ACC510 Financial Reporting Task 2 – Major Assignment, Semester 2

VerifiedAdded on 2020/03/16

|11

|2453

|135

Homework Assignment

AI Summary

This document presents a comprehensive solution for ACC510 Financial Reporting Task 2, covering various aspects of financial accounting. It begins with a case study analysis based on AASB 116, focusing on fair value measurement of property, plant, and equipment, including considerations for 'highest and best use' and application to aged care homes. The solution then addresses Exercise 7.14, applying AASB 136 to impairment testing, including detailed calculations and journal entries for both 2016 and 2017. Case Study 6.1 is analyzed, differentiating between research and development phases according to AASB 138, and explaining the accounting treatment for research and development costs. Finally, the solution tackles Exercise 9.19, which involves accounting for employee benefits and defined benefit plans, including calculations for the deficit of the fund, net defined benefit liability, net interest, and reconciliation, along with a summary journal entry. References to relevant accounting standards and literature are also provided.

ACC510 - Financial Reporting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1.Case Study 3.1.....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................5

2. Impairment Test 31/12/17....................................................................................................5

a. Calculations........................................................................................................................5

b. General Journal Entries 31/12/17:.....................................................................................6

Question 3.Case Study 6.1.....................................................................................................................7

Accounting Justification:................................................................................................................7

Relevant Issues:.............................................................................................................................7

1. Difference between two phases:...........................................................................................7

2. Accounting for Research & Development:.............................................................................7

3. Decision / Conclusion / Reasons and Justification:................................................................8

Question 4. Ex 9.19................................................................................................................................8

Accounting Justification:................................................................................................................8

Relevant Issues:.............................................................................................................................8

1. Deficit of Fund.......................................................................................................................8

2. Net Defined Benefit Liability..................................................................................................8

3. Net Interest............................................................................................................................8

4. Reconciliation........................................................................................................................9

5. Summary Journal.................................................................................................................10

References...........................................................................................................................................11

Page 2 of 11

Question 1.Case Study 3.1.....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................5

2. Impairment Test 31/12/17....................................................................................................5

a. Calculations........................................................................................................................5

b. General Journal Entries 31/12/17:.....................................................................................6

Question 3.Case Study 6.1.....................................................................................................................7

Accounting Justification:................................................................................................................7

Relevant Issues:.............................................................................................................................7

1. Difference between two phases:...........................................................................................7

2. Accounting for Research & Development:.............................................................................7

3. Decision / Conclusion / Reasons and Justification:................................................................8

Question 4. Ex 9.19................................................................................................................................8

Accounting Justification:................................................................................................................8

Relevant Issues:.............................................................................................................................8

1. Deficit of Fund.......................................................................................................................8

2. Net Defined Benefit Liability..................................................................................................8

3. Net Interest............................................................................................................................8

4. Reconciliation........................................................................................................................9

5. Summary Journal.................................................................................................................10

References...........................................................................................................................................11

Page 2 of 11

Question 1.Case Study 3.1

Accounting Justification:

AASB 116 outlines the accounting treatment for property, plant and equipment. For the

measurement of fair value of these tangible asset this standards lays down provisions for recognition

and measurement of fair value (AASB 116.Property Plant and Equipment, 2016). The initial cost of

acquiring the asset and the subsequent cost for repairs and maintenance are included in the cost of

the asset for the measurement of fair value. The measurement of any item of plant, property and

equipment is done at cost. The cost of an item will be the cash price paid. For the purpose of

recognition the entity can use the revaluation model or cost model provided by the standard. As per

the cost model the cost of the asset less its accumulated depreciation would be the book value. The

revaluation model measures fair value of any asset at a particular date after considering the market

participants interest in the property.

Relevant Issues:

1. Highest & Best Use

The concept of highest and best use reflects an assumption upon which the fair value

of the asset is based. For the purpose of determining most probable selling price it may

be appropriate to reflect highest and best use. Determination of highest and best use

involves recognizing the motivations of market participants. These motivations are

based up on expectations of benefits that will accrue to property owner.

2. Application to aged care home

When not for profit entities acquire an asset as result of charity, then the cost of the

item will be its fair value measured at the date of acquiring the asset (Collings, 2015). The

initial recognition is done at fair value. For the Not- For- profit entities it is reasonable to

valuate an asset at the cost model, after the initial recognition. The fair value is generally

measured by the market evidence undertaken by professional.

3. Two possible uses

Thus, two possible uses of any asset will be its current use and the highest and the best use.

The physical assets of old aged home are not put to their best use. If the asset is sold to any

market participant, he will use the asset to generate profit. This creates discrepancy in

measuring the fair value.

Page 3 of 11

Accounting Justification:

AASB 116 outlines the accounting treatment for property, plant and equipment. For the

measurement of fair value of these tangible asset this standards lays down provisions for recognition

and measurement of fair value (AASB 116.Property Plant and Equipment, 2016). The initial cost of

acquiring the asset and the subsequent cost for repairs and maintenance are included in the cost of

the asset for the measurement of fair value. The measurement of any item of plant, property and

equipment is done at cost. The cost of an item will be the cash price paid. For the purpose of

recognition the entity can use the revaluation model or cost model provided by the standard. As per

the cost model the cost of the asset less its accumulated depreciation would be the book value. The

revaluation model measures fair value of any asset at a particular date after considering the market

participants interest in the property.

Relevant Issues:

1. Highest & Best Use

The concept of highest and best use reflects an assumption upon which the fair value

of the asset is based. For the purpose of determining most probable selling price it may

be appropriate to reflect highest and best use. Determination of highest and best use

involves recognizing the motivations of market participants. These motivations are

based up on expectations of benefits that will accrue to property owner.

2. Application to aged care home

When not for profit entities acquire an asset as result of charity, then the cost of the

item will be its fair value measured at the date of acquiring the asset (Collings, 2015). The

initial recognition is done at fair value. For the Not- For- profit entities it is reasonable to

valuate an asset at the cost model, after the initial recognition. The fair value is generally

measured by the market evidence undertaken by professional.

