Managing Financial Resources Decisions

VerifiedAdded on 2020/01/28

|20

|5692

|64

Report

AI Summary

This report provides a comprehensive analysis of financial resource management and decision-making. It covers various aspects, including sources of finance (internal and external), financial planning and its importance (budgeting, implications of finance inadequacy, and overtrading), assessment of decisions by different stakeholders (partners, venture capitalists, and finance brokers), cash budget analysis, unit cost calculation, investment techniques (Net Present Value, Internal Rate of Return, and Payback Period), and interpretation of financial statements through ratio analysis (acid test ratio and asset turnover ratio). The report uses a case study of Clariton Antiques Limited to illustrate the concepts and techniques discussed. The analysis includes detailed calculations and interpretations of financial data, demonstrating the application of financial management principles in real-world scenarios. The conclusion summarizes the key findings and emphasizes the importance of financial planning for organizational success.

MANAGING FINANCIAL RESOURCES AND DECISIONS

STUDENT NAME:

STUDENT ID:

UNIVERSITY:

STUDENT NAME:

STUDENT ID:

UNIVERSITY:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Sources of finance......................................................................................................................4

1.2 Assessment................................................................................................................................5

Task 2...............................................................................................................................................6

2.1 Analysis.....................................................................................................................................6

a) Dividends................................................................................................................................7

2.2 Financial Planning and its importance:......................................................................................7

2.3 Assessment report on various decisions on:..............................................................................9

Task 3.............................................................................................................................................12

3.1 Cash budget and its analysis:...................................................................................................12

3.2 Calculation of unit cost calculation:........................................................................................13

3.3 Investment techniques and its review:.....................................................................................14

Task 4.............................................................................................................................................17

4.1 Important Components of financial statements:......................................................................17

4.2 Balance Sheet format Comparison:.........................................................................................18

4.3 Interpretations via ratios calculations:.....................................................................................18

Conclusion:....................................................................................................................................19

Reference List:...............................................................................................................................20

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

1.1 Sources of finance......................................................................................................................4

1.2 Assessment................................................................................................................................5

Task 2...............................................................................................................................................6

2.1 Analysis.....................................................................................................................................6

a) Dividends................................................................................................................................7

2.2 Financial Planning and its importance:......................................................................................7

2.3 Assessment report on various decisions on:..............................................................................9

Task 3.............................................................................................................................................12

3.1 Cash budget and its analysis:...................................................................................................12

3.2 Calculation of unit cost calculation:........................................................................................13

3.3 Investment techniques and its review:.....................................................................................14

Task 4.............................................................................................................................................17

4.1 Important Components of financial statements:......................................................................17

4.2 Balance Sheet format Comparison:.........................................................................................18

4.3 Interpretations via ratios calculations:.....................................................................................18

Conclusion:....................................................................................................................................19

Reference List:...............................................................................................................................20

Introduction:

Present as well as future prospects of financial positions of any one person or an entire

organization can ideally be evaluated using a Financial Plan. Several important points are

covered by such a plan. The main areas such as allocation as well as details of the assets,

planning for retirement, main liabilities, and goals of investment, estate, and taxation are covered

in details in the aforementioned plan. Various statements are used for the development of a

proper and well furnished documented record for the same. The main company chosen for study

and review is Clariton Antiques limited. The headquarters of the chosen firm is situated in

London, the capital city of England and a prominent city of the United Kingdom. Herein, this

study is about the creation of a detailed monetary plan as well as a proper analytical evaluation

of the operations that have been used.

Task 1

1.1 Sources of finance

There are several sources that can be used in this context. Availability of said sources is adequate

for single people as well as entire financial entities. They are:

a) Business that is unincorporated

Businesses that are unincorporated are more commonly known as an unincorporated business

for the sake of convenience. The businesses that do not have separate legal identities from those

that own them are called unincorporated businesses.

According to Bishop (2015, p.89), main businesses that are covered in this type are ones that are

smaller in size in comparison to others. Though such businesses are tinier in size, the main

sources of funding that they have include partners or capital of the proprietor. Often enough,

such sources are the only sources of funding. Funding for day to day working capital necessity

and expansion of capital is a major necessity that is served by small loans as well.

b) Business that is incorporated

Businesses that offer several perks, as well as benefits of a single partnership, including

protection of liability and extra deduction of taxes, are termed as incorporated businesses.

Raising capital is through sales of company shares is definitely possible through the formation of

Present as well as future prospects of financial positions of any one person or an entire

organization can ideally be evaluated using a Financial Plan. Several important points are

covered by such a plan. The main areas such as allocation as well as details of the assets,

planning for retirement, main liabilities, and goals of investment, estate, and taxation are covered

in details in the aforementioned plan. Various statements are used for the development of a

proper and well furnished documented record for the same. The main company chosen for study

and review is Clariton Antiques limited. The headquarters of the chosen firm is situated in

London, the capital city of England and a prominent city of the United Kingdom. Herein, this

study is about the creation of a detailed monetary plan as well as a proper analytical evaluation

of the operations that have been used.

Task 1

1.1 Sources of finance

There are several sources that can be used in this context. Availability of said sources is adequate

for single people as well as entire financial entities. They are:

a) Business that is unincorporated

Businesses that are unincorporated are more commonly known as an unincorporated business

for the sake of convenience. The businesses that do not have separate legal identities from those

that own them are called unincorporated businesses.

