Financial Resource Management Report: Poundland Group plc Analysis

VerifiedAdded on 2020/06/03

|11

|2754

|170

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, using Poundland Group plc as a case study. It begins by differentiating between financial and management accounts, outlining their respective roles and purposes. The report then describes the function of various financial statements for both profit and non-profit organizations, including the statement of financial position, income statement, cash flow statement, and statement of changes in equity. It also examines the information needs of different stakeholder groups, categorizing them as primary, secondary, internal, and external, and detailing the types of financial reports each group requires. The core of the report involves a detailed ratio analysis of Poundland Group plc's financial statements for two consecutive years, calculating and interpreting key ratios such as gross profit margin, net profit margin, return on capital employed, inventory turnover, and various liquidity and solvency ratios. Finally, the report compares the company's financial performance and position over the two-year period based on the calculated ratios, providing insights into its financial health and performance trends.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the difference between financial accounts and management accounts......................1

b) Describe the purpose of various financial statements in a profit and non profit organisation

.....................................................................................................................................................3

c) Various groups of stakeholders and measure their different information needs.....................4

TASK 2............................................................................................................................................5

a) ratio analysis with the help of financial statements of Poundland group plc..........................5

b) Comparison of the performance and position of the business for two years on the basis of

figures..........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Explain the difference between financial accounts and management accounts......................1

b) Describe the purpose of various financial statements in a profit and non profit organisation

.....................................................................................................................................................3

c) Various groups of stakeholders and measure their different information needs.....................4

TASK 2............................................................................................................................................5

a) ratio analysis with the help of financial statements of Poundland group plc..........................5

b) Comparison of the performance and position of the business for two years on the basis of

figures..........................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Finance is one of the essential sources of an organisation. Effective use of management

and operation helps to improve the financial structure of an organisation and helps to attain

desired objectives and aims (Ashwell, 2014). This report is based upon a case study of

Poundland group plc which is a premium segment of the London stock market. Importance of

financial accounts subject to managing financial recurses are defined in this context. Difference

between financial accountants and management accountants also defined. Performance of

organisation is evaluated with the help of ratio analysis. Suggestions and recommendations are

given in subject to improve the financial performance of company.

TASK 1

a) Explain the difference between financial accounts and management accounts

Financial accounts

it is one of the essential accounting technique which remain associated with managing

financial resources and recording financial transaction. All the financial accounting is a process

of recording financial transactions, events and records in ethical and systematic manner. Various

type of financial accounting rules and principle are found in order to produce financial reports

and accounts (Bridoux and Stoelhorst, 2014). This process helps to summarise financial

statements, reports and accounts subject to evaluate to analyse financial performance and

monetary needs for upcoming years. This process helps to record the transaction for a specific

period and duration.

Financial accounts present financial reports, analysation of financial statements and

preparing of financial statements. Finance managers and accountants are hired to operate this

process effectively and efficiently. Financial information which are provided by the managers

and helps to stakeholder, owners, directors, government bodies, suppliers and financial

institutions and banks.

Management accountants

This is also a process of preparing management reports and accounts for better formation

and framing of management accountants (Taylor, Doherty and McGraw, 2015). This is the part

of decision making and strategic planning process which helps to analyse the financial

performance and analysing the statement of organisation. With the helps of this process

managers and accountant become eligible to phrase the financial and accounting information in

1

Finance is one of the essential sources of an organisation. Effective use of management

and operation helps to improve the financial structure of an organisation and helps to attain

desired objectives and aims (Ashwell, 2014). This report is based upon a case study of

Poundland group plc which is a premium segment of the London stock market. Importance of

financial accounts subject to managing financial recurses are defined in this context. Difference

between financial accountants and management accountants also defined. Performance of

organisation is evaluated with the help of ratio analysis. Suggestions and recommendations are

given in subject to improve the financial performance of company.

TASK 1

a) Explain the difference between financial accounts and management accounts

Financial accounts

it is one of the essential accounting technique which remain associated with managing

financial resources and recording financial transaction. All the financial accounting is a process

of recording financial transactions, events and records in ethical and systematic manner. Various

type of financial accounting rules and principle are found in order to produce financial reports

and accounts (Bridoux and Stoelhorst, 2014). This process helps to summarise financial

statements, reports and accounts subject to evaluate to analyse financial performance and

monetary needs for upcoming years. This process helps to record the transaction for a specific

period and duration.

Financial accounts present financial reports, analysation of financial statements and

preparing of financial statements. Finance managers and accountants are hired to operate this

process effectively and efficiently. Financial information which are provided by the managers

and helps to stakeholder, owners, directors, government bodies, suppliers and financial

institutions and banks.

Management accountants

This is also a process of preparing management reports and accounts for better formation

and framing of management accountants (Taylor, Doherty and McGraw, 2015). This is the part

of decision making and strategic planning process which helps to analyse the financial

performance and analysing the statement of organisation. With the helps of this process

managers and accountant become eligible to phrase the financial and accounting information in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

systematic and effective manner. It helps managers to take short term and long term management

decision for sustainable growth and development (financial ratios, 2017).

