Financial Resource Management Task 1: Assessment One Solution

VerifiedAdded on 2023/01/11

|15

|5339

|52

Homework Assignment

AI Summary

This assignment solution delves into the core principles of financial resource management, encompassing the revenue, expense, matching, cost, and objectivity principles. It then provides a detailed analysis of financial statements, including profit and loss statements, balance sheets, and cash flow statements, explaining their key features and interrelationships. The solution also explores different types of communication, such as written and oral, and their application in a business context. Additionally, it covers essential aspects of effective communication in the workplace, emphasizing data-driven and collaborative approaches. Finally, the document outlines the requirements for financial reporting, including the necessary documents and the GST reporting cycle, providing a comprehensive overview of financial management concepts.

MANAGE FINANCIAL RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 1

Assessment one:

1.

(a) Revenue principle- In accordance of this principle, revenue will only be registered if (1) the

method of raising revenue is reasonably completed and (2) the transaction has been carried out.

The old rule is a reaffirmation. The concept of revenue recognition along with the matching

theory is a foundation for accrual accounting. The principle of revenue recognition implies that

income should be recorded when earned, not when it is raised. For example, managing with a

snowflake finishes a group parking lot for the usual $ 100 rate. It can find an unlimited revenue

supply, regardless of whether it increases the allowance by the person- buy for half a month.

This idea is reinforced in the foundation of accounting collection.

(b) The expense principle- The principal difference between accrual reports and cash is the concept

of expense recognition. In order to remember that, if money is received or charged, the accrual

accounting method considers revenues and expenses. Nevertheless, as long as currency is

obtained or charged, the cash management system considers sales or expenses. For instance, a

company spends $100,000 to good and services, that also sells for $150,000 in the coming

season. The $100,000 costs should not be recorded as an expense until the month after the

corresponding income is also identified, under the principle of expense recognition. Anything

else, the present month will surpass the costs by $100,000 and the next month by $100,000.

(c) The matching principle- The concept of matching is one of the fundamental accounting rules. In

the period in which the related profits are received, the underlying principle directs a

corporation to record an expense on its income statement. In the event that a cost isn't

legitimately attached to incomes, the cost ought to be accounted for on the salary proclamation

in the bookkeeping time frame in which it lapses or is spent. In the event that the future

advantage of an expense can't be resolved, it ought to be charged to cost right away.

(d) The cost principle- One of the fundamental principles for accounting is the cost principle. This is

also known as traditional accounting principle. Accounts must be reported at the moment when

the property is purchased in the sum of cash (or the equivalent). In addition, inflation or market

value enhancements will not increase the number registered. (An exception was the change in

market value of a company's short-term equity investment, whose company stock is active in

the large stock exchange.)

(e) The objectivity principle- The concept of objectivity is that a company's monetary statements

are based on solid proof. The purpose of that concept is to prevent financial reports that have

Assessment one:

1.

(a) Revenue principle- In accordance of this principle, revenue will only be registered if (1) the

method of raising revenue is reasonably completed and (2) the transaction has been carried out.

The old rule is a reaffirmation. The concept of revenue recognition along with the matching

theory is a foundation for accrual accounting. The principle of revenue recognition implies that

income should be recorded when earned, not when it is raised. For example, managing with a

snowflake finishes a group parking lot for the usual $ 100 rate. It can find an unlimited revenue

supply, regardless of whether it increases the allowance by the person- buy for half a month.

This idea is reinforced in the foundation of accounting collection.

(b) The expense principle- The principal difference between accrual reports and cash is the concept

of expense recognition. In order to remember that, if money is received or charged, the accrual

accounting method considers revenues and expenses. Nevertheless, as long as currency is

obtained or charged, the cash management system considers sales or expenses. For instance, a

company spends $100,000 to good and services, that also sells for $150,000 in the coming

season. The $100,000 costs should not be recorded as an expense until the month after the

corresponding income is also identified, under the principle of expense recognition. Anything

else, the present month will surpass the costs by $100,000 and the next month by $100,000.

(c) The matching principle- The concept of matching is one of the fundamental accounting rules. In

the period in which the related profits are received, the underlying principle directs a

corporation to record an expense on its income statement. In the event that a cost isn't

legitimately attached to incomes, the cost ought to be accounted for on the salary proclamation

in the bookkeeping time frame in which it lapses or is spent. In the event that the future

advantage of an expense can't be resolved, it ought to be charged to cost right away.

(d) The cost principle- One of the fundamental principles for accounting is the cost principle. This is

also known as traditional accounting principle. Accounts must be reported at the moment when

the property is purchased in the sum of cash (or the equivalent). In addition, inflation or market

value enhancements will not increase the number registered. (An exception was the change in

market value of a company's short-term equity investment, whose company stock is active in

the large stock exchange.)

(e) The objectivity principle- The concept of objectivity is that a company's monetary statements

are based on solid proof. The purpose of that concept is to prevent financial reports that have

their views and partialities slanted by the management and accounting department of the

organization. The rule of objectivity is the idea that the association's budget summaries are

based on substantial validation. The goal behind this standard is to prevent the accounting

administration and branch from creating tax reports that depend on your feelings and opinions.

For example, if the board accepts that it will receive an immediate payment from an application,

it can cash in the proceeds from the payment, despite the fact that evidence that pretends that

such a result will not occur. An increasingly targeted vision is awaiting further data before

making such a diagnosis.

2.

Financial statements are detailed reports of a company, individual or other entity's financial transactions

and role. Structured and in a simple to understand way, appropriate financial information is provided.

