Comprehensive Analysis of Recording Business Transactions

VerifiedAdded on 2023/01/03

|15

|2647

|97

Homework Assignment

AI Summary

This assignment solution provides a comprehensive overview of recording business transactions. It begins with an introduction to accounting and decision-makers' needs, followed by a discussion of the advantages and disadvantages of accounting within a business unit. The solution includes detailed journal entries for David, general ledgers for Pearce & Sons, a trial balance, and the drafting of an income statement for the Airman company. Furthermore, the assignment addresses the impact of the COVID-19 pandemic on the income statement, highlighting the importance of financial sustainability and the challenges faced by businesses during the crisis. The solution offers insights into how to assess the financial effects of the pandemic, specifically relating to revenues, expenses, and the adjustments required for accurate financial reporting.

RECORDING BUSINESS TRANSACTION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART 1.........................................................................................................................................................3

PART 2.........................................................................................................................................................6

PART 3.........................................................................................................................................................8

PART 4.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION...........................................................................................................................................3

PART 1.........................................................................................................................................................3

PART 2.........................................................................................................................................................6

PART 3.........................................................................................................................................................8

PART 4.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION

Accounting refers to a set or collection of activities concerning the monitoring, measurement,

review and description of an individual's personal financial performance data inside the company

segment, which is only carried out with accounting assistance (Hoyle, 2015). Virtually,

accounting is simply a formal corporate language and associated operations. This helps the

organization to turn ongoing events into delivered effectively that can be classified as per their

respective usage and significance. These declarations and reports shall be made in such a way as

to aid in the assessment, along with the corporate status, of the financial performance. The

research includes numerous topics pertaining to revenue and expenditure transaction logging.

The study addresses financial decision to what degree they need accounting knowledge,

accounting advantages and drawbacks, as well as realistic activities to document company

transactions and file financial reports.

PART 1

Recognize who are decision-makers and describe their requirement/needs with regard to

accounting-information.

The decision-makers are a human, normally in the leadership, who makes difficult decisions that

strongly influence the company, operates. Employee workers who are great decision learn how

to fix problems easily and use logical thinking capabilities to resolve problems faster (Loughran

and McDonald, 2016). They can quickly weigh the multiple options and decide on the outcome

that best suits the organization and its employees.

The collection, analysis and description of all financial information in the manner they may be

included in reporting are used in financial management. These types of reports, which contain

financial information, are useful for the production of a satisfactory financial and fiscal strategy

and policy. In the near future, this company is able to deal with their success. While also being

able to give end users great customer deals. All of the activities starting from recruitment to

firing include the estimation of the sales target, the resource planning of promotional events, and

also the choosing of different techniques and software to execute various tasks and functions.

And senior leaders and general administrators make both of these choices.

Accounting refers to a set or collection of activities concerning the monitoring, measurement,

review and description of an individual's personal financial performance data inside the company

segment, which is only carried out with accounting assistance (Hoyle, 2015). Virtually,

accounting is simply a formal corporate language and associated operations. This helps the

organization to turn ongoing events into delivered effectively that can be classified as per their

respective usage and significance. These declarations and reports shall be made in such a way as

to aid in the assessment, along with the corporate status, of the financial performance. The

research includes numerous topics pertaining to revenue and expenditure transaction logging.

The study addresses financial decision to what degree they need accounting knowledge,

accounting advantages and drawbacks, as well as realistic activities to document company

transactions and file financial reports.

PART 1

Recognize who are decision-makers and describe their requirement/needs with regard to

accounting-information.

The decision-makers are a human, normally in the leadership, who makes difficult decisions that

strongly influence the company, operates. Employee workers who are great decision learn how

to fix problems easily and use logical thinking capabilities to resolve problems faster (Loughran

and McDonald, 2016). They can quickly weigh the multiple options and decide on the outcome

that best suits the organization and its employees.

The collection, analysis and description of all financial information in the manner they may be

included in reporting are used in financial management. These types of reports, which contain

financial information, are useful for the production of a satisfactory financial and fiscal strategy

and policy. In the near future, this company is able to deal with their success. While also being

able to give end users great customer deals. All of the activities starting from recruitment to

firing include the estimation of the sales target, the resource planning of promotional events, and

also the choosing of different techniques and software to execute various tasks and functions.

And senior leaders and general administrators make both of these choices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Decision makers are primarily senior management staff within the company, such as Tesco, and

has an executive board focused on international UK retailers, which are the company's main

judgment (Vasarhelyi, Kogan and Tuttle, 2015). The Organization of Boards of Directors with

diverse viewpoints, perspectives and opinions benefits the members of the Group by better

organizational success. The Board consists of the Chairman, the Senior Internal Auditor, and the

Chief Operating Officer of the Company, the Financial Officer, and a set of individual semi

officers. The board of Tesco is composed of:

Jhon Allan Non-executive Chairman

Ken Murphy Group Chief Executive

Alan Stewart CFO

Stewart Gilliland Independent Non-executive Director.

Byron Grote Independent Non-executive Director.

Alison Platt Independent Non-executive Director.

Mikael Olsson Independent Non-executive Director.

Steve Golsby Independent Non-executive Director.

Simon Patterson Independent Non-executive Director.

They need accounting framework for strategic, tracking and making decisions on the cost of

sales, profitability and liquidity of the company. Decision-makers are interested in assessing the

group's ability to raise profits in the future. It is responsible for assessing the institution's

liquidity and meeting its financial responsibilities on time (Wild, Shaw and Chiappetta, 2015).