3. Two possible uses

Thus, two possible uses of any asset will be its current use and the highest and the best use.

The physical assets of old aged home are not put to their best use. If the asset is sold to any

market participant, he will use the asset to generate profit. This creates discrepancy in

measuring the fair value.

Page 3 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2. Ex 7.14

Accounting Justification:

AASB 136 provides provision relating to impairment of assets. Para 58 to 64 of the specified

standard provides specification relating to recognition and measurement of impairment loss

on assets.

Relevant Issues:

Para 104-108 specifies the provision relating to impairment of loss on cash generated unit.

Same provision have been applied in present case in order the ascertain capital loss on cash

generating unit.

1. Impairment Test 31/12/16

a. Calculations:

Impairment loss of Time

Total carried value of Time - Recoverable value of Time = Impairment loss (Liang and Riedl,

2013)

$1244 -$1044

=$200

Allocation of impairment loss to specified asset:

Goodwill

Impairment loss will be provided to goodwill till its value becomes zero (Capalbo, 2013); thus out of

$200, $25 will be allocated to goodwill.

Patent

As fair value of patent at the end of year is individually available i.e. $220; thus the same will

recorded at books at this value. The amount of loss allocated to patent will be $240- $220 i.e.$20

Plant

The remaining amount of impairment loss will be allocated to plant i.e. ($ 200 -$25 -$20) $155. Thus,

the amount at which plant will be recorded in books of accounts will be ($850- $155) i.e. $ 695.

Impairment loss of Leisure

Total carried value of Time - Recoverable value of Time = Impairment loss

=$1002 -$990

=$12

Allocation of impairment loss to specified asset:

Page 4 of 11

Accounting Justification:

AASB 136 provides provision relating to impairment of assets. Para 58 to 64 of the specified

standard provides specification relating to recognition and measurement of impairment loss

on assets.

Relevant Issues:

Para 104-108 specifies the provision relating to impairment of loss on cash generated unit.

Same provision have been applied in present case in order the ascertain capital loss on cash

generating unit.

1. Impairment Test 31/12/16

a. Calculations:

Impairment loss of Time

Total carried value of Time - Recoverable value of Time = Impairment loss (Liang and Riedl,

2013)

$1244 -$1044

=$200

Allocation of impairment loss to specified asset:

Goodwill

Impairment loss will be provided to goodwill till its value becomes zero (Capalbo, 2013); thus out of

$200, $25 will be allocated to goodwill.

Patent

As fair value of patent at the end of year is individually available i.e. $220; thus the same will

recorded at books at this value. The amount of loss allocated to patent will be $240- $220 i.e.$20

Plant

The remaining amount of impairment loss will be allocated to plant i.e. ($ 200 -$25 -$20) $155. Thus,

the amount at which plant will be recorded in books of accounts will be ($850- $155) i.e. $ 695.

Impairment loss of Leisure

Total carried value of Time - Recoverable value of Time = Impairment loss

=$1002 -$990

=$12

Allocation of impairment loss to specified asset:

