Financial Ratio Analysis and Investment Recommendations Report

VerifiedAdded on 2023/01/16

|11

|2313

|34

Report

AI Summary

This report presents a comprehensive financial analysis, evaluating the performance of two companies, Jones Ltd and Millet Ltd, through the computation and interpretation of various financial ratios. The analysis includes operating profit ratio, return on shareholders' funds, return on equity, inventory turnover, accounts receivables collection period, quick ratio, gearing ratio, interest cover ratio, dividend cover ratio, and dividend per share. The report then critically analyzes the limitations of financial ratios in decision-making, considering factors like historical data, aggregation, operational changes, accounting policies, company strategy, and inflation. Furthermore, the report delves into cost classification, including direct and indirect costs, functional classifications, and behavioral classifications (fixed, variable, and semi-variable costs). A job cost statement is framed, and the report concludes with a recommendation to the managers on whether to accept a quote, based on the financial analysis and profitability assessment. The report suggests accepting a quote of £7450.99 as it will generate sufficient profits.

Managing Financial Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................3

a. Computing ratios .....................................................................................................................3

b. Evaluating performance of both the organization and providing appropriate

recommendations within which Benns Ltd need to make investment ........................................4

c. Critically analysing limitation of the financial ratios in the process of decision making

within business enterprise ...........................................................................................................7

TASK 2............................................................................................................................................8

a. Determining several forms of the cost classification ..............................................................8

b. Framing a statement ................................................................................................................8

c. Advising the managers in relation to accept the quote or not ...............................................10

REFERENCES..............................................................................................................................11

TASK 1............................................................................................................................................3

a. Computing ratios .....................................................................................................................3

b. Evaluating performance of both the organization and providing appropriate

recommendations within which Benns Ltd need to make investment ........................................4

c. Critically analysing limitation of the financial ratios in the process of decision making

within business enterprise ...........................................................................................................7

TASK 2............................................................................................................................................8

a. Determining several forms of the cost classification ..............................................................8

b. Framing a statement ................................................................................................................8

c. Advising the managers in relation to accept the quote or not ...............................................10

REFERENCES..............................................................................................................................11

TASK 1

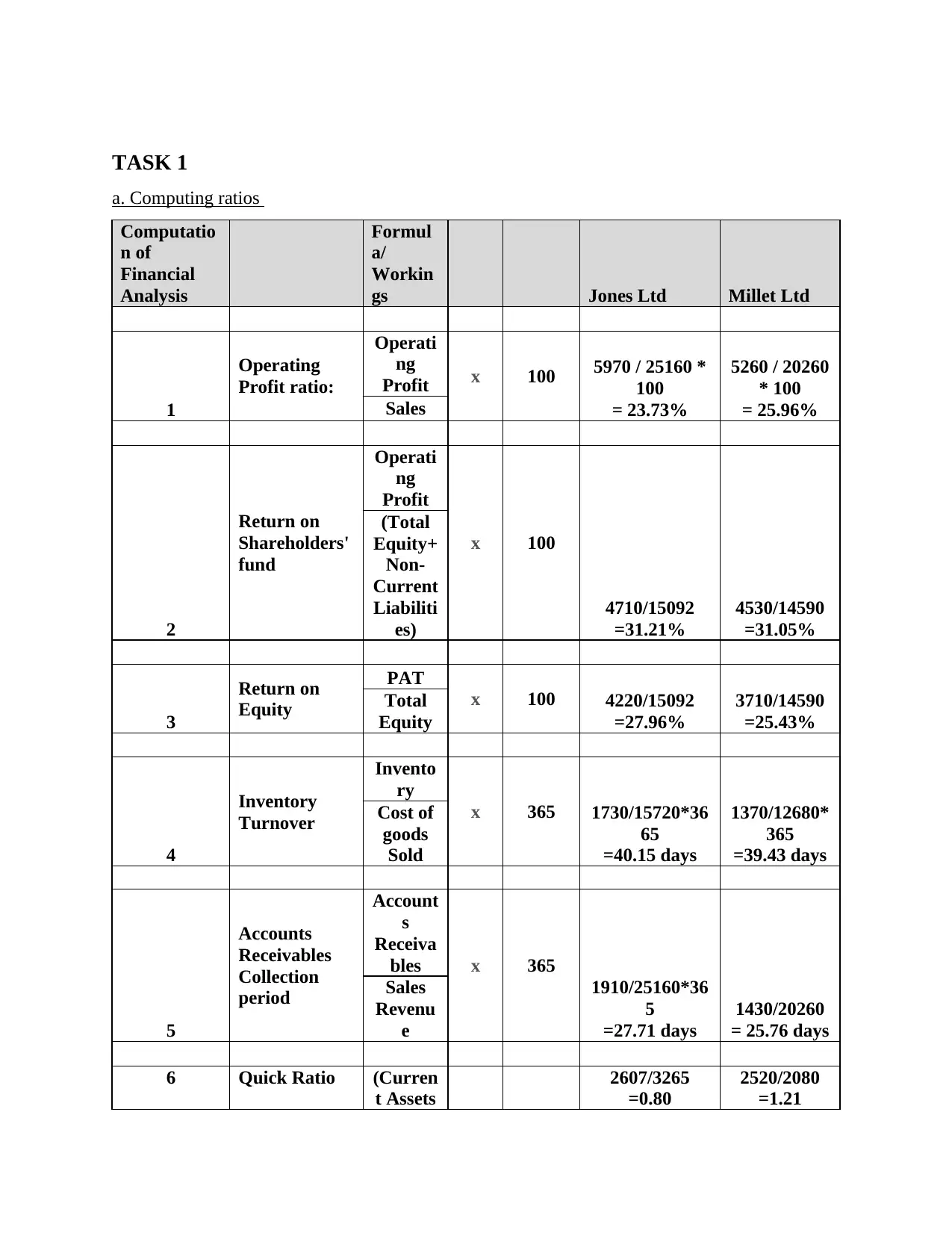

a. Computing ratios

Computatio

n of

Financial

Analysis

Formul

a/

Workin

gs Jones Ltd Millet Ltd

1

Operating

Profit ratio:

Operati

ng

Profit x 100 5970 / 25160 *

100

= 23.73%

5260 / 20260

* 100

= 25.96%Sales

2

Return on

Shareholders'

fund

Operati

ng

Profit

x 100

4710/15092

=31.21%

4530/14590

=31.05%

(Total

Equity+

Non-

Current

Liabiliti

es)

