Analyzing Financial Resources in the Hospitality Sector: A Report

VerifiedAdded on 2023/06/16

|15

|3133

|92

Report

AI Summary

This report provides an in-depth analysis of managing financial resources within the hospitality industry. It begins by explaining Generally Accepted Accounting Principles (GAAP) and identifying various users of financial statements, along with their information needs. The report discusses the relevance of income statements, balance sheets, and cash flow statements to loan and trade creditors. Furthermore, it explores the components that supplement financial statements in an annual report and delves into key financial reporting concepts. A significant portion of the report is dedicated to interpreting financial statements using financial ratios, comparing performance across two years, and evaluating key metrics such as net profit margin, return on assets (ROA), return on equity (ROE), current ratio, and quick ratio, offering insights into the financial health and operational efficiency of Smart Resort Ltd. The analysis concludes with recommendations for improving financial performance and stakeholder value.

Managing Financial

Resources in the Hospitality

Industry

Resources in the Hospitality

Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction....................................................................................................................................3

Main Body......................................................................................................................................3

Meaning of generally accepted accounting principles and various users of financial statements

as well as the assessment of information needs of different decision makers.............................3

Discussion about the three statements of income, financial position and cash flows that would

be of most interest to a loan creditor and a trade creditor...........................................................4

The components which supplement the financial statements in an annual report and discussion

of financial reporting concepts....................................................................................................5

Interpretation of the financial statements using appropriate financial ratios and comparison of

both year performances................................................................................................................7

Conclusion....................................................................................................................................13

References.....................................................................................................................................15

Introduction....................................................................................................................................3

Main Body......................................................................................................................................3

Meaning of generally accepted accounting principles and various users of financial statements

as well as the assessment of information needs of different decision makers.............................3

Discussion about the three statements of income, financial position and cash flows that would

be of most interest to a loan creditor and a trade creditor...........................................................4

The components which supplement the financial statements in an annual report and discussion

of financial reporting concepts....................................................................................................5

Interpretation of the financial statements using appropriate financial ratios and comparison of

both year performances................................................................................................................7

Conclusion....................................................................................................................................13

References.....................................................................................................................................15

Introduction

Financial resource can be termed as the accumulation of the liquid assets within a given entity.

Management of financial resources can be characterized as complex task as it involves multiple

set of practices (Brigham and Houston, 2021). The report highlight upon the GAAP principles of

financial accounting and the users of financial statements. It involves the detailed discussion

about the financial statements in regard with their suitability to trade creditor and loan creditor.

The essential components of financial statement along with reporting concepts are signified

within the report. At last, interpretation of the given financial statements with accurate results

and evaluation of the same are also presented appropriately.

Main Body

Meaning of generally accepted accounting principles and various users of financial statements as

well as the assessment of information needs of different decision makers

Generally accepted accounting principles generally refereed as GAAP is a set of rules and

procedures that are planned to modulate corporate accounting and financial reporting. It covers

guidelines of accounting, accounting standards and specific accounting practices depending upon

industry. It is the most transparent way of recording the financial information. It relies on ten

principles which are consistency, non-compensation, permanent methods, prudence, regularity,

sincerity, materiality, good faith, continuity and periodicity (Madura, 2020). GAAP has made

decisions easy for investors and other stakeholders of the company to take the decisions as they

can compare the performance with other companies also.

Various users of financial statements and the information needs of different decision makers are

given below:

Company management: They need the information because they need to check every

month the profitability, liquidity and cash flow of the firm and can compare it with

previous months. So that they can take the decision for the betterment of the company.

Competitors: They need information so they can know the financial position of their rival

companies and can change their strategies for the betterment of company.

Financial resource can be termed as the accumulation of the liquid assets within a given entity.

Management of financial resources can be characterized as complex task as it involves multiple

set of practices (Brigham and Houston, 2021). The report highlight upon the GAAP principles of

financial accounting and the users of financial statements. It involves the detailed discussion

about the financial statements in regard with their suitability to trade creditor and loan creditor.

The essential components of financial statement along with reporting concepts are signified

within the report. At last, interpretation of the given financial statements with accurate results

and evaluation of the same are also presented appropriately.

Main Body

Meaning of generally accepted accounting principles and various users of financial statements as

well as the assessment of information needs of different decision makers

Generally accepted accounting principles generally refereed as GAAP is a set of rules and

procedures that are planned to modulate corporate accounting and financial reporting. It covers

guidelines of accounting, accounting standards and specific accounting practices depending upon

industry. It is the most transparent way of recording the financial information. It relies on ten

principles which are consistency, non-compensation, permanent methods, prudence, regularity,

sincerity, materiality, good faith, continuity and periodicity (Madura, 2020). GAAP has made

decisions easy for investors and other stakeholders of the company to take the decisions as they

can compare the performance with other companies also.

Various users of financial statements and the information needs of different decision makers are

given below:

Company management: They need the information because they need to check every

month the profitability, liquidity and cash flow of the firm and can compare it with

previous months. So that they can take the decision for the betterment of the company.

Competitors: They need information so they can know the financial position of their rival

companies and can change their strategies for the betterment of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Customers: They need information of financial position of company because they will be

purchasing goods or services from them and they want to know if the supplying company

can sustain in long run.

Employees: They need information because they want to know the profitability of the

business as their salaries, increment, bonus depends upon that.

Governments: They need information because they want to know if the company is

paying appropriate amount of tax or not and whether they are following corporate and

labour laws.

