Comprehensive Case Study: Financial Reporting of Tesco PLC and IFRS

VerifiedAdded on 2020/06/04

|17

|3327

|76

Case Study

AI Summary

This case study examines the financial reporting practices of Tesco PLC, a major player in the retail sector. It begins by outlining the purpose of financial reporting and the conceptual frameworks underpinning it, emphasizing the role of IFRS. The study then identifies Tesco's stakeholders and their reliance on financial information. It explores how financial reporting supports firm objectives, detailing the components of financial statements such as income statements, cash flow statements, and balance sheets. The analysis includes an interpretation of Tesco's financial performance, particularly its profitability ratios, comparing 2016 and 2017. The case study also highlights the differences between IFRS and IAS, the advantages of IFRS, and the factors influencing global compliance. Overall, the case study provides a comprehensive overview of Tesco PLC's financial reporting, its implications, and its adherence to international standards.

CASE STUDY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1.Purpose of financial reporting:.................................................................................................1

2. Conceptual frameworks of financial reporting:......................................................................2

3. Stakeholder of Tesco plc and and its benefits from financial information:............................2

4. Financial reporting for meeting firm objectives:....................................................................3

6. Financial statement of Tesco plc and interpretation of financial performance:......................6

7. Difference between IFRS and IAS..........................................................................................9

8. Advantages of IFRS..............................................................................................................10

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it:................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

1.Purpose of financial reporting:.................................................................................................1

2. Conceptual frameworks of financial reporting:......................................................................2

3. Stakeholder of Tesco plc and and its benefits from financial information:............................2

4. Financial reporting for meeting firm objectives:....................................................................3

6. Financial statement of Tesco plc and interpretation of financial performance:......................6

7. Difference between IFRS and IAS..........................................................................................9

8. Advantages of IFRS..............................................................................................................10

9.Various degree of compliances with the IFRS by firms across the globe and components

affecting it:................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In this era, every company is adhering the financial regulations in the firm. This is the

process for manufacturing statements which shows firm's financial status to management,

investors and the government (Beyer, A. and et. al., 2010). There are basically four reporting

tools covers in financial reporting. Income statements, balance sheet, cash flow statement and

statements of shareholders equity. These all are used by the firm in order to draw business

strategy. Tesco plc is a supermarket chain which deals in the retail sector. By using financial

reporting, tesco plc can make strategies in order to get the higher advantages.

TASK

1.Purpose of financial reporting:

IFRS framework is the major tools which identify the basic concepts that can be used for

formulation and presentation of financial statements for external users. The IFRS framework

serves as a handbook to the Board in emerging estimated IFRSS and also introducing guidebook

for redressing accounting issues which are not addressed directly under an International

Financial Reporting Standard (Li, 2010.

In the missing of an interpretation which is especially applies to a transaction,

administration are requires to implement its judgement in emerging and applying an accounting

policy which results in information that is justified. In formulation of judgement, IAS 8.11 needs

management to adopt the definitions, acknowledgement criteria, and a measuring concepts for

assets, liabilities, income, and expenses under IFRS framework. This is the main financial

regulatory body which are used to adhere by each company for incorporating business

accounting tools. These are required to frame accounts accordingly. However, these are required

to make their business operations effectively. These financial reporting information are used by

the outsiders and the top level management for making making the strategies. Now, this also

been seen that the management is not able to make their business objectives effective. The

outsiders, with the help of financial statements, are able to make certain investment decisions

after analysing the firm performance (Armstrong, Guay and Weber, 2010). However this has to

be sure that the financial statements are made by the Tesco plc is using the IFRS and regulatory

framework for formulating various financial statement in order to make their business

operations. However, these are made by the accounts specialist so that the transparency can be

1

In this era, every company is adhering the financial regulations in the firm. This is the

process for manufacturing statements which shows firm's financial status to management,

investors and the government (Beyer, A. and et. al., 2010). There are basically four reporting

tools covers in financial reporting. Income statements, balance sheet, cash flow statement and

statements of shareholders equity. These all are used by the firm in order to draw business

strategy. Tesco plc is a supermarket chain which deals in the retail sector. By using financial

reporting, tesco plc can make strategies in order to get the higher advantages.