Each organization that sells and offers its stock to the open must document money related reports and

explanations with the Securities and Exchange Commission (SEC). The three fundamental budget reports

are the monetary record and salary proclamation. The income proclamation is a significant report that

helps open a breeze invested individual’s knowledge into all the exchanges that experience an

organization. Below three types of financial statements are mentioned that are as follows:

Profit and loss statement- One of the company's financial statements, which displays income and

expenditure during a given period is an income statement or profit and loss account (also known to as

profit and loss statement (P&L), profit or loss statements, revenue statement, analysis of income

performance, declaration of profit or income statement, assertion of earnings, operating statement or

statement of operational activities). It shows whether the income (also referred to as "top line"), since

accounting for both sales and cost, is converted into net revenue or net profit. It has below mentioned

features that are as follows:

This statement is made periodically and after planning a organization gets an indication whether

it has profited or gained in the year.

The income and loss statement just displays the figures without explaining whether benefit or

loss are achieved which does not explain what a corporation performs in plain terms.

This statement does not show the company's capital costs such as procurement of buildings or

installation of plants and machines. Yet income or expenses from the disposal of capital assets

are expressed in profit and loss accounts.

Balance sheet- It can be defined as a financial statement includes the framework for the calculation of

returns levels and measures the allocation of resources at a given period, and lists the properties,

liabilities and equities of the business at a specific level. It has below mentioned features that are as

follows:

It is not a time, but a specific day, to file a balance sheet.

organization. The rule of objectivity is the idea that the association's budget summaries are

based on substantial validation. The goal behind this standard is to prevent the accounting

administration and branch from creating tax reports that depend on your feelings and opinions.

For example, if the board accepts that it will receive an immediate payment from an application,

it can cash in the proceeds from the payment, despite the fact that evidence that pretends that

such a result will not occur. An increasingly targeted vision is awaiting further data before

making such a diagnosis.

2.

Financial statements are detailed reports of a company, individual or other entity's financial transactions

and role. Structured and in a simple to understand way, appropriate financial information is provided.

Each organization that sells and offers its stock to the open must document money related reports and

explanations with the Securities and Exchange Commission (SEC). The three fundamental budget reports

are the monetary record and salary proclamation. The income proclamation is a significant report that

helps open a breeze invested individual’s knowledge into all the exchanges that experience an

organization. Below three types of financial statements are mentioned that are as follows:

Profit and loss statement- One of the company's financial statements, which displays income and

expenditure during a given period is an income statement or profit and loss account (also known to as

profit and loss statement (P&L), profit or loss statements, revenue statement, analysis of income

performance, declaration of profit or income statement, assertion of earnings, operating statement or

statement of operational activities). It shows whether the income (also referred to as "top line"), since

accounting for both sales and cost, is converted into net revenue or net profit. It has below mentioned

features that are as follows:

This statement is made periodically and after planning a organization gets an indication whether

it has profited or gained in the year.

The income and loss statement just displays the figures without explaining whether benefit or

loss are achieved which does not explain what a corporation performs in plain terms.

This statement does not show the company's capital costs such as procurement of buildings or

installation of plants and machines. Yet income or expenses from the disposal of capital assets

are expressed in profit and loss accounts.

Balance sheet- It can be defined as a financial statement includes the framework for the calculation of

returns levels and measures the allocation of resources at a given period, and lists the properties,

liabilities and equities of the business at a specific level. It has below mentioned features that are as

follows:

It is not a time, but a specific day, to file a balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The balance sheet is not accessible after the timeline is written up as a function of the

assumption that it properly represents the company's financial condition.

The sums of the two sides, i.e. the balance sheet assets and liabilities, must be counted as Assets

= Liabilities and Capital. If not, an error could also occur.

Cash flow statement- A cash flow statement is a financial statement which gives historical information

on all cash inflows obtained from the company's long - term activities and external sources of

investment. A cash flow statement is a balance sheet that provides complete information on the cash

flows an organization receives from its ongoing activities and external sources of risk. In the same way it

encompasses every wave of money that businesses pay for and profit at a given time.

Company financial statements offer speculators and auditors a snapshot of the large number of

exchanges that remain in the business, in which each exchange increases its wealth. Defining revenue is

considered the most natural of the budget shortfalls because it follows the money the company made in

three main ways: through business, business and finance. These three components are called total

revenue.

It has below mentioned features that are as follows:

The Cash Flow Statement is very vibrant since from the start of the period until the end of the

term the expenditure of cash was recorded.

The transition of financial roles of structural, acquisition and financial operations can be seen by

an observer. The analysis is based on this transition.

This statement helps in the calculation of operational cash / cash flows.

How they are all linked and dependent on each other-

Income statement, balance sheet, and cash flow analysis are contained in the annual

statements. The following bullet points show that these three statements interconnect in several ways:

On the statement of profits, the net profit number is applied to the revenue line item on the

balance sheet, and increases the sum of equity on the balance sheet.

The net profit statistic is often seen as a cash flow line element in the financial flows of the cash

flows analysis.

The balance sheet also contains the actual capital position in the cash flow statement.

3.

(a) Written communication- Written communication includes all kinds of interactions using the written

word. Communication is a key to any endeavor affecting more than one individual. There was a

assumption that it properly represents the company's financial condition.

The sums of the two sides, i.e. the balance sheet assets and liabilities, must be counted as Assets

= Liabilities and Capital. If not, an error could also occur.

Cash flow statement- A cash flow statement is a financial statement which gives historical information

on all cash inflows obtained from the company's long - term activities and external sources of

investment. A cash flow statement is a balance sheet that provides complete information on the cash

flows an organization receives from its ongoing activities and external sources of risk. In the same way it

encompasses every wave of money that businesses pay for and profit at a given time.

Company financial statements offer speculators and auditors a snapshot of the large number of

exchanges that remain in the business, in which each exchange increases its wealth. Defining revenue is

considered the most natural of the budget shortfalls because it follows the money the company made in

three main ways: through business, business and finance. These three components are called total

revenue.

