Financial Reporting Analysis: Tesco, Financial Statements, and IFRS

VerifiedAdded on 2021/02/19

|16

|4262

|68

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, exploring its context, purpose, and the regulatory framework, including IAS and IFRS. It examines the qualitative characteristics of financial information and identifies the main stakeholders of an organization, detailing how they benefit from financial reporting. The report further discusses the value of financial reporting in meeting organizational objectives and driving growth. It presents the main financial statements, including the statement of profit or loss, statement of changes in equity, and balance sheet, and explains how to interpret and communicate financial performance. The differences between IAS and IFRS are highlighted, along with the benefits of IFRS and varying degrees of compliance. The report uses Tesco as a case study to illustrate these concepts, providing practical examples and insights into financial reporting practices within a FTSE company.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1. Context and purpose of financial reporting:............................................................................3

2. Conceptual and regulatory framework along with qualitative characteristics of information:

......................................................................................................................................................4

3. Main stakeholders of an organisation and explain how they benefit:......................................5

4. Value of financial reporting for meeting organisational objectives and growth:....................7

5. Present the main financial statements:.....................................................................................7

6. Interpret and communicate the financial performance:...........................................................9

7. Difference between IAS and IFRS:.......................................................................................11

8. Benefits of IFRS:...................................................................................................................11

9. Identify the varying degrees of compliance with IFRS:........................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

ANNEXURE..................................................................................................................................15

INTRODUCTION...........................................................................................................................3

1. Context and purpose of financial reporting:............................................................................3

2. Conceptual and regulatory framework along with qualitative characteristics of information:

......................................................................................................................................................4

3. Main stakeholders of an organisation and explain how they benefit:......................................5

4. Value of financial reporting for meeting organisational objectives and growth:....................7

5. Present the main financial statements:.....................................................................................7

6. Interpret and communicate the financial performance:...........................................................9

7. Difference between IAS and IFRS:.......................................................................................11

8. Benefits of IFRS:...................................................................................................................11

9. Identify the varying degrees of compliance with IFRS:........................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

ANNEXURE..................................................................................................................................15

INTRODUCTION

Financial reporting is combined set of activities and practices which are dedicated

towards prompt presentation and reporting of monetary events and other business transaction in

systematic and regularised manner. Practices involved in financial reporting ensures proper and

effective compliance of relevant accounting policies, procedures and other statutory

requirements. Financial reporting requires disclosing fiscal data over a defined time period to the

multiple stakeholders on organisation's fiscal efficiencies and performance position. These

stakeholders involve–shareholders, investors, government bodies, banks, debt providers. The

purpose of study report is to enhance comprehension of financial reporting as well as its

significance to enterprises (Billings and Lewis‐Western, 2016). Its aim is to continue providing

information and inputs to a company's management, which are used for monitoring, evaluation,

performance metrics and decision-making purposes. As a junior auditor of a large accounting

and consultancy enterprise, Smith & Williamson, a FTSE company is selected to better explain

all the above-mentioned terms and that company is Tesco.

The study evaluates main context and aim of financial reporting, major qualitative

features which required to generate reliable financial, corporation's stakeholders and importance

of financial information and role of financial-reporting. Moreover, it contains practical sum

related to preparation of IAS based financial statement. It also contains key departure between

IFRS and IAS and degree of compliances related to them.

1. Context and purpose of financial reporting:

In commercial environment, financial reporting has now been known to play a crucial

role in the development and establishment of the global financial system. The principal purpose

is to ensure that users have data and facts that is efficient and valuable so that significant choices

are made in order to improve enterprise effectiveness. Managers need an annual report

summarizing the effectiveness and the condition of their corporation to assess how often they

have achieved their business throughout an accounting period. Financial reporting is also

concerned with adoption of regulatory and compliance framework-based structure (Cohen and

Karatzimas, 2015). Reporting in corporations is done by accountants and management personnel

on periodical basis like annual, quarter, monthly etc. For both internal and external purposes

financial reporting is used by corporations which ultimately supports decision-making. It is the

Financial reporting is combined set of activities and practices which are dedicated

towards prompt presentation and reporting of monetary events and other business transaction in

systematic and regularised manner. Practices involved in financial reporting ensures proper and

effective compliance of relevant accounting policies, procedures and other statutory

requirements. Financial reporting requires disclosing fiscal data over a defined time period to the

multiple stakeholders on organisation's fiscal efficiencies and performance position. These

stakeholders involve–shareholders, investors, government bodies, banks, debt providers. The

purpose of study report is to enhance comprehension of financial reporting as well as its

significance to enterprises (Billings and Lewis‐Western, 2016). Its aim is to continue providing

information and inputs to a company's management, which are used for monitoring, evaluation,

performance metrics and decision-making purposes. As a junior auditor of a large accounting

and consultancy enterprise, Smith & Williamson, a FTSE company is selected to better explain

all the above-mentioned terms and that company is Tesco.

The study evaluates main context and aim of financial reporting, major qualitative

features which required to generate reliable financial, corporation's stakeholders and importance

of financial information and role of financial-reporting. Moreover, it contains practical sum

related to preparation of IAS based financial statement. It also contains key departure between

IFRS and IAS and degree of compliances related to them.

1. Context and purpose of financial reporting:

In commercial environment, financial reporting has now been known to play a crucial

role in the development and establishment of the global financial system. The principal purpose

is to ensure that users have data and facts that is efficient and valuable so that significant choices

are made in order to improve enterprise effectiveness. Managers need an annual report

summarizing the effectiveness and the condition of their corporation to assess how often they

have achieved their business throughout an accounting period. Financial reporting is also

concerned with adoption of regulatory and compliance framework-based structure (Cohen and

Karatzimas, 2015). Reporting in corporations is done by accountants and management personnel

on periodical basis like annual, quarter, monthly etc. For both internal and external purposes

financial reporting is used by corporations which ultimately supports decision-making. It is the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

presentation of corporation's significant monetary information & certain operations to different

stakeholders to support them at every stage in period get core performance information about

incorporation. In this context following are core purposes linked to financial reporting, as

discussed below:

Financial reporting's principal aim is to avoid conflicts related to accounting procedures

adopted by ensuring proper compliance with accounting standards like IAS, IFRS etc.