TASK

1.Purpose of financial reporting:

IFRS framework is the major tools which identify the basic concepts that can be used for

formulation and presentation of financial statements for external users. The IFRS framework

serves as a handbook to the Board in emerging estimated IFRSS and also introducing guidebook

for redressing accounting issues which are not addressed directly under an International

Financial Reporting Standard (Li, 2010.

In the missing of an interpretation which is especially applies to a transaction,

administration are requires to implement its judgement in emerging and applying an accounting

policy which results in information that is justified. In formulation of judgement, IAS 8.11 needs

management to adopt the definitions, acknowledgement criteria, and a measuring concepts for

assets, liabilities, income, and expenses under IFRS framework. This is the main financial

regulatory body which are used to adhere by each company for incorporating business

accounting tools. These are required to frame accounts accordingly. However, these are required

to make their business operations effectively. These financial reporting information are used by

the outsiders and the top level management for making making the strategies. Now, this also

been seen that the management is not able to make their business objectives effective. The

outsiders, with the help of financial statements, are able to make certain investment decisions

after analysing the firm performance (Armstrong, Guay and Weber, 2010). However this has to

be sure that the financial statements are made by the Tesco plc is using the IFRS and regulatory

framework for formulating various financial statement in order to make their business

operations. However, these are made by the accounts specialist so that the transparency can be

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieved. Various regulatory frameworks are used while formulating their business financial

statement. Financial statements are used by the company for knowing the financial performance

in order to make their business operations effective.

2. Conceptual frameworks of financial reporting:

Under financial reporting, a conceptual framework is the theory which is made by the

accounting prepared by the standard setting body against which practical issues could be tested

objectively (Chen and et. al., 2011). A conceptual framework addresses the fundamental

financial reporting problems like- objectives and users of financial statements, characteristics

which form accounting information useable, the fundamental elements of financial statements,

and concepts for addressing these factors under the financial statements.

There are certain benefits of conceptual framework of financial reporting. Which covers:

framing concise definitions which enables discussion of accounting factors; rendering guidance

to accounting standards setters at the time of emerging and reviewing financial reporting rules;

assisting to insure that accounting standards are pursuant with the organisation; assisting

framework makers and auditors to address financial reporting problems under the absence of

accounting standard, and assisting to lower the volume of accounting standards by rendering an

overarching theory of accounting which could be applied to specific reporting issues.

The emergence of first conceptual framework was emerged in the late 1970s by the Financial

Accounting Standard Board (Barth and Landsman, 2010).

3. Stakeholder of Tesco plc and and its benefits from financial information:

Stakeholders: That group of an individual without whom a company cannot exist or operate its

activities are known as stakeholders. Individuals who has some kind of interest in an enterprise

are known as stakeholders. These are the one who affect the activities and business actions of an

organisation. Customers, employees, shareholders, suppliers, local community and national

government are the main stakeholders of an organisation.

It is very essential that all stakeholders of company should have information about the

funds of company as this help in run the business properly and contribute in making more

profits. Financial conditions of a company are one of the major concern for creditors and

investors. Capital provider and creditors of a company rely on financial conditions of a company

for safety. All investors need to know where their money went. Various financial statements such

as balance sheet give them detail information about investment of firm. As balance sheet is list of

2

statement. Financial statements are used by the company for knowing the financial performance

in order to make their business operations effective.

2. Conceptual frameworks of financial reporting:

Under financial reporting, a conceptual framework is the theory which is made by the

accounting prepared by the standard setting body against which practical issues could be tested

objectively (Chen and et. al., 2011). A conceptual framework addresses the fundamental

financial reporting problems like- objectives and users of financial statements, characteristics

which form accounting information useable, the fundamental elements of financial statements,

and concepts for addressing these factors under the financial statements.

There are certain benefits of conceptual framework of financial reporting. Which covers:

framing concise definitions which enables discussion of accounting factors; rendering guidance

to accounting standards setters at the time of emerging and reviewing financial reporting rules;

assisting to insure that accounting standards are pursuant with the organisation; assisting

framework makers and auditors to address financial reporting problems under the absence of

accounting standard, and assisting to lower the volume of accounting standards by rendering an

overarching theory of accounting which could be applied to specific reporting issues.

