Financial Resource Management Report: Analysis of Financial Statements

VerifiedAdded on 2020/10/22

|10

|2972

|260

Report

AI Summary

This report delves into the intricacies of financial resource management, beginning with a comparison between financial and management accounts, highlighting their distinct purposes and applications. It then explores the vital objectives of utilizing financial statements, differentiating between profit-oriented and non-profit organizations. The report proceeds to analyze various stakeholder groups and the critical data they require for decision-making. Furthermore, it undertakes a detailed examination of the financial performance of "Poundland Group Plc." through the calculation and interpretation of key financial ratios such as ROCE, current ratio, and gearing ratio. The analysis covers the years 2015 and 2016, offering insights into the company's financial health and performance trends. The report emphasizes the importance of financial data for stakeholders and the role of financial statements in assessing organizational growth and development.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Comparison among financial and management account......................................................1

1.2: Identify and make analyse of vital objectives of using financial statements.......................3

1.3: Various group of stakeholders and evaluating their vital data.............................................4

TASK 2............................................................................................................................................5

a): Calculation of various ratios..................................................................................................5

b): Compare the overall performance and present position........................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Comparison among financial and management account......................................................1

1.2: Identify and make analyse of vital objectives of using financial statements.......................3

1.3: Various group of stakeholders and evaluating their vital data.............................................4

TASK 2............................................................................................................................................5

a): Calculation of various ratios..................................................................................................5

b): Compare the overall performance and present position........................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

These days, it has been seen that Finance is a fundamental perspective that is related with

learning of each capital speculations. It manages flow of benefits and obligations over the time

under the given circumstances of different phases of vulnerability show in any basic leadership.

It has been discovered that without having appropriate accessibility of assets, a business can't

survive for longer time frame. This task report gives urgent data about financial and management

accounts. In addition, The purpose for which financial statements are used in both profit and non

profit organisation has been discussed in detail in this report. Assessment of various group of

stakeholders and make investigation of required information (inzhi, 2013). The general

information of "Poundland Group Plc." will be investigated by utilizing different types of ratios

in a detailed manner.

TASK 1

1.1: Comparison among financial and management account

It has been seen that each business association needs to influence utilization of

bookkeeping data with a specific end goal to have appropriate assessment of current year

execution of the organization. According to the specified contextual investigation of "Stratford

Yachts Ltd", they are not capable be present new product offerings. Customary items are the

significant parts of this organization however in ongoing time, they have produced most extreme

turnover to keep up their general exhibitions. Subsequent to making legitimate review in regards

to different offices and other fundamental things, they have chosen to name another

administration specialist who can help the organization to build its growth as well as overall

performance in an effective as well as efficient manner (Yin, 2016).

It is essential for Stratford Yachts Ltd to deal with their money related matters in more

promising ways so chances of getting most extreme advantages can be improved. In agreement

to assess execution of an association, it is important to make utilization of both financial and

management details at the same period of time. They happens to be more crucial piece of any

business undertaking. By they do have certain similarities which will be clarify as follows:

