Management Accounting: Systems, Reports, and Performance Analysis

VerifiedAdded on 2022/12/26

|19

|4540

|48

Report

AI Summary

This report on management accounting provides a comprehensive overview of various systems, methods, and their applications within an organizational context, specifically referencing The London College. It explores the role of management accounting in decision-making, planning, and controlling business strategies, including the use of tools like variance analysis and break-even analysis. The report details different reporting methods, such as inventory management and job costing, and their benefits in terms of relevance, updated information, reliability, understandability, and accuracy. It includes calculations for cost cards using both absorption and marginal costing, along with income statements under both costing methods. The report also covers financial report analysis, including estimating expenses, inventory valuation, and break-even point calculations, demonstrating how these techniques can be applied to improve organizational performance and achieve sustainable success. Finally, the report touches on cash flow management and collection schedules.

MANAGEMENT

ACCOUNTING

1

ACCOUNTING

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Section one...................................................................................................................................3

1.1. ...............................................................................................................................................3

1.2.................................................................................................................................................4

1.3 ................................................................................................................................................4

1.4.................................................................................................................................................5

2.1. ...............................................................................................................................................5

2.2. ...............................................................................................................................................8

2.3 ................................................................................................................................................8

2.4.................................................................................................................................................9

Part 2..............................................................................................................................................10

3.1...............................................................................................................................................10

3.2 ..............................................................................................................................................11

4.1...............................................................................................................................................11

4.2...............................................................................................................................................12

4.3 ..............................................................................................................................................13

4.4 ..............................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Section one...................................................................................................................................3

1.1. ...............................................................................................................................................3

1.2.................................................................................................................................................4

1.3 ................................................................................................................................................4

1.4.................................................................................................................................................5

2.1. ...............................................................................................................................................5

2.2. ...............................................................................................................................................8

2.3 ................................................................................................................................................8

2.4.................................................................................................................................................9

Part 2..............................................................................................................................................10

3.1...............................................................................................................................................10

3.2 ..............................................................................................................................................11

4.1...............................................................................................................................................11

4.2...............................................................................................................................................12

4.3 ..............................................................................................................................................13

4.4 ..............................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION

Management accounting refers to that aspect of accounting which provides financial

information for the purpose of relevant decision making by the managers in the organisation. It

can be defined in different ways like the application of professional knowledge and skills while

preparing financial reports that could aid internal management of the business in framing

strategic policies along with carrying out effective planning and controlling the operation of the

concern (Pasch, 2019). Costing, budgeting and variance analysis are some of the tools and

techniques of management accounting. In this report, the various management accounting

systems, methods of preparing financial reports along with the preparation of financial reports

using tools and techniques of MA will be discussed. Also, it will be explained how these MAS

can be applied within organisation and how it helps in improving the performance of the concern

which leads to sustainable success for the organisation. This report will be based on The London

College, UK.

MAIN BODY

Section one

1.1.

Management accounting is the process of analysing the financial statement of the

company with the help of systems in order to take decision. For this purpose, the company have

to appoint the well qualified managers (Ammar, 2017). The requirements of management

accounting systems are including the following which helps the managers of The London

College in achieving their goals:

The managers of the London college use the MA information for the purpose of creating

and analysing the budgets and forecasts in order to plan, organise and control the

business strategies.

In order to analyse the data, they also use the variance analysis and break even analysis

tool so that they can identify the performance of the business is under or over

performance or balance (Yoder, and et.al., 2017).

With the help of accounting systems, they complete their work in less time and also

without any error. It is because the manual work involves lots of mistakes and errors.

3

Management accounting refers to that aspect of accounting which provides financial

information for the purpose of relevant decision making by the managers in the organisation. It

can be defined in different ways like the application of professional knowledge and skills while

preparing financial reports that could aid internal management of the business in framing

strategic policies along with carrying out effective planning and controlling the operation of the

concern (Pasch, 2019). Costing, budgeting and variance analysis are some of the tools and

techniques of management accounting. In this report, the various management accounting

systems, methods of preparing financial reports along with the preparation of financial reports

using tools and techniques of MA will be discussed. Also, it will be explained how these MAS

can be applied within organisation and how it helps in improving the performance of the concern

which leads to sustainable success for the organisation. This report will be based on The London

College, UK.

MAIN BODY

Section one

1.1.

Management accounting is the process of analysing the financial statement of the

company with the help of systems in order to take decision. For this purpose, the company have

to appoint the well qualified managers (Ammar, 2017). The requirements of management

accounting systems are including the following which helps the managers of The London

College in achieving their goals:

The managers of the London college use the MA information for the purpose of creating

and analysing the budgets and forecasts in order to plan, organise and control the

business strategies.

In order to analyse the data, they also use the variance analysis and break even analysis

tool so that they can identify the performance of the business is under or over

performance or balance (Yoder, and et.al., 2017).

With the help of accounting systems, they complete their work in less time and also

without any error. It is because the manual work involves lots of mistakes and errors.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The systems record the performance of each employee on daily basis. So mangers use

this to visualize the performance of employees and further motivate them for the same.

In case if the actual and planned performance have any gap and such gaps are

controllable, then the company motivates their employees in order to improve their

efficiency.

1.2

Management Accounting reporting methods

Inventory management system: It is the system of reporting the inventory movement in and

from the business, where the store manager tracks and simultaneously reports the inventory

throughout the chain of supply that is right from inventory acquisition to production to end sales.

By overseeing the inventory of the business, the management undertakes to ensure that there

would be no situations like under stocking and over stocking (Hlaciuc and et.al., 2017).

Job costing system: It refers to that system of costing where the overhead costs are assigned to

specific jobs or to various cost pools. This costing method is suitable where there are various

tasks or jobs or contracts are performed under one head.

Price optimization: Here the price of the products or services are determined by studying how

the variations in a demand is occurring due to corresponding change in the level of price. These

data of demand variations when combined with the cost related and available inventory levels in

order to determine and reach at an optimum price level (Li, 2018).