The emergence of first conceptual framework was emerged in the late 1970s by the Financial

Accounting Standard Board (Barth and Landsman, 2010).

3. Stakeholder of Tesco plc and and its benefits from financial information:

Stakeholders: That group of an individual without whom a company cannot exist or operate its

activities are known as stakeholders. Individuals who has some kind of interest in an enterprise

are known as stakeholders. These are the one who affect the activities and business actions of an

organisation. Customers, employees, shareholders, suppliers, local community and national

government are the main stakeholders of an organisation.

It is very essential that all stakeholders of company should have information about the

funds of company as this help in run the business properly and contribute in making more

profits. Financial conditions of a company are one of the major concern for creditors and

investors. Capital provider and creditors of a company rely on financial conditions of a company

for safety. All investors need to know where their money went. Various financial statements such

as balance sheet give them detail information about investment of firm. As balance sheet is list of

2

all company's debts and it help equity investors to better understand the financial condition of

company. Further financial reports help investors to get information about sales, purchase, loss

and profits of company. Income statement help investors to evaluate company's past

performance. Cash flow statement help stakeholders to get information about exchange of cash

and it help investors to know whether company have enough cash to pay its expenses or not

(Costello, 2011).

Like the other financial reports statement of shareholders equity because it help them to

know about the changes take place in equity components and retain earning of a company at a

specific period of time. Overall various financial reports help stakeholders to know about the

financial positioning of a company and guide investors whether to provide financial help to

company or not. It reveal the information like whether firm has funds to pay its expenses or not.

With the help of financial report of TESCO its stakeholders can decide whether to invest in its

business activities or not.

4. Financial reporting for meeting firm objectives:

The financial reporting is helpful in meeting the organisational objectives. In the financial

report, this includes the balance sheet, profit and loss statement, cash flow statements etc. with

the help of this, company can analyse its financial performance and also compare its

performance level with the any other business rivals. From this, the business firm can compare to

make improvement in its current position. Now, this also has been seen that the financial

reporting does not only helps the firm to attain its financial objectives but also make business

sustainable and attract investors to invest in the organisation (Agoglia, Doupnik and Tsakumis,

2011). Financial reporting within the firm is made by complying various accounting standards

for making transparency within the firm. There are so many accounting regulatory bodies which

made certain rules and standards for completing firms financial reporting and assures

transparency as well.

International accounting standards and International financial reporting standards are the main

bodies which set out the standards for accounting, and every firm is required to adheres these set

out rules for making financial statements. The main objectives of financial reporting helps the

firm to render existing and potential investors and creditors with relevant informations which

could guide them in forming business decisions on investments, lending and other “ resource

allocation” matters. Financial reporting includes:

3

company. Further financial reports help investors to get information about sales, purchase, loss

and profits of company. Income statement help investors to evaluate company's past

performance. Cash flow statement help stakeholders to get information about exchange of cash

and it help investors to know whether company have enough cash to pay its expenses or not

(Costello, 2011).

Like the other financial reports statement of shareholders equity because it help them to

know about the changes take place in equity components and retain earning of a company at a

specific period of time. Overall various financial reports help stakeholders to know about the

financial positioning of a company and guide investors whether to provide financial help to

company or not. It reveal the information like whether firm has funds to pay its expenses or not.

With the help of financial report of TESCO its stakeholders can decide whether to invest in its

business activities or not.

4. Financial reporting for meeting firm objectives:

The financial reporting is helpful in meeting the organisational objectives. In the financial

report, this includes the balance sheet, profit and loss statement, cash flow statements etc. with

the help of this, company can analyse its financial performance and also compare its

performance level with the any other business rivals. From this, the business firm can compare to

make improvement in its current position. Now, this also has been seen that the financial

reporting does not only helps the firm to attain its financial objectives but also make business

sustainable and attract investors to invest in the organisation (Agoglia, Doupnik and Tsakumis,

2011). Financial reporting within the firm is made by complying various accounting standards

for making transparency within the firm. There are so many accounting regulatory bodies which

made certain rules and standards for completing firms financial reporting and assures

transparency as well.