Page 4 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

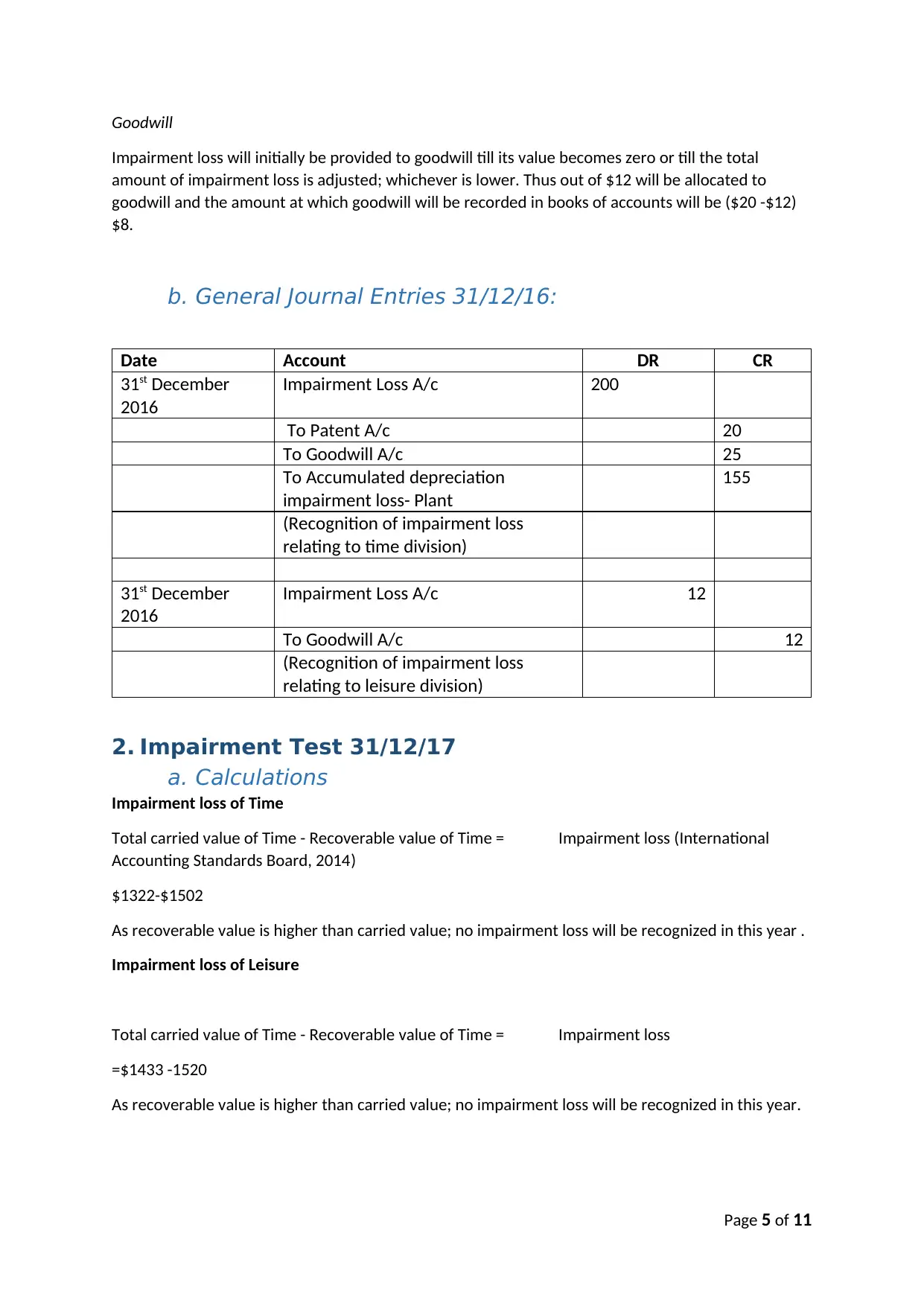

Goodwill

Impairment loss will initially be provided to goodwill till its value becomes zero or till the total

amount of impairment loss is adjusted; whichever is lower. Thus out of $12 will be allocated to

goodwill and the amount at which goodwill will be recorded in books of accounts will be ($20 -$12)

$8.

b. General Journal Entries 31/12/16:

Date Account DR CR

31st December

2016

Impairment Loss A/c 200

To Patent A/c 20

To Goodwill A/c 25

To Accumulated depreciation

impairment loss- Plant

155

(Recognition of impairment loss

relating to time division)

31st December

2016

Impairment Loss A/c 12

To Goodwill A/c 12

(Recognition of impairment loss

relating to leisure division)

2. Impairment Test 31/12/17

a. Calculations

Impairment loss of Time

Total carried value of Time - Recoverable value of Time = Impairment loss (International

Accounting Standards Board, 2014)

$1322-$1502

As recoverable value is higher than carried value; no impairment loss will be recognized in this year .

Impairment loss of Leisure

Total carried value of Time - Recoverable value of Time = Impairment loss

=$1433 -1520

As recoverable value is higher than carried value; no impairment loss will be recognized in this year.

Page 5 of 11

Impairment loss will initially be provided to goodwill till its value becomes zero or till the total

amount of impairment loss is adjusted; whichever is lower. Thus out of $12 will be allocated to

goodwill and the amount at which goodwill will be recorded in books of accounts will be ($20 -$12)

$8.

b. General Journal Entries 31/12/16:

Date Account DR CR

31st December

2016

Impairment Loss A/c 200

To Patent A/c 20

To Goodwill A/c 25

To Accumulated depreciation

impairment loss- Plant

155

(Recognition of impairment loss

relating to time division)

31st December

2016

Impairment Loss A/c 12

To Goodwill A/c 12

(Recognition of impairment loss

relating to leisure division)

2. Impairment Test 31/12/17

a. Calculations

Impairment loss of Time

Total carried value of Time - Recoverable value of Time = Impairment loss (International

Accounting Standards Board, 2014)

$1322-$1502

As recoverable value is higher than carried value; no impairment loss will be recognized in this year .

Impairment loss of Leisure

Total carried value of Time - Recoverable value of Time = Impairment loss

=$1433 -1520

As recoverable value is higher than carried value; no impairment loss will be recognized in this year.

