FNSACC504: Financial Reports - Data Compilation and Presentation

VerifiedAdded on 2023/06/03

|27

|4589

|257

Homework Assignment

AI Summary

This FNSACC504 assessment solution provides detailed answers to questions on data compilation and financial reporting for corporate entities. It includes data conversion and consolidation procedures, spreadsheet tasks involving batting averages of a cricket team, depreciation calculations using diminishing value and prime cost methods, and retail inventory method calculations. The solution also covers journal entries with GST, presentation of car sales data in pie charts and line graphs, and a review of National Australia Bank's financial report for compliance with statutory requirements. Furthermore, it addresses ethical issues in governance and the alignment of organizational policies with statutory reporting requirements. Desklib offers this and many more solved assignments.

Assessment Workbook – FNSACC504 1 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment 1: Short Answer Questions

The objective of this section is to demonstrate 1.0 Compile data

Question 2

a. Give three (3) data conversion procedures and explain when you would use them to

compile data in accordance with organisational policy and procedures.

The following are the data conversion procedures:

Running the new system parallel to the old system. In this, both of the systems are run

parallel as against one another.

Phase in the new system. This includes the conversion of just location which contains

the data to migrate.

Direct changeover. This means converting the entire system into the new system

(Small business chron, 2018).

b. Give three (3) consolidation procedures used in accounting and explain used to

compile data in accordance with organisational policy and procedures.

The following are the 3 conversion procedures:

Consolidation: this is when a company (investor) holds more than 51% of the

share capital of the other company (investee). In such cases, both of the books

of the companies are combined as one.

Equity method: this is when an investee possess a minor ownership of the

share capital in the investee.

Assessment Workbook – FNSACC504 2 | P a g e Version 3.0

The objective of this section is to demonstrate 1.0 Compile data

Question 2

a. Give three (3) data conversion procedures and explain when you would use them to

compile data in accordance with organisational policy and procedures.

The following are the data conversion procedures:

Running the new system parallel to the old system. In this, both of the systems are run

parallel as against one another.

Phase in the new system. This includes the conversion of just location which contains

the data to migrate.

Direct changeover. This means converting the entire system into the new system

(Small business chron, 2018).

b. Give three (3) consolidation procedures used in accounting and explain used to

compile data in accordance with organisational policy and procedures.

The following are the 3 conversion procedures:

Consolidation: this is when a company (investor) holds more than 51% of the

share capital of the other company (investee). In such cases, both of the books

of the companies are combined as one.

Equity method: this is when an investee possess a minor ownership of the

share capital in the investee.

Assessment Workbook – FNSACC504 2 | P a g e Version 3.0

Equity pick up: this is when the cost method includes the recording of an

investment as an asset and also records the dividends as an income to the

investor (Corporate finance institute, 2018).