Investment analyst: They need information because they want to guide their clients

whether to invest or not in the company.

Investors: They will require the information as they have invested in the company and

they are eager to know what is the position of their investment.

Lenders: They need information because they are lending their money to the company

and want to know their credit worthiness.

Rating agencies: They will require information to rate the company on their credit

worthiness.

Researchers: They require information to conduct their research in accounting.

Union: They need information so that any malpractice can be avoid by the company in

terms of pay scale to the union members that they stand for.

Discussion about the three statements of income, financial position and cash flows that would be

of most interest to a loan creditor and a trade creditor

Income statements reflects upon the respective revenues well as expenses of the business

firm. It helps the business firms in analyzing and evaluating their actual financial

performance in regard with acquiring knowledge about their concerned profits and losses.

The major aim of balance sheet is to depict the appropriate assets as well as liabilities of the

chosen organization. The higher amount of asset reflects that the financial position of the firm is

fostering whereas the higher level of liabilities denotes the hindrance financial position of the

firm (Apte and Kapshe, 2020).

purchasing goods or services from them and they want to know if the supplying company

can sustain in long run.

Employees: They need information because they want to know the profitability of the

business as their salaries, increment, bonus depends upon that.

Governments: They need information because they want to know if the company is

paying appropriate amount of tax or not and whether they are following corporate and

labour laws.

Investment analyst: They need information because they want to guide their clients

whether to invest or not in the company.

Investors: They will require the information as they have invested in the company and

they are eager to know what is the position of their investment.

Lenders: They need information because they are lending their money to the company

and want to know their credit worthiness.

Rating agencies: They will require information to rate the company on their credit

worthiness.

Researchers: They require information to conduct their research in accounting.

Union: They need information so that any malpractice can be avoid by the company in

terms of pay scale to the union members that they stand for.

Discussion about the three statements of income, financial position and cash flows that would be

of most interest to a loan creditor and a trade creditor

Income statements reflects upon the respective revenues well as expenses of the business

firm. It helps the business firms in analyzing and evaluating their actual financial

performance in regard with acquiring knowledge about their concerned profits and losses.

The major aim of balance sheet is to depict the appropriate assets as well as liabilities of the

chosen organization. The higher amount of asset reflects that the financial position of the firm is

fostering whereas the higher level of liabilities denotes the hindrance financial position of the

firm (Apte and Kapshe, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cash flow statement is formulated with the primary reason of evaluating the inflow of

cash as well as outflow of cash in the specific business institution.

Trade Creditor

In context to trade creditor, the most suitable and appropriate financial statement would be

income statement as it would help the same to ascertain the financial performance of the firm.

This will assist the same to analyze how the business will be able to recompense the considerate

loans appropriately, if any. The reason for the same can be stated as the fact that cash flow is

always interpreted in order to gain perspective in regard with extent to which a trade loan can be

repaid by a specific company.

Loan Creditor

In reference to loan creditor, it would be vital for the same to capitalize upon balance sheet

statements. This is because it shows and represents the track of the company in consideration

with recording the assets and liabilities in a timely and consistent manner (Broyles, 2020). This

helps the loan creditor to analyze the viability and competency of the firm in terms of repayment

of the loan. The balance sheet also reflects upon the financial health of a given entity which in

turn highlight upon the tendency of the same to meet up to the obligations in a set defined

manner.

The components which supplement the financial statements in an annual report and discussion of

financial reporting concepts

Financial statement can be termed as the structured and systemized set of documents which

reflect upon the financial position of a given enterprise. The major purpose of inclusion of

financial statement is to project the financial status of a company within particular duration of

time i.e. in usual terms, an accounting year. The financial statements provide an in depth analysis

of the financial transactions facilitated by the business institution in a given period of time

(Keown, Scott, Martin and Petty, 2020). In addition to this, the firm can also track its financial

cash as well as outflow of cash in the specific business institution.

Trade Creditor

In context to trade creditor, the most suitable and appropriate financial statement would be

income statement as it would help the same to ascertain the financial performance of the firm.

This will assist the same to analyze how the business will be able to recompense the considerate

loans appropriately, if any. The reason for the same can be stated as the fact that cash flow is

always interpreted in order to gain perspective in regard with extent to which a trade loan can be

repaid by a specific company.

Loan Creditor

In reference to loan creditor, it would be vital for the same to capitalize upon balance sheet

statements. This is because it shows and represents the track of the company in consideration

with recording the assets and liabilities in a timely and consistent manner (Broyles, 2020). This

helps the loan creditor to analyze the viability and competency of the firm in terms of repayment

of the loan. The balance sheet also reflects upon the financial health of a given entity which in

turn highlight upon the tendency of the same to meet up to the obligations in a set defined

manner.

The components which supplement the financial statements in an annual report and discussion of

financial reporting concepts

Financial statement can be termed as the structured and systemized set of documents which

reflect upon the financial position of a given enterprise. The major purpose of inclusion of

financial statement is to project the financial status of a company within particular duration of

time i.e. in usual terms, an accounting year. The financial statements provide an in depth analysis

of the financial transactions facilitated by the business institution in a given period of time

(Keown, Scott, Martin and Petty, 2020). In addition to this, the firm can also track its financial

inflows and outflows by keeping an appropriate check upon its concerned financial statements.