International accounting standards and International financial reporting standards are the main

bodies which set out the standards for accounting, and every firm is required to adheres these set

out rules for making financial statements. The main objectives of financial reporting helps the

firm to render existing and potential investors and creditors with relevant informations which

could guide them in forming business decisions on investments, lending and other “ resource

allocation” matters. Financial reporting includes:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income statements: This is the main statement under which firm covers revenues and

expenditures. On the basis of such revenues and expenditures, income statement is prepared

(Council, 2010). The income statement also offers insights on how efficient firm managed by

telling observers these things as how much amount of profits and how long it takes to sell items

in stocks.

Cash flow statements: A main disadvantage of the income statement is that this only reports

only the earnings of the firm and spendings overall. Which does not reflects the cash position of

the firm (Nobes, 2014). Hence, this can be said that the cash flow statements is the main tool to

know about the cash earnings and expenses. As, cash is the major source for running the firm. If

cash does not exist then firm cannot survive. This statement helps the firm to know about the

amount which is left for the firm and used for the business operations.

Balance sheet: This is the most perfect tool which represents the financial positions about all its

assets and liabilities. On the assets side, this reflects to the outsiders and observers, how much

amount the firm has, inventory has, and how much amount this is anticipating to gather from its

customers and what physical property it has (Iatridis and Rouvolis, 2010). On the liability side,

this reflects the amount which the company owes- to suppliers, to lenders, to its own workers and

to others. Mostly, the balance sheet represents to an observer at a glance the answers to key

questions about firm's financial health: the amount of debt is carrying, whether this has money

available to pay forthcoming bills, how well this is handling this inventory and aggregations- and

whether this is in danger of becoming insolvent from liabilities which exceeds assets.

Owner's equity statements: Equity is the difference between firm's assets and its liabilities, so

they could think of it as part of firm's entire value which belongs to the investor. The equity

statement defines how much stake owners have in the firm (Epstein and Jermakowicz, 2010).5.

4

expenditures. On the basis of such revenues and expenditures, income statement is prepared

(Council, 2010). The income statement also offers insights on how efficient firm managed by

telling observers these things as how much amount of profits and how long it takes to sell items

in stocks.

Cash flow statements: A main disadvantage of the income statement is that this only reports

only the earnings of the firm and spendings overall. Which does not reflects the cash position of

the firm (Nobes, 2014). Hence, this can be said that the cash flow statements is the main tool to

know about the cash earnings and expenses. As, cash is the major source for running the firm. If

cash does not exist then firm cannot survive. This statement helps the firm to know about the

amount which is left for the firm and used for the business operations.

Balance sheet: This is the most perfect tool which represents the financial positions about all its

assets and liabilities. On the assets side, this reflects to the outsiders and observers, how much

amount the firm has, inventory has, and how much amount this is anticipating to gather from its

customers and what physical property it has (Iatridis and Rouvolis, 2010). On the liability side,

this reflects the amount which the company owes- to suppliers, to lenders, to its own workers and

to others. Mostly, the balance sheet represents to an observer at a glance the answers to key

questions about firm's financial health: the amount of debt is carrying, whether this has money

available to pay forthcoming bills, how well this is handling this inventory and aggregations- and

whether this is in danger of becoming insolvent from liabilities which exceeds assets.

Owner's equity statements: Equity is the difference between firm's assets and its liabilities, so

they could think of it as part of firm's entire value which belongs to the investor. The equity

statement defines how much stake owners have in the firm (Epstein and Jermakowicz, 2010).5.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