Main purpose behind adoption of Financial reporting is that it facilitates effective linking

of organisational objectives and decision-making processes with company's accounting

framework dedicated to present and prepare fiscal reports.

It facilitates effective and prompt decision making for investors by providing key fiscal

reports and statements.

It aims to remove any misleading information. which can be reported in financial

statements of corporation (Dichev, 2017).

It supports management of major productive activities of company by providing useful

and quick information.

Provide relevant information through financial statements based on which banks and

financial institutions provides loans and credit-related facilities.

Financial reports generated under process of financial reporting build trust in users of

corporation's financial reports.

2. Conceptual and regulatory framework along with qualitative characteristics of information:

Conceptual and Regulatory framework: Regulatory framework is a mechanism which

assure effective compliance of rules and regulations issued by regulatory authorities. It aims to

assure that individuals obtain a reasonable level of information to make massive decisions based

on their concern in reporting organization.

While a conceptual framework relates to coherent structure of interlinked principles and

objectives (Durnev and Magnan, 2017). A framework that sets out the essence, feature, and

boundaries of business's financial accounting as well as reporting. Conceptual frameworks may

extend to plenty of areas, but where particularly relating to financial reporting is concerned, a

conceptual framework could be viewed as a declaration of GAAP that constitute a reference

point for evaluating current practices and developing fresh ones. Conceptual Framework's aim is

to assist in preparation of financial statements in developing accounting-policies for events or

stakeholders to support them at every stage in period get core performance information about

incorporation. In this context following are core purposes linked to financial reporting, as

discussed below:

Financial reporting's principal aim is to avoid conflicts related to accounting procedures

adopted by ensuring proper compliance with accounting standards like IAS, IFRS etc.

Main purpose behind adoption of Financial reporting is that it facilitates effective linking

of organisational objectives and decision-making processes with company's accounting

framework dedicated to present and prepare fiscal reports.

It facilitates effective and prompt decision making for investors by providing key fiscal

reports and statements.

It aims to remove any misleading information. which can be reported in financial

statements of corporation (Dichev, 2017).

It supports management of major productive activities of company by providing useful

and quick information.

Provide relevant information through financial statements based on which banks and

financial institutions provides loans and credit-related facilities.

Financial reports generated under process of financial reporting build trust in users of

corporation's financial reports.

2. Conceptual and regulatory framework along with qualitative characteristics of information:

Conceptual and Regulatory framework: Regulatory framework is a mechanism which

assure effective compliance of rules and regulations issued by regulatory authorities. It aims to

assure that individuals obtain a reasonable level of information to make massive decisions based

on their concern in reporting organization.

While a conceptual framework relates to coherent structure of interlinked principles and

objectives (Durnev and Magnan, 2017). A framework that sets out the essence, feature, and

boundaries of business's financial accounting as well as reporting. Conceptual frameworks may

extend to plenty of areas, but where particularly relating to financial reporting is concerned, a

conceptual framework could be viewed as a declaration of GAAP that constitute a reference

point for evaluating current practices and developing fresh ones. Conceptual Framework's aim is

to assist in preparation of financial statements in developing accounting-policies for events or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transactions not covered by existing standards. These frameworks enable development in

accounting practices in conjunction with recognized principles of accounting standards and

generally accepted accounting principles (GAAP). With much more complicated and advanced

operations and corporations, it enables accounts developers and auditors dealing with non-

accounting but financial nature operations. Principle-based accountability norms should be more

difficult to bypass, so frameworks reinforce the legitimacy of accounting practice as well as

financial reporting.

Qualitative characteristics:

Qualitative characteristics refers to quality criteria for information generated form

financial reporting processes. These characteristics make all information related to any

corporation, useful and relevant for business decision-making. Consideration of these threshold

qualities in information generated is crucial to determine appropriate usage of information. In

this context following are significant qualitative characteristics which contributes in making

information more reliable, as follows:

Completeness:

This is basic criteria and qualitative characteristic which requires that information

retrieved form financial reporting' processes should be complete and information must contain all

the necessary descriptions and explanations. Information must be complete in all aspects and

covers all significant facts or figures are clearly mentioned (Kotas, 2014).

Bias-free information:

Information required to be bias-free. Financial statements are often not unbiased if they

affect decision-making or judgements to obtain a predefined result or outcome by selecting or

presenting data.

Free from error:

Information inside the boundaries of subjectivity has to be free from mistake. A material

error, mistake or misrepresentation may result in financial reports being incorrect or inaccurate

and therefore untrustworthy and inadequate in aspects of their significance (Krismiaji, Aryani

and Suhardjanto, 2016).

3. Main stakeholders of an organisation and explain how they benefit:

Stakeholders are parties which are closely associated with business and its environment

and highly affected by actions of corporation or could affect organisation's actions. These are

accounting practices in conjunction with recognized principles of accounting standards and

generally accepted accounting principles (GAAP). With much more complicated and advanced

operations and corporations, it enables accounts developers and auditors dealing with non-

accounting but financial nature operations. Principle-based accountability norms should be more

difficult to bypass, so frameworks reinforce the legitimacy of accounting practice as well as

financial reporting.

Qualitative characteristics:

Qualitative characteristics refers to quality criteria for information generated form

financial reporting processes. These characteristics make all information related to any

corporation, useful and relevant for business decision-making. Consideration of these threshold

qualities in information generated is crucial to determine appropriate usage of information. In

this context following are significant qualitative characteristics which contributes in making

information more reliable, as follows:

Completeness:

This is basic criteria and qualitative characteristic which requires that information

retrieved form financial reporting' processes should be complete and information must contain all

the necessary descriptions and explanations. Information must be complete in all aspects and

covers all significant facts or figures are clearly mentioned (Kotas, 2014).

