Comprehensive Report on Managing Financial Resources in Business

VerifiedAdded on 2020/12/09

|13

|3524

|240

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, focusing on cost analysis, break-even points, and cash budgeting within the context of a UK-based company, New Horizons Accountants Ltd. The report begins with an introduction to financial resources and their importance, followed by a detailed examination of various cost types (fixed, variable, and semi-variable), and their impact on business operations. It also includes the use of a cost-volume-profit graph to illustrate the relationship between costs, volume, and profit, alongside the calculation of break-even points in both units and pound sterling for Beta Company. Furthermore, the report addresses the preparation of a cash budget for Alpha Ltd and explores the effects of changes in sales volume and costs on profitability and break-even points. The report concludes with a cash budget and a summary of the key findings.

MANAGING

FINANCIAL

RESOURCES

FINANCIAL

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1 A........................................................................................................................................3

1.Various types cost in a business...............................................................................................3

2. Use of cost volume profit graph..............................................................................................6

TASK 1 B........................................................................................................................................7

1. Break even point in unit and pound sterling...........................................................................7

2. CVP graph showing break even point.....................................................................................8

3. Income at desired sales 18500 units........................................................................................9

4. If managers is paid £6 per blouse, than effect on BEP:..........................................................9

5. Change in profit when selling 23500 units...........................................................................10

6. Change in BEP if salaries are increased by 214000..............................................................10

TASK 2..........................................................................................................................................10

1. Cash budget...........................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION ..........................................................................................................................3

TASK 1 A........................................................................................................................................3

1.Various types cost in a business...............................................................................................3

2. Use of cost volume profit graph..............................................................................................6

TASK 1 B........................................................................................................................................7

1. Break even point in unit and pound sterling...........................................................................7

2. CVP graph showing break even point.....................................................................................8

3. Income at desired sales 18500 units........................................................................................9

4. If managers is paid £6 per blouse, than effect on BEP:..........................................................9

5. Change in profit when selling 23500 units...........................................................................10

6. Change in BEP if salaries are increased by 214000..............................................................10

TASK 2..........................................................................................................................................10

1. Cash budget...........................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The financial resources are important part of organization and set of liquid assets of an

organization such as cash, liquid financial investment (stocks, bonds), short term bank deposits.

These resources are mostly using for move out to operate business operation like as buying

goods and services, and carry out long term investments. Managing financial resources involved

management of financial resources in organization prospective. It aims to provide terms and

techniques of accountancy to manager to easily understand of financial report sand communicate

about that. In this project the company taken is New Horizons accountants Ltd, which is related

to UK.

This project report included various tasks which are classify in types of costs with

examples, cost information on a cost volume profit graph, calculation of break even point in unit

and pound sterling of Beta Company, prepare cash budget of Alpha Ltd and cover all

adjustments in task.

TASK 1 A

1.Various types cost in a business

Cost - The word 'cost' means the sum of expenditure(actual or imaginary) incurred on

specified things or activity. It is a monetary amount that a company incurred in order to produce

goods and services. It is usually a monetary terms of resources, efforts, risk incurred, time and

utilities consumed, materials and possibility forgone in production or the goods and services

delivered. All expenditure are considered as a costs but all costs (such as which is obtained by

acquiring of an income- generating assets)are not considered as a expenditure. All this expenses

were recorded in bookkeeping records. For example, if we calculate the cost for preparing a

pizza, it itself incurred many other costs such as the flour cost, labor, other overheads. In the

same way , cost of production of any products or work as specified by the firm can be ascertain.

From the buyer's viewpoint, its is also called the price, it simply means that the amount which

the seller charges for the particular product. Cost is associated with factors of production such as

cost of capital, cost of labor, cost of a fixed assets. Cost of capital is measured in terms of

interest expenses which is specifically used to purchase the fixed assets. Cost of labor, which

were used to measured the remuneration and welfare basically used for manufacture of services

and goods. Cost of fixed assets, which measured in depreciation and were used for production.

The financial resources are important part of organization and set of liquid assets of an

organization such as cash, liquid financial investment (stocks, bonds), short term bank deposits.

These resources are mostly using for move out to operate business operation like as buying

goods and services, and carry out long term investments. Managing financial resources involved

management of financial resources in organization prospective. It aims to provide terms and

techniques of accountancy to manager to easily understand of financial report sand communicate

about that. In this project the company taken is New Horizons accountants Ltd, which is related

to UK.

This project report included various tasks which are classify in types of costs with

examples, cost information on a cost volume profit graph, calculation of break even point in unit

and pound sterling of Beta Company, prepare cash budget of Alpha Ltd and cover all

adjustments in task.

TASK 1 A

1.Various types cost in a business

Cost - The word 'cost' means the sum of expenditure(actual or imaginary) incurred on

specified things or activity. It is a monetary amount that a company incurred in order to produce

goods and services. It is usually a monetary terms of resources, efforts, risk incurred, time and

utilities consumed, materials and possibility forgone in production or the goods and services

delivered. All expenditure are considered as a costs but all costs (such as which is obtained by

acquiring of an income- generating assets)are not considered as a expenditure. All this expenses

were recorded in bookkeeping records. For example, if we calculate the cost for preparing a

pizza, it itself incurred many other costs such as the flour cost, labor, other overheads. In the

same way , cost of production of any products or work as specified by the firm can be ascertain.

From the buyer's viewpoint, its is also called the price, it simply means that the amount which

the seller charges for the particular product. Cost is associated with factors of production such as

cost of capital, cost of labor, cost of a fixed assets. Cost of capital is measured in terms of

interest expenses which is specifically used to purchase the fixed assets. Cost of labor, which

were used to measured the remuneration and welfare basically used for manufacture of services

and goods. Cost of fixed assets, which measured in depreciation and were used for production.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Elements of costs is categorised in three groups i.e. labour, expenses and material.

Labour: It is the essential elements of production. For the process of raw material into

the finished goods, there is the need of human resources as human resources is

considered as labour. It is basically classified in following two categories:

◦ Direct Labour, and

◦ Indirect labour

Expenses: The cost which are incurred to produce the finished goods except the labour

and the material costs is known as expenses. It is also classified into the followings:

◦ Indirect expenses (the overhead items ), and

◦ Direct expenses

Material: To produce or to manufacture anything material is necessary. All material are

the entire part of the finished products. The component by which the product were made

is material, it can be in a manufacture state or in a raw state. It is of two types:

◦ Direct material, and

◦ Indirect material

Types of cost:

Fixed cost: Fixed costs is the cost which is fixed it doesn't vary with the changes

occurred in the output. If there is variations in the output level no changes occurred in

the volume. Fixed cost also change, if the period of time is considered for the longer

period to modify the firms capability. With the variation in the production value than the

per unit of fixed cost will also vary accordingly. If the production decreases than the

fixed costs increases and if there is increase in production than fixed cost will decrease.

For Example- salary of employees, building rent, depreciation on plant and machinery,

building insurances. Sometimes fixed cost are considered as the overhead costs. Whether

the organisation produce 100 widgets or 10000 widgets it incurred. Depreciation, salaries

and rent were included in fixed assets when the budget of any firms were prepared and

also property taxes and insurances were enclosed in manufacturing overheads.

Variable cost: The cost were variable inputs were exploited is termed as variable costs.

These costs directly depends on the output they fluctuate with the changes occurred in

output level. During the process of production, the ratio between the output and variable

costs depends upon the resources and fixed facilities used in the firms. For example –

Labour: It is the essential elements of production. For the process of raw material into

the finished goods, there is the need of human resources as human resources is

considered as labour. It is basically classified in following two categories:

◦ Direct Labour, and

◦ Indirect labour

Expenses: The cost which are incurred to produce the finished goods except the labour

and the material costs is known as expenses. It is also classified into the followings:

◦ Indirect expenses (the overhead items ), and

◦ Direct expenses

Material: To produce or to manufacture anything material is necessary. All material are

the entire part of the finished products. The component by which the product were made

is material, it can be in a manufacture state or in a raw state. It is of two types:

◦ Direct material, and

◦ Indirect material

Types of cost:

Fixed cost: Fixed costs is the cost which is fixed it doesn't vary with the changes

occurred in the output. If there is variations in the output level no changes occurred in

the volume. Fixed cost also change, if the period of time is considered for the longer

period to modify the firms capability. With the variation in the production value than the

per unit of fixed cost will also vary accordingly. If the production decreases than the

fixed costs increases and if there is increase in production than fixed cost will decrease.

For Example- salary of employees, building rent, depreciation on plant and machinery,

building insurances. Sometimes fixed cost are considered as the overhead costs. Whether

the organisation produce 100 widgets or 10000 widgets it incurred. Depreciation, salaries

and rent were included in fixed assets when the budget of any firms were prepared and

also property taxes and insurances were enclosed in manufacturing overheads.

Variable cost: The cost were variable inputs were exploited is termed as variable costs.

These costs directly depends on the output they fluctuate with the changes occurred in

output level. During the process of production, the ratio between the output and variable

costs depends upon the resources and fixed facilities used in the firms. For example –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditure on labour, raw material cost, repair costs. Direct labour, direct material and

direct expense are also the examples of variable costs. Variable costs increases and

decreases according to the changes occurred in the volume of production. Let's take the

example of toys manufacturer - before shipping a toy manufacturer always packed the

product. It is considered as a variable costs, if the manufacturer manufacture more

products i.e. toys then the cost of packaging also increases. Yet if the manufacturer's

production level of toy decreases then the variable costs which is associated with the

packaging will also decrease. For an organisation variable cost is considered as the

financial impact when the services or products were delivered or produces.

Semi - variable cost: The costs which contains both the elements fixed costs as well as

the variable costs is known as semi- variable costs. Its is partially affected by the

variations occurred in the activity activity level. It is the cost , where some portion

remains fixed at the given production level and the other portion fluctuate with the

variations occurred in the mass of production but doesn't occurred in the same proportion

of the different production. For example - if the output of production is upto 50%,

expenses may not vary but if it may gain by 5% for all 20% gain in product over 50%

but up to 70%.

formula: By using the formula , semi- variable costs are separated into the variable costs

and fixed costs:

Semi- variable cost = Fixed cost + variable costs

Variable cost per unit = change in cost / change in output

2. Use of cost volume profit graph

Cost volume profit is a part of cost accounting and using for short run decision and

elementary instruction. Cost volume profit chart is a graphical representation of cost production

profit analysis. It is show relationship between produced volume units and produced cost units

like as fixed costs, total sales and total costs. After result management using this information for

calculate estimate budget and also for predict sales which is based on production schedules. If

projected sales are not met so manager using this graph for predict future losses. Through this

graph simply calculated break even analysis, target income sales. It also analysis of short run

investments in operational decisions. Role of CVP analysis is more in management accounting as

compared with financial accounting. With the help of this analysis, decision making process is

direct expense are also the examples of variable costs. Variable costs increases and

decreases according to the changes occurred in the volume of production. Let's take the

example of toys manufacturer - before shipping a toy manufacturer always packed the

product. It is considered as a variable costs, if the manufacturer manufacture more

products i.e. toys then the cost of packaging also increases. Yet if the manufacturer's

production level of toy decreases then the variable costs which is associated with the

packaging will also decrease. For an organisation variable cost is considered as the

financial impact when the services or products were delivered or produces.

Semi - variable cost: The costs which contains both the elements fixed costs as well as

the variable costs is known as semi- variable costs. Its is partially affected by the

variations occurred in the activity activity level. It is the cost , where some portion

remains fixed at the given production level and the other portion fluctuate with the

variations occurred in the mass of production but doesn't occurred in the same proportion

of the different production. For example - if the output of production is upto 50%,

expenses may not vary but if it may gain by 5% for all 20% gain in product over 50%

but up to 70%.

formula: By using the formula , semi- variable costs are separated into the variable costs

and fixed costs:

Semi- variable cost = Fixed cost + variable costs

Variable cost per unit = change in cost / change in output

2. Use of cost volume profit graph

Cost volume profit is a part of cost accounting and using for short run decision and

elementary instruction. Cost volume profit chart is a graphical representation of cost production

profit analysis. It is show relationship between produced volume units and produced cost units

like as fixed costs, total sales and total costs. After result management using this information for

calculate estimate budget and also for predict sales which is based on production schedules. If

projected sales are not met so manager using this graph for predict future losses. Through this

graph simply calculated break even analysis, target income sales. It also analysis of short run

investments in operational decisions. Role of CVP analysis is more in management accounting as

compared with financial accounting. With the help of this analysis, decision making process is

facilitated by companies. It can ascertain contribution margin. Elements of this analysis includes

cost associated with production and sales of goods, volume is the total number of units, and

profit which is the difference amount of selling price and production cost of goods and services.

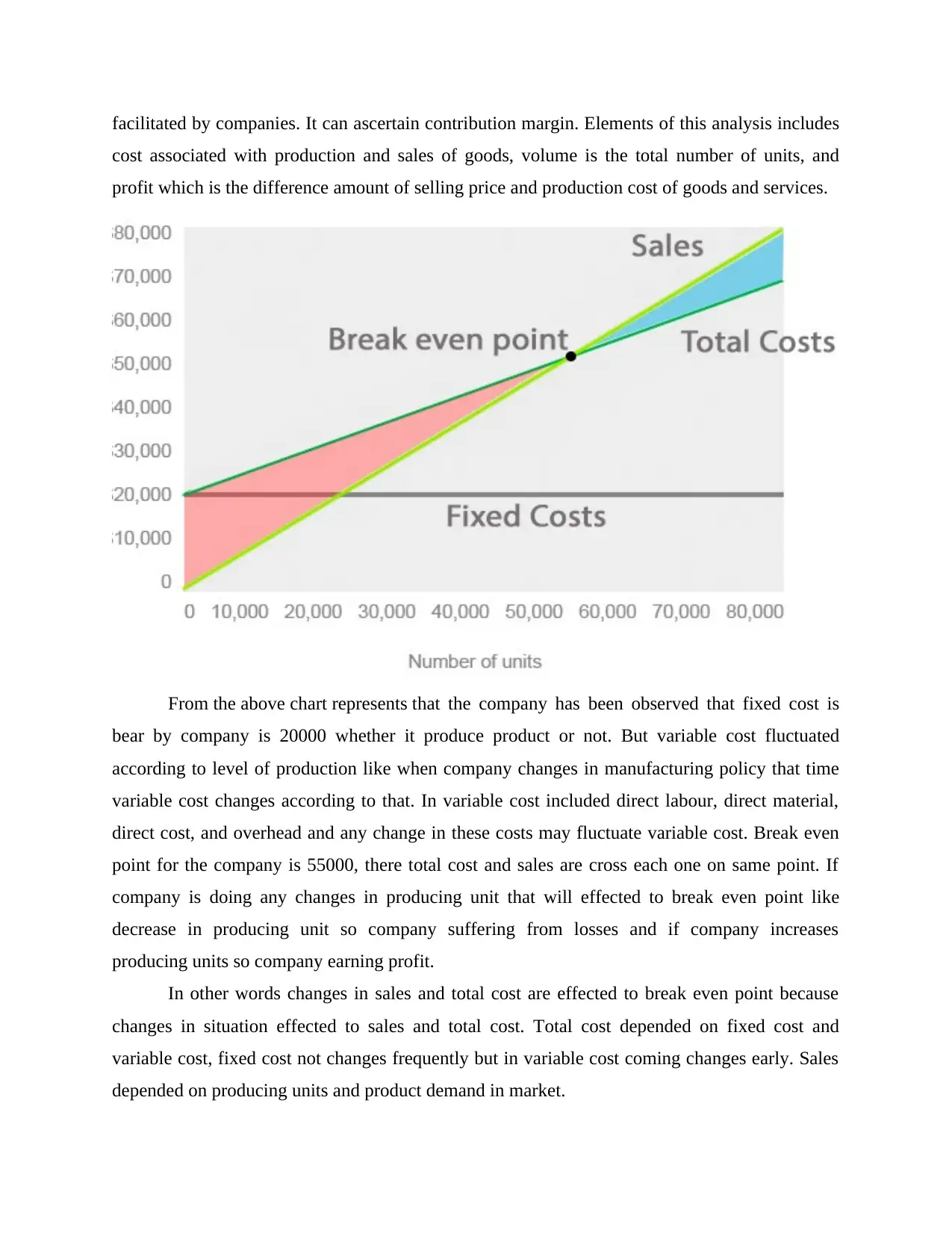

From the above chart represents that the company has been observed that fixed cost is

bear by company is 20000 whether it produce product or not. But variable cost fluctuated

according to level of production like when company changes in manufacturing policy that time

variable cost changes according to that. In variable cost included direct labour, direct material,

direct cost, and overhead and any change in these costs may fluctuate variable cost. Break even

point for the company is 55000, there total cost and sales are cross each one on same point. If

company is doing any changes in producing unit that will effected to break even point like

decrease in producing unit so company suffering from losses and if company increases

producing units so company earning profit.

In other words changes in sales and total cost are effected to break even point because

changes in situation effected to sales and total cost. Total cost depended on fixed cost and

variable cost, fixed cost not changes frequently but in variable cost coming changes early. Sales

depended on producing units and product demand in market.

cost associated with production and sales of goods, volume is the total number of units, and

profit which is the difference amount of selling price and production cost of goods and services.

From the above chart represents that the company has been observed that fixed cost is

bear by company is 20000 whether it produce product or not. But variable cost fluctuated

according to level of production like when company changes in manufacturing policy that time

variable cost changes according to that. In variable cost included direct labour, direct material,

direct cost, and overhead and any change in these costs may fluctuate variable cost. Break even

point for the company is 55000, there total cost and sales are cross each one on same point. If

company is doing any changes in producing unit that will effected to break even point like

decrease in producing unit so company suffering from losses and if company increases

producing units so company earning profit.

In other words changes in sales and total cost are effected to break even point because

changes in situation effected to sales and total cost. Total cost depended on fixed cost and

variable cost, fixed cost not changes frequently but in variable cost coming changes early. Sales

depended on producing units and product demand in market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1 B

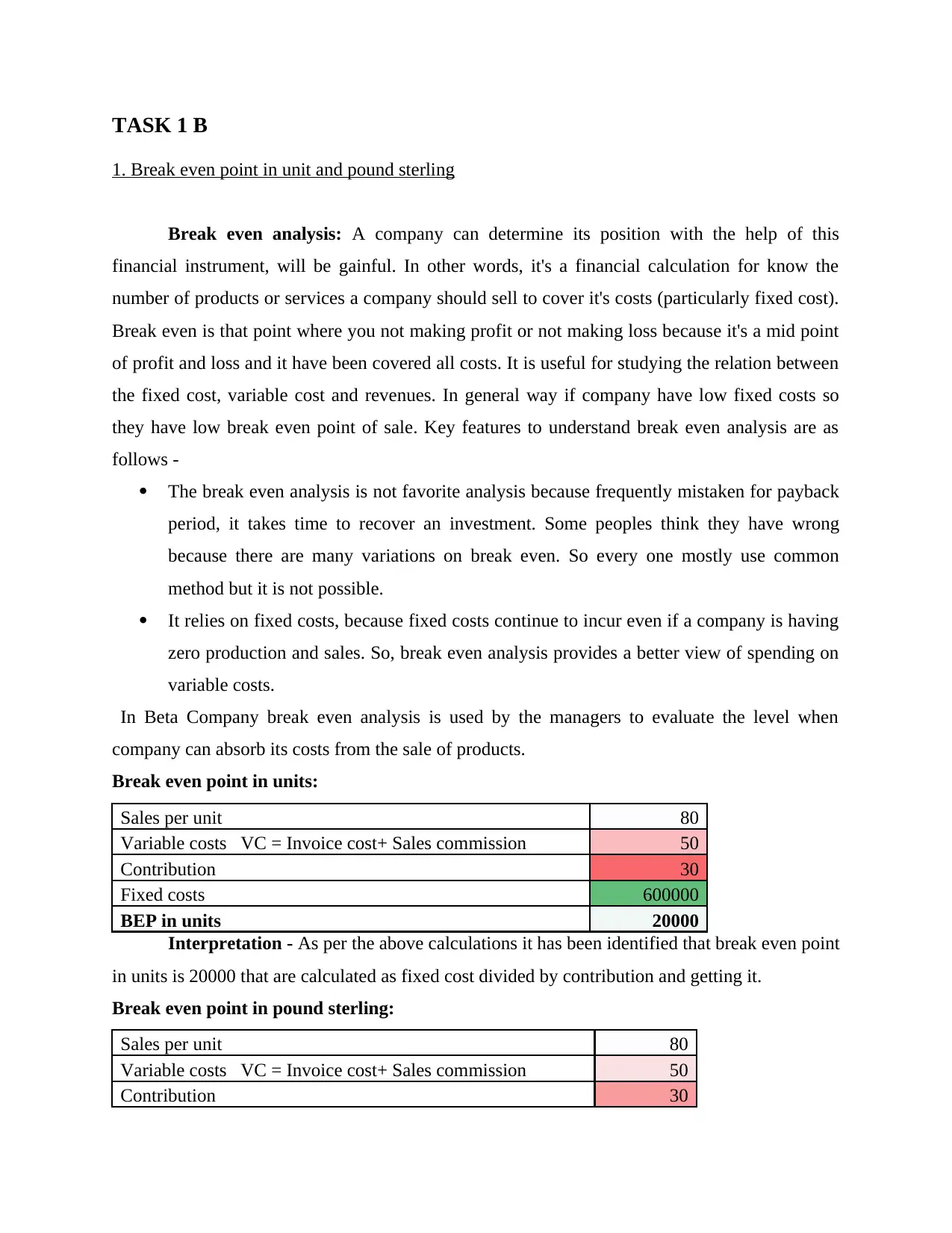

1. Break even point in unit and pound sterling

Break even analysis: A company can determine its position with the help of this

financial instrument, will be gainful. In other words, it's a financial calculation for know the

number of products or services a company should sell to cover it's costs (particularly fixed cost).

Break even is that point where you not making profit or not making loss because it's a mid point

of profit and loss and it have been covered all costs. It is useful for studying the relation between

the fixed cost, variable cost and revenues. In general way if company have low fixed costs so

they have low break even point of sale. Key features to understand break even analysis are as

follows -

The break even analysis is not favorite analysis because frequently mistaken for payback

period, it takes time to recover an investment. Some peoples think they have wrong

because there are many variations on break even. So every one mostly use common

method but it is not possible.

It relies on fixed costs, because fixed costs continue to incur even if a company is having

zero production and sales. So, break even analysis provides a better view of spending on

variable costs.

In Beta Company break even analysis is used by the managers to evaluate the level when

company can absorb its costs from the sale of products.

Break even point in units:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 50

Contribution 30

Fixed costs 600000

BEP in units 20000

Interpretation - As per the above calculations it has been identified that break even point

in units is 20000 that are calculated as fixed cost divided by contribution and getting it.

Break even point in pound sterling:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 50

Contribution 30

1. Break even point in unit and pound sterling

Break even analysis: A company can determine its position with the help of this

financial instrument, will be gainful. In other words, it's a financial calculation for know the

number of products or services a company should sell to cover it's costs (particularly fixed cost).

Break even is that point where you not making profit or not making loss because it's a mid point

of profit and loss and it have been covered all costs. It is useful for studying the relation between

the fixed cost, variable cost and revenues. In general way if company have low fixed costs so

they have low break even point of sale. Key features to understand break even analysis are as

follows -

The break even analysis is not favorite analysis because frequently mistaken for payback

period, it takes time to recover an investment. Some peoples think they have wrong

because there are many variations on break even. So every one mostly use common

method but it is not possible.

It relies on fixed costs, because fixed costs continue to incur even if a company is having

zero production and sales. So, break even analysis provides a better view of spending on

variable costs.

In Beta Company break even analysis is used by the managers to evaluate the level when

company can absorb its costs from the sale of products.

Break even point in units:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 50

Contribution 30

Fixed costs 600000

BEP in units 20000

Interpretation - As per the above calculations it has been identified that break even point

in units is 20000 that are calculated as fixed cost divided by contribution and getting it.

Break even point in pound sterling:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 50

Contribution 30

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed costs 600000

Profit volume ratio PVR = Contribution / sales * 100 37.50%

BEP in sales 1600000

Interpretation - From the above calculations in pound sterling it has been identified that

break even point in sales is 20000 units and sales unit is 160000 (80*20000). If the company

wants to recover all the costs so company have to sales at least 20000 blouses.

2. CVP graph showing break even point

The CVP graph is formulated with the help of following data:

Total units Total fixed Sells Profit

5000 600000 400000 -450000

10000 600000 800000 -300000

20000 600000 1600000 0

25000 600000 2000000 84000

30000 600000 2400000 300000

Interpretation - With the help of graph reflects that 20000 units are the BEP point of the

company where company do not getting profit and do not getting loss. If the company sells

blouses more than 20000 so company will be able to earn profit.

Profit volume ratio PVR = Contribution / sales * 100 37.50%

BEP in sales 1600000

Interpretation - From the above calculations in pound sterling it has been identified that

break even point in sales is 20000 units and sales unit is 160000 (80*20000). If the company

wants to recover all the costs so company have to sales at least 20000 blouses.

2. CVP graph showing break even point

The CVP graph is formulated with the help of following data:

Total units Total fixed Sells Profit

5000 600000 400000 -450000

10000 600000 800000 -300000

20000 600000 1600000 0

25000 600000 2000000 84000

30000 600000 2400000 300000

Interpretation - With the help of graph reflects that 20000 units are the BEP point of the

company where company do not getting profit and do not getting loss. If the company sells

blouses more than 20000 so company will be able to earn profit.

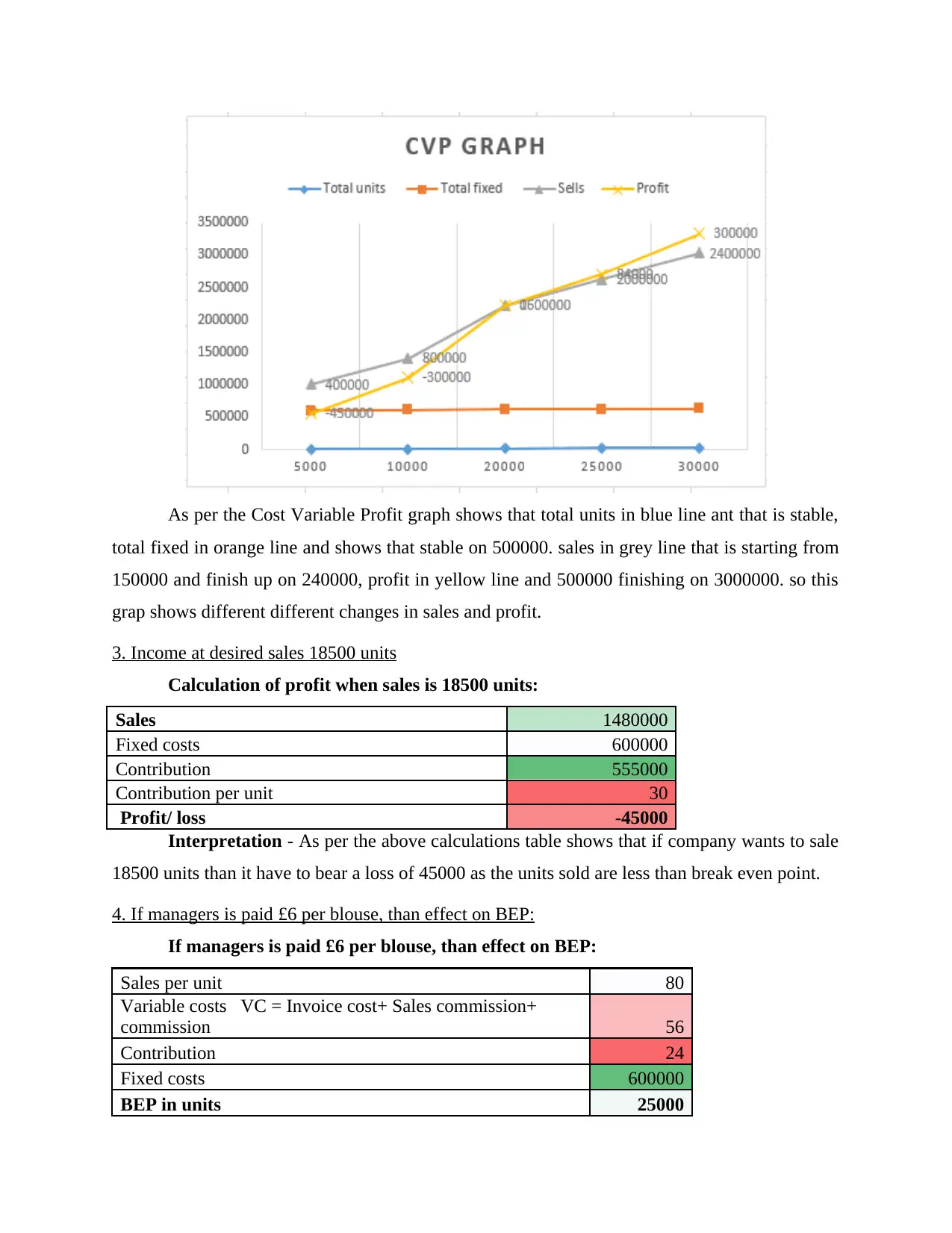

As per the Cost Variable Profit graph shows that total units in blue line ant that is stable,

total fixed in orange line and shows that stable on 500000. sales in grey line that is starting from

150000 and finish up on 240000, profit in yellow line and 500000 finishing on 3000000. so this

grap shows different different changes in sales and profit.