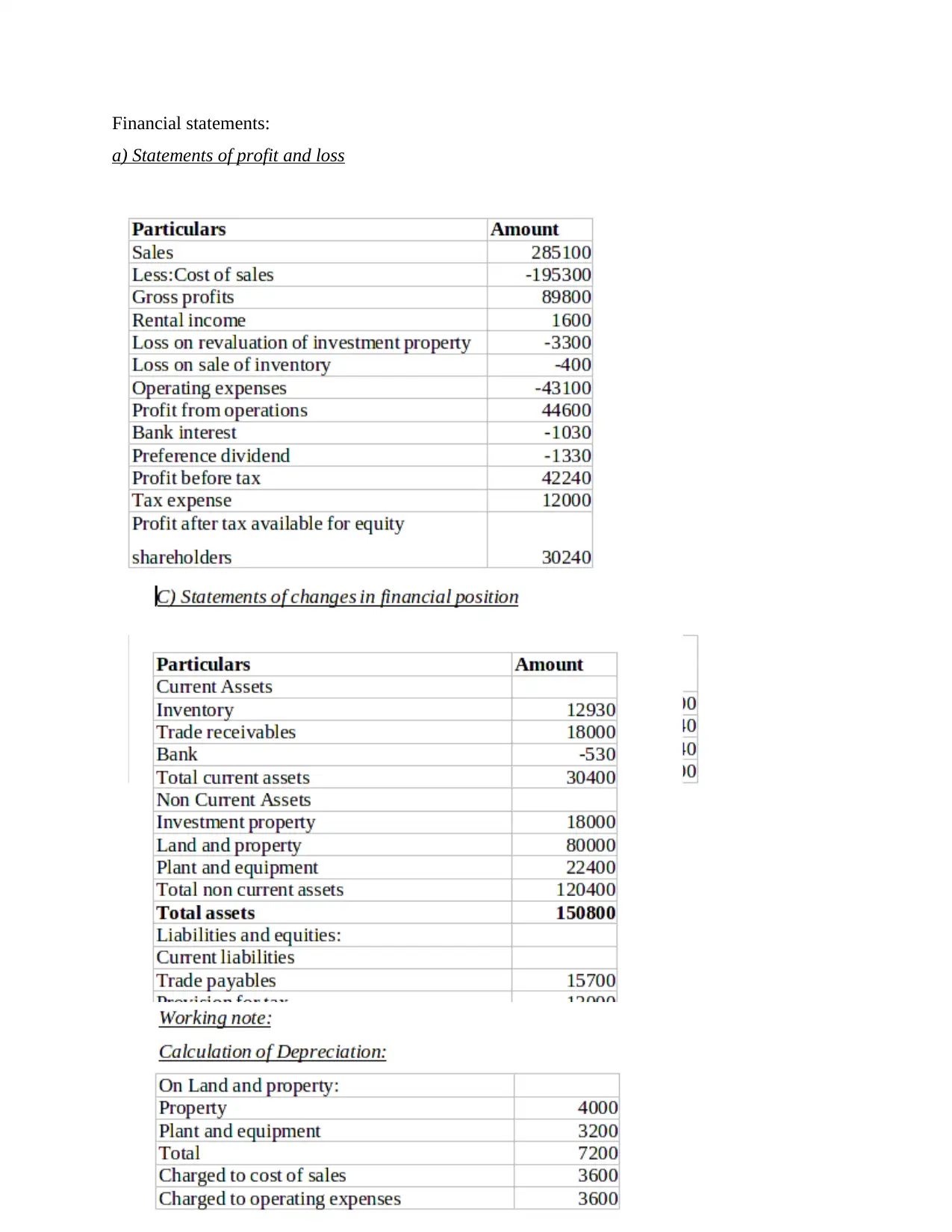

Financial statements:

a) Statements of profit and loss

5

a) Statements of profit and loss

5

Cash flows are the transactions which are carried out in business and in which cash is

involved. Almost all the transactions involve cash and in statement of cash flows they are to be

represented by bifurcating them in three categories. They are operating, investing and financing

activities. From the profit and loss account the amounts which are to be shown in this includes

sales, bank interest, income from rent and dividend (Ball, Jayaraman and Shivakumar, 2012). All

the amount which is received from sales and paid for the purchase of inventory is to be

incorporated. All of the expenses which are paid and other incomes which are earned in cash are

presented. From statement of balance sheet there is no amount which is to be shown in current

case otherwise the change which take place in equity that means the amount received on issue of

shares or redemption of shares is to be included. In this opening amount is to be reconciled with

the closing amount of cash that is presents so that it can be known that there is no fraud that has

been carried out in respect of it. Also it is determined that all the funds have been utilised in the

best manner possible for the overall benefit of organisation.