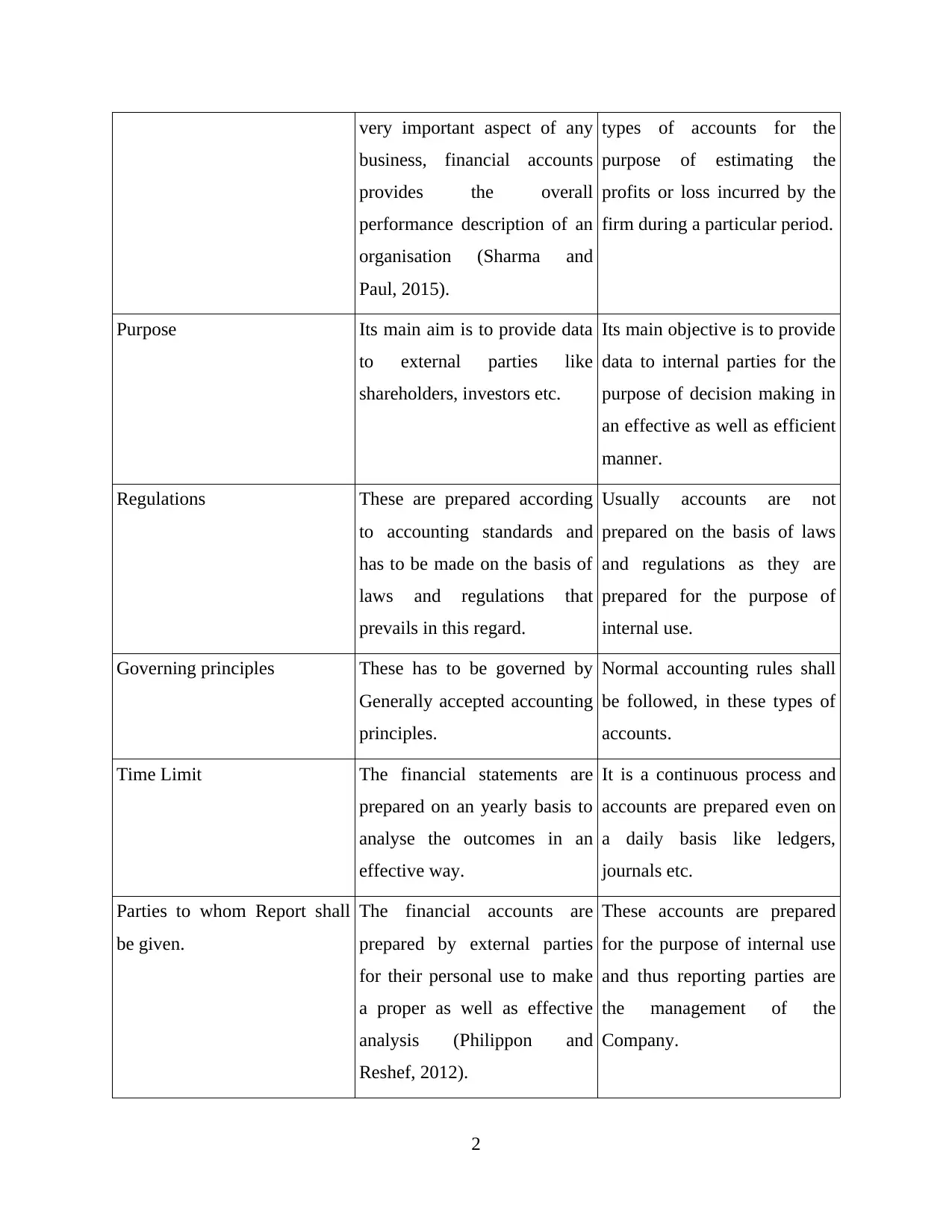

Particulars Financial accounts Management accounts

Definition The financial statement is a Management may use such

1

These days, it has been seen that Finance is a fundamental perspective that is related with

learning of each capital speculations. It manages flow of benefits and obligations over the time

under the given circumstances of different phases of vulnerability show in any basic leadership.

It has been discovered that without having appropriate accessibility of assets, a business can't

survive for longer time frame. This task report gives urgent data about financial and management

accounts. In addition, The purpose for which financial statements are used in both profit and non

profit organisation has been discussed in detail in this report. Assessment of various group of

stakeholders and make investigation of required information (inzhi, 2013). The general

information of "Poundland Group Plc." will be investigated by utilizing different types of ratios

in a detailed manner.

TASK 1

1.1: Comparison among financial and management account

It has been seen that each business association needs to influence utilization of

bookkeeping data with a specific end goal to have appropriate assessment of current year

execution of the organization. According to the specified contextual investigation of "Stratford

Yachts Ltd", they are not capable be present new product offerings. Customary items are the

significant parts of this organization however in ongoing time, they have produced most extreme

turnover to keep up their general exhibitions. Subsequent to making legitimate review in regards

to different offices and other fundamental things, they have chosen to name another

administration specialist who can help the organization to build its growth as well as overall

performance in an effective as well as efficient manner (Yin, 2016).

It is essential for Stratford Yachts Ltd to deal with their money related matters in more

promising ways so chances of getting most extreme advantages can be improved. In agreement

to assess execution of an association, it is important to make utilization of both financial and

management details at the same period of time. They happens to be more crucial piece of any

business undertaking. By they do have certain similarities which will be clarify as follows:

Particulars Financial accounts Management accounts

Definition The financial statement is a Management may use such

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

very important aspect of any

business, financial accounts

provides the overall

performance description of an

organisation (Sharma and

Paul, 2015).

types of accounts for the

purpose of estimating the

profits or loss incurred by the

firm during a particular period.

Purpose Its main aim is to provide data

to external parties like

shareholders, investors etc.

Its main objective is to provide

data to internal parties for the

purpose of decision making in

an effective as well as efficient

manner.

Regulations These are prepared according

to accounting standards and

has to be made on the basis of

laws and regulations that

prevails in this regard.

Usually accounts are not

prepared on the basis of laws

and regulations as they are

prepared for the purpose of

internal use.

Governing principles These has to be governed by

Generally accepted accounting

principles.

Normal accounting rules shall

be followed, in these types of

accounts.