3

Return on

Equity

PAT

x 100 4220/15092

=27.96%

3710/14590

=25.43%

Total

Equity

4

Inventory

Turnover

Invento

ry

x 365 1730/15720*36

65

=40.15 days

1370/12680*

365

=39.43 days

Cost of

goods

Sold

5

Accounts

Receivables

Collection

period

Account

s

Receiva

bles x 365

1910/25160*36

5

=27.71 days

1430/20260

= 25.76 days

Sales

Revenu

e

6 Quick Ratio (Curren

t Assets

2607/3265

=0.80

2520/2080

=1.21

a. Computing ratios

Computatio

n of

Financial

Analysis

Formul

a/

Workin

gs Jones Ltd Millet Ltd

1

Operating

Profit ratio:

Operati

ng

Profit x 100 5970 / 25160 *

100

= 23.73%

5260 / 20260

* 100

= 25.96%Sales

2

Return on

Shareholders'

fund

Operati

ng

Profit

x 100

4710/15092

=31.21%

4530/14590

=31.05%

(Total

Equity+

Non-

Current

Liabiliti

es)

3

Return on

Equity

PAT

x 100 4220/15092

=27.96%

3710/14590

=25.43%

Total

Equity

4

Inventory

Turnover

Invento

ry

x 365 1730/15720*36

65

=40.15 days

1370/12680*

365

=39.43 days

Cost of

goods

Sold

5

Accounts

Receivables

Collection

period

Account

s

Receiva

bles x 365

1910/25160*36

5

=27.71 days

1430/20260

= 25.76 days

Sales

Revenu

e

6 Quick Ratio (Curren

t Assets

2607/3265

=0.80

2520/2080

=1.21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

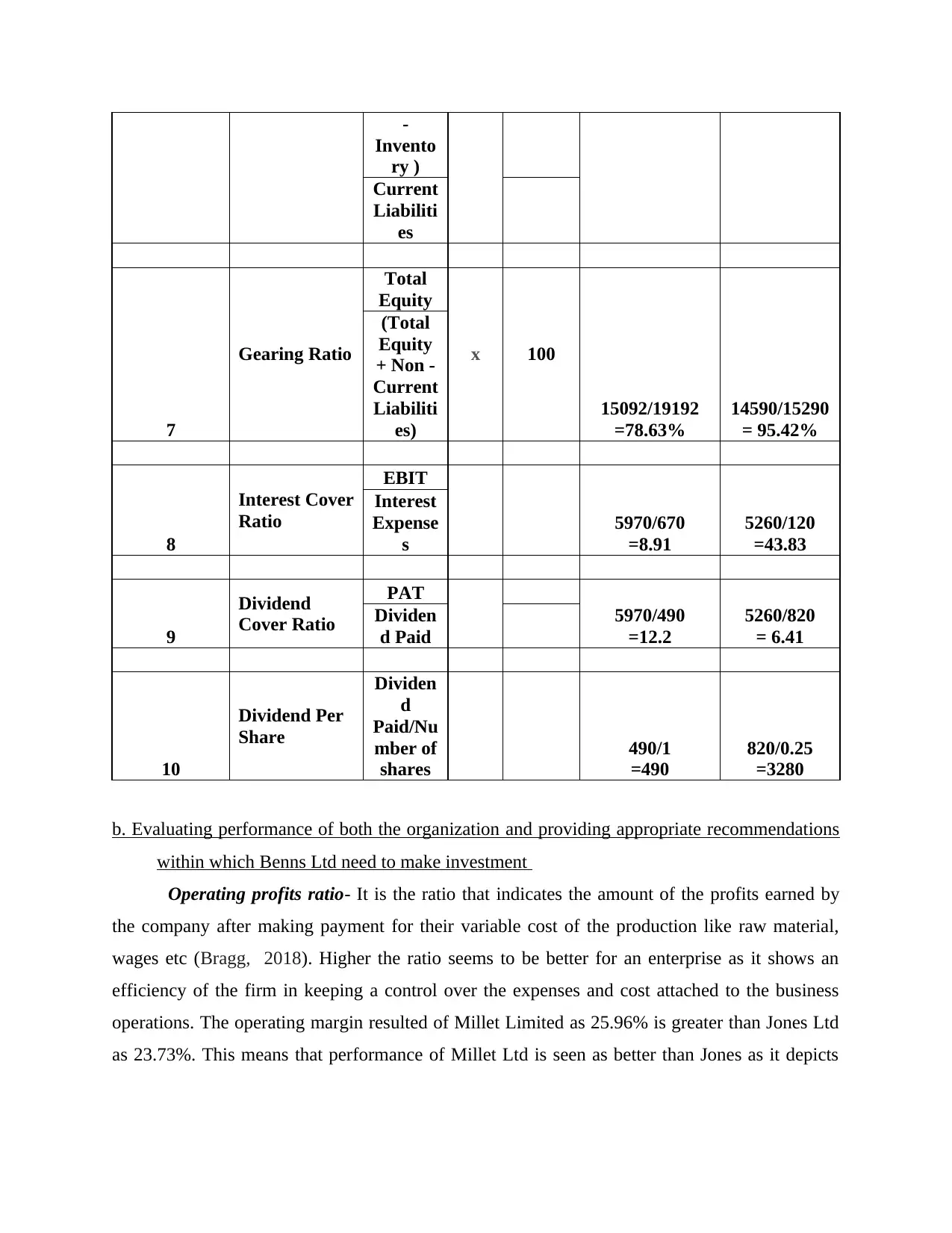

-

Invento

ry )

Current

Liabiliti

es

7

Gearing Ratio

Total

Equity

x 100

15092/19192

=78.63%

14590/15290

= 95.42%

(Total

Equity

+ Non -

Current

Liabiliti

es)

8

Interest Cover

Ratio

EBIT

5970/670

=8.91

5260/120

=43.83

Interest

Expense

s

9

Dividend

Cover Ratio

PAT

5970/490

=12.2

5260/820

= 6.41

Dividen

d Paid

10

Dividend Per

Share

Dividen

d

Paid/Nu

mber of

shares

490/1

=490

820/0.25

=3280

b. Evaluating performance of both the organization and providing appropriate recommendations

within which Benns Ltd need to make investment

Operating profits ratio- It is the ratio that indicates the amount of the profits earned by

the company after making payment for their variable cost of the production like raw material,

wages etc (Bragg, 2018). Higher the ratio seems to be better for an enterprise as it shows an

efficiency of the firm in keeping a control over the expenses and cost attached to the business

operations. The operating margin resulted of Millet Limited as 25.96% is greater than Jones Ltd

as 23.73%. This means that performance of Millet Ltd is seen as better than Jones as it depicts