Page 5 of 11

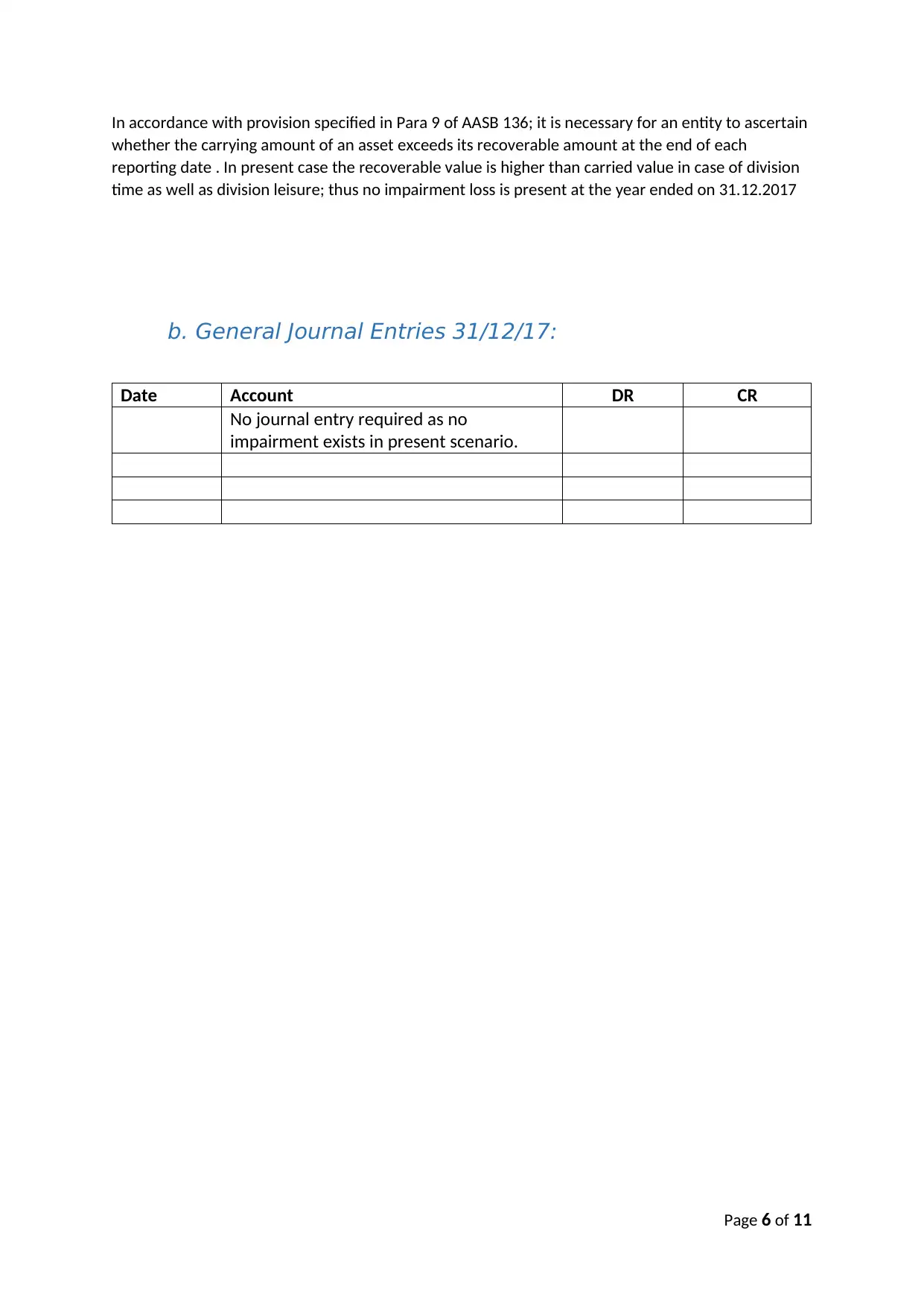

In accordance with provision specified in Para 9 of AASB 136; it is necessary for an entity to ascertain

whether the carrying amount of an asset exceeds its recoverable amount at the end of each

reporting date . In present case the recoverable value is higher than carried value in case of division

time as well as division leisure; thus no impairment loss is present at the year ended on 31.12.2017

b. General Journal Entries 31/12/17:

Date Account DR CR

No journal entry required as no

impairment exists in present scenario.

Page 6 of 11

whether the carrying amount of an asset exceeds its recoverable amount at the end of each

reporting date . In present case the recoverable value is higher than carried value in case of division

time as well as division leisure; thus no impairment loss is present at the year ended on 31.12.2017

b. General Journal Entries 31/12/17:

Date Account DR CR

No journal entry required as no

impairment exists in present scenario.

Page 6 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

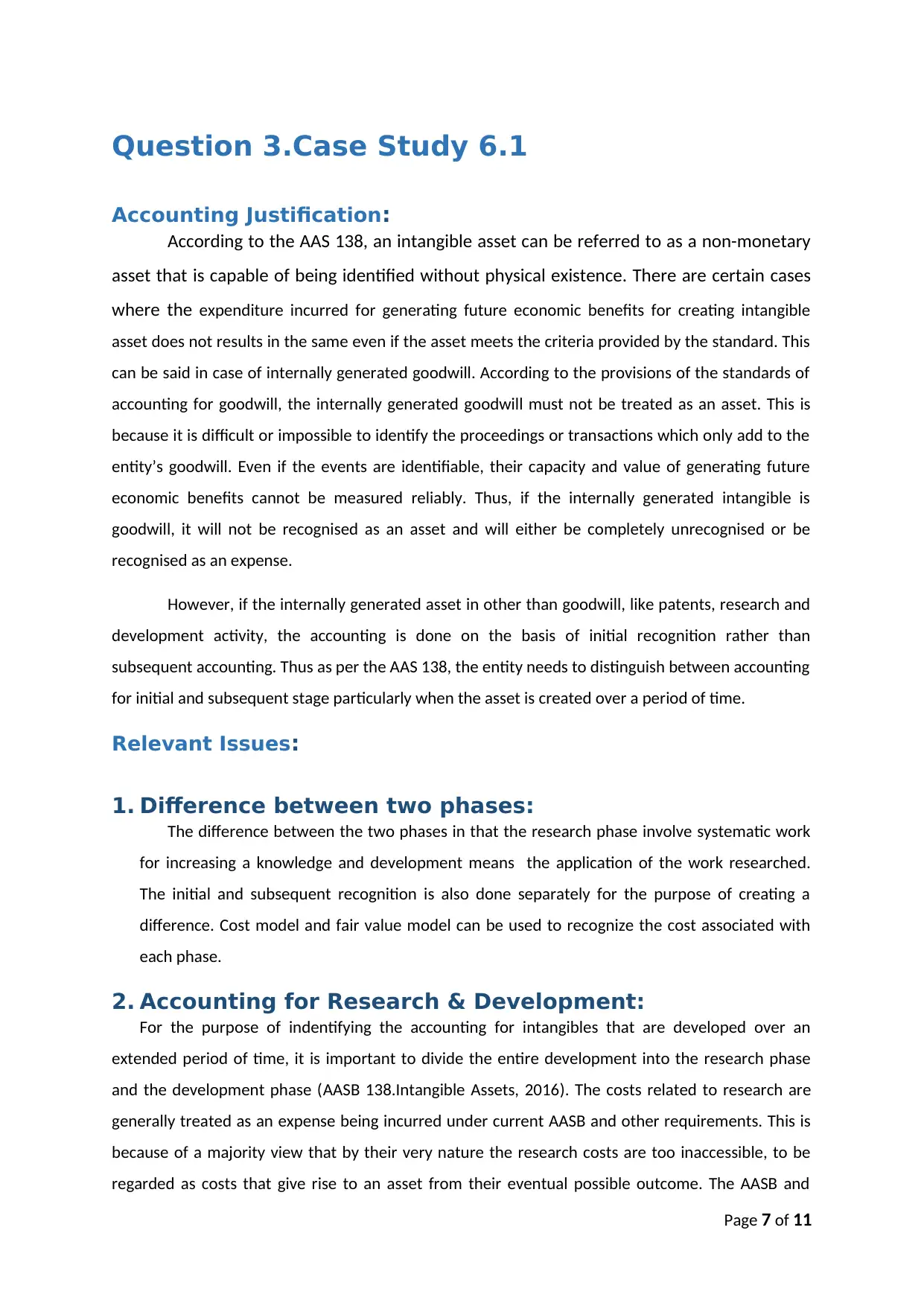

Question 3.Case Study 6.1

Accounting Justification:

According to the AAS 138, an intangible asset can be referred to as a non-monetary

asset that is capable of being identified without physical existence. There are certain cases

where the expenditure incurred for generating future economic benefits for creating intangible

asset does not results in the same even if the asset meets the criteria provided by the standard. This

can be said in case of internally generated goodwill. According to the provisions of the standards of

accounting for goodwill, the internally generated goodwill must not be treated as an asset. This is

because it is difficult or impossible to identify the proceedings or transactions which only add to the

entity’s goodwill. Even if the events are identifiable, their capacity and value of generating future

economic benefits cannot be measured reliably. Thus, if the internally generated intangible is

goodwill, it will not be recognised as an asset and will either be completely unrecognised or be

recognised as an expense.

