ACC510: Financial Reporting Task 2 - Major Assignment, Semester 2

VerifiedAdded on 2020/03/13

|12

|2190

|32

Homework Assignment

AI Summary

This document presents a comprehensive solution for ACC510 Financial Reporting Task 2, covering key aspects of financial reporting. The solution addresses four main questions, including a case study on fair value measurement and the "highest and best use" principle, with detailed accounting justifications and relevant issues. It also includes an exercise on impairment testing, providing calculations and journal entries for both 2016 and 2017. Furthermore, the assignment explores accounting for research and development, differentiating between research and development phases and providing accounting treatments. Finally, the solution tackles an exercise on employee benefits, focusing on a defined benefit plan, calculating the net defined benefit liability, net interest, and a reconciliation of the defined benefit obligation and plan assets, along with the summary journal entries. The document references relevant AASB standards throughout the solution.

ACC510(ATMC) - Financial Reporting

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Task 2 – Major Assignment

Semester 2 - 2017

Student Name:

Student ID #:

Campus:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................4

2. Impairment Test 31/12/17....................................................................................................4

a. Calculations........................................................................................................................4

b. General Journal Entries 31/12/17:.....................................................................................4

Question 3. Case Study 6.1....................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Difference between two phases:...........................................................................................5

2. Accounting for Research & Development:.............................................................................5

3. Decision / Conclusion / Reasons and Justification:................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 12

Question 1. Case Study 3.1....................................................................................................................3

Accounting Justification:................................................................................................................3

Relevant Issues:.............................................................................................................................3

1. Highest & Best Use................................................................................................................3

2. Application to aged care home..............................................................................................3

3. Two possible uses..................................................................................................................3

Question 2. Ex 7.14................................................................................................................................4

Accounting Justification:................................................................................................................4

Relevant Issues:.............................................................................................................................4

1. Impairment Test 31/12/16....................................................................................................4

a. Calculations:.......................................................................................................................4

b. General Journal Entries 31/12/16:.....................................................................................4

2. Impairment Test 31/12/17....................................................................................................4

a. Calculations........................................................................................................................4

b. General Journal Entries 31/12/17:.....................................................................................4

Question 3. Case Study 6.1....................................................................................................................5

Accounting Justification:................................................................................................................5

Relevant Issues:.............................................................................................................................5

1. Difference between two phases:...........................................................................................5

2. Accounting for Research & Development:.............................................................................5

3. Decision / Conclusion / Reasons and Justification:................................................................5

Question 4. Ex 9.19................................................................................................................................6

Accounting Justification:................................................................................................................6

Relevant Issues:.............................................................................................................................6

1. Deficit of Fund...........................................................................................................................6

2. Net Defined Benefit Liability......................................................................................................6

3. Net Interest................................................................................................................................6

4. Reconciliation............................................................................................................................6

5. Summary Journal.......................................................................................................................6

