Analyzing Financial Statements and Managing Resources Report

VerifiedAdded on 2022/12/14

|15

|4272

|384

Report

AI Summary

This report provides a comprehensive analysis of financial resource management, covering key aspects such as financial statements, ratio analysis, and the identification of stakeholder needs. The report delves into the interpretation of financial ratios, including profitability, liquidity, and solvency ratios, to assess a company's performance. It also examines the financial information needs of different stakeholders, such as board members, shareholders, banks, customers, creditors, and competitors. Furthermore, the report explores the concept of cost-plus pricing, its implementation challenges, and its benefits. The analysis includes two assignments focusing on financial statement analysis, ratio interpretation, and the importance of resource management for overall business efficiency and decision-making. This report provides insights into how businesses can effectively manage their financial resources to improve profitability and achieve their strategic goals.

Managing financial

resources

resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

Assignment 1...................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Q1. Identifying the various financial statements and financial ratios.........................................1

Q2. Interpret the financial ratios of the company........................................................................3

Q3. Identifying the financial information needs of different stakeholders..................................5

CONCLUSION................................................................................................................................6

Assignment 2...................................................................................................................................7

INTRODUCTION...........................................................................................................................7

MAIN BODY..................................................................................................................................7

Question 2. Identifying the meaning of cost-plus pricing and problems using this approach.....7

Question 3. Identifying the financial ratios of the company.......................................................8

Question 4. Analysing the terms..................................................................................................9

Conclusion.....................................................................................................................................11

REFERENCES..............................................................................................................................12

Contents...........................................................................................................................................2

Assignment 1...................................................................................................................................1

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Q1. Identifying the various financial statements and financial ratios.........................................1

Q2. Interpret the financial ratios of the company........................................................................3

Q3. Identifying the financial information needs of different stakeholders..................................5

CONCLUSION................................................................................................................................6

Assignment 2...................................................................................................................................7

INTRODUCTION...........................................................................................................................7

MAIN BODY..................................................................................................................................7

Question 2. Identifying the meaning of cost-plus pricing and problems using this approach.....7

Question 3. Identifying the financial ratios of the company.......................................................8

Question 4. Analysing the terms..................................................................................................9

Conclusion.....................................................................................................................................11

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assignment 1

INTRODUCTION

To ensure the organization's efficiency, resource management means effectively controlling

and tracking the various resources that are used (Zachosova, 2019). They contribute to

improving the company's working performance, which is done and accomplished by employees

and management. It is important to recognise the company's structure and requirements in order

to efficiently manage them, which can be achieved by examining the company's overall role. The

ability to successfully manage resources and other factors helps in assessing the firm's overall

effectiveness. This article looks at various financial ratios and income statements, and also the

financial data availability of different stakeholders. Aside from that, evaluating the sense of cost-

plus pricing and researching the problems with the strategy. This also involves the numerous

variances that help in determining the firm's effectiveness, which leads to a number of

management benefits aimed at increasing profitability.

MAIN BODY

Q1. Identifying the various financial statements and financial ratios

Financial statements are records that show a company's financial performance at the end of

the year in detail. It shows the official records of all required financial transactions that take

place in the company. They aid information users in assessing the financial health, liquidity, and

productivity of an organisation. This represents the company's financial implications of the deal.

Financial statements are used to calculate profits and are an essential part of an annual report of

the company. A list of financial statements is given below:

Income statements- This is the accounting information that many companies use to

reflect on their financial performance over time. The revenue and expense statements for

a particular year are also known as profit and loss statements. Any of the elements are as

follows:

Revenue- It refers to a company's sales of goods and services within a given accounting

period. This information can be gathered from both cash and credit transactions, and it can be

used to determine efficiency and reap a variety of benefits.

INTRODUCTION

To ensure the organization's efficiency, resource management means effectively controlling

and tracking the various resources that are used (Zachosova, 2019). They contribute to

improving the company's working performance, which is done and accomplished by employees

and management. It is important to recognise the company's structure and requirements in order

to efficiently manage them, which can be achieved by examining the company's overall role. The

ability to successfully manage resources and other factors helps in assessing the firm's overall

effectiveness. This article looks at various financial ratios and income statements, and also the

financial data availability of different stakeholders. Aside from that, evaluating the sense of cost-

plus pricing and researching the problems with the strategy. This also involves the numerous

variances that help in determining the firm's effectiveness, which leads to a number of

management benefits aimed at increasing profitability.

MAIN BODY

Q1. Identifying the various financial statements and financial ratios

Financial statements are records that show a company's financial performance at the end of

the year in detail. It shows the official records of all required financial transactions that take

place in the company. They aid information users in assessing the financial health, liquidity, and

productivity of an organisation. This represents the company's financial implications of the deal.