It has below mentioned features that are as follows:

The Cash Flow Statement is very vibrant since from the start of the period until the end of the

term the expenditure of cash was recorded.

The transition of financial roles of structural, acquisition and financial operations can be seen by

an observer. The analysis is based on this transition.

This statement helps in the calculation of operational cash / cash flows.

How they are all linked and dependent on each other-

Income statement, balance sheet, and cash flow analysis are contained in the annual

statements. The following bullet points show that these three statements interconnect in several ways:

On the statement of profits, the net profit number is applied to the revenue line item on the

balance sheet, and increases the sum of equity on the balance sheet.

The net profit statistic is often seen as a cash flow line element in the financial flows of the cash

flows analysis.

The balance sheet also contains the actual capital position in the cash flow statement.

3.

(a) Written communication- Written communication includes all kinds of interactions using the written

word. Communication is a key to any endeavor affecting more than one individual. There was a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

misunderstanding. This is effective when there is any official announcement or there is more number of

listeners.

Oral communication - Verbal communication is the use of words for information sharing with others.

Consequently, these can involve correspondence both spoken and published. However, many people

use this word just to explain speech. This is used for informal communication. Skills are a wonderful

relationship between kids and achievements in an academic and commercial world. However, have you

ever experienced fear or discomfort before attending a scheduled employee meeting or speaking in

front of a crowd? Understanding when to choose oral communication and cleaning up your oral skills

can help you at every stage of your career.

With pushes for innovation, they continue to create new types of oral letters. Video intercoms and video

collections combine audio and video so that workers in displaced areas can see and talk to each other.

Other typical types of oral communication include digital broadcasts (audio calls that can be accessed via

the Internet) and Voice over Internet Protocol (VoIP), which allows guests to communicate on the

Internet and maintain a strategic distance from telephone rates. Skype is a case of VoIP.

(b)

Data-driven and measurable- The data-driven and measurable interaction of employees should

be. Usually, people can easily get information to assert cause and effect and improve their

tactics.

Personal, Specific and Actionable- This idea is simpler to say than done: workers will be open to

similar contact asking them what to do.

Sensitivity to employee time and attention- Employee sensitivity obeys step two because they

are indistinguishable – both aspects really are the identical greater concept: respecting

employees.

Collaborative and enabling- Budgets for workplace contact usually do not rise. This means that

we need to be entrepreneurs if the impacts of our teams on our organizations are to be

measured.

Creatively designed- Clever architecture makes use and enhances with every incarnation of data

reflecting real human behavior patterns. Good design makes the experience that has been

designed feel as though it was made for me while upholding my time and quickly reaches my

desired result.

(c)

Lack of communication creates unsatisfactory expectations. Teams are missing delays,

customers are missing appointments and project participants seem to be not aware of their

roles.

listeners.

Oral communication - Verbal communication is the use of words for information sharing with others.

Consequently, these can involve correspondence both spoken and published. However, many people

use this word just to explain speech. This is used for informal communication. Skills are a wonderful

relationship between kids and achievements in an academic and commercial world. However, have you

ever experienced fear or discomfort before attending a scheduled employee meeting or speaking in

front of a crowd? Understanding when to choose oral communication and cleaning up your oral skills

can help you at every stage of your career.

With pushes for innovation, they continue to create new types of oral letters. Video intercoms and video

collections combine audio and video so that workers in displaced areas can see and talk to each other.

Other typical types of oral communication include digital broadcasts (audio calls that can be accessed via

the Internet) and Voice over Internet Protocol (VoIP), which allows guests to communicate on the

Internet and maintain a strategic distance from telephone rates. Skype is a case of VoIP.

(b)

Data-driven and measurable- The data-driven and measurable interaction of employees should

be. Usually, people can easily get information to assert cause and effect and improve their

tactics.

Personal, Specific and Actionable- This idea is simpler to say than done: workers will be open to

similar contact asking them what to do.

Sensitivity to employee time and attention- Employee sensitivity obeys step two because they

are indistinguishable – both aspects really are the identical greater concept: respecting

employees.

Collaborative and enabling- Budgets for workplace contact usually do not rise. This means that

we need to be entrepreneurs if the impacts of our teams on our organizations are to be

measured.

Creatively designed- Clever architecture makes use and enhances with every incarnation of data

reflecting real human behavior patterns. Good design makes the experience that has been

designed feel as though it was made for me while upholding my time and quickly reaches my

desired result.

(c)

Lack of communication creates unsatisfactory expectations. Teams are missing delays,

customers are missing appointments and project participants seem to be not aware of their

roles.

Intensive emotions spend more time in emotional management than usual when it comes to

people. Productivity declines and honesty is substituted with an all-day feeling of relaxation.

Unhappy consumers can be a symbol of poor communication. In the event that teams miss

deadlines, superiors are usually anxious and upset, and customers are also frustrated.

4.