However, if the internally generated asset in other than goodwill, like patents, research and

development activity, the accounting is done on the basis of initial recognition rather than

subsequent accounting. Thus as per the AAS 138, the entity needs to distinguish between accounting

for initial and subsequent stage particularly when the asset is created over a period of time.

Relevant Issues:

1. Difference between two phases:

The difference between the two phases in that the research phase involve systematic work

for increasing a knowledge and development means the application of the work researched.

The initial and subsequent recognition is also done separately for the purpose of creating a

difference. Cost model and fair value model can be used to recognize the cost associated with

each phase.

2. Accounting for Research & Development:

For the purpose of indentifying the accounting for intangibles that are developed over an

extended period of time, it is important to divide the entire development into the research phase

and the development phase (AASB 138.Intangible Assets, 2016). The costs related to research are

generally treated as an expense being incurred under current AASB and other requirements. This is

because of a majority view that by their very nature the research costs are too inaccessible, to be

regarded as costs that give rise to an asset from their eventual possible outcome. The AASB and

Page 7 of 11

Accounting Justification:

According to the AAS 138, an intangible asset can be referred to as a non-monetary

asset that is capable of being identified without physical existence. There are certain cases

where the expenditure incurred for generating future economic benefits for creating intangible

asset does not results in the same even if the asset meets the criteria provided by the standard. This

can be said in case of internally generated goodwill. According to the provisions of the standards of

accounting for goodwill, the internally generated goodwill must not be treated as an asset. This is

because it is difficult or impossible to identify the proceedings or transactions which only add to the

entity’s goodwill. Even if the events are identifiable, their capacity and value of generating future

economic benefits cannot be measured reliably. Thus, if the internally generated intangible is

goodwill, it will not be recognised as an asset and will either be completely unrecognised or be

recognised as an expense.

However, if the internally generated asset in other than goodwill, like patents, research and

development activity, the accounting is done on the basis of initial recognition rather than

subsequent accounting. Thus as per the AAS 138, the entity needs to distinguish between accounting

for initial and subsequent stage particularly when the asset is created over a period of time.

Relevant Issues:

1. Difference between two phases:

The difference between the two phases in that the research phase involve systematic work

for increasing a knowledge and development means the application of the work researched.

The initial and subsequent recognition is also done separately for the purpose of creating a

difference. Cost model and fair value model can be used to recognize the cost associated with

each phase.

2. Accounting for Research & Development:

For the purpose of indentifying the accounting for intangibles that are developed over an

extended period of time, it is important to divide the entire development into the research phase

and the development phase (AASB 138.Intangible Assets, 2016). The costs related to research are

generally treated as an expense being incurred under current AASB and other requirements. This is

because of a majority view that by their very nature the research costs are too inaccessible, to be

regarded as costs that give rise to an asset from their eventual possible outcome. The AASB and

Page 7 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

certain other national standard setting Boards require the costs associated with the development of

intangible to be capitalised if it meets the specific criteria.

3. Decision / Conclusion / Reasons and Justification:

In order to eliminate the issues arising from the difference between acquiring and developing

assets, it is necessary to account for developed asset as per the provisions provided above.

