus, it is a domestic gas producer and caters its services

within the length and breadth of the country. The company is under obligation to comply with

the Corporations Act 2001 to report its performance and position by preparing annual report as

per the act. The company has prepared annual report as per the requirements of Corporations Act

2001 to circulate the reports to the stakeholders of the company. The annual reports of a

company is prepared to provide the stakeholders of the company useful information about its

functioning and operations. Financial statements are an integral part of annual reports of a

company.

As per conceptual framework of financial reporting a business entity must prepare a complete set

of financial statements that shall include income statement or statement of profit and loss,

Balance sheet or statement of financial position, statement of cash flows, statement of changes in

equity and notes to accounts. In case of a non-business entity instead of profit and loss statement

CORPORATE ACCOUNTING

accounting and financial reporting are still very much in existence. Thus, the users of financial

reports have not been fully assured with the ability of financial reports to disclose the true and

correct financial results and position of an entity. Similarly, the accountants who are responsible

to prepare and present financial statements have more than one alternative accounting principle

and policies available to disclose certain items in financial reports. The inability of accounting

standards to standardize accounting principles and policies to reduce the alternative accounting

practices to one is one of the main restricting factors in conceptual framework of financial

reporting to be effective (Ceustermans, Breesch & Branson, 2012).

Practical application of conceptual framework in an entity:

South Australia Northern Territory Oil Search (Santos) Limited is an Australian energy company

is the country’s second largest oil and gas producer. The company produces gas to supply in the

Australian states and territories only. Thus, it is a domestic gas producer and caters its services

within the length and breadth of the country. The company is under obligation to comply with

the Corporations Act 2001 to report its performance and position by preparing annual report as

per the act. The company has prepared annual report as per the requirements of Corporations Act

2001 to circulate the reports to the stakeholders of the company. The annual reports of a

company is prepared to provide the stakeholders of the company useful information about its

functioning and operations. Financial statements are an integral part of annual reports of a

company.

As per conceptual framework of financial reporting a business entity must prepare a complete set

of financial statements that shall include income statement or statement of profit and loss,

Balance sheet or statement of financial position, statement of cash flows, statement of changes in

equity and notes to accounts. In case of a non-business entity instead of profit and loss statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

an income and expenditure statement is provided. The conceptual framework of financial

reporting also requires compliance with accounting standards applicable in the country while

recording financial transactions in the books of accounts of an organization as well as in

preparing financial reports from such records.

An energy company in addition to the requirements of complying with the financial reporting

requirements also have the responsibility to comply with the social and environmental

requirements to report matters related to corporate social responsibilities. It is clear from the

annual report 2018 of the company that it has not prepared an integrated statement outlining the

financial and nonfinancial elements in company’s business operations. However, the company

has prepared a complete set of financial statements as per the requirement of conceptual

framework of financial reporting. The company has prepared income statement, comprehensive

income statement, statement of financial position, cash flow statement, statement of changes in

equity and notes to accounts ("Financial Statements", 2012).

Notes to the consolidated financial statements of the company outlines the following:

I. The provisions of Corporations Act 2001, the accounting standards issued by the

AASB and other pronouncements made by the Board have been followed in

preparation and presentation of consolidated and indidviauls financial reports of the

company.

II. The financial statements are in compliance with the AASBs and IFRSs as issued by

the AASB and IASB. Along with that the new amendments and notifications issued

by the respective boards have also been followed.

CORPORATE ACCOUNTING

an income and expenditure statement is provided. The conceptual framework of financial

reporting also requires compliance with accounting standards applicable in the country while

recording financial transactions in the books of accounts of an organization as well as in

preparing financial reports from such records.