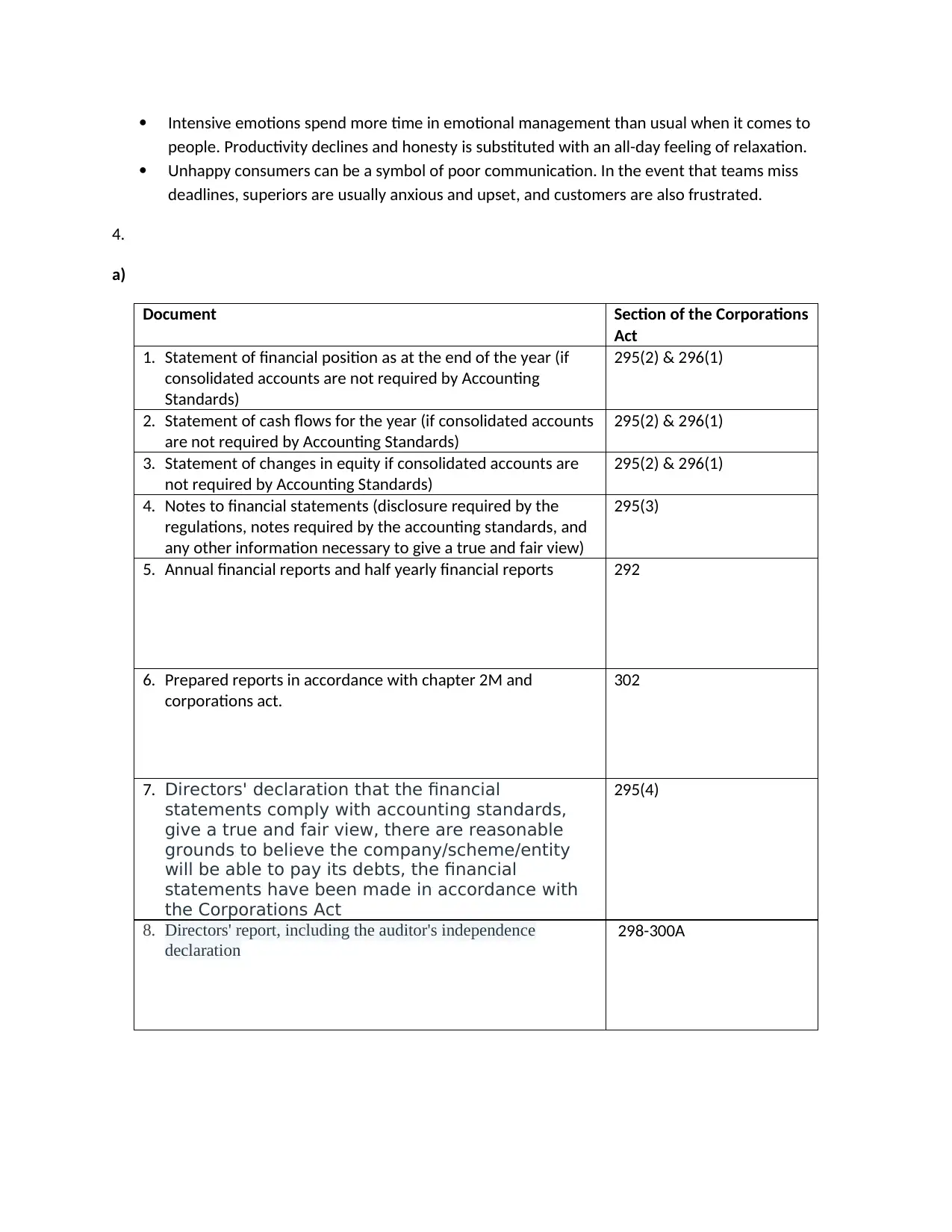

a)

Document Section of the Corporations

Act

1. Statement of financial position as at the end of the year (if

consolidated accounts are not required by Accounting

Standards)

295(2) & 296(1)

2. Statement of cash flows for the year (if consolidated accounts

are not required by Accounting Standards)

295(2) & 296(1)

3. Statement of changes in equity if consolidated accounts are

not required by Accounting Standards)

295(2) & 296(1)

4. Notes to financial statements (disclosure required by the

regulations, notes required by the accounting standards, and

any other information necessary to give a true and fair view)

295(3)

5. Annual financial reports and half yearly financial reports 292

6. Prepared reports in accordance with chapter 2M and

corporations act.

302

7. Directors' declaration that the financial

statements comply with accounting standards,

give a true and fair view, there are reasonable

grounds to believe the company/scheme/entity

will be able to pay its debts, the financial

statements have been made in accordance with

the Corporations Act

295(4)

8. Directors' report, including the auditor's independence

declaration

298-300A

people. Productivity declines and honesty is substituted with an all-day feeling of relaxation.

Unhappy consumers can be a symbol of poor communication. In the event that teams miss

deadlines, superiors are usually anxious and upset, and customers are also frustrated.

4.

a)

Document Section of the Corporations

Act

1. Statement of financial position as at the end of the year (if

consolidated accounts are not required by Accounting

Standards)

295(2) & 296(1)

2. Statement of cash flows for the year (if consolidated accounts

are not required by Accounting Standards)

295(2) & 296(1)

3. Statement of changes in equity if consolidated accounts are

not required by Accounting Standards)

295(2) & 296(1)

4. Notes to financial statements (disclosure required by the

regulations, notes required by the accounting standards, and

any other information necessary to give a true and fair view)

295(3)

5. Annual financial reports and half yearly financial reports 292

6. Prepared reports in accordance with chapter 2M and

corporations act.

302

7. Directors' declaration that the financial

statements comply with accounting standards,

give a true and fair view, there are reasonable

grounds to believe the company/scheme/entity

will be able to pay its debts, the financial

statements have been made in accordance with

the Corporations Act

295(4)

8. Directors' report, including the auditor's independence

declaration

298-300A

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9. Auditor’s report 301 and 308

b) GST reporting and payment cycle will be one of the following:

Monthly – if your GST turnover is $20 million or more.

Quarterly – if your GST turnover is less than $20 million – and we have not told you that you

must report monthly.

Annually – if you are voluntarily registered for GST. That is, you are registered for GST; and your

GST turnover is under $75,000 ($150,000 for not-for-profit bodies).

Depending on your circumstances, you can change the cycle you use to report and pay GST. This may

happen when your GST turnover changes or if you choose to report and pay using a different cycle.

c) You can elect to report and pay GST annually. You can only use this method if you are voluntarily

registered for GST. That is, you are registered for GST and your turnover is under $75,000 (or $150,000

for not-for-profit bodies).