Question 3

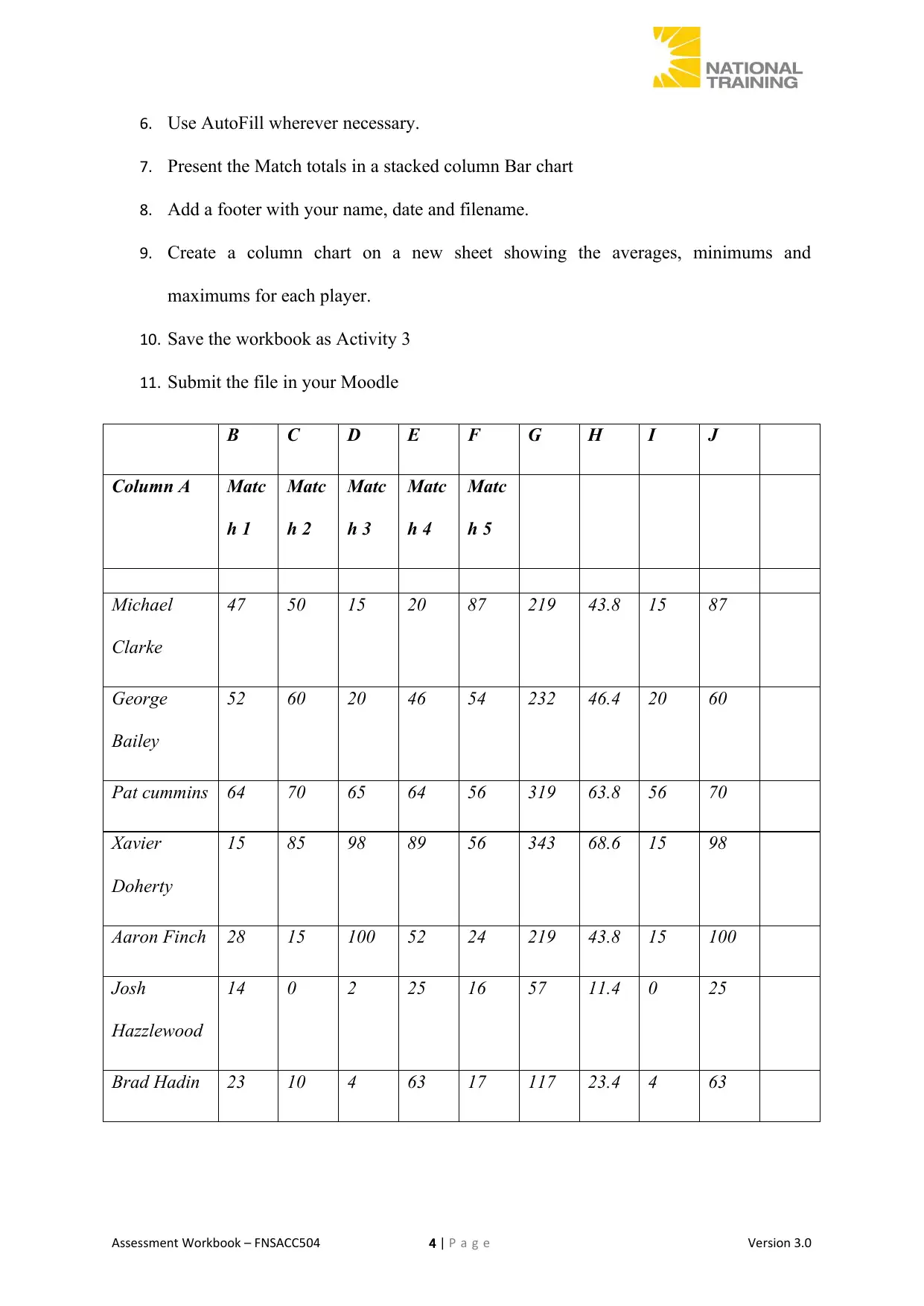

Complete the tasks below and ensure they are correctly entered into a spreadsheet.

1. Create a new workbook to reflect the batting average of the Australia cricket team

over a designated period in a series of 5 matches.

2. Names of the below batsmen should be listed down in Column A.

a. Michael Clarke

b. George Bailey

c. Pat Cummins

d. Xavier Doherty

e. Aaron Finch

f. Josh Hazlewood

g. Brad Hadin

h. James Faulkner

i. Mitchel Johnson

j. Mitchell Starc

k. David Warner

3. Matches 1, 2, 3, 4 and 5 headings should be in columns B, C, D, E and F respectively.

Input run score for each player of each match. (could be any figures of your choice)

4. Record the individual totals in column G and average score in Column H

5. Calculate minimum and maximum runs for each match and each player in column I

and J respectively

Assessment Workbook – FNSACC504 3 | P a g e Version 3.0

investment as an asset and also records the dividends as an income to the

investor (Corporate finance institute, 2018).

Question 3

Complete the tasks below and ensure they are correctly entered into a spreadsheet.

1. Create a new workbook to reflect the batting average of the Australia cricket team

over a designated period in a series of 5 matches.

2. Names of the below batsmen should be listed down in Column A.

a. Michael Clarke

b. George Bailey

c. Pat Cummins

d. Xavier Doherty

e. Aaron Finch

f. Josh Hazlewood

g. Brad Hadin

h. James Faulkner

i. Mitchel Johnson

j. Mitchell Starc

k. David Warner

3. Matches 1, 2, 3, 4 and 5 headings should be in columns B, C, D, E and F respectively.

Input run score for each player of each match. (could be any figures of your choice)

4. Record the individual totals in column G and average score in Column H

5. Calculate minimum and maximum runs for each match and each player in column I

and J respectively

Assessment Workbook – FNSACC504 3 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