Financial statements are used to calculate profits and are an essential part of an annual report of

the company. A list of financial statements is given below:

Income statements- This is the accounting information that many companies use to

reflect on their financial performance over time. The revenue and expense statements for

a particular year are also known as profit and loss statements. Any of the elements are as

follows:

Revenue- It refers to a company's sales of goods and services within a given accounting

period. This information can be gathered from both cash and credit transactions, and it can be

used to determine efficiency and reap a variety of benefits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit and loss- Benefit or loss refers to the net profits received after deducting expenses

from revenue. Benefit will occur if revenue exceeds expenditures; if expenses surpass revenue, a

loss will result (Sansa, 2020).

Expenses- This is the day-to-day expense of doing business that a company incurs.

Operating expenses include things like salaries and depreciation.

Balance sheet- The asset, liability, and equity positions at the end of the accounting

period are depicted on the balance sheet, also known as the statements of financial

condition. This is an important feature of the financial report because it helps users of

financial statements who are looking for details about the company's financial status. This

assists in the assessment of the company's success and efficacy, and the execution of vital

strategic decisions.

Statements of cash flow- This is a compilation of financial statements that describes

both cash inflows and outflows from the company's ongoing operations and international

sources. It also provides all cash outflows for business activities and acquisitions over

time, as well as a rundown of all transactions for the investor. The cash flow has three

sections that can help an investor determine the stock of a business. The three types of

activities involved in this are operating activities, spending activities, and funding

activities. Each company has its own way of measuring efficiency and managing cash

flow.

Ratio analysis- It is the process of examining various pieces of financial data found in a

company's financial statements in order to evaluate the firm's effectiveness and profitability. This

is mainly used by the external analyst to evaluate various aspects of the firm, such as profitability

ratios, liquidity, and solvency. This is very useful for calculating cumulative outcomes of

different ratios. Some of the ratios are as follows:

Liquidity ratio- This calculates a company's capacity to complete an obligation using

existing assets when it is in financial trouble and unable to pay its debts and obligations.

It can quickly convert its assets into cash and use that money to pay off any debts it owes.

A few examples include the current ratio, quick ratio, and cash ratio (Kuisma, 2017).

Solvency ratio- To assess a company's long-term financial stability, this ratio compares

its debt levels to its assets and annual earnings. Related ratios include the debt to capital

ratio, debt ratio, interest coverage ratio, and equity multiplier. Governments, banks, staff,

from revenue. Benefit will occur if revenue exceeds expenditures; if expenses surpass revenue, a

loss will result (Sansa, 2020).

Expenses- This is the day-to-day expense of doing business that a company incurs.

Operating expenses include things like salaries and depreciation.

Balance sheet- The asset, liability, and equity positions at the end of the accounting

period are depicted on the balance sheet, also known as the statements of financial

condition. This is an important feature of the financial report because it helps users of

financial statements who are looking for details about the company's financial status. This

assists in the assessment of the company's success and efficacy, and the execution of vital

strategic decisions.

Statements of cash flow- This is a compilation of financial statements that describes

both cash inflows and outflows from the company's ongoing operations and international

sources. It also provides all cash outflows for business activities and acquisitions over

time, as well as a rundown of all transactions for the investor. The cash flow has three

sections that can help an investor determine the stock of a business. The three types of

activities involved in this are operating activities, spending activities, and funding

activities. Each company has its own way of measuring efficiency and managing cash

flow.

Ratio analysis- It is the process of examining various pieces of financial data found in a

company's financial statements in order to evaluate the firm's effectiveness and profitability. This

is mainly used by the external analyst to evaluate various aspects of the firm, such as profitability

ratios, liquidity, and solvency. This is very useful for calculating cumulative outcomes of

different ratios. Some of the ratios are as follows:

Liquidity ratio- This calculates a company's capacity to complete an obligation using

existing assets when it is in financial trouble and unable to pay its debts and obligations.

It can quickly convert its assets into cash and use that money to pay off any debts it owes.

A few examples include the current ratio, quick ratio, and cash ratio (Kuisma, 2017).

Solvency ratio- To assess a company's long-term financial stability, this ratio compares

its debt levels to its assets and annual earnings. Related ratios include the debt to capital

ratio, debt ratio, interest coverage ratio, and equity multiplier. Governments, banks, staff,

and institutional investors mainly use these to determine a company's solvency, helping

them to make informed investment and other decisions.

Profitability ratio- This measure evaluates a company's ability to make profits as well as

the associated costs. A higher profit ratio means that an organization's activities are more

profitable and competitive. Investors and others use this ratio is used to evaluate a company's

performance and make educated decisions about next steps. Return on equity, return on asset,

operating margin, gross margin, and return on invested capital are all important profitability

indicators. They are crucial in precisely determining the company's outcomes.

Q2. Interpret the financial ratios of the company

Following are the interpretation of financial ratios of the organisation are as follows-

Gross profit-

Year 2020

Gross profit 200000

Net sales 500000

GP Ratio 40

Gross profit is a profitability metric that measures the ratio of gross profit to sales. This

company's gross profit margin in 2020 will be 40%, which is a satisfactory level. A higher gross

margin means that the company was able to cover other expenses such as operating and funding

by effectively managing its cost of sales. As a result, the gross profit is stable (Voltan and De

Fuentes, 2016).

Expense ratio-

Year 2020

Administration

expenses 101000

Net sales 500000

Expense’s ratio 20.2

The cost ratio is a measurement of the relationship between operating costs and sales

value. These are required in order to calculate the percentage of revenue consumed by various

operating expenses. This company's expenses are 20.2 percent, indicating just how much of cost

them to make informed investment and other decisions.

Profitability ratio- This measure evaluates a company's ability to make profits as well as

the associated costs. A higher profit ratio means that an organization's activities are more

profitable and competitive. Investors and others use this ratio is used to evaluate a company's

performance and make educated decisions about next steps. Return on equity, return on asset,

operating margin, gross margin, and return on invested capital are all important profitability

indicators. They are crucial in precisely determining the company's outcomes.

Q2. Interpret the financial ratios of the company

Following are the interpretation of financial ratios of the organisation are as follows-

Gross profit-

Year 2020

Gross profit 200000

Net sales 500000

GP Ratio 40

Gross profit is a profitability metric that measures the ratio of gross profit to sales. This

company's gross profit margin in 2020 will be 40%, which is a satisfactory level. A higher gross

margin means that the company was able to cover other expenses such as operating and funding

by effectively managing its cost of sales. As a result, the gross profit is stable (Voltan and De

Fuentes, 2016).

Expense ratio-

Year 2020

Administration

expenses 101000

Net sales 500000

Expense’s ratio 20.2

The cost ratio is a measurement of the relationship between operating costs and sales

value. These are required in order to calculate the percentage of revenue consumed by various

operating expenses. This company's expenses are 20.2 percent, indicating just how much of cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio is borne by revenue and how much of the expense and sales ratio is interrelated, as well as

the business's efficiency and effectiveness.

Net profit-

Year 2020

Net profit 84000

Net sales 500000

Net profit ratio 16.8

The percentage relationship between net profit and net sales can be expressed. Gross

profit minus operating expenses and income tax equals net profit. In the above table, the Net

Profit Ratio is 16.8 percent, showing that the company is more profitable and efficient. This ratio

helps in the analysis of overall effectiveness, and further steps to improve production and

increase efficiency can be taken through the sector. The company has a high net profit margin as

a result of its ability to manage costs efficiently (Holm, Drogendijk and ul Haq, 2020).

Operating ratio-

Year 2020

Cost of goods sold 300000

Operating expenses 113000

Net sales 500000

Operating ratio 82.6

The operating ratio compares gross operating costs to net sales to assess a company's

management efficiency. The lower the figure, the more successful the company is at generating

revenue and cutting costs. The company's ratio is 85 percent, which is better than what

management would like to achieve. This means that the company's costs are greater than the

amount of money it has received in sales. The business benefits from lowering the ratio, but the

company's efficiency suffers as a result.

Operating profit ratio-

Year 2020

Sales 500000

Cost of goods sold 300000

the business's efficiency and effectiveness.

Net profit-

Year 2020

Net profit 84000

Net sales 500000

Net profit ratio 16.8

The percentage relationship between net profit and net sales can be expressed. Gross

profit minus operating expenses and income tax equals net profit. In the above table, the Net

Profit Ratio is 16.8 percent, showing that the company is more profitable and efficient. This ratio

helps in the analysis of overall effectiveness, and further steps to improve production and

increase efficiency can be taken through the sector. The company has a high net profit margin as

a result of its ability to manage costs efficiently (Holm, Drogendijk and ul Haq, 2020).

Operating ratio-

Year 2020

Cost of goods sold 300000

Operating expenses 113000

Net sales 500000

Operating ratio 82.6

The operating ratio compares gross operating costs to net sales to assess a company's

management efficiency. The lower the figure, the more successful the company is at generating

revenue and cutting costs. The company's ratio is 85 percent, which is better than what

management would like to achieve. This means that the company's costs are greater than the

amount of money it has received in sales. The business benefits from lowering the ratio, but the

company's efficiency suffers as a result.