Time Limit The financial statements are

prepared on an yearly basis to

analyse the outcomes in an

effective way.

It is a continuous process and

accounts are prepared even on

a daily basis like ledgers,

journals etc.

Parties to whom Report shall

be given.

The financial accounts are

prepared by external parties

for their personal use to make

a proper as well as effective

analysis (Philippon and

Reshef, 2012).

These accounts are prepared

for the purpose of internal use

and thus reporting parties are

the management of the

Company.

2

business, financial accounts

provides the overall

performance description of an

organisation (Sharma and

Paul, 2015).

types of accounts for the

purpose of estimating the

profits or loss incurred by the

firm during a particular period.

Purpose Its main aim is to provide data

to external parties like

shareholders, investors etc.

Its main objective is to provide

data to internal parties for the

purpose of decision making in

an effective as well as efficient

manner.

Regulations These are prepared according

to accounting standards and

has to be made on the basis of

laws and regulations that

prevails in this regard.

Usually accounts are not

prepared on the basis of laws

and regulations as they are

prepared for the purpose of

internal use.

Governing principles These has to be governed by

Generally accepted accounting

principles.

Normal accounting rules shall

be followed, in these types of

accounts.

Time Limit The financial statements are

prepared on an yearly basis to

analyse the outcomes in an

effective way.

It is a continuous process and

accounts are prepared even on

a daily basis like ledgers,

journals etc.

Parties to whom Report shall

be given.

The financial accounts are

prepared by external parties

for their personal use to make

a proper as well as effective

analysis (Philippon and

Reshef, 2012).