1.3

Benefits and application of management accounting system

Relevance: MA provides for key insights into a company's internal management to help

managers in decision making activities. They provide support in accomplishing decision making

tasks by providing useful information related to financial health (Gatti, 2018).

Updated information: As management accounting is done throughout the year, so it provides for

up to date information to the financial decision makers regarding various aspects of the business

operations.

Reliability: MA accounting reports and budgets as prepared on the basis of past information and

future estimations are done on the basis of these information, so there is a factor of reliability

which is ensured by management accounting systems (Dearman, Lechner and Shanklin, 2018).

4

this to visualize the performance of employees and further motivate them for the same.

In case if the actual and planned performance have any gap and such gaps are

controllable, then the company motivates their employees in order to improve their

efficiency.

1.2

Management Accounting reporting methods

Inventory management system: It is the system of reporting the inventory movement in and

from the business, where the store manager tracks and simultaneously reports the inventory

throughout the chain of supply that is right from inventory acquisition to production to end sales.

By overseeing the inventory of the business, the management undertakes to ensure that there

would be no situations like under stocking and over stocking (Hlaciuc and et.al., 2017).

Job costing system: It refers to that system of costing where the overhead costs are assigned to

specific jobs or to various cost pools. This costing method is suitable where there are various

tasks or jobs or contracts are performed under one head.

Price optimization: Here the price of the products or services are determined by studying how

the variations in a demand is occurring due to corresponding change in the level of price. These

data of demand variations when combined with the cost related and available inventory levels in

order to determine and reach at an optimum price level (Li, 2018).

1.3

Benefits and application of management accounting system

Relevance: MA provides for key insights into a company's internal management to help

managers in decision making activities. They provide support in accomplishing decision making

tasks by providing useful information related to financial health (Gatti, 2018).

Updated information: As management accounting is done throughout the year, so it provides for

up to date information to the financial decision makers regarding various aspects of the business

operations.

Reliability: MA accounting reports and budgets as prepared on the basis of past information and

future estimations are done on the basis of these information, so there is a factor of reliability

which is ensured by management accounting systems (Dearman, Lechner and Shanklin, 2018).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Understandable: MA system provides information that can be easily understand by managers,

and this feature of MAS only provides for support in decision making as it ensures that the

information is understandable by management.

Accuracy: The MAS provides for accurate information as the professionals who are highly

experienced and possessing expertise are involved in preparing MA reports (Saukkonen, Laine

and Suomala, 2018).

Thus, The London College can by utilizing the MAS achieves higher level of success and

improves their profitability by planning and controlling business activities through management

accounting information.

1.4

Integration of management accounting systems in organisational context and importance

of methods of reporting

The management accounting reports includes various reports such as budgets report, cost

report, performance report etc. The significance of this reports are increasing day by day because

it helps the managers of the company in tracking the performance of the business and taking the

appropriate decision for the same (Aureli, and et.al., 2019). Further, the reports also help them in

planning and regulating the different strategies of the business in case if the business in in under

performance. The reports also help the managers in selecting the best investment plans in case if

there are more than one project exist by the use of investment appraisal techniques. The company

also able to determine the cost associated with each department, job, process etc.

The management accounting system can be effectively integrated within an organisation in order

to make wise decision. Like cash flow analysis can be integrated within the function of liquidity

management of the organisation. Similarly, account receivables can be effectively managed by

organisations in collecting their outstanding debts. The system of budgeting guides an

organisation like The London College in estimating their financial performance for the upcoming

period in the future. Also, management accounting system like forecasting and trend analysis

allows an organisation to prepare themselves for the future positive and negative situations. In

addition to all this, management can plan the quantity of inventory they need to order and

planning for minimum and maximum inventory level at different periods can be done effectively.

5

and this feature of MAS only provides for support in decision making as it ensures that the

information is understandable by management.

Accuracy: The MAS provides for accurate information as the professionals who are highly

experienced and possessing expertise are involved in preparing MA reports (Saukkonen, Laine

and Suomala, 2018).

Thus, The London College can by utilizing the MAS achieves higher level of success and

improves their profitability by planning and controlling business activities through management

accounting information.

1.4

Integration of management accounting systems in organisational context and importance

of methods of reporting

The management accounting reports includes various reports such as budgets report, cost

report, performance report etc. The significance of this reports are increasing day by day because

it helps the managers of the company in tracking the performance of the business and taking the

appropriate decision for the same (Aureli, and et.al., 2019). Further, the reports also help them in

planning and regulating the different strategies of the business in case if the business in in under

performance. The reports also help the managers in selecting the best investment plans in case if

there are more than one project exist by the use of investment appraisal techniques. The company

also able to determine the cost associated with each department, job, process etc.

The management accounting system can be effectively integrated within an organisation in order

to make wise decision. Like cash flow analysis can be integrated within the function of liquidity

management of the organisation. Similarly, account receivables can be effectively managed by

organisations in collecting their outstanding debts. The system of budgeting guides an

organisation like The London College in estimating their financial performance for the upcoming

period in the future. Also, management accounting system like forecasting and trend analysis

allows an organisation to prepare themselves for the future positive and negative situations. In

addition to all this, management can plan the quantity of inventory they need to order and

planning for minimum and maximum inventory level at different periods can be done effectively.