Bias-free information:

Information required to be bias-free. Financial statements are often not unbiased if they

affect decision-making or judgements to obtain a predefined result or outcome by selecting or

presenting data.

Free from error:

Information inside the boundaries of subjectivity has to be free from mistake. A material

error, mistake or misrepresentation may result in financial reports being incorrect or inaccurate

and therefore untrustworthy and inadequate in aspects of their significance (Krismiaji, Aryani

and Suhardjanto, 2016).

3. Main stakeholders of an organisation and explain how they benefit:

Stakeholders are parties which are closely associated with business and its environment

and highly affected by actions of corporation or could affect organisation's actions. These are

interested or concerned in corporation's fiscal results and outcomes in direct or indirect manner.

Corporations are also benefited or influenced by actions and decisions of stakeholders.

Identification of current actions and potential steps are necessary to minimise the negative

impact of such actions and steps. Stakeholder in organisational context are categorised by

internal and external.

Internal Stakeholders are crucial part of business enterprise, these mainly includes

employees, managing officials, directors etc. Here is discussion on internal stakeholders and how

they get benefited from financial information, as follows:

Employees: These are not only effective resources of a corporation but also crucial

internal stakeholders which works for business's objectives and targets. They are get benefited by

financial information as they want to be assured about corporation's future and current growth to

ensure their future in respective organisation (Lail, MacGregor and Stuebs, 2017).

Directors: Directors are also internal stakeholders who always worried about

corporation's performance and growth in industry. Directors majorly use financial information to

take appropriate and momentous corporate decisions and competitive strategies with aim to

achieve targeted performance and results.

External stakeholders are not integral part of corporation but affects functioning and

performance. Major external stakeholders are suppliers, regulatory bodies, government,

customers etc. Following is discussion on main external stakeholders and in which way they are

get benefited from financial information, as follows:

Government and regulatory authority: These are top influencers and external

stakeholders as every organisation is required to follow guidelines and instructions issued by

them. They apply financial information to assess tax liabilities of corporation as this is the main

income source of government which is beneficial for government to increase tax revenue.

Financial information also advantageous for government also using to establish control by

ensuring that all rules and compliances are followed or not (Mio, 2016).

Customer: They are most considerable external stakeholders who are responsible for

corporation's sales. Financial information is beneficial for company's customers to determines its

brand value and popularity of products.

Corporations are also benefited or influenced by actions and decisions of stakeholders.

Identification of current actions and potential steps are necessary to minimise the negative

impact of such actions and steps. Stakeholder in organisational context are categorised by

internal and external.

Internal Stakeholders are crucial part of business enterprise, these mainly includes

employees, managing officials, directors etc. Here is discussion on internal stakeholders and how

they get benefited from financial information, as follows:

Employees: These are not only effective resources of a corporation but also crucial

internal stakeholders which works for business's objectives and targets. They are get benefited by

financial information as they want to be assured about corporation's future and current growth to

ensure their future in respective organisation (Lail, MacGregor and Stuebs, 2017).

Directors: Directors are also internal stakeholders who always worried about

corporation's performance and growth in industry. Directors majorly use financial information to

take appropriate and momentous corporate decisions and competitive strategies with aim to

achieve targeted performance and results.

External stakeholders are not integral part of corporation but affects functioning and

performance. Major external stakeholders are suppliers, regulatory bodies, government,

customers etc. Following is discussion on main external stakeholders and in which way they are

get benefited from financial information, as follows:

Government and regulatory authority: These are top influencers and external

stakeholders as every organisation is required to follow guidelines and instructions issued by

them. They apply financial information to assess tax liabilities of corporation as this is the main

income source of government which is beneficial for government to increase tax revenue.

Financial information also advantageous for government also using to establish control by

ensuring that all rules and compliances are followed or not (Mio, 2016).

Customer: They are most considerable external stakeholders who are responsible for

corporation's sales. Financial information is beneficial for company's customers to determines its

brand value and popularity of products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Value of financial reporting for meeting organisational objectives and growth:

Financial reporting help to assess and produce financial statements and reports which

guarantees the accuracy and reliability of information stated in it. On basis of these financial

statements corporations determines their strategies and key action-plans. The financial

statements are beneficial for each entity which can aid in accomplishment of objectives of an

entity. The management uses various key financial reports related to every business operation to

evaluate the full performance as well as present situation in any accounting period. It also

supports to develop efficient policies and plans as per the corporation's need so that general

economic and fiscal status could be readily interpreted by financial reporting. It supports whole

managerial structure by providing relevancy features in generated information. Based on

financial reporting results managers prepare budgets based on targeted growth and objectives.

Financial Reporting and organisation's development:

Financial reporting information supports different organisational operations to bring new

developments and improvements. It covers information related to all major operations and

activities of organisation which further used by managing officials to prepare blueprint for

overall development of business entity (Mukhlisin, Hudaib and Azid, 2015). Following are

benefits of financial reporting in context of

organisational development, as discussed below:

Develop real time controlling: Financial reporting processes generates updated and real-

time information of organisation's key operations which finally used by managing personnel to

establish and develop real-time controlling over all organisational functions.

Structure for thorough analysis: Financial reporting information and results are used to

develop a structure for full and detailed analysis of performance over specific period with aim to

overall development of corporation.

Structured debt-management: It also facilitates an organised and structured debt-

management which assist management to avoid adversities related to liquidity position of

business enterprise (Nnadi and Soobaroyen, 2015).