These accounts are prepared

for the purpose of internal use

and thus reporting parties are

the management of the

Company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

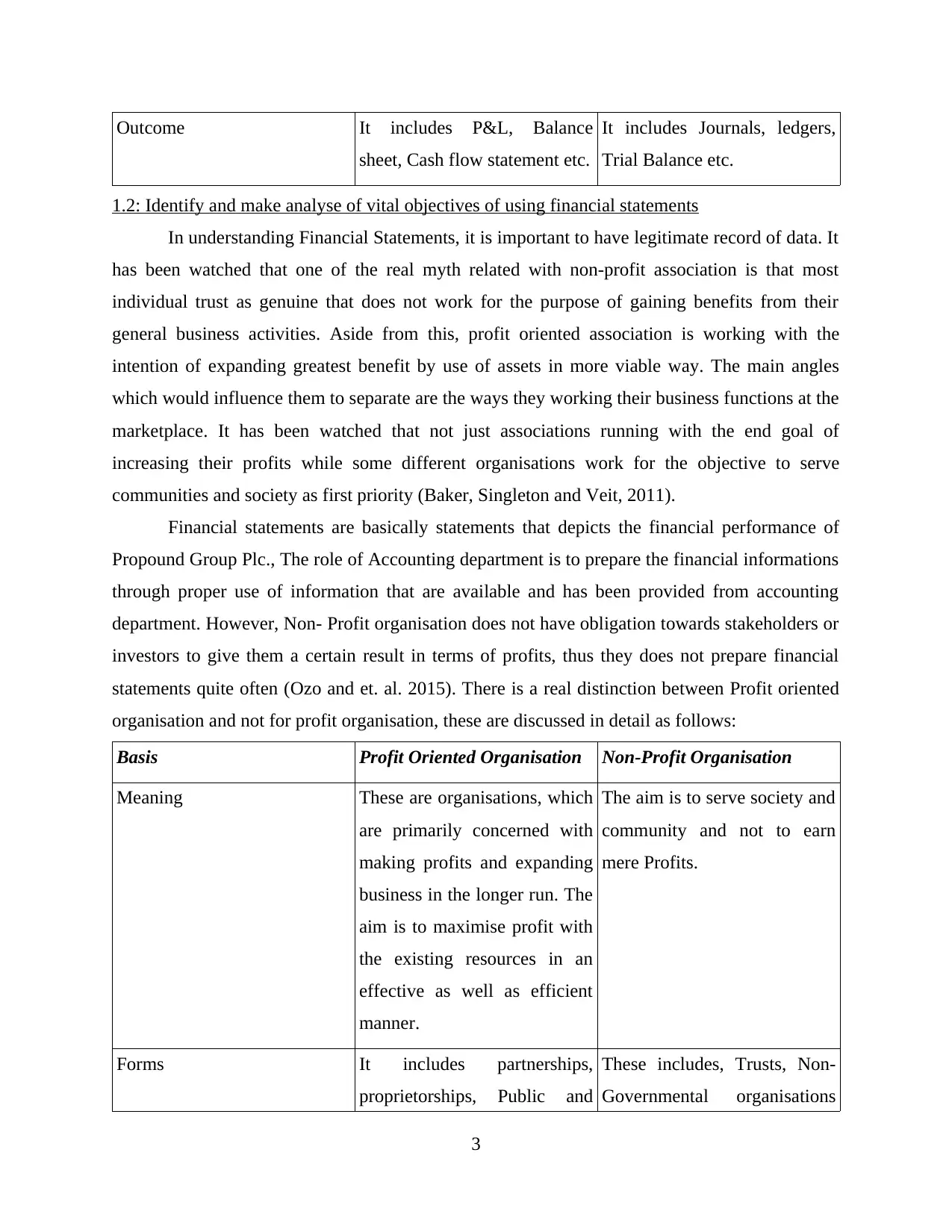

Outcome It includes P&L, Balance

sheet, Cash flow statement etc.

It includes Journals, ledgers,

Trial Balance etc.

1.2: Identify and make analyse of vital objectives of using financial statements

In understanding Financial Statements, it is important to have legitimate record of data. It

has been watched that one of the real myth related with non-profit association is that most

individual trust as genuine that does not work for the purpose of gaining benefits from their

general business activities. Aside from this, profit oriented association is working with the

intention of expanding greatest benefit by use of assets in more viable way. The main angles

which would influence them to separate are the ways they working their business functions at the

marketplace. It has been watched that not just associations running with the end goal of

increasing their profits while some different organisations work for the objective to serve

communities and society as first priority (Baker, Singleton and Veit, 2011).

Financial statements are basically statements that depicts the financial performance of

Propound Group Plc., The role of Accounting department is to prepare the financial informations

through proper use of information that are available and has been provided from accounting

department. However, Non- Profit organisation does not have obligation towards stakeholders or

investors to give them a certain result in terms of profits, thus they does not prepare financial

statements quite often (Ozo and et. al. 2015). There is a real distinction between Profit oriented

organisation and not for profit organisation, these are discussed in detail as follows:

Basis Profit Oriented Organisation Non-Profit Organisation

Meaning These are organisations, which

are primarily concerned with

making profits and expanding

business in the longer run. The

aim is to maximise profit with

the existing resources in an

effective as well as efficient

manner.

The aim is to serve society and

community and not to earn

mere Profits.

Forms It includes partnerships,

proprietorships, Public and

These includes, Trusts, Non-

Governmental organisations

3

sheet, Cash flow statement etc.

It includes Journals, ledgers,

Trial Balance etc.

1.2: Identify and make analyse of vital objectives of using financial statements

In understanding Financial Statements, it is important to have legitimate record of data. It

has been watched that one of the real myth related with non-profit association is that most

individual trust as genuine that does not work for the purpose of gaining benefits from their

general business activities. Aside from this, profit oriented association is working with the

intention of expanding greatest benefit by use of assets in more viable way. The main angles

which would influence them to separate are the ways they working their business functions at the

marketplace. It has been watched that not just associations running with the end goal of

increasing their profits while some different organisations work for the objective to serve

communities and society as first priority (Baker, Singleton and Veit, 2011).

Financial statements are basically statements that depicts the financial performance of

Propound Group Plc., The role of Accounting department is to prepare the financial informations

through proper use of information that are available and has been provided from accounting

department. However, Non- Profit organisation does not have obligation towards stakeholders or

investors to give them a certain result in terms of profits, thus they does not prepare financial

statements quite often (Ozo and et. al. 2015). There is a real distinction between Profit oriented

organisation and not for profit organisation, these are discussed in detail as follows:

Basis Profit Oriented Organisation Non-Profit Organisation

Meaning These are organisations, which

are primarily concerned with

making profits and expanding

business in the longer run. The

aim is to maximise profit with

the existing resources in an

effective as well as efficient

manner.

The aim is to serve society and

community and not to earn

mere Profits.

Forms It includes partnerships,

proprietorships, Public and

These includes, Trusts, Non-

Governmental organisations

3

Private companies etc. etc.

Income Sources Their income sources is the

funds received from

shareholders.

They largely depends on

external charity through

subscriptions, donations, and

various other fess etc.

Treatment of Extra Funds The money earned over the

and above the cost is sent to

general or capital reserve

account for future expansion

and growth.

The surplus earned are

transferred to capital gains

(Baker and Wurgler, 2011).

Thus, Financial statements plays a very crucial role in the overall growth and

development of the organisation

1.3: Various group of stakeholders and evaluating their vital data

It has been seen that "Propound Group Plc" needs to influence utilization of their money

related informations keeping in mind the end goal to decide current position of the organization.