An energy company in addition to the requirements of complying with the financial reporting

requirements also have the responsibility to comply with the social and environmental

requirements to report matters related to corporate social responsibilities. It is clear from the

annual report 2018 of the company that it has not prepared an integrated statement outlining the

financial and nonfinancial elements in company’s business operations. However, the company

has prepared a complete set of financial statements as per the requirement of conceptual

framework of financial reporting. The company has prepared income statement, comprehensive

income statement, statement of financial position, cash flow statement, statement of changes in

equity and notes to accounts ("Financial Statements", 2012).

Notes to the consolidated financial statements of the company outlines the following:

I. The provisions of Corporations Act 2001, the accounting standards issued by the

AASB and other pronouncements made by the Board have been followed in

preparation and presentation of consolidated and indidviauls financial reports of the

company.

II. The financial statements are in compliance with the AASBs and IFRSs as issued by

the AASB and IASB. Along with that the new amendments and notifications issued

by the respective boards have also been followed.

8

CORPORATE ACCOUNTING

III. The financial statements have been prepared on historical cost basis except financial

instruments that have been valued using fair value concept of accounting.

Basis of preparation of accounting and key events:

The management has used assumptions and judgments to apply accounting policies and

principles where more than one alternative accounting principle, and policies were available. The

key events that influenced the financial performance and position of the company include

production of 58.9 mmboe and sales of 78.3 mmboe. In addition the sale of non-core assets of

$152 million with a gain of $112 million on disposal along with increase in net debt to $3,549

million have influenced the financial state and affairs of the company (Iatridis, 2016).

The company has used AASB 15 to recognize revenue in the books of accounts to comply with

the financial reporting requirements. Before getting into detailed discussion about the recognition

and measurement of different items of revenue and expenditures in the income statement of the

company a complied income statement of the company over the last four years is produced

below as a point of reference. The annual reports of last three years have been used to comply

the income statement of the company below.