Page 2 of 12

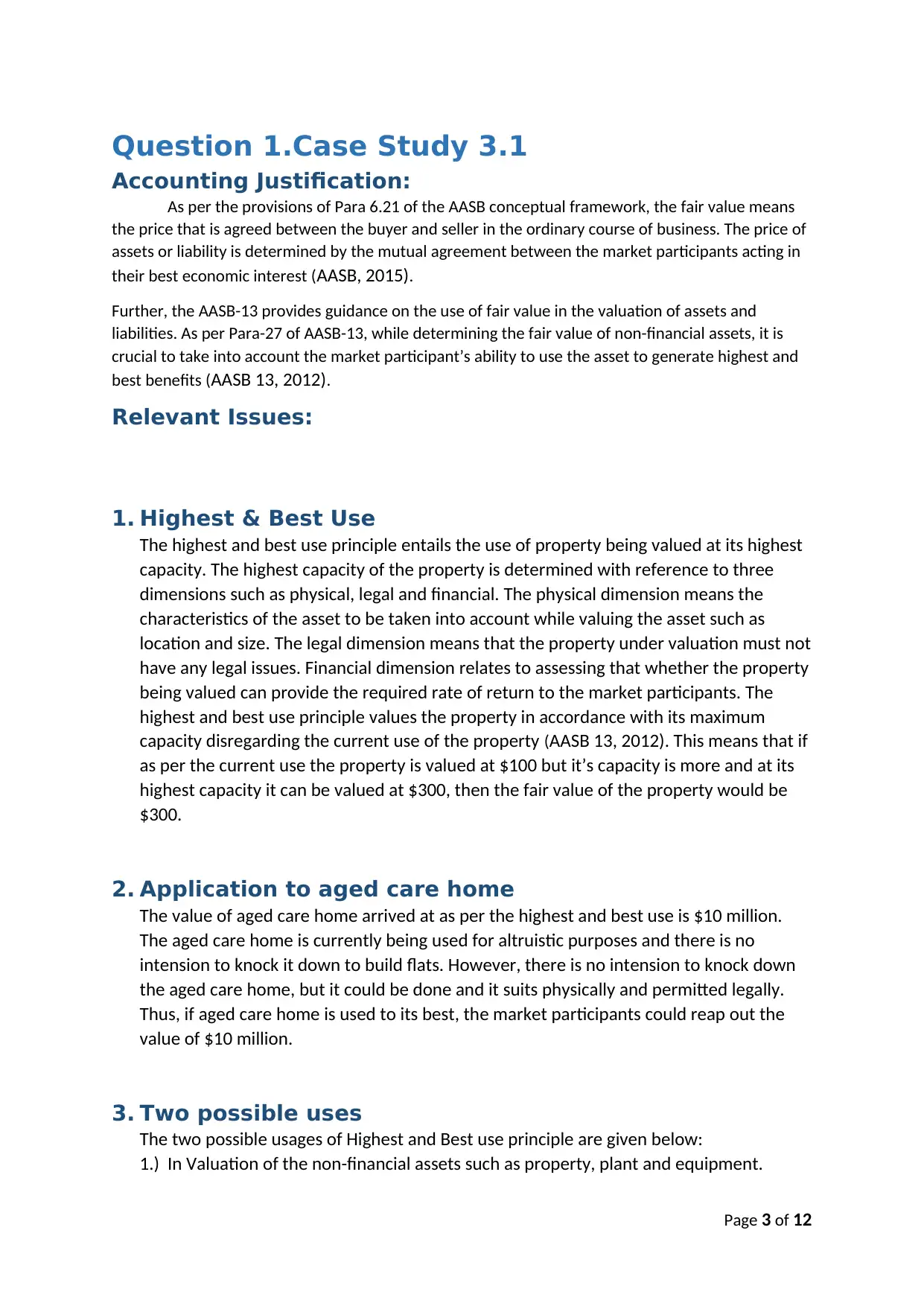

Question 1.Case Study 3.1

Accounting Justification:

As per the provisions of Para 6.21 of the AASB conceptual framework, the fair value means

the price that is agreed between the buyer and seller in the ordinary course of business. The price of

assets or liability is determined by the mutual agreement between the market participants acting in

their best economic interest (AASB, 2015).

Further, the AASB-13 provides guidance on the use of fair value in the valuation of assets and

liabilities. As per Para-27 of AASB-13, while determining the fair value of non-financial assets, it is

crucial to take into account the market participant’s ability to use the asset to generate highest and

best benefits (AASB 13, 2012).

Relevant Issues:

1. Highest & Best Use

The highest and best use principle entails the use of property being valued at its highest

capacity. The highest capacity of the property is determined with reference to three

dimensions such as physical, legal and financial. The physical dimension means the

characteristics of the asset to be taken into account while valuing the asset such as

location and size. The legal dimension means that the property under valuation must not

have any legal issues. Financial dimension relates to assessing that whether the property

being valued can provide the required rate of return to the market participants. The

highest and best use principle values the property in accordance with its maximum

capacity disregarding the current use of the property (AASB 13, 2012). This means that if

as per the current use the property is valued at $100 but it’s capacity is more and at its

highest capacity it can be valued at $300, then the fair value of the property would be

$300.

2. Application to aged care home

The value of aged care home arrived at as per the highest and best use is $10 million.

The aged care home is currently being used for altruistic purposes and there is no

intension to knock it down to build flats. However, there is no intension to knock down

the aged care home, but it could be done and it suits physically and permitted legally.

Thus, if aged care home is used to its best, the market participants could reap out the

value of $10 million.

3. Two possible uses

The two possible usages of Highest and Best use principle are given below:

1.) In Valuation of the non-financial assets such as property, plant and equipment.

Page 3 of 12

Accounting Justification:

As per the provisions of Para 6.21 of the AASB conceptual framework, the fair value means

the price that is agreed between the buyer and seller in the ordinary course of business. The price of

assets or liability is determined by the mutual agreement between the market participants acting in

their best economic interest (AASB, 2015).

Further, the AASB-13 provides guidance on the use of fair value in the valuation of assets and

liabilities. As per Para-27 of AASB-13, while determining the fair value of non-financial assets, it is

crucial to take into account the market participant’s ability to use the asset to generate highest and

best benefits (AASB 13, 2012).

Relevant Issues:

1. Highest & Best Use

The highest and best use principle entails the use of property being valued at its highest

capacity. The highest capacity of the property is determined with reference to three

dimensions such as physical, legal and financial. The physical dimension means the

characteristics of the asset to be taken into account while valuing the asset such as

location and size. The legal dimension means that the property under valuation must not

have any legal issues. Financial dimension relates to assessing that whether the property

being valued can provide the required rate of return to the market participants. The

highest and best use principle values the property in accordance with its maximum

capacity disregarding the current use of the property (AASB 13, 2012). This means that if

as per the current use the property is valued at $100 but it’s capacity is more and at its

highest capacity it can be valued at $300, then the fair value of the property would be

$300.

2. Application to aged care home

The value of aged care home arrived at as per the highest and best use is $10 million.

The aged care home is currently being used for altruistic purposes and there is no

intension to knock it down to build flats. However, there is no intension to knock down

the aged care home, but it could be done and it suits physically and permitted legally.

Thus, if aged care home is used to its best, the market participants could reap out the

value of $10 million.

3. Two possible uses

The two possible usages of Highest and Best use principle are given below:

1.) In Valuation of the non-financial assets such as property, plant and equipment.

Page 3 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.) In the valuation of non-current liabilities (AASB 13, 2012).