It is vital for them to give appropriate esteem and enthusiasm to their outside and inside peoples

and groups, those are consistently working with the thought process to make greatest benefit in a

accounting term. It has been nearly looked that stakeholders are directly or indirectly related with

organization's future basic leadership process. They require to be all the more powerful and

valuable people in taking essential business task for the upcoming time. The business Managers

are in charge of impacting different key partners and grow full help for the task.

Through this approach would help director to evaluate add up to help to best way. All the

stakeholders must keep in mind the business interest for the purpose of making a effective

business plans in the long run. This will convey appropriate inclusion in framing of undertaking

and proper execution of most recent designs and strategies those are useful in improvement of an

organisation (Fan, Wei and Xu, 2011). This will improve their chances of getting right kind of

success at the market place.

The various types of Stakeholders that are important for an organisation are as follows:

Stakeholders: These are the parties who are directly affected by the performance of the

company in the longer run, these stakeholders includes customers, suppliers, governments etc.

4

Income Sources Their income sources is the

funds received from

shareholders.

They largely depends on

external charity through

subscriptions, donations, and

various other fess etc.

Treatment of Extra Funds The money earned over the

and above the cost is sent to

general or capital reserve

account for future expansion

and growth.

The surplus earned are

transferred to capital gains

(Baker and Wurgler, 2011).

Thus, Financial statements plays a very crucial role in the overall growth and

development of the organisation

1.3: Various group of stakeholders and evaluating their vital data

It has been seen that "Propound Group Plc" needs to influence utilization of their money

related informations keeping in mind the end goal to decide current position of the organization.

It is vital for them to give appropriate esteem and enthusiasm to their outside and inside peoples

and groups, those are consistently working with the thought process to make greatest benefit in a

accounting term. It has been nearly looked that stakeholders are directly or indirectly related with

organization's future basic leadership process. They require to be all the more powerful and

valuable people in taking essential business task for the upcoming time. The business Managers

are in charge of impacting different key partners and grow full help for the task.

Through this approach would help director to evaluate add up to help to best way. All the

stakeholders must keep in mind the business interest for the purpose of making a effective

business plans in the long run. This will convey appropriate inclusion in framing of undertaking

and proper execution of most recent designs and strategies those are useful in improvement of an

organisation (Fan, Wei and Xu, 2011). This will improve their chances of getting right kind of

success at the market place.

The various types of Stakeholders that are important for an organisation are as follows:

Stakeholders: These are the parties who are directly affected by the performance of the

company in the longer run, these stakeholders includes customers, suppliers, governments etc.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

They all are responsible for forming a organisation and thus the overall success and failure of a

firm, directly impacts the financial health of Stakeholders in the longer run. These stakeholders

can be divided into two parts, Primary and Secondary Stakeholders.

Primary Stakeholders: They are the one who are directly responsible for the growth and

development of the business, and they have a direct link with the success and Failure of

company, thus it is quite important to make sure that their role is not undermined in an

organisation. The risk of loss is also borne by these stakeholders, these primary Stakeholders are:

Partners:They earn profits and bears the loss directly, thus they play a crucial role in the success

of organisation, they are also known as shareholders of the organisation. They make strategies

and conduct overall research for the purpose of growth and development of the organisation.

Employees: They are the one who works for the company, on salary basis and are not directly

affected with company's profitability, it is an obligation on the company to pay salary, whether

profits has been made or not.

Customers: These are the most important part of any organisation, they are responsible for firm's

growth, if they will purchase goods and services of the organisation, then only company will be

able to make necessary profits in the longer run (Ding and Wermers, 2012).

Secondary Stakeholders: They does not directly hold any stake in the organisation, but are

influenced by the activities of the organisation in the longer run. These are parties are discussed

in detail as follows:

Competitors: They gets affected with the success or failure of the organisation in the longer run.

Hence they keep an eye on the performance of the organisation.

Government: The rules as well as regulations has been abided by the management or not is

checked by the Government, they also frame policies like taxation and fiscal etc, on the basis of

health of the sector and organisation (Coles, Lemmon and Meschke, 2012).

