Financial Resource Decision Making and Financial Statement Analysis

VerifiedAdded on 2020/01/28

|15

|4233

|340

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, crucial for the success of small and medium-sized businesses. It begins by identifying various sources of finance, such as bank loans, overdrafts, personal savings, asset sales, and leasing, along with their implications for a retail business. The report then emphasizes the significance of financial planning, including budgeting and cost analysis, and discusses the information needs of internal and external stakeholders. Furthermore, it examines the impact of financial sources on financial statements and delves into investment appraisal techniques, like payback period, to assess project viability. The report uses a scenario involving a retail business seeking a franchise contract to illustrate these concepts, providing practical insights into financial decision-making.

MANAGING

FINANCIAL

RESOURCE DECISION

FINANCIAL

RESOURCE DECISION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION .....................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Identify the sources of finance available to business................................................1

AC 1.2 Implication of finance sources..................................................................................2

AC 1.3 Most appropriate finance source for the business ....................................................2

AC 2.1 Cost of each identified finance sources.....................................................................3

AC 2.2 Importance of financial planning..............................................................................3

AC 2.3 Information needs of internal and external decision makers....................................4

AC 2.4 Impact of financial sources in the financial statements............................................4

AC 3.1 Forecasted budget for six months.............................................................................5

AC 3.2 Calculation of unit cost.............................................................................................5

AC 3.3 Investment appraisal techniques...............................................................................6

TASK 2......................................................................................................................................8

AC 4.1 Discussion of main financial statements...................................................................8

AC 4.2 Main financial statement of different types of business...........................................8

AC 4.3 Interpreting the financial statements.........................................................................9

CONCLUSION .......................................................................................................................10

REFERENCES.........................................................................................................................12

INTRODUCTION .....................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Identify the sources of finance available to business................................................1

AC 1.2 Implication of finance sources..................................................................................2

AC 1.3 Most appropriate finance source for the business ....................................................2

AC 2.1 Cost of each identified finance sources.....................................................................3

AC 2.2 Importance of financial planning..............................................................................3

AC 2.3 Information needs of internal and external decision makers....................................4

AC 2.4 Impact of financial sources in the financial statements............................................4

AC 3.1 Forecasted budget for six months.............................................................................5

AC 3.2 Calculation of unit cost.............................................................................................5

AC 3.3 Investment appraisal techniques...............................................................................6

TASK 2......................................................................................................................................8

AC 4.1 Discussion of main financial statements...................................................................8

AC 4.2 Main financial statement of different types of business...........................................8

AC 4.3 Interpreting the financial statements.........................................................................9

CONCLUSION .......................................................................................................................10

REFERENCES.........................................................................................................................12

INTRODUCTION

Finance plays a crucial role in the businesses. Every small and medium sized

organization needs adequate availability of financial resources to operate successfully in the

market. Moreover, firms do not require generating sufficient funds only they need to manage

it in an efficient way. The present project report will provide assistance to determine the

finance sources available to small and medium sized businesses with their implications.

Furthermore, it will discuss the role of financial plans in the finance management. In addition

to it, budgetary tools, investment appraisal techniques, unit cost and financial statement

analysis will be discussed in order to take good managerial decisions.

TASK 1

AC 1.1 Identify the sources of finance available to business

The scenario depicts that government intends to spend 1£ in every £3 with the small

businesses thus, it is a big opportunity for small firms. According to it, firms who employed

250 employees or less is known as SME. There is a great opportunity for the growth of small

scale retail business in UK, and the decided contract is to get the franchise of Dunkin

Doughnuts. The scenario indicates that available funds to the retail business is 20000£ with a

maximum contract bid price to 300000£. Therefore, additional finance sources available to

retail business are explained below:

Bank Loans: Financial institutions such as banks provide funds for different time

durations at an implied interest rate. Borrowing funds through banks helps to generate large

amount of finance for the small scale retail business (Brealey and et.al, 2012). It is an

external source of finance and fulfils the need of financial resources to a great extent.

Bank overdraft: Overdraft is a facility that allows users to withdraw higher funds than

available in bank balance. It provides assistance to fulfil immediate fund’s requirement of

retail organization. Bank charges interest on this facility whose rate is comparatively higher

than loan interest rate.

Personal savings: It is a cheaper source of finance for SME as available at lower cost.

Firm owners can use their personal savings for business purpose. Moreover, it helps to

maximize entrepreneur control on the business.

Sales of assets: Unused business assets can be disposed off in the market for getting

required amount of funds. It is a short term finance source and helps to acquire funds up to a

limited extent.

1 | P a g e

Finance plays a crucial role in the businesses. Every small and medium sized

organization needs adequate availability of financial resources to operate successfully in the

market. Moreover, firms do not require generating sufficient funds only they need to manage

it in an efficient way. The present project report will provide assistance to determine the

finance sources available to small and medium sized businesses with their implications.

Furthermore, it will discuss the role of financial plans in the finance management. In addition

to it, budgetary tools, investment appraisal techniques, unit cost and financial statement

analysis will be discussed in order to take good managerial decisions.

TASK 1

AC 1.1 Identify the sources of finance available to business

The scenario depicts that government intends to spend 1£ in every £3 with the small

businesses thus, it is a big opportunity for small firms. According to it, firms who employed

250 employees or less is known as SME. There is a great opportunity for the growth of small

scale retail business in UK, and the decided contract is to get the franchise of Dunkin

Doughnuts. The scenario indicates that available funds to the retail business is 20000£ with a

maximum contract bid price to 300000£. Therefore, additional finance sources available to

retail business are explained below:

Bank Loans: Financial institutions such as banks provide funds for different time

durations at an implied interest rate. Borrowing funds through banks helps to generate large

amount of finance for the small scale retail business (Brealey and et.al, 2012). It is an

external source of finance and fulfils the need of financial resources to a great extent.

Bank overdraft: Overdraft is a facility that allows users to withdraw higher funds than

available in bank balance. It provides assistance to fulfil immediate fund’s requirement of

retail organization. Bank charges interest on this facility whose rate is comparatively higher

than loan interest rate.

Personal savings: It is a cheaper source of finance for SME as available at lower cost.

Firm owners can use their personal savings for business purpose. Moreover, it helps to

maximize entrepreneur control on the business.

Sales of assets: Unused business assets can be disposed off in the market for getting

required amount of funds. It is a short term finance source and helps to acquire funds up to a

limited extent.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lease: Small scale retail sector companies can acquire fixed business assets on lease

without purchasing them. Firms have to pay rental charges periodically for using assets.

Thus, with the instalment payments, interest charges are also required to pay to the lessor.

AC 1.2 Implication of finance sources

Bank loans: Retail organization needs to pay interest charge at a fixed time interval.