Page 4 of 12

Page 4 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

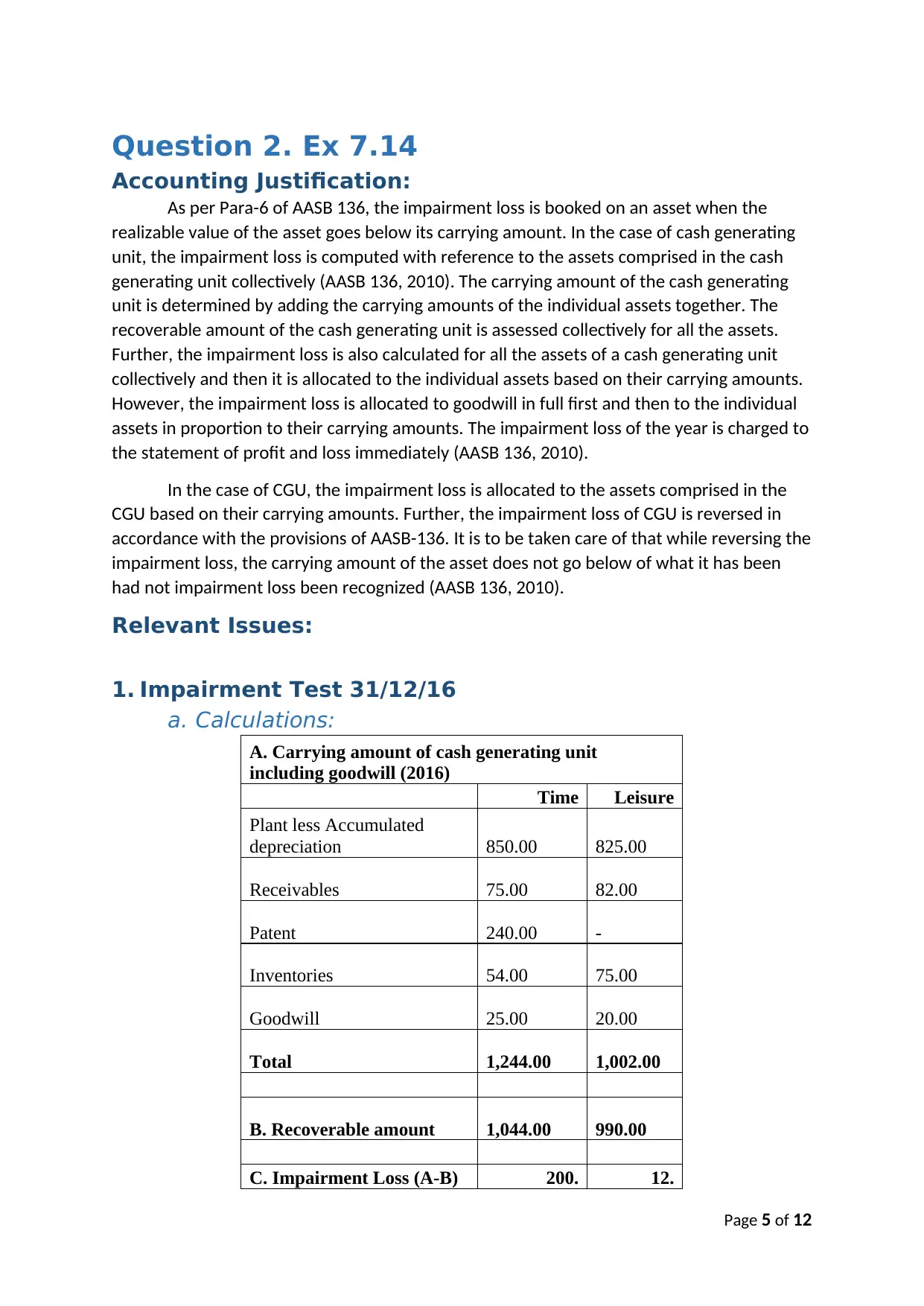

Question 2. Ex 7.14

Accounting Justification:

As per Para-6 of AASB 136, the impairment loss is booked on an asset when the

realizable value of the asset goes below its carrying amount. In the case of cash generating

unit, the impairment loss is computed with reference to the assets comprised in the cash

generating unit collectively (AASB 136, 2010). The carrying amount of the cash generating

unit is determined by adding the carrying amounts of the individual assets together. The

recoverable amount of the cash generating unit is assessed collectively for all the assets.

Further, the impairment loss is also calculated for all the assets of a cash generating unit

collectively and then it is allocated to the individual assets based on their carrying amounts.

However, the impairment loss is allocated to goodwill in full first and then to the individual

assets in proportion to their carrying amounts. The impairment loss of the year is charged to

the statement of profit and loss immediately (AASB 136, 2010).

In the case of CGU, the impairment loss is allocated to the assets comprised in the

CGU based on their carrying amounts. Further, the impairment loss of CGU is reversed in

accordance with the provisions of AASB-136. It is to be taken care of that while reversing the

impairment loss, the carrying amount of the asset does not go below of what it has been

had not impairment loss been recognized (AASB 136, 2010).

Relevant Issues:

1. Impairment Test 31/12/16

a. Calculations:

A. Carrying amount of cash generating unit

including goodwill (2016)

Time Leisure

Plant less Accumulated

depreciation 850.00 825.00

Receivables 75.00 82.00

Patent 240.00 -

Inventories 54.00 75.00

Goodwill 25.00 20.00

Total 1,244.00 1,002.00

B. Recoverable amount 1,044.00 990.00

C. Impairment Loss (A-B) 200. 12.

Page 5 of 12

Accounting Justification:

As per Para-6 of AASB 136, the impairment loss is booked on an asset when the

realizable value of the asset goes below its carrying amount. In the case of cash generating

unit, the impairment loss is computed with reference to the assets comprised in the cash

generating unit collectively (AASB 136, 2010). The carrying amount of the cash generating

unit is determined by adding the carrying amounts of the individual assets together. The

recoverable amount of the cash generating unit is assessed collectively for all the assets.

Further, the impairment loss is also calculated for all the assets of a cash generating unit

collectively and then it is allocated to the individual assets based on their carrying amounts.

However, the impairment loss is allocated to goodwill in full first and then to the individual

assets in proportion to their carrying amounts. The impairment loss of the year is charged to

the statement of profit and loss immediately (AASB 136, 2010).

In the case of CGU, the impairment loss is allocated to the assets comprised in the

CGU based on their carrying amounts. Further, the impairment loss of CGU is reversed in

accordance with the provisions of AASB-136. It is to be taken care of that while reversing the

impairment loss, the carrying amount of the asset does not go below of what it has been

had not impairment loss been recognized (AASB 136, 2010).