By various quantities, such as debt-equity percentage, liquidity ratios, etc. They want accounting

statistics to consider the company's short-term or longer-term financial health. Similarly, with the

help of statement of cash flows, the requirement for narrower and lengthier funds may be

established. Financial accounts/statements represent all company-related accounting activities in

a nutshell that enables the management committee to use this information in the execution of

plans in a viable and easy manner, including corporate managers. The financial reports are

worked out on the basis of general principles and practices that are similar across the industry.

This encourages them to differentiate it from other entrants in order to put themselves across

customer's purchase. It lays out a management/BOD structure for taking capital budgeting

has an executive board focused on international UK retailers, which are the company's main

judgment (Vasarhelyi, Kogan and Tuttle, 2015). The Organization of Boards of Directors with

diverse viewpoints, perspectives and opinions benefits the members of the Group by better

organizational success. The Board consists of the Chairman, the Senior Internal Auditor, and the

Chief Operating Officer of the Company, the Financial Officer, and a set of individual semi

officers. The board of Tesco is composed of:

Jhon Allan Non-executive Chairman

Ken Murphy Group Chief Executive

Alan Stewart CFO

Stewart Gilliland Independent Non-executive Director.

Byron Grote Independent Non-executive Director.

Alison Platt Independent Non-executive Director.

Mikael Olsson Independent Non-executive Director.

Steve Golsby Independent Non-executive Director.

Simon Patterson Independent Non-executive Director.

They need accounting framework for strategic, tracking and making decisions on the cost of

sales, profitability and liquidity of the company. Decision-makers are interested in assessing the

group's ability to raise profits in the future. It is responsible for assessing the institution's

liquidity and meeting its financial responsibilities on time (Wild, Shaw and Chiappetta, 2015).

By various quantities, such as debt-equity percentage, liquidity ratios, etc. They want accounting

statistics to consider the company's short-term or longer-term financial health. Similarly, with the

help of statement of cash flows, the requirement for narrower and lengthier funds may be

established. Financial accounts/statements represent all company-related accounting activities in

a nutshell that enables the management committee to use this information in the execution of

plans in a viable and easy manner, including corporate managers. The financial reports are

worked out on the basis of general principles and practices that are similar across the industry.

This encourages them to differentiate it from other entrants in order to put themselves across

customer's purchase. It lays out a management/BOD structure for taking capital budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decisions, and whether those decisions are desirable and economically feasible for the company

to take. In addition, estimates and forecasts are also focused on the organization's financial

details and on adjustments according to market conditions. That's also important not only for

comparative study, but also for the context in which useful information is collected by non-

financial data.

Merits and demerits of accounting within a business unit:

Advantages:

Comparison of performance

It makes it easier to compare one period started financial reporting with others. In accordance

with the business requirements, administrators may also review the formal reporting of both

financial and accounting activities (Brewer, Garrison and Noreen, 2015).

Decision- Making

Decisions are taken simpler for executives when financial transfers are thoroughly accounted for.

Financial reports allow managers of different companies to prepare their future activities,

organize operations. This includes information on revenue outflows and inflows as well as

revenues and expenses that make it possible to estimate the shortfall or surplus inside the

resources that should be administered in a reasonable time. This also helps to provide clarity and

supervision for fraud analysis and tracking.

Disadvantage:

Describes, in monetary sense, accounting information

Non-fiscal expenditures are unable to have an effect on financial accounts. Accountants can be

judged only for activities of a financial sort (Warren, Moffitt and Byrnes, 2015). Financial

occurrences are evidently interpreted in financial terms. As a result, during the execution of

legislation and the making of determining the reasons, it offers an incomplete picture. In the

context of a towing company, the shareholders cannot make choices on other factors, such as

fiscal, social and other factors, on the basis of accounting books.

to take. In addition, estimates and forecasts are also focused on the organization's financial

details and on adjustments according to market conditions. That's also important not only for

comparative study, but also for the context in which useful information is collected by non-

financial data.

Merits and demerits of accounting within a business unit:

Advantages:

Comparison of performance

It makes it easier to compare one period started financial reporting with others. In accordance

with the business requirements, administrators may also review the formal reporting of both

financial and accounting activities (Brewer, Garrison and Noreen, 2015).

Decision- Making

Decisions are taken simpler for executives when financial transfers are thoroughly accounted for.

Financial reports allow managers of different companies to prepare their future activities,

organize operations. This includes information on revenue outflows and inflows as well as

revenues and expenses that make it possible to estimate the shortfall or surplus inside the

resources that should be administered in a reasonable time. This also helps to provide clarity and

supervision for fraud analysis and tracking.

Disadvantage:

Describes, in monetary sense, accounting information

Non-fiscal expenditures are unable to have an effect on financial accounts. Accountants can be

judged only for activities of a financial sort (Warren, Moffitt and Byrnes, 2015). Financial

occurrences are evidently interpreted in financial terms. As a result, during the execution of

legislation and the making of determining the reasons, it offers an incomplete picture. In the

context of a towing company, the shareholders cannot make choices on other factors, such as

fiscal, social and other factors, on the basis of accounting books.

Accounting statistics may be prone to prejudice.

