Financial Resources Management: Radisson Plc Financial Planning

VerifiedAdded on 2023/04/10

|17

|4119

|256

Report

AI Summary

This report provides a comprehensive analysis of financial resource management within the context of Radisson Plc. It identifies various sources of finance, evaluates their implications, and analyzes the cost of funding. The importance of financial planning is highlighted, along with an assessment of information needs for financial decision-making. The report also examines the impact of financing options on financial statements and discusses the significance of budgeting for variation. Furthermore, it covers unit cost calculation, pricing decisions, investment appraisal techniques, and compares the formats of financial statements for public and private limited companies, concluding with an interpretation of Radisson Plc's financial performance.

FINANCIAL RESOURCES

MANAGEMENT.

MANAGEMENT.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Identification of source of finance....................................................................................3

1.2 Implications of different sources of finance.....................................................................4

1.3 Evaluation.........................................................................................................................4

TASK 2............................................................................................................................................5

2.1Analyse the cost of funding...............................................................................................5

2.2.The importance of financial planning...............................................................................6

2.3 assessment of the information needs for financial decision making...............................6

2.4 the impact of suggested financing option on the financial statement...............................7

TASK3.............................................................................................................................................7

3.1 The importance of budgets for variation..........................................................................7

3.2 Calculation of unit cost and pricing decisions..................................................................8

3.3 Assessment of investment appraisal techniques...............................................................9

TASK4...........................................................................................................................................10

4.1Income Statements, Statement of Cash Flows and the Statement of Financial Position.10

4.2 Comparing the formats of financial statements..............................................................12

4.3 Interpreting the financial statements of a public limited company and a private limited

company...............................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCE.................................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Identification of source of finance....................................................................................3

1.2 Implications of different sources of finance.....................................................................4

1.3 Evaluation.........................................................................................................................4

TASK 2............................................................................................................................................5

2.1Analyse the cost of funding...............................................................................................5

2.2.The importance of financial planning...............................................................................6

2.3 assessment of the information needs for financial decision making...............................6

2.4 the impact of suggested financing option on the financial statement...............................7

TASK3.............................................................................................................................................7

3.1 The importance of budgets for variation..........................................................................7

3.2 Calculation of unit cost and pricing decisions..................................................................8

3.3 Assessment of investment appraisal techniques...............................................................9

TASK4...........................................................................................................................................10

4.1Income Statements, Statement of Cash Flows and the Statement of Financial Position.10

4.2 Comparing the formats of financial statements..............................................................12

4.3 Interpreting the financial statements of a public limited company and a private limited

company...............................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCE.................................................................................................................................16

INTRODUCTION

Financial resource management is highly concerned with making effective and optimum use of

money. The rationale behind this, in business monetary resources is one of the main factors that

have high level of impact on the effectual execution of plan. In this, financial tools and

techniques have high level of significance which in turn helps in making control on

overspending. Hence, technique of budgeting control provides deeper insight about the

performance level of each department. Moreover, by making comparison of the actual

performance with the standard aspects business unit can assess the deviations take place in the

financial aspects (Broadbent, Cullen, 2012). In this way, by taking corrective measure business

unit can make profit.

TASK 1

1.1 Identification of source of finance.

Financing and raising of funds is crucial to start a business and elevate it as a profit

earning entity. There are numerous sources to be taken into consideration while raising funds.

Radisson Plc. can consider for sources and categories them into two main categories: Debt

Financing and Equity Financing. Before that Radisson Plc (Chandra, 2008). need to consider

how much money it will need and when they will need it. The financial needs of a business will

vary according to the type and size. The best alternatives for Radisson Plc are:

Equity Financing:

Personal savings: Personal resources include cash in hand, personal bank balances, private

properties/real estate etc. which is being maintained by the owner or Radisson Plc for its further

establishment. The first option for financing is owner's or Radisson Plc's savings or equity.

Profit earned/Retained Earnings. – Profit earned during the normal course of a business is the

second option i.e., by reinvesting this amount for expansion of Radisson Plc.

Venture Capital: Financing from individuals or companies, investing in young and private

businesses in exchange for an ownership share of the business. Venture capital firms usually

participate in the businesses that have a competitive edge or a strong financial worth (Khan,

2008).