Moreover, entrepreneur has to keep a security against the borrowed funds (Brush, Edelman

and Manolova, 2015). They have to fulfil all the legal formalities as per the bank

requirement. Another implication is that in case of any default in payments, banks have legal

right to dispose off the security in order to generate loan liabilities of the entrepreneur.

Overdraft: The implication of overdraft is that enterprises need to pay off the interest

on the taken overdraft. Bank charges normally high rate of interest on overdraft as compare to

loans. Furthermore, the facility is available up to a limited extent. Continuous bank overdraft

in the balance sheet affects company's image in a negative way.

Personal savings: Business owner can use their personal savings in the firm. The

implication is that it helps to maintain owner’s control on the firm. The reason behind is that

it reduces the amount of external borrowings.

Sale of assets: Retail organization has to make some expenditure in order to sale

assets in the market. It includes the expenses of attorney, advertisement and removal of assets

from the factories.

Lease: Small and medium sized retail business owner has to pay hire or rental charges

on the timely basis. Furthermore, the ownership is not transferred as firms do not purchase

those assets. In addition to it, if, enterprises do not paid their liabilities timely than asset’s

owner has legal right to get back the fixed assets from the lessee.

AC 1.3 Most appropriate finance source for the business

On the basis of above implications, it can be reported that bank loans will be the most

appropriate finance source for the retail business. The reason behind choosing such source is

that bank provides funds for short-term, medium-term and long term as per the financial

requirement. Moreover, loans can be generated through providing collateral security.

Another, it does not diversify business control to the lenders from the entrepreneurs (Rao,

2010). Furthermore, through making regular payment of interest and instalment, company

can discharge its loan’s liabilities on maturity date. Another most important benefit of

choosing bank loans is that retail sector organizations will be provided taxation relief on the

interest payments. This in turn helps to get tax benefits and maximize profitability.

2 | P a g e

without purchasing them. Firms have to pay rental charges periodically for using assets.

Thus, with the instalment payments, interest charges are also required to pay to the lessor.

AC 1.2 Implication of finance sources

Bank loans: Retail organization needs to pay interest charge at a fixed time interval.

Moreover, entrepreneur has to keep a security against the borrowed funds (Brush, Edelman

and Manolova, 2015). They have to fulfil all the legal formalities as per the bank

requirement. Another implication is that in case of any default in payments, banks have legal

right to dispose off the security in order to generate loan liabilities of the entrepreneur.

Overdraft: The implication of overdraft is that enterprises need to pay off the interest

on the taken overdraft. Bank charges normally high rate of interest on overdraft as compare to

loans. Furthermore, the facility is available up to a limited extent. Continuous bank overdraft

in the balance sheet affects company's image in a negative way.

Personal savings: Business owner can use their personal savings in the firm. The

implication is that it helps to maintain owner’s control on the firm. The reason behind is that

it reduces the amount of external borrowings.

Sale of assets: Retail organization has to make some expenditure in order to sale

assets in the market. It includes the expenses of attorney, advertisement and removal of assets

from the factories.

Lease: Small and medium sized retail business owner has to pay hire or rental charges

on the timely basis. Furthermore, the ownership is not transferred as firms do not purchase

those assets. In addition to it, if, enterprises do not paid their liabilities timely than asset’s

owner has legal right to get back the fixed assets from the lessee.

AC 1.3 Most appropriate finance source for the business

On the basis of above implications, it can be reported that bank loans will be the most

appropriate finance source for the retail business. The reason behind choosing such source is

that bank provides funds for short-term, medium-term and long term as per the financial

requirement. Moreover, loans can be generated through providing collateral security.

Another, it does not diversify business control to the lenders from the entrepreneurs (Rao,

2010). Furthermore, through making regular payment of interest and instalment, company

can discharge its loan’s liabilities on maturity date. Another most important benefit of

choosing bank loans is that retail sector organizations will be provided taxation relief on the

interest payments. This in turn helps to get tax benefits and maximize profitability.

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC 2.1 Cost of each identified finance sources

Bank Loans: Small and Medium sized retail business owner has to pay periodically

interest plus instalment charges on borrowed funds. The interest rate has been decided

according to the loan amount and time required.

Overdraft: On the extent of amount withdrawn, entrepreneur requires to pay interest

charges. The overdraft interest rate is comparatively higher than loan interest rate.

Sales of assets: Efforts that have been taken place to sale assets in the market will

include in the cost. It involves attorney fees, permits and the charges paid to remove assets

from the service.

Personal savings: It does not impose any fixed cost to the business owner. However,

opportunity cost includes in personal savings. For instance: if, owner does not invest their

personal savings then he can invest it for an alternative purpose and generate return on it

(Durst and Wilhelm, 2012). Thus, loss of return on alternative investment will also be the

cost of personal savings.

Lease: The amount of rental charges is considered as the cost of lease. Moreover,

instalment charges include interest imposed cost to the entrepreneur of small scale retail

business.

AC 2.2 Importance of financial planning

In the present complex business environment, financial planning is very important for

all SMEs. It is the process of assessing the financial needs and fulfils them in an exact

manner. Collection of funds at lower the cost implied lower the financial cost to the

companies. In context to retail sector, it helps to achieve the financial objectives of the

enterprise. Financial planner plays a major role in making financial plans. It forecast the

future incomes of various divisions and departments and allocates them in the operating

functions in an appropriate manner (Hin, Kadir and Bohari, 2013). It mainly aims at

managing the company's funds in an effective way. Budget is one of the most important

financial planning tool that forecast probable incomes and expenditures for the future period.

The main aim of it is to achieve set business targets through maximizing the company's

revenues and controlling the business expenditures. It provide assistance to retail sector

organizations to ensure optimum and maximum allocation of resources in operating activities

such as rent and other utilities. This in turn, funds can be managed in an effective manner

(Muller, 2012). Moreover, it helps to make better investment plans and managing the risk for

3 | P a g e

Bank Loans: Small and Medium sized retail business owner has to pay periodically

interest plus instalment charges on borrowed funds. The interest rate has been decided

according to the loan amount and time required.

Overdraft: On the extent of amount withdrawn, entrepreneur requires to pay interest

charges. The overdraft interest rate is comparatively higher than loan interest rate.

Sales of assets: Efforts that have been taken place to sale assets in the market will

include in the cost. It involves attorney fees, permits and the charges paid to remove assets

from the service.

Personal savings: It does not impose any fixed cost to the business owner. However,

opportunity cost includes in personal savings. For instance: if, owner does not invest their

personal savings then he can invest it for an alternative purpose and generate return on it

(Durst and Wilhelm, 2012). Thus, loss of return on alternative investment will also be the

cost of personal savings.

Lease: The amount of rental charges is considered as the cost of lease. Moreover,

instalment charges include interest imposed cost to the entrepreneur of small scale retail

business.