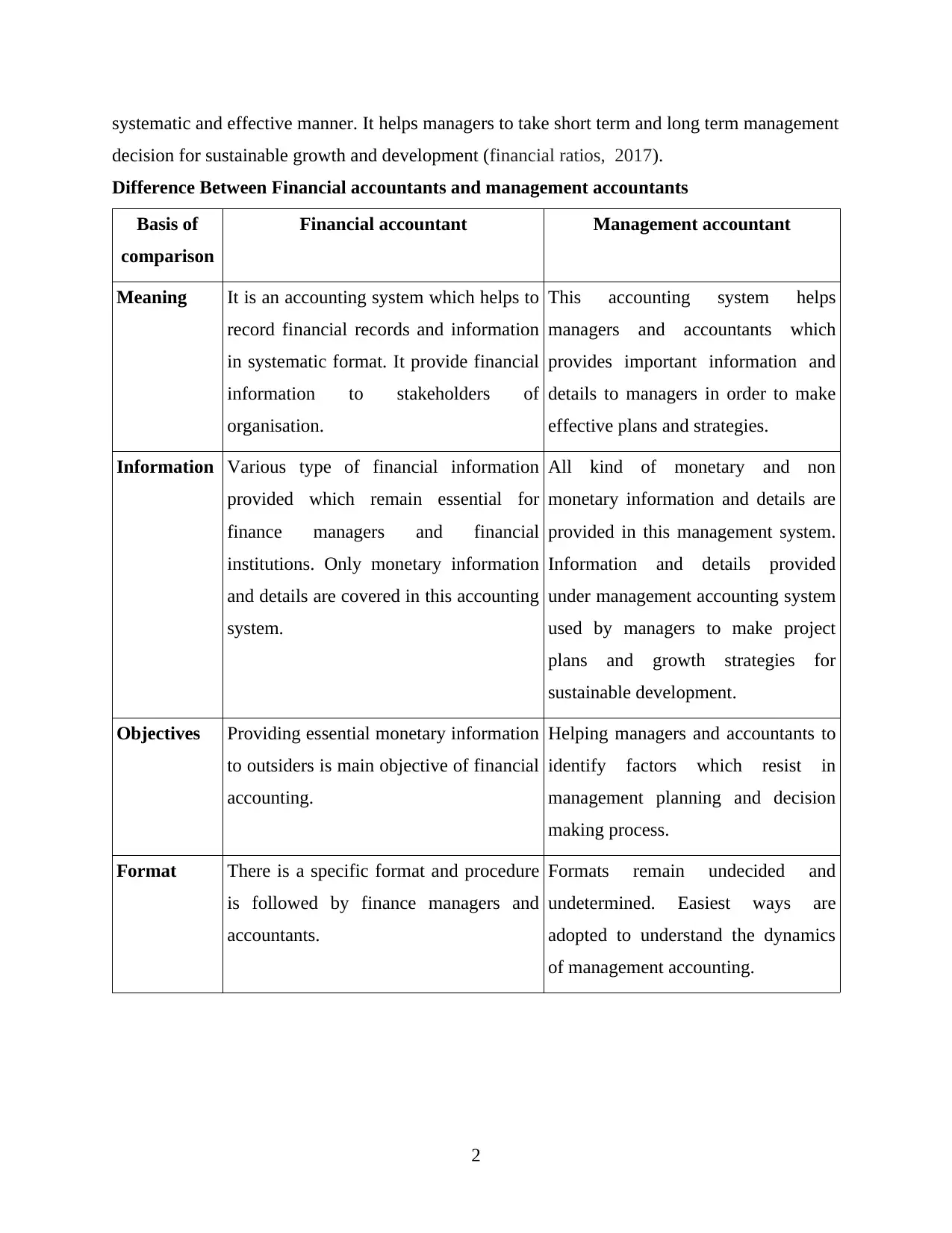

Difference Between Financial accountants and management accountants

Basis of

comparison

Financial accountant Management accountant

Meaning It is an accounting system which helps to

record financial records and information

in systematic format. It provide financial

information to stakeholders of

organisation.

This accounting system helps

managers and accountants which

provides important information and

details to managers in order to make

effective plans and strategies.

Information Various type of financial information

provided which remain essential for

finance managers and financial

institutions. Only monetary information

and details are covered in this accounting

system.

All kind of monetary and non

monetary information and details are

provided in this management system.

Information and details provided

under management accounting system

used by managers to make project

plans and growth strategies for

sustainable development.

Objectives Providing essential monetary information

to outsiders is main objective of financial

accounting.

Helping managers and accountants to

identify factors which resist in

management planning and decision

making process.

Format There is a specific format and procedure

is followed by finance managers and

accountants.

Formats remain undecided and

undetermined. Easiest ways are

adopted to understand the dynamics

of management accounting.

2

decision for sustainable growth and development (financial ratios, 2017).

Difference Between Financial accountants and management accountants

Basis of

comparison

Financial accountant Management accountant

Meaning It is an accounting system which helps to

record financial records and information

in systematic format. It provide financial

information to stakeholders of

organisation.

This accounting system helps

managers and accountants which

provides important information and

details to managers in order to make

effective plans and strategies.

Information Various type of financial information

provided which remain essential for

finance managers and financial

institutions. Only monetary information

and details are covered in this accounting

system.

All kind of monetary and non

monetary information and details are

provided in this management system.

Information and details provided

under management accounting system

used by managers to make project

plans and growth strategies for

sustainable development.

Objectives Providing essential monetary information

to outsiders is main objective of financial

accounting.

Helping managers and accountants to

identify factors which resist in

management planning and decision

making process.

Format There is a specific format and procedure

is followed by finance managers and

accountants.