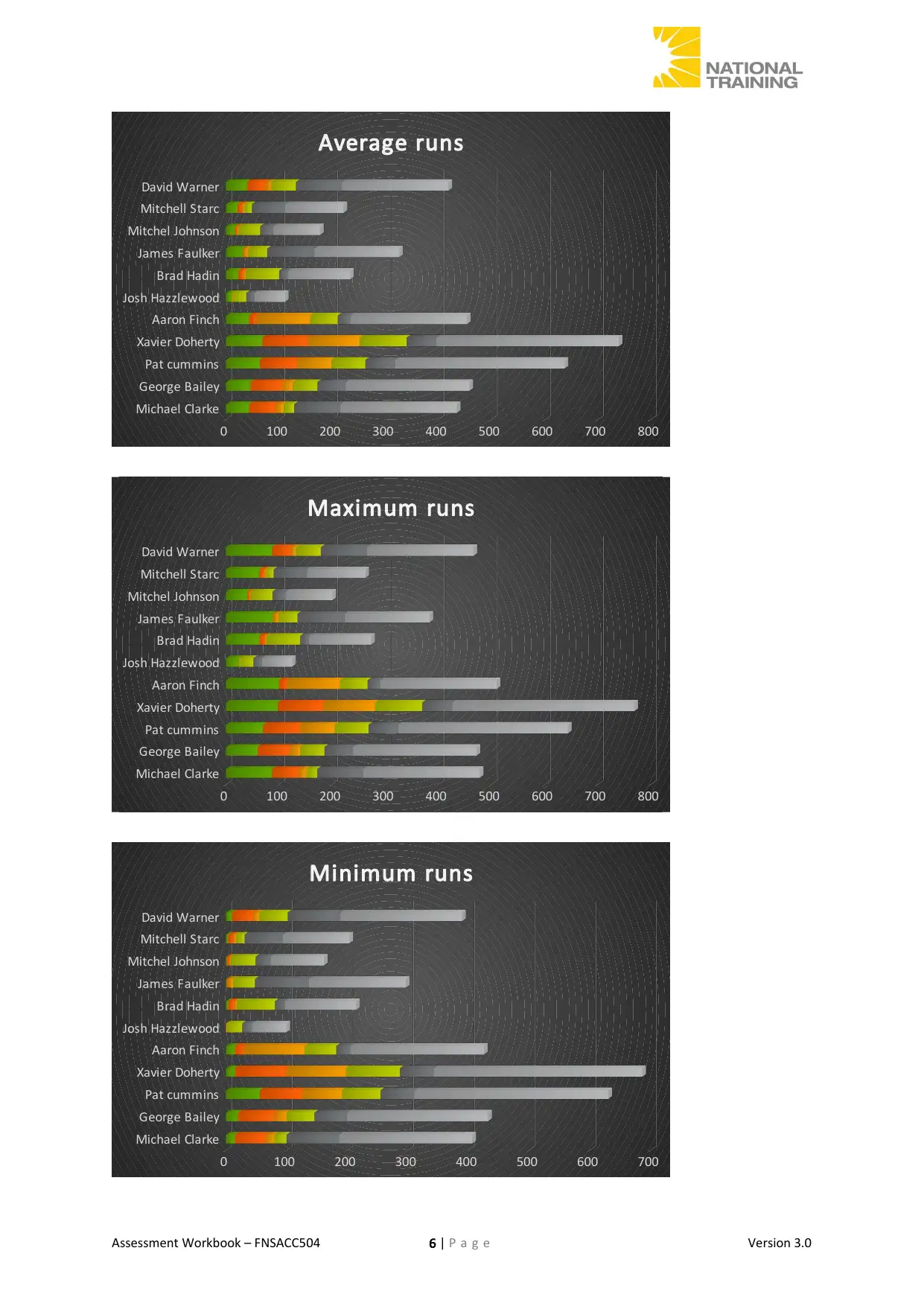

6. Use AutoFill wherever necessary.

7. Present the Match totals in a stacked column Bar chart

8. Add a footer with your name, date and filename.

9. Create a column chart on a new sheet showing the averages, minimums and

maximums for each player.

10. Save the workbook as Activity 3

11. Submit the file in your Moodle

B C D E F G H I J

Column A Matc

h 1

Matc

h 2

Matc

h 3

Matc

h 4

Matc

h 5

Michael

Clarke

47 50 15 20 87 219 43.8 15 87

George

Bailey

52 60 20 46 54 232 46.4 20 60

Pat cummins 64 70 65 64 56 319 63.8 56 70

Xavier

Doherty

15 85 98 89 56 343 68.6 15 98

Aaron Finch 28 15 100 52 24 219 43.8 15 100

Josh

Hazzlewood

14 0 2 25 16 57 11.4 0 25

Brad Hadin 23 10 4 63 17 117 23.4 4 63

Assessment Workbook – FNSACC504 4 | P a g e Version 3.0

7. Present the Match totals in a stacked column Bar chart

8. Add a footer with your name, date and filename.

9. Create a column chart on a new sheet showing the averages, minimums and

maximums for each player.

10. Save the workbook as Activity 3

11. Submit the file in your Moodle

B C D E F G H I J

Column A Matc

h 1

Matc

h 2

Matc

h 3

Matc

h 4

Matc

h 5

Michael

Clarke

47 50 15 20 87 219 43.8 15 87

George

Bailey

52 60 20 46 54 232 46.4 20 60

Pat cummins 64 70 65 64 56 319 63.8 56 70

Xavier

Doherty

15 85 98 89 56 343 68.6 15 98

Aaron Finch 28 15 100 52 24 219 43.8 15 100

Josh

Hazzlewood

14 0 2 25 16 57 11.4 0 25

Brad Hadin 23 10 4 63 17 117 23.4 4 63

Assessment Workbook – FNSACC504 4 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

James

Faulker

25 2 8 36 89 160 32 2 89

Mitchel

Johnson

16 4 2 41 25 88 17.6 2 41

Mitchell

Starc

20 9 4 14 63 110 22 4 63

David

Warner

21 35 10 47 87 200 40 10 87

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700

Total of runs

Assessment Workbook – FNSACC504 5 | P a g e Version 3.0

Faulker

25 2 8 36 89 160 32 2 89

Mitchel

Johnson

16 4 2 41 25 88 17.6 2 41

Mitchell

Starc

20 9 4 14 63 110 22 4 63

David

Warner

21 35 10 47 87 200 40 10 87

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700

Total of runs

Assessment Workbook – FNSACC504 5 | P a g e Version 3.0

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700 800

Average runs

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700 800

Maximum runs

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700

Minimum runs

Assessment Workbook – FNSACC504 6 | P a g e Version 3.0

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700 800

Average runs

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700 800

Maximum runs

Michael Clarke

George Bailey

Pat cummins

Xavier Doherty

Aaron Finch

Josh Hazzlewood

Brad Hadin

James Faulker

Mitchel Johnson

Mitchell Starc

David Warner

0 100 200 300 400 500 600 700

Minimum runs

Assessment Workbook – FNSACC504 6 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