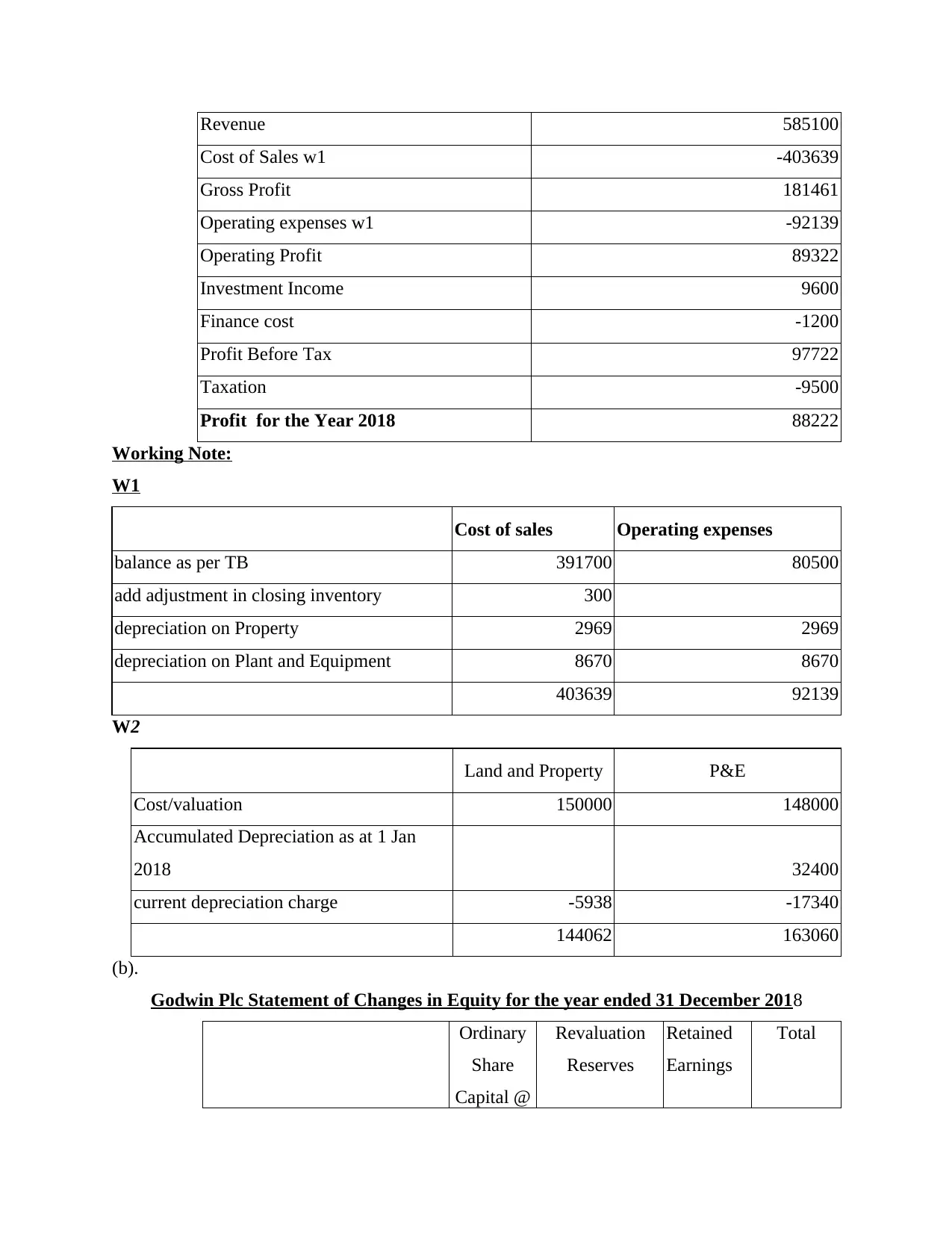

5. Present the main financial statements:

(a).

GODWIN Plc Statement of Profit or Loss for the year ended 31 December 2018

£

Financial reporting help to assess and produce financial statements and reports which

guarantees the accuracy and reliability of information stated in it. On basis of these financial

statements corporations determines their strategies and key action-plans. The financial

statements are beneficial for each entity which can aid in accomplishment of objectives of an

entity. The management uses various key financial reports related to every business operation to

evaluate the full performance as well as present situation in any accounting period. It also

supports to develop efficient policies and plans as per the corporation's need so that general

economic and fiscal status could be readily interpreted by financial reporting. It supports whole

managerial structure by providing relevancy features in generated information. Based on

financial reporting results managers prepare budgets based on targeted growth and objectives.

Financial Reporting and organisation's development:

Financial reporting information supports different organisational operations to bring new

developments and improvements. It covers information related to all major operations and

activities of organisation which further used by managing officials to prepare blueprint for

overall development of business entity (Mukhlisin, Hudaib and Azid, 2015). Following are

benefits of financial reporting in context of

organisational development, as discussed below:

Develop real time controlling: Financial reporting processes generates updated and real-

time information of organisation's key operations which finally used by managing personnel to

establish and develop real-time controlling over all organisational functions.

Structure for thorough analysis: Financial reporting information and results are used to

develop a structure for full and detailed analysis of performance over specific period with aim to

overall development of corporation.

Structured debt-management: It also facilitates an organised and structured debt-

management which assist management to avoid adversities related to liquidity position of

business enterprise (Nnadi and Soobaroyen, 2015).

5. Present the main financial statements:

(a).

GODWIN Plc Statement of Profit or Loss for the year ended 31 December 2018

£

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revenue 585100

Cost of Sales w1 -403639

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Working Note:

W1

Cost of sales Operating expenses

balance as per TB 391700 80500

add adjustment in closing inventory 300

depreciation on Property 2969 2969

depreciation on Plant and Equipment 8670 8670

403639 92139

W2

Land and Property P&E

Cost/valuation 150000 148000

Accumulated Depreciation as at 1 Jan

2018 32400

current depreciation charge -5938 -17340

144062 163060

(b).

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

Ordinary

Share

Capital @

Revaluation

Reserves

Retained

Earnings

Total

Cost of Sales w1 -403639

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Working Note:

W1

Cost of sales Operating expenses

balance as per TB 391700 80500

add adjustment in closing inventory 300

depreciation on Property 2969 2969

depreciation on Plant and Equipment 8670 8670

403639 92139

W2

Land and Property P&E

Cost/valuation 150000 148000

Accumulated Depreciation as at 1 Jan

2018 32400

current depreciation charge -5938 -17340

144062 163060

(b).