Formats remain undecided and

undetermined. Easiest ways are

adopted to understand the dynamics

of management accounting.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

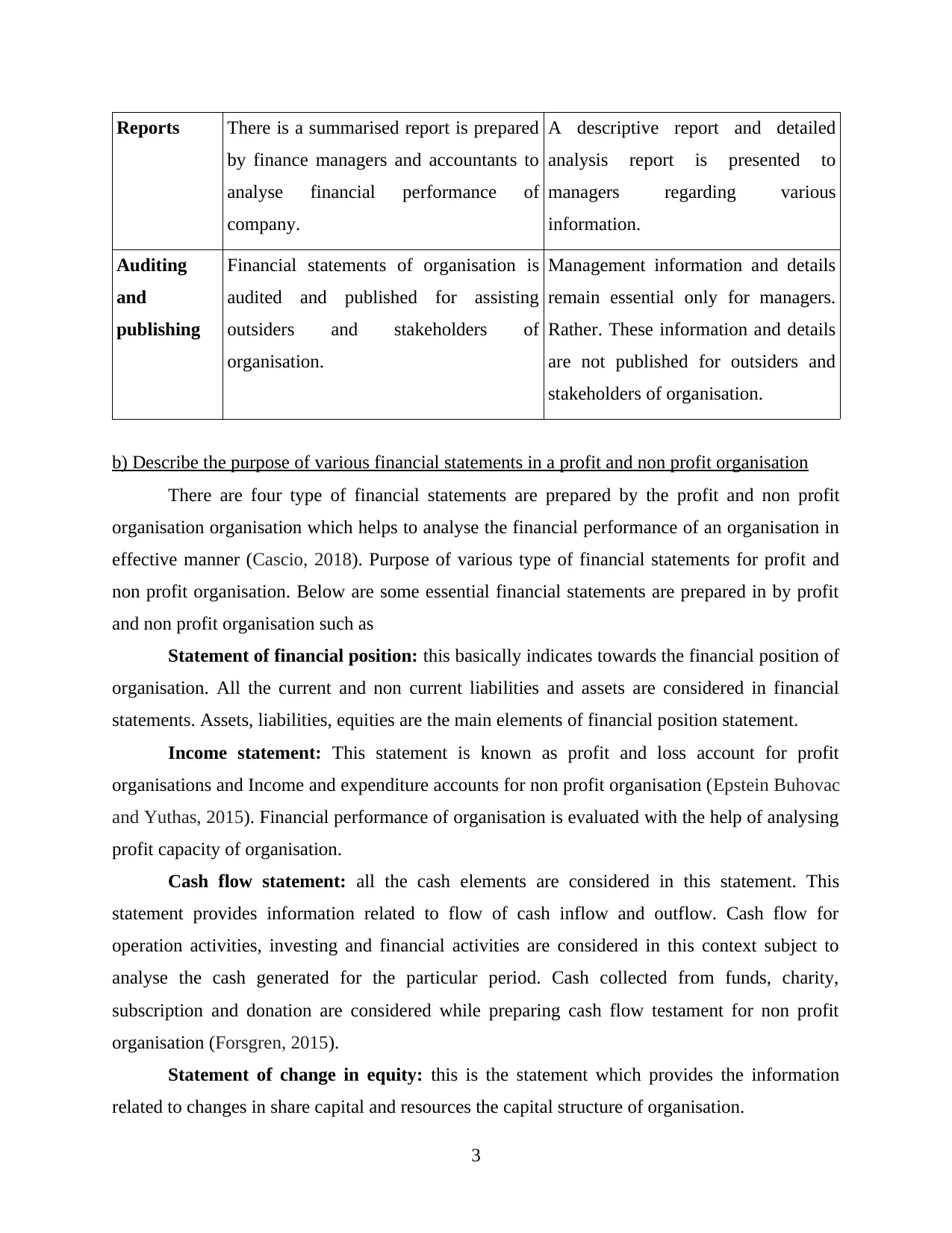

Reports There is a summarised report is prepared

by finance managers and accountants to

analyse financial performance of

company.

A descriptive report and detailed

analysis report is presented to

managers regarding various

information.

Auditing

and

publishing

Financial statements of organisation is

audited and published for assisting

outsiders and stakeholders of

organisation.

Management information and details

remain essential only for managers.

Rather. These information and details

are not published for outsiders and

stakeholders of organisation.