Financial professionals have a personal effect on the accounting reports of the company. In order

to measure the company's income, the finance manager can use different inventory valuation

metrics, values of different, income identification and capital expenditure, etc.

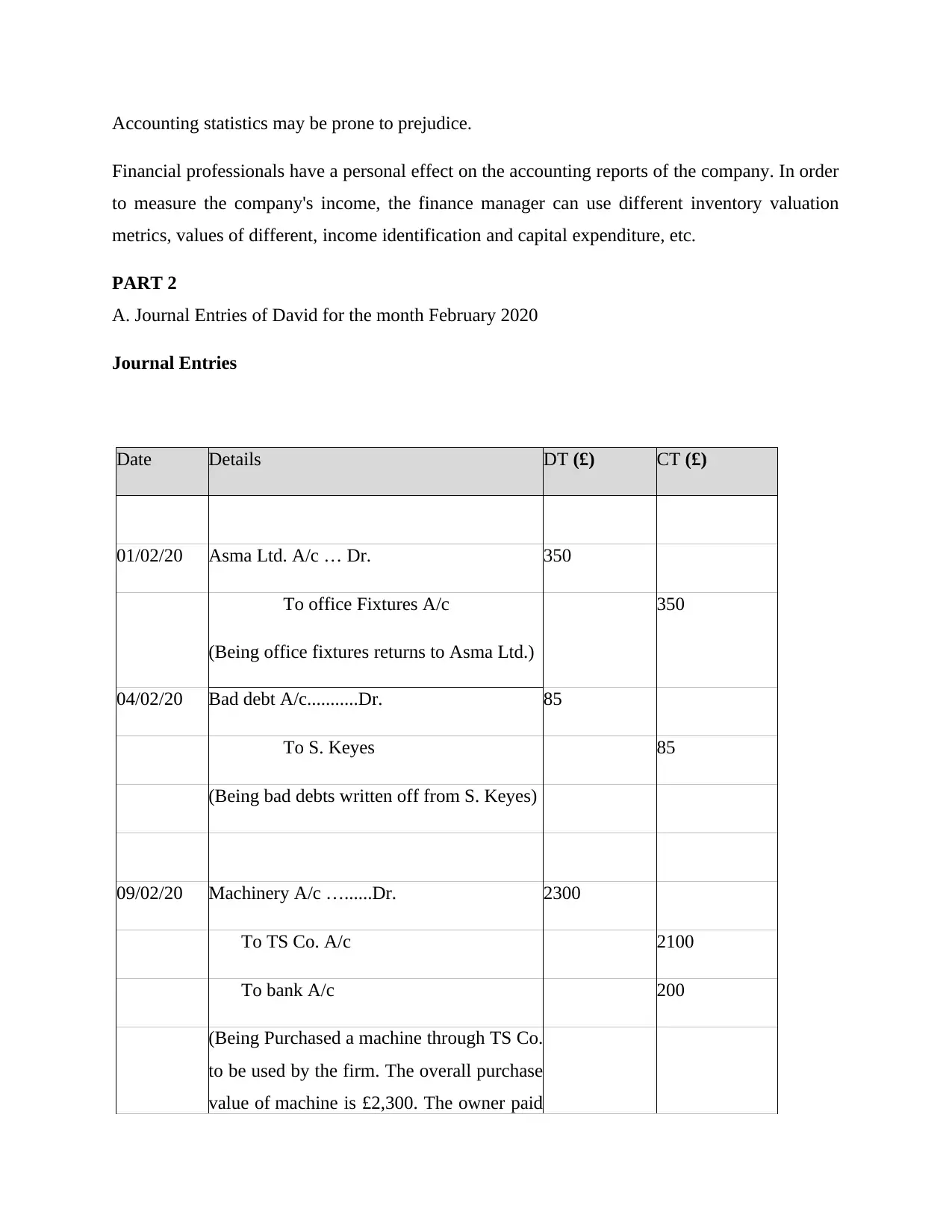

PART 2

A. Journal Entries of David for the month February 2020

Journal Entries

Date Details DT (£) CT (£)

01/02/20 Asma Ltd. A/c … Dr. 350

To office Fixtures A/c

(Being office fixtures returns to Asma Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S. Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS Co.

to be used by the firm. The overall purchase

value of machine is £2,300. The owner paid

Financial professionals have a personal effect on the accounting reports of the company. In order

to measure the company's income, the finance manager can use different inventory valuation

metrics, values of different, income identification and capital expenditure, etc.

PART 2

A. Journal Entries of David for the month February 2020

Journal Entries

Date Details DT (£) CT (£)

01/02/20 Asma Ltd. A/c … Dr. 350

To office Fixtures A/c

(Being office fixtures returns to Asma Ltd.)