According to Bishop (2015, p.89), main businesses that are covered in this type are ones that are

smaller in size in comparison to others. Though such businesses are tinier in size, the main

sources of funding that they have include partners or capital of the proprietor. Often enough,

such sources are the only sources of funding. Funding for day to day working capital necessity

and expansion of capital is a major necessity that is served by small loans as well.

b) Business that is incorporated

Businesses that offer several perks, as well as benefits of a single partnership, including

protection of liability and extra deduction of taxes, are termed as incorporated businesses.

Raising capital is through sales of company shares is definitely possible through the formation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

one's own corporation (Cebula and Clark, 2014, p.98). In direct contrast to their unincorporated

counterparts, they do have a legal identity distinct and separate from their owners and leaders.

For the chosen financial entity, funds are made available by raising them from the public using

equities. One main benefit of this method is the fact that major capital can be raised at just one

go. Equity and its financing is ideally the main route for an achievement of the venture capital.

Some of the shares are not made public in any shape or form, with their sole responsibility being

raising required capital for individual investors that can include people with close personal

connections to owners such as family and friends (Gopalan et al. 2014, p.1108). These kinds of

investments are visibly attractive to them, and chances of success in this regard are increased

manifold.

1.2 Assessment

Main sources are generally divided into two broad categories:

a) Internal sources

Internal sources are those that are generated by sources that are present in the financial entity.

The main advantage that these sources accord is the amount of savings generated in terms of

interest rate cost (Henning, 2015, p.25). Effective management of time is also a very creditable

achievement. This directly leads to proper figuring out of availability with regards to

requirement. Major sources such as asset selling that is among the last resorts available to any

company are generally not required to be used except in worst case scenarios.

Malhotra et al. (2014, p.95) state that the Main disadvantages of someone using their own money

in these sorts of ventures include a lack of mentoring that those who fund their own businesses

have to face. Others generally have investors, as well as capitalists; provide effective guidance in

this regard. These benefits are not available to the self-funding individuals and corporate entities.

Many times, using one’s own money leads to a strain in the personal financial state.

b) External sources

Sources that are external are those that organizations manage to obtain from markets, that is,

mainly from out of the company. This type generally meets long-term goals and objectives. The

main purpose and reason behind the usage of these sources are lack of money or capital within

the financial organization (McDonnell, 2014, p.725). Shares, commercial papers, and

commercial loans are great examples of the aforementioned.

counterparts, they do have a legal identity distinct and separate from their owners and leaders.

For the chosen financial entity, funds are made available by raising them from the public using

equities. One main benefit of this method is the fact that major capital can be raised at just one

go. Equity and its financing is ideally the main route for an achievement of the venture capital.

Some of the shares are not made public in any shape or form, with their sole responsibility being

raising required capital for individual investors that can include people with close personal

connections to owners such as family and friends (Gopalan et al. 2014, p.1108). These kinds of

investments are visibly attractive to them, and chances of success in this regard are increased

manifold.

1.2 Assessment

Main sources are generally divided into two broad categories:

a) Internal sources

Internal sources are those that are generated by sources that are present in the financial entity.

The main advantage that these sources accord is the amount of savings generated in terms of

interest rate cost (Henning, 2015, p.25). Effective management of time is also a very creditable

achievement. This directly leads to proper figuring out of availability with regards to

requirement. Major sources such as asset selling that is among the last resorts available to any

company are generally not required to be used except in worst case scenarios.

Malhotra et al. (2014, p.95) state that the Main disadvantages of someone using their own money

in these sorts of ventures include a lack of mentoring that those who fund their own businesses

have to face. Others generally have investors, as well as capitalists; provide effective guidance in

this regard. These benefits are not available to the self-funding individuals and corporate entities.

Many times, using one’s own money leads to a strain in the personal financial state.

b) External sources

Sources that are external are those that organizations manage to obtain from markets, that is,

mainly from out of the company. This type generally meets long-term goals and objectives. The

main purpose and reason behind the usage of these sources are lack of money or capital within

the financial organization (McDonnell, 2014, p.725). Shares, commercial papers, and

commercial loans are great examples of the aforementioned.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Evaluation

The stated financial entity has been trying to focus on the opening of another branch, which has

the potential of increasing its overall sales of operation. The main requirement according to the

developed plans has been observed to be £0.500 million. Internal sources are not enough to

satisfy all the requirements and necessities.

Since internal sources are not enough, in this case, it is important that the chosen firm uses

external sources for appropriate funding of its overall capital requirement (Prete et al. 2016,

p.91). Using such sources has the potential to provide appropriate funding that will last for a

longer duration. Long term solution to the problem of lack of funding is thus solved using the

aforementioned method.