If you are eligible and have elected to report and pay GST annually, you do not need to report or pay any

GST during the year. At the end of the financial year, you must report and pay any amount due.

If you are using the deferred GST scheme you need to withdraw from the scheme.

5.

(a) In accounting and finance, capital costs are the costs of the financial resources of a corporation or,

with an investor's perspective, the "necessary return on investment of stock shares of a portfolio

company." It is used to test a company's current initiatives.

The option of funding allows the capital expense of growing company a key aspect, since it defines the

capital structure of the organization. Firms attempt the optimal financing mix, which offers proper

resources and reduces capital cost. Capital costs are fixed, one-time expenses incurred on the purchase

of land, buildings, construction, and equipment used in the production of goods or in the rendering of

services. In other words, it is the total cost needed to bring a project to a commercially operable status.

(b) No, Investor A should not invest in the business because average rate of return is less than cost of

capital which will result in loss to him and it is clear that if cost is more than income; business cannot

survive in long run. Thus it is suggested that A should not choose this alternative for investment.

b) GST reporting and payment cycle will be one of the following:

Monthly – if your GST turnover is $20 million or more.

Quarterly – if your GST turnover is less than $20 million – and we have not told you that you

must report monthly.

Annually – if you are voluntarily registered for GST. That is, you are registered for GST; and your

GST turnover is under $75,000 ($150,000 for not-for-profit bodies).

Depending on your circumstances, you can change the cycle you use to report and pay GST. This may

happen when your GST turnover changes or if you choose to report and pay using a different cycle.

c) You can elect to report and pay GST annually. You can only use this method if you are voluntarily

registered for GST. That is, you are registered for GST and your turnover is under $75,000 (or $150,000

for not-for-profit bodies).

If you are eligible and have elected to report and pay GST annually, you do not need to report or pay any

GST during the year. At the end of the financial year, you must report and pay any amount due.

If you are using the deferred GST scheme you need to withdraw from the scheme.

5.

(a) In accounting and finance, capital costs are the costs of the financial resources of a corporation or,

with an investor's perspective, the "necessary return on investment of stock shares of a portfolio

company." It is used to test a company's current initiatives.

The option of funding allows the capital expense of growing company a key aspect, since it defines the

capital structure of the organization. Firms attempt the optimal financing mix, which offers proper

resources and reduces capital cost. Capital costs are fixed, one-time expenses incurred on the purchase

of land, buildings, construction, and equipment used in the production of goods or in the rendering of

services. In other words, it is the total cost needed to bring a project to a commercially operable status.

(b) No, Investor A should not invest in the business because average rate of return is less than cost of

capital which will result in loss to him and it is clear that if cost is more than income; business cannot

survive in long run. Thus it is suggested that A should not choose this alternative for investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(c) Working capital is a financial metric representing required to operate liquidity for a company, an

organization, or another entity, including government bodies. Working capital, also known as net

working capital (NWC), is the difference between an organization's current resources, such as cash,

credits (invoices not paid by customers) and investments of finished raw materials and goods and

current liabilities as for example, the responsibility of the creditor. Net working capital is a percentage of

an organization's liquidity and refers to the difference between current working resources and current

operating liabilities. These numbers are usually identical and come from the group's assets as well as

credits as well as deposits, fewer records to pay and fewer expenses collected. To figure the working

capital, contrast an organization's present resources with its present liabilities. Current resources

recorded on an organization's monetary record incorporate money, debt claims, stock and different

resources that are required to be exchanged or transformed into money in under one year. Current

liabilities incorporate records payable, compensation, charges payable, and the present segment of long

haul obligation. Current resources are accessible inside a year. Current liabilities are expected inside a

year.

Working capital is a percentage of liquidity, the effectiveness of an organization's operations and its

current financial wellbeing. If an organization has a good working capital, it should eventually contribute

and improve. If a group's current facilities do not exceed its current responsibilities, then it may be

difficult to develop or pay attention to loan masters, or even to fail.

The net value of the working capital is different. All the assets except the liability are measured by net

worth. Economic capital tests just the current savings, minus the remaining liabilities. Current debts

include short-term debts such as payable accounts, payroll and back debts.

6.

Activity Financing/Investment Decision

(a) Investment

(b) Financing

(c) Investment

(d) Investment

(e) Financing

(f) Investment

(g) Financing

7.

(a) Increasing income applies to increasing the firm's dollar sales. According to this objective, action

should be taken to boost profits and to prevent actions which reduce profit. As indicated by this

objective, the activities that expansion benefits ought to be attempted and those that decline benefits

are to be maintained a strategic distance from. The individuals who are supportive of benefit

augmentation contend that benefit is a trial of monetary effectiveness; it prompts successful use of

organization, or another entity, including government bodies. Working capital, also known as net

working capital (NWC), is the difference between an organization's current resources, such as cash,

credits (invoices not paid by customers) and investments of finished raw materials and goods and

current liabilities as for example, the responsibility of the creditor. Net working capital is a percentage of

an organization's liquidity and refers to the difference between current working resources and current

operating liabilities. These numbers are usually identical and come from the group's assets as well as

credits as well as deposits, fewer records to pay and fewer expenses collected. To figure the working

capital, contrast an organization's present resources with its present liabilities. Current resources

recorded on an organization's monetary record incorporate money, debt claims, stock and different

resources that are required to be exchanged or transformed into money in under one year. Current

liabilities incorporate records payable, compensation, charges payable, and the present segment of long

haul obligation. Current resources are accessible inside a year. Current liabilities are expected inside a

year.

Working capital is a percentage of liquidity, the effectiveness of an organization's operations and its

current financial wellbeing. If an organization has a good working capital, it should eventually contribute

and improve. If a group's current facilities do not exceed its current responsibilities, then it may be

difficult to develop or pay attention to loan masters, or even to fail.