Invento

ry )

Current

Liabiliti

es

7

Gearing Ratio

Total

Equity

x 100

15092/19192

=78.63%

14590/15290

= 95.42%

(Total

Equity

+ Non -

Current

Liabiliti

es)

8

Interest Cover

Ratio

EBIT

5970/670

=8.91

5260/120

=43.83

Interest

Expense

s

9

Dividend

Cover Ratio

PAT

5970/490

=12.2

5260/820

= 6.41

Dividen

d Paid

10

Dividend Per

Share

Dividen

d

Paid/Nu

mber of

shares

490/1

=490

820/0.25

=3280

b. Evaluating performance of both the organization and providing appropriate recommendations

within which Benns Ltd need to make investment

Operating profits ratio- It is the ratio that indicates the amount of the profits earned by

the company after making payment for their variable cost of the production like raw material,

wages etc (Bragg, 2018). Higher the ratio seems to be better for an enterprise as it shows an

efficiency of the firm in keeping a control over the expenses and cost attached to the business

operations. The operating margin resulted of Millet Limited as 25.96% is greater than Jones Ltd

as 23.73%. This means that performance of Millet Ltd is seen as better than Jones as it depicts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that former company is generating large amount of profits after paying off its that incurs in

relation to sales.

Return on the shareholders funds- It means a ratio regarding overall profitability that in

turn indicates profits accounted of an enterprise relating to funds that are been supplied by

owners or the shareholders. Higher percentage depicts that more amount of money has been

returned to the investors. The ratio of both the company resulted as 31% which means that both

the firms are facilitating sufficient amount of profits to their investors.

ROE- This profitability ratio measures capability of an entity in generating profits from

that of its investment in the firm. It shows the profits attained by the firm in respect of each

common stock. In accordance to the results generated, ROE of the Jones Ltd is higher that is

27.96% in comparison to Millet Ltd equating to 25.43%. This means that Jones made an efficient

use of equity for generating higher returns as compared to Millet.

ITR- It is counted as efficiency ratio which reflects the manner in which inventory could

be managed effectively by comparing it with the COGS with that of the average value of the

inventory for the particular accounting period. Higher value of the ratio is reflected as fast

moving inventory while the lower ratio seen as slow moving or an obsolete inventory within the

stock. The ITR of Millet Ltd is said to good because it takes only 39.3 days in converting its

inventory into the cash but Jones takes more time in turning out its inventory into the cash.

Accounts receivables days-It refers to number of days for which the customer invoice

remains outstanding prior to its collection. It is been measured for determining an effectiveness

of an entity's credit and the collection efforts for allowing the credit to the reputed customers and

also depicts an ability of the firm in collecting the cash from the customer within the specified

time-frame. Accounts receivable days of Millet Ltd depicted better from the above evaluation

than Jones Ltd because it collects the amount due in a timely manner and within less number

days in comparison to Jones. This in turn indicates that an entity does not leave it invoices

outstanding for longer time period.

Quick ratio- This ratio refers to an indicator of the firm's current liquidity position and

measures an ability of the company in meeting their short run obligations with majority of its

liquid assets. A quick ratio that resulted as higher than 1, it means it has enough number of quick

assets in order to meet its short term liabilities (Varadharajan and et.al., 2015). As the quick ratio

of Millet Ltd is higher than 1 that is 1.21 which clearly states that it has sufficient quick assets in

relation to sales.

Return on the shareholders funds- It means a ratio regarding overall profitability that in

turn indicates profits accounted of an enterprise relating to funds that are been supplied by

owners or the shareholders. Higher percentage depicts that more amount of money has been

returned to the investors. The ratio of both the company resulted as 31% which means that both

the firms are facilitating sufficient amount of profits to their investors.

ROE- This profitability ratio measures capability of an entity in generating profits from

that of its investment in the firm. It shows the profits attained by the firm in respect of each

common stock. In accordance to the results generated, ROE of the Jones Ltd is higher that is

27.96% in comparison to Millet Ltd equating to 25.43%. This means that Jones made an efficient

use of equity for generating higher returns as compared to Millet.

ITR- It is counted as efficiency ratio which reflects the manner in which inventory could

be managed effectively by comparing it with the COGS with that of the average value of the

inventory for the particular accounting period. Higher value of the ratio is reflected as fast

moving inventory while the lower ratio seen as slow moving or an obsolete inventory within the

stock. The ITR of Millet Ltd is said to good because it takes only 39.3 days in converting its

inventory into the cash but Jones takes more time in turning out its inventory into the cash.

Accounts receivables days-It refers to number of days for which the customer invoice

remains outstanding prior to its collection. It is been measured for determining an effectiveness

of an entity's credit and the collection efforts for allowing the credit to the reputed customers and

also depicts an ability of the firm in collecting the cash from the customer within the specified

time-frame. Accounts receivable days of Millet Ltd depicted better from the above evaluation

than Jones Ltd because it collects the amount due in a timely manner and within less number

days in comparison to Jones. This in turn indicates that an entity does not leave it invoices

outstanding for longer time period.

Quick ratio- This ratio refers to an indicator of the firm's current liquidity position and

measures an ability of the company in meeting their short run obligations with majority of its

liquid assets. A quick ratio that resulted as higher than 1, it means it has enough number of quick

assets in order to meet its short term liabilities (Varadharajan and et.al., 2015). As the quick ratio

of Millet Ltd is higher than 1 that is 1.21 which clearly states that it has sufficient quick assets in

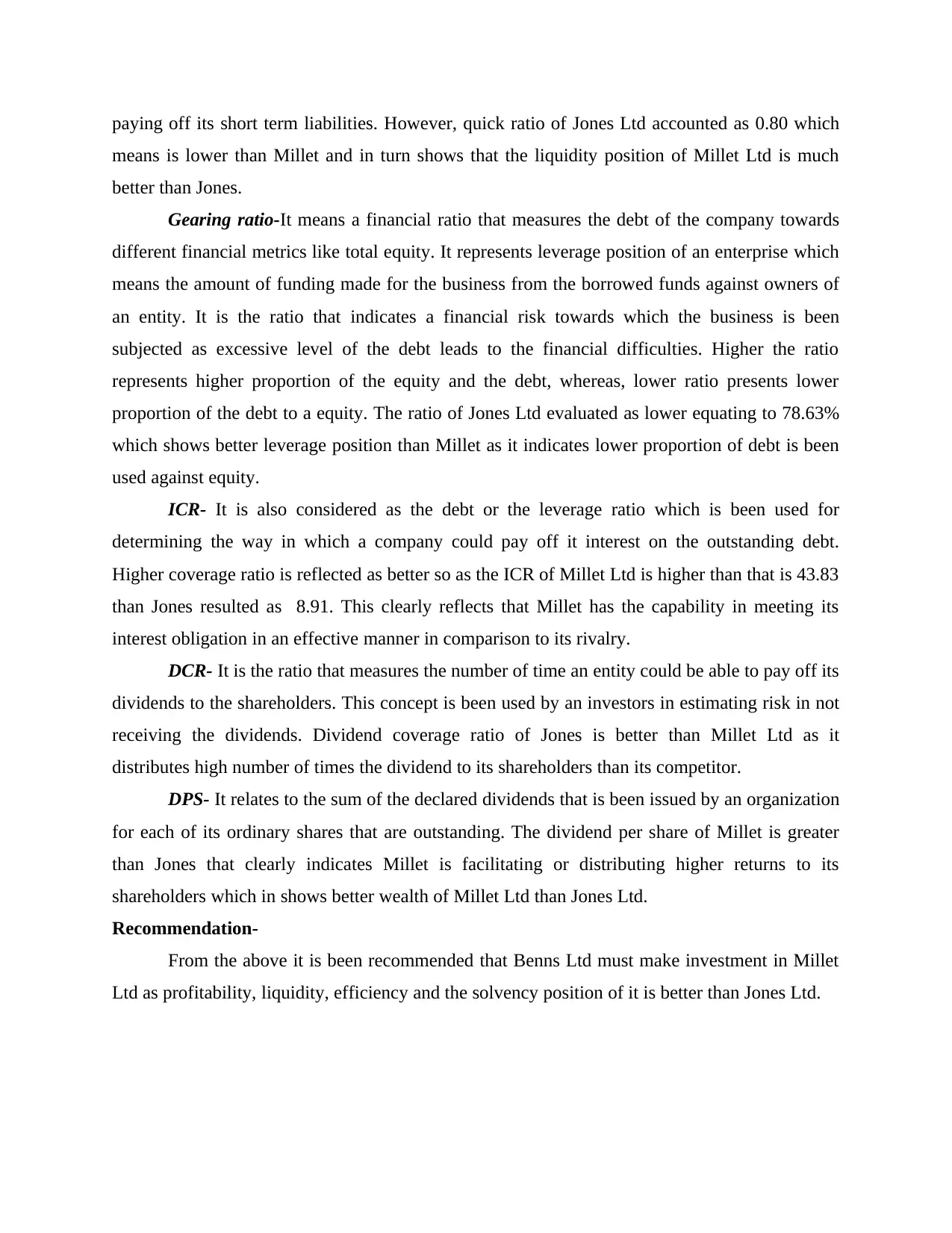

paying off its short term liabilities. However, quick ratio of Jones Ltd accounted as 0.80 which

means is lower than Millet and in turn shows that the liquidity position of Millet Ltd is much

better than Jones.

Gearing ratio-It means a financial ratio that measures the debt of the company towards

different financial metrics like total equity. It represents leverage position of an enterprise which

means the amount of funding made for the business from the borrowed funds against owners of

an entity. It is the ratio that indicates a financial risk towards which the business is been

subjected as excessive level of the debt leads to the financial difficulties. Higher the ratio

represents higher proportion of the equity and the debt, whereas, lower ratio presents lower

proportion of the debt to a equity. The ratio of Jones Ltd evaluated as lower equating to 78.63%

which shows better leverage position than Millet as it indicates lower proportion of debt is been

used against equity.

ICR- It is also considered as the debt or the leverage ratio which is been used for

determining the way in which a company could pay off it interest on the outstanding debt.

Higher coverage ratio is reflected as better so as the ICR of Millet Ltd is higher than that is 43.83

than Jones resulted as 8.91. This clearly reflects that Millet has the capability in meeting its

interest obligation in an effective manner in comparison to its rivalry.

DCR- It is the ratio that measures the number of time an entity could be able to pay off its

dividends to the shareholders. This concept is been used by an investors in estimating risk in not

receiving the dividends. Dividend coverage ratio of Jones is better than Millet Ltd as it

distributes high number of times the dividend to its shareholders than its competitor.

DPS- It relates to the sum of the declared dividends that is been issued by an organization

for each of its ordinary shares that are outstanding. The dividend per share of Millet is greater

than Jones that clearly indicates Millet is facilitating or distributing higher returns to its

shareholders which in shows better wealth of Millet Ltd than Jones Ltd.

Recommendation-

From the above it is been recommended that Benns Ltd must make investment in Millet

Ltd as profitability, liquidity, efficiency and the solvency position of it is better than Jones Ltd.

means is lower than Millet and in turn shows that the liquidity position of Millet Ltd is much

better than Jones.

Gearing ratio-It means a financial ratio that measures the debt of the company towards

different financial metrics like total equity. It represents leverage position of an enterprise which

means the amount of funding made for the business from the borrowed funds against owners of

an entity. It is the ratio that indicates a financial risk towards which the business is been

subjected as excessive level of the debt leads to the financial difficulties. Higher the ratio

represents higher proportion of the equity and the debt, whereas, lower ratio presents lower

proportion of the debt to a equity. The ratio of Jones Ltd evaluated as lower equating to 78.63%

which shows better leverage position than Millet as it indicates lower proportion of debt is been

used against equity.

ICR- It is also considered as the debt or the leverage ratio which is been used for

determining the way in which a company could pay off it interest on the outstanding debt.

Higher coverage ratio is reflected as better so as the ICR of Millet Ltd is higher than that is 43.83

than Jones resulted as 8.91. This clearly reflects that Millet has the capability in meeting its

interest obligation in an effective manner in comparison to its rivalry.