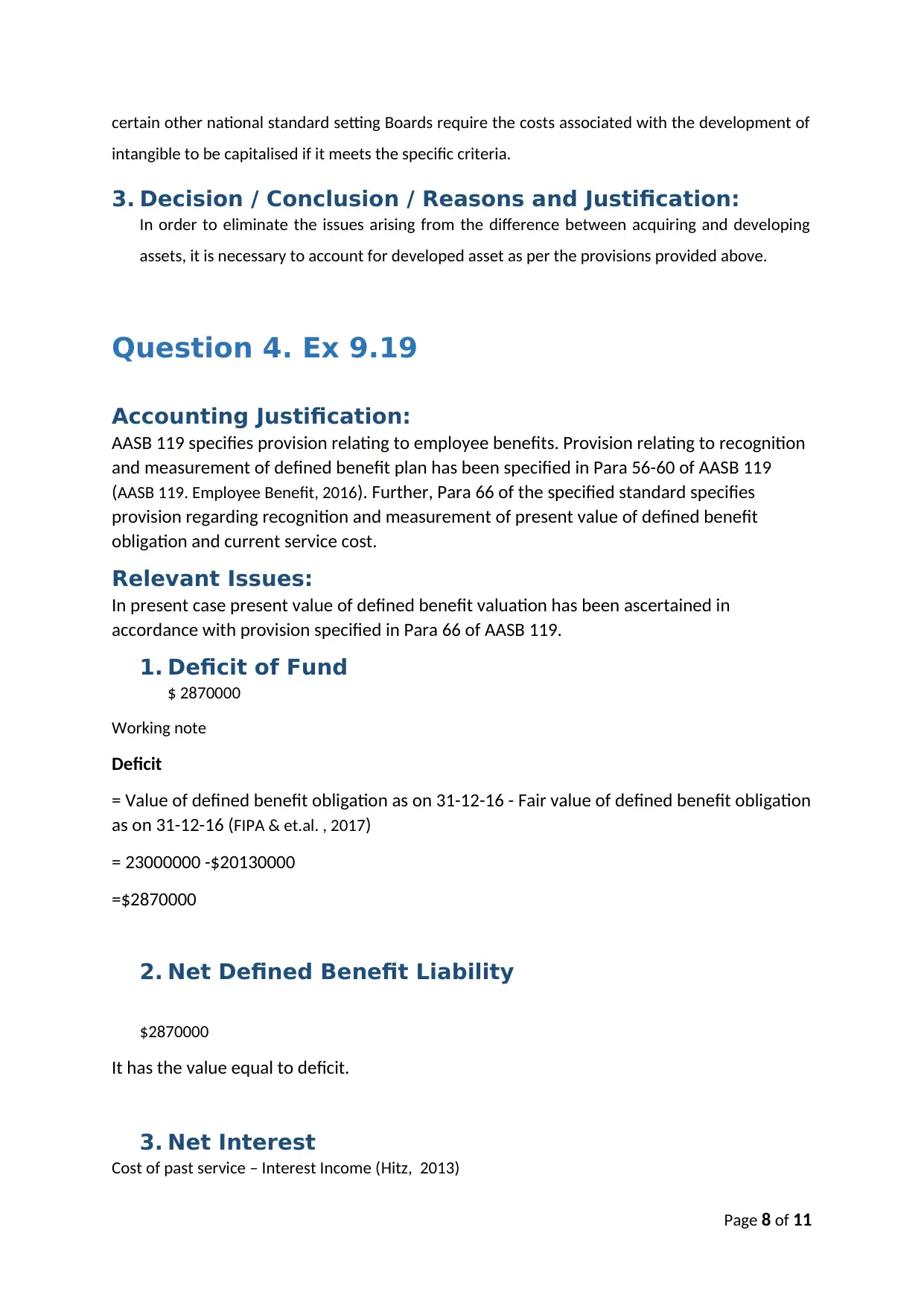

Question 4. Ex 9.19

Accounting Justification:

AASB 119 specifies provision relating to employee benefits. Provision relating to recognition

and measurement of defined benefit plan has been specified in Para 56-60 of AASB 119

(AASB 119. Employee Benefit, 2016). Further, Para 66 of the specified standard specifies

provision regarding recognition and measurement of present value of defined benefit

obligation and current service cost.

Relevant Issues:

In present case present value of defined benefit valuation has been ascertained in

accordance with provision specified in Para 66 of AASB 119.

1. Deficit of Fund

$ 2870000

Working note

Deficit

= Value of defined benefit obligation as on 31-12-16 - Fair value of defined benefit obligation

as on 31-12-16 (FIPA & et.al. , 2017)

= 23000000 -$20130000

=$2870000

2. Net Defined Benefit Liability

$2870000

It has the value equal to deficit.

3. Net Interest

Cost of past service – Interest Income (Hitz, 2013)

Page 8 of 11

intangible to be capitalised if it meets the specific criteria.

3. Decision / Conclusion / Reasons and Justification:

In order to eliminate the issues arising from the difference between acquiring and developing

assets, it is necessary to account for developed asset as per the provisions provided above.

Question 4. Ex 9.19

Accounting Justification:

AASB 119 specifies provision relating to employee benefits. Provision relating to recognition

and measurement of defined benefit plan has been specified in Para 56-60 of AASB 119

(AASB 119. Employee Benefit, 2016). Further, Para 66 of the specified standard specifies

provision regarding recognition and measurement of present value of defined benefit

obligation and current service cost.

Relevant Issues:

In present case present value of defined benefit valuation has been ascertained in

accordance with provision specified in Para 66 of AASB 119.

1. Deficit of Fund

$ 2870000

Working note

Deficit

= Value of defined benefit obligation as on 31-12-16 - Fair value of defined benefit obligation

as on 31-12-16 (FIPA & et.al. , 2017)

= 23000000 -$20130000

=$2870000

2. Net Defined Benefit Liability

$2870000

It has the value equal to deficit.

3. Net Interest

Cost of past service – Interest Income (Hitz, 2013)

Page 8 of 11

= (20000000+2000000 *10%) -(19000000 *10%)