The components of financial statements are mentioned below: -

Assets

Assets can be characterized as an integral part of financial statements as it denotes upon the

economic leverage capitalized by the company through a serious operation. Few of the examples

the assets can be termed building, property, machinery debtors, cash in hand and bank etc. In

financial accounting, asses have been divided into two types i.e. current and fixed

(Ramachandran and Kakani, 2020). The current assets are the kind of assets which cannot be

depreciated easily as well as they facilities short term benefit within a specific organization. The

another type of asset is named as fixed asset highlights upon the assets which are capitalized by

the firm over a period of year. These assets are not taken into consideration for trading purposes.

Liabilities

Liabilities can be termed as the obligation encountered by the business organization which is

mandatory to be fulfilled by the same. Liabilities may be defined as the set of requirement which

needs to be satisfied by the institution resulting in the outflow of economic resources for the

firm. Accounts payable, short and long term loans, taxes, overdrafts are some of the major

examples of liabilities faced by the company (Robison, Hanson and Black, 2020). Liabilities

comprise of two common type which is current and noncurrent. Current liabilities can be

fulfilled by an entity within a year whereas noncurrent liabilities must be paid off for a longer

duration which is more than a year.

Revenues

Revenues refers to the specific economic perk or benefits gathered by a business entity during

the course of a financial year. Revenues are extremely beneficial for the firm as they assist the

firm in operating its business practices within its respective industry in smooth manner. The

attainment revenues by a firm denotes the success of the same in target market environment.

Equity

The components of financial statements are mentioned below: -

Assets

Assets can be characterized as an integral part of financial statements as it denotes upon the

economic leverage capitalized by the company through a serious operation. Few of the examples

the assets can be termed building, property, machinery debtors, cash in hand and bank etc. In

financial accounting, asses have been divided into two types i.e. current and fixed

(Ramachandran and Kakani, 2020). The current assets are the kind of assets which cannot be

depreciated easily as well as they facilities short term benefit within a specific organization. The

another type of asset is named as fixed asset highlights upon the assets which are capitalized by

the firm over a period of year. These assets are not taken into consideration for trading purposes.

Liabilities

Liabilities can be termed as the obligation encountered by the business organization which is

mandatory to be fulfilled by the same. Liabilities may be defined as the set of requirement which

needs to be satisfied by the institution resulting in the outflow of economic resources for the

firm. Accounts payable, short and long term loans, taxes, overdrafts are some of the major

examples of liabilities faced by the company (Robison, Hanson and Black, 2020). Liabilities

comprise of two common type which is current and noncurrent. Current liabilities can be

fulfilled by an entity within a year whereas noncurrent liabilities must be paid off for a longer

duration which is more than a year.

Revenues

Revenues refers to the specific economic perk or benefits gathered by a business entity during

the course of a financial year. Revenues are extremely beneficial for the firm as they assist the

firm in operating its business practices within its respective industry in smooth manner. The

attainment revenues by a firm denotes the success of the same in target market environment.

Equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The deduction of liabilities from the assets result in the acquisition of the equity capital of a

particular business institution. The payment of dividends by an organization., the revaluation of

the gains acquired by an entity, the existing share capital as well as the retention loss or profit

attained by the firm comes under the equity competent of the same. Cash basis as well as accrual

basis can specified as the respective principles which are taken into consideration while

recording the revenues and incomes within the financial statements (Agustina and Mardiana,

2020).

Expenses

Expenses denotes the decrement in the economic considerations possessed by a business

institution within an accounting year. This refers to outflow of the existing assets and other

economic leverage of the firm. Rent, depreciation, tax deductions, transport and travel expense,

salary expense etc., are some of the common types of expenses which needs to be met by a

business firm. Expense are generally recorded as operating cost within the income statements.

Interpretation of the financial statements using appropriate financial ratios and comparison of

both year performances

Evaluation of Ratios forms a crucial part of decision-making in an organisational firm.

Being working as a director of Smart Resort Ltd. evaluation of rations derived from financial

data made available with suitable interpretation are as follows (Nguyen and et. al., 2020);

Ratio Formula

Net Profit Margin Net sales-COGS/ Net sales

ROA Net income/ Total Assets

ROE Net income/ Shareholders' Equity

Current Ratio CA/CL

particular business institution. The payment of dividends by an organization., the revaluation of

the gains acquired by an entity, the existing share capital as well as the retention loss or profit

attained by the firm comes under the equity competent of the same. Cash basis as well as accrual

basis can specified as the respective principles which are taken into consideration while

recording the revenues and incomes within the financial statements (Agustina and Mardiana,

2020).

Expenses

Expenses denotes the decrement in the economic considerations possessed by a business

institution within an accounting year. This refers to outflow of the existing assets and other

economic leverage of the firm. Rent, depreciation, tax deductions, transport and travel expense,

salary expense etc., are some of the common types of expenses which needs to be met by a

business firm. Expense are generally recorded as operating cost within the income statements.

Interpretation of the financial statements using appropriate financial ratios and comparison of

both year performances

Evaluation of Ratios forms a crucial part of decision-making in an organisational firm.