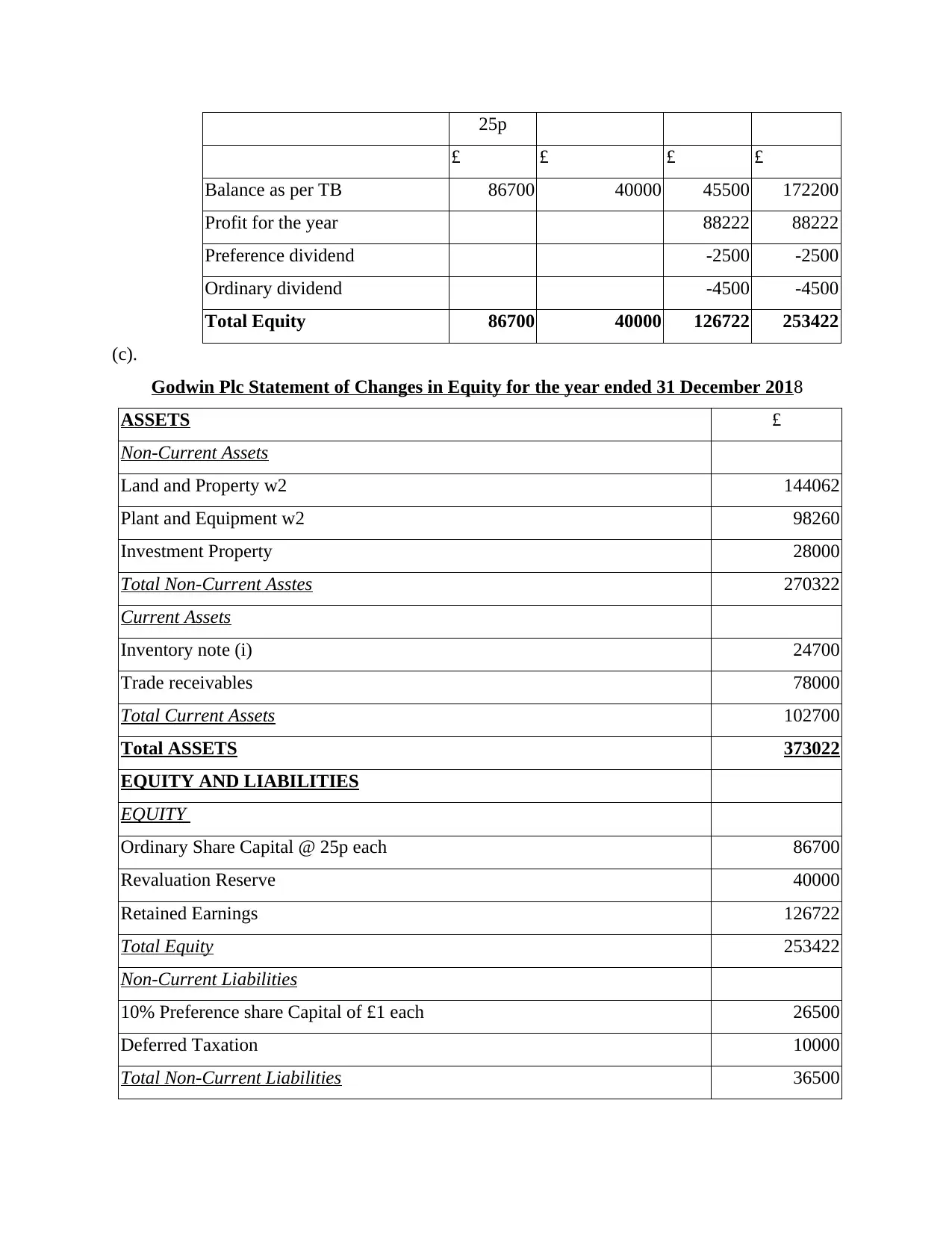

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

Ordinary

Share

Capital @

Revaluation

Reserves

Retained

Earnings

Total

25p

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

(c).

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

Plant and Equipment w2 98260

Investment Property 28000

Total Non-Current Asstes 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

Total Equity 253422

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

(c).

Godwin Plc Statement of Changes in Equity for the year ended 31 December 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