Relevant Issues:

1. Impairment Test 31/12/16

a. Calculations:

A. Carrying amount of cash generating unit

including goodwill (2016)

Time Leisure

Plant less Accumulated

depreciation 850.00 825.00

Receivables 75.00 82.00

Patent 240.00 -

Inventories 54.00 75.00

Goodwill 25.00 20.00

Total 1,244.00 1,002.00

B. Recoverable amount 1,044.00 990.00

C. Impairment Loss (A-B) 200. 12.

Page 5 of 12

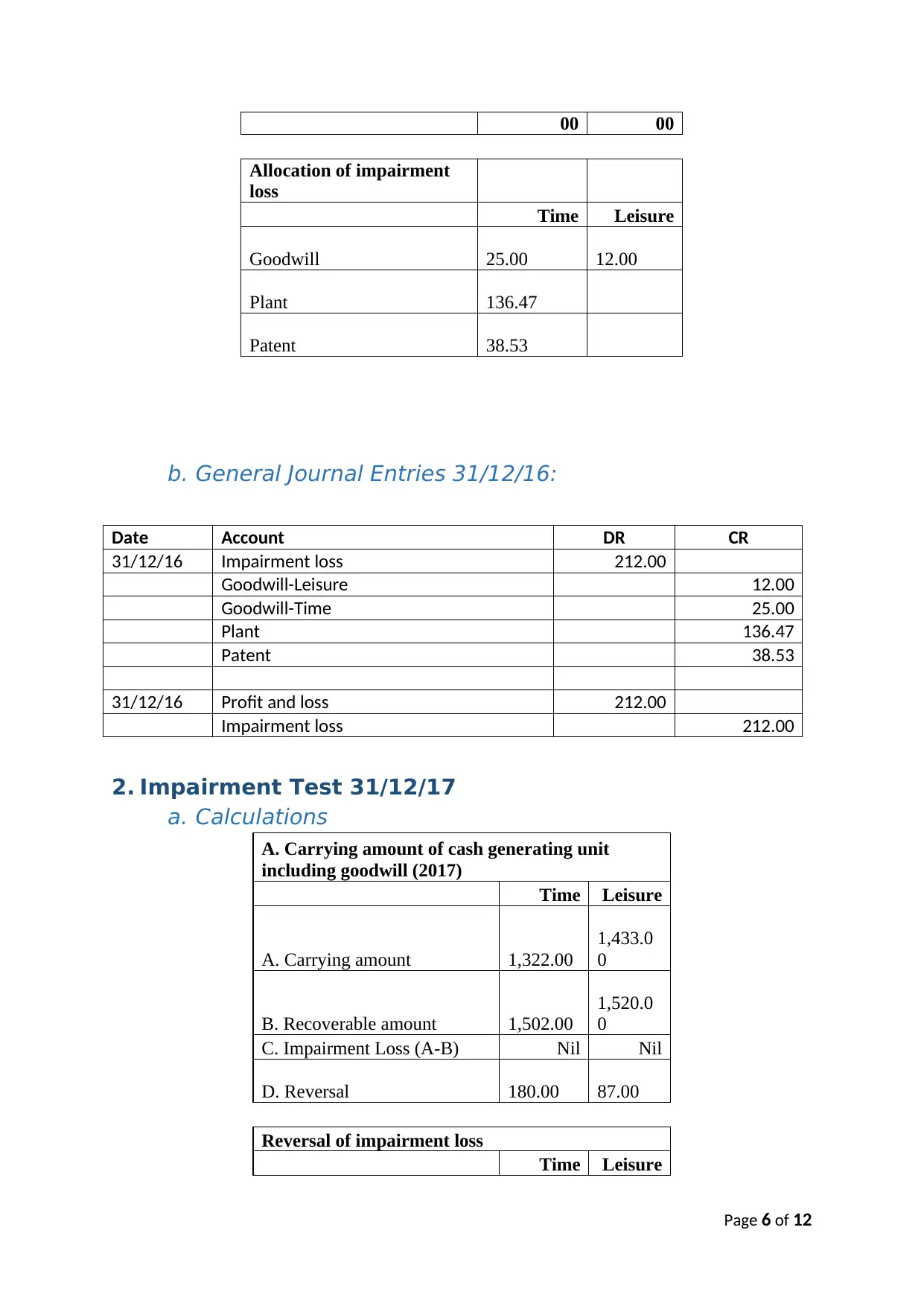

00 00

Allocation of impairment

loss

Time Leisure

Goodwill 25.00 12.00

Plant 136.47

Patent 38.53

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/16 Impairment loss 212.00

Goodwill-Leisure 12.00

Goodwill-Time 25.00

Plant 136.47

Patent 38.53

31/12/16 Profit and loss 212.00

Impairment loss 212.00

2. Impairment Test 31/12/17

a. Calculations

A. Carrying amount of cash generating unit

including goodwill (2017)

Time Leisure

A. Carrying amount 1,322.00

1,433.0

0

B. Recoverable amount 1,502.00

1,520.0

0

C. Impairment Loss (A-B) Nil Nil

D. Reversal 180.00 87.00

Reversal of impairment loss

Time Leisure

Page 6 of 12

Allocation of impairment

loss

Time Leisure

Goodwill 25.00 12.00

Plant 136.47

Patent 38.53

b. General Journal Entries 31/12/16:

Date Account DR CR

31/12/16 Impairment loss 212.00

Goodwill-Leisure 12.00

Goodwill-Time 25.00

Plant 136.47

Patent 38.53

31/12/16 Profit and loss 212.00

Impairment loss 212.00

2. Impairment Test 31/12/17

a. Calculations

A. Carrying amount of cash generating unit

including goodwill (2017)