Being working as a director of Smart Resort Ltd. evaluation of rations derived from financial

data made available with suitable interpretation are as follows (Nguyen and et. al., 2020);

Ratio Formula

Net Profit Margin Net sales-COGS/ Net sales

ROA Net income/ Total Assets

ROE Net income/ Shareholders' Equity

Current Ratio CA/CL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

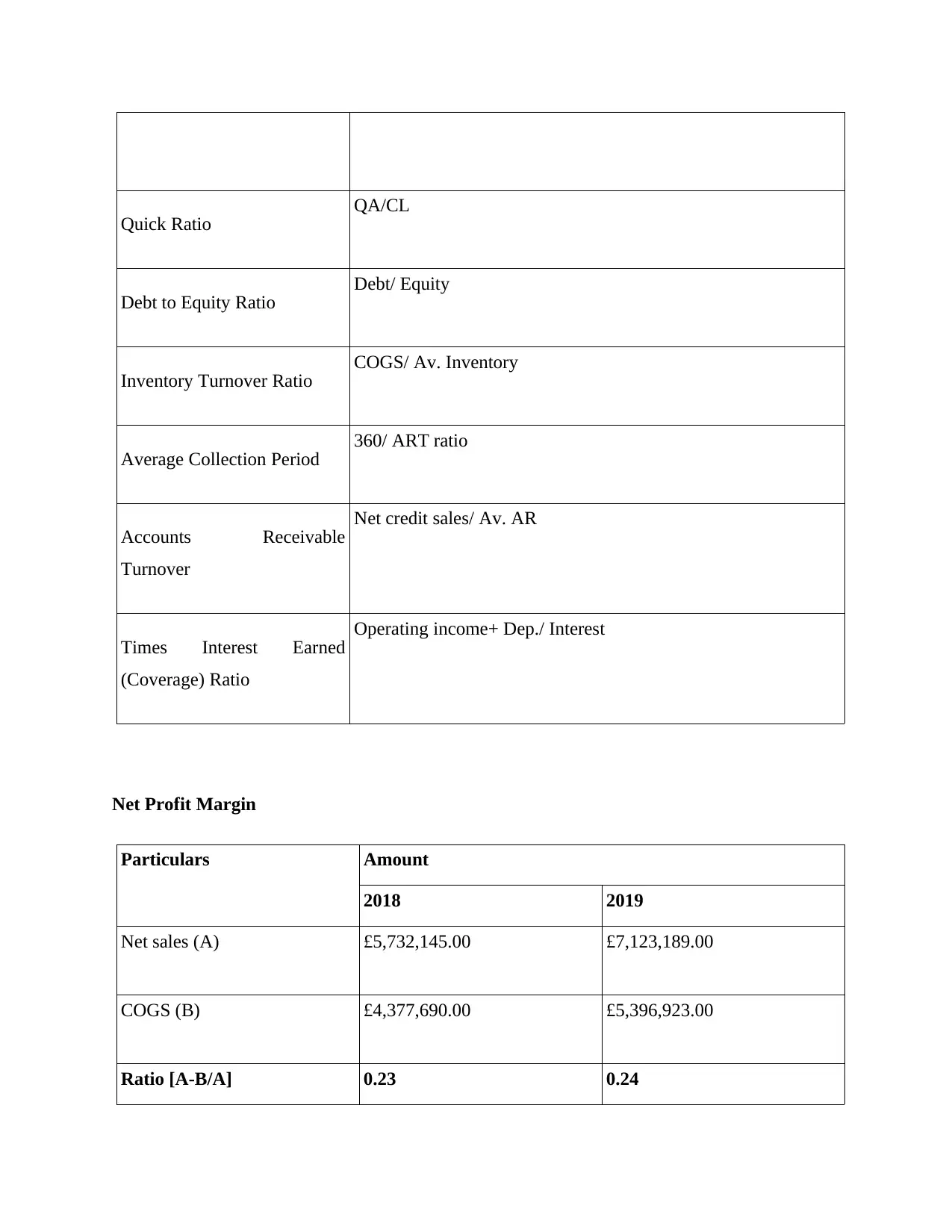

Quick Ratio QA/CL

Debt to Equity Ratio Debt/ Equity

Inventory Turnover Ratio COGS/ Av. Inventory

Average Collection Period 360/ ART ratio

Accounts Receivable

Turnover

Net credit sales/ Av. AR

Times Interest Earned

(Coverage) Ratio

Operating income+ Dep./ Interest

Net Profit Margin

Particulars Amount

2018 2019

Net sales (A) £5,732,145.00 £7,123,189.00

COGS (B) £4,377,690.00 £5,396,923.00

Ratio [A-B/A] 0.23 0.24

Debt to Equity Ratio Debt/ Equity

Inventory Turnover Ratio COGS/ Av. Inventory

Average Collection Period 360/ ART ratio

Accounts Receivable

Turnover

Net credit sales/ Av. AR

Times Interest Earned

(Coverage) Ratio

Operating income+ Dep./ Interest

Net Profit Margin

Particulars Amount

2018 2019

Net sales (A) £5,732,145.00 £7,123,189.00

COGS (B) £4,377,690.00 £5,396,923.00

Ratio [A-B/A] 0.23 0.24

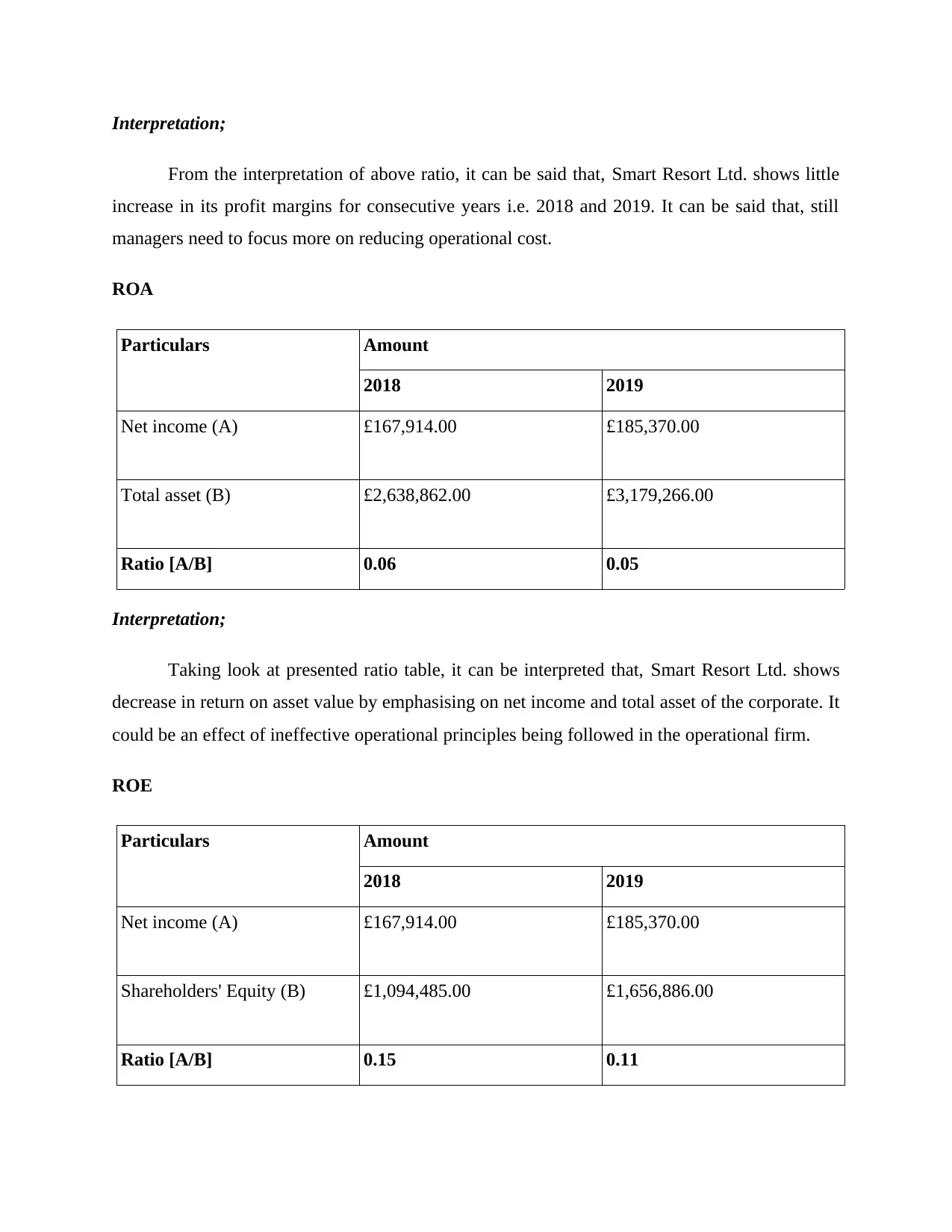

Interpretation;

From the interpretation of above ratio, it can be said that, Smart Resort Ltd. shows little