350

04/02/20 Bad debt A/c...........Dr. 85

To S. Keyes 85

(Being bad debts written off from S. Keyes)

09/02/20 Machinery A/c …......Dr. 2300

To TS Co. A/c 2100

To bank A/c 200

(Being Purchased a machine through TS Co.

to be used by the firm. The overall purchase

value of machine is £2,300. The owner paid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

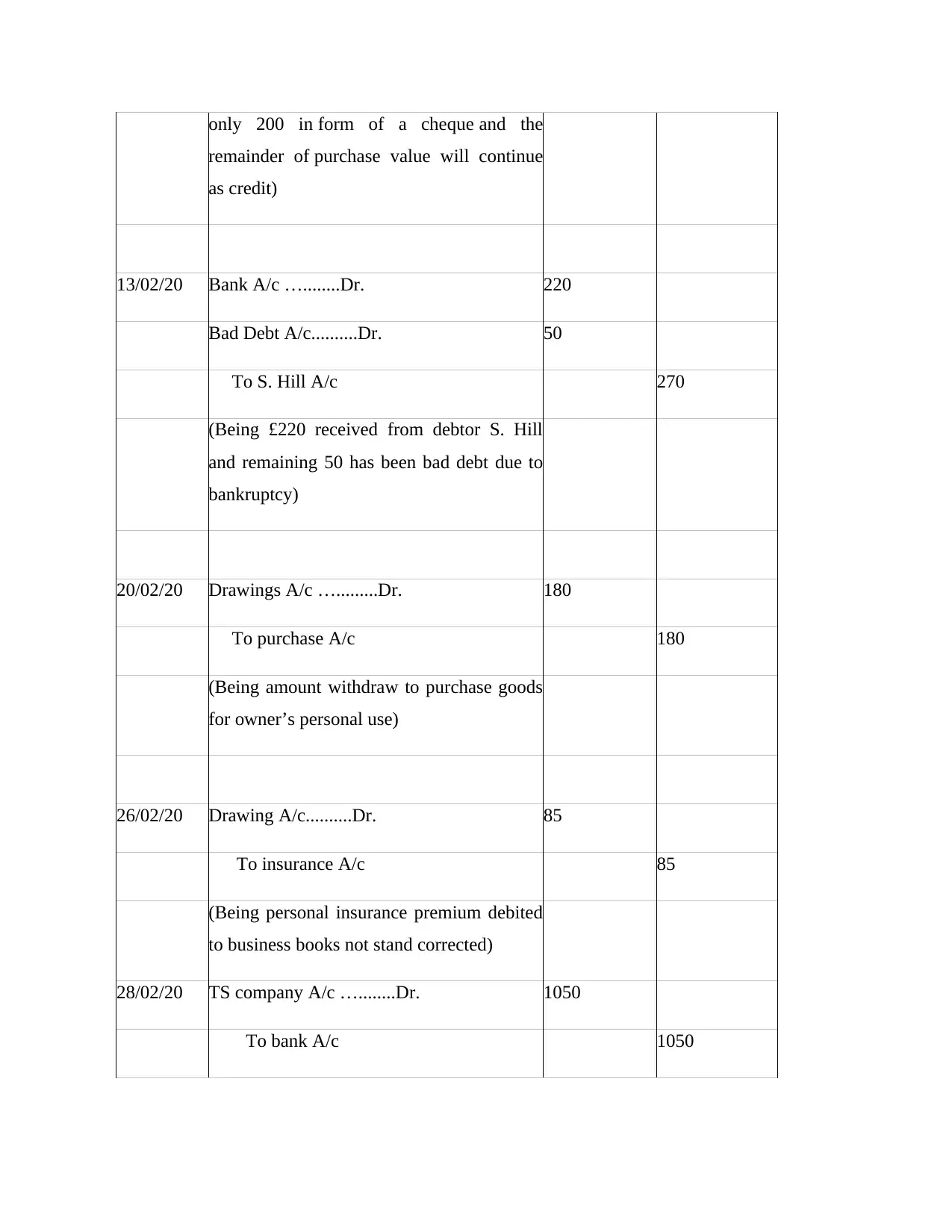

only 200 in form of a cheque and the

remainder of purchase value will continue

as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due to

bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase goods

for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium debited

to business books not stand corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

remainder of purchase value will continue

as credit)

13/02/20 Bank A/c …........Dr. 220

Bad Debt A/c..........Dr. 50

To S. Hill A/c 270

(Being £220 received from debtor S. Hill

and remaining 50 has been bad debt due to

bankruptcy)

20/02/20 Drawings A/c ….........Dr. 180

To purchase A/c 180

(Being amount withdraw to purchase goods

for owner’s personal use)

26/02/20 Drawing A/c..........Dr. 85

To insurance A/c 85

(Being personal insurance premium debited

to business books not stand corrected)

28/02/20 TS company A/c …........Dr. 1050

To bank A/c 1050

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Being half payment of machinery paid by

owner to TS company)