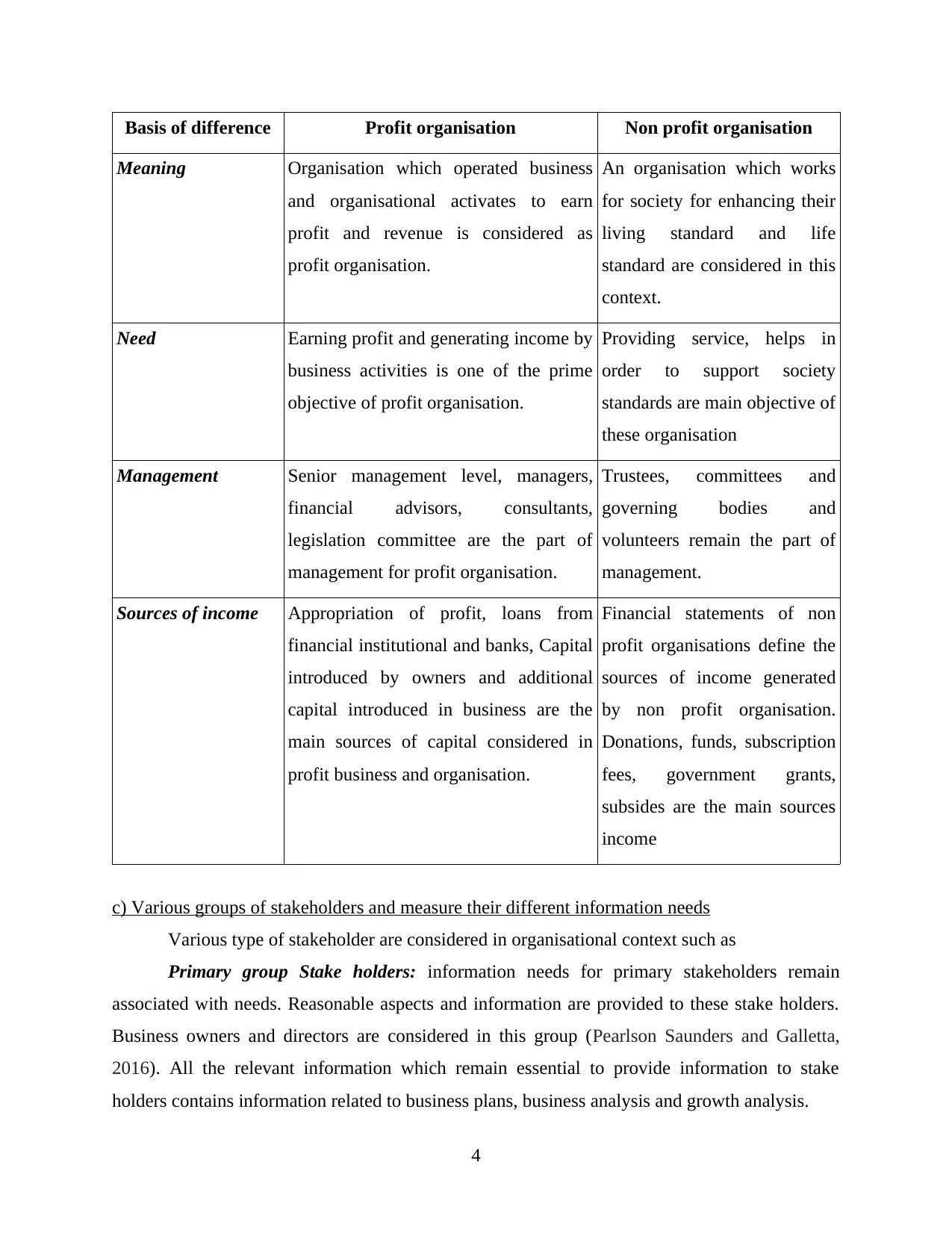

b) Describe the purpose of various financial statements in a profit and non profit organisation

There are four type of financial statements are prepared by the profit and non profit

organisation organisation which helps to analyse the financial performance of an organisation in

effective manner (Cascio, 2018). Purpose of various type of financial statements for profit and

non profit organisation. Below are some essential financial statements are prepared in by profit

and non profit organisation such as

Statement of financial position: this basically indicates towards the financial position of

organisation. All the current and non current liabilities and assets are considered in financial

statements. Assets, liabilities, equities are the main elements of financial position statement.

Income statement: This statement is known as profit and loss account for profit

organisations and Income and expenditure accounts for non profit organisation (Epstein Buhovac

and Yuthas, 2015). Financial performance of organisation is evaluated with the help of analysing

profit capacity of organisation.

Cash flow statement: all the cash elements are considered in this statement. This

statement provides information related to flow of cash inflow and outflow. Cash flow for

operation activities, investing and financial activities are considered in this context subject to

analyse the cash generated for the particular period. Cash collected from funds, charity,

subscription and donation are considered while preparing cash flow testament for non profit

organisation (Forsgren, 2015).

Statement of change in equity: this is the statement which provides the information

related to changes in share capital and resources the capital structure of organisation.

3

by finance managers and accountants to

analyse financial performance of

company.

A descriptive report and detailed

analysis report is presented to

managers regarding various

information.

Auditing

and

publishing

Financial statements of organisation is

audited and published for assisting

outsiders and stakeholders of

organisation.

Management information and details

remain essential only for managers.

Rather. These information and details

are not published for outsiders and

stakeholders of organisation.

b) Describe the purpose of various financial statements in a profit and non profit organisation

There are four type of financial statements are prepared by the profit and non profit

organisation organisation which helps to analyse the financial performance of an organisation in

effective manner (Cascio, 2018). Purpose of various type of financial statements for profit and

non profit organisation. Below are some essential financial statements are prepared in by profit

and non profit organisation such as

Statement of financial position: this basically indicates towards the financial position of

organisation. All the current and non current liabilities and assets are considered in financial

statements. Assets, liabilities, equities are the main elements of financial position statement.

Income statement: This statement is known as profit and loss account for profit

organisations and Income and expenditure accounts for non profit organisation (Epstein Buhovac

and Yuthas, 2015). Financial performance of organisation is evaluated with the help of analysing

profit capacity of organisation.

Cash flow statement: all the cash elements are considered in this statement. This

statement provides information related to flow of cash inflow and outflow. Cash flow for

operation activities, investing and financial activities are considered in this context subject to

analyse the cash generated for the particular period. Cash collected from funds, charity,

subscription and donation are considered while preparing cash flow testament for non profit

organisation (Forsgren, 2015).

Statement of change in equity: this is the statement which provides the information

related to changes in share capital and resources the capital structure of organisation.

3

Basis of difference Profit organisation Non profit organisation

Meaning Organisation which operated business

and organisational activates to earn

profit and revenue is considered as

profit organisation.

An organisation which works

for society for enhancing their

living standard and life

standard are considered in this

context.

Need Earning profit and generating income by

business activities is one of the prime

objective of profit organisation.

Providing service, helps in

order to support society

standards are main objective of

these organisation

Management Senior management level, managers,

financial advisors, consultants,

legislation committee are the part of

management for profit organisation.

Trustees, committees and

governing bodies and

volunteers remain the part of

management.

Sources of income Appropriation of profit, loans from

financial institutional and banks, Capital

introduced by owners and additional

capital introduced in business are the

main sources of capital considered in

profit business and organisation.

Financial statements of non

profit organisations define the

sources of income generated

by non profit organisation.

Donations, funds, subscription

fees, government grants,

subsides are the main sources

income

c) Various groups of stakeholders and measure their different information needs

Various type of stakeholder are considered in organisational context such as

Primary group Stake holders: information needs for primary stakeholders remain

associated with needs. Reasonable aspects and information are provided to these stake holders.

Business owners and directors are considered in this group (Pearlson Saunders and Galletta,

2016). All the relevant information which remain essential to provide information to stake

holders contains information related to business plans, business analysis and growth analysis.

4

Meaning Organisation which operated business

and organisational activates to earn

profit and revenue is considered as

profit organisation.

An organisation which works

for society for enhancing their

living standard and life

standard are considered in this

context.

Need Earning profit and generating income by

business activities is one of the prime

objective of profit organisation.

Providing service, helps in

order to support society

standards are main objective of

these organisation

Management Senior management level, managers,

financial advisors, consultants,

legislation committee are the part of

management for profit organisation.

Trustees, committees and

governing bodies and

volunteers remain the part of

management.

Sources of income Appropriation of profit, loans from

financial institutional and banks, Capital

introduced by owners and additional

capital introduced in business are the

main sources of capital considered in

profit business and organisation.

Financial statements of non

profit organisations define the

sources of income generated

by non profit organisation.

Donations, funds, subscription

fees, government grants,

subsides are the main sources

income

c) Various groups of stakeholders and measure their different information needs

Various type of stakeholder are considered in organisational context such as

Primary group Stake holders: information needs for primary stakeholders remain

associated with needs. Reasonable aspects and information are provided to these stake holders.

Business owners and directors are considered in this group (Pearlson Saunders and Galletta,

2016). All the relevant information which remain essential to provide information to stake

holders contains information related to business plans, business analysis and growth analysis.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Secondary stakeholders: It includes the such stakeholders which don't have direct

relation with organisation but considered as important part of organisation. Such stakeholders

have their indirect interest and management of organisation need to take the approval of such

stakeholders while take any decisions (Purce, 2014). The major secondary stakeholders of pound

land are financial institutions, investors, companies shareholders etc. It is the duty of the

management of organisation is to provide different kind of informations to their secondary

stakeholders. The important reports which are used by such stakeholders to improve their

information are income statement, profit and loss account, balance sheet etc. Profit and loss

account is important report which is used by the stakeholders to analyse the financial condition

of organisation.

Internal stakeholders: There are large number of internal stakeholders which are present

in organisation. Such stakeholders have direct relation with organisation (Smith, 2014). These

stakeholders are directly affected by the organisational activities and their decision makings. The

internal stakeholders of Pound land are employees, managers, team leaders etc. The different

kind reports are prepared by the organisation like job cost, inventory, performance etc. which are

used by such internal parties to improves their decision making and accomplish their targets.

External: External stakeholders of Pound land are suppliers, customers etc. Both these

stakeholders have their important position in organisation (Snell, Morris and Bohlander, 2015).

Customers are important for every organisation and satisfaction of their demand helps in

improvement of sales and profitability. The different reports which helps to provide adequate

information to customers are income statement and profit and loss accounts. It helps in

assessment of the credibility of organisation. On other hand suppliers of organisation required to

know about the different offering of organisation which helps in effective providence of services.

It helps the organisation to gather the view points of such stakeholders and improves their

business functions.