5

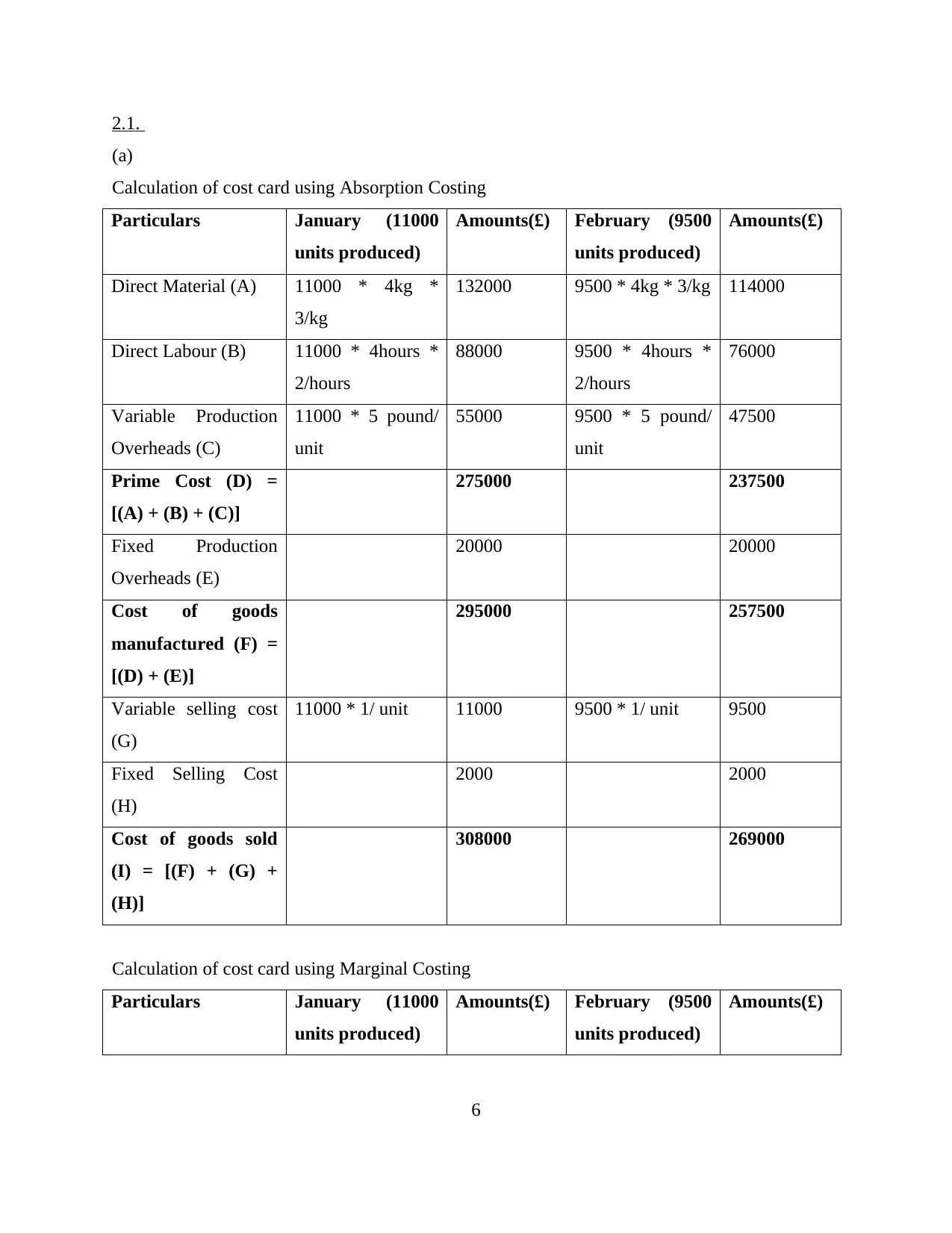

2.1.

(a)

Calculation of cost card using Absorption Costing

Particulars January (11000

units produced)

Amounts(£) February (9500

units produced)

Amounts(£)

Direct Material (A) 11000 * 4kg *

3/kg

132000 9500 * 4kg * 3/kg 114000

Direct Labour (B) 11000 * 4hours *

2/hours

88000 9500 * 4hours *

2/hours

76000

Variable Production

Overheads (C)

11000 * 5 pound/

unit

55000 9500 * 5 pound/

unit

47500

Prime Cost (D) =

[(A) + (B) + (C)]

275000 237500

Fixed Production

Overheads (E)

20000 20000

Cost of goods

manufactured (F) =

[(D) + (E)]

295000 257500

Variable selling cost

(G)

11000 * 1/ unit 11000 9500 * 1/ unit 9500

Fixed Selling Cost

(H)

2000 2000

Cost of goods sold

(I) = [(F) + (G) +

(H)]

308000 269000

Calculation of cost card using Marginal Costing

Particulars January (11000

units produced)

Amounts(£) February (9500

units produced)

Amounts(£)

6

(a)

Calculation of cost card using Absorption Costing

Particulars January (11000

units produced)

Amounts(£) February (9500

units produced)

Amounts(£)

Direct Material (A) 11000 * 4kg *

3/kg

132000 9500 * 4kg * 3/kg 114000

Direct Labour (B) 11000 * 4hours *

2/hours

88000 9500 * 4hours *

2/hours

76000

Variable Production

Overheads (C)

11000 * 5 pound/

unit

55000 9500 * 5 pound/

unit

47500

Prime Cost (D) =

[(A) + (B) + (C)]

275000 237500

Fixed Production

Overheads (E)

20000 20000

Cost of goods

manufactured (F) =

[(D) + (E)]

295000 257500

Variable selling cost

(G)

11000 * 1/ unit 11000 9500 * 1/ unit 9500

Fixed Selling Cost

(H)

2000 2000

Cost of goods sold

(I) = [(F) + (G) +

(H)]

308000 269000

Calculation of cost card using Marginal Costing

Particulars January (11000

units produced)

Amounts(£) February (9500

units produced)

Amounts(£)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct Material 12 per unit (4kg *

3)

12 per unit (4kg *

3)

Add Direct Labour 8 per units (4

hours * 2)

8 per units (4

hours * 2)

Add Variable

overheads (Variable

production + Variable

sales overheads)

6 per unit (5 + 1) 6 per unit (5 + 1)

Variable cost per

unit

26 per unit 26 per unit

Total Variable cost 11000 * 26 286000 9500 * 26 247000

Add Fixed Production

overheads

20000/10000 *

11000

22000 20000/10000 *

9500

19000

Add Fixed Sales

overheads

2000 2000

Total cost 310000 268000

(b)

Merits of Absorption costing:

This method takes all cost of production into the consideration while calculating the

profit rather than only the direct cost (LIU and PAN, 2018).

This method provides more accurate information related to profits to the company in case

if all the goods of the company are not sold in a particular period.

Demerits of Absorption costing:

AC skewed profit and loss of the company because it does not deduct all the fixed cost

from the sales revenue. But it seized the fixed production cost of closing stock with itself

only.

If company want to compare the profitability of its two product line than variable costing

is more considerable than the AC (LIU and PAN, 2018).

Merits of Marginal costing:

7

3)

12 per unit (4kg *

3)

Add Direct Labour 8 per units (4

hours * 2)

8 per units (4

hours * 2)

Add Variable

overheads (Variable

production + Variable

sales overheads)

6 per unit (5 + 1) 6 per unit (5 + 1)

Variable cost per

unit

26 per unit 26 per unit

Total Variable cost 11000 * 26 286000 9500 * 26 247000

Add Fixed Production

overheads

20000/10000 *

11000

22000 20000/10000 *

9500

19000

Add Fixed Sales

overheads

2000 2000

Total cost 310000 268000

(b)

Merits of Absorption costing:

This method takes all cost of production into the consideration while calculating the

profit rather than only the direct cost (LIU and PAN, 2018).

This method provides more accurate information related to profits to the company in case

if all the goods of the company are not sold in a particular period.

Demerits of Absorption costing:

AC skewed profit and loss of the company because it does not deduct all the fixed cost

from the sales revenue. But it seized the fixed production cost of closing stock with itself

only.

If company want to compare the profitability of its two product line than variable costing

is more considerable than the AC (LIU and PAN, 2018).

Merits of Marginal costing:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

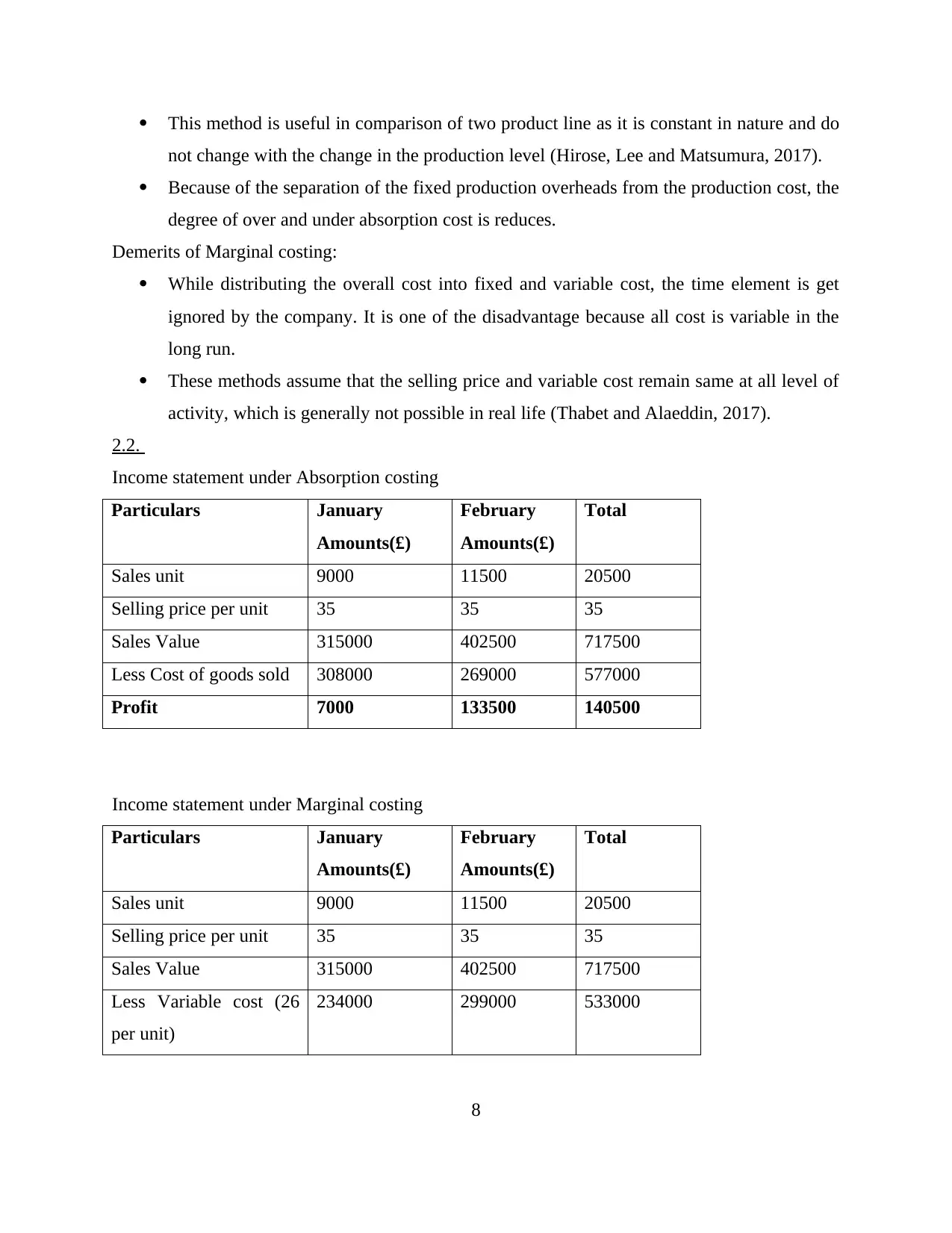

This method is useful in comparison of two product line as it is constant in nature and do

not change with the change in the production level (Hirose, Lee and Matsumura, 2017).

Because of the separation of the fixed production overheads from the production cost, the

degree of over and under absorption cost is reduces.

Demerits of Marginal costing:

While distributing the overall cost into fixed and variable cost, the time element is get

ignored by the company. It is one of the disadvantage because all cost is variable in the

long run.

These methods assume that the selling price and variable cost remain same at all level of

activity, which is generally not possible in real life (Thabet and Alaeddin, 2017).

2.2.