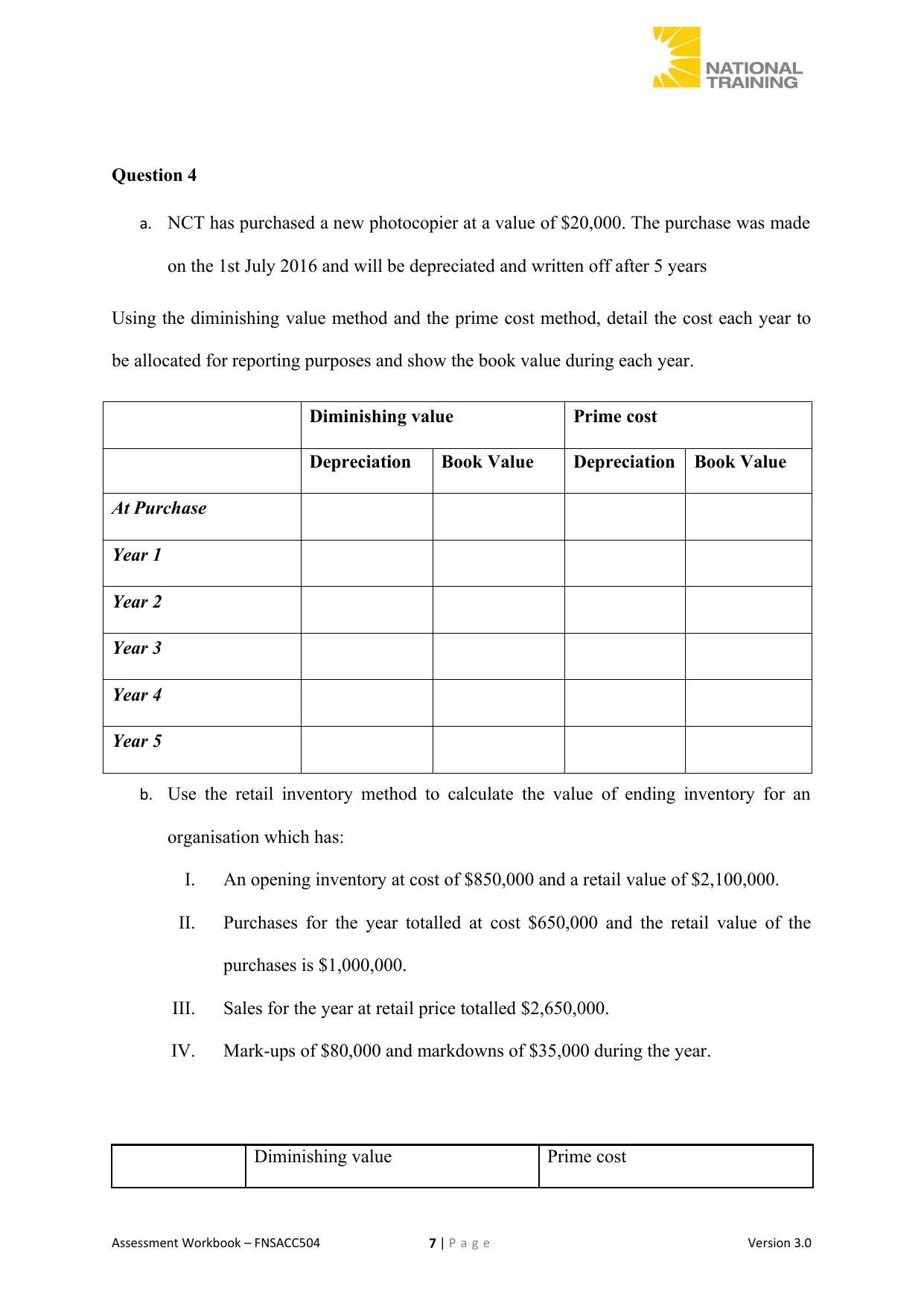

Question 4

a. NCT has purchased a new photocopier at a value of $20,000. The purchase was made

on the 1st July 2016 and will be depreciated and written off after 5 years

Using the diminishing value method and the prime cost method, detail the cost each year to

be allocated for reporting purposes and show the book value during each year.

Diminishing value Prime cost

Depreciation Book Value Depreciation Book Value

At Purchase

Year 1

Year 2

Year 3

Year 4

Year 5

b. Use the retail inventory method to calculate the value of ending inventory for an

organisation which has:

I. An opening inventory at cost of $850,000 and a retail value of $2,100,000.

II. Purchases for the year totalled at cost $650,000 and the retail value of the

purchases is $1,000,000.

III. Sales for the year at retail price totalled $2,650,000.

IV. Mark-ups of $80,000 and markdowns of $35,000 during the year.

Diminishing value Prime cost

Assessment Workbook – FNSACC504 7 | P a g e Version 3.0

a. NCT has purchased a new photocopier at a value of $20,000. The purchase was made

on the 1st July 2016 and will be depreciated and written off after 5 years

Using the diminishing value method and the prime cost method, detail the cost each year to

be allocated for reporting purposes and show the book value during each year.