TASK 2

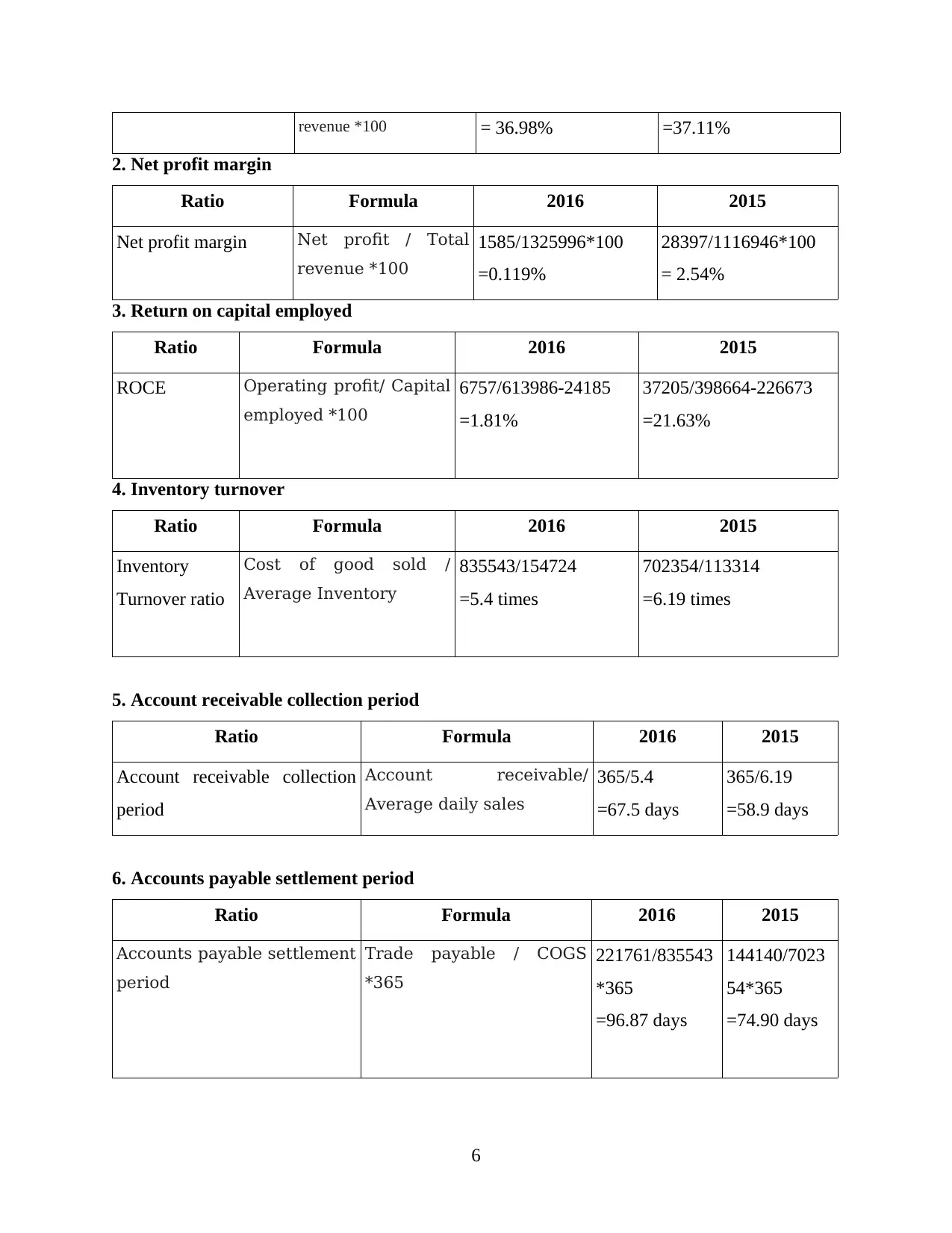

a) ratio analysis with the help of financial statements of Poundland group plc

1. Gross profit margin ratio

Ratio Formula 2016 2015

Gross profit margin Gross profit / Total 490453/1325996*100 414592/1116946*100

5

relation with organisation but considered as important part of organisation. Such stakeholders

have their indirect interest and management of organisation need to take the approval of such

stakeholders while take any decisions (Purce, 2014). The major secondary stakeholders of pound

land are financial institutions, investors, companies shareholders etc. It is the duty of the

management of organisation is to provide different kind of informations to their secondary

stakeholders. The important reports which are used by such stakeholders to improve their

information are income statement, profit and loss account, balance sheet etc. Profit and loss

account is important report which is used by the stakeholders to analyse the financial condition

of organisation.

Internal stakeholders: There are large number of internal stakeholders which are present

in organisation. Such stakeholders have direct relation with organisation (Smith, 2014). These

stakeholders are directly affected by the organisational activities and their decision makings. The

internal stakeholders of Pound land are employees, managers, team leaders etc. The different

kind reports are prepared by the organisation like job cost, inventory, performance etc. which are

used by such internal parties to improves their decision making and accomplish their targets.

External: External stakeholders of Pound land are suppliers, customers etc. Both these

stakeholders have their important position in organisation (Snell, Morris and Bohlander, 2015).

Customers are important for every organisation and satisfaction of their demand helps in

improvement of sales and profitability. The different reports which helps to provide adequate

information to customers are income statement and profit and loss accounts. It helps in

assessment of the credibility of organisation. On other hand suppliers of organisation required to

know about the different offering of organisation which helps in effective providence of services.

It helps the organisation to gather the view points of such stakeholders and improves their

business functions.