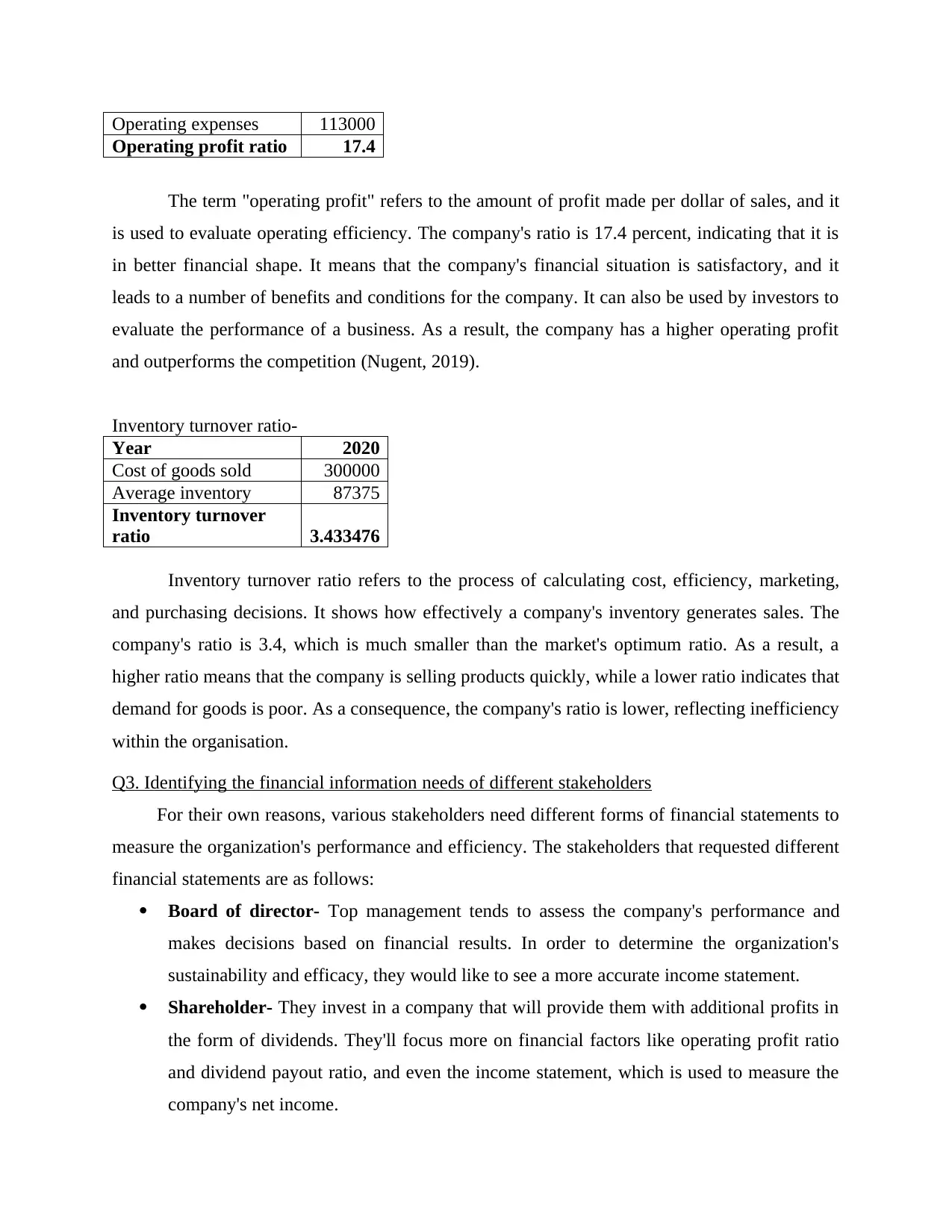

Operating profit ratio-

Year 2020

Sales 500000

Cost of goods sold 300000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Operating expenses 113000

Operating profit ratio 17.4

The term "operating profit" refers to the amount of profit made per dollar of sales, and it

is used to evaluate operating efficiency. The company's ratio is 17.4 percent, indicating that it is

in better financial shape. It means that the company's financial situation is satisfactory, and it

leads to a number of benefits and conditions for the company. It can also be used by investors to

evaluate the performance of a business. As a result, the company has a higher operating profit

and outperforms the competition (Nugent, 2019).