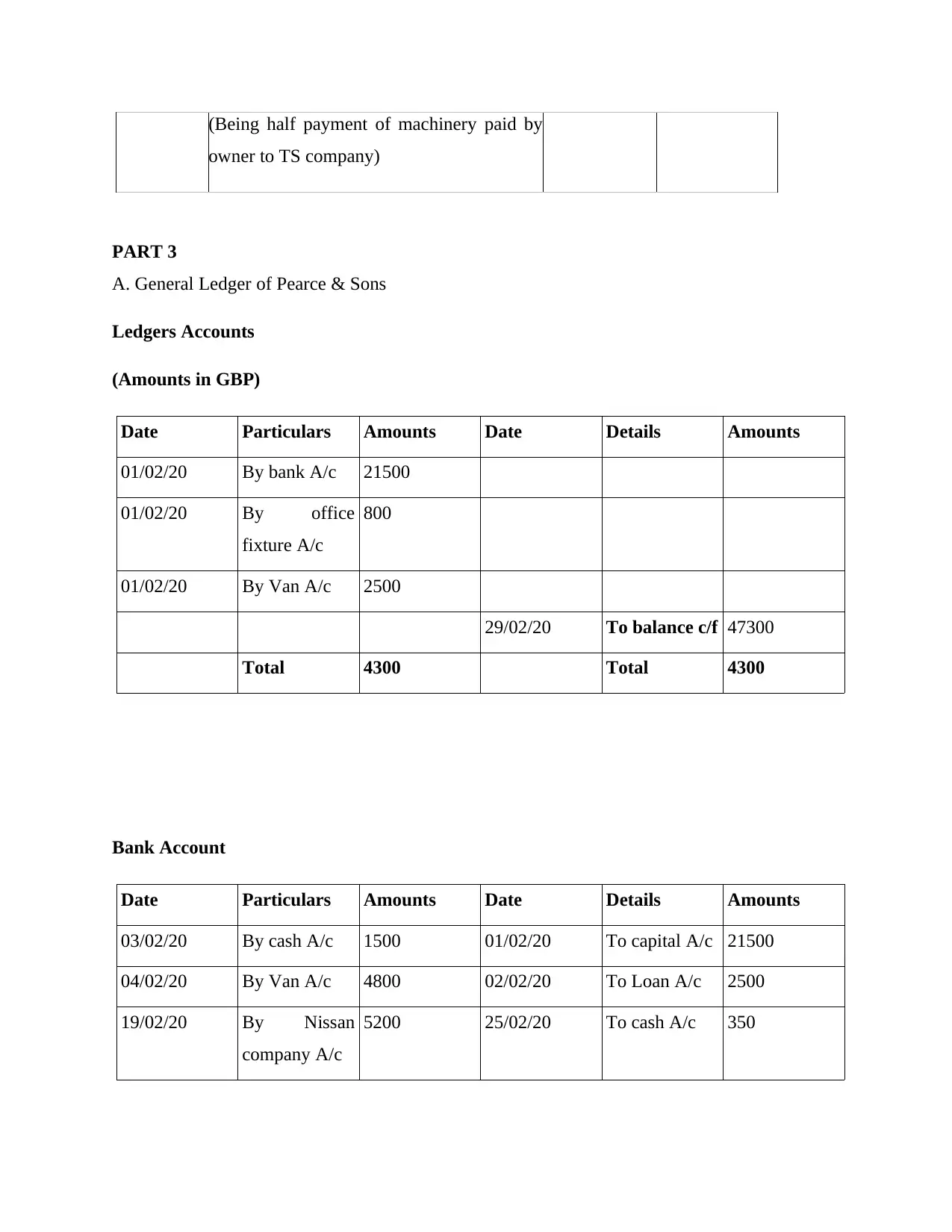

PART 3

A. General Ledger of Pearce & Sons

Ledgers Accounts

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

owner to TS company)

PART 3

A. General Ledger of Pearce & Sons

Ledgers Accounts

(Amounts in GBP)

Date Particulars Amounts Date Details Amounts

01/02/20 By bank A/c 21500

01/02/20 By office

fixture A/c

800

01/02/20 By Van A/c 2500

29/02/20 To balance c/f 47300

Total 4300 Total 4300

Bank Account

Date Particulars Amounts Date Details Amounts

03/02/20 By cash A/c 1500 01/02/20 To capital A/c 21500

04/02/20 By Van A/c 4800 02/02/20 To Loan A/c 2500

19/02/20 By Nissan

company A/c

5200 25/02/20 To cash A/c 350

28/02/20 By balance c/f 12230

Total 24350 Total 24350

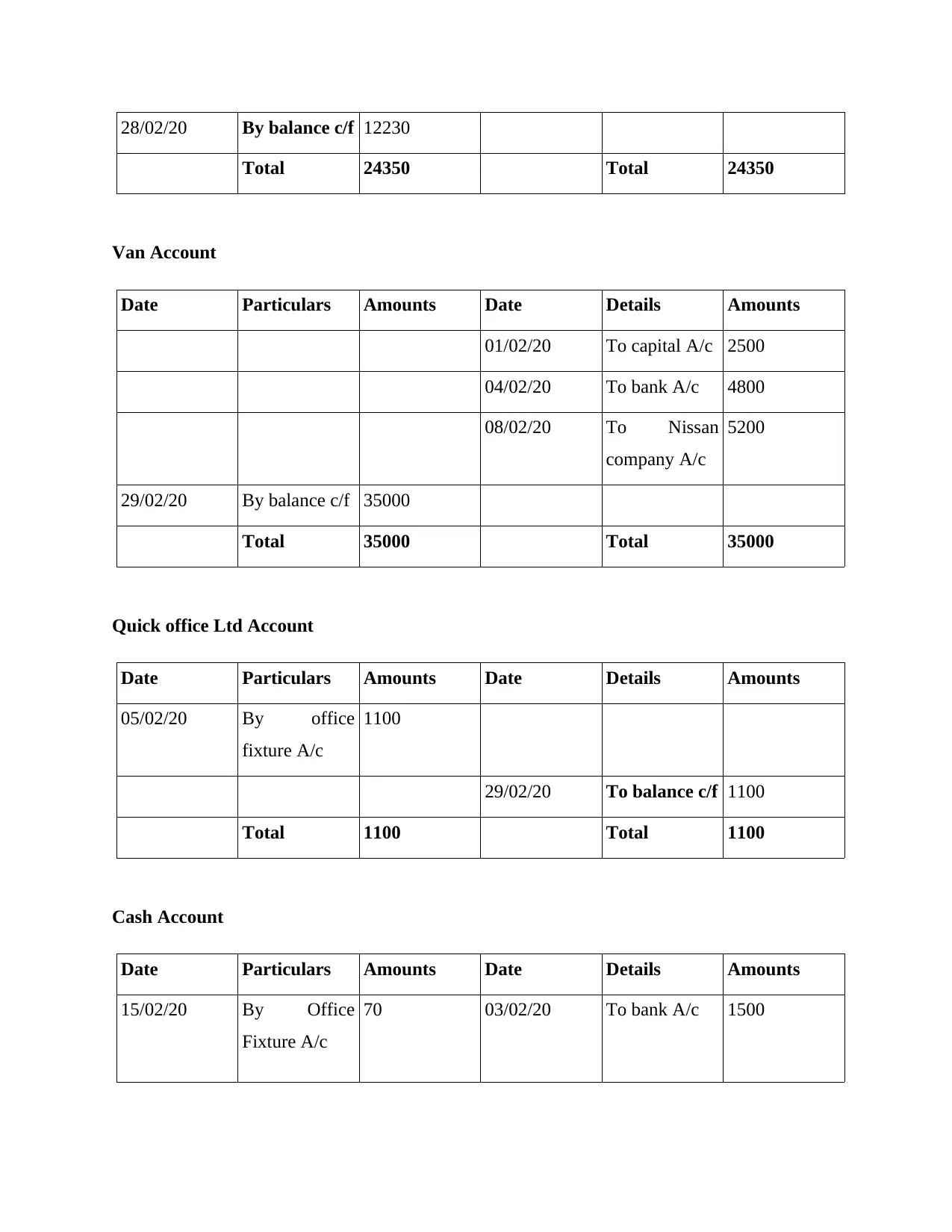

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

04/02/20 To bank A/c 4800

08/02/20 To Nissan

company A/c

5200

29/02/20 By balance c/f 35000

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

Total 24350 Total 24350

Van Account

Date Particulars Amounts Date Details Amounts

01/02/20 To capital A/c 2500

04/02/20 To bank A/c 4800

08/02/20 To Nissan

company A/c

5200

29/02/20 By balance c/f 35000

Total 35000 Total 35000

Quick office Ltd Account

Date Particulars Amounts Date Details Amounts

05/02/20 By office

fixture A/c

1100

29/02/20 To balance c/f 1100

Total 1100 Total 1100

Cash Account

Date Particulars Amounts Date Details Amounts

15/02/20 By Office

Fixture A/c

70 03/02/20 To bank A/c 1500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