Diminishing value Prime cost

Depreciation Book Value Depreciation Book Value

At Purchase

Year 1

Year 2

Year 3

Year 4

Year 5

b. Use the retail inventory method to calculate the value of ending inventory for an

organisation which has:

I. An opening inventory at cost of $850,000 and a retail value of $2,100,000.

II. Purchases for the year totalled at cost $650,000 and the retail value of the

purchases is $1,000,000.

III. Sales for the year at retail price totalled $2,650,000.

IV. Mark-ups of $80,000 and markdowns of $35,000 during the year.

Diminishing value Prime cost

Assessment Workbook – FNSACC504 7 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

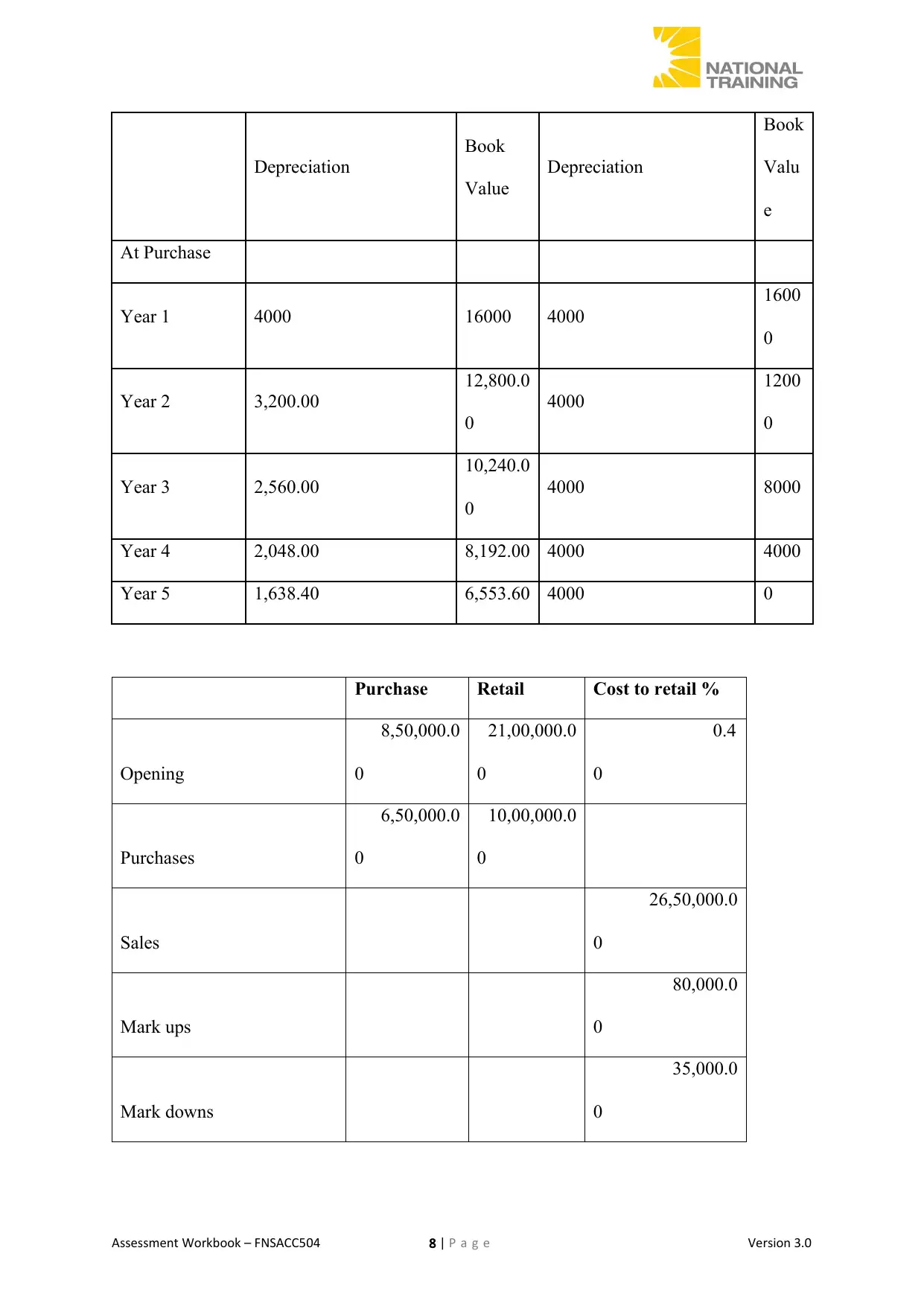

Depreciation

Book

Value

Depreciation

Book

Valu

e

At Purchase

Year 1 4000 16000 4000

1600

0

Year 2 3,200.00

12,800.0

0

4000

1200

0

Year 3 2,560.00

10,240.0

0

4000 8000

Year 4 2,048.00 8,192.00 4000 4000

Year 5 1,638.40 6,553.60 4000 0

Purchase Retail Cost to retail %

Opening

8,50,000.0

0

21,00,000.0

0

0.4

0

Purchases

6,50,000.0

0

10,00,000.0

0

Sales

26,50,000.0

0

Mark ups