TASK 2

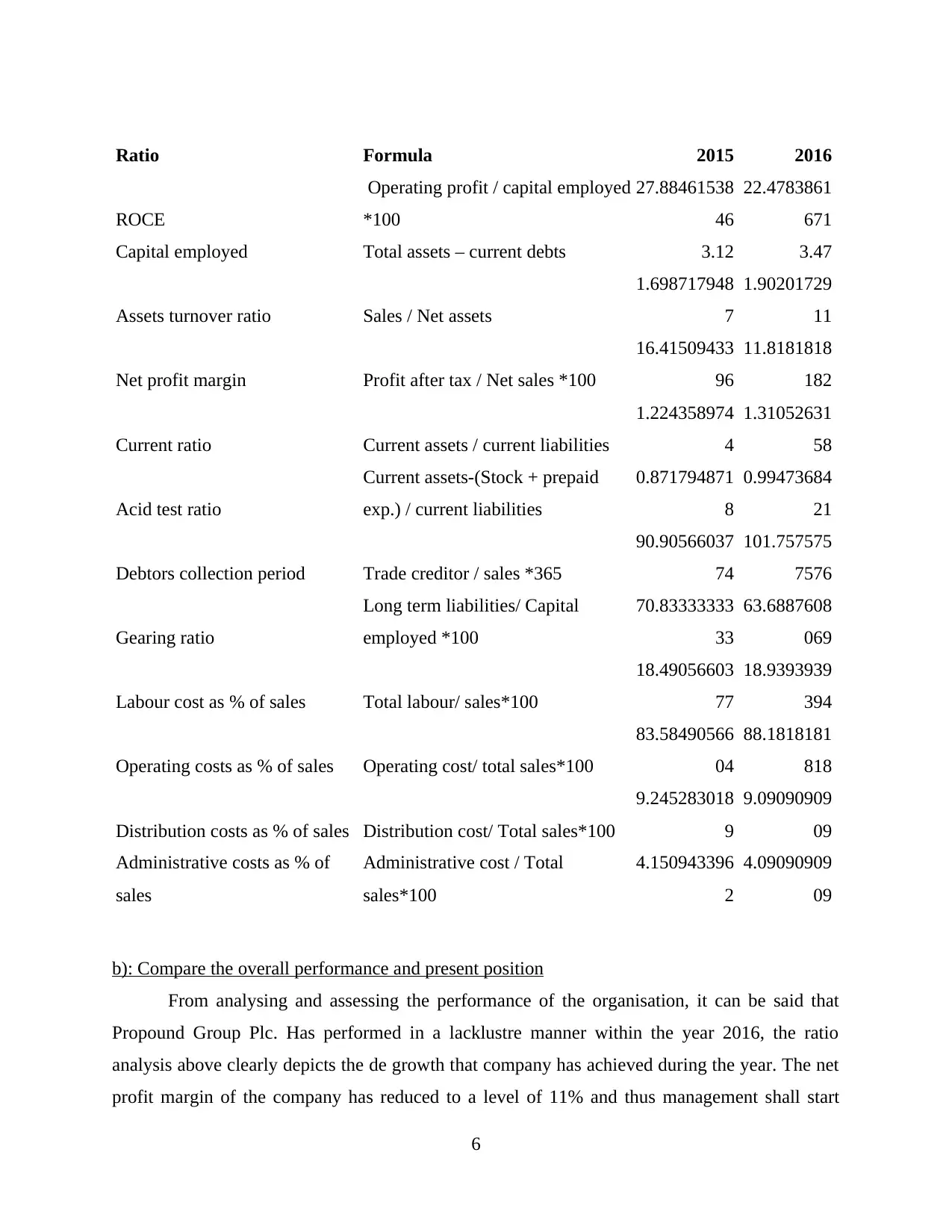

a): Calculation of various ratios

Ratios are a crucial part of financial analysis, Ratio Analysis sum up the health of an

organisation with right kind of ratios that will allow an investor or a user of financial resources to

reach to a conclusion as to what is the existing position of the firm and how it will perform going

forward in the longer run.

5

firm, directly impacts the financial health of Stakeholders in the longer run. These stakeholders

can be divided into two parts, Primary and Secondary Stakeholders.

Primary Stakeholders: They are the one who are directly responsible for the growth and

development of the business, and they have a direct link with the success and Failure of

company, thus it is quite important to make sure that their role is not undermined in an

organisation. The risk of loss is also borne by these stakeholders, these primary Stakeholders are:

Partners:They earn profits and bears the loss directly, thus they play a crucial role in the success

of organisation, they are also known as shareholders of the organisation. They make strategies

and conduct overall research for the purpose of growth and development of the organisation.

Employees: They are the one who works for the company, on salary basis and are not directly

affected with company's profitability, it is an obligation on the company to pay salary, whether

profits has been made or not.

Customers: These are the most important part of any organisation, they are responsible for firm's

growth, if they will purchase goods and services of the organisation, then only company will be

able to make necessary profits in the longer run (Ding and Wermers, 2012).

Secondary Stakeholders: They does not directly hold any stake in the organisation, but are

influenced by the activities of the organisation in the longer run. These are parties are discussed

in detail as follows:

Competitors: They gets affected with the success or failure of the organisation in the longer run.