6. Financial statement of Tesco plc and interpretation of financial performance:

6

involved. Almost all the transactions involve cash and in statement of cash flows they are to be

represented by bifurcating them in three categories. They are operating, investing and financing

activities. From the profit and loss account the amounts which are to be shown in this includes

sales, bank interest, income from rent and dividend (Ball, Jayaraman and Shivakumar, 2012). All

the amount which is received from sales and paid for the purchase of inventory is to be

incorporated. All of the expenses which are paid and other incomes which are earned in cash are

presented. From statement of balance sheet there is no amount which is to be shown in current

case otherwise the change which take place in equity that means the amount received on issue of

shares or redemption of shares is to be included. In this opening amount is to be reconciled with

the closing amount of cash that is presents so that it can be known that there is no fraud that has

been carried out in respect of it. Also it is determined that all the funds have been utilised in the

best manner possible for the overall benefit of organisation.

6. Financial statement of Tesco plc and interpretation of financial performance:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

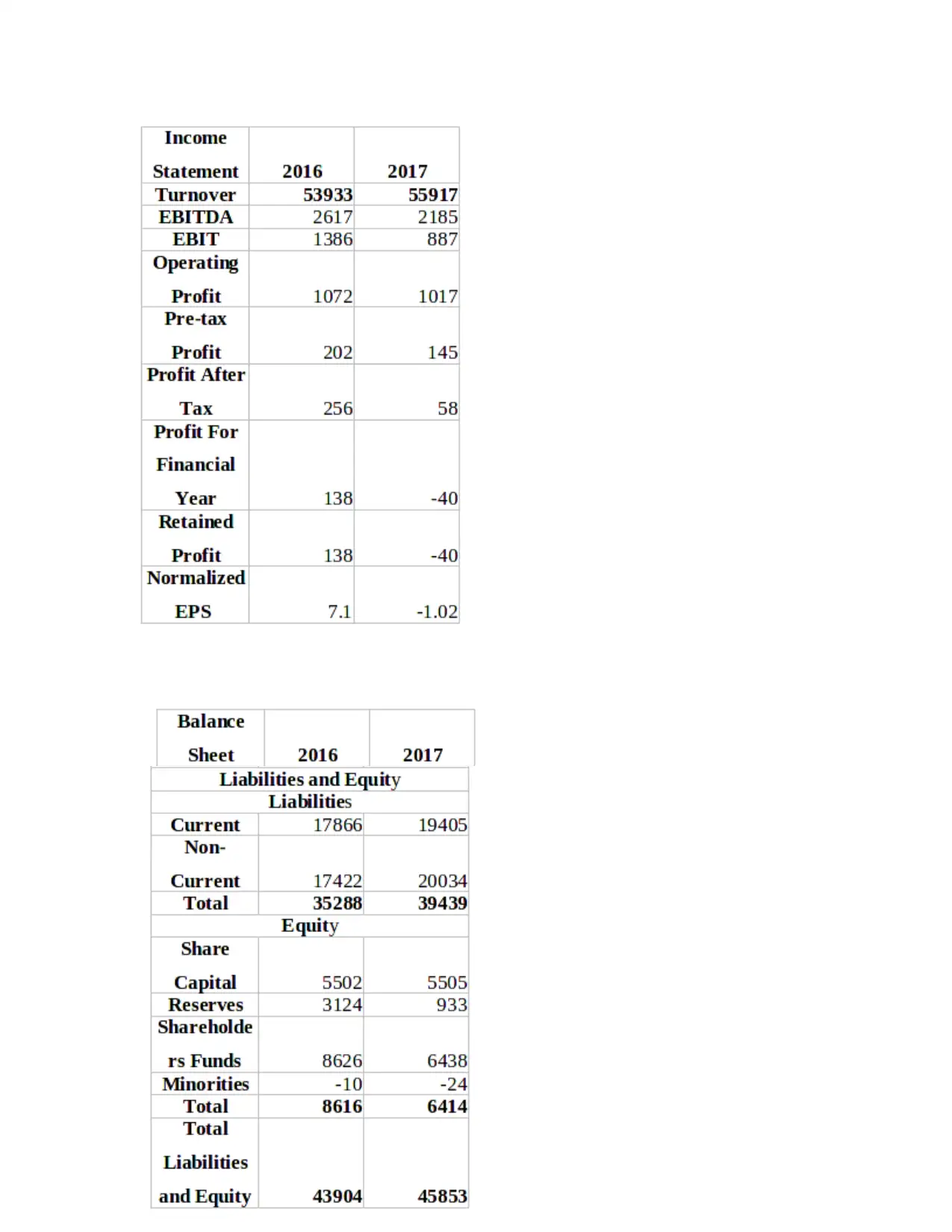

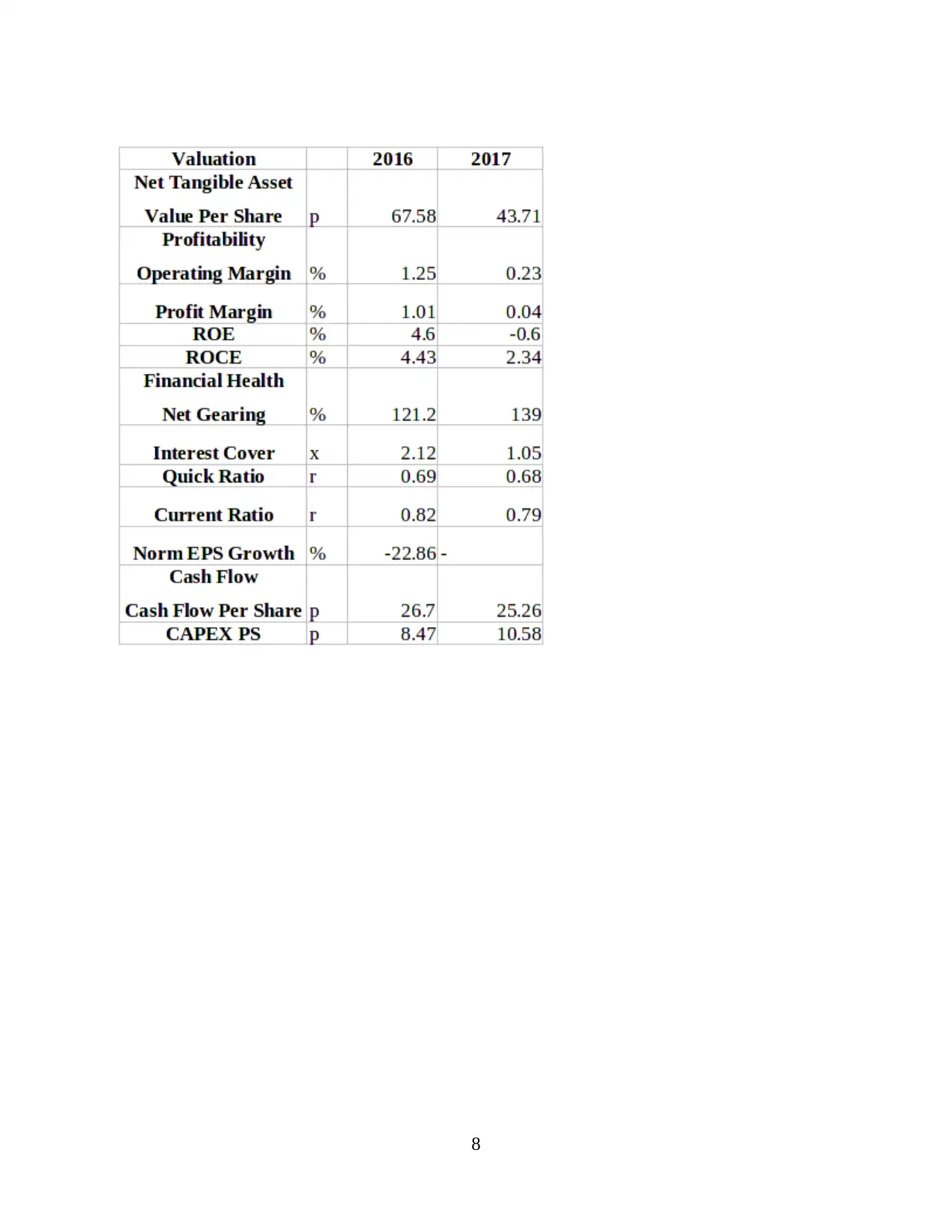

From the above mentioned financial statements, if we talk about the profitability, then we

will find that the company profit margin was 1.01 in 2016 which was reduced to 0.04 in 2017.