Task 2

2.1 Analysis

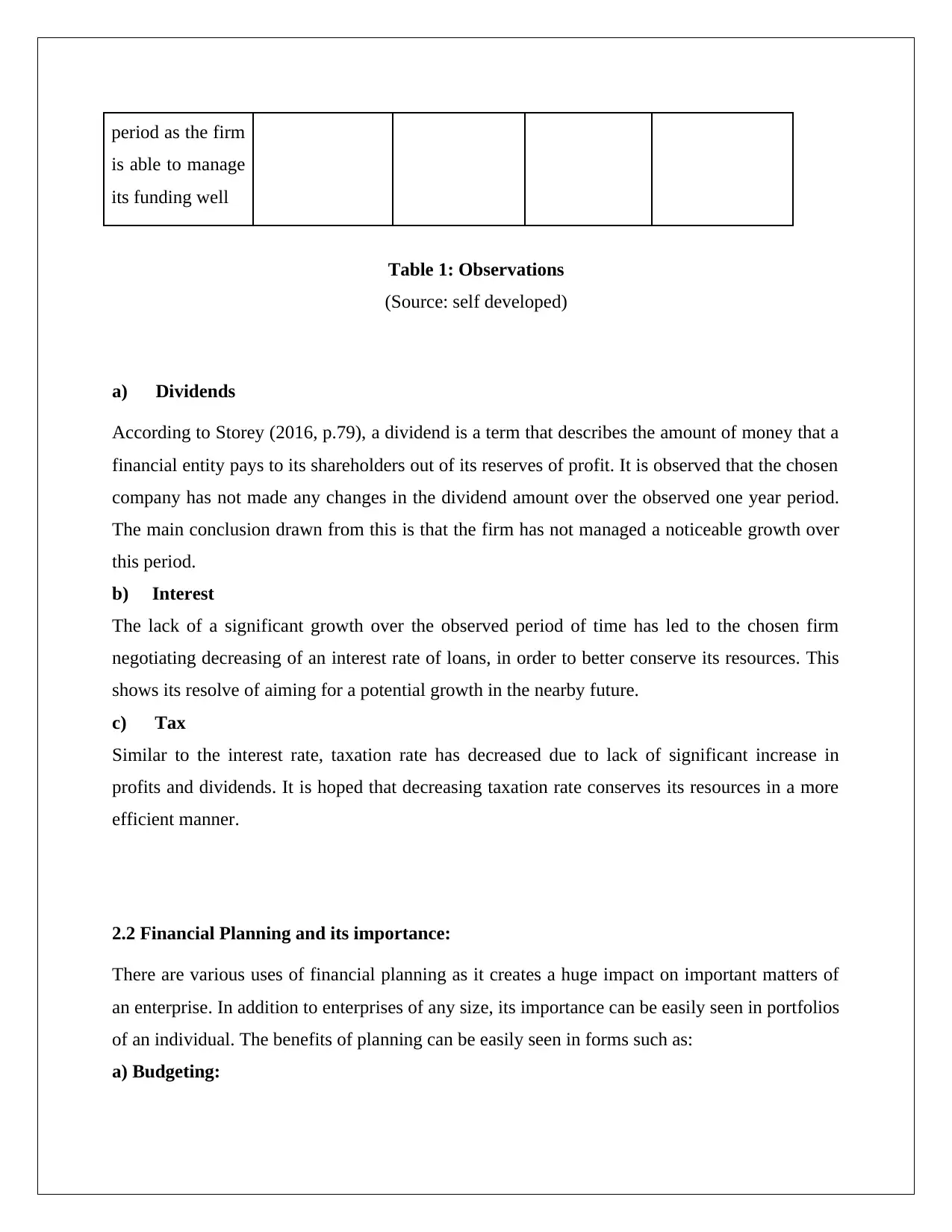

Particulars20142015ChangesObservations

Dividends£8000£8000Negligible

There has been a

lack of dividends

in the observed

one year period

Interest18.76 %18.08%0.68%

A small fall of

0.68% in the

interest rate has

been observed

Tax18.76 %18.08%0.68%

Taxation expense

has decreased

slightly over the

observed one

The stated financial entity has been trying to focus on the opening of another branch, which has

the potential of increasing its overall sales of operation. The main requirement according to the

developed plans has been observed to be £0.500 million. Internal sources are not enough to

satisfy all the requirements and necessities.

Since internal sources are not enough, in this case, it is important that the chosen firm uses

external sources for appropriate funding of its overall capital requirement (Prete et al. 2016,

p.91). Using such sources has the potential to provide appropriate funding that will last for a

longer duration. Long term solution to the problem of lack of funding is thus solved using the

aforementioned method.

Task 2

2.1 Analysis

Particulars20142015ChangesObservations

Dividends£8000£8000Negligible

There has been a

lack of dividends

in the observed

one year period

Interest18.76 %18.08%0.68%

A small fall of

0.68% in the

interest rate has

been observed

Tax18.76 %18.08%0.68%

Taxation expense

has decreased

slightly over the

observed one

period as the firm

is able to manage

its funding well

Table 1: Observations

(Source: self developed)

a) Dividends

According to Storey (2016, p.79), a dividend is a term that describes the amount of money that a

financial entity pays to its shareholders out of its reserves of profit. It is observed that the chosen

company has not made any changes in the dividend amount over the observed one year period.

The main conclusion drawn from this is that the firm has not managed a noticeable growth over

this period.

b) Interest

The lack of a significant growth over the observed period of time has led to the chosen firm

negotiating decreasing of an interest rate of loans, in order to better conserve its resources. This

shows its resolve of aiming for a potential growth in the nearby future.

c) Tax

Similar to the interest rate, taxation rate has decreased due to lack of significant increase in

profits and dividends. It is hoped that decreasing taxation rate conserves its resources in a more

efficient manner.

2.2 Financial Planning and its importance:

There are various uses of financial planning as it creates a huge impact on important matters of

an enterprise. In addition to enterprises of any size, its importance can be easily seen in portfolios

of an individual. The benefits of planning can be easily seen in forms such as:

a) Budgeting:

is able to manage

its funding well

Table 1: Observations

(Source: self developed)

a) Dividends

According to Storey (2016, p.79), a dividend is a term that describes the amount of money that a

financial entity pays to its shareholders out of its reserves of profit. It is observed that the chosen

company has not made any changes in the dividend amount over the observed one year period.

The main conclusion drawn from this is that the firm has not managed a noticeable growth over

this period.

b) Interest

The lack of a significant growth over the observed period of time has led to the chosen firm

negotiating decreasing of an interest rate of loans, in order to better conserve its resources. This

shows its resolve of aiming for a potential growth in the nearby future.

c) Tax

Similar to the interest rate, taxation rate has decreased due to lack of significant increase in

profits and dividends. It is hoped that decreasing taxation rate conserves its resources in a more

efficient manner.

2.2 Financial Planning and its importance:

There are various uses of financial planning as it creates a huge impact on important matters of

an enterprise. In addition to enterprises of any size, its importance can be easily seen in portfolios

of an individual. The benefits of planning can be easily seen in forms such as:

a) Budgeting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budgets are those statements that help in visualizing the performance of business. It is ideally

presented in table format with help of figures. On a general basis, a budget helps in estimating

expenses in reference with incomes which firm at present bears or expects in future. Above

chosen entity, if prepares a budget as per observations acquired by Finance Manager of the

corporation can help firmly in various ways. First and the foremost advantage it can experience

is control of operations. According to Bruton et al. (2015, p.15) have clearly mentioned that

Control is acquired as managers take decisions upon variance analysis. For example, from

figures of income statements, it can be clearly seen that in 2015 operating expenses were higher

which declined in 2016. However, sales cost have increased and finance costs remained stagnant.

Therefore, these aspects need to be covered well in budget.

Secondly, the budget helps in target setting as per department divisions. This can help firmly in

sorting well areas which it lacks behind and areas in which it can improve (Carbó‐Valverde et al.

2016, p.119). Thirdly, it helps in measuring performances as by favourable variance and with the

present status of a business. Lastly budget needs to be monitored well in the context of achieving

desired results.

There can be various repercussions an entity can face if it fails to prepare an ideal budget, such

as over expenses, a performance of firms cannot be measured properly. Further, entities with the

lack of budget even fail to meet deadlines and fulfill their tasks.

b) Implications as failure in maintaining finance inadequacy:

There might be various forms of allegations an entity might face if it fails to maintain inadequacy

in financial aspects. Finance adequacy helps in integrating of various resources in reference with

expenses or necessities of the firm. In order to make profit and escalation of growth continuously

a successful financial plan is acquired. Collins et al. (2014, p.185) have well stated that financial

adequacy helps in the sorting of both surplus areas along with deficit areas. For example,

discounted in cash flows helps in identification of investment areas which can help in deriving

better yield. Further, there are certain investment appraisal techniques that are very well covered

in the adequacy of finance such as users ease, degree acquired in accuracy terms. Measurements

of cash flow such as factors affecting, interest rates all are adequately required by an entity.

c) Overtrading:

presented in table format with help of figures. On a general basis, a budget helps in estimating

expenses in reference with incomes which firm at present bears or expects in future. Above

chosen entity, if prepares a budget as per observations acquired by Finance Manager of the

corporation can help firmly in various ways. First and the foremost advantage it can experience

is control of operations. According to Bruton et al. (2015, p.15) have clearly mentioned that

Control is acquired as managers take decisions upon variance analysis. For example, from

figures of income statements, it can be clearly seen that in 2015 operating expenses were higher

which declined in 2016. However, sales cost have increased and finance costs remained stagnant.

Therefore, these aspects need to be covered well in budget.

Secondly, the budget helps in target setting as per department divisions. This can help firmly in

sorting well areas which it lacks behind and areas in which it can improve (Carbó‐Valverde et al.

2016, p.119). Thirdly, it helps in measuring performances as by favourable variance and with the

present status of a business. Lastly budget needs to be monitored well in the context of achieving

desired results.

There can be various repercussions an entity can face if it fails to prepare an ideal budget, such

as over expenses, a performance of firms cannot be measured properly. Further, entities with the

lack of budget even fail to meet deadlines and fulfill their tasks.

b) Implications as failure in maintaining finance inadequacy:

There might be various forms of allegations an entity might face if it fails to maintain inadequacy

in financial aspects. Finance adequacy helps in integrating of various resources in reference with

expenses or necessities of the firm. In order to make profit and escalation of growth continuously

a successful financial plan is acquired. Collins et al. (2014, p.185) have well stated that financial

adequacy helps in the sorting of both surplus areas along with deficit areas. For example,

discounted in cash flows helps in identification of investment areas which can help in deriving

better yield. Further, there are certain investment appraisal techniques that are very well covered

in the adequacy of finance such as users ease, degree acquired in accuracy terms. Measurements

of cash flow such as factors affecting, interest rates all are adequately required by an entity.

c) Overtrading:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Trading on general terms helps in maximizing profits in a firm. It helps in expanding capital.