Income statement under Absorption costing

Particulars January

Amounts(£)

February

Amounts(£)

Total

Sales unit 9000 11500 20500

Selling price per unit 35 35 35

Sales Value 315000 402500 717500

Less Cost of goods sold 308000 269000 577000

Profit 7000 133500 140500

Income statement under Marginal costing

Particulars January

Amounts(£)

February

Amounts(£)

Total

Sales unit 9000 11500 20500

Selling price per unit 35 35 35

Sales Value 315000 402500 717500

Less Variable cost (26

per unit)

234000 299000 533000

8

not change with the change in the production level (Hirose, Lee and Matsumura, 2017).

Because of the separation of the fixed production overheads from the production cost, the

degree of over and under absorption cost is reduces.

Demerits of Marginal costing:

While distributing the overall cost into fixed and variable cost, the time element is get

ignored by the company. It is one of the disadvantage because all cost is variable in the

long run.

These methods assume that the selling price and variable cost remain same at all level of

activity, which is generally not possible in real life (Thabet and Alaeddin, 2017).

2.2.

Income statement under Absorption costing

Particulars January

Amounts(£)

February

Amounts(£)

Total

Sales unit 9000 11500 20500

Selling price per unit 35 35 35

Sales Value 315000 402500 717500

Less Cost of goods sold 308000 269000 577000

Profit 7000 133500 140500

Income statement under Marginal costing

Particulars January

Amounts(£)

February

Amounts(£)

Total

Sales unit 9000 11500 20500

Selling price per unit 35 35 35

Sales Value 315000 402500 717500

Less Variable cost (26

per unit)

234000 299000 533000

8

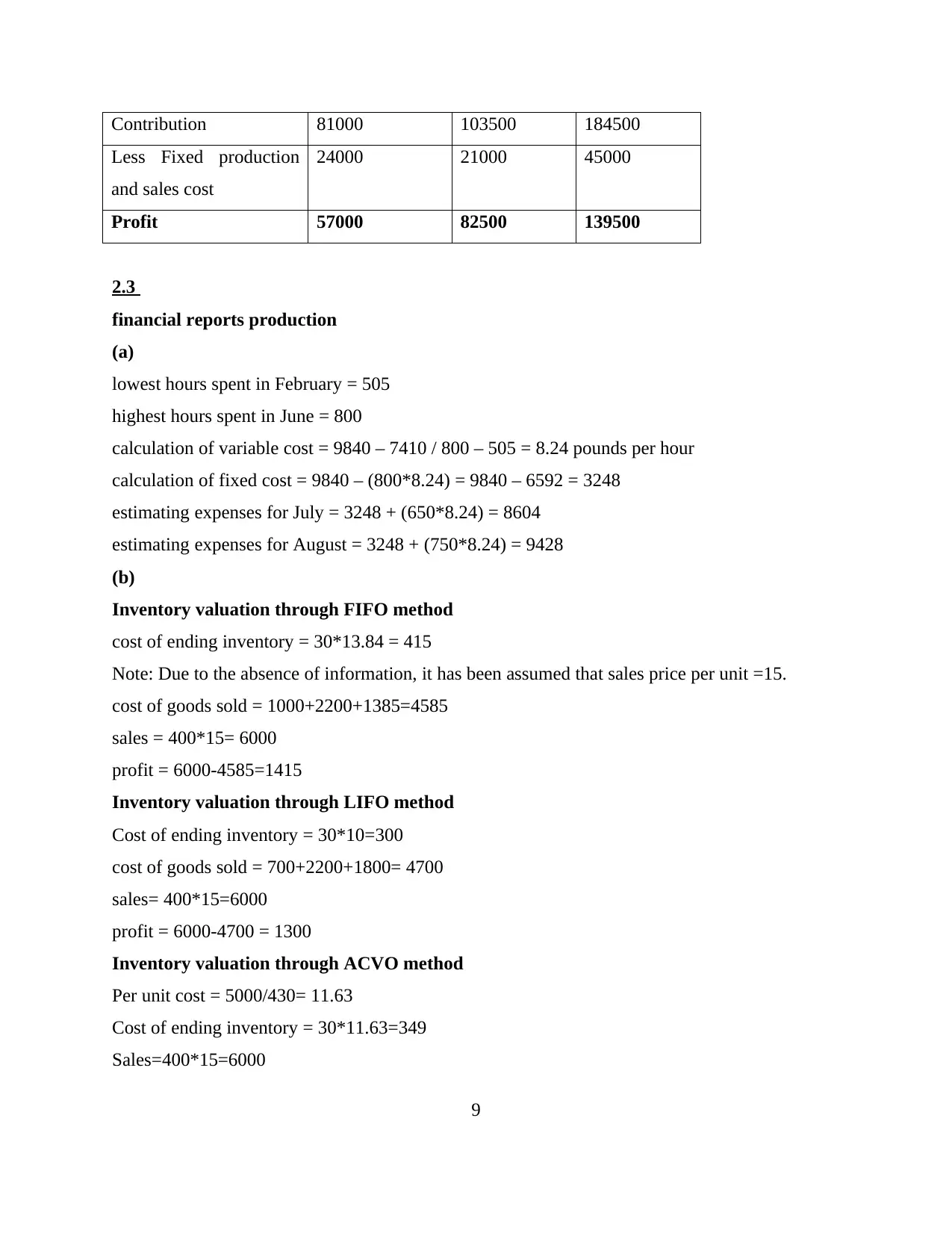

Contribution 81000 103500 184500

Less Fixed production

and sales cost

24000 21000 45000

Profit 57000 82500 139500

2.3

financial reports production

(a)

lowest hours spent in February = 505

highest hours spent in June = 800

calculation of variable cost = 9840 – 7410 / 800 – 505 = 8.24 pounds per hour

calculation of fixed cost = 9840 – (800*8.24) = 9840 – 6592 = 3248

estimating expenses for July = 3248 + (650*8.24) = 8604

estimating expenses for August = 3248 + (750*8.24) = 9428

(b)

Inventory valuation through FIFO method

cost of ending inventory = 30*13.84 = 415

Note: Due to the absence of information, it has been assumed that sales price per unit =15.