DCR- It is the ratio that measures the number of time an entity could be able to pay off its

dividends to the shareholders. This concept is been used by an investors in estimating risk in not

receiving the dividends. Dividend coverage ratio of Jones is better than Millet Ltd as it

distributes high number of times the dividend to its shareholders than its competitor.

DPS- It relates to the sum of the declared dividends that is been issued by an organization

for each of its ordinary shares that are outstanding. The dividend per share of Millet is greater

than Jones that clearly indicates Millet is facilitating or distributing higher returns to its

shareholders which in shows better wealth of Millet Ltd than Jones Ltd.

Recommendation-

From the above it is been recommended that Benns Ltd must make investment in Millet

Ltd as profitability, liquidity, efficiency and the solvency position of it is better than Jones Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

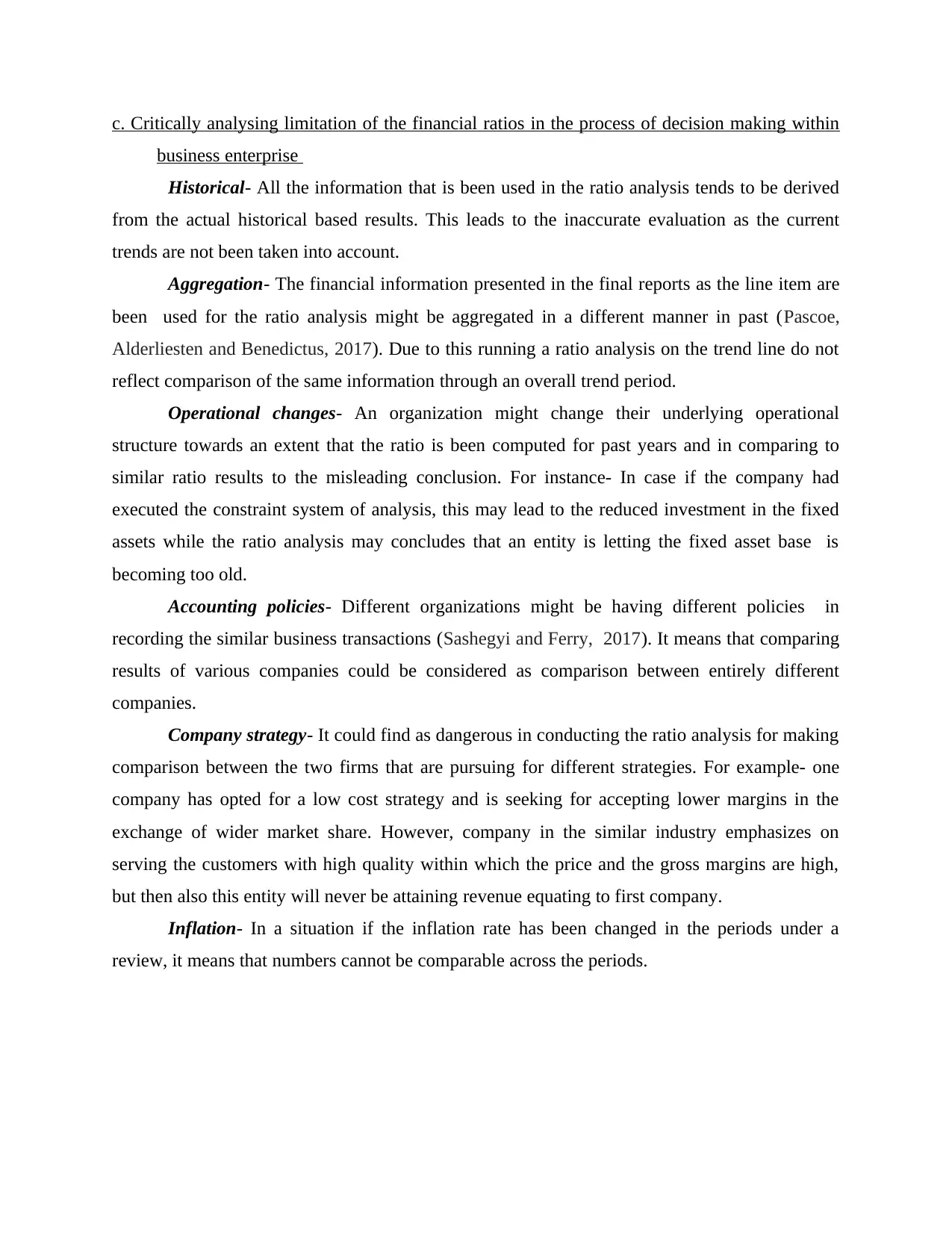

c. Critically analysing limitation of the financial ratios in the process of decision making within

business enterprise

Historical- All the information that is been used in the ratio analysis tends to be derived

from the actual historical based results. This leads to the inaccurate evaluation as the current

trends are not been taken into account.

Aggregation- The financial information presented in the final reports as the line item are

been used for the ratio analysis might be aggregated in a different manner in past (Pascoe,

Alderliesten and Benedictus, 2017). Due to this running a ratio analysis on the trend line do not

reflect comparison of the same information through an overall trend period.

Operational changes- An organization might change their underlying operational

structure towards an extent that the ratio is been computed for past years and in comparing to

similar ratio results to the misleading conclusion. For instance- In case if the company had

executed the constraint system of analysis, this may lead to the reduced investment in the fixed

assets while the ratio analysis may concludes that an entity is letting the fixed asset base is

becoming too old.

Accounting policies- Different organizations might be having different policies in

recording the similar business transactions (Sashegyi and Ferry, 2017). It means that comparing

results of various companies could be considered as comparison between entirely different

companies.

Company strategy- It could find as dangerous in conducting the ratio analysis for making

comparison between the two firms that are pursuing for different strategies. For example- one

company has opted for a low cost strategy and is seeking for accepting lower margins in the

exchange of wider market share. However, company in the similar industry emphasizes on

serving the customers with high quality within which the price and the gross margins are high,

but then also this entity will never be attaining revenue equating to first company.

Inflation- In a situation if the inflation rate has been changed in the periods under a

review, it means that numbers cannot be comparable across the periods.

business enterprise

Historical- All the information that is been used in the ratio analysis tends to be derived

from the actual historical based results. This leads to the inaccurate evaluation as the current

trends are not been taken into account.