= = $2200000-$1900000

= $300000

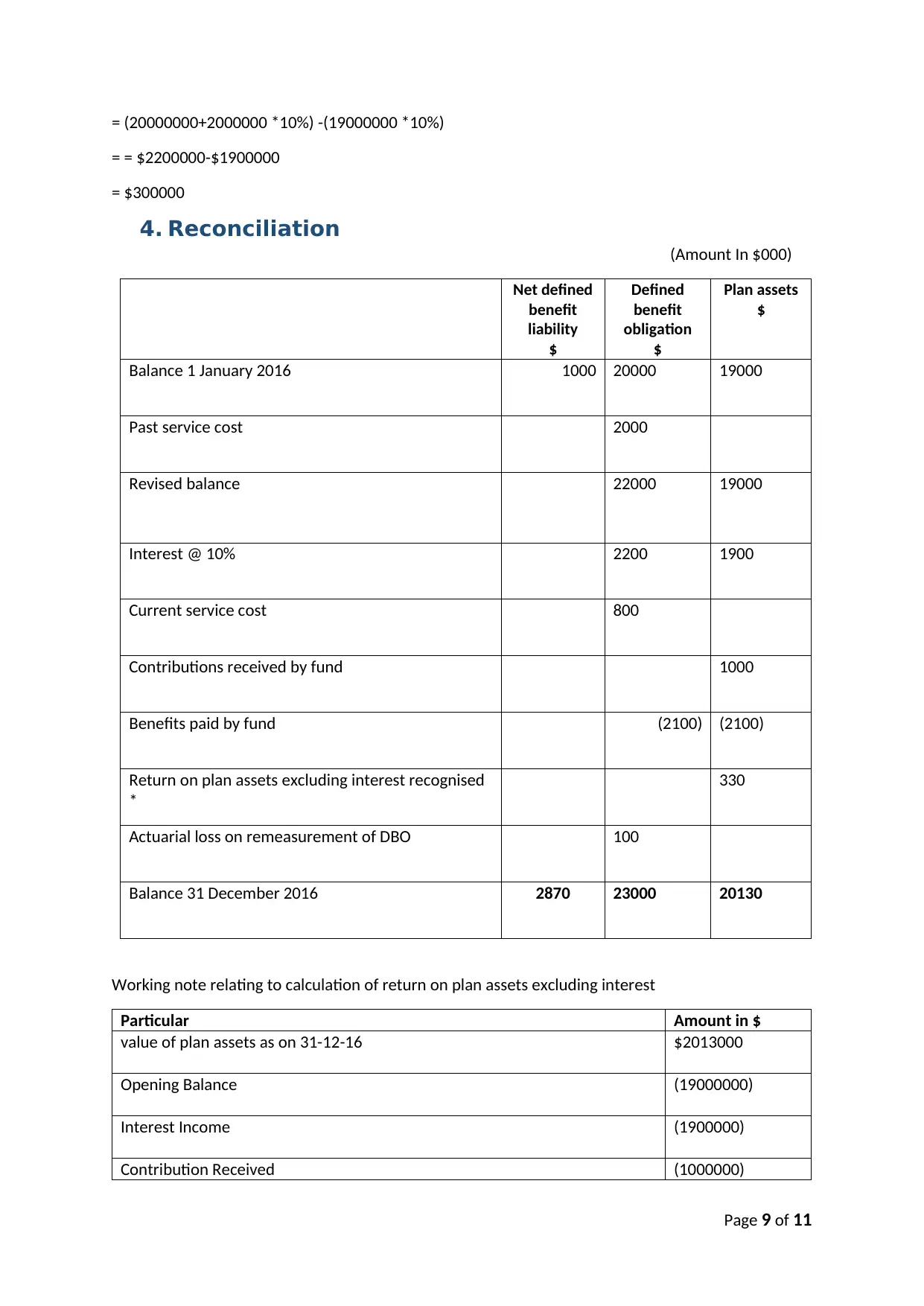

4. Reconciliation

(Amount In $000)

Net defined

benefit

liability

$

Defined

benefit

obligation

$

Plan assets

$

Balance 1 January 2016 1000 20000 19000

Past service cost 2000

Revised balance 22000 19000

Interest @ 10% 2200 1900

Current service cost 800

Contributions received by fund 1000

Benefits paid by fund (2100) (2100)

Return on plan assets excluding interest recognised

*

330

Actuarial loss on remeasurement of DBO 100

Balance 31 December 2016 2870 23000 20130

Working note relating to calculation of return on plan assets excluding interest

Particular Amount in $

value of plan assets as on 31-12-16 $2013000

Opening Balance (19000000)

Interest Income (1900000)

Contribution Received (1000000)

Page 9 of 11

= = $2200000-$1900000

= $300000

4. Reconciliation

(Amount In $000)

Net defined

benefit

liability

$

Defined

benefit

obligation

$

Plan assets

$

Balance 1 January 2016 1000 20000 19000

Past service cost 2000

Revised balance 22000 19000

Interest @ 10% 2200 1900

Current service cost 800

Contributions received by fund 1000

Benefits paid by fund (2100) (2100)

Return on plan assets excluding interest recognised

*

330

Actuarial loss on remeasurement of DBO 100

Balance 31 December 2016 2870 23000 20130

Working note relating to calculation of return on plan assets excluding interest

Particular Amount in $

value of plan assets as on 31-12-16 $2013000

Opening Balance (19000000)

Interest Income (1900000)

Contribution Received (1000000)

Page 9 of 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Benefit paid 2100000