With capital expansion operations performed by entities can be done well. However, if there is

overtrading it can lead various overturn effects. On simpler terms overtrading refers to

engagement of various business activities apart from resources available and funds acquired from

the capital market. Over trading ideally, happens when there are too many operations performed

by a corporation. It results in increased interest expenses which ultimately lowers profit of

company (Fuchs et al. 2014, p.185). Mainly there is a shortage of working capital which firm

faces as one of the biggest drawbacks. Further, increased in borrowings leads in liquidity

problems in books of the company. In order to detect overtrading or under trading there are

various ratios that can help in figuring out if any exist infirm. Ratios such as Current, Quick

which ultimately helps in identifying unexpected changes along with any seasonal demands if an

enterprise has faced or expects in near future.

2.3 Assessment report on various decisions on:

Various important decisions are taken by parties that help in taking important financial decisions

in respect with a company. In addition to monetary decisions, there are certain important areas

such operations, sales, marketing which requires proper assessment that is based on important

credentials. Some parties require referring these credentials in order to derive certain

conclusions. The parties that need to take major financing decisions upon provided information:

The stakeholders of the organization are very crucial to all organizations. The employees, the

shareholders, the customers and the like are the important stakeholders. The organizational

operations are carried out through the involvement of all the stakeholders related to any

organization. The stakeholders help the organization in incorporating all the organizational

objectives and goals in relation to the target market.

a) Partners:

Partners of an entity every there and then require taking various important decision in sequence

with the smooth functioning of business. Partners are those folks that invest capital in the firm

which is the major backbone of a company. According to Gigler et al. (2014, p.375) mentioned

that partners first preference is reviewing of all reports that are made by internal auditors. These

are those reports that are only prepared for management or board. These reports are not presented

With capital expansion operations performed by entities can be done well. However, if there is

overtrading it can lead various overturn effects. On simpler terms overtrading refers to

engagement of various business activities apart from resources available and funds acquired from

the capital market. Over trading ideally, happens when there are too many operations performed

by a corporation. It results in increased interest expenses which ultimately lowers profit of

company (Fuchs et al. 2014, p.185). Mainly there is a shortage of working capital which firm

faces as one of the biggest drawbacks. Further, increased in borrowings leads in liquidity

problems in books of the company. In order to detect overtrading or under trading there are

various ratios that can help in figuring out if any exist infirm. Ratios such as Current, Quick

which ultimately helps in identifying unexpected changes along with any seasonal demands if an

enterprise has faced or expects in near future.

2.3 Assessment report on various decisions on:

Various important decisions are taken by parties that help in taking important financial decisions

in respect with a company. In addition to monetary decisions, there are certain important areas

such operations, sales, marketing which requires proper assessment that is based on important

credentials. Some parties require referring these credentials in order to derive certain

conclusions. The parties that need to take major financing decisions upon provided information:

The stakeholders of the organization are very crucial to all organizations. The employees, the

shareholders, the customers and the like are the important stakeholders. The organizational

operations are carried out through the involvement of all the stakeholders related to any

organization. The stakeholders help the organization in incorporating all the organizational

objectives and goals in relation to the target market.

a) Partners:

Partners of an entity every there and then require taking various important decision in sequence

with the smooth functioning of business. Partners are those folks that invest capital in the firm

which is the major backbone of a company. According to Gigler et al. (2014, p.375) mentioned

that partners first preference is reviewing of all reports that are made by internal auditors. These

are those reports that are only prepared for management or board. These reports are not presented

to the public. After reviewing these reports partners are easily able to identify frauds that take

place within a company. Further inactive partners, as they are not involved with operations of

business access only balance sheet, income statement.

Those individuals who are willing to become partners of above-chosen entity might address

various kinds of information. The important ones such as customer or client list of the company.

The potential capacity of a firm which can easily evaluate very well by sales and profit acquired

and further by comparing with previous years. Further, major shareholders of a company are

even seen as it affects the image of an enterprise. Workforce strength also lays an important

impact in functioning; therefore, numbers of employees are seen. Clariton Antiques as they are

only selling only stolen antiques, therefore its litigation history is very well checked by partners.

b) Venture Capitalist:

We Capital limited a venture capitalist entity which has approached above stated firm for

financing. This entity has shown a keen interest in operations of the above stated organization as

by becoming partners in the stake of 20% of profits in return on investment. Therefore, in order

to take this decision venture providing entity accesses certain information such as the potential of

the enterprise. Organizations presently, its production figures which clearly describes input as

well as output. Goldstein and Sapra (2014, p45) have clearly stated that future expectations of an

enterprise are also clearly seen which can be reflected easily through growth plan, budgets. Even

projects are verified which the corporation is willing to invest is looked. The potential capacity

of investment in projects can be ensured through various methods. The most ideal method is Net

Present Value method.

b) Finance broker:

With activities performed by brokers also lead to various changes such as there is an increase in

current assets like cash. Even there is an increase in non current liability of business.

In above stated organization, finance broker which in return of investment has charged some

fees. In return of capital investment of (£) 500000 the broker has made some charges as

brokerage fees.

Finance Broker Capital 500000 -500000

(£) years (£)

Cumulative

amount (£)

place within a company. Further inactive partners, as they are not involved with operations of

business access only balance sheet, income statement.

Those individuals who are willing to become partners of above-chosen entity might address

various kinds of information. The important ones such as customer or client list of the company.