The net value of the working capital is different. All the assets except the liability are measured by net

worth. Economic capital tests just the current savings, minus the remaining liabilities. Current debts

include short-term debts such as payable accounts, payroll and back debts.

6.

Activity Financing/Investment Decision

(a) Investment

(b) Financing

(c) Investment

(d) Investment

(e) Financing

(f) Investment

(g) Financing

7.

(a) Increasing income applies to increasing the firm's dollar sales. According to this objective, action

should be taken to boost profits and to prevent actions which reduce profit. As indicated by this

objective, the activities that expansion benefits ought to be attempted and those that decline benefits

are to be maintained a strategic distance from. The individuals who are supportive of benefit

augmentation contend that benefit is a trial of monetary effectiveness; it prompts successful use of

terrifying financial assets in each business firm, and it prompts all out financial government assistance

since it expands the financial proficiency of each individual firm. Subsequently, benefit amplification is

viewed as a fundamental rule for money related dynamic.

Simply giving offers and utilizing the returns in the Treasury bill can boost the measure of benefit. In any

case, this would bring about a reduction in income for every offer (EPS). This objective isn't evident

whether the budgetary chief should make such to move to augment the benefit.

(b) A maximum return to stockholders is and should be the goal of all corporate activities, according to

the SWM principle. To accomplish this aim, management evaluates the cost and pacing correlated with

the expected profit per share in order to increase the common stock price of the business.

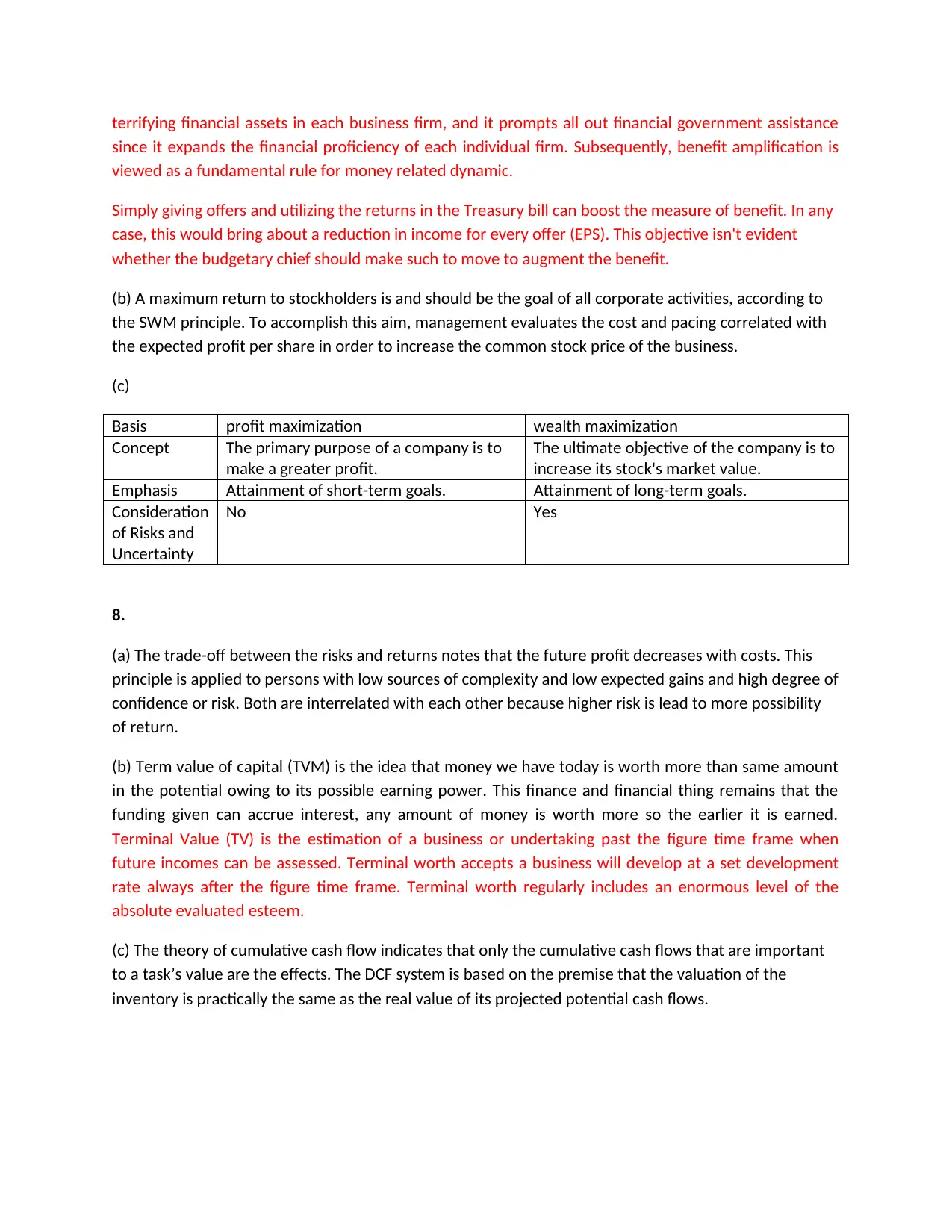

(c)

Basis profit maximization wealth maximization

Concept The primary purpose of a company is to

make a greater profit.

The ultimate objective of the company is to

increase its stock's market value.

Emphasis Attainment of short-term goals. Attainment of long-term goals.

Consideration

of Risks and

Uncertainty

No Yes

8.

(a) The trade-off between the risks and returns notes that the future profit decreases with costs. This

principle is applied to persons with low sources of complexity and low expected gains and high degree of

confidence or risk. Both are interrelated with each other because higher risk is lead to more possibility

of return.

(b) Term value of capital (TVM) is the idea that money we have today is worth more than same amount

in the potential owing to its possible earning power. This finance and financial thing remains that the

funding given can accrue interest, any amount of money is worth more so the earlier it is earned.

Terminal Value (TV) is the estimation of a business or undertaking past the figure time frame when

future incomes can be assessed. Terminal worth accepts a business will develop at a set development

rate always after the figure time frame. Terminal worth regularly includes an enormous level of the

absolute evaluated esteem.

(c) The theory of cumulative cash flow indicates that only the cumulative cash flows that are important

to a task’s value are the effects. The DCF system is based on the premise that the valuation of the

inventory is practically the same as the real value of its projected potential cash flows.

since it expands the financial proficiency of each individual firm. Subsequently, benefit amplification is

viewed as a fundamental rule for money related dynamic.

Simply giving offers and utilizing the returns in the Treasury bill can boost the measure of benefit. In any

case, this would bring about a reduction in income for every offer (EPS). This objective isn't evident

whether the budgetary chief should make such to move to augment the benefit.

(b) A maximum return to stockholders is and should be the goal of all corporate activities, according to

the SWM principle. To accomplish this aim, management evaluates the cost and pacing correlated with

the expected profit per share in order to increase the common stock price of the business.

(c)

Basis profit maximization wealth maximization

Concept The primary purpose of a company is to

make a greater profit.

The ultimate objective of the company is to

increase its stock's market value.

Emphasis Attainment of short-term goals. Attainment of long-term goals.

Consideration

of Risks and

Uncertainty

No Yes

8.

(a) The trade-off between the risks and returns notes that the future profit decreases with costs. This

principle is applied to persons with low sources of complexity and low expected gains and high degree of

confidence or risk. Both are interrelated with each other because higher risk is lead to more possibility

of return.

(b) Term value of capital (TVM) is the idea that money we have today is worth more than same amount

in the potential owing to its possible earning power. This finance and financial thing remains that the

funding given can accrue interest, any amount of money is worth more so the earlier it is earned.

Terminal Value (TV) is the estimation of a business or undertaking past the figure time frame when

future incomes can be assessed. Terminal worth accepts a business will develop at a set development

rate always after the figure time frame. Terminal worth regularly includes an enormous level of the

absolute evaluated esteem.

(c) The theory of cumulative cash flow indicates that only the cumulative cash flows that are important

to a task’s value are the effects. The DCF system is based on the premise that the valuation of the

inventory is practically the same as the real value of its projected potential cash flows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

PART A

Written Report

a) Capacity (coverage) of the Finance Policy and Procedure (FPP) Manual

Finance Authorization Policy: All currency exchanges identified in this procedure must be approved by

the authorized individual before accepting the exchange. This agreement must be combined with other

specific equity strategies where appropriate.

Bank Account Policy: This approach establishes the requirements for using financial amounts, including

opening, closing license, mixing in terms and conditions, damaging ledgers and exchanging books

accounts.

Petty Cash Policy: Small funds should be used to pay private business expenses of up to $ 100 where

listing contributions are not payable or Visa is not supported or equipped.

New Supplier Policy: All suppliers must review and identify a new company in accordance with this

approach to ensure that the supplier management is in line with the business goals.

b) Policy area gaps

The policies which are not covered in FPP are; management systems for information management and

Financial risk management which is very essential for any reporting system and FPP manual to cover

essential information of internal management.

c) Draft policy and procedures

Financial reporting responsibilities of Apex Learning Institute’s CEO as a director of the company:

Management systems for information management

Policy Number: 015

Policy Date: DD/MM/YYYY

Purpose of the policy

The purpose of the information management policy is to ensure that complete and detailed records of

all issues under consideration and that the Council's choices are made, maintained and maintained or

eliminated appropriately and subject to relevant promulgation. This will allow the Council to achieve

data performance, modernization and business development. It will also meet accountability

PART A

Written Report

a) Capacity (coverage) of the Finance Policy and Procedure (FPP) Manual

Finance Authorization Policy: All currency exchanges identified in this procedure must be approved by

the authorized individual before accepting the exchange. This agreement must be combined with other

specific equity strategies where appropriate.

Bank Account Policy: This approach establishes the requirements for using financial amounts, including

opening, closing license, mixing in terms and conditions, damaging ledgers and exchanging books

accounts.

Petty Cash Policy: Small funds should be used to pay private business expenses of up to $ 100 where

listing contributions are not payable or Visa is not supported or equipped.

New Supplier Policy: All suppliers must review and identify a new company in accordance with this

approach to ensure that the supplier management is in line with the business goals.

b) Policy area gaps

The policies which are not covered in FPP are; management systems for information management and

Financial risk management which is very essential for any reporting system and FPP manual to cover

essential information of internal management.

c) Draft policy and procedures

Financial reporting responsibilities of Apex Learning Institute’s CEO as a director of the company:

Management systems for information management

Policy Number: 015

Policy Date: DD/MM/YYYY

Purpose of the policy

The purpose of the information management policy is to ensure that complete and detailed records of

all issues under consideration and that the Council's choices are made, maintained and maintained or

eliminated appropriately and subject to relevant promulgation. This will allow the Council to achieve

data performance, modernization and business development. It will also meet accountability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

commitments, pledging to guarantee the rights and interests of the government, the company, its

employees, customers and the network.