80,000.0

0

Mark downs

35,000.0

0

Assessment Workbook – FNSACC504 8 | P a g e Version 3.0

Book

Value

Depreciation

Book

Valu

e

At Purchase

Year 1 4000 16000 4000

1600

0

Year 2 3,200.00

12,800.0

0

4000

1200

0

Year 3 2,560.00

10,240.0

0

4000 8000

Year 4 2,048.00 8,192.00 4000 4000

Year 5 1,638.40 6,553.60 4000 0

Purchase Retail Cost to retail %

Opening

8,50,000.0

0

21,00,000.0

0

0.4

0

Purchases

6,50,000.0

0

10,00,000.0

0

Sales

26,50,000.0

0

Mark ups

80,000.0

0

Mark downs

35,000.0

0

Assessment Workbook – FNSACC504 8 | P a g e Version 3.0

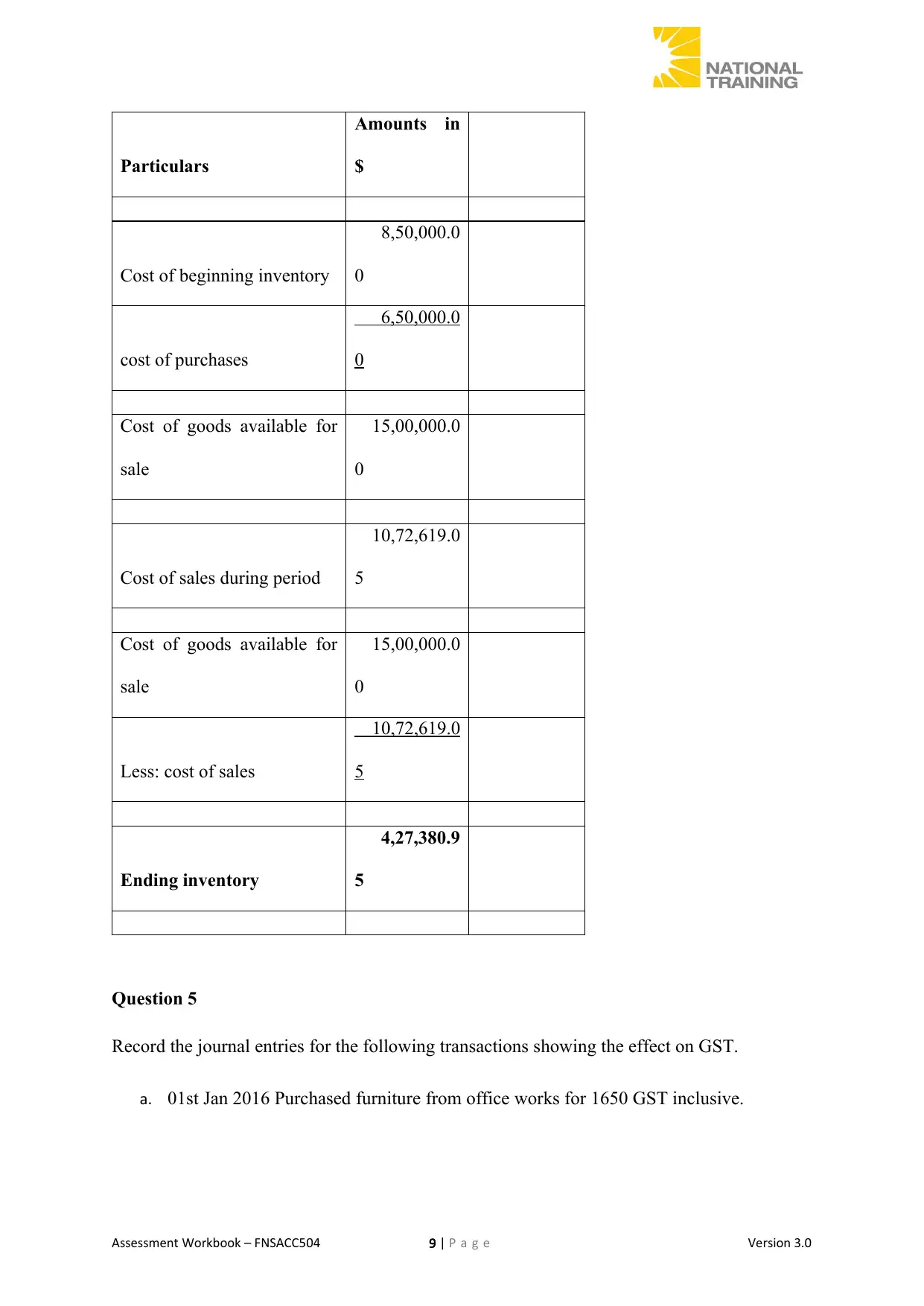

Particulars

Amounts in

$

Cost of beginning inventory

8,50,000.0

0

cost of purchases

6,50,000.0

0

Cost of goods available for

sale

15,00,000.0

0

Cost of sales during period

10,72,619.0

5

Cost of goods available for

sale

15,00,000.0

0

Less: cost of sales

10,72,619.0

5

Ending inventory

4,27,380.9

5

Question 5

Record the journal entries for the following transactions showing the effect on GST.

a. 01st Jan 2016 Purchased furniture from office works for 1650 GST inclusive.