The potential capacity of a firm which can easily evaluate very well by sales and profit acquired

and further by comparing with previous years. Further, major shareholders of a company are

even seen as it affects the image of an enterprise. Workforce strength also lays an important

impact in functioning; therefore, numbers of employees are seen. Clariton Antiques as they are

only selling only stolen antiques, therefore its litigation history is very well checked by partners.

b) Venture Capitalist:

We Capital limited a venture capitalist entity which has approached above stated firm for

financing. This entity has shown a keen interest in operations of the above stated organization as

by becoming partners in the stake of 20% of profits in return on investment. Therefore, in order

to take this decision venture providing entity accesses certain information such as the potential of

the enterprise. Organizations presently, its production figures which clearly describes input as

well as output. Goldstein and Sapra (2014, p45) have clearly stated that future expectations of an

enterprise are also clearly seen which can be reflected easily through growth plan, budgets. Even

projects are verified which the corporation is willing to invest is looked. The potential capacity

of investment in projects can be ensured through various methods. The most ideal method is Net

Present Value method.

b) Finance broker:

With activities performed by brokers also lead to various changes such as there is an increase in

current assets like cash. Even there is an increase in non current liability of business.

In above stated organization, finance broker which in return of investment has charged some

fees. In return of capital investment of (£) 500000 the broker has made some charges as

brokerage fees.

Finance Broker Capital 500000 -500000

(£) years (£)

Cumulative

amount (£)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

initial 500000 1 115000 -385000

100000 2 115000 -270000

5000 3 115000 -155000

10000 4 115000 -40000

total 115000 5 115000 75000

6 115000 190000

7 115000 305000

8 115000 420000

9 115000 535000

10 115000 650000

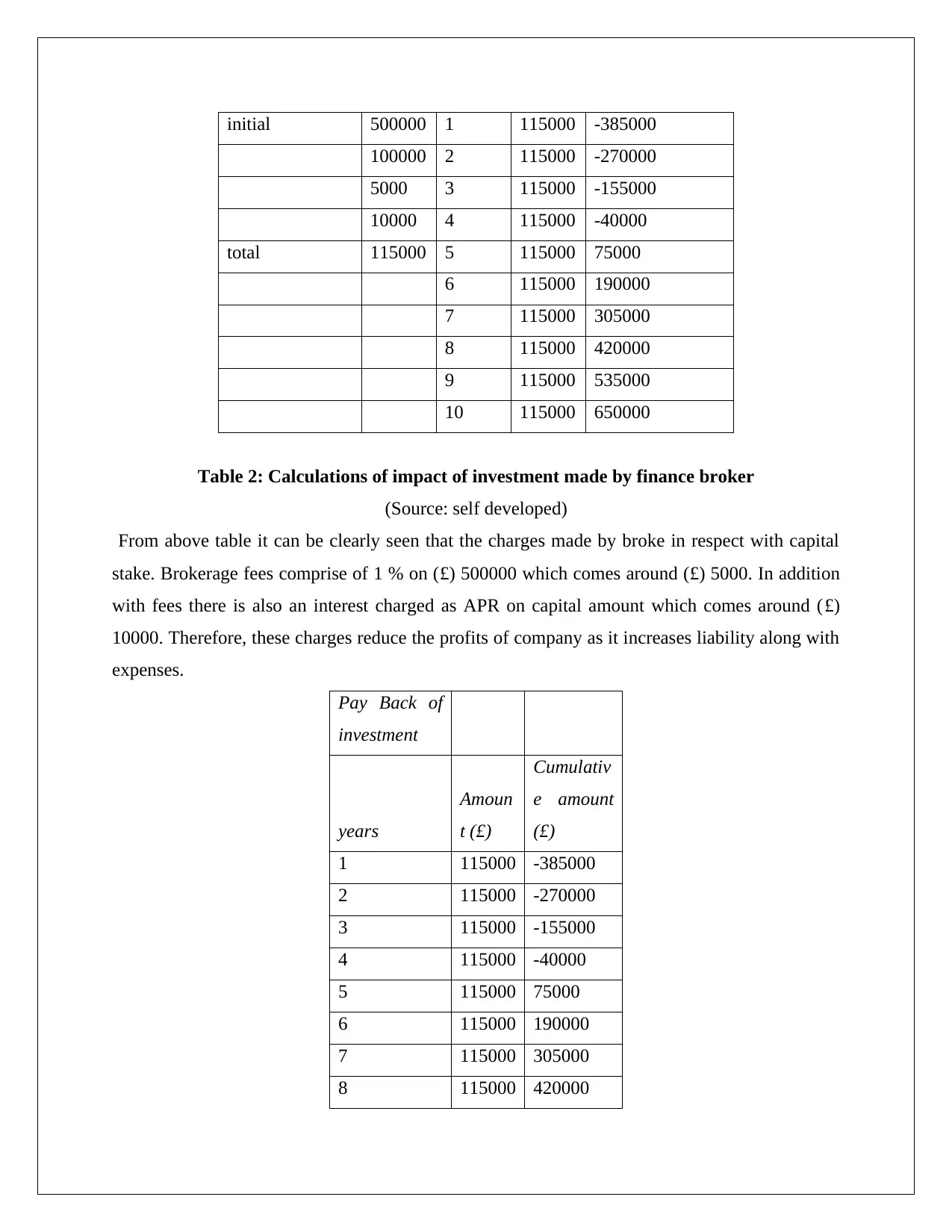

Table 2: Calculations of impact of investment made by finance broker

(Source: self developed)

From above table it can be clearly seen that the charges made by broke in respect with capital

stake. Brokerage fees comprise of 1 % on (£) 500000 which comes around (£) 5000. In addition

with fees there is also an interest charged as APR on capital amount which comes around (£)

10000. Therefore, these charges reduce the profits of company as it increases liability along with

expenses.