Inventory turnover ratio-

Year 2020

Cost of goods sold 300000

Average inventory 87375

Inventory turnover

ratio 3.433476

Inventory turnover ratio refers to the process of calculating cost, efficiency, marketing,

and purchasing decisions. It shows how effectively a company's inventory generates sales. The

company's ratio is 3.4, which is much smaller than the market's optimum ratio. As a result, a

higher ratio means that the company is selling products quickly, while a lower ratio indicates that

demand for goods is poor. As a consequence, the company's ratio is lower, reflecting inefficiency

within the organisation.

Q3. Identifying the financial information needs of different stakeholders

For their own reasons, various stakeholders need different forms of financial statements to

measure the organization's performance and efficiency. The stakeholders that requested different

financial statements are as follows:

Board of director- Top management tends to assess the company's performance and

makes decisions based on financial results. In order to determine the organization's

sustainability and efficacy, they would like to see a more accurate income statement.

Shareholder- They invest in a company that will provide them with additional profits in

the form of dividends. They'll focus more on financial factors like operating profit ratio

and dividend payout ratio, and even the income statement, which is used to measure the

company's net income.

Operating profit ratio 17.4

The term "operating profit" refers to the amount of profit made per dollar of sales, and it

is used to evaluate operating efficiency. The company's ratio is 17.4 percent, indicating that it is

in better financial shape. It means that the company's financial situation is satisfactory, and it

leads to a number of benefits and conditions for the company. It can also be used by investors to

evaluate the performance of a business. As a result, the company has a higher operating profit

and outperforms the competition (Nugent, 2019).

Inventory turnover ratio-

Year 2020

Cost of goods sold 300000

Average inventory 87375

Inventory turnover

ratio 3.433476

Inventory turnover ratio refers to the process of calculating cost, efficiency, marketing,

and purchasing decisions. It shows how effectively a company's inventory generates sales. The

company's ratio is 3.4, which is much smaller than the market's optimum ratio. As a result, a

higher ratio means that the company is selling products quickly, while a lower ratio indicates that

demand for goods is poor. As a consequence, the company's ratio is lower, reflecting inefficiency

within the organisation.

Q3. Identifying the financial information needs of different stakeholders

For their own reasons, various stakeholders need different forms of financial statements to

measure the organization's performance and efficiency. The stakeholders that requested different

financial statements are as follows:

Board of director- Top management tends to assess the company's performance and

makes decisions based on financial results. In order to determine the organization's

sustainability and efficacy, they would like to see a more accurate income statement.

Shareholder- They invest in a company that will provide them with additional profits in

the form of dividends. They'll focus more on financial factors like operating profit ratio

and dividend payout ratio, and even the income statement, which is used to measure the

company's net income.

Banks- These individuals are deeply invested in the company and want to ensure that its

debts and other obligations are met. They used to take all of the required measures before

granting them loans, and as a result, they were able to make good decisions. It helps in

the assessment of a corporation's effectiveness, and they do so by reviewing the

company's cash flow and calculating the acid ratio to see if they can meet their liabilities

or not (ŠIKÝŘ, Sekerin and Gorokhova, 2018).

Customer- They care for the company's long-term viability as a reliable supplier and

sales price rises, among other things. They'd have to evaluate the company's efficiency

and growth. They would need to look at the financial statements and balance sheet to

assess the organization's performance.

Creditors- They are interested in the company and want to know about its liquidity and

dependability so that they can make timely transactions and keep a close eye on the

company's cash position. The balance sheet and income statement are among the

financial reports reviewed. Other financial ratios piqued their interest, such as the overall

payment period to accounts receivable expressed in days.

Competitors- They were also interested in the company's financial results to see whether

it was improving or deteriorating in comparison to its own. To do so, they must evaluate

and manage expenses and expenditures, as well as examine the income statement,

balance sheet, and cash flow statement to assess overall performance and make

correlations with other companies (Twerefou and Tutu, 2017).

CONCLUSION

According to the report, managing capital would help the business manage its overall

efficiency and output, which would be more beneficial to the company. This article discusses

financial statements that help in assessing an organization's performance, such as income

statements, balance sheets, and cash flow statements, as well as other financial ratios. Aside from

that, the different types of ratios used in calculating the performance of a company are being

decided. Identifying the numerous financial statements that have been used to assess the firm's

performance by various stakeholders.

debts and other obligations are met. They used to take all of the required measures before

granting them loans, and as a result, they were able to make good decisions. It helps in

the assessment of a corporation's effectiveness, and they do so by reviewing the

company's cash flow and calculating the acid ratio to see if they can meet their liabilities

or not (ŠIKÝŘ, Sekerin and Gorokhova, 2018).