AC 2.2 Importance of financial planning

In the present complex business environment, financial planning is very important for

all SMEs. It is the process of assessing the financial needs and fulfils them in an exact

manner. Collection of funds at lower the cost implied lower the financial cost to the

companies. In context to retail sector, it helps to achieve the financial objectives of the

enterprise. Financial planner plays a major role in making financial plans. It forecast the

future incomes of various divisions and departments and allocates them in the operating

functions in an appropriate manner (Hin, Kadir and Bohari, 2013). It mainly aims at

managing the company's funds in an effective way. Budget is one of the most important

financial planning tool that forecast probable incomes and expenditures for the future period.

The main aim of it is to achieve set business targets through maximizing the company's

revenues and controlling the business expenditures. It provide assistance to retail sector

organizations to ensure optimum and maximum allocation of resources in operating activities

such as rent and other utilities. This in turn, funds can be managed in an effective manner

(Muller, 2012). Moreover, it helps to make better investment plans and managing the risk for

3 | P a g e

the retail sector. Thus, it is clear that efficient financial planning greatly contributes towards

strengthen the financial position of the retail business.

AC 2.3 Information needs of internal and external decision makers

Different decision makers need distinct information to meet their purpose. In context

to retail sector, managers as an internal users need information about the company's

performance. They measure business profitability and financial strength in order to take good

managerial decisions and make business growth. They are responsible for running the

operating functions without any difficulties. They make proper administration of business

resources, reduce operational and financial risks and run business successfully (Cassar, Ittner

and Cavalluzzo, 2015). On contrary, external stakeholders includes outsiders of the

organizations such as suppliers, investors and lenders. Suppliers who provide goods to the

retail business are interested to know the liquidity position. They measure the business ability

to pay the short-term liabilities to secure their funds. Investors make invest in the funds thus;

they measure business profitability and financial growth to ensure their return. On contrary,

lenders also lend money to the retail organization thus; they measure the solvency position of

the company. They determine their funds security, minimize risk and getting the payments at

right time (Power, Sharda, and Burstein, 2015). Moreover, they measure the business

earnings capacity and performance to take better lending decisions.

AC 2.4 Impact of financial sources in the financial statements

Financial statements include profitability statement and statement of financial

position. Small scale retail entrepreneur prepares these statements in order to assess the

operational and financial performance. Thus, the used financial source will be shows in the

financial statements and impact the business profits and financial status.

In balance sheet, the amount of borrowed funds will be show in the liability side and

raise the cash availability. Thus, it increases the business current assets and long term

liabilities. However, in profit and loss account, interest payment will be shows as

expenditures and decrease profitability. Further, it reduces the cash balance of the company.

Another, overdraft will enhance the current liabilities and cash balance in the business and

interest on overdraft is an expenses hence, shows in profit and loss account and reduce

profitability (Cowling, Liu and Ledger, 2012). Further, sales of assets will results in lowering

the retail company's assets and improve the cash balance. Further, the profits or loss on sales

will be show as income or expenses in profit and loss account. Personal savings investment

will increase the equity and cash balance. Thus, both the assets and liabilities will be

4 | P a g e

strengthen the financial position of the retail business.

AC 2.3 Information needs of internal and external decision makers

Different decision makers need distinct information to meet their purpose. In context

to retail sector, managers as an internal users need information about the company's

performance. They measure business profitability and financial strength in order to take good

managerial decisions and make business growth. They are responsible for running the

operating functions without any difficulties. They make proper administration of business

resources, reduce operational and financial risks and run business successfully (Cassar, Ittner

and Cavalluzzo, 2015). On contrary, external stakeholders includes outsiders of the

organizations such as suppliers, investors and lenders. Suppliers who provide goods to the

retail business are interested to know the liquidity position. They measure the business ability

to pay the short-term liabilities to secure their funds. Investors make invest in the funds thus;

they measure business profitability and financial growth to ensure their return. On contrary,

lenders also lend money to the retail organization thus; they measure the solvency position of

the company. They determine their funds security, minimize risk and getting the payments at

right time (Power, Sharda, and Burstein, 2015). Moreover, they measure the business

earnings capacity and performance to take better lending decisions.

AC 2.4 Impact of financial sources in the financial statements

Financial statements include profitability statement and statement of financial

position. Small scale retail entrepreneur prepares these statements in order to assess the

operational and financial performance. Thus, the used financial source will be shows in the

financial statements and impact the business profits and financial status.

In balance sheet, the amount of borrowed funds will be show in the liability side and

raise the cash availability. Thus, it increases the business current assets and long term

liabilities. However, in profit and loss account, interest payment will be shows as

expenditures and decrease profitability. Further, it reduces the cash balance of the company.

Another, overdraft will enhance the current liabilities and cash balance in the business and

interest on overdraft is an expenses hence, shows in profit and loss account and reduce

profitability (Cowling, Liu and Ledger, 2012). Further, sales of assets will results in lowering

the retail company's assets and improve the cash balance. Further, the profits or loss on sales

will be show as income or expenses in profit and loss account. Personal savings investment

will increase the equity and cash balance. Thus, both the assets and liabilities will be

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increased through personal savings. Lease charges will be represent as an expenses in profit

and loss account and decrease profits and cash balance of the company.

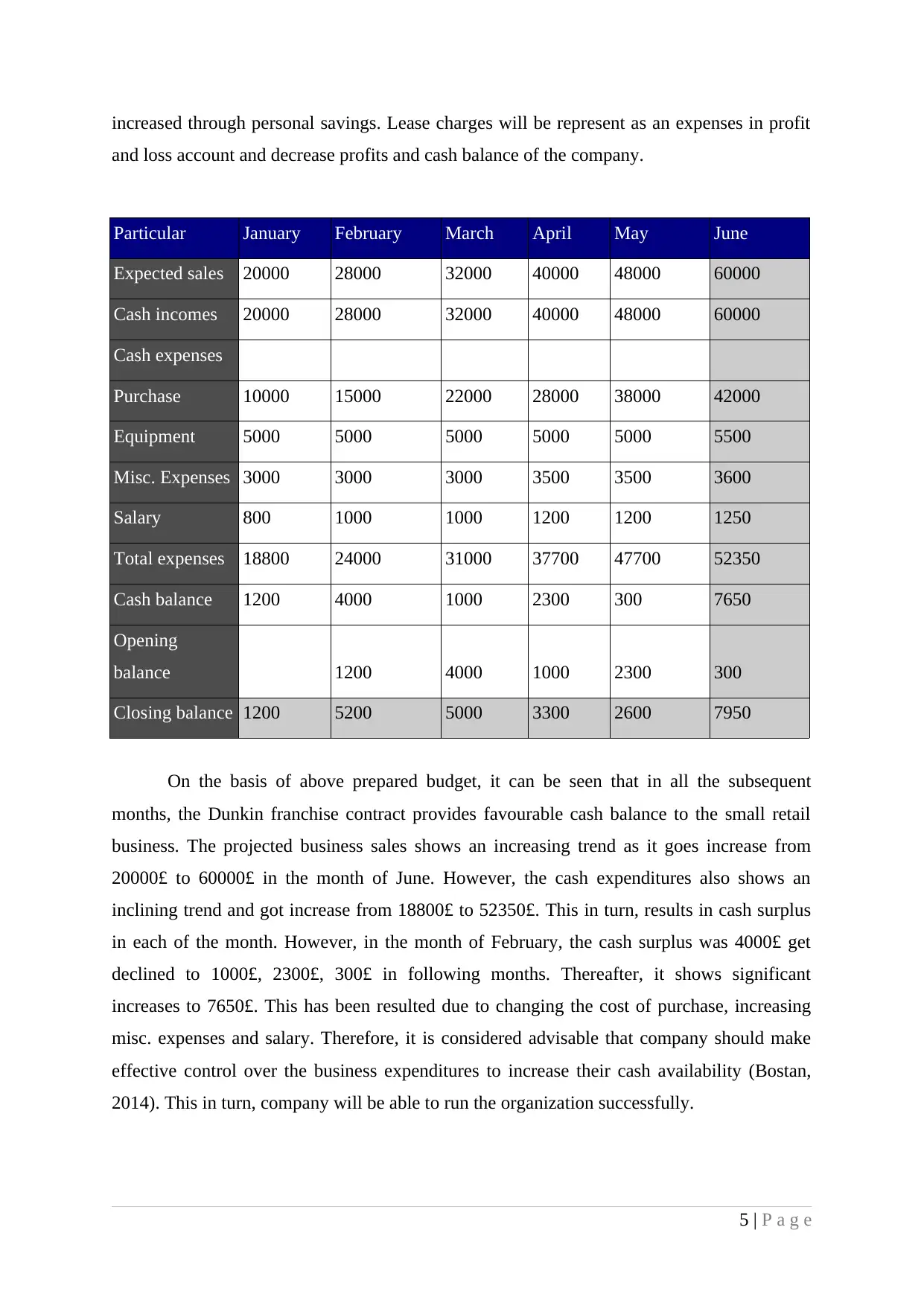

AC 3.1 Forecasted budget for six months

Particular January February March April May June

Expected sales 20000 28000 32000 40000 48000 60000

Cash incomes 20000 28000 32000 40000 48000 60000

Cash expenses

Purchase 10000 15000 22000 28000 38000 42000

Equipment 5000 5000 5000 5000 5000 5500

Misc. Expenses 3000 3000 3000 3500 3500 3600

Salary 800 1000 1000 1200 1200 1250

Total expenses 18800 24000 31000 37700 47700 52350

Cash balance 1200 4000 1000 2300 300 7650

Opening

balance 1200 4000 1000 2300 300

Closing balance 1200 5200 5000 3300 2600 7950

On the basis of above prepared budget, it can be seen that in all the subsequent

months, the Dunkin franchise contract provides favourable cash balance to the small retail

business. The projected business sales shows an increasing trend as it goes increase from

20000£ to 60000£ in the month of June. However, the cash expenditures also shows an

inclining trend and got increase from 18800£ to 52350£. This in turn, results in cash surplus

in each of the month. However, in the month of February, the cash surplus was 4000£ get

declined to 1000£, 2300£, 300£ in following months. Thereafter, it shows significant

increases to 7650£. This has been resulted due to changing the cost of purchase, increasing

misc. expenses and salary. Therefore, it is considered advisable that company should make

effective control over the business expenditures to increase their cash availability (Bostan,

2014). This in turn, company will be able to run the organization successfully.

5 | P a g e

and loss account and decrease profits and cash balance of the company.

AC 3.1 Forecasted budget for six months

Particular January February March April May June

Expected sales 20000 28000 32000 40000 48000 60000

Cash incomes 20000 28000 32000 40000 48000 60000

Cash expenses

Purchase 10000 15000 22000 28000 38000 42000

Equipment 5000 5000 5000 5000 5000 5500

Misc. Expenses 3000 3000 3000 3500 3500 3600

Salary 800 1000 1000 1200 1200 1250

Total expenses 18800 24000 31000 37700 47700 52350

Cash balance 1200 4000 1000 2300 300 7650

Opening

balance 1200 4000 1000 2300 300

Closing balance 1200 5200 5000 3300 2600 7950

On the basis of above prepared budget, it can be seen that in all the subsequent

months, the Dunkin franchise contract provides favourable cash balance to the small retail

business. The projected business sales shows an increasing trend as it goes increase from

20000£ to 60000£ in the month of June. However, the cash expenditures also shows an

inclining trend and got increase from 18800£ to 52350£. This in turn, results in cash surplus

in each of the month. However, in the month of February, the cash surplus was 4000£ get

declined to 1000£, 2300£, 300£ in following months. Thereafter, it shows significant

increases to 7650£. This has been resulted due to changing the cost of purchase, increasing

misc. expenses and salary. Therefore, it is considered advisable that company should make

effective control over the business expenditures to increase their cash availability (Bostan,

2014). This in turn, company will be able to run the organization successfully.