Pay Back of

investment

years

Amoun

t (£)

Cumulativ

e amount

(£)

1 115000 -385000

2 115000 -270000

3 115000 -155000

4 115000 -40000

5 115000 75000

6 115000 190000

7 115000 305000

8 115000 420000

100000 2 115000 -270000

5000 3 115000 -155000

10000 4 115000 -40000

total 115000 5 115000 75000

6 115000 190000

7 115000 305000

8 115000 420000

9 115000 535000

10 115000 650000

Table 2: Calculations of impact of investment made by finance broker

(Source: self developed)

From above table it can be clearly seen that the charges made by broke in respect with capital

stake. Brokerage fees comprise of 1 % on (£) 500000 which comes around (£) 5000. In addition

with fees there is also an interest charged as APR on capital amount which comes around (£)

10000. Therefore, these charges reduce the profits of company as it increases liability along with

expenses.

Pay Back of

investment

years

Amoun

t (£)

Cumulativ

e amount

(£)

1 115000 -385000

2 115000 -270000

3 115000 -155000

4 115000 -40000

5 115000 75000

6 115000 190000

7 115000 305000

8 115000 420000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9 115000 535000

10 115000 650000

payback

period

4.6521

7

Table 3: Payback of investment done

(Source: self developed)

From above table it can be clearly seen that on investment made the entity can expect profit from

above investment since 4.65 years. Till 4.65 years this date organization is unable to make profits

and incur losses.

Task 3

3.1 Cash budget and its analysis:

Cash flow refers to an ideal flow of cash that is held on day to day basis with in organization.

There are inflows along with outflows that are very well covered with in operations of firm.

Inflows are basically those payments which a firm receives from its customers. On other hand

outflows are those payments which are done by business.

Therefore Cash flow is calculated by using formula:

Net flow = Cash inflow – Outflow of cash incurred in business.

Cash budget helps in various kinds of forecast .Forecasts such as inflows that is acquired through

sales done to customers. Other sources such as payments received from debtors lie in inflows of

business (Herndon et al. 2014, p.269).Outflows include different payments such as rent,

overhead, wages, salaries, operating expenses. Raw material expenses and variable cost expenses

all are categorized as cash outflow.

There are various important aspects which can be clearly observed as in inflow. In an ideal cash

flow budget which clearly describes sales forecast of organization, outflows made by business in

reference with sales.

Particular

s

Sales

forecast (£)

Payments

made(£)

Recovery

made(£)

10 115000 650000

payback

period

4.6521

7

Table 3: Payback of investment done

(Source: self developed)

From above table it can be clearly seen that on investment made the entity can expect profit from

above investment since 4.65 years. Till 4.65 years this date organization is unable to make profits

and incur losses.

Task 3

3.1 Cash budget and its analysis:

Cash flow refers to an ideal flow of cash that is held on day to day basis with in organization.

There are inflows along with outflows that are very well covered with in operations of firm.

Inflows are basically those payments which a firm receives from its customers. On other hand

outflows are those payments which are done by business.

Therefore Cash flow is calculated by using formula:

Net flow = Cash inflow – Outflow of cash incurred in business.

Cash budget helps in various kinds of forecast .Forecasts such as inflows that is acquired through

sales done to customers. Other sources such as payments received from debtors lie in inflows of

business (Herndon et al. 2014, p.269).Outflows include different payments such as rent,

overhead, wages, salaries, operating expenses. Raw material expenses and variable cost expenses

all are categorized as cash outflow.

There are various important aspects which can be clearly observed as in inflow. In an ideal cash

flow budget which clearly describes sales forecast of organization, outflows made by business in

reference with sales.

Particular

s

Sales

forecast (£)

Payments

made(£)

Recovery

made(£)