Plant and Equipment w2 98260

Investment Property 28000

Total Non-Current Asstes 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

Total Equity 253422

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

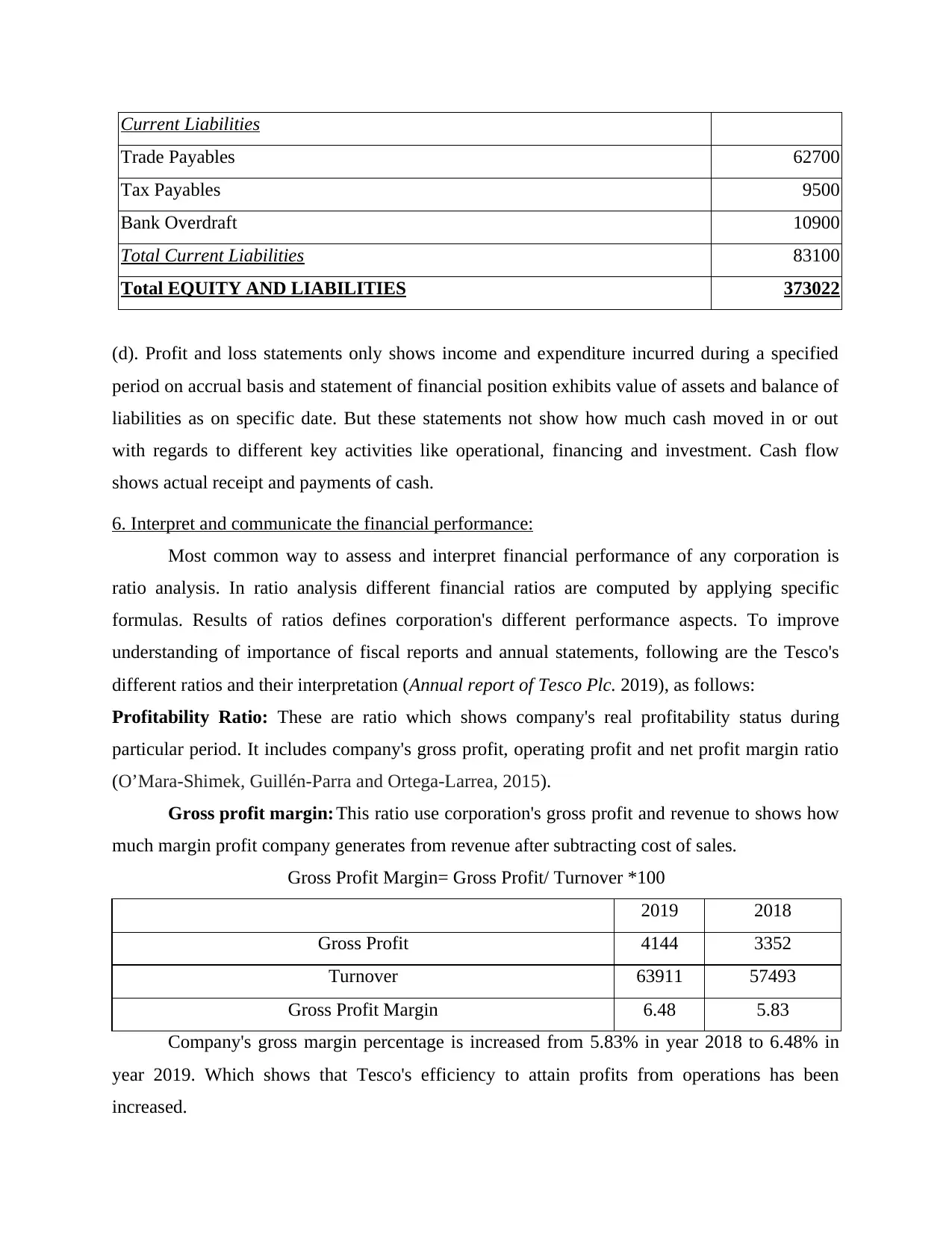

Current Liabilities

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

(d). Profit and loss statements only shows income and expenditure incurred during a specified

period on accrual basis and statement of financial position exhibits value of assets and balance of

liabilities as on specific date. But these statements not show how much cash moved in or out

with regards to different key activities like operational, financing and investment. Cash flow

shows actual receipt and payments of cash.

6. Interpret and communicate the financial performance:

Most common way to assess and interpret financial performance of any corporation is

ratio analysis. In ratio analysis different financial ratios are computed by applying specific

formulas. Results of ratios defines corporation's different performance aspects. To improve

understanding of importance of fiscal reports and annual statements, following are the Tesco's

different ratios and their interpretation (Annual report of Tesco Plc. 2019), as follows:

Profitability Ratio: These are ratio which shows company's real profitability status during

particular period. It includes company's gross profit, operating profit and net profit margin ratio

(O’Mara-Shimek, Guillén-Parra and Ortega-Larrea, 2015).

Gross profit margin: This ratio use corporation's gross profit and revenue to shows how

much margin profit company generates from revenue after subtracting cost of sales.

Gross Profit Margin= Gross Profit/ Turnover *100

2019 2018

Gross Profit 4144 3352

Turnover 63911 57493

Gross Profit Margin 6.48 5.83

Company's gross margin percentage is increased from 5.83% in year 2018 to 6.48% in

year 2019. Which shows that Tesco's efficiency to attain profits from operations has been

increased.

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

(d). Profit and loss statements only shows income and expenditure incurred during a specified

period on accrual basis and statement of financial position exhibits value of assets and balance of

liabilities as on specific date. But these statements not show how much cash moved in or out

with regards to different key activities like operational, financing and investment. Cash flow

shows actual receipt and payments of cash.

6. Interpret and communicate the financial performance:

Most common way to assess and interpret financial performance of any corporation is

ratio analysis. In ratio analysis different financial ratios are computed by applying specific

formulas. Results of ratios defines corporation's different performance aspects. To improve

understanding of importance of fiscal reports and annual statements, following are the Tesco's

different ratios and their interpretation (Annual report of Tesco Plc. 2019), as follows:

Profitability Ratio: These are ratio which shows company's real profitability status during

particular period. It includes company's gross profit, operating profit and net profit margin ratio

(O’Mara-Shimek, Guillén-Parra and Ortega-Larrea, 2015).

Gross profit margin: This ratio use corporation's gross profit and revenue to shows how

much margin profit company generates from revenue after subtracting cost of sales.

Gross Profit Margin= Gross Profit/ Turnover *100

2019 2018

Gross Profit 4144 3352

Turnover 63911 57493

Gross Profit Margin 6.48 5.83

Company's gross margin percentage is increased from 5.83% in year 2018 to 6.48% in

year 2019. Which shows that Tesco's efficiency to attain profits from operations has been