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

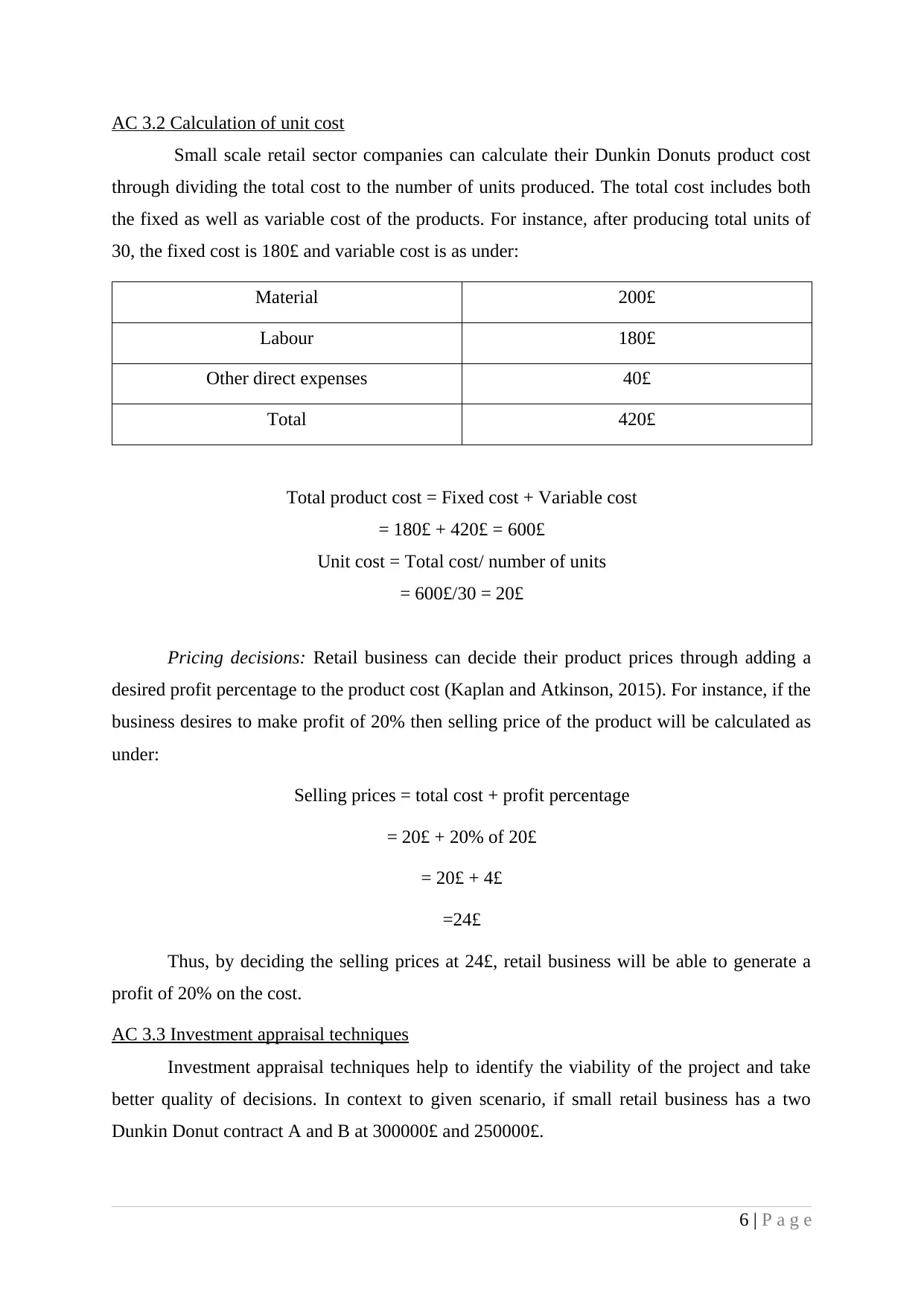

AC 3.2 Calculation of unit cost

Small scale retail sector companies can calculate their Dunkin Donuts product cost

through dividing the total cost to the number of units produced. The total cost includes both

the fixed as well as variable cost of the products. For instance, after producing total units of

30, the fixed cost is 180£ and variable cost is as under:

Material 200£

Labour 180£

Other direct expenses 40£

Total 420£

Total product cost = Fixed cost + Variable cost

= 180£ + 420£ = 600£

Unit cost = Total cost/ number of units

= 600£/30 = 20£

Pricing decisions: Retail business can decide their product prices through adding a

desired profit percentage to the product cost (Kaplan and Atkinson, 2015). For instance, if the

business desires to make profit of 20% then selling price of the product will be calculated as

under:

Selling prices = total cost + profit percentage

= 20£ + 20% of 20£

= 20£ + 4£

=24£

Thus, by deciding the selling prices at 24£, retail business will be able to generate a

profit of 20% on the cost.

AC 3.3 Investment appraisal techniques

Investment appraisal techniques help to identify the viability of the project and take

better quality of decisions. In context to given scenario, if small retail business has a two

Dunkin Donut contract A and B at 300000£ and 250000£.

6 | P a g e

Small scale retail sector companies can calculate their Dunkin Donuts product cost

through dividing the total cost to the number of units produced. The total cost includes both

the fixed as well as variable cost of the products. For instance, after producing total units of

30, the fixed cost is 180£ and variable cost is as under:

Material 200£

Labour 180£

Other direct expenses 40£

Total 420£

Total product cost = Fixed cost + Variable cost

= 180£ + 420£ = 600£

Unit cost = Total cost/ number of units

= 600£/30 = 20£

Pricing decisions: Retail business can decide their product prices through adding a

desired profit percentage to the product cost (Kaplan and Atkinson, 2015). For instance, if the

business desires to make profit of 20% then selling price of the product will be calculated as

under:

Selling prices = total cost + profit percentage

= 20£ + 20% of 20£

= 20£ + 4£

=24£

Thus, by deciding the selling prices at 24£, retail business will be able to generate a

profit of 20% on the cost.

AC 3.3 Investment appraisal techniques

Investment appraisal techniques help to identify the viability of the project and take

better quality of decisions. In context to given scenario, if small retail business has a two

Dunkin Donut contract A and B at 300000£ and 250000£.

6 | P a g e

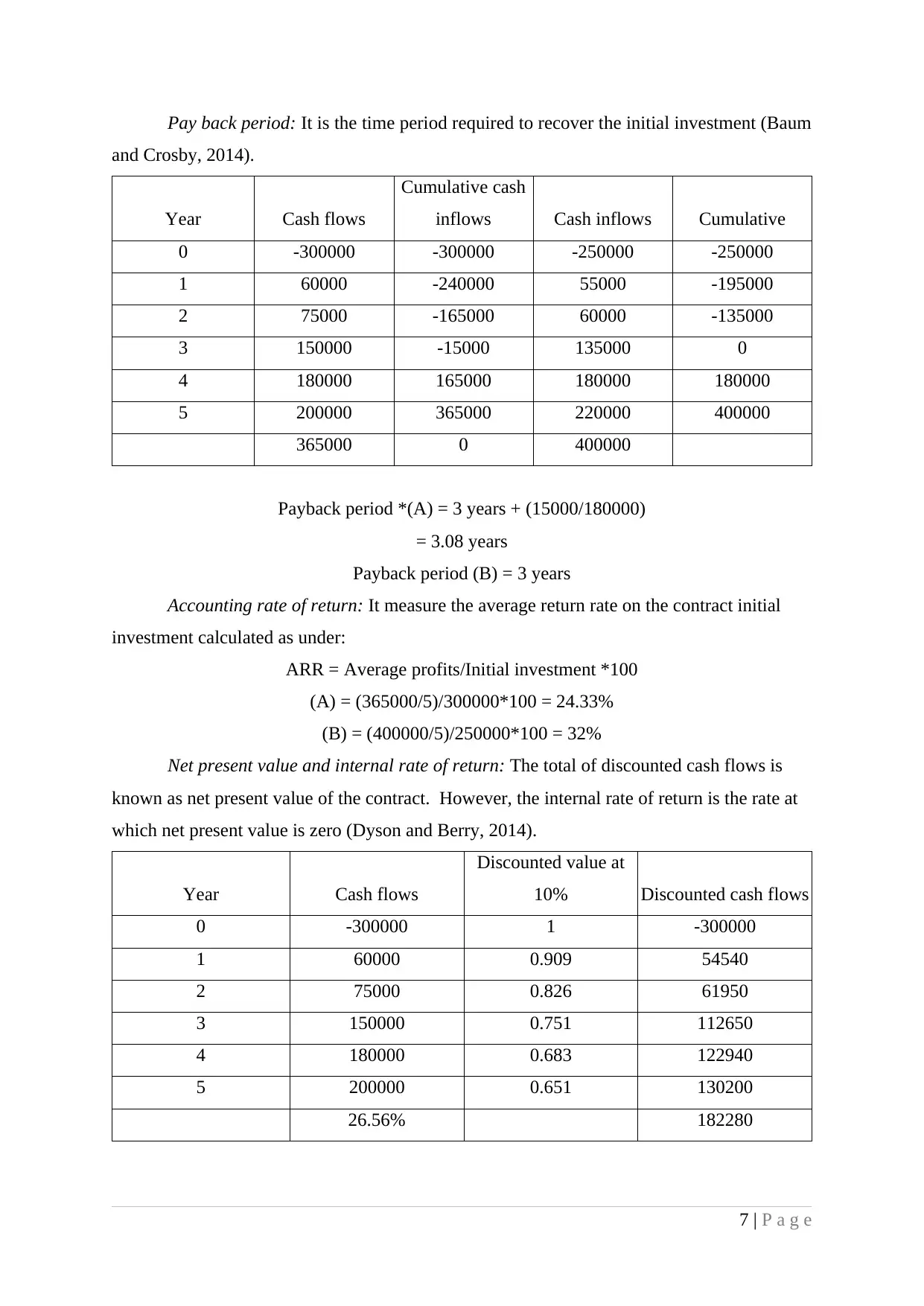

Pay back period: It is the time period required to recover the initial investment (Baum

and Crosby, 2014).

Year Cash flows

Cumulative cash

inflows Cash inflows Cumulative

0 -300000 -300000 -250000 -250000

1 60000 -240000 55000 -195000

2 75000 -165000 60000 -135000

3 150000 -15000 135000 0

4 180000 165000 180000 180000

5 200000 365000 220000 400000

365000 0 400000

Payback period *(A) = 3 years + (15000/180000)

= 3.08 years

Payback period (B) = 3 years

Accounting rate of return: It measure the average return rate on the contract initial

investment calculated as under:

ARR = Average profits/Initial investment *100

(A) = (365000/5)/300000*100 = 24.33%

(B) = (400000/5)/250000*100 = 32%

Net present value and internal rate of return: The total of discounted cash flows is

known as net present value of the contract. However, the internal rate of return is the rate at

which net present value is zero (Dyson and Berry, 2014).

Year Cash flows

Discounted value at

10% Discounted cash flows

0 -300000 1 -300000

1 60000 0.909 54540

2 75000 0.826 61950

3 150000 0.751 112650

4 180000 0.683 122940

5 200000 0.651 130200

26.56% 182280

7 | P a g e

and Crosby, 2014).

Year Cash flows

Cumulative cash

inflows Cash inflows Cumulative

0 -300000 -300000 -250000 -250000

1 60000 -240000 55000 -195000

2 75000 -165000 60000 -135000

3 150000 -15000 135000 0

4 180000 165000 180000 180000

5 200000 365000 220000 400000

365000 0 400000

Payback period *(A) = 3 years + (15000/180000)

= 3.08 years

Payback period (B) = 3 years

Accounting rate of return: It measure the average return rate on the contract initial

investment calculated as under:

ARR = Average profits/Initial investment *100

(A) = (365000/5)/300000*100 = 24.33%

(B) = (400000/5)/250000*100 = 32%

Net present value and internal rate of return: The total of discounted cash flows is

known as net present value of the contract. However, the internal rate of return is the rate at

which net present value is zero (Dyson and Berry, 2014).

Year Cash flows

Discounted value at

10% Discounted cash flows

0 -300000 1 -300000

1 60000 0.909 54540

2 75000 0.826 61950

3 150000 0.751 112650

4 180000 0.683 122940

5 200000 0.651 130200

26.56% 182280

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

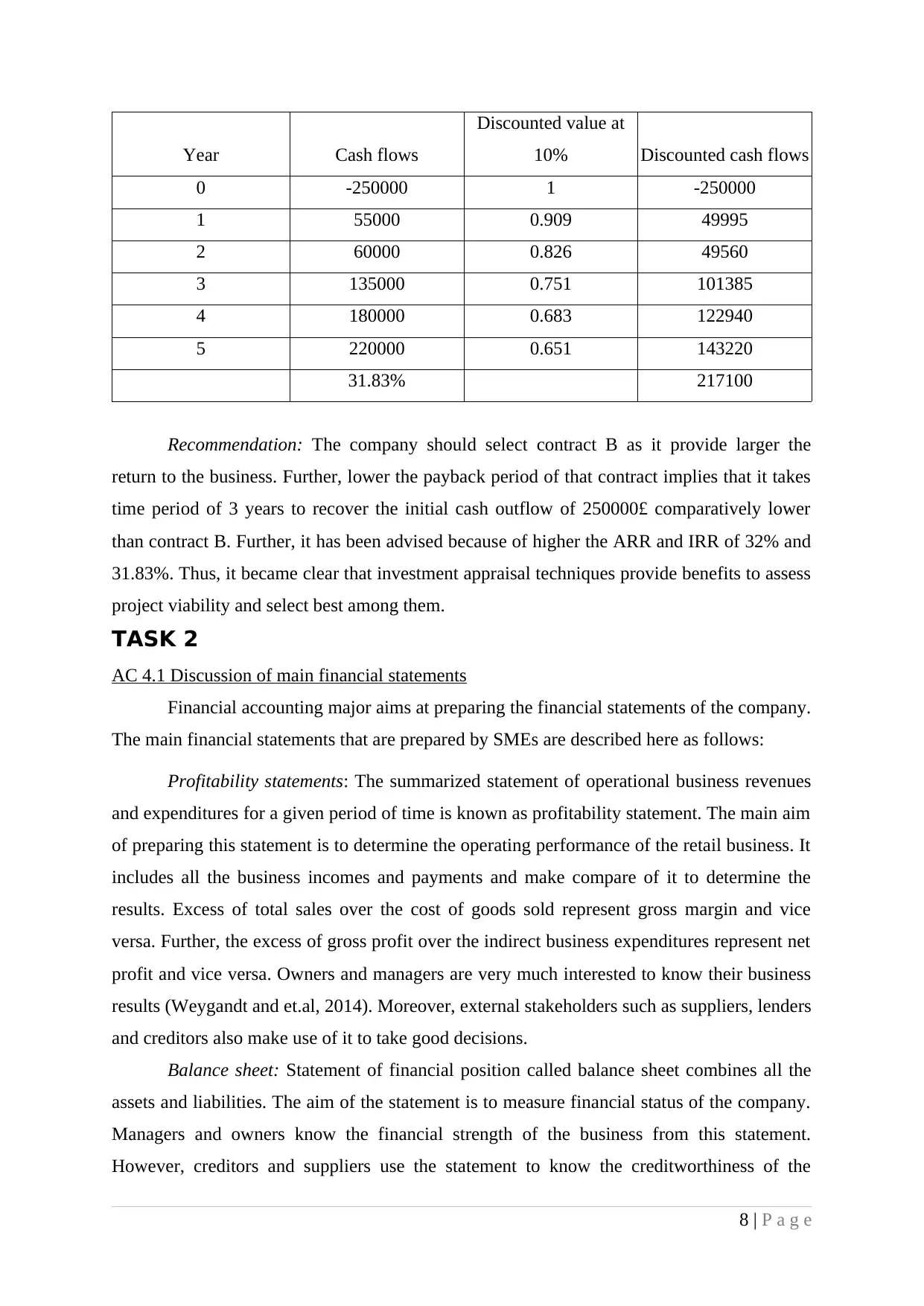

Year Cash flows

Discounted value at

10% Discounted cash flows

0 -250000 1 -250000

1 55000 0.909 49995

2 60000 0.826 49560

3 135000 0.751 101385

4 180000 0.683 122940

5 220000 0.651 143220

31.83% 217100

Recommendation: The company should select contract B as it provide larger the

return to the business. Further, lower the payback period of that contract implies that it takes

time period of 3 years to recover the initial cash outflow of 250000£ comparatively lower

than contract B. Further, it has been advised because of higher the ARR and IRR of 32% and

31.83%. Thus, it became clear that investment appraisal techniques provide benefits to assess

project viability and select best among them.

TASK 2

AC 4.1 Discussion of main financial statements

Financial accounting major aims at preparing the financial statements of the company.

The main financial statements that are prepared by SMEs are described here as follows:

Profitability statements: The summarized statement of operational business revenues

and expenditures for a given period of time is known as profitability statement. The main aim

of preparing this statement is to determine the operating performance of the retail business. It

includes all the business incomes and payments and make compare of it to determine the

results. Excess of total sales over the cost of goods sold represent gross margin and vice

versa. Further, the excess of gross profit over the indirect business expenditures represent net

profit and vice versa. Owners and managers are very much interested to know their business

results (Weygandt and et.al, 2014). Moreover, external stakeholders such as suppliers, lenders

and creditors also make use of it to take good decisions.

Balance sheet: Statement of financial position called balance sheet combines all the

assets and liabilities. The aim of the statement is to measure financial status of the company.

Managers and owners know the financial strength of the business from this statement.

However, creditors and suppliers use the statement to know the creditworthiness of the

8 | P a g e

Discounted value at

10% Discounted cash flows

0 -250000 1 -250000

1 55000 0.909 49995

2 60000 0.826 49560

3 135000 0.751 101385

4 180000 0.683 122940

5 220000 0.651 143220

31.83% 217100

Recommendation: The company should select contract B as it provide larger the

return to the business. Further, lower the payback period of that contract implies that it takes

time period of 3 years to recover the initial cash outflow of 250000£ comparatively lower

than contract B. Further, it has been advised because of higher the ARR and IRR of 32% and

31.83%. Thus, it became clear that investment appraisal techniques provide benefits to assess

project viability and select best among them.

TASK 2

AC 4.1 Discussion of main financial statements

Financial accounting major aims at preparing the financial statements of the company.

The main financial statements that are prepared by SMEs are described here as follows:

Profitability statements: The summarized statement of operational business revenues

and expenditures for a given period of time is known as profitability statement. The main aim

of preparing this statement is to determine the operating performance of the retail business. It

includes all the business incomes and payments and make compare of it to determine the

results. Excess of total sales over the cost of goods sold represent gross margin and vice

versa. Further, the excess of gross profit over the indirect business expenditures represent net

profit and vice versa. Owners and managers are very much interested to know their business

results (Weygandt and et.al, 2014). Moreover, external stakeholders such as suppliers, lenders

and creditors also make use of it to take good decisions.

Balance sheet: Statement of financial position called balance sheet combines all the

assets and liabilities. The aim of the statement is to measure financial status of the company.

Managers and owners know the financial strength of the business from this statement.

However, creditors and suppliers use the statement to know the creditworthiness of the

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company (Voss and Voss, 2013.). Further, investors know the solvency position from this

statement to take qualitative decisions.

AC 4.2 Main financial statement of different types of business

Sole trade: Venture prepares profitability statement to know their business return in

terms of profit. It includes expenditures such as purchase, rent, salary, stationery and so on.

However, incomes comprise sales and other revenue. The proprietor is not obliged to follow

any specified structure to prepare the statement.

Partnership: Combining the contribution of two or more persons with an organization

is the form of partnership. Partners make contribute their funds and efforts to run the business

successfully. Thus, they prepare profitability through including incomes and expenditures and

measure profitability. Moreover, profit and loss appropriation and partners’ capital account

are also prepared as per the partnership act (Healy and Palepu, 2012.).

Company: Another form of business organization is company prepare necessary

statements to satisfy the owners. It is legally obliged to prepare profitability statement and

measure operational result. Moreover, balance sheet includes the assets and liabilities and

measure financial status. Another, cash flow statement is prepared to determine the cash

earning capacity through measuring the cash inflows and outflows from various business

functions (Ormiston and Fraser, 2013). In addition to it, fund flow statement and statement of

changes in equity and retained earnings are also prepared by them to measure the changes in

value reported in two different accounting periods.