Customer- They care for the company's long-term viability as a reliable supplier and

sales price rises, among other things. They'd have to evaluate the company's efficiency

and growth. They would need to look at the financial statements and balance sheet to

assess the organization's performance.

Creditors- They are interested in the company and want to know about its liquidity and

dependability so that they can make timely transactions and keep a close eye on the

company's cash position. The balance sheet and income statement are among the

financial reports reviewed. Other financial ratios piqued their interest, such as the overall

payment period to accounts receivable expressed in days.

Competitors- They were also interested in the company's financial results to see whether

it was improving or deteriorating in comparison to its own. To do so, they must evaluate

and manage expenses and expenditures, as well as examine the income statement,

balance sheet, and cash flow statement to assess overall performance and make

correlations with other companies (Twerefou and Tutu, 2017).

CONCLUSION

According to the report, managing capital would help the business manage its overall

efficiency and output, which would be more beneficial to the company. This article discusses

financial statements that help in assessing an organization's performance, such as income

statements, balance sheets, and cash flow statements, as well as other financial ratios. Aside from

that, the different types of ratios used in calculating the performance of a company are being

decided. Identifying the numerous financial statements that have been used to assess the firm's

performance by various stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assignment 2

INTRODUCTION

The effectiveness of the company is calculated in this article, as well as the importance of

understanding the nature of cost-plus pricing, the complexities of applying this strategy in the

company, and the benefit of doing so (Haque, 2020). Aside from that, using those ratios to assess

the company's efficiency and liquidity will help you make better decisions. Identifying an entity's

cost and budget by examining the various variances used in the company.

MAIN BODY

Question 2. Identifying the meaning of cost-plus pricing and problems using this approach

Cost-plus pricing refers to a system in which a company calculates the cost of a product to

the company and then adds a percentage to the price to determine the selling price to the

customer. It's a simple cost-based pricing method for deciding the price of goods and services.

To determine the cost of providing a product or service, the direct material cost, direct labour

cost, and overhead must all be considered. A mark-up percentage is added to the net cost to

measure the selling price and profit. This necessitates a thorough understanding of all company

expenses and where they originate. This information is crucial for generating accurate cost

estimates, particularly for services and single-buyer products that were previously manufactured

for individual customers. Since it ignores competitor costs, this method is not acceptable for

deciding the price of a product that will be sold in a competitive environment.

Some problems are there while using this approach is as follows-

Limits price segmentation- As a result; the ability to price for different market segments

is essentially restricted. Setting prices based on how consumers segment value helps to

increase market capture. As a result, creativity is limited, and the ingenuity and

uniqueness of the products sold suffers as a result.

Lacks market orientation- The most critical mistake is that it fails to consider

marketability. A price is usually set without regard for whether or not a particular buyer

will consider the product to be great value at the time (González-Torres, Rodríguez-

Sánchez and Pelechano-Barahona, 2021).

INTRODUCTION

The effectiveness of the company is calculated in this article, as well as the importance of

understanding the nature of cost-plus pricing, the complexities of applying this strategy in the

company, and the benefit of doing so (Haque, 2020). Aside from that, using those ratios to assess

the company's efficiency and liquidity will help you make better decisions. Identifying an entity's

cost and budget by examining the various variances used in the company.

MAIN BODY

Question 2. Identifying the meaning of cost-plus pricing and problems using this approach

Cost-plus pricing refers to a system in which a company calculates the cost of a product to

the company and then adds a percentage to the price to determine the selling price to the

customer. It's a simple cost-based pricing method for deciding the price of goods and services.

To determine the cost of providing a product or service, the direct material cost, direct labour

cost, and overhead must all be considered. A mark-up percentage is added to the net cost to

measure the selling price and profit. This necessitates a thorough understanding of all company

expenses and where they originate. This information is crucial for generating accurate cost

estimates, particularly for services and single-buyer products that were previously manufactured

for individual customers. Since it ignores competitor costs, this method is not acceptable for

deciding the price of a product that will be sold in a competitive environment.

Some problems are there while using this approach is as follows-

Limits price segmentation- As a result; the ability to price for different market segments

is essentially restricted. Setting prices based on how consumers segment value helps to

increase market capture. As a result, creativity is limited, and the ingenuity and

uniqueness of the products sold suffers as a result.

Lacks market orientation- The most critical mistake is that it fails to consider

marketability. A price is usually set without regard for whether or not a particular buyer

will consider the product to be great value at the time (González-Torres, Rodríguez-

Sánchez and Pelechano-Barahona, 2021).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production inconsistency- This is a practical concern as well, since cost of production

are not constant, resulting in a moving target or the possibility of profit margin

fluctuations. The products used in the product, on the other hand, could become more

expensive or difficult to procure, reducing the firm's gross margin efficiency.