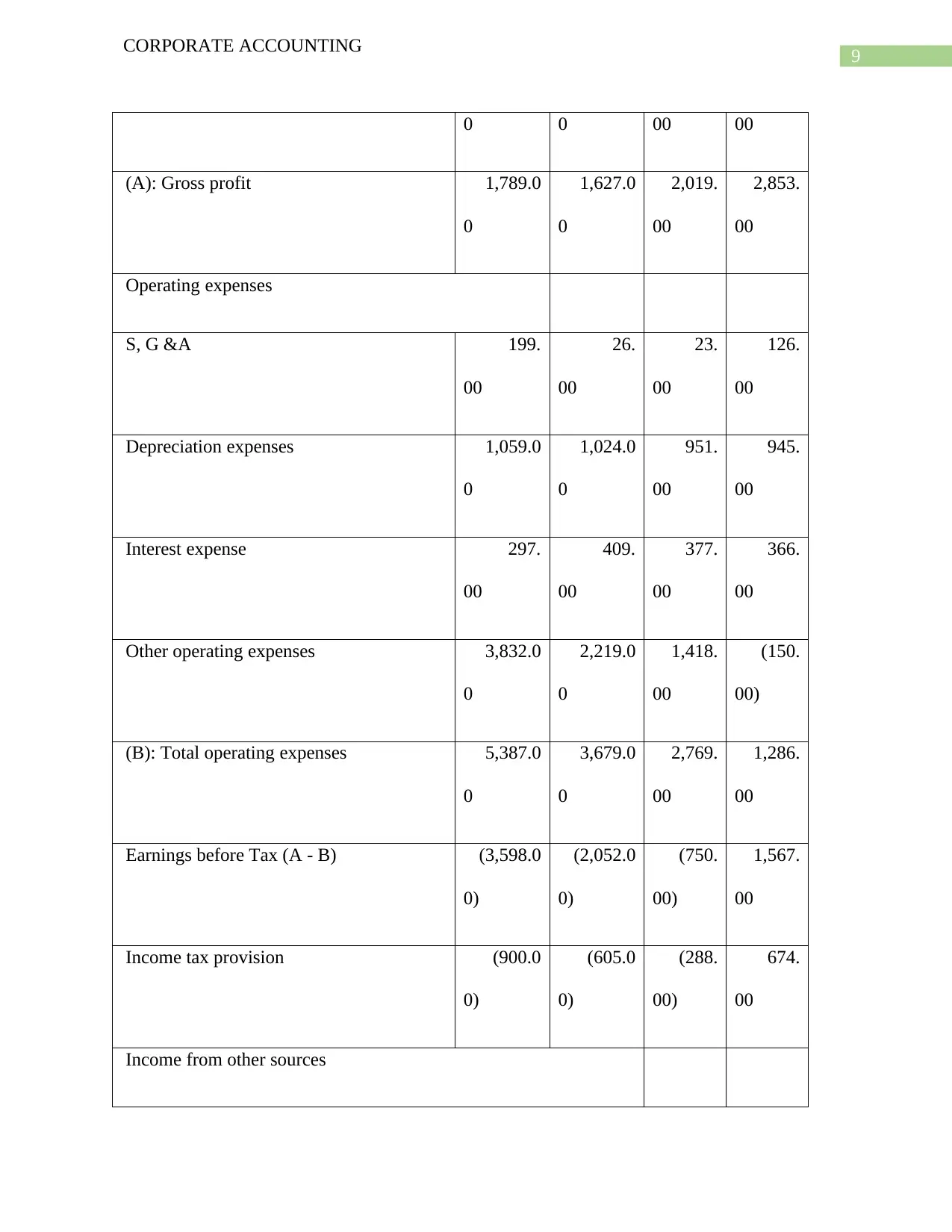

INCOME STATEMENT OF SANTOS LTD.

AU$ millions 2015-12 2016-12 2017-

12

2018-

12

Income from supply of energy 3,246.0

0

3,585.0

0

3,983.

00

5,186.

00

Less: Cost of Production 1,457.0 1,958.0 1,964. 2,332.

CORPORATE ACCOUNTING

III. The financial statements have been prepared on historical cost basis except financial

instruments that have been valued using fair value concept of accounting.

Basis of preparation of accounting and key events:

The management has used assumptions and judgments to apply accounting policies and

principles where more than one alternative accounting principle, and policies were available. The

key events that influenced the financial performance and position of the company include

production of 58.9 mmboe and sales of 78.3 mmboe. In addition the sale of non-core assets of

$152 million with a gain of $112 million on disposal along with increase in net debt to $3,549

million have influenced the financial state and affairs of the company (Iatridis, 2016).

The company has used AASB 15 to recognize revenue in the books of accounts to comply with

the financial reporting requirements. Before getting into detailed discussion about the recognition

and measurement of different items of revenue and expenditures in the income statement of the

company a complied income statement of the company over the last four years is produced

below as a point of reference. The annual reports of last three years have been used to comply

the income statement of the company below.

INCOME STATEMENT OF SANTOS LTD.

AU$ millions 2015-12 2016-12 2017-

12

2018-

12

Income from supply of energy 3,246.0

0

3,585.0

0

3,983.

00

5,186.

00

Less: Cost of Production 1,457.0 1,958.0 1,964. 2,332.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

0 0 00 00

(A): Gross profit 1,789.0

0

1,627.0

0

2,019.

00

2,853.

00

Operating expenses

S, G &A 199.

00

26.

00

23.

00

126.

00

Depreciation expenses 1,059.0

0

1,024.0

0

951.

00

945.

00

Interest expense 297.

00

409.

00

377.

00

366.

00

Other operating expenses 3,832.0

0

2,219.0

0

1,418.

00

(150.

00)

(B): Total operating expenses 5,387.0

0

3,679.0

0

2,769.

00

1,286.

00

Earnings before Tax (A - B) (3,598.0

0)

(2,052.0

0)

(750.

00)

1,567.

00

Income tax provision (900.0

0)

(605.0

0)

(288.