Return on plan excluding interest $330000

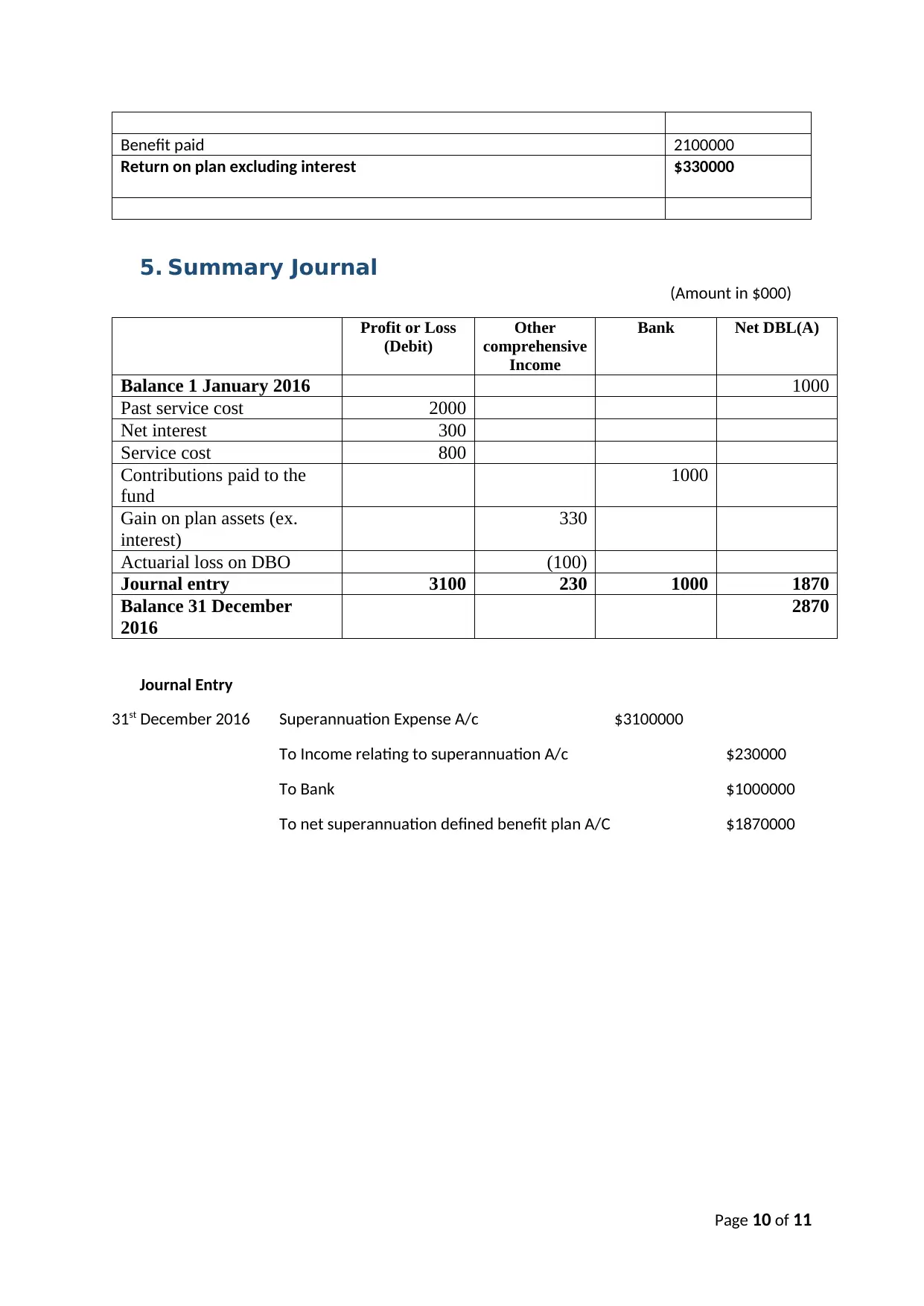

5. Summary Journal

(Amount in $000)

Profit or Loss

(Debit)

Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016 1000

Past service cost 2000

Net interest 300

Service cost 800

Contributions paid to the

fund

1000

Gain on plan assets (ex.

interest)

330

Actuarial loss on DBO (100)

Journal entry 3100 230 1000 1870

Balance 31 December

2016

2870

Journal Entry

31st December 2016 Superannuation Expense A/c $3100000

To Income relating to superannuation A/c $230000

To Bank $1000000

To net superannuation defined benefit plan A/C $1870000

Page 10 of 11

Return on plan excluding interest $330000

5. Summary Journal

(Amount in $000)

Profit or Loss

(Debit)

Other

comprehensive

Income

Bank Net DBL(A)

Balance 1 January 2016 1000

Past service cost 2000

Net interest 300

Service cost 800

Contributions paid to the

fund

1000

Gain on plan assets (ex.

interest)

330

Actuarial loss on DBO (100)

Journal entry 3100 230 1000 1870

Balance 31 December

2016

2870

Journal Entry

31st December 2016 Superannuation Expense A/c $3100000

To Income relating to superannuation A/c $230000

To Bank $1000000

To net superannuation defined benefit plan A/C $1870000

Page 10 of 11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journal

Capalbo, F., (2013). Impairment of Assets.

Collings, S., (2013) Impairment of Assets. Interpretation and Application of UK GAAP: For

Accounting Periods Commencing On or After 1 January 2015, Pp.241-259.

Dinh, T., Eierle, B., Schultze, W. &Steeger, L., (2015). Research and development,

uncertainty, and analysts’ forecasts: The case of IAS 38. Journal of International

Financial Management & Accounting, 26(3). Pp.257-293.

FIPA, M.T.G., Stylianou, M.V., Carey, P., Cooper, B., Tanewski, G. &Mroczkowski, N., (2017).

Accounting of Defined benefit plan. IPA-Deakin SME Research Centre.

Hitz, J.M., (2013). Capitalize or expense? Recent evidence on the accounting for intangible

assets under IAS 38 by STOXX 200 firms. Zeitschrift für Internationale

Rechnungslegung IRZ, 5, Pp.319-324.

International Accounting Standards Board, (2014). International accounting standards IAS

36, Impairment of assets, and IAS 38, Intangible assets. IASCF Publications Dept..

Liang, L. and Riedl, E.J., (2013). The effect of fair value versus historical cost reporting model

on analyst forecast accuracy. The Accounting Review, 89(3), Pp.1151-1177.

Online

AASB 116.Property Plant and Equipment. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-

04_COMPjun09_07-09.pdf>. [Accessed on 8th October 2017.]

AASB 119. Employee Benefit. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11.pdf>. [Accessed

on 8th October 2017.]

AASB 138.Intangible Assets. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-

04_COMPjun14_07-14.pdf>. [Accessed on 8th October 2017.]

Page 11 of 11

Books and Journal

Capalbo, F., (2013). Impairment of Assets.

Collings, S., (2013) Impairment of Assets. Interpretation and Application of UK GAAP: For

Accounting Periods Commencing On or After 1 January 2015, Pp.241-259.

Dinh, T., Eierle, B., Schultze, W. &Steeger, L., (2015). Research and development,

uncertainty, and analysts’ forecasts: The case of IAS 38. Journal of International

Financial Management & Accounting, 26(3). Pp.257-293.

FIPA, M.T.G., Stylianou, M.V., Carey, P., Cooper, B., Tanewski, G. &Mroczkowski, N., (2017).

Accounting of Defined benefit plan. IPA-Deakin SME Research Centre.

Hitz, J.M., (2013). Capitalize or expense? Recent evidence on the accounting for intangible

assets under IAS 38 by STOXX 200 firms. Zeitschrift für Internationale

Rechnungslegung IRZ, 5, Pp.319-324.

International Accounting Standards Board, (2014). International accounting standards IAS

36, Impairment of assets, and IAS 38, Intangible assets. IASCF Publications Dept..

Liang, L. and Riedl, E.J., (2013). The effect of fair value versus historical cost reporting model

on analyst forecast accuracy. The Accounting Review, 89(3), Pp.1151-1177.

Online

AASB 116.Property Plant and Equipment. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-

04_COMPjun09_07-09.pdf>. [Accessed on 8th October 2017.]

AASB 119. Employee Benefit. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11.pdf>. [Accessed

on 8th October 2017.]

AASB 138.Intangible Assets. (2016). (PDF). Available through <

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-

04_COMPjun14_07-14.pdf>. [Accessed on 8th October 2017.]

Page 11 of 11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.