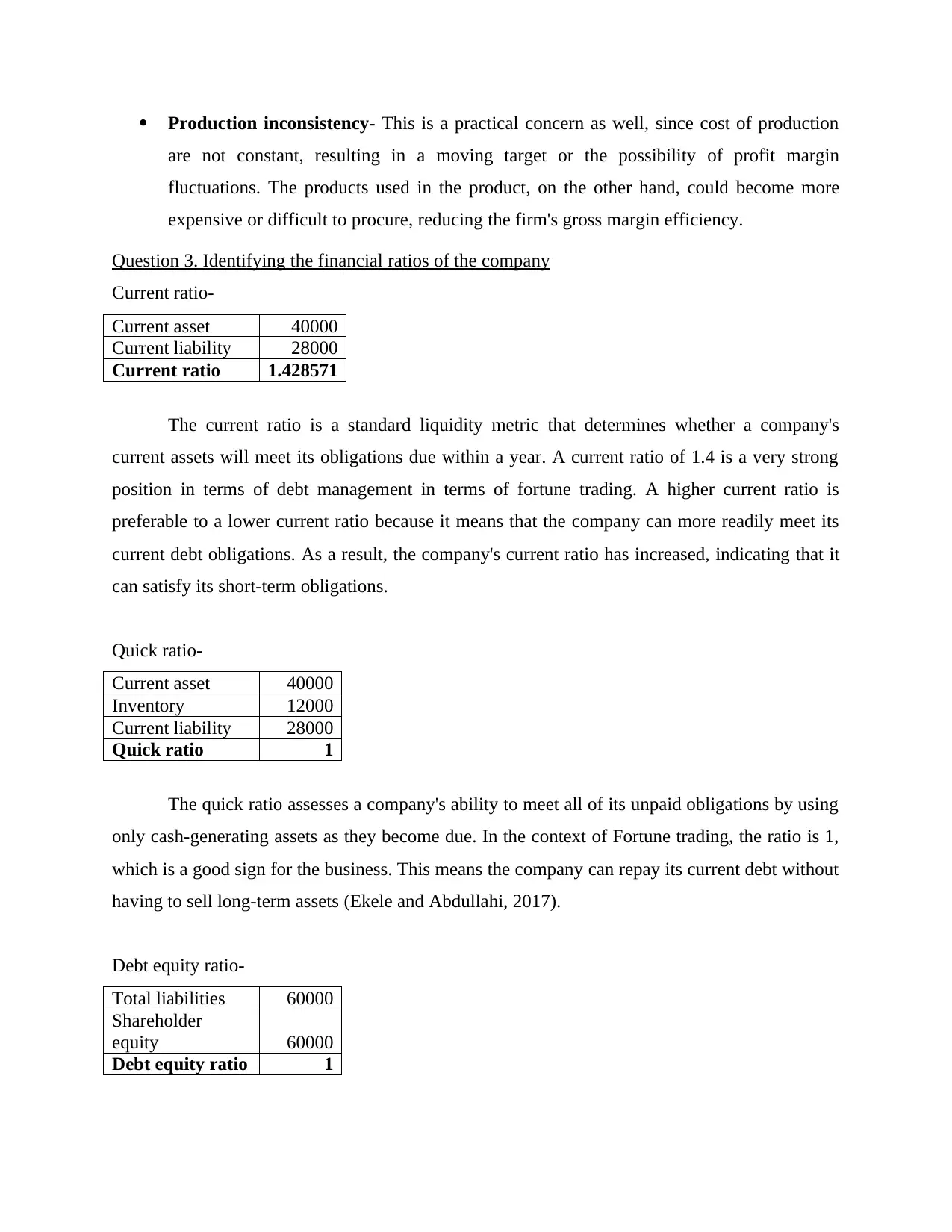

Question 3. Identifying the financial ratios of the company

Current ratio-

Current asset 40000

Current liability 28000

Current ratio 1.428571

The current ratio is a standard liquidity metric that determines whether a company's

current assets will meet its obligations due within a year. A current ratio of 1.4 is a very strong

position in terms of debt management in terms of fortune trading. A higher current ratio is

preferable to a lower current ratio because it means that the company can more readily meet its

current debt obligations. As a result, the company's current ratio has increased, indicating that it

can satisfy its short-term obligations.