Procedure

Staff must ensure that it officially records everything under consideration and the activities to be carried

out in their official activities. For example, if the activity is conducted over the phone, the notes of the

main points of the discussion must be described. Official meetings must include minutes. The board of

directors asks its employees to create and maintain records that report on their activities and

organization in a complete and detailed way, this includes:

All kinds of records made or received made or spoken

Email (email, internal and external)

Copy

Phone message

Customer requirements

Objections

d) Improved Budget Audit and Compliance procedures

The approach to determining spending plans across the board is a key threat to managers and the

administrative tool. Although the review found that management was proving effective in all

administrations, it was also considered to be a very soft mindset and deficiencies in control were found

that reduced operational capacity. These complexities are linked to the review of products identified

elsewhere, such as consumer understanding, responsibility and the DMT approach.

e) References

Herrmann, V., Christel, M.L., Christensen, T., Weber, K. and Williams, A., FINANCIAL POLICIES AND

PROCEDURES HANDBOOK.

Atashbar, T., Arani, A.A., Antoun, J. and Bossert, T., 2017. Health reform policy-making: Fiscal

sustainability matters (The case of Iran’s PresidentCare). Journal of Policy Modeling, 39(6), pp.1086-

1101.

"Accounting and financial policies and procedures | Business Victoria."

http://www.business.vic.gov.au/money-profit-and-accounting/financial-processes-and-procedures/

accounting-and-financial-policies-and-procedures. Accessed 13 Dec. 2018

employees, customers and the network.

Procedure

Staff must ensure that it officially records everything under consideration and the activities to be carried

out in their official activities. For example, if the activity is conducted over the phone, the notes of the

main points of the discussion must be described. Official meetings must include minutes. The board of

directors asks its employees to create and maintain records that report on their activities and

organization in a complete and detailed way, this includes:

All kinds of records made or received made or spoken

Email (email, internal and external)

Copy

Phone message

Customer requirements

Objections

d) Improved Budget Audit and Compliance procedures

The approach to determining spending plans across the board is a key threat to managers and the

administrative tool. Although the review found that management was proving effective in all

administrations, it was also considered to be a very soft mindset and deficiencies in control were found

that reduced operational capacity. These complexities are linked to the review of products identified

elsewhere, such as consumer understanding, responsibility and the DMT approach.

e) References

Herrmann, V., Christel, M.L., Christensen, T., Weber, K. and Williams, A., FINANCIAL POLICIES AND

PROCEDURES HANDBOOK.

Atashbar, T., Arani, A.A., Antoun, J. and Bossert, T., 2017. Health reform policy-making: Fiscal

sustainability matters (The case of Iran’s PresidentCare). Journal of Policy Modeling, 39(6), pp.1086-

1101.

"Accounting and financial policies and procedures | Business Victoria."

http://www.business.vic.gov.au/money-profit-and-accounting/financial-processes-and-procedures/

accounting-and-financial-policies-and-procedures. Accessed 13 Dec. 2018

PART B

1. Purpose and agenda of meeting

To fill the gap of policies on financial risk management and management systems for information

management in the context of financial reporting responsibilities of Apex Learning Institute’s CEO as a

director of the company. Also present the feedback on improvement suggestions in Budget Audit and

Compliance procedures. The difference between collections with and without plans can lead to

confusion, causing a little confusion than few results. A plan tells participants that the collection will be

managed in detail and the goal is profit. Organizations gather to finalize things, share data, create plans,

report on progress, provide clarity and make a decision. A plan can guarantee that the collection will

remain in line with the goal and that unusual work and routine activities will follow as recommended. A

plan can help a group of employees to work as a work organization.

2. Policy area gaps

There are two policy gaps in FPP manual that are Risk management and management systems for

information management both are important aspects from financial management point of view and

required to assess the risk within organization and collecting information on which system and function

required to be integrated with information management system.

3. Policies and procedures suggested to CEO

Explanation of representation and consistency should be provided by each honoree / commander / fire

chief as a formal declaration of their obligation to comply with leg management provisions and

strategies. To describe their situation, all employees should be reminded of the board of directors' risk-

related responsibility and the annual performance assessments should include an appropriate

assessment of the same. .

First, risk at a company level should be monitored as a feature of the relevant USQ administrative and

corporate formats. This approach, carried out and encouraged by a Vice-Chancellor (VCE), will entail

leading progress:

Any operational location including risk management assessment for all businesses;

The unification of the risks to the board of directors in the essential institutional and executive

and patrimonial organization of the managers organizing the forms;

An annual audit of the risk posed by managers by the Control and Risk Committee.

1. Purpose and agenda of meeting

To fill the gap of policies on financial risk management and management systems for information

management in the context of financial reporting responsibilities of Apex Learning Institute’s CEO as a

director of the company. Also present the feedback on improvement suggestions in Budget Audit and

Compliance procedures. The difference between collections with and without plans can lead to

confusion, causing a little confusion than few results. A plan tells participants that the collection will be

managed in detail and the goal is profit. Organizations gather to finalize things, share data, create plans,

report on progress, provide clarity and make a decision. A plan can guarantee that the collection will

remain in line with the goal and that unusual work and routine activities will follow as recommended. A

plan can help a group of employees to work as a work organization.

2. Policy area gaps

There are two policy gaps in FPP manual that are Risk management and management systems for

information management both are important aspects from financial management point of view and

required to assess the risk within organization and collecting information on which system and function

required to be integrated with information management system.

3. Policies and procedures suggested to CEO

Explanation of representation and consistency should be provided by each honoree / commander / fire

chief as a formal declaration of their obligation to comply with leg management provisions and

strategies. To describe their situation, all employees should be reminded of the board of directors' risk-

related responsibility and the annual performance assessments should include an appropriate

assessment of the same. .

First, risk at a company level should be monitored as a feature of the relevant USQ administrative and

corporate formats. This approach, carried out and encouraged by a Vice-Chancellor (VCE), will entail

leading progress:

Any operational location including risk management assessment for all businesses;

The unification of the risks to the board of directors in the essential institutional and executive

and patrimonial organization of the managers organizing the forms;

An annual audit of the risk posed by managers by the Control and Risk Committee.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.