25/02/20 By bank A/c 350

29/02/20 By balance c/f 1080

Total 1500 Total 1500

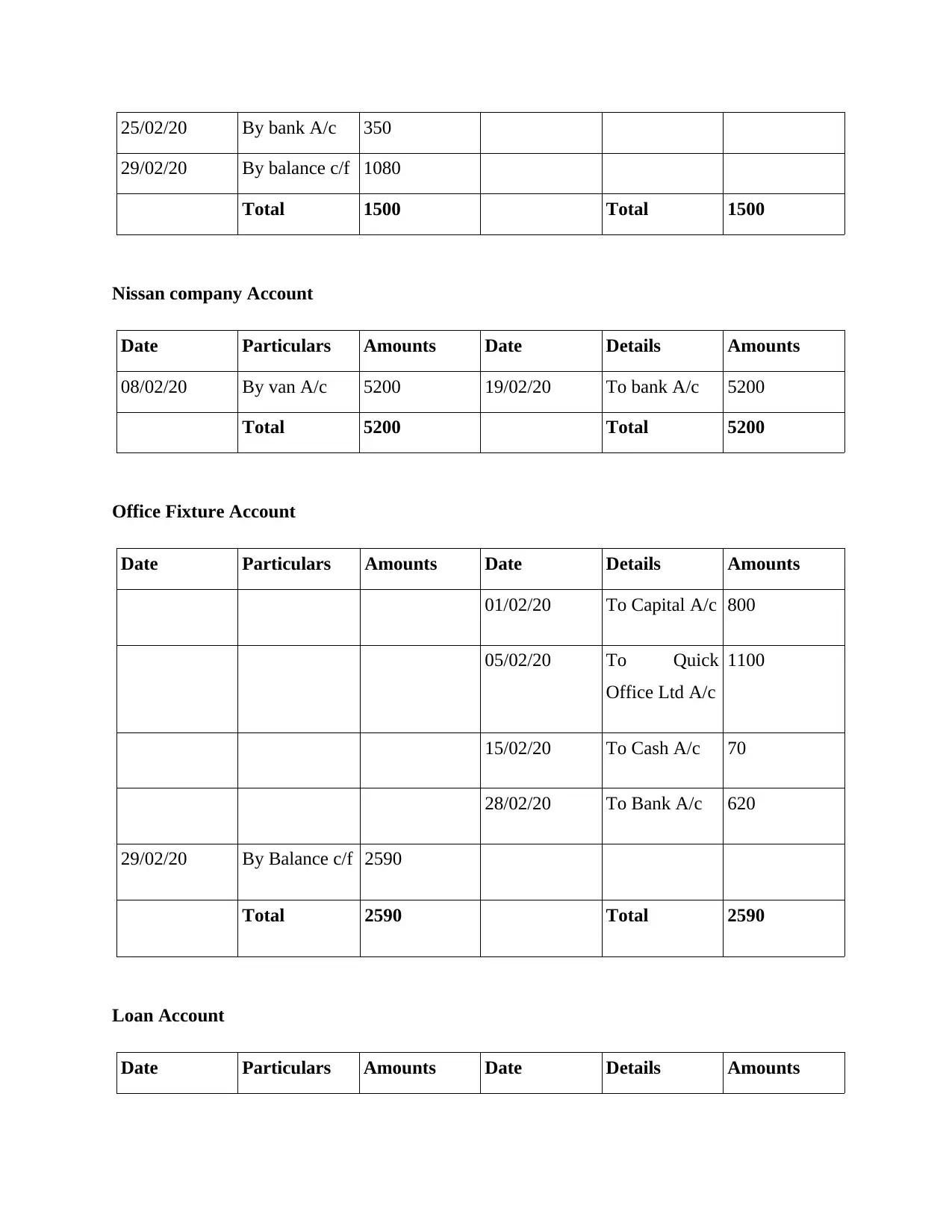

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amounts Date Details Amounts

01/02/20 To Capital A/c 800

05/02/20 To Quick

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

29/02/20 By balance c/f 1080

Total 1500 Total 1500

Nissan company Account

Date Particulars Amounts Date Details Amounts

08/02/20 By van A/c 5200 19/02/20 To bank A/c 5200

Total 5200 Total 5200

Office Fixture Account

Date Particulars Amounts Date Details Amounts

01/02/20 To Capital A/c 800

05/02/20 To Quick

Office Ltd A/c

1100

15/02/20 To Cash A/c 70

28/02/20 To Bank A/c 620

29/02/20 By Balance c/f 2590

Total 2590 Total 2590

Loan Account

Date Particulars Amounts Date Details Amounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

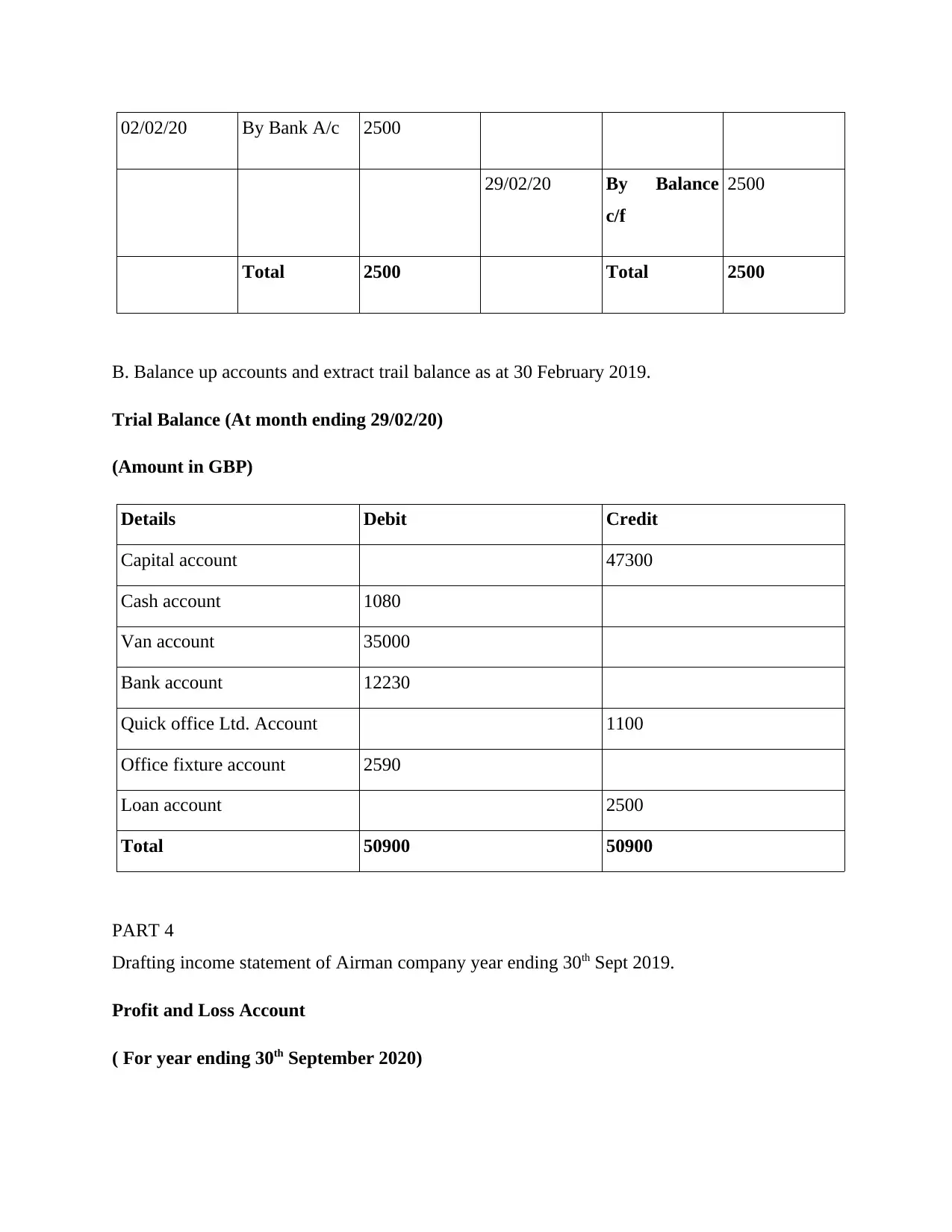

02/02/20 By Bank A/c 2500

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

Loan account 2500

Total 50900 50900

PART 4

Drafting income statement of Airman company year ending 30th Sept 2019.