Hence they keep an eye on the performance of the organisation.

Government: The rules as well as regulations has been abided by the management or not is

checked by the Government, they also frame policies like taxation and fiscal etc, on the basis of

health of the sector and organisation (Coles, Lemmon and Meschke, 2012).

TASK 2

a): Calculation of various ratios

Ratios are a crucial part of financial analysis, Ratio Analysis sum up the health of an

organisation with right kind of ratios that will allow an investor or a user of financial resources to

reach to a conclusion as to what is the existing position of the firm and how it will perform going

forward in the longer run.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio Formula 2015 2016

ROCE

Operating profit / capital employed

*100

27.88461538

46

22.4783861

671

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets

1.698717948

7

1.90201729

11

Net profit margin Profit after tax / Net sales *100

16.41509433

96

11.8181818

182

Current ratio Current assets / current liabilities

1.224358974

4

1.31052631

58

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities

0.871794871

8

0.99473684

21

Debtors collection period Trade creditor / sales *365

90.90566037

74

101.757575

7576

Gearing ratio

Long term liabilities/ Capital

employed *100

70.83333333

33

63.6887608

069

Labour cost as % of sales Total labour/ sales*100

18.49056603

77

18.9393939

394

Operating costs as % of sales Operating cost/ total sales*100

83.58490566

04

88.1818181

818

Distribution costs as % of sales Distribution cost/ Total sales*100

9.245283018

9

9.09090909

09

Administrative costs as % of

sales

Administrative cost / Total

sales*100

4.150943396

2

4.09090909

09

b): Compare the overall performance and present position

From analysing and assessing the performance of the organisation, it can be said that

Propound Group Plc. Has performed in a lacklustre manner within the year 2016, the ratio

analysis above clearly depicts the de growth that company has achieved during the year. The net

profit margin of the company has reduced to a level of 11% and thus management shall start

6

ROCE

Operating profit / capital employed

*100

27.88461538

46

22.4783861

671

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets

1.698717948

7

1.90201729

11

Net profit margin Profit after tax / Net sales *100

16.41509433

96

11.8181818

182

Current ratio Current assets / current liabilities

1.224358974

4

1.31052631

58

Acid test ratio

Current assets-(Stock + prepaid

exp.) / current liabilities

0.871794871

8

0.99473684

21

Debtors collection period Trade creditor / sales *365

90.90566037

74

101.757575

7576

Gearing ratio

Long term liabilities/ Capital

employed *100

70.83333333

33

63.6887608

069

Labour cost as % of sales Total labour/ sales*100

18.49056603

77

18.9393939

394

Operating costs as % of sales Operating cost/ total sales*100

83.58490566

04

88.1818181

818

Distribution costs as % of sales Distribution cost/ Total sales*100

9.245283018

9

9.09090909

09

Administrative costs as % of

sales

Administrative cost / Total

sales*100

4.150943396

2

4.09090909

09

b): Compare the overall performance and present position

From analysing and assessing the performance of the organisation, it can be said that

Propound Group Plc. Has performed in a lacklustre manner within the year 2016, the ratio

analysis above clearly depicts the de growth that company has achieved during the year. The net

profit margin of the company has reduced to a level of 11% and thus management shall start

6

focusing on its profitability in an effective manner. The Liquidity ratio of the company is close to

the ideal position that is 1:1 and, is a positive factor for the company. The labour cost of the

company is around 18% in both year. The operating cost of the company has risen to 88% from

83%, thus it can be said, that there is a specific need to overcome these challenges in an effective

manner to gain get back on to the path of Financial Growth as well as development. Management

of Propound Group Plc shall focus on improving the financial health of the organisation in an

effective as well as efficient manner.

CONCLUSION

From the above undertaking report, it has been presumed that taking care of money is

very intense task for each business. The results gathered out of general execution of the specified

organization is being assessed in more viable way. For this reason, they a well viable

examination is done in the middle of back and administration accounts with the goal that genuine

distinction can be decide in more effectively. Further, examination is create significant outcomes

from analyse benefit and non-benefit association budgetary articulations. The general

investigation helps with figuring particular proportions those are being useful in making

correlation among set industry targets. Toward the end, utilization of information with a specific

end goal to better understanding of monetary strategies in regard to expand better development

and execution in coming future time.

7

the ideal position that is 1:1 and, is a positive factor for the company. The labour cost of the

company is around 18% in both year. The operating cost of the company has risen to 88% from

83%, thus it can be said, that there is a specific need to overcome these challenges in an effective

manner to gain get back on to the path of Financial Growth as well as development. Management

of Propound Group Plc shall focus on improving the financial health of the organisation in an

effective as well as efficient manner.