increase in its profit margins for consecutive years i.e. 2018 and 2019. It can be said that, still

managers need to focus more on reducing operational cost.

ROA

Particulars Amount

2018 2019

Net income (A) £167,914.00 £185,370.00

Total asset (B) £2,638,862.00 £3,179,266.00

Ratio [A/B] 0.06 0.05

Interpretation;

Taking look at presented ratio table, it can be interpreted that, Smart Resort Ltd. shows

decrease in return on asset value by emphasising on net income and total asset of the corporate. It

could be an effect of ineffective operational principles being followed in the operational firm.

ROE

Particulars Amount

2018 2019

Net income (A) £167,914.00 £185,370.00

Shareholders' Equity (B) £1,094,485.00 £1,656,886.00

Ratio [A/B] 0.15 0.11

From the interpretation of above ratio, it can be said that, Smart Resort Ltd. shows little

increase in its profit margins for consecutive years i.e. 2018 and 2019. It can be said that, still

managers need to focus more on reducing operational cost.

ROA

Particulars Amount

2018 2019

Net income (A) £167,914.00 £185,370.00

Total asset (B) £2,638,862.00 £3,179,266.00

Ratio [A/B] 0.06 0.05

Interpretation;

Taking look at presented ratio table, it can be interpreted that, Smart Resort Ltd. shows

decrease in return on asset value by emphasising on net income and total asset of the corporate. It

could be an effect of ineffective operational principles being followed in the operational firm.

ROE

Particulars Amount

2018 2019

Net income (A) £167,914.00 £185,370.00

Shareholders' Equity (B) £1,094,485.00 £1,656,886.00

Ratio [A/B] 0.15 0.11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

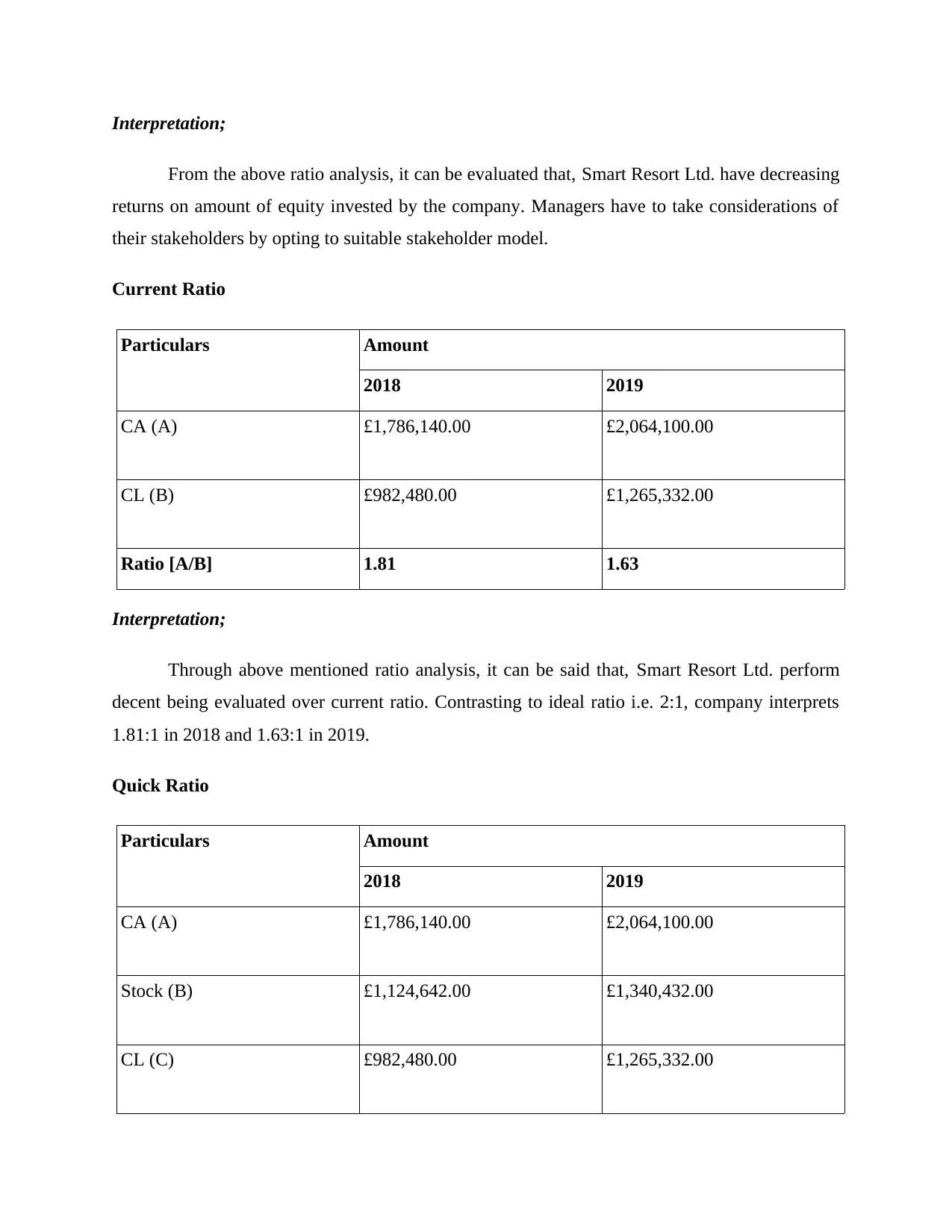

Interpretation;

From the above ratio analysis, it can be evaluated that, Smart Resort Ltd. have decreasing

returns on amount of equity invested by the company. Managers have to take considerations of

their stakeholders by opting to suitable stakeholder model.

Current Ratio

Particulars Amount

2018 2019

CA (A) £1,786,140.00 £2,064,100.00

CL (B) £982,480.00 £1,265,332.00

Ratio [A/B] 1.81 1.63

Interpretation;

Through above mentioned ratio analysis, it can be said that, Smart Resort Ltd. perform

decent being evaluated over current ratio. Contrasting to ideal ratio i.e. 2:1, company interprets

1.81:1 in 2018 and 1.63:1 in 2019.

Quick Ratio

Particulars Amount

2018 2019

CA (A) £1,786,140.00 £2,064,100.00

Stock (B) £1,124,642.00 £1,340,432.00

CL (C) £982,480.00 £1,265,332.00

From the above ratio analysis, it can be evaluated that, Smart Resort Ltd. have decreasing

returns on amount of equity invested by the company. Managers have to take considerations of

their stakeholders by opting to suitable stakeholder model.

Current Ratio

Particulars Amount

2018 2019

CA (A) £1,786,140.00 £2,064,100.00

CL (B) £982,480.00 £1,265,332.00

Ratio [A/B] 1.81 1.63

Interpretation;

Through above mentioned ratio analysis, it can be said that, Smart Resort Ltd. perform

decent being evaluated over current ratio. Contrasting to ideal ratio i.e. 2:1, company interprets

1.81:1 in 2018 and 1.63:1 in 2019.