Time Leisure

A. Carrying amount 1,322.00

1,433.0

0

B. Recoverable amount 1,502.00

1,520.0

0

C. Impairment Loss (A-B) Nil Nil

D. Reversal 180.00 87.00

Reversal of impairment loss

Time Leisure

Page 6 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

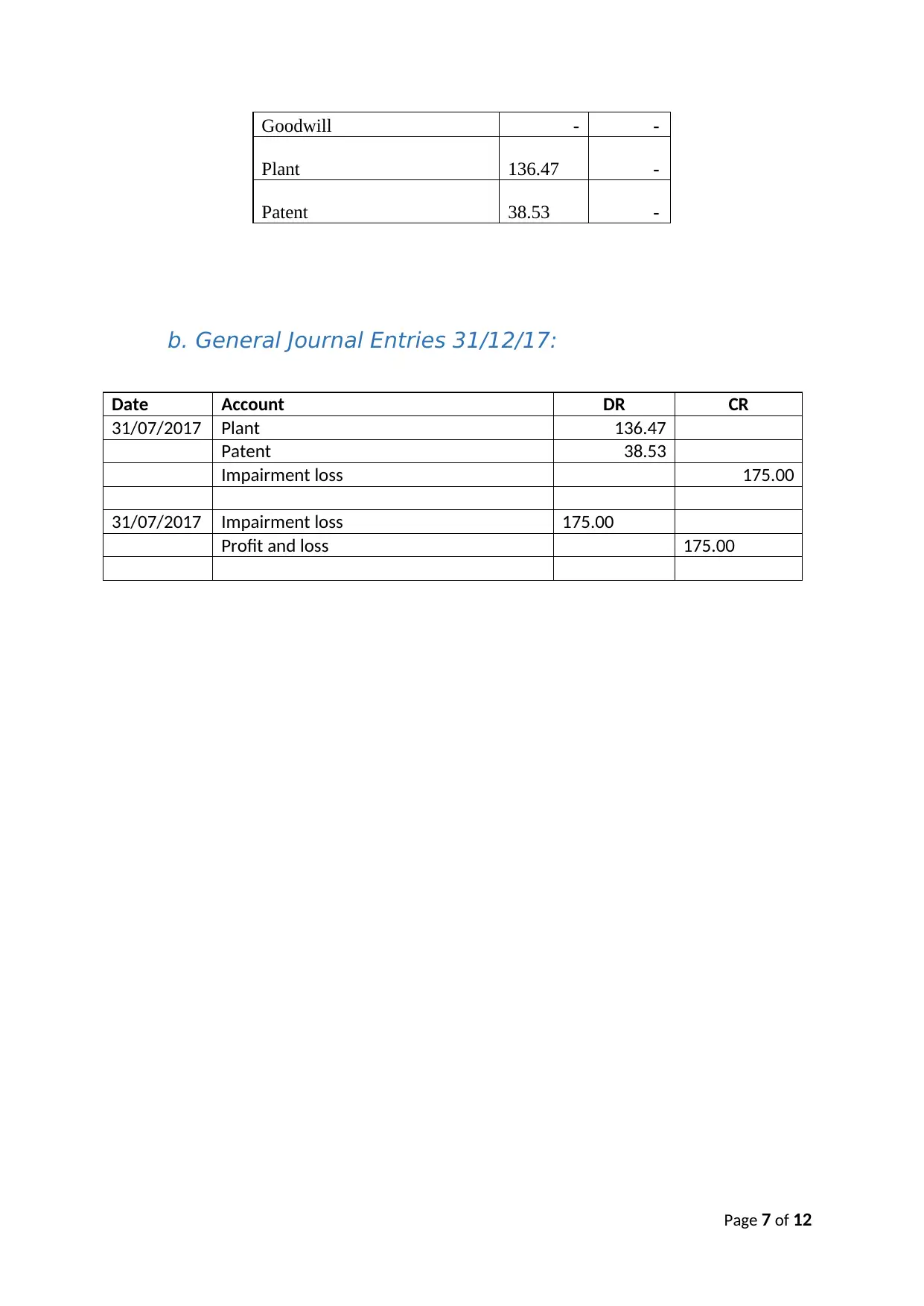

Goodwill - -

Plant 136.47 -

Patent 38.53 -

b. General Journal Entries 31/12/17:

Date Account DR CR

31/07/2017 Plant 136.47

Patent 38.53

Impairment loss 175.00

31/07/2017 Impairment loss 175.00

Profit and loss 175.00

Page 7 of 12

Plant 136.47 -

Patent 38.53 -

b. General Journal Entries 31/12/17:

Date Account DR CR

31/07/2017 Plant 136.47

Patent 38.53

Impairment loss 175.00

31/07/2017 Impairment loss 175.00

Profit and loss 175.00

Page 7 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3.Case Study 6.1

Accounting Justification:

According to the conceptual framework, to be able to recognize a financial

transaction as asset, it should be a resource under the entity’s control which arose as a

result of past events and from which economic benefits are expected in future (AASB, 2015).

Further, AASB 138, “Intangible assets” makes it clear that only the paid intangibles

are to be accounted for as asset in the books. The internally generated goodwill or patent is

to be accounted as asset only when it meets the recognition criteria (AASB 138, 2014).

Relevant Issues:

1. Difference between two phases:

The expenditure incurred on the development of an intangible asset is divided into two

phases such as research and development. The research phase is the initial phase in

which activities on the development of intangible assets initiates (AASB 138, 2014).

Further, the development phase starts after completion of the research phase. The

activities in the research phase do not give rise to any asset and therefore entire

expenditure of the research phase is expensed in the profit and loss account. However,

the activities of the development phase may give rise to the intangible asset. Whether

the intangible asset is being created or not will depend upon the satisfaction of the

prescribed criteria. If the prescribed criterion is met, the expenses incurred in the

development phase after meeting the prescribed criteria will be capitalized as asset

(AASB 138, 2014).