00)

674.

00

Income from other sources

CORPORATE ACCOUNTING

0 0 00 00

(A): Gross profit 1,789.0

0

1,627.0

0

2,019.

00

2,853.

00

Operating expenses

S, G &A 199.

00

26.

00

23.

00

126.

00

Depreciation expenses 1,059.0

0

1,024.0

0

951.

00

945.

00

Interest expense 297.

00

409.

00

377.

00

366.

00

Other operating expenses 3,832.0

0

2,219.0

0

1,418.

00

(150.

00)

(B): Total operating expenses 5,387.0

0

3,679.0

0

2,769.

00

1,286.

00

Earnings before Tax (A - B) (3,598.0

0)

(2,052.0

0)

(750.

00)

1,567.

00

Income tax provision (900.0

0)

(605.0

0)

(288.

00)

674.

00

Income from other sources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Earnings from continuing operations after

tax

(2,698.0

0)

(1,447.0

0)

(462.

00)

893.

00

Net earnings available to common

shareholders

(2,698.0

0)

(1,447.0

0)

(462.

00)

893.

00

Earnings per share

Basic (2.3

4)

(0.8

0)

(0.

22)

0.

43

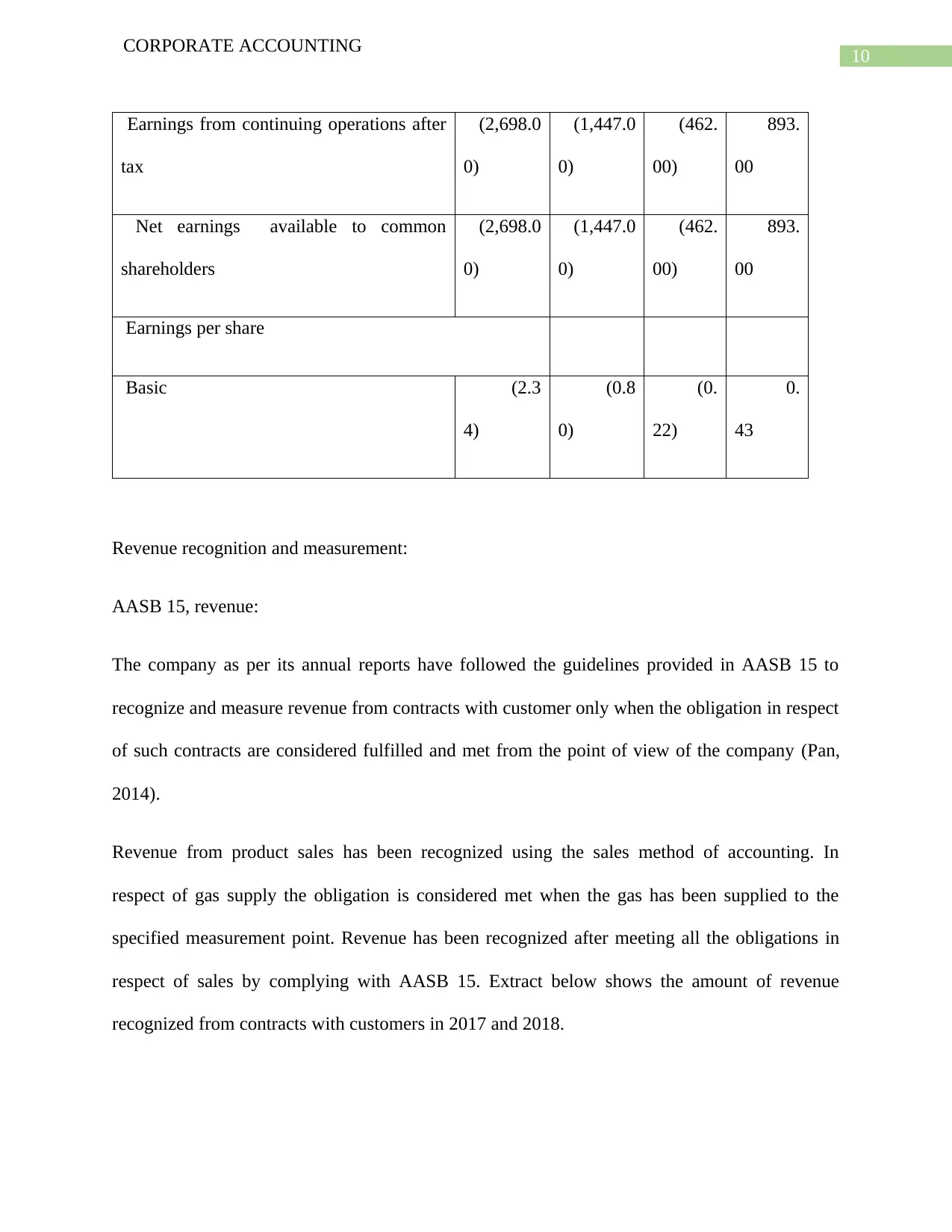

Revenue recognition and measurement:

AASB 15, revenue:

The company as per its annual reports have followed the guidelines provided in AASB 15 to

recognize and measure revenue from contracts with customer only when the obligation in respect

of such contracts are considered fulfilled and met from the point of view of the company (Pan,

2014).

Revenue from product sales has been recognized using the sales method of accounting. In

respect of gas supply the obligation is considered met when the gas has been supplied to the

specified measurement point. Revenue has been recognized after meeting all the obligations in

respect of sales by complying with AASB 15. Extract below shows the amount of revenue

recognized from contracts with customers in 2017 and 2018.

CORPORATE ACCOUNTING

Earnings from continuing operations after

tax

(2,698.0

0)

(1,447.0

0)

(462.

00)

893.

00

Net earnings available to common

shareholders

(2,698.0

0)

(1,447.0

0)

(462.

00)

893.

00

Earnings per share

Basic (2.3

4)

(0.8

0)

(0.

22)

0.

43

Revenue recognition and measurement:

AASB 15, revenue:

The company as per its annual reports have followed the guidelines provided in AASB 15 to