TASK 2

a) ratio analysis with the help of financial statements of Poundland group plc

1. Gross profit margin ratio

Ratio Formula 2016 2015

Gross profit margin Gross profit / Total 490453/1325996*100 414592/1116946*100

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

revenue *100 = 36.98% =37.11%

2. Net profit margin

Ratio Formula 2016 2015

Net profit margin Net profit / Total

revenue *100

1585/1325996*100

=0.119%

28397/1116946*100

= 2.54%

3. Return on capital employed

Ratio Formula 2016 2015

ROCE Operating profit/ Capital

employed *100

6757/613986-24185

=1.81%

37205/398664-226673

=21.63%

4. Inventory turnover

Ratio Formula 2016 2015

Inventory

Turnover ratio

Cost of good sold /

Average Inventory

835543/154724

=5.4 times

702354/113314

=6.19 times

5. Account receivable collection period

Ratio Formula 2016 2015

Account receivable collection

period

Account receivable/

Average daily sales

365/5.4

=67.5 days

365/6.19

=58.9 days

6. Accounts payable settlement period

Ratio Formula 2016 2015

Accounts payable settlement

period

Trade payable / COGS

*365

221761/835543

*365

=96.87 days

144140/7023

54*365

=74.90 days

6

2. Net profit margin

Ratio Formula 2016 2015

Net profit margin Net profit / Total

revenue *100

1585/1325996*100

=0.119%

28397/1116946*100

= 2.54%

3. Return on capital employed

Ratio Formula 2016 2015

ROCE Operating profit/ Capital

employed *100

6757/613986-24185

=1.81%

37205/398664-226673

=21.63%

4. Inventory turnover

Ratio Formula 2016 2015

Inventory

Turnover ratio

Cost of good sold /

Average Inventory

835543/154724

=5.4 times

702354/113314

=6.19 times

5. Account receivable collection period

Ratio Formula 2016 2015

Account receivable collection

period

Account receivable/

Average daily sales

365/5.4

=67.5 days

365/6.19

=58.9 days

6. Accounts payable settlement period

Ratio Formula 2016 2015

Accounts payable settlement

period

Trade payable / COGS

*365

221761/835543

*365

=96.87 days

144140/7023

54*365

=74.90 days

6

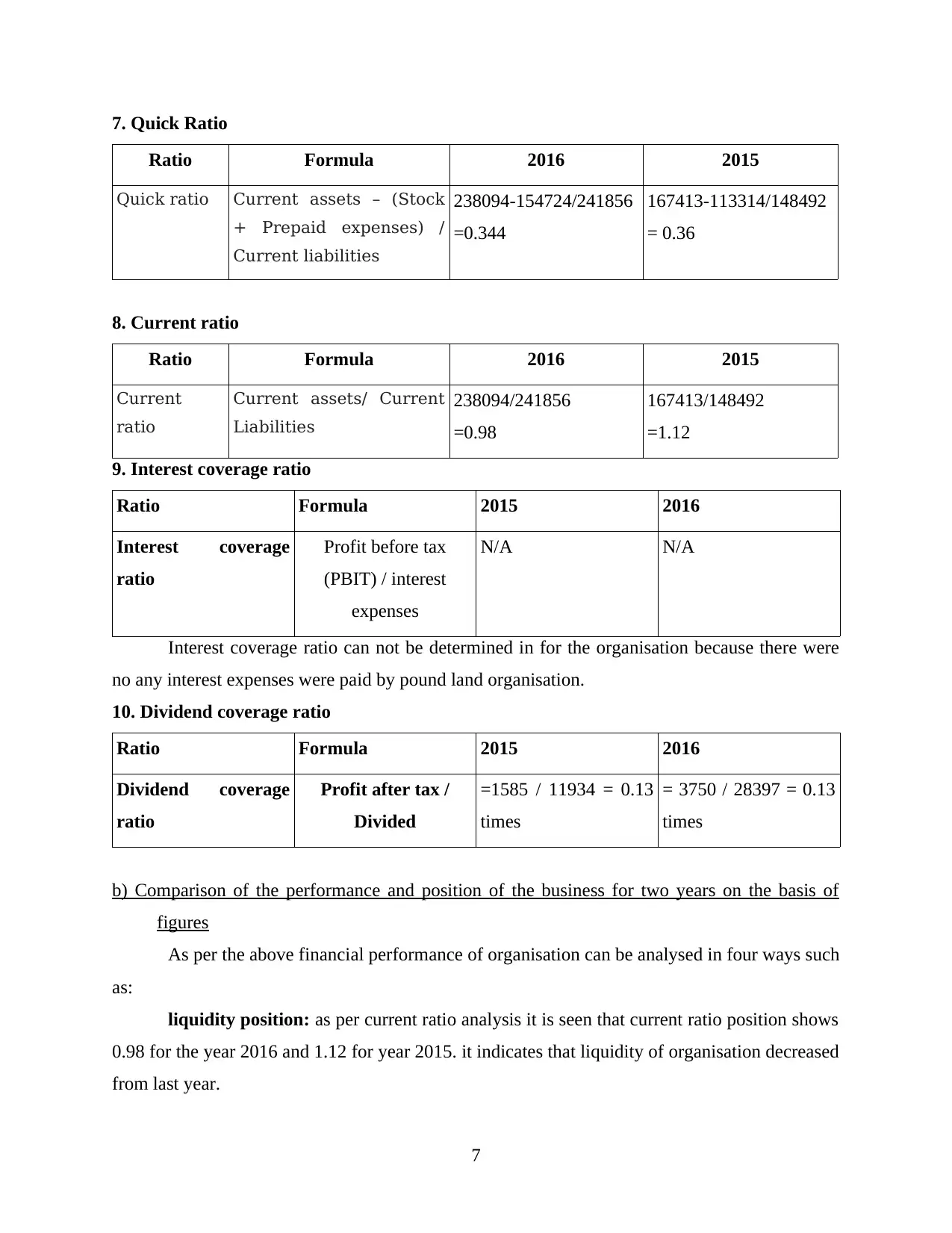

7. Quick Ratio

Ratio Formula 2016 2015

Quick ratio Current assets – (Stock

+ Prepaid expenses) /

Current liabilities

238094-154724/241856

=0.344

167413-113314/148492

= 0.36

8. Current ratio

Ratio Formula 2016 2015

Current

ratio

Current assets/ Current

Liabilities

238094/241856

=0.98

167413/148492

=1.12

9. Interest coverage ratio

Ratio Formula 2015 2016

Interest coverage

ratio

Profit before tax

(PBIT) / interest

expenses

N/A N/A

Interest coverage ratio can not be determined in for the organisation because there were

no any interest expenses were paid by pound land organisation.

10. Dividend coverage ratio

Ratio Formula 2015 2016

Dividend coverage

ratio

Profit after tax /

Divided

=1585 / 11934 = 0.13

times

= 3750 / 28397 = 0.13

times

b) Comparison of the performance and position of the business for two years on the basis of

figures

As per the above financial performance of organisation can be analysed in four ways such

as:

liquidity position: as per current ratio analysis it is seen that current ratio position shows

0.98 for the year 2016 and 1.12 for year 2015. it indicates that liquidity of organisation decreased

from last year.

7

Ratio Formula 2016 2015

Quick ratio Current assets – (Stock

+ Prepaid expenses) /

Current liabilities

238094-154724/241856

=0.344

167413-113314/148492

= 0.36

8. Current ratio

Ratio Formula 2016 2015

Current

ratio

Current assets/ Current

Liabilities

238094/241856

=0.98

167413/148492

=1.12

9. Interest coverage ratio

Ratio Formula 2015 2016

Interest coverage

ratio

Profit before tax

(PBIT) / interest

expenses

N/A N/A

Interest coverage ratio can not be determined in for the organisation because there were

no any interest expenses were paid by pound land organisation.