Profit and Loss Account

( For year ending 30th September 2020)

29/02/20 By Balance

c/f

2500

Total 2500 Total 2500

B. Balance up accounts and extract trail balance as at 30 February 2019.

Trial Balance (At month ending 29/02/20)

(Amount in GBP)

Details Debit Credit

Capital account 47300

Cash account 1080

Van account 35000

Bank account 12230

Quick office Ltd. Account 1100

Office fixture account 2590

Loan account 2500

Total 50900 50900

PART 4

Drafting income statement of Airman company year ending 30th Sept 2019.

Profit and Loss Account

( For year ending 30th September 2020)

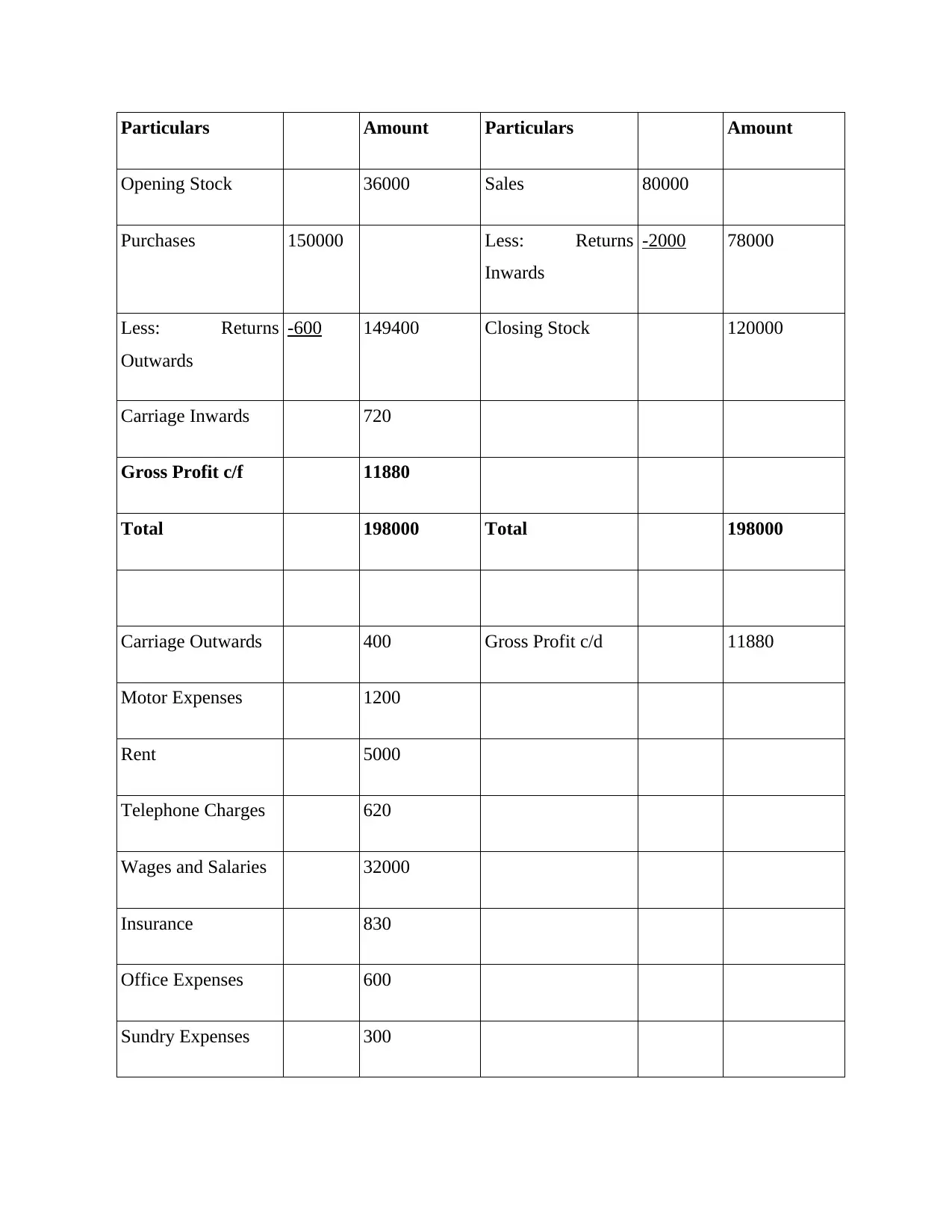

Particulars Amount Particulars Amount

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

Opening Stock 36000 Sales 80000

Purchases 150000 Less: Returns

Inwards

-2000 78000

Less: Returns

Outwards

-600 149400 Closing Stock 120000

Carriage Inwards 720

Gross Profit c/f 11880

Total 198000 Total 198000

Carriage Outwards 400 Gross Profit c/d 11880

Motor Expenses 1200

Rent 5000

Telephone Charges 620

Wages and Salaries 32000

Insurance 830

Office Expenses 600

Sundry Expenses 300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.