cost of goods sold = 1000+2200+1385=4585

sales = 400*15= 6000

profit = 6000-4585=1415

Inventory valuation through LIFO method

Cost of ending inventory = 30*10=300

cost of goods sold = 700+2200+1800= 4700

sales= 400*15=6000

profit = 6000-4700 = 1300

Inventory valuation through ACVO method

Per unit cost = 5000/430= 11.63

Cost of ending inventory = 30*11.63=349

Sales=400*15=6000

9

Less Fixed production

and sales cost

24000 21000 45000

Profit 57000 82500 139500

2.3

financial reports production

(a)

lowest hours spent in February = 505

highest hours spent in June = 800

calculation of variable cost = 9840 – 7410 / 800 – 505 = 8.24 pounds per hour

calculation of fixed cost = 9840 – (800*8.24) = 9840 – 6592 = 3248

estimating expenses for July = 3248 + (650*8.24) = 8604

estimating expenses for August = 3248 + (750*8.24) = 9428

(b)

Inventory valuation through FIFO method

cost of ending inventory = 30*13.84 = 415

Note: Due to the absence of information, it has been assumed that sales price per unit =15.

cost of goods sold = 1000+2200+1385=4585

sales = 400*15= 6000

profit = 6000-4585=1415

Inventory valuation through LIFO method

Cost of ending inventory = 30*10=300

cost of goods sold = 700+2200+1800= 4700

sales= 400*15=6000

profit = 6000-4700 = 1300

Inventory valuation through ACVO method

Per unit cost = 5000/430= 11.63

Cost of ending inventory = 30*11.63=349

Sales=400*15=6000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost of goods sold = 400*11.63=4652

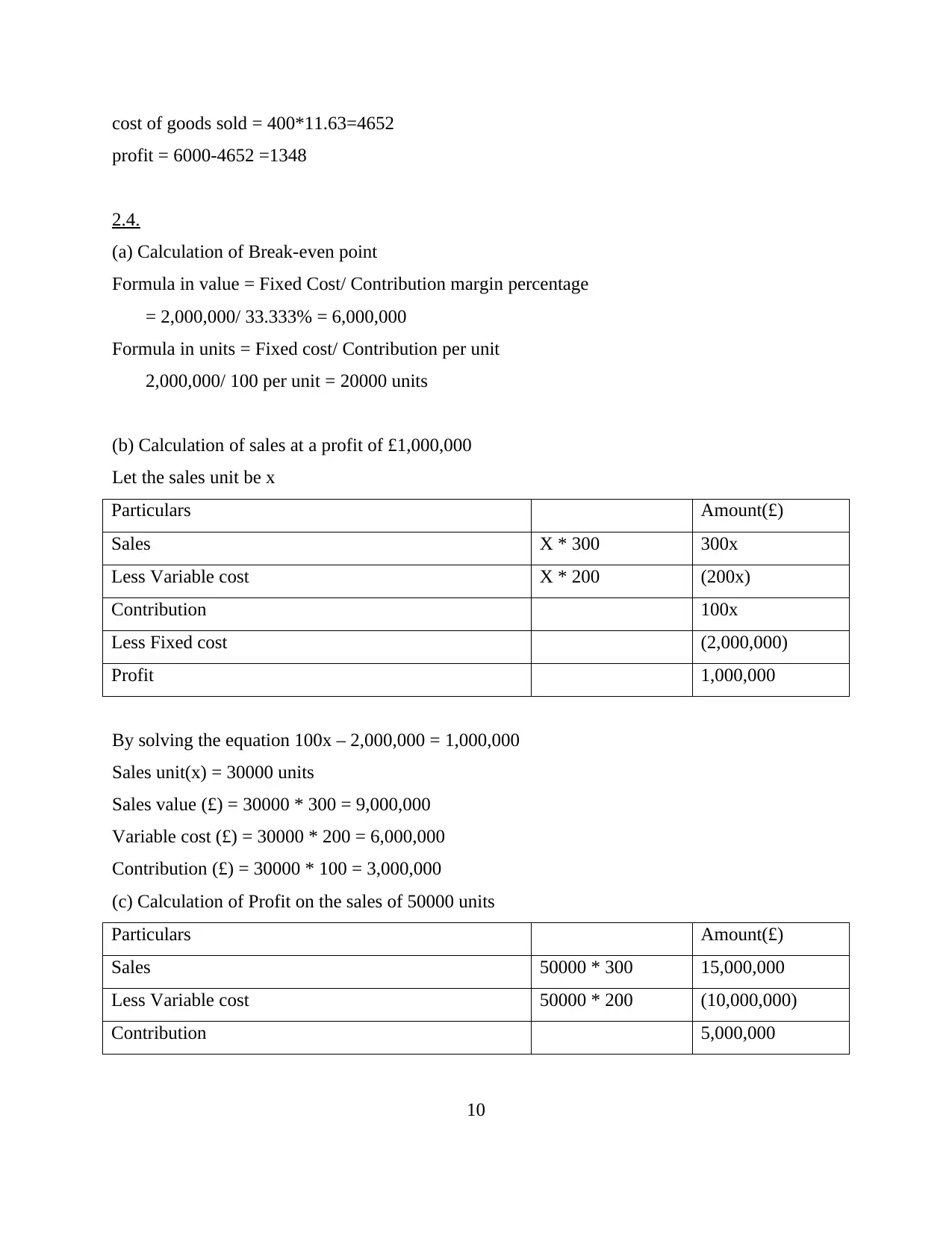

profit = 6000-4652 =1348

2.4.