Quick ratio-

Current asset 40000

Inventory 12000

Current liability 28000

Quick ratio 1

The quick ratio assesses a company's ability to meet all of its unpaid obligations by using

only cash-generating assets as they become due. In the context of Fortune trading, the ratio is 1,

which is a good sign for the business. This means the company can repay its current debt without

having to sell long-term assets (Ekele and Abdullahi, 2017).

Debt equity ratio-

Total liabilities 60000

Shareholder

equity 60000

Debt equity ratio 1

are not constant, resulting in a moving target or the possibility of profit margin

fluctuations. The products used in the product, on the other hand, could become more

expensive or difficult to procure, reducing the firm's gross margin efficiency.

Question 3. Identifying the financial ratios of the company

Current ratio-

Current asset 40000

Current liability 28000

Current ratio 1.428571

The current ratio is a standard liquidity metric that determines whether a company's

current assets will meet its obligations due within a year. A current ratio of 1.4 is a very strong

position in terms of debt management in terms of fortune trading. A higher current ratio is

preferable to a lower current ratio because it means that the company can more readily meet its

current debt obligations. As a result, the company's current ratio has increased, indicating that it

can satisfy its short-term obligations.

Quick ratio-

Current asset 40000

Inventory 12000

Current liability 28000

Quick ratio 1

The quick ratio assesses a company's ability to meet all of its unpaid obligations by using

only cash-generating assets as they become due. In the context of Fortune trading, the ratio is 1,

which is a good sign for the business. This means the company can repay its current debt without

having to sell long-term assets (Ekele and Abdullahi, 2017).

Debt equity ratio-

Total liabilities 60000

Shareholder

equity 60000

Debt equity ratio 1

Debt to equity is a measure that shows how volatile a company's debt status is and is used

to determine its financial leverage. In terms of Fortune trading, the ratio is 1, which is not a

positive sign for the company. It means that the company is paying its debt with its own money

and that the company is a high-risk investment. When the ratio of a business is less than one, it is

less volatile than when it is greater than one.

Proprietary ratio-

Shareholder

equity 60000

Total asset 120000

Proprietary ratio 0.5

The proprietary ratio represents the stockholder's contribution to the company's total

wealth, and as such, it gives a rough estimate of the amount of capitalization actually being used

to support the company. Fortune Trading has a debt-to-equity ratio of 0.5, which is not ideal

since the company's operations are heavily dependent on debt. As a result, a higher ratio

indicates that the scheme is stronger and that creditors are better protected (Berenguer and Shen,

2020).

Question 4. Analysing the terms

A financial budget is a budget for a business that distributes funds to different departments

and activities in order to efficiently control the company's cash flow. There are three parts of a

financial budget:

Cash budget- This section includes information about the company's cash inflows and

outflows. The process of preparing a company's cash flow is dynamic rather than static.

Budgeted Balance sheet- Other budgets, the most significant of which is the production

budget, are included.

Capital expenditure budget- This includes the company's machinery and facilities, as

well as any other capital assets.

Variance analysis- In this analysis, the discrepancy between actual and predicted behaviour

is quantified. This form of study is beneficial to business management. The variance analysis

would show a $2000 gap if the sales budget was $10000 and the real sales were $8000.

to determine its financial leverage. In terms of Fortune trading, the ratio is 1, which is not a

positive sign for the company. It means that the company is paying its debt with its own money

and that the company is a high-risk investment. When the ratio of a business is less than one, it is

less volatile than when it is greater than one.

Proprietary ratio-

Shareholder

equity 60000

Total asset 120000

Proprietary ratio 0.5

The proprietary ratio represents the stockholder's contribution to the company's total

wealth, and as such, it gives a rough estimate of the amount of capitalization actually being used

to support the company. Fortune Trading has a debt-to-equity ratio of 0.5, which is not ideal

since the company's operations are heavily dependent on debt. As a result, a higher ratio

indicates that the scheme is stronger and that creditors are better protected (Berenguer and Shen,

2020).

Question 4. Analysing the terms

A financial budget is a budget for a business that distributes funds to different departments

and activities in order to efficiently control the company's cash flow. There are three parts of a

financial budget:

Cash budget- This section includes information about the company's cash inflows and

outflows. The process of preparing a company's cash flow is dynamic rather than static.

Budgeted Balance sheet- Other budgets, the most significant of which is the production

budget, are included.

Capital expenditure budget- This includes the company's machinery and facilities, as

well as any other capital assets.

Variance analysis- In this analysis, the discrepancy between actual and predicted behaviour

is quantified. This form of study is beneficial to business management. The variance analysis

would show a $2000 gap if the sales budget was $10000 and the real sales were $8000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.