Quick Ratio

Particulars Amount

2018 2019

CA (A) £1,786,140.00 £2,064,100.00

Stock (B) £1,124,642.00 £1,340,432.00

CL (C) £982,480.00 £1,265,332.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

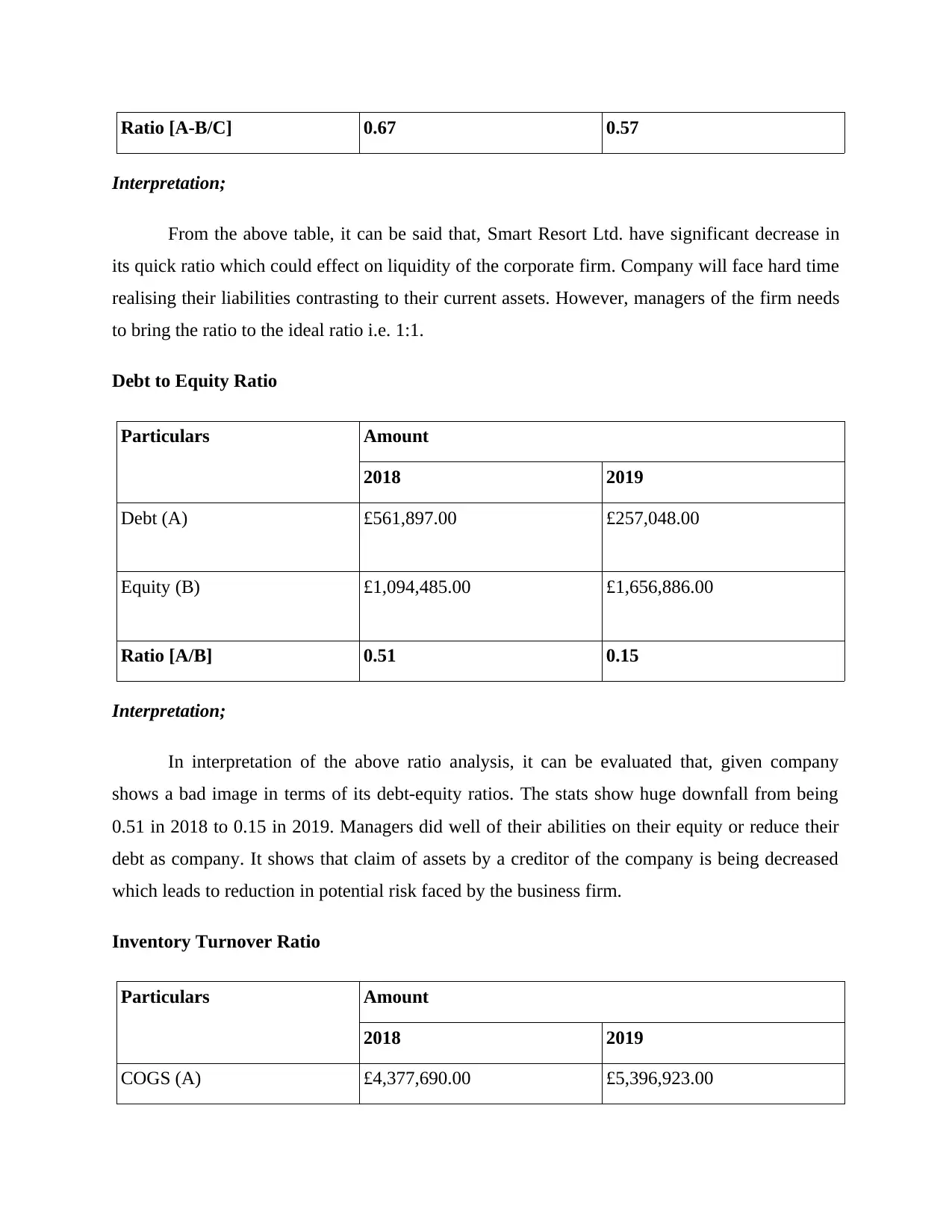

Ratio [A-B/C] 0.67 0.57

Interpretation;

From the above table, it can be said that, Smart Resort Ltd. have significant decrease in

its quick ratio which could effect on liquidity of the corporate firm. Company will face hard time

realising their liabilities contrasting to their current assets. However, managers of the firm needs

to bring the ratio to the ideal ratio i.e. 1:1.

Debt to Equity Ratio

Particulars Amount

2018 2019

Debt (A) £561,897.00 £257,048.00

Equity (B) £1,094,485.00 £1,656,886.00

Ratio [A/B] 0.51 0.15

Interpretation;

In interpretation of the above ratio analysis, it can be evaluated that, given company

shows a bad image in terms of its debt-equity ratios. The stats show huge downfall from being

0.51 in 2018 to 0.15 in 2019. Managers did well of their abilities on their equity or reduce their

debt as company. It shows that claim of assets by a creditor of the company is being decreased

which leads to reduction in potential risk faced by the business firm.

Inventory Turnover Ratio

Particulars Amount

2018 2019

COGS (A) £4,377,690.00 £5,396,923.00

Interpretation;

From the above table, it can be said that, Smart Resort Ltd. have significant decrease in

its quick ratio which could effect on liquidity of the corporate firm. Company will face hard time

realising their liabilities contrasting to their current assets. However, managers of the firm needs

to bring the ratio to the ideal ratio i.e. 1:1.

Debt to Equity Ratio

Particulars Amount

2018 2019

Debt (A) £561,897.00 £257,048.00

Equity (B) £1,094,485.00 £1,656,886.00

Ratio [A/B] 0.51 0.15

Interpretation;

In interpretation of the above ratio analysis, it can be evaluated that, given company

shows a bad image in terms of its debt-equity ratios. The stats show huge downfall from being

0.51 in 2018 to 0.15 in 2019. Managers did well of their abilities on their equity or reduce their

debt as company. It shows that claim of assets by a creditor of the company is being decreased

which leads to reduction in potential risk faced by the business firm.