Assessment Workbook – FNSACC504 9 | P a g e Version 3.0

Amounts in

$

Cost of beginning inventory

8,50,000.0

0

cost of purchases

6,50,000.0

0

Cost of goods available for

sale

15,00,000.0

0

Cost of sales during period

10,72,619.0

5

Cost of goods available for

sale

15,00,000.0

0

Less: cost of sales

10,72,619.0

5

Ending inventory

4,27,380.9

5

Question 5

Record the journal entries for the following transactions showing the effect on GST.

a. 01st Jan 2016 Purchased furniture from office works for 1650 GST inclusive.

Assessment Workbook – FNSACC504 9 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

01.01.2016 Furniture $1650

To Office works $1650

b. 31st Jan 2016 Purchased motor vehicle at a cost $30,000 Registration of the motor

vehicle was $730 from Essendon Mazda plus GST

31.01.2016 Motor vehicle $30,730

To Office works $30,730

c. 14th Feb 2016 sold items to a customer for $7000 plus GST. Payment terms are 30

days after the purchase

14.02.2016 Accounts receivables $7,000

To Sales revenue $7,000

Payment after 30 days

14.03.2016 Cash $7,000

To Accounts receivables $7,000

d. 20/03/2016 Paid supplier of stock purchased in cash for $15000 plus GST

20.03.2016 Accounts payable $15,000

Assessment Workbook – FNSACC504 10 | P a g e Version 3.0

To Office works $1650

b. 31st Jan 2016 Purchased motor vehicle at a cost $30,000 Registration of the motor

vehicle was $730 from Essendon Mazda plus GST

31.01.2016 Motor vehicle $30,730

To Office works $30,730

c. 14th Feb 2016 sold items to a customer for $7000 plus GST. Payment terms are 30

days after the purchase

14.02.2016 Accounts receivables $7,000

To Sales revenue $7,000

Payment after 30 days

14.03.2016 Cash $7,000

To Accounts receivables $7,000

d. 20/03/2016 Paid supplier of stock purchased in cash for $15000 plus GST

20.03.2016 Accounts payable $15,000

Assessment Workbook – FNSACC504 10 | P a g e Version 3.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To Cash $15,000