increased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

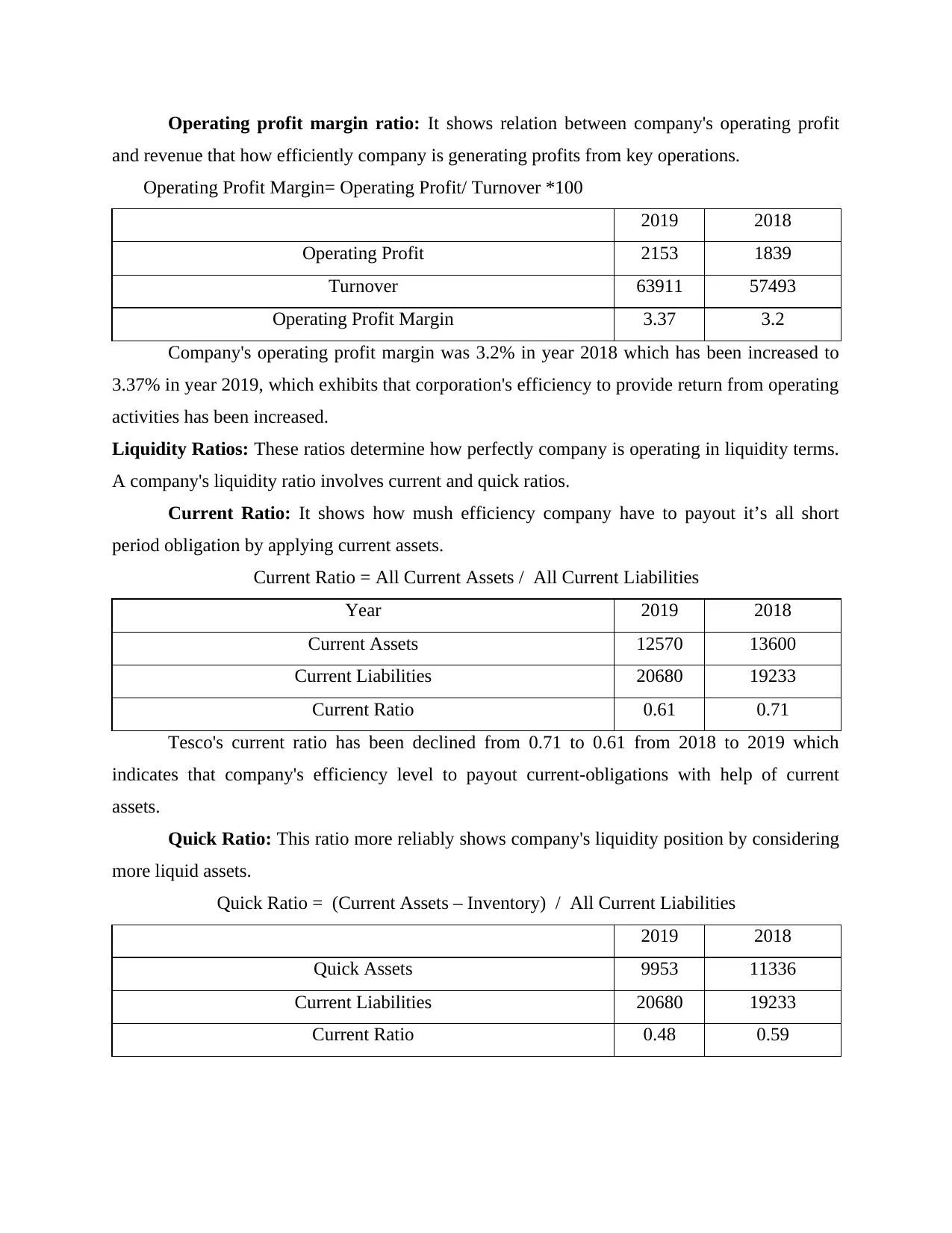

Operating profit margin ratio: It shows relation between company's operating profit

and revenue that how efficiently company is generating profits from key operations.

Operating Profit Margin= Operating Profit/ Turnover *100

2019 2018

Operating Profit 2153 1839

Turnover 63911 57493

Operating Profit Margin 3.37 3.2

Company's operating profit margin was 3.2% in year 2018 which has been increased to

3.37% in year 2019, which exhibits that corporation's efficiency to provide return from operating

activities has been increased.

Liquidity Ratios: These ratios determine how perfectly company is operating in liquidity terms.

A company's liquidity ratio involves current and quick ratios.

Current Ratio: It shows how mush efficiency company have to payout it’s all short

period obligation by applying current assets.

Current Ratio = All Current Assets / All Current Liabilities

Year 2019 2018

Current Assets 12570 13600

Current Liabilities 20680 19233

Current Ratio 0.61 0.71

Tesco's current ratio has been declined from 0.71 to 0.61 from 2018 to 2019 which

indicates that company's efficiency level to payout current-obligations with help of current

assets.

Quick Ratio: This ratio more reliably shows company's liquidity position by considering

more liquid assets.

Quick Ratio = (Current Assets – Inventory) / All Current Liabilities

2019 2018

Quick Assets 9953 11336

Current Liabilities 20680 19233

Current Ratio 0.48 0.59

and revenue that how efficiently company is generating profits from key operations.

Operating Profit Margin= Operating Profit/ Turnover *100

2019 2018

Operating Profit 2153 1839

Turnover 63911 57493

Operating Profit Margin 3.37 3.2

Company's operating profit margin was 3.2% in year 2018 which has been increased to

3.37% in year 2019, which exhibits that corporation's efficiency to provide return from operating

activities has been increased.

Liquidity Ratios: These ratios determine how perfectly company is operating in liquidity terms.

A company's liquidity ratio involves current and quick ratios.

Current Ratio: It shows how mush efficiency company have to payout it’s all short

period obligation by applying current assets.

Current Ratio = All Current Assets / All Current Liabilities

Year 2019 2018

Current Assets 12570 13600

Current Liabilities 20680 19233

Current Ratio 0.61 0.71

Tesco's current ratio has been declined from 0.71 to 0.61 from 2018 to 2019 which

indicates that company's efficiency level to payout current-obligations with help of current

assets.

Quick Ratio: This ratio more reliably shows company's liquidity position by considering

more liquid assets.