(a) Calculation of Break-even point

Formula in value = Fixed Cost/ Contribution margin percentage

= 2,000,000/ 33.333% = 6,000,000

Formula in units = Fixed cost/ Contribution per unit

2,000,000/ 100 per unit = 20000 units

(b) Calculation of sales at a profit of £1,000,000

Let the sales unit be x

Particulars Amount(£)

Sales X * 300 300x

Less Variable cost X * 200 (200x)

Contribution 100x

Less Fixed cost (2,000,000)

Profit 1,000,000

By solving the equation 100x – 2,000,000 = 1,000,000

Sales unit(x) = 30000 units

Sales value (£) = 30000 * 300 = 9,000,000

Variable cost (£) = 30000 * 200 = 6,000,000

Contribution (£) = 30000 * 100 = 3,000,000

(c) Calculation of Profit on the sales of 50000 units

Particulars Amount(£)

Sales 50000 * 300 15,000,000

Less Variable cost 50000 * 200 (10,000,000)

Contribution 5,000,000

10

profit = 6000-4652 =1348

2.4.

(a) Calculation of Break-even point

Formula in value = Fixed Cost/ Contribution margin percentage

= 2,000,000/ 33.333% = 6,000,000

Formula in units = Fixed cost/ Contribution per unit

2,000,000/ 100 per unit = 20000 units

(b) Calculation of sales at a profit of £1,000,000

Let the sales unit be x

Particulars Amount(£)

Sales X * 300 300x

Less Variable cost X * 200 (200x)

Contribution 100x

Less Fixed cost (2,000,000)

Profit 1,000,000

By solving the equation 100x – 2,000,000 = 1,000,000

Sales unit(x) = 30000 units

Sales value (£) = 30000 * 300 = 9,000,000

Variable cost (£) = 30000 * 200 = 6,000,000

Contribution (£) = 30000 * 100 = 3,000,000

(c) Calculation of Profit on the sales of 50000 units

Particulars Amount(£)

Sales 50000 * 300 15,000,000

Less Variable cost 50000 * 200 (10,000,000)

Contribution 5,000,000

10

Paraphrase This Document

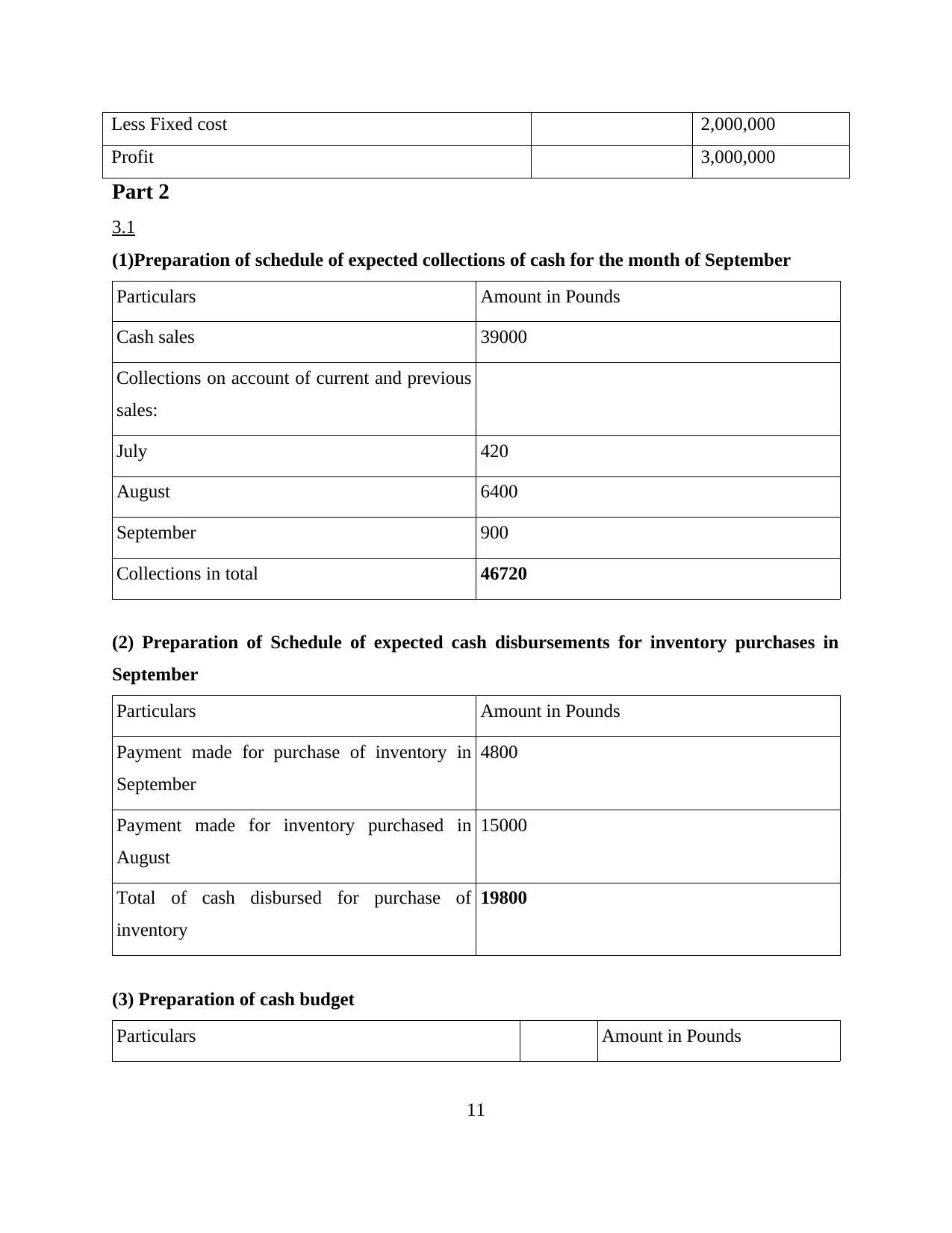

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less Fixed cost 2,000,000

Profit 3,000,000

Part 2

3.1

(1)Preparation of schedule of expected collections of cash for the month of September

Particulars Amount in Pounds

Cash sales 39000

Collections on account of current and previous

sales:

July 420

August 6400

September 900

Collections in total 46720

(2) Preparation of Schedule of expected cash disbursements for inventory purchases in