The activities of the research phase are aimed at exploration of the new knowledge. On

the other hand, the activities of the development phase focus on the design,

construction and testing (Dagwell, Wines, & Lambert, 2015).

2. Accounting for Research & Development:

The accounting for research and development expenditure depends upon the nature

and substance of the financial transactions. The expenses incurred in the research phase

which is the initial phase of the research project are necessarily to be expensed to the

profit and loss account. Thus, the research expenditure is charged to the income

statement in the year in which it is incurred. At the research phase, there are no

indications that the intangible asset would arise therefore capitalization of the

expenditure is not permissible as per the accounting rules (AASB 138, 2014).

However, as the development starts, substantial activities on the project under

development start taking place. There are certain conditions such as completion of

technical feasibility, measurement, and valuation which need to be satisfied for

capitalization of the expenditure of the development phase. If these conditions are met,

Page 8 of 12

Accounting Justification:

According to the conceptual framework, to be able to recognize a financial

transaction as asset, it should be a resource under the entity’s control which arose as a

result of past events and from which economic benefits are expected in future (AASB, 2015).

Further, AASB 138, “Intangible assets” makes it clear that only the paid intangibles

are to be accounted for as asset in the books. The internally generated goodwill or patent is

to be accounted as asset only when it meets the recognition criteria (AASB 138, 2014).

Relevant Issues:

1. Difference between two phases:

The expenditure incurred on the development of an intangible asset is divided into two

phases such as research and development. The research phase is the initial phase in

which activities on the development of intangible assets initiates (AASB 138, 2014).

Further, the development phase starts after completion of the research phase. The

activities in the research phase do not give rise to any asset and therefore entire

expenditure of the research phase is expensed in the profit and loss account. However,

the activities of the development phase may give rise to the intangible asset. Whether

the intangible asset is being created or not will depend upon the satisfaction of the

prescribed criteria. If the prescribed criterion is met, the expenses incurred in the

development phase after meeting the prescribed criteria will be capitalized as asset

(AASB 138, 2014).

The activities of the research phase are aimed at exploration of the new knowledge. On

the other hand, the activities of the development phase focus on the design,

construction and testing (Dagwell, Wines, & Lambert, 2015).

2. Accounting for Research & Development:

The accounting for research and development expenditure depends upon the nature

and substance of the financial transactions. The expenses incurred in the research phase

which is the initial phase of the research project are necessarily to be expensed to the

profit and loss account. Thus, the research expenditure is charged to the income

statement in the year in which it is incurred. At the research phase, there are no

indications that the intangible asset would arise therefore capitalization of the

expenditure is not permissible as per the accounting rules (AASB 138, 2014).

However, as the development starts, substantial activities on the project under

development start taking place. There are certain conditions such as completion of

technical feasibility, measurement, and valuation which need to be satisfied for

capitalization of the expenditure of the development phase. If these conditions are met,

Page 8 of 12

the expenditure of the development phase would be capitalized and recognized as asset

in the balance sheet which will be amortized over the period of time (AASB 138, 2014).

3. Decision / Conclusion / Reasons and Justification:

The internally generated goodwill or patent would be recognized only when the

prescribed recognition criteria is met. The research expenses would be charged to the

profit and loss account and the expenses of development phase would be capitalized in

the books as asset.

Question 4. Ex 9.19

Accounting Justification:

As per Para 4.24 of the conceptual framework, a liability is a financial item that

requires outflow of the resources (AASB, 2015). It is an obligation on the company the

settlement of which will require outflow of the resource embodying economic benefits.

Further, the conceptual framework provides that a liability should be booked when there

arises on obligation and the amount is fairly measurable (Horngren, et al. 2012).

The AASB 119 contains provisions in regards to accounting treatment of the

employee benefits plans (AASB 119, 2011). As per this standard, the post employee benefit

plans are divided into two categories such as defined contribution and defined benefit

plans. Under the defined contribution plan the entity does not bear the risk of changes in

the market conditions but under the defined benefit plan the risk of the entity. The liability

under the defined benefit plan is recognised upon service being performed by the employee

based on the actuarial estimates (Dagwell, Wines, & Lambert, 2015).

Relevant Issues:

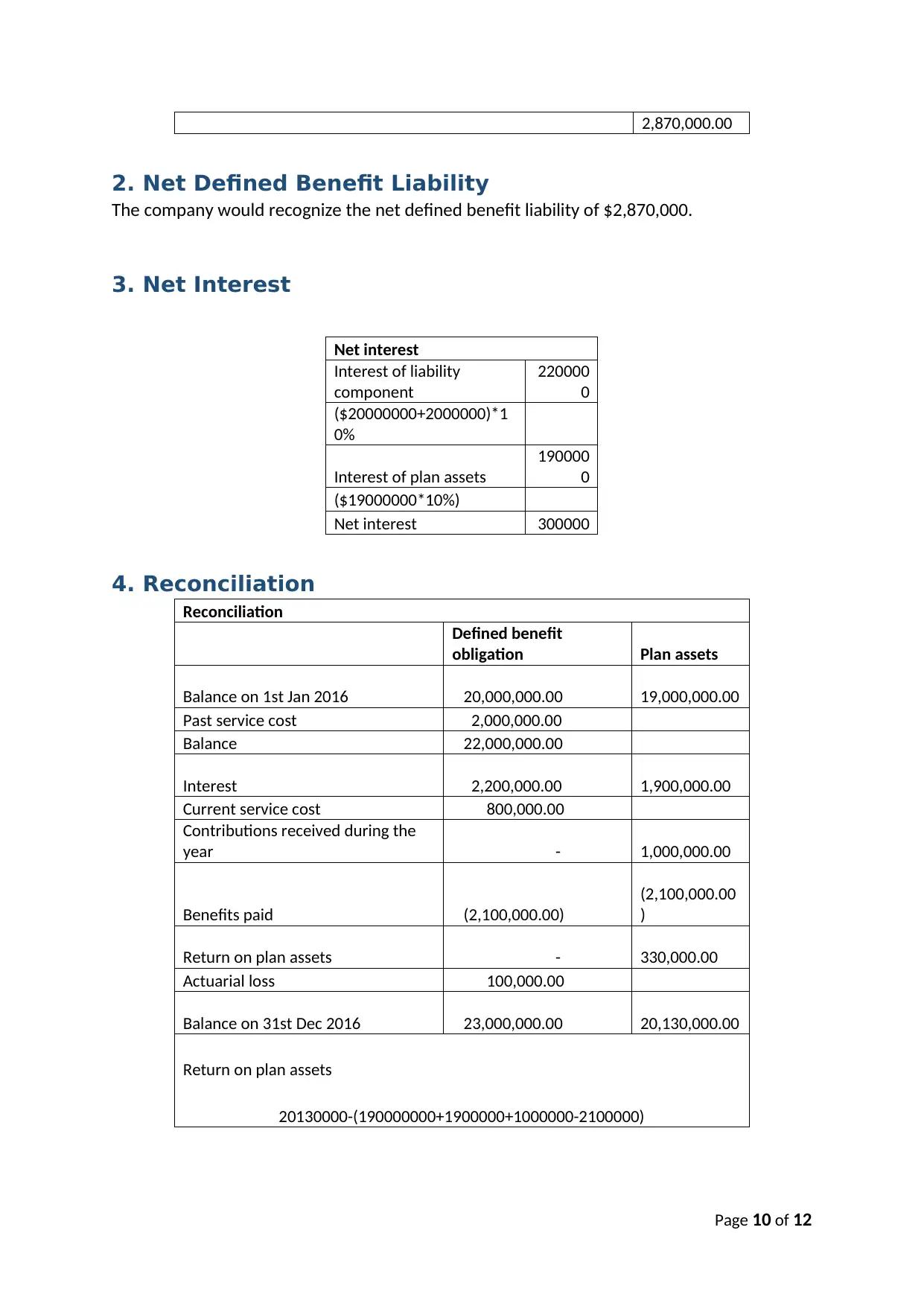

1. Deficit of Fund

Deficit of the fund

Present value of the defined benefit obligation 31 December

2016

23,000,000.0

0

Fair value of plan assets 31 December 2016

20,130,000.0

0

Deficit

Page 9 of 12

in the balance sheet which will be amortized over the period of time (AASB 138, 2014).

3. Decision / Conclusion / Reasons and Justification:

The internally generated goodwill or patent would be recognized only when the

prescribed recognition criteria is met. The research expenses would be charged to the

profit and loss account and the expenses of development phase would be capitalized in

the books as asset.

Question 4. Ex 9.19

Accounting Justification:

As per Para 4.24 of the conceptual framework, a liability is a financial item that

requires outflow of the resources (AASB, 2015). It is an obligation on the company the

settlement of which will require outflow of the resource embodying economic benefits.

Further, the conceptual framework provides that a liability should be booked when there

arises on obligation and the amount is fairly measurable (Horngren, et al. 2012).

The AASB 119 contains provisions in regards to accounting treatment of the

employee benefits plans (AASB 119, 2011). As per this standard, the post employee benefit

plans are divided into two categories such as defined contribution and defined benefit

plans. Under the defined contribution plan the entity does not bear the risk of changes in

the market conditions but under the defined benefit plan the risk of the entity. The liability

under the defined benefit plan is recognised upon service being performed by the employee

based on the actuarial estimates (Dagwell, Wines, & Lambert, 2015).

Relevant Issues:

1. Deficit of Fund

Deficit of the fund

Present value of the defined benefit obligation 31 December

2016

23,000,000.0

0

Fair value of plan assets 31 December 2016

20,130,000.0

0

Deficit

Page 9 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2,870,000.00

2. Net Defined Benefit Liability

The company would recognize the net defined benefit liability of $2,870,000.

3. Net Interest

Net interest

Interest of liability

component

220000

0

($20000000+2000000)*1

0%

Interest of plan assets

190000

0

($19000000*10%)

Net interest 300000

4. Reconciliation

Reconciliation

Defined benefit

obligation Plan assets

Balance on 1st Jan 2016 20,000,000.00 19,000,000.00

Past service cost 2,000,000.00

Balance 22,000,000.00

Interest 2,200,000.00 1,900,000.00

Current service cost 800,000.00

Contributions received during the

year - 1,000,000.00

Benefits paid (2,100,000.00)

(2,100,000.00

)

Return on plan assets - 330,000.00

Actuarial loss 100,000.00

Balance on 31st Dec 2016 23,000,000.00 20,130,000.00

Return on plan assets

20130000-(190000000+1900000+1000000-2100000)

Page 10 of 12

2. Net Defined Benefit Liability

The company would recognize the net defined benefit liability of $2,870,000.