Inventory Turnover Ratio

Particulars Amount

2018 2019

COGS (A) £4,377,690.00 £5,396,923.00

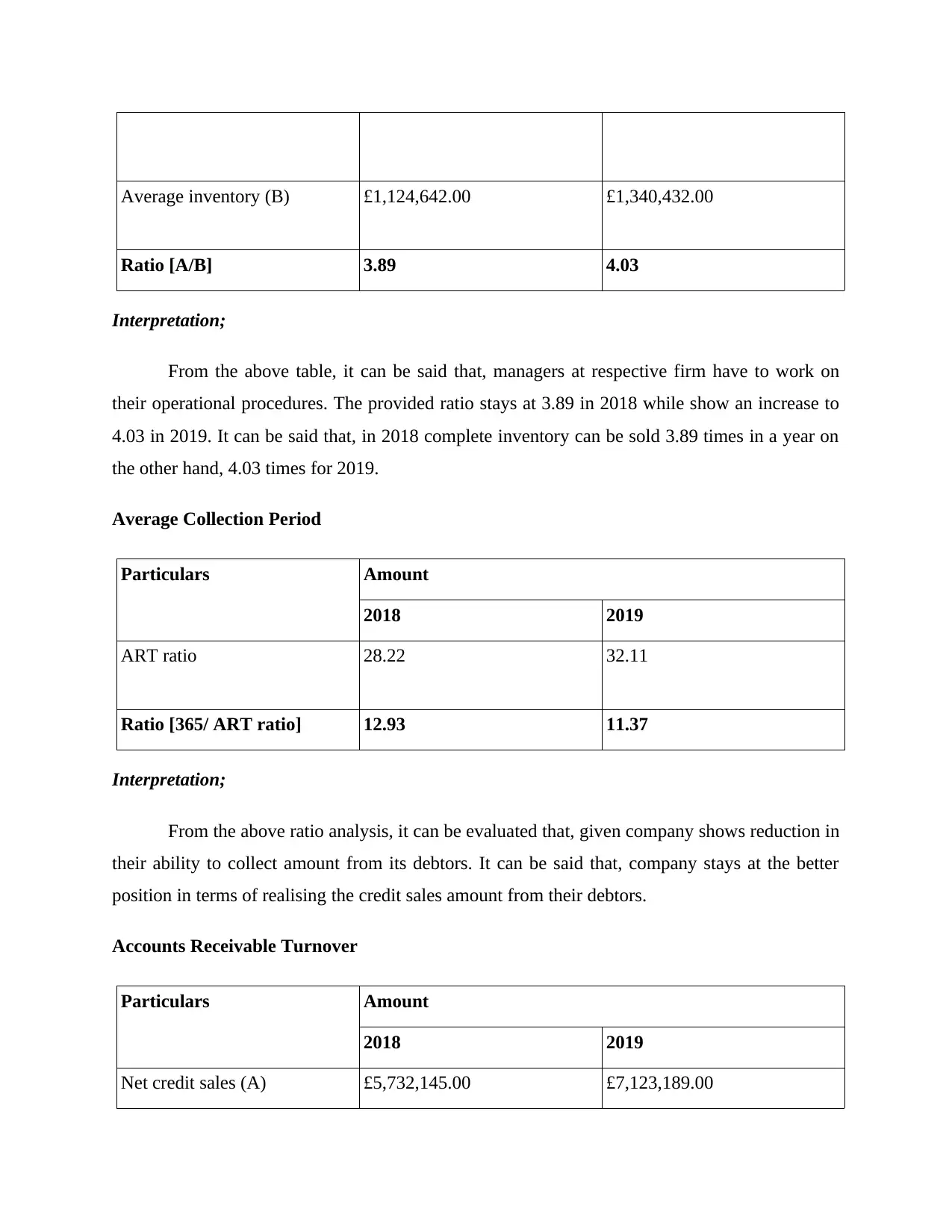

Average inventory (B) £1,124,642.00 £1,340,432.00

Ratio [A/B] 3.89 4.03

Interpretation;

From the above table, it can be said that, managers at respective firm have to work on

their operational procedures. The provided ratio stays at 3.89 in 2018 while show an increase to

4.03 in 2019. It can be said that, in 2018 complete inventory can be sold 3.89 times in a year on

the other hand, 4.03 times for 2019.

Average Collection Period

Particulars Amount

2018 2019

ART ratio 28.22 32.11

Ratio [365/ ART ratio] 12.93 11.37

Interpretation;

From the above ratio analysis, it can be evaluated that, given company shows reduction in

their ability to collect amount from its debtors. It can be said that, company stays at the better

position in terms of realising the credit sales amount from their debtors.

Accounts Receivable Turnover

Particulars Amount

2018 2019

Net credit sales (A) £5,732,145.00 £7,123,189.00

Ratio [A/B] 3.89 4.03

Interpretation;

From the above table, it can be said that, managers at respective firm have to work on

their operational procedures. The provided ratio stays at 3.89 in 2018 while show an increase to

4.03 in 2019. It can be said that, in 2018 complete inventory can be sold 3.89 times in a year on

the other hand, 4.03 times for 2019.

Average Collection Period

Particulars Amount

2018 2019

ART ratio 28.22 32.11

Ratio [365/ ART ratio] 12.93 11.37

Interpretation;

From the above ratio analysis, it can be evaluated that, given company shows reduction in

their ability to collect amount from its debtors. It can be said that, company stays at the better

position in terms of realising the credit sales amount from their debtors.

Accounts Receivable Turnover

Particulars Amount

2018 2019

Net credit sales (A) £5,732,145.00 £7,123,189.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.