Aggregation- The financial information presented in the final reports as the line item are

been used for the ratio analysis might be aggregated in a different manner in past (Pascoe,

Alderliesten and Benedictus, 2017). Due to this running a ratio analysis on the trend line do not

reflect comparison of the same information through an overall trend period.

Operational changes- An organization might change their underlying operational

structure towards an extent that the ratio is been computed for past years and in comparing to

similar ratio results to the misleading conclusion. For instance- In case if the company had

executed the constraint system of analysis, this may lead to the reduced investment in the fixed

assets while the ratio analysis may concludes that an entity is letting the fixed asset base is

becoming too old.

Accounting policies- Different organizations might be having different policies in

recording the similar business transactions (Sashegyi and Ferry, 2017). It means that comparing

results of various companies could be considered as comparison between entirely different

companies.

Company strategy- It could find as dangerous in conducting the ratio analysis for making

comparison between the two firms that are pursuing for different strategies. For example- one

company has opted for a low cost strategy and is seeking for accepting lower margins in the

exchange of wider market share. However, company in the similar industry emphasizes on

serving the customers with high quality within which the price and the gross margins are high,

but then also this entity will never be attaining revenue equating to first company.

Inflation- In a situation if the inflation rate has been changed in the periods under a

review, it means that numbers cannot be comparable across the periods.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

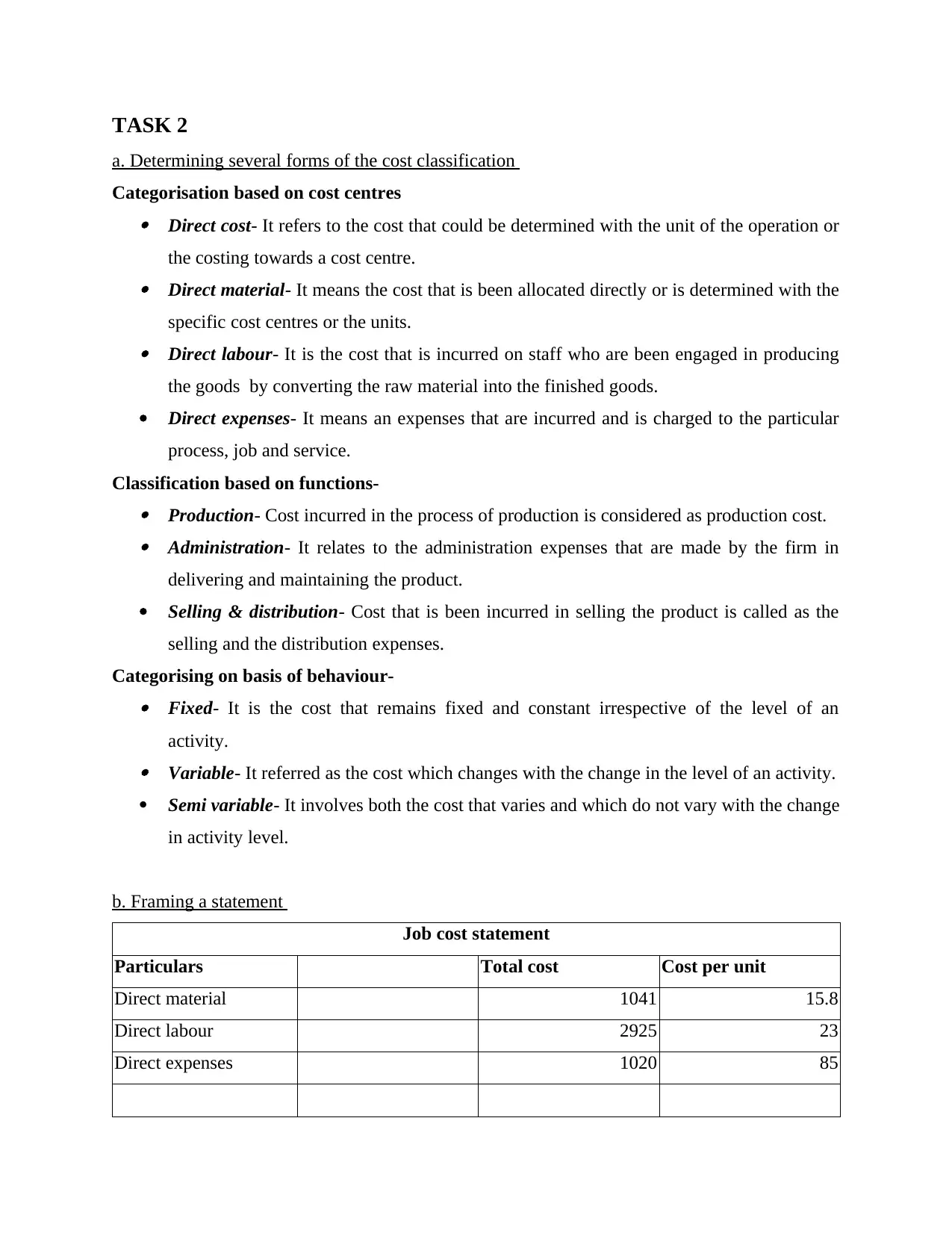

TASK 2

a. Determining several forms of the cost classification

Categorisation based on cost centres Direct cost- It refers to the cost that could be determined with the unit of the operation or

the costing towards a cost centre. Direct material- It means the cost that is been allocated directly or is determined with the

specific cost centres or the units. Direct labour- It is the cost that is incurred on staff who are been engaged in producing

the goods by converting the raw material into the finished goods.

Direct expenses- It means an expenses that are incurred and is charged to the particular

process, job and service.

Classification based on functions- Production- Cost incurred in the process of production is considered as production cost. Administration- It relates to the administration expenses that are made by the firm in

delivering and maintaining the product.

Selling & distribution- Cost that is been incurred in selling the product is called as the

selling and the distribution expenses.

Categorising on basis of behaviour- Fixed- It is the cost that remains fixed and constant irrespective of the level of an

activity. Variable- It referred as the cost which changes with the change in the level of an activity.

Semi variable- It involves both the cost that varies and which do not vary with the change

in activity level.

b. Framing a statement

Job cost statement

Particulars Total cost Cost per unit

Direct material 1041 15.8

Direct labour 2925 23

Direct expenses 1020 85

a. Determining several forms of the cost classification

Categorisation based on cost centres Direct cost- It refers to the cost that could be determined with the unit of the operation or

the costing towards a cost centre. Direct material- It means the cost that is been allocated directly or is determined with the

specific cost centres or the units. Direct labour- It is the cost that is incurred on staff who are been engaged in producing

the goods by converting the raw material into the finished goods.