The objective of this section is to demonstrate 2.0 Prepare reports

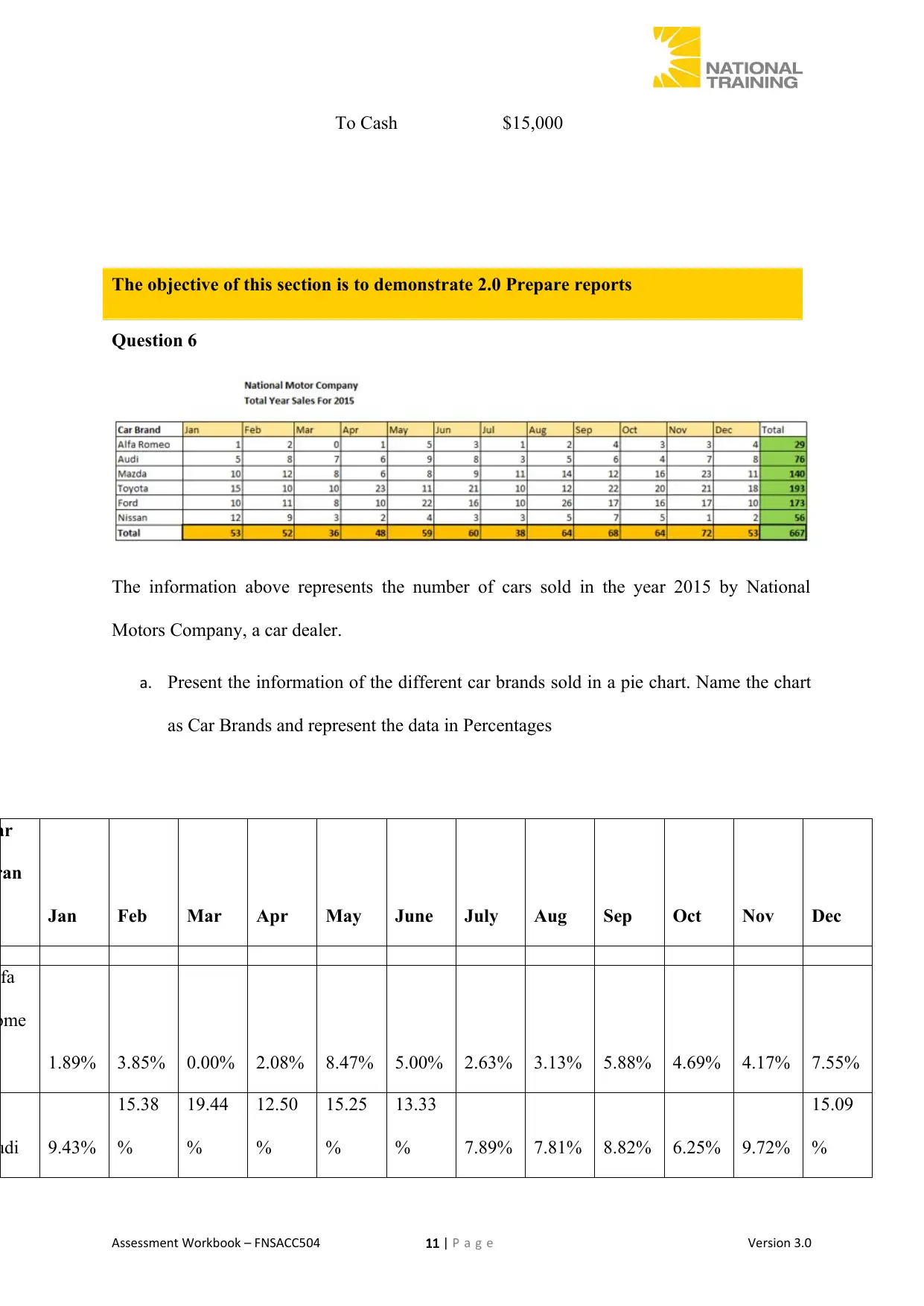

Question 6

The information above represents the number of cars sold in the year 2015 by National

Motors Company, a car dealer.

a. Present the information of the different car brands sold in a pie chart. Name the chart

as Car Brands and represent the data in Percentages

ar

ran

Jan Feb Mar Apr May June July Aug Sep Oct Nov Dec

lfa

ome

1.89% 3.85% 0.00% 2.08% 8.47% 5.00% 2.63% 3.13% 5.88% 4.69% 4.17% 7.55%

udi 9.43%

15.38

%

19.44

%

12.50

%

15.25

%

13.33

% 7.89% 7.81% 8.82% 6.25% 9.72%

15.09

%

Assessment Workbook – FNSACC504 11 | P a g e Version 3.0

The objective of this section is to demonstrate 2.0 Prepare reports

Question 6

The information above represents the number of cars sold in the year 2015 by National

Motors Company, a car dealer.

a. Present the information of the different car brands sold in a pie chart. Name the chart

as Car Brands and represent the data in Percentages

ar

ran

Jan Feb Mar Apr May June July Aug Sep Oct Nov Dec

lfa

ome

1.89% 3.85% 0.00% 2.08% 8.47% 5.00% 2.63% 3.13% 5.88% 4.69% 4.17% 7.55%

udi 9.43%

15.38

%

19.44

%

12.50

%

15.25

%

13.33

% 7.89% 7.81% 8.82% 6.25% 9.72%

15.09

%

Assessment Workbook – FNSACC504 11 | P a g e Version 3.0

azd 18.87

%

23.08

%

22.22

%

12.50

%

13.56

%

15.00

%

28.95

%

21.88

%

17.65

%

25.00

%

31.94

%

20.75

%

oyot 28.30

%

19.23

%

27.78

%

47.92

%

18.64

%

35.00

%

26.32

%

18.75

%

32.35

%

31.25

%

29.17

%

33.96

%

ord

18.87

%

21.15

%

22.22

%

20.83

%

37.29

%

26.67

%

26.32

%

40.63

%

25.00

%

25.00

%

23.61

%

18.87

%

issa 22.64

%

17.31

% 8.33% 4.17% 6.78% 5.00% 7.89% 7.81%

10.29

% 7.81% 1.39% 3.77%

otal 1 1 1 1 1 1 1 1 1 1 1 1

Save the workbook as workbook as activity 6 and submit it with this assessment

b. Present the monthly sales in a line graph to show the trend. Name the graph Monthly

sales

Car Brands

Alfa Romeo Audi Mazda Toyota Ford

Nissan

Assessment Workbook – FNSACC504 12 | P a g e Version 3.0

%

23.08

%

22.22

%

12.50

%

13.56

%

15.00

%

28.95

%

21.88

%

17.65

%

25.00

%

31.94

%

20.75

%

oyot 28.30

%

19.23

%

27.78

%

47.92

%

18.64

%

35.00

%

26.32

%

18.75

%

32.35

%

31.25

%

29.17

%

33.96

%

ord

18.87

%

21.15

%

22.22

%

20.83

%

37.29

%

26.67

%

26.32

%

40.63

%

25.00

%

25.00

%

23.61

%

18.87

%

issa 22.64

%

17.31

% 8.33% 4.17% 6.78% 5.00% 7.89% 7.81%

10.29

% 7.81% 1.39% 3.77%

otal 1 1 1 1 1 1 1 1 1 1 1 1

Save the workbook as workbook as activity 6 and submit it with this assessment

b. Present the monthly sales in a line graph to show the trend. Name the graph Monthly

sales

Car Brands

Alfa Romeo Audi Mazda Toyota Ford

Nissan

Assessment Workbook – FNSACC504 12 | P a g e Version 3.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.