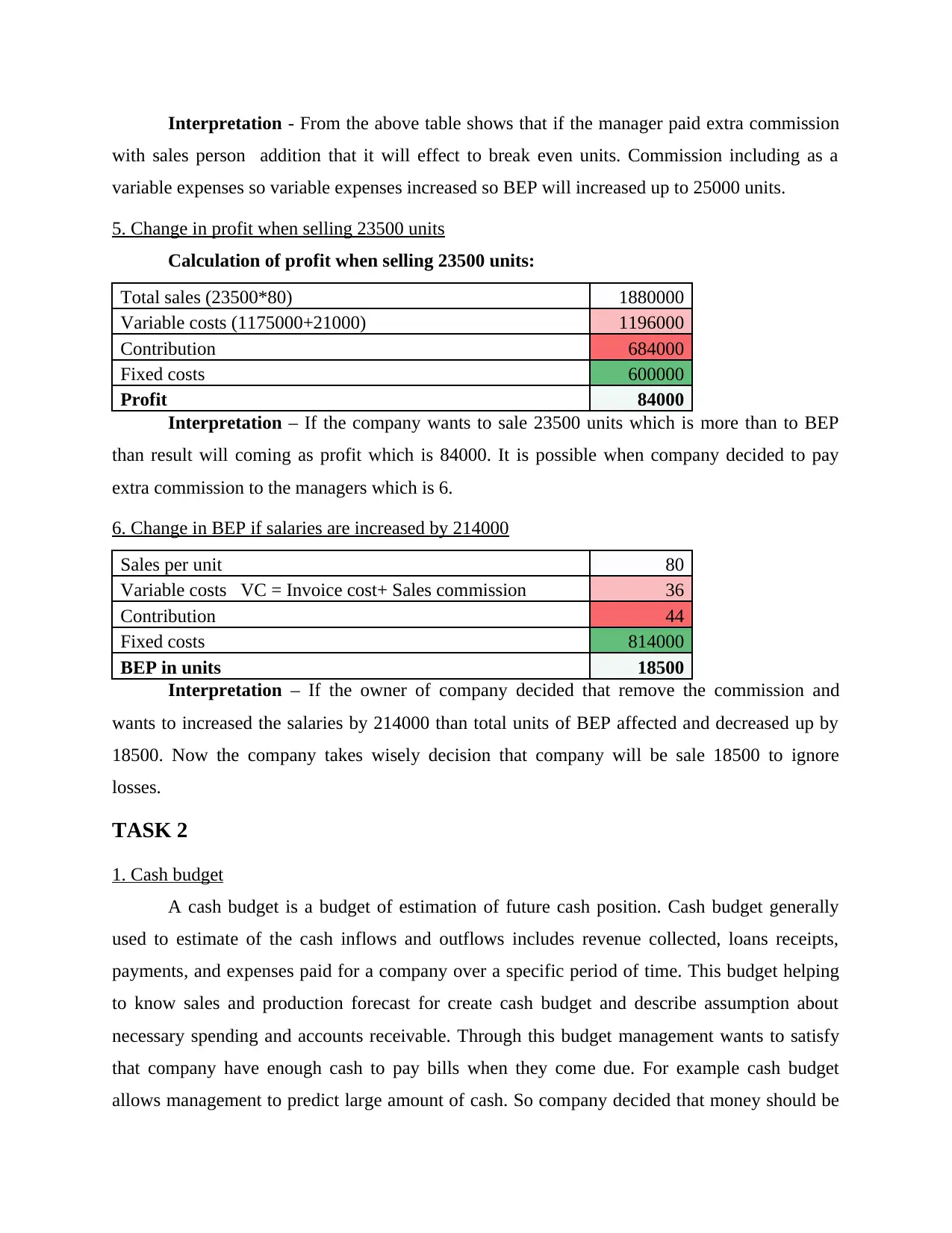

3. Income at desired sales 18500 units

Calculation of profit when sales is 18500 units:

Sales 1480000

Fixed costs 600000

Contribution 555000

Contribution per unit 30

Profit/ loss -45000

Interpretation - As per the above calculations table shows that if company wants to sale

18500 units than it have to bear a loss of 45000 as the units sold are less than break even point.

4. If managers is paid £6 per blouse, than effect on BEP:

If managers is paid £6 per blouse, than effect on BEP:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission+

commission 56

Contribution 24

Fixed costs 600000

BEP in units 25000

total fixed in orange line and shows that stable on 500000. sales in grey line that is starting from

150000 and finish up on 240000, profit in yellow line and 500000 finishing on 3000000. so this

grap shows different different changes in sales and profit.

3. Income at desired sales 18500 units

Calculation of profit when sales is 18500 units:

Sales 1480000

Fixed costs 600000

Contribution 555000

Contribution per unit 30

Profit/ loss -45000

Interpretation - As per the above calculations table shows that if company wants to sale

18500 units than it have to bear a loss of 45000 as the units sold are less than break even point.

4. If managers is paid £6 per blouse, than effect on BEP:

If managers is paid £6 per blouse, than effect on BEP:

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission+

commission 56

Contribution 24

Fixed costs 600000

BEP in units 25000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation - From the above table shows that if the manager paid extra commission

with sales person addition that it will effect to break even units. Commission including as a

variable expenses so variable expenses increased so BEP will increased up to 25000 units.

5. Change in profit when selling 23500 units

Calculation of profit when selling 23500 units:

Total sales (23500*80) 1880000

Variable costs (1175000+21000) 1196000

Contribution 684000

Fixed costs 600000

Profit 84000

Interpretation – If the company wants to sale 23500 units which is more than to BEP

than result will coming as profit which is 84000. It is possible when company decided to pay

extra commission to the managers which is 6.

6. Change in BEP if salaries are increased by 214000

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 36

Contribution 44

Fixed costs 814000

BEP in units 18500

Interpretation – If the owner of company decided that remove the commission and

wants to increased the salaries by 214000 than total units of BEP affected and decreased up by

18500. Now the company takes wisely decision that company will be sale 18500 to ignore

losses.

TASK 2

1. Cash budget

A cash budget is a budget of estimation of future cash position. Cash budget generally

used to estimate of the cash inflows and outflows includes revenue collected, loans receipts,

payments, and expenses paid for a company over a specific period of time. This budget helping

to know sales and production forecast for create cash budget and describe assumption about

necessary spending and accounts receivable. Through this budget management wants to satisfy

that company have enough cash to pay bills when they come due. For example cash budget

allows management to predict large amount of cash. So company decided that money should be

with sales person addition that it will effect to break even units. Commission including as a

variable expenses so variable expenses increased so BEP will increased up to 25000 units.

5. Change in profit when selling 23500 units

Calculation of profit when selling 23500 units:

Total sales (23500*80) 1880000

Variable costs (1175000+21000) 1196000

Contribution 684000

Fixed costs 600000

Profit 84000

Interpretation – If the company wants to sale 23500 units which is more than to BEP

than result will coming as profit which is 84000. It is possible when company decided to pay

extra commission to the managers which is 6.

6. Change in BEP if salaries are increased by 214000

Sales per unit 80

Variable costs VC = Invoice cost+ Sales commission 36

Contribution 44

Fixed costs 814000

BEP in units 18500

Interpretation – If the owner of company decided that remove the commission and

wants to increased the salaries by 214000 than total units of BEP affected and decreased up by

18500. Now the company takes wisely decision that company will be sale 18500 to ignore

losses.

TASK 2

1. Cash budget

A cash budget is a budget of estimation of future cash position. Cash budget generally

used to estimate of the cash inflows and outflows includes revenue collected, loans receipts,

payments, and expenses paid for a company over a specific period of time. This budget helping

to know sales and production forecast for create cash budget and describe assumption about

necessary spending and accounts receivable. Through this budget management wants to satisfy

that company have enough cash to pay bills when they come due. For example cash budget

allows management to predict large amount of cash. So company decided that money should be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

invested to earn interest on this amount. Excess cash better used to expand and develop new

operations for company accounts. After that management predict to cash levels of the company.

In Alpha Ltd. Accountant prepare cash budget which is based on assumptions and

previous year's data to get the information of account receivable and money spend. It is a

summary of all the month's cash transactions information. In cash budget through giving all

information to owner and manager. It is an estimation of current and future position of the

company and describe financial strength.

Cash budget for Alpha Ltd:

Particular January February March

Receipts

Cash Sales 75 80 90

Collection from credit sales 300 285 282

Total (a) 375 365 372

Payment

Payment for credit purchase 180 196 200

Operating cost 122 123 123

Payment for vehicle 100

Total (b) 302 419 323

Net Receipt payment (a-b) 73 -54 49

Cash Balance at start 25 48 -102

Cash Balance at end 48 -102 151

Credit Sales

January – 75% value of December+ 15% value of November + 10% value of October

= 300*75% + 300*15% + 300*10%

= 225 + 45 + 30 = 300

February - 75% value of January + 15% value of December + 10% value of November

= 280*75% + 300*15% + 300*10%

operations for company accounts. After that management predict to cash levels of the company.

In Alpha Ltd. Accountant prepare cash budget which is based on assumptions and

previous year's data to get the information of account receivable and money spend. It is a

summary of all the month's cash transactions information. In cash budget through giving all

information to owner and manager. It is an estimation of current and future position of the

company and describe financial strength.

Cash budget for Alpha Ltd:

Particular January February March

Receipts

Cash Sales 75 80 90

Collection from credit sales 300 285 282

Total (a) 375 365 372

Payment

Payment for credit purchase 180 196 200

Operating cost 122 123 123

Payment for vehicle 100

Total (b) 302 419 323

Net Receipt payment (a-b) 73 -54 49

Cash Balance at start 25 48 -102

Cash Balance at end 48 -102 151

Credit Sales

January – 75% value of December+ 15% value of November + 10% value of October

= 300*75% + 300*15% + 300*10%

= 225 + 45 + 30 = 300

February - 75% value of January + 15% value of December + 10% value of November

= 280*75% + 300*15% + 300*10%

= 210 + 45 + 30 = 285

March - 75% value of February + 15% value of January + 10% value of December

= 280*75% + 280*15% + 300*10%

= 210 + 42 + 30 = 282

Credit purchase

January – 80% value of December + 20% value of November

= 180*80% + 180*20*

= 144 + 36 = 180

February - 80% value of January + 20% value of December

= 200*80% + 180*20%

= 160 + 36 = 196

March - 80% value of February + 20% value of January

= 200*80% + 200*20%

= 160 + 40 = 200

After the estimation of cash budget of Alpha Ltd. It has been analyzed that company

having profit at the end of January month which is 48, and in month of February is company

excruciating from a loss of 102, and in month of march the company earning profit are 151. It is

the because the company is selling goods on credit to the clients and not getting cash on timing

from the clients and buying on credit from seller. The loss in month of February is because of

payment of vehicle.

CONCLUSION

All the above report summarizing that financial resources major part of business that

provided liquidity to an organization. It is require for start up, established and run for business.

In business knows different different types cost like as variable, fixed or semi variable that are

effected to business. These cost are core part of business and know that which element are

related to cost. Cost volume profit graph describe that cost related to total cost, variable cost and

fixed cost. A company conduct a break even analysis and calculate of BEP in units which shows

the level of sales and the company covered all expenses and cost are occur in manufacturing

process. In this situation company earn no profit or no loss. Estimate cash budget is using for

future period and know level of cash.

March - 75% value of February + 15% value of January + 10% value of December

= 280*75% + 280*15% + 300*10%

= 210 + 42 + 30 = 282

Credit purchase

January – 80% value of December + 20% value of November

= 180*80% + 180*20*

= 144 + 36 = 180

February - 80% value of January + 20% value of December

= 200*80% + 180*20%

= 160 + 36 = 196

March - 80% value of February + 20% value of January

= 200*80% + 200*20%

= 160 + 40 = 200

After the estimation of cash budget of Alpha Ltd. It has been analyzed that company

having profit at the end of January month which is 48, and in month of February is company

excruciating from a loss of 102, and in month of march the company earning profit are 151. It is

the because the company is selling goods on credit to the clients and not getting cash on timing

from the clients and buying on credit from seller. The loss in month of February is because of

payment of vehicle.

CONCLUSION

All the above report summarizing that financial resources major part of business that

provided liquidity to an organization. It is require for start up, established and run for business.

In business knows different different types cost like as variable, fixed or semi variable that are

effected to business. These cost are core part of business and know that which element are

related to cost. Cost volume profit graph describe that cost related to total cost, variable cost and

fixed cost. A company conduct a break even analysis and calculate of BEP in units which shows

the level of sales and the company covered all expenses and cost are occur in manufacturing

process. In this situation company earn no profit or no loss. Estimate cash budget is using for

future period and know level of cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.