Direct expenses- It means an expenses that are incurred and is charged to the particular

process, job and service.

Classification based on functions- Production- Cost incurred in the process of production is considered as production cost. Administration- It relates to the administration expenses that are made by the firm in

delivering and maintaining the product.

Selling & distribution- Cost that is been incurred in selling the product is called as the

selling and the distribution expenses.

Categorising on basis of behaviour- Fixed- It is the cost that remains fixed and constant irrespective of the level of an

activity. Variable- It referred as the cost which changes with the change in the level of an activity.

Semi variable- It involves both the cost that varies and which do not vary with the change

in activity level.

b. Framing a statement

Job cost statement

Particulars Total cost Cost per unit

Direct material 1041 15.8

Direct labour 2925 23

Direct expenses 1020 85

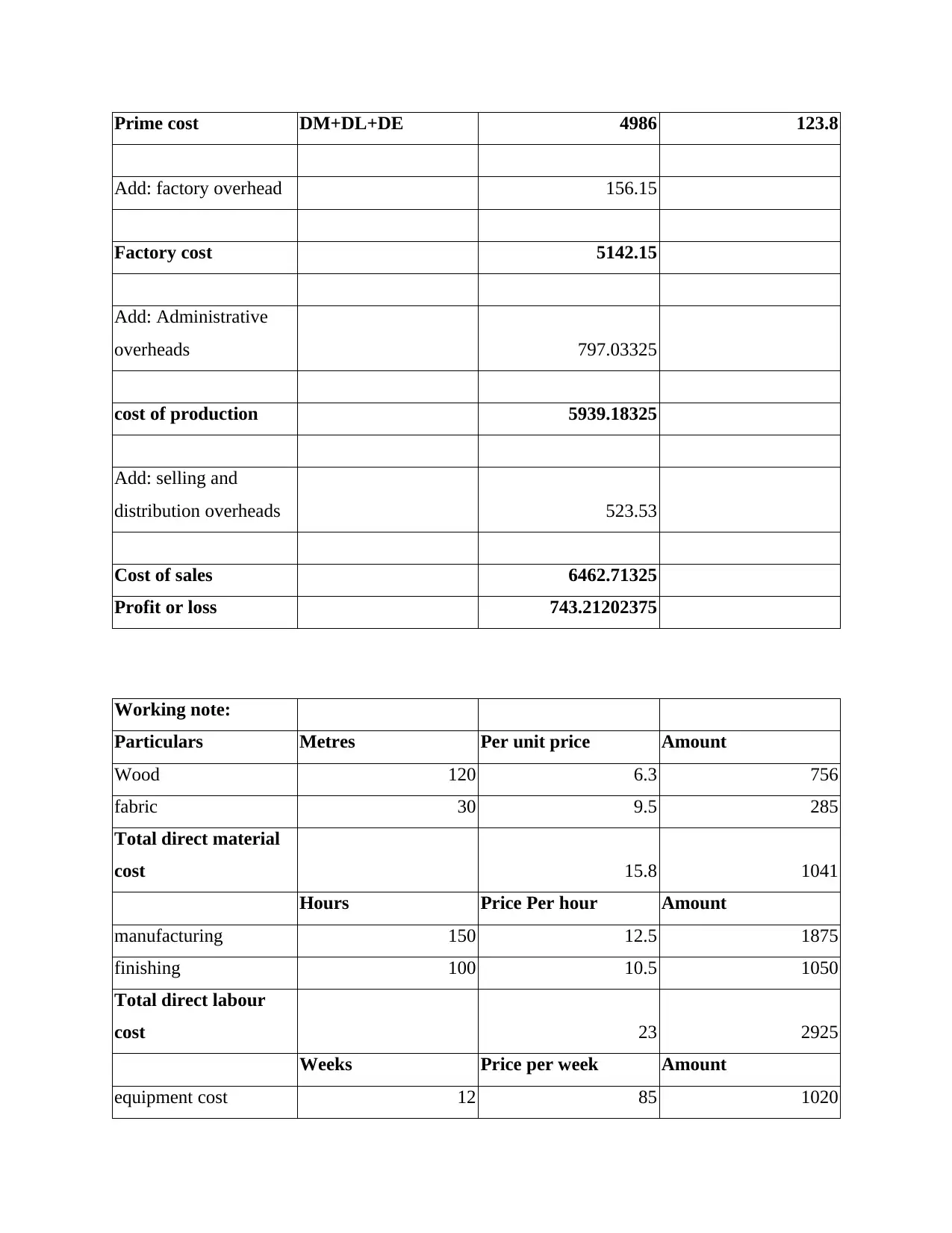

Prime cost DM+DL+DE 4986 123.8

Add: factory overhead 156.15

Factory cost 5142.15

Add: Administrative

overheads 797.03325

cost of production 5939.18325

Add: selling and

distribution overheads 523.53

Cost of sales 6462.71325

Profit or loss 743.21202375

Working note:

Particulars Metres Per unit price Amount

Wood 120 6.3 756

fabric 30 9.5 285

Total direct material

cost 15.8 1041

Hours Price Per hour Amount

manufacturing 150 12.5 1875

finishing 100 10.5 1050

Total direct labour

cost 23 2925

Weeks Price per week Amount

equipment cost 12 85 1020

Add: factory overhead 156.15

Factory cost 5142.15

Add: Administrative

overheads 797.03325

cost of production 5939.18325

Add: selling and

distribution overheads 523.53

Cost of sales 6462.71325

Profit or loss 743.21202375

Working note:

Particulars Metres Per unit price Amount

Wood 120 6.3 756

fabric 30 9.5 285

Total direct material

cost 15.8 1041

Hours Price Per hour Amount

manufacturing 150 12.5 1875

finishing 100 10.5 1050

Total direct labour

cost 23 2925

Weeks Price per week Amount

equipment cost 12 85 1020

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

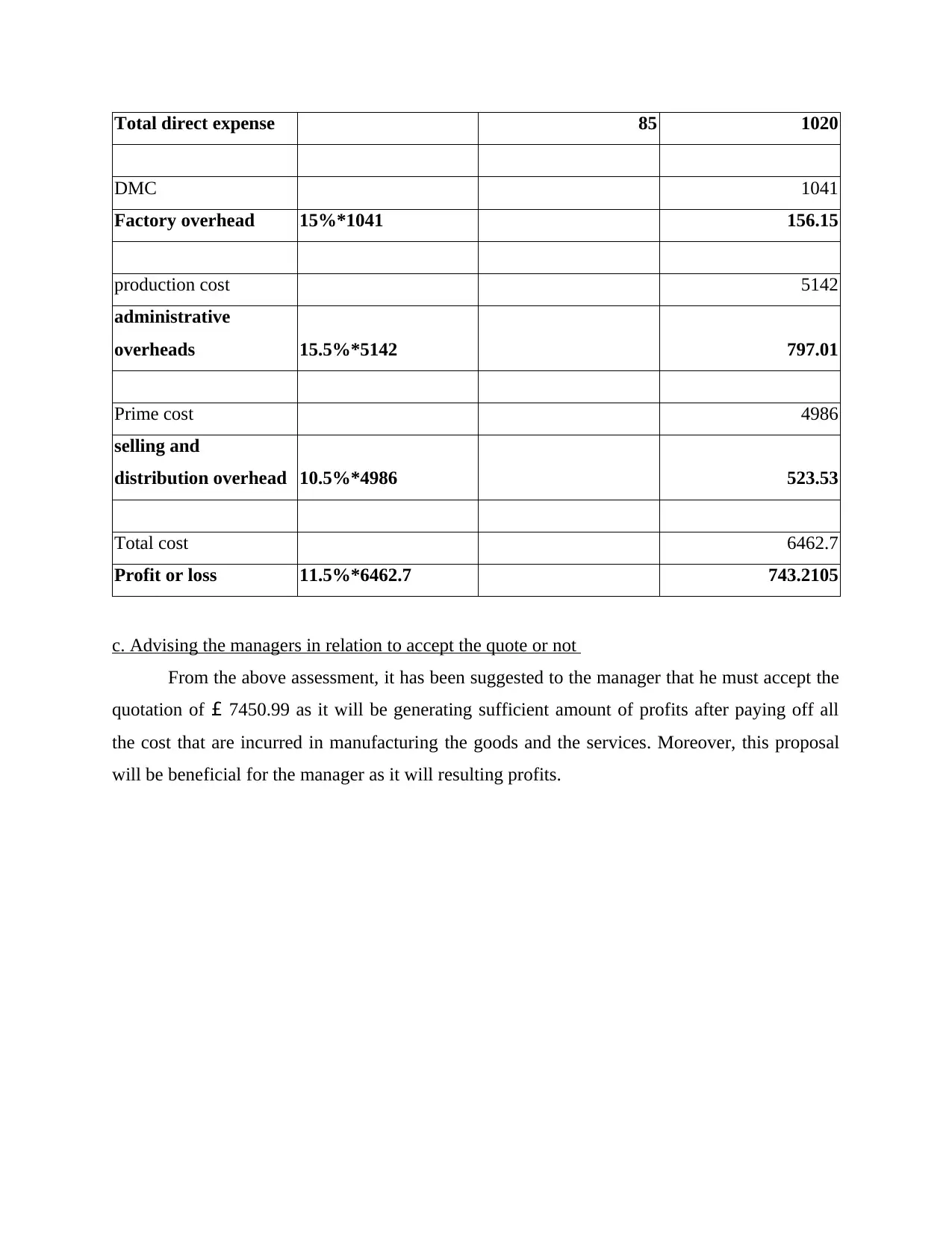

Total direct expense 85 1020

DMC 1041

Factory overhead 15%*1041 156.15

production cost 5142

administrative

overheads 15.5%*5142 797.01

Prime cost 4986

selling and

distribution overhead 10.5%*4986 523.53

Total cost 6462.7

Profit or loss 11.5%*6462.7 743.2105

c. Advising the managers in relation to accept the quote or not

From the above assessment, it has been suggested to the manager that he must accept the

quotation of £ 7450.99 as it will be generating sufficient amount of profits after paying off all

the cost that are incurred in manufacturing the goods and the services. Moreover, this proposal

will be beneficial for the manager as it will resulting profits.

DMC 1041

Factory overhead 15%*1041 156.15

production cost 5142

administrative

overheads 15.5%*5142 797.01

Prime cost 4986

selling and

distribution overhead 10.5%*4986 523.53

Total cost 6462.7

Profit or loss 11.5%*6462.7 743.2105

c. Advising the managers in relation to accept the quote or not

From the above assessment, it has been suggested to the manager that he must accept the

quotation of £ 7450.99 as it will be generating sufficient amount of profits after paying off all

the cost that are incurred in manufacturing the goods and the services. Moreover, this proposal

will be beneficial for the manager as it will resulting profits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Bragg, S. M., 2018. The Interpretation of Financial Statements. AccountingTools, Incorporated.

Pascoe, J. A., Alderliesten, R. C. and Benedictus, R., 2017. On the physical interpretation of the

R-ratio effect and the LEFM parameters used for fatigue crack growth in adhesive

bonds. International Journal of Fatigue. 97. pp.162-176.

Sashegyi, A. and Ferry, D., 2017. On the interpretation of the hazard ratio and communication of

survival benefit. The oncologist. 22(4). pp.484-486.

Varadharajan, S. and et.al., 2015. Exploring in silico prediction of the unbound brain-to-plasma

drug concentration ratio: model validation, renewal, and interpretation. Journal of

pharmaceutical sciences. 104(3). pp.1197-1206.

Books and journals

Bragg, S. M., 2018. The Interpretation of Financial Statements. AccountingTools, Incorporated.

Pascoe, J. A., Alderliesten, R. C. and Benedictus, R., 2017. On the physical interpretation of the

R-ratio effect and the LEFM parameters used for fatigue crack growth in adhesive

bonds. International Journal of Fatigue. 97. pp.162-176.

Sashegyi, A. and Ferry, D., 2017. On the interpretation of the hazard ratio and communication of

survival benefit. The oncologist. 22(4). pp.484-486.

Varadharajan, S. and et.al., 2015. Exploring in silico prediction of the unbound brain-to-plasma

drug concentration ratio: model validation, renewal, and interpretation. Journal of

pharmaceutical sciences. 104(3). pp.1197-1206.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.