recognize and measure revenue from contracts with customer only when the obligation in respect

of such contracts are considered fulfilled and met from the point of view of the company (Pan,

2014).

Revenue from product sales has been recognized using the sales method of accounting. In

respect of gas supply the obligation is considered met when the gas has been supplied to the

specified measurement point. Revenue has been recognized after meeting all the obligations in

respect of sales by complying with AASB 15. Extract below shows the amount of revenue

recognized from contracts with customers in 2017 and 2018.

11

CORPORATE ACCOUNTING

Contract assets:

The company has recognized contract assets on acquisition of Quadrant Energy by following the

AASB 15 and relevant notification issued by the AASB in this regard. The difference between

the contract price and the market price at the date of acquisition of Quadrant energy has been

recognized as contract asset as per the requirements of AASB 16 (2019).

Contract liabilities:

Again liabilities attracted from contracts with customers has been measured and recorded in the

books of accounts by following the guidelines provided in AASB 15. The extract below shows

the amount of contract assets and contract liabilities reported by the company in 2017 and 2018

by following the requirements of AASB 15.

CORPORATE ACCOUNTING

Contract assets:

The company has recognized contract assets on acquisition of Quadrant Energy by following the

AASB 15 and relevant notification issued by the AASB in this regard. The difference between

the contract price and the market price at the date of acquisition of Quadrant energy has been

recognized as contract asset as per the requirements of AASB 16 (2019).

Contract liabilities:

Again liabilities attracted from contracts with customers has been measured and recorded in the

books of accounts by following the guidelines provided in AASB 15. The extract below shows

the amount of contract assets and contract liabilities reported by the company in 2017 and 2018

by following the requirements of AASB 15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.