10. Dividend coverage ratio

Ratio Formula 2015 2016

Dividend coverage

ratio

Profit after tax /

Divided

=1585 / 11934 = 0.13

times

= 3750 / 28397 = 0.13

times

b) Comparison of the performance and position of the business for two years on the basis of

figures

As per the above financial performance of organisation can be analysed in four ways such

as:

liquidity position: as per current ratio analysis it is seen that current ratio position shows

0.98 for the year 2016 and 1.12 for year 2015. it indicates that liquidity of organisation decreased

from last year.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability position: it is seen that gross profit margin was calculated as 36.98% for

the year ended 2016 and 37.11% for the year 2015. Net profit margin ratio for 2015 2.54% and

0.11% in respect of 2016. profitability also get decreased for the upcoming year.

Debt position: return on capital employed is calculated for the year 2015 was calculated

as 21.63% and 1.81% for the year ended 2014. as per above analysis it is seen that the return also

get decreased for subsequent years.

Operating Performance: dividend ratio was calculated for both the year was calculated

same which is .13 times. Account receivable collection ratio is calculated as 75 days for 2015

and 68 days for the year 2015.

as per above analysis of financial performance it is seen that profitability of organisation

decreased from the year 2015 to 2016. due to long term debts and liabilities.

CONCLUSION

This report is prepared to define the importance of financial management in order to

maintain financial resources. There is a difference between financial accountants and

management accountants. Financial information needs are defined in respect of stakeholders.

Types of financial statements are defined for non-profit organisations and profit organisation.

Financial analysis also done in respect of Poundland group plc. Financial performance of

organisation also defined in this context.

8

the year ended 2016 and 37.11% for the year 2015. Net profit margin ratio for 2015 2.54% and

0.11% in respect of 2016. profitability also get decreased for the upcoming year.

Debt position: return on capital employed is calculated for the year 2015 was calculated

as 21.63% and 1.81% for the year ended 2014. as per above analysis it is seen that the return also

get decreased for subsequent years.

Operating Performance: dividend ratio was calculated for both the year was calculated

same which is .13 times. Account receivable collection ratio is calculated as 75 days for 2015

and 68 days for the year 2015.

as per above analysis of financial performance it is seen that profitability of organisation

decreased from the year 2015 to 2016. due to long term debts and liabilities.

CONCLUSION

This report is prepared to define the importance of financial management in order to

maintain financial resources. There is a difference between financial accountants and

management accountants. Financial information needs are defined in respect of stakeholders.

Types of financial statements are defined for non-profit organisations and profit organisation.

Financial analysis also done in respect of Poundland group plc. Financial performance of

organisation also defined in this context.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Ashwell, M., 2014. Managing Financial Resources. Developing Skills for Business Leadership,

p.401.

Bridoux, F. and Stoelhorst, J.W., 2014. Microfoundations for stakeholder theory: Managing

stakeholders with heterogeneous motives. Strategic Management Journal, 35(1),

pp.107-125.

Cascio, W., 2018. Managing human resources. McGraw-Hill Education.

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning, 48(1), pp.35-45.

Forsgren, M., 2015. Managing the Internationalization Process (routledge Revivals): The

Swedish Case. Routledge.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and Using Information

Systems, Binder Ready Version: A Strategic Approach. John Wiley & Sons.

Purce, J., 2014. The impact of corporate strategy on human resource management. New

Perspectives on Human Resource Management (Routledge Revivals), 67.

Smith, W.K., 2014. Dynamic decision making: A model of senior leaders managing strategic

paradoxes. Academy of Management Journal, 57(6), pp.1592-1623.

Snell, S.A., Morris, S. and Bohlander, G.W., 2015. Managing human resources. Nelson

Education.

Taylor, T., Doherty, A. and McGraw, P., 2015. Managing people in sport organizations: A

strategic human resource management perspective. Routledge.

Online

financial ratios, 2017. [Online]. Available through:

<https://www.investopedia.com/university/ratio-analysis/using-ratios.asp>.

9

Books and Journals:

Ashwell, M., 2014. Managing Financial Resources. Developing Skills for Business Leadership,

p.401.

Bridoux, F. and Stoelhorst, J.W., 2014. Microfoundations for stakeholder theory: Managing

stakeholders with heterogeneous motives. Strategic Management Journal, 35(1),

pp.107-125.

Cascio, W., 2018. Managing human resources. McGraw-Hill Education.

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning, 48(1), pp.35-45.

Forsgren, M., 2015. Managing the Internationalization Process (routledge Revivals): The

Swedish Case. Routledge.

Pearlson, K.E., Saunders, C.S. and Galletta, D.F., 2016. Managing and Using Information

Systems, Binder Ready Version: A Strategic Approach. John Wiley & Sons.

Purce, J., 2014. The impact of corporate strategy on human resource management. New

Perspectives on Human Resource Management (Routledge Revivals), 67.

Smith, W.K., 2014. Dynamic decision making: A model of senior leaders managing strategic

paradoxes. Academy of Management Journal, 57(6), pp.1592-1623.

Snell, S.A., Morris, S. and Bohlander, G.W., 2015. Managing human resources. Nelson

Education.

Taylor, T., Doherty, A. and McGraw, P., 2015. Managing people in sport organizations: A

strategic human resource management perspective. Routledge.

Online

financial ratios, 2017. [Online]. Available through:

<https://www.investopedia.com/university/ratio-analysis/using-ratios.asp>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.