3. Net Interest

Net interest

Interest of liability

component

220000

0

($20000000+2000000)*1

0%

Interest of plan assets

190000

0

($19000000*10%)

Net interest 300000

4. Reconciliation

Reconciliation

Defined benefit

obligation Plan assets

Balance on 1st Jan 2016 20,000,000.00 19,000,000.00

Past service cost 2,000,000.00

Balance 22,000,000.00

Interest 2,200,000.00 1,900,000.00

Current service cost 800,000.00

Contributions received during the

year - 1,000,000.00

Benefits paid (2,100,000.00)

(2,100,000.00

)

Return on plan assets - 330,000.00

Actuarial loss 100,000.00

Balance on 31st Dec 2016 23,000,000.00 20,130,000.00

Return on plan assets

20130000-(190000000+1900000+1000000-2100000)

Page 10 of 12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

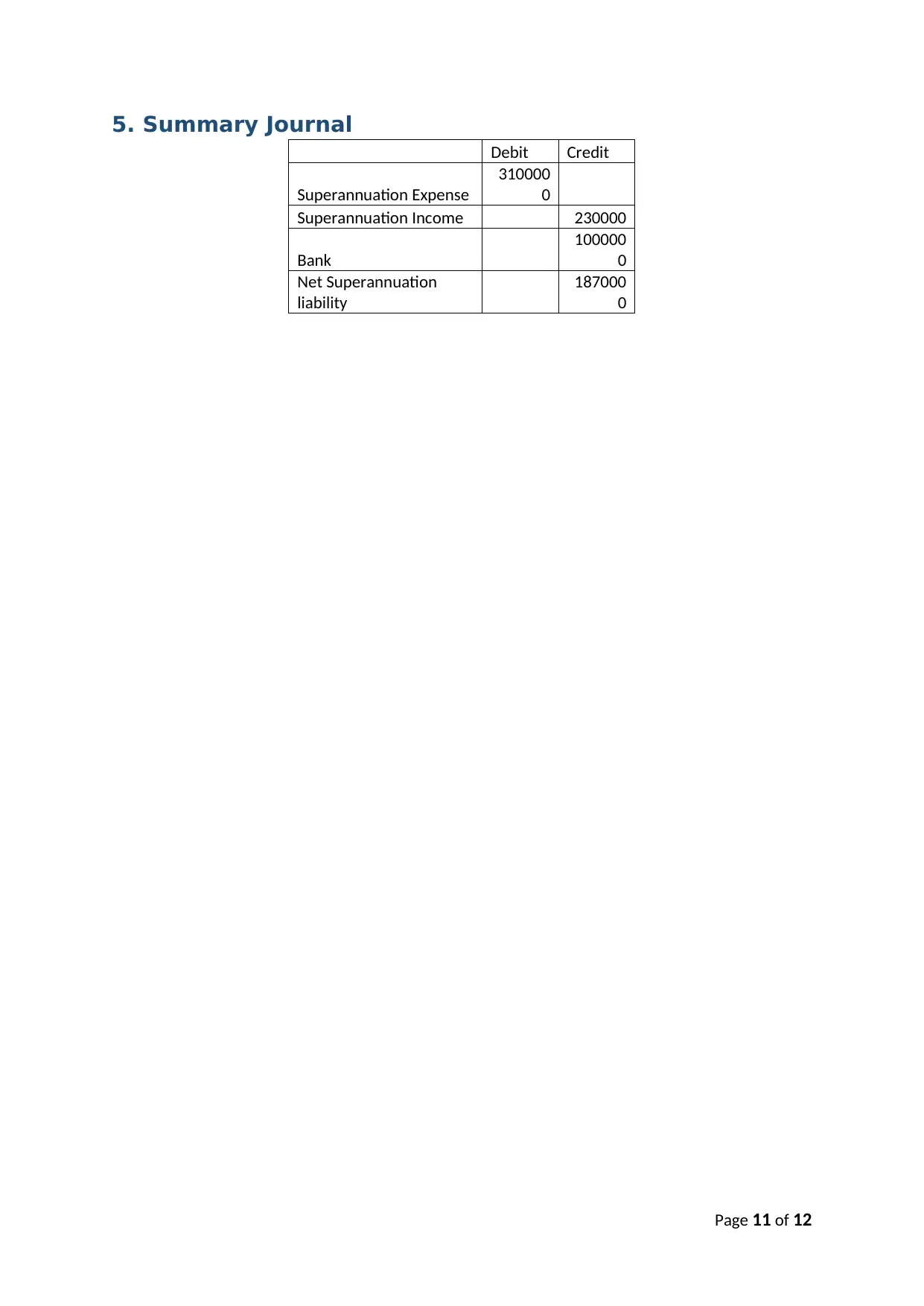

5. Summary Journal

Debit Credit

Superannuation Expense

310000

0

Superannuation Income 230000

Bank

100000

0

Net Superannuation

liability

187000

0

Page 11 of 12

Debit Credit

Superannuation Expense

310000

0

Superannuation Income 230000

Bank

100000

0

Net Superannuation

liability

187000

0

Page 11 of 12

References

Horngren, C. et al. 2012. Accounting. Pearson Higher Education AU.

Dagwell, R., Wines, G., & Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

AASB 13. (2012). Fair value measurement. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_09-

11_COMPdec12_07-13.pdf

AASB. (2015). Conceptual framework. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

AASB 136. (2010). Impairment of assets. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-

04_COMPjun09_01-10.pdf

AASB 138. (2014). Intangible assets. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPoct15_01-18.pdf

AASB 119. (2011). Employee Benefits. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11.pdf

Page 12 of 12

Horngren, C. et al. 2012. Accounting. Pearson Higher Education AU.

Dagwell, R., Wines, G., & Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

AASB 13. (2012). Fair value measurement. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_09-

11_COMPdec12_07-13.pdf

AASB. (2015). Conceptual framework. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

AASB 136. (2010). Impairment of assets. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB136_07-

04_COMPjun09_01-10.pdf

AASB 138. (2014). Intangible assets. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPoct15_01-18.pdf

AASB 119. (2011). Employee Benefits. Retrieved August 15, 2017, from

http://www.aasb.gov.au/admin/file/content105/c9/AASB119_09-11.pdf

Page 12 of 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.