September

Particulars Amount in Pounds

Payment made for purchase of inventory in

September

4800

Payment made for inventory purchased in

August

15000

Total of cash disbursed for purchase of

inventory

19800

(3) Preparation of cash budget

Particulars Amount in Pounds

11

Profit 3,000,000

Part 2

3.1

(1)Preparation of schedule of expected collections of cash for the month of September

Particulars Amount in Pounds

Cash sales 39000

Collections on account of current and previous

sales:

July 420

August 6400

September 900

Collections in total 46720

(2) Preparation of Schedule of expected cash disbursements for inventory purchases in

September

Particulars Amount in Pounds

Payment made for purchase of inventory in

September

4800

Payment made for inventory purchased in

August

15000

Total of cash disbursed for purchase of

inventory

19800

(3) Preparation of cash budget

Particulars Amount in Pounds

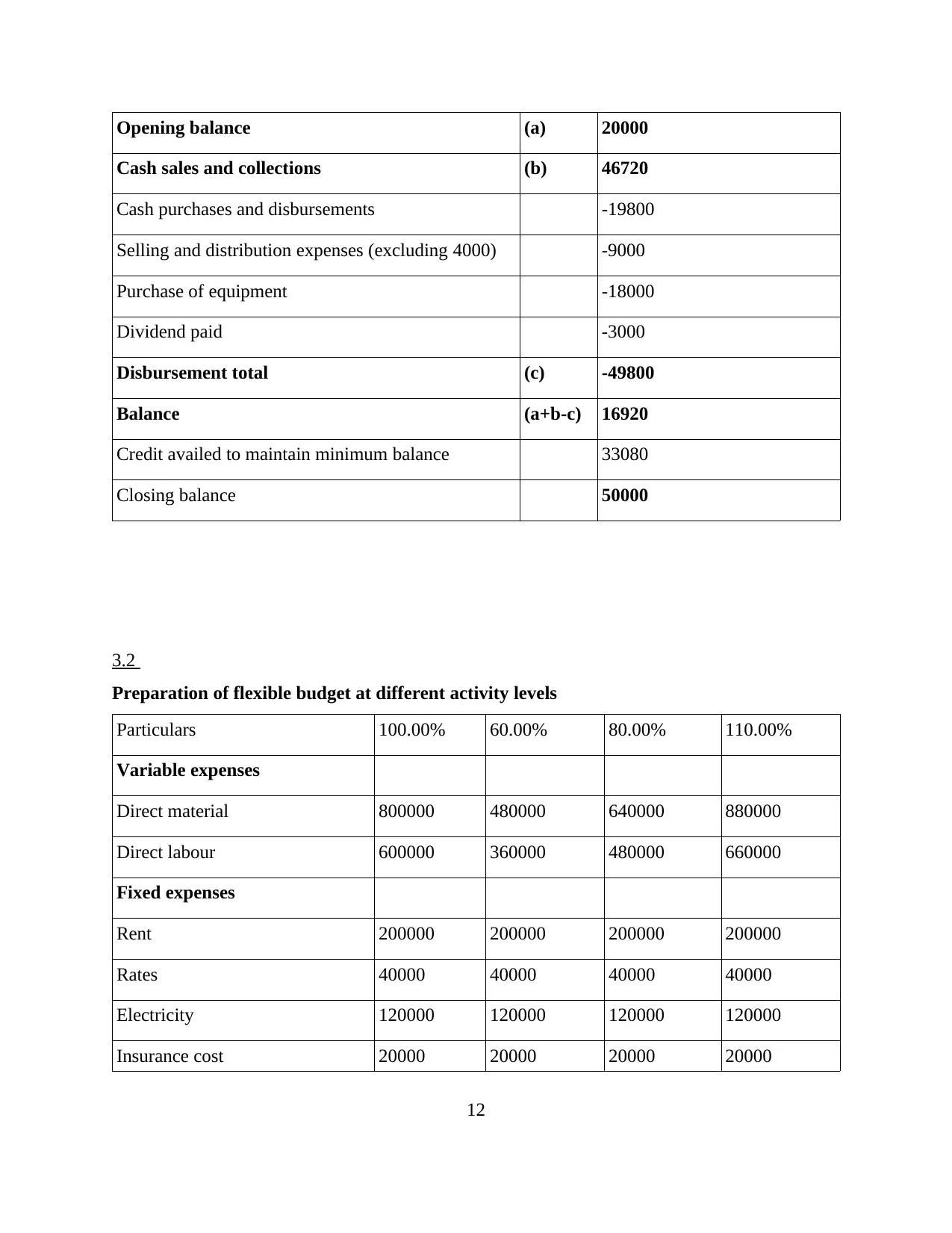

11

Opening balance (a) 20000

Cash sales and collections (b) 46720

Cash purchases and disbursements -19800

Selling and distribution expenses (excluding 4000) -9000

Purchase of equipment -18000

Dividend paid -3000

Disbursement total (c) -49800

Balance (a+b-c) 16920

Credit availed to maintain minimum balance 33080

Closing balance 50000

3.2

Preparation of flexible budget at different activity levels

Particulars 100.00% 60.00% 80.00% 110.00%

Variable expenses

Direct material 800000 480000 640000 880000

Direct labour 600000 360000 480000 660000

Fixed expenses

Rent 200000 200000 200000 200000

Rates 40000 40000 40000 40000

Electricity 120000 120000 120000 120000

Insurance cost 20000 20000 20000 20000

12

Cash sales and collections (b) 46720

Cash purchases and disbursements -19800

Selling and distribution expenses (excluding 4000) -9000

Purchase of equipment -18000

Dividend paid -3000

Disbursement total (c) -49800

Balance (a+b-c) 16920

Credit availed to maintain minimum balance 33080

Closing balance 50000

3.2

Preparation of flexible budget at different activity levels

Particulars 100.00% 60.00% 80.00% 110.00%

Variable expenses

Direct material 800000 480000 640000 880000

Direct labour 600000 360000 480000 660000

Fixed expenses

Rent 200000 200000 200000 200000

Rates 40000 40000 40000 40000

Electricity 120000 120000 120000 120000

Insurance cost 20000 20000 20000 20000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.