January 300000 807250 -397250

February 450000 137250 -84500

March 600000 1197250 -681750

April 300000 437250 -819000

May 300000 227250 -746250

June 75000 219750 -891000

total 2025000 3026000 -891000

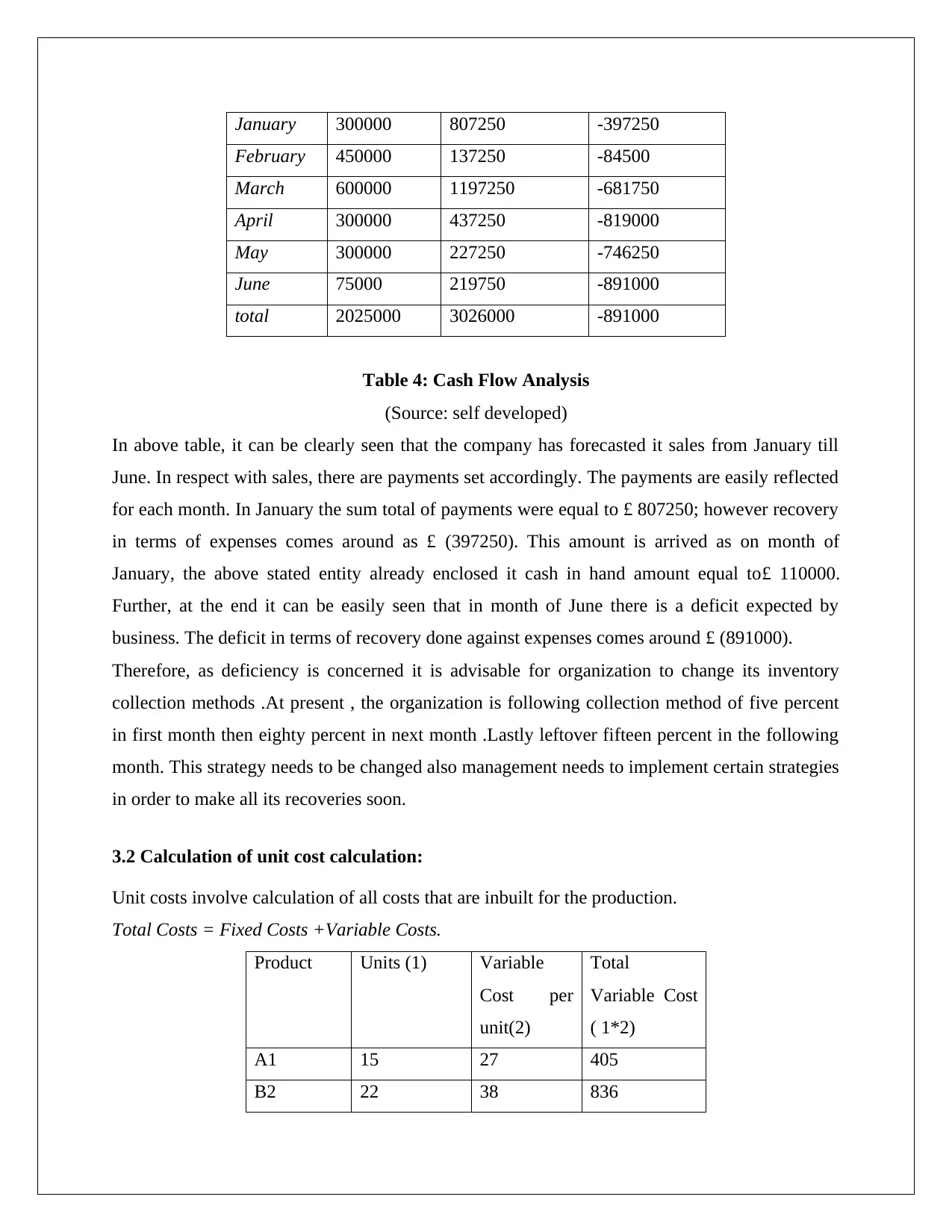

Table 4: Cash Flow Analysis

(Source: self developed)

In above table, it can be clearly seen that the company has forecasted it sales from January till

June. In respect with sales, there are payments set accordingly. The payments are easily reflected

for each month. In January the sum total of payments were equal to £ 807250; however recovery

in terms of expenses comes around as £ (397250). This amount is arrived as on month of

January, the above stated entity already enclosed it cash in hand amount equal to£ 110000.

Further, at the end it can be easily seen that in month of June there is a deficit expected by

business. The deficit in terms of recovery done against expenses comes around £ (891000).

Therefore, as deficiency is concerned it is advisable for organization to change its inventory

collection methods .At present , the organization is following collection method of five percent

in first month then eighty percent in next month .Lastly leftover fifteen percent in the following

month. This strategy needs to be changed also management needs to implement certain strategies

in order to make all its recoveries soon.

3.2 Calculation of unit cost calculation:

Unit costs involve calculation of all costs that are inbuilt for the production.

Total Costs = Fixed Costs +Variable Costs.

Product Units (1) Variable

Cost per

unit(2)

Total

Variable Cost

( 1*2)

A1 15 27 405

B2 22 38 836

February 450000 137250 -84500

March 600000 1197250 -681750

April 300000 437250 -819000

May 300000 227250 -746250

June 75000 219750 -891000

total 2025000 3026000 -891000

Table 4: Cash Flow Analysis

(Source: self developed)

In above table, it can be clearly seen that the company has forecasted it sales from January till

June. In respect with sales, there are payments set accordingly. The payments are easily reflected

for each month. In January the sum total of payments were equal to £ 807250; however recovery

in terms of expenses comes around as £ (397250). This amount is arrived as on month of

January, the above stated entity already enclosed it cash in hand amount equal to£ 110000.

Further, at the end it can be easily seen that in month of June there is a deficit expected by

business. The deficit in terms of recovery done against expenses comes around £ (891000).

Therefore, as deficiency is concerned it is advisable for organization to change its inventory

collection methods .At present , the organization is following collection method of five percent

in first month then eighty percent in next month .Lastly leftover fifteen percent in the following

month. This strategy needs to be changed also management needs to implement certain strategies

in order to make all its recoveries soon.

3.2 Calculation of unit cost calculation:

Unit costs involve calculation of all costs that are inbuilt for the production.

Total Costs = Fixed Costs +Variable Costs.

Product Units (1) Variable

Cost per

unit(2)

Total

Variable Cost

( 1*2)

A1 15 27 405

B2 22 38 836

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.