Quick Ratio = (Current Assets – Inventory) / All Current Liabilities

2019 2018

Quick Assets 9953 11336

Current Liabilities 20680 19233

Current Ratio 0.48 0.59

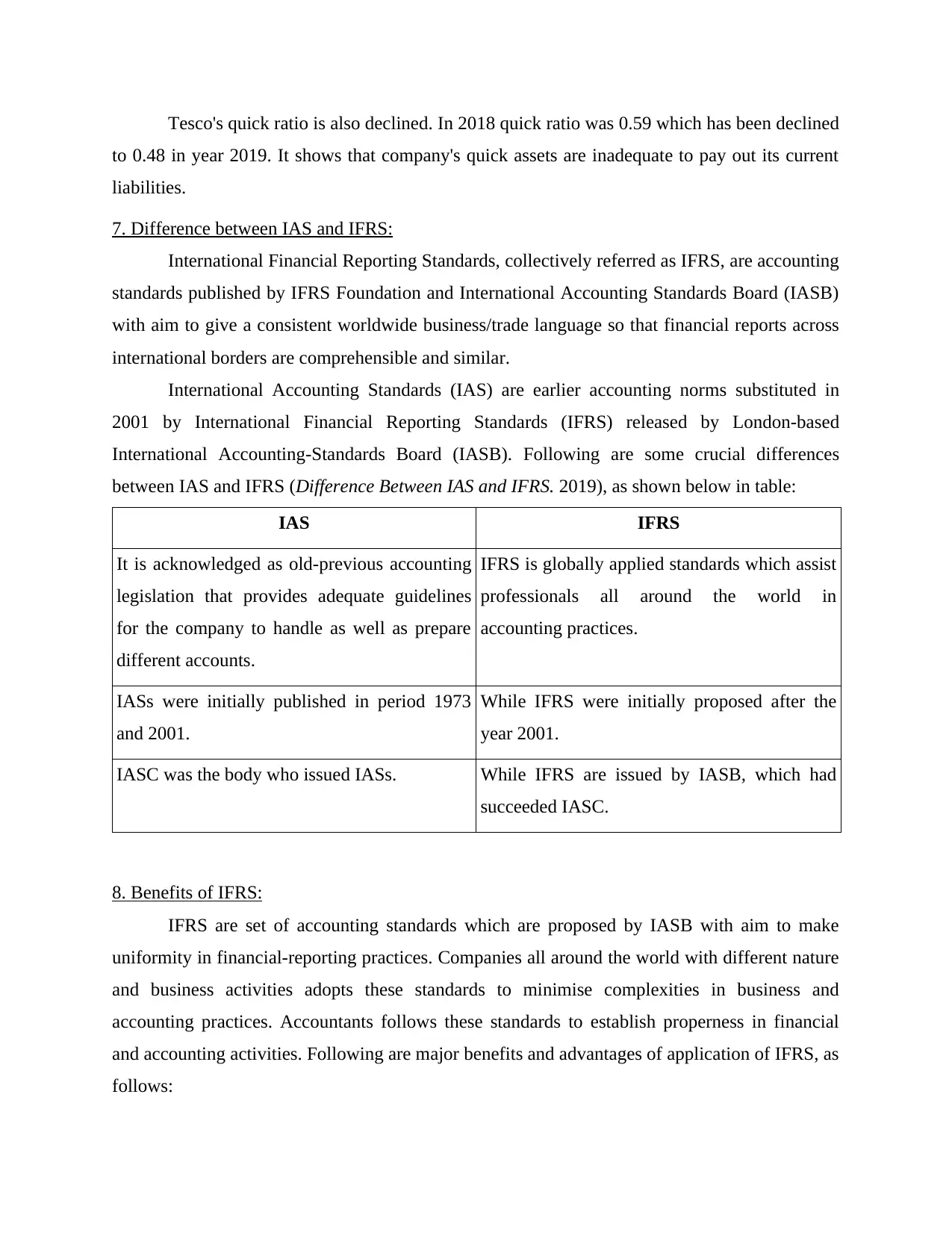

Tesco's quick ratio is also declined. In 2018 quick ratio was 0.59 which has been declined

to 0.48 in year 2019. It shows that company's quick assets are inadequate to pay out its current

liabilities.

7. Difference between IAS and IFRS:

International Financial Reporting Standards, collectively referred as IFRS, are accounting

standards published by IFRS Foundation and International Accounting Standards Board (IASB)

with aim to give a consistent worldwide business/trade language so that financial reports across

international borders are comprehensible and similar.

International Accounting Standards (IAS) are earlier accounting norms substituted in

2001 by International Financial Reporting Standards (IFRS) released by London-based

International Accounting-Standards Board (IASB). Following are some crucial differences

between IAS and IFRS (Difference Between IAS and IFRS. 2019), as shown below in table:

IAS IFRS

It is acknowledged as old-previous accounting

legislation that provides adequate guidelines

for the company to handle as well as prepare

different accounts.

IFRS is globally applied standards which assist

professionals all around the world in

accounting practices.

IASs were initially published in period 1973

and 2001.

While IFRS were initially proposed after the

year 2001.

IASC was the body who issued IASs. While IFRS are issued by IASB, which had

succeeded IASC.

8. Benefits of IFRS:

IFRS are set of accounting standards which are proposed by IASB with aim to make

uniformity in financial-reporting practices. Companies all around the world with different nature

and business activities adopts these standards to minimise complexities in business and

accounting practices. Accountants follows these standards to establish properness in financial

and accounting activities. Following are major benefits and advantages of application of IFRS, as

follows:

to 0.48 in year 2019. It shows that company's quick assets are inadequate to pay out its current

liabilities.

7. Difference between IAS and IFRS:

International Financial Reporting Standards, collectively referred as IFRS, are accounting

standards published by IFRS Foundation and International Accounting Standards Board (IASB)

with aim to give a consistent worldwide business/trade language so that financial reports across

international borders are comprehensible and similar.

International Accounting Standards (IAS) are earlier accounting norms substituted in

2001 by International Financial Reporting Standards (IFRS) released by London-based

International Accounting-Standards Board (IASB). Following are some crucial differences

between IAS and IFRS (Difference Between IAS and IFRS. 2019), as shown below in table:

IAS IFRS

It is acknowledged as old-previous accounting

legislation that provides adequate guidelines

for the company to handle as well as prepare

different accounts.

IFRS is globally applied standards which assist

professionals all around the world in

accounting practices.

IASs were initially published in period 1973

and 2001.

While IFRS were initially proposed after the

year 2001.

IASC was the body who issued IASs. While IFRS are issued by IASB, which had

succeeded IASC.

8. Benefits of IFRS:

IFRS are set of accounting standards which are proposed by IASB with aim to make

uniformity in financial-reporting practices. Companies all around the world with different nature

and business activities adopts these standards to minimise complexities in business and

accounting practices. Accountants follows these standards to establish properness in financial

and accounting activities. Following are major benefits and advantages of application of IFRS, as

follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.