FNS40610 Certificate IV Accounting: Assessment 1 - Financial Reports

VerifiedAdded on 2019/10/09

|5

|1273

|105

Homework Assignment

AI Summary

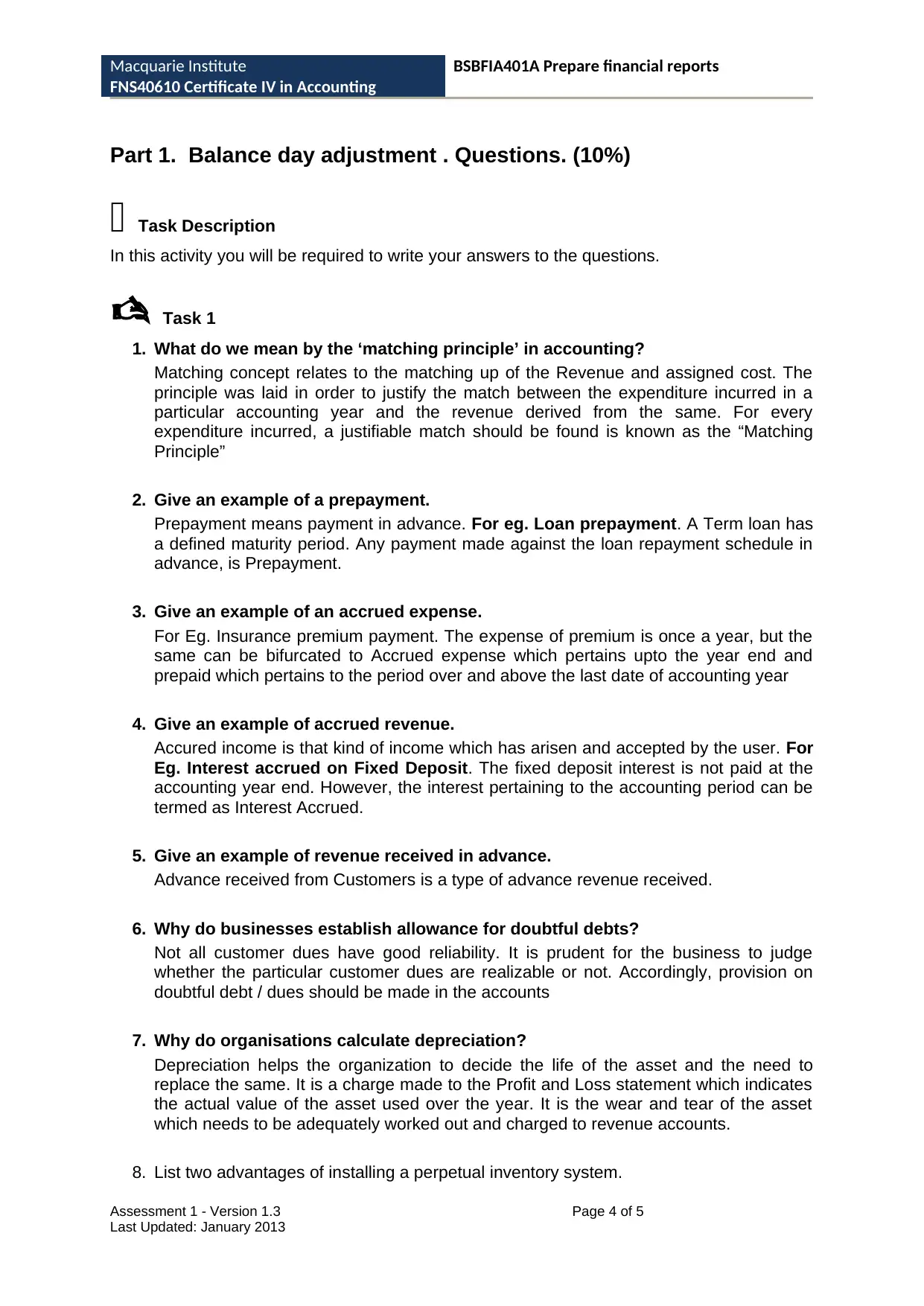

This document presents a completed accounting assessment for the FNS40610 Certificate IV in Accounting. The assessment comprises four parts, each contributing to the overall grade. Part 1 focuses on balance day adjustments, requiring answers to questions about the matching principle, prepayments, accrued expenses, accrued revenue, revenue received in advance, allowance for doubtful debts, depreciation, and perpetual inventory systems. The assessment also includes a portfolio of evidence drawn from the textbook 'Accounting: A practical approach' by Pearson. Further parts of the assessment involve creating balance day adjustment journal entries, closing entries, trading and profit and loss accounts, an income statement, and a balance sheet. The final parts involve completing a worksheet for final reports (10 column) and maintaining an asset register, covering depreciation and disposal of non-current assets. The student demonstrates understanding of key accounting concepts and the ability to apply them in practical scenarios.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.