AC 4.3 interpreting the financial statements

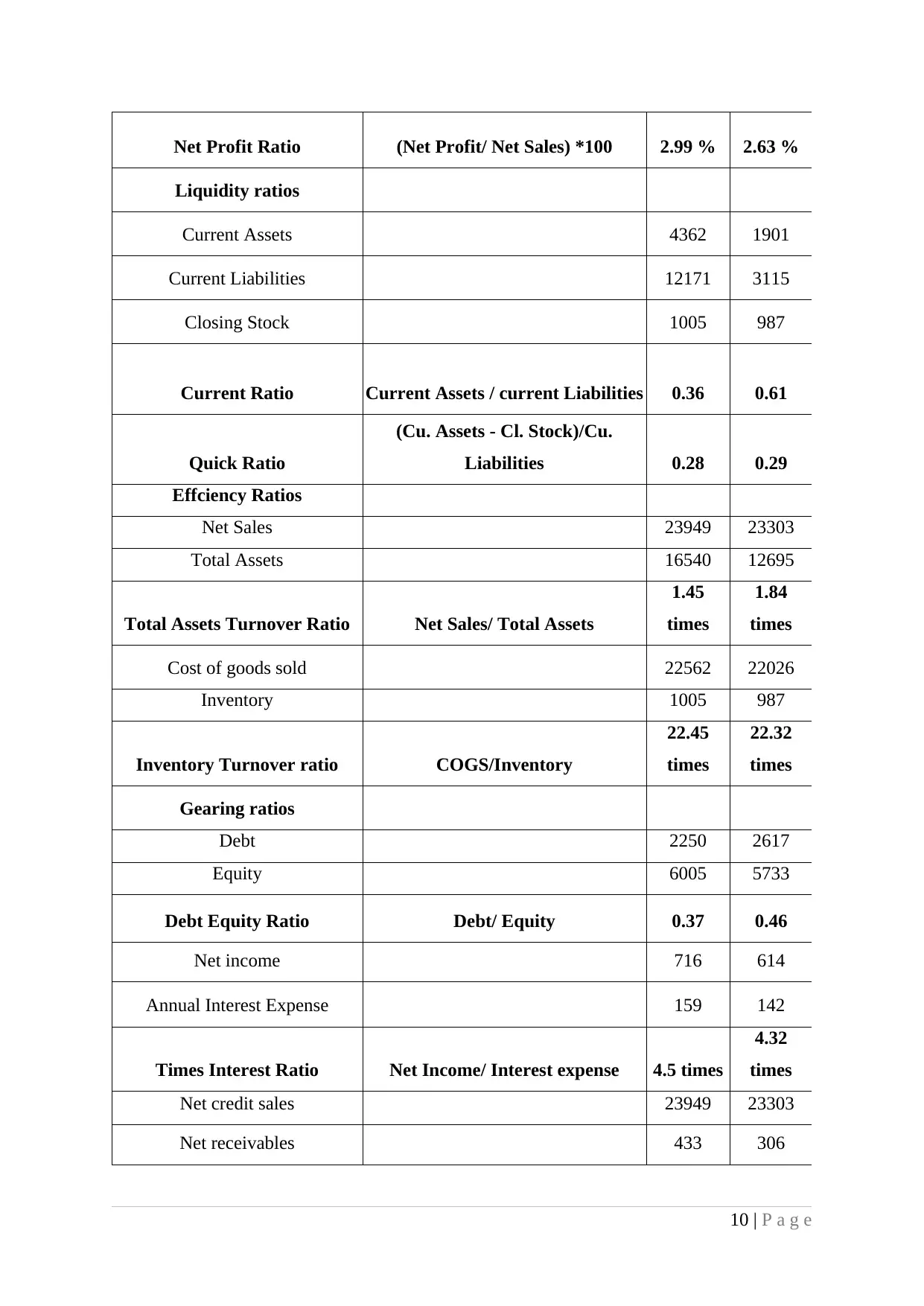

Sainsbury is the largest supermarket chain of UK, headquartered in Holborn, London.

Ratios Formula 2014 2013

Profitability ratios

Gross profit 1377 1277

Operating profit 1009 887

Net profit 716 614

Net Sales 23949 23303

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 %

Operating Profit Ratio (Operating Profit/ Net Sales) *100 4.21 % 3.81%

9 | P a g e

statement to take qualitative decisions.

AC 4.2 Main financial statement of different types of business

Sole trade: Venture prepares profitability statement to know their business return in

terms of profit. It includes expenditures such as purchase, rent, salary, stationery and so on.

However, incomes comprise sales and other revenue. The proprietor is not obliged to follow

any specified structure to prepare the statement.

Partnership: Combining the contribution of two or more persons with an organization

is the form of partnership. Partners make contribute their funds and efforts to run the business

successfully. Thus, they prepare profitability through including incomes and expenditures and

measure profitability. Moreover, profit and loss appropriation and partners’ capital account

are also prepared as per the partnership act (Healy and Palepu, 2012.).

Company: Another form of business organization is company prepare necessary

statements to satisfy the owners. It is legally obliged to prepare profitability statement and

measure operational result. Moreover, balance sheet includes the assets and liabilities and

measure financial status. Another, cash flow statement is prepared to determine the cash

earning capacity through measuring the cash inflows and outflows from various business

functions (Ormiston and Fraser, 2013). In addition to it, fund flow statement and statement of

changes in equity and retained earnings are also prepared by them to measure the changes in

value reported in two different accounting periods.

AC 4.3 interpreting the financial statements

Sainsbury is the largest supermarket chain of UK, headquartered in Holborn, London.

Ratios Formula 2014 2013

Profitability ratios

Gross profit 1377 1277

Operating profit 1009 887

Net profit 716 614

Net Sales 23949 23303

Gross Profit Ratio (Gross Profit/ Net Sales) *100 5.75 % 5.48 %

Operating Profit Ratio (Operating Profit/ Net Sales) *100 4.21 % 3.81%

9 | P a g e

Net Profit Ratio (Net Profit/ Net Sales) *100 2.99 % 2.63 %

Liquidity ratios

Current Assets 4362 1901

Current Liabilities 12171 3115

Closing Stock 1005 987

Current Ratio Current Assets / current Liabilities 0.36 0.61

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29

Effciency Ratios

Net Sales 23949 23303

Total Assets 16540 12695

Total Assets Turnover Ratio Net Sales/ Total Assets

1.45

times

1.84

times

Cost of goods sold 22562 22026

Inventory 1005 987

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

Gearing ratios

Debt 2250 2617

Equity 6005 5733

Debt Equity Ratio Debt/ Equity 0.37 0.46

Net income 716 614

Annual Interest Expense 159 142

Times Interest Ratio Net Income/ Interest expense 4.5 times

4.32

times

Net credit sales 23949 23303

Net receivables 433 306

10 | P a g e

Liquidity ratios

Current Assets 4362 1901

Current Liabilities 12171 3115

Closing Stock 1005 987

Current Ratio Current Assets / current Liabilities 0.36 0.61

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.28 0.29

Effciency Ratios

Net Sales 23949 23303

Total Assets 16540 12695

Total Assets Turnover Ratio Net Sales/ Total Assets

1.45

times

1.84

times

Cost of goods sold 22562 22026

Inventory 1005 987

Inventory Turnover ratio COGS/Inventory

22.45

times

22.32

times

Gearing ratios

Debt 2250 2617

Equity 6005 5733

Debt Equity Ratio Debt/ Equity 0.37 0.46

Net income 716 614

Annual Interest Expense 159 142

Times Interest Ratio Net Income/ Interest expense 4.5 times

4.32

times

Net credit sales 23949 23303

Net receivables 433 306

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.