this shows that firm operating profit margin is reducing as compare to the last year. Return on

equity of the firm in 2016 was 4.6 which also reduced to -0.6 in 2017. return on capital employed

of the firm does also reflects the negative figure in 2017 as compare to the previous year figure.

Hence, in terms of profitability, firm performance is getting down as compare to the 2016

financial positions.

However, the firm's quick ratio is almost same to the last year ratio, and current ratio slightly

change.

So, this is observed that the company needs to make their business positions effective by using

firm's resources effectively so that the operations could have framed great.

7. Difference between IFRS and IAS

IAS are set of standards which International accounting standards committee issue and

are required to be complied by all the companies. They were developed so that financial

statements can be understood in better manner and also the chances of misrepresentation is

reduced with the help of them. In them, the manner in which any particular transaction shall be

recorded in statements is specified (Iatridis, 2010). Then, IASC was taken over by IASB in 2001

and decided that the standards which are there currently will be adopted but after some

modifications being made to them. They were revised to bring them at international level and

named them as international financial reporting standards. By this change was made to all the

businesses and markets. Although IFRS is revised form of IAS but there are some differences

which exist among them. The main difference is the time period, according to which all

standards which were issued till 2011 are known as IAS and the ones that were made after this

period are considered as IFRS. IASC is authorise for the purpose of issuance of IAS and in

respect of IFRS the authority which is responsible for making of them is IASB. The rules which

are made in IFRS in respect of measurement, identification, disclosure and presentation of

various assets that are held is different from what has been mentioned in IAS. The total standards

which are made in IFRS are 9 whereas there were total 39 IAS that has been issued.

Another difference which can be noted is the meaning of bold text which is represented

under both cases. In IFRS It refers to guiding principles of that standards and they are

compulsory elements In case of IAS which are required to be followed by all without any

9

will find that the company profit margin was 1.01 in 2016 which was reduced to 0.04 in 2017.

this shows that firm operating profit margin is reducing as compare to the last year. Return on

equity of the firm in 2016 was 4.6 which also reduced to -0.6 in 2017. return on capital employed

of the firm does also reflects the negative figure in 2017 as compare to the previous year figure.

Hence, in terms of profitability, firm performance is getting down as compare to the 2016

financial positions.

However, the firm's quick ratio is almost same to the last year ratio, and current ratio slightly

change.

So, this is observed that the company needs to make their business positions effective by using

firm's resources effectively so that the operations could have framed great.

7. Difference between IFRS and IAS

IAS are set of standards which International accounting standards committee issue and

are required to be complied by all the companies. They were developed so that financial

statements can be understood in better manner and also the chances of misrepresentation is

reduced with the help of them. In them, the manner in which any particular transaction shall be

recorded in statements is specified (Iatridis, 2010). Then, IASC was taken over by IASB in 2001

and decided that the standards which are there currently will be adopted but after some

modifications being made to them. They were revised to bring them at international level and

named them as international financial reporting standards. By this change was made to all the

businesses and markets. Although IFRS is revised form of IAS but there are some differences

which exist among them. The main difference is the time period, according to which all

standards which were issued till 2011 are known as IAS and the ones that were made after this

period are considered as IFRS. IASC is authorise for the purpose of issuance of IAS and in

respect of IFRS the authority which is responsible for making of them is IASB. The rules which

are made in IFRS in respect of measurement, identification, disclosure and presentation of

various assets that are held is different from what has been mentioned in IAS. The total standards

which are made in IFRS are 9 whereas there were total 39 IAS that has been issued.

Another difference which can be noted is the meaning of bold text which is represented

under both cases. In IFRS It refers to guiding principles of that standards and they are

compulsory elements In case of IAS which are required to be followed by all without any

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.