CONCLUSION

From the above undertaking report, it has been presumed that taking care of money is

very intense task for each business. The results gathered out of general execution of the specified

organization is being assessed in more viable way. For this reason, they a well viable

examination is done in the middle of back and administration accounts with the goal that genuine

distinction can be decide in more effectively. Further, examination is create significant outcomes

from analyse benefit and non-benefit association budgetary articulations. The general

investigation helps with figuring particular proportions those are being useful in making

correlation among set industry targets. Toward the end, utilization of information with a specific

end goal to better understanding of monetary strategies in regard to expand better development

and execution in coming future time.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

inzhi, M., 2013. Controlling Shareholders, Professional Managers and Independent Directors in

the Family Enterprise Governance. Peking University Law Review. 1. p.014.

Yin, C., 2016. The optimal size of hedge funds: conflict between investors and fund managers.

The Journal of Finance. 71(4). pp.1857-1894.

Sharma, P. and Paul, S., 2015. Testing the skill of mutual fund managers: evidence from India.

Managerial Finance. 41(8). pp.806-824.

Philippon, T. and Reshef, A., 2012. Wages and human capital in the US finance industry: 1909–

2006. The Quarterly Journal of Economics. 127(4). pp.1551-1609.

Ozo, F. K. and et. al. 2015. Corporate dividend policy in practice: the views of Nigerian financial

managers. Managerial Finance. 41(11). pp.1159-1175.

Fan, J. P., Wei, K. J. and Xu, X., 2011. Corporate finance and governance in emerging markets:

A selective review and an agenda for future research.

Ding, B. and Wermers, R., 2012. Mutual fund performance and governance structure: The role of

portfolio managers and boards of directors.

Coles, J. L., Lemmon, M. L. and Meschke, J.F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance.

Journal of Financial Economics. 103(1). pp.149-168.

Baker, M. and Wurgler, J., 2011. Behavioral corporate finance: An updated survey (No.

w17333). National Bureau of Economic Research.

Baker, H. K., Singleton, J. C. and Veit, E. T., 2011. Survey research in corporate finance:

bridging the gap between theory and practice. Oxford University Press.

Ang, W. R., Gregoriou, G. N. and Lean, H. H., 2014. Market-timing skills of socially responsible

investment fund managers: The case of North America versus Europe. Journal of Asset

Management. 15(6). pp.366-377.

Online

Meaning of finance reporting and record, 2017. [Online] Avalialble

through<https://www.amazon.com/Finance-Managers-Harvard-Business-Essentials/dp/

1578518768>

8

Books and Journals

inzhi, M., 2013. Controlling Shareholders, Professional Managers and Independent Directors in

the Family Enterprise Governance. Peking University Law Review. 1. p.014.

Yin, C., 2016. The optimal size of hedge funds: conflict between investors and fund managers.

The Journal of Finance. 71(4). pp.1857-1894.

Sharma, P. and Paul, S., 2015. Testing the skill of mutual fund managers: evidence from India.

Managerial Finance. 41(8). pp.806-824.

Philippon, T. and Reshef, A., 2012. Wages and human capital in the US finance industry: 1909–

2006. The Quarterly Journal of Economics. 127(4). pp.1551-1609.

Ozo, F. K. and et. al. 2015. Corporate dividend policy in practice: the views of Nigerian financial

managers. Managerial Finance. 41(11). pp.1159-1175.

Fan, J. P., Wei, K. J. and Xu, X., 2011. Corporate finance and governance in emerging markets:

A selective review and an agenda for future research.

Ding, B. and Wermers, R., 2012. Mutual fund performance and governance structure: The role of

portfolio managers and boards of directors.

Coles, J. L., Lemmon, M. L. and Meschke, J.F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance.

Journal of Financial Economics. 103(1). pp.149-168.

Baker, M. and Wurgler, J., 2011. Behavioral corporate finance: An updated survey (No.

w17333). National Bureau of Economic Research.

Baker, H. K., Singleton, J. C. and Veit, E. T., 2011. Survey research in corporate finance:

bridging the gap between theory and practice. Oxford University Press.

Ang, W. R., Gregoriou, G. N. and Lean, H. H., 2014. Market-timing skills of socially responsible

investment fund managers: The case of North America versus Europe. Journal of Asset

Management. 15(6). pp.366-377.

Online

Meaning of finance reporting and record, 2017. [Online] Avalialble

through<https://www.amazon.com/Finance-Managers-Harvard-Business-Essentials/dp/

1578518768>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.