Financial resource management is highly concerned with making effective and optimum use of

money. The rationale behind this, in business monetary resources is one of the main factors that

have high level of impact on the effectual execution of plan. In this, financial tools and

techniques have high level of significance which in turn helps in making control on

overspending. Hence, technique of budgeting control provides deeper insight about the

performance level of each department. Moreover, by making comparison of the actual

performance with the standard aspects business unit can assess the deviations take place in the

financial aspects (Broadbent, Cullen, 2012). In this way, by taking corrective measure business

unit can make profit.

TASK 1

1.1 Identification of source of finance.

Financing and raising of funds is crucial to start a business and elevate it as a profit

earning entity. There are numerous sources to be taken into consideration while raising funds.

Radisson Plc. can consider for sources and categories them into two main categories: Debt

Financing and Equity Financing. Before that Radisson Plc (Chandra, 2008). need to consider

how much money it will need and when they will need it. The financial needs of a business will

vary according to the type and size. The best alternatives for Radisson Plc are:

Equity Financing:

Personal savings: Personal resources include cash in hand, personal bank balances, private

properties/real estate etc. which is being maintained by the owner or Radisson Plc for its further

establishment. The first option for financing is owner's or Radisson Plc's savings or equity.

Profit earned/Retained Earnings. – Profit earned during the normal course of a business is the

second option i.e., by reinvesting this amount for expansion of Radisson Plc.

Venture Capital: Financing from individuals or companies, investing in young and private

businesses in exchange for an ownership share of the business. Venture capital firms usually

participate in the businesses that have a competitive edge or a strong financial worth (Khan,

2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Angel Investors: Individual professionals and businesses who are interested in helping small

businesses to survive and grow gradually. Entrepreneurial skills and own funds of these business

angel are devoted into business of RadissonPlc. So, the objective is more than just focusing on

fiscal returns, and can be called as an informal venture capital.

Share capital (Equity Offerings) – Radisson Plc sells stock(shares) directly to the public which

have a nominal/face value on which shareholders claims dividend after a given period or at times

of extra profit.

Debt Financing:

Banks loans and Other Commercial Lenders: Most lenders require a solid business plan, positive

track record, and plenty of collateral. Funds lend by Radisson Plc, provided in exchange of

security can be on small, medium and long-term basis and the bank will fix the time sets and

rate of interest (Petty, 2015).

Bank O/D: A short term loan facility when bank balance of Radisson Plc becomes zero or below

the bank allows withdrawal of an agreed amount limit on which interest is charged.

1.2 Implications of different sources of finance

Four factors determines how Radisson Plc gets financial support: its fiscal potential, the

maturity, the types of assets held by Radisson Plc and the preferences of the owner(s) between

debt and equity. And there are three privileges which deliver the choice between debt financing

and equity financing: Radisson Plc's budding profitability, financial risks, and voting power.

Bank Loans (debt) rather than issuing shares (owner’s equity) increases the probability of higher

rates of return to the owners. But debt finance exposes the owners to greater financial risk. On

the other hand, if Radisson Plc issues stock rather than bank loans/bank overdrafts, it reduces the

potential rates of return and entreats them to give up some voting control in order to reduce risk

(Whittington, Delaney, 2011).

1.3 Evaluation.

It requires the awareness of financial sources to match the finance which Radisson Plc

will need:

Establishing the company – financial investors like venture/angel investors are the best

choice.

businesses to survive and grow gradually. Entrepreneurial skills and own funds of these business

angel are devoted into business of RadissonPlc. So, the objective is more than just focusing on

fiscal returns, and can be called as an informal venture capital.

Share capital (Equity Offerings) – Radisson Plc sells stock(shares) directly to the public which

have a nominal/face value on which shareholders claims dividend after a given period or at times

of extra profit.

Debt Financing:

Banks loans and Other Commercial Lenders: Most lenders require a solid business plan, positive

track record, and plenty of collateral. Funds lend by Radisson Plc, provided in exchange of

security can be on small, medium and long-term basis and the bank will fix the time sets and

rate of interest (Petty, 2015).

Bank O/D: A short term loan facility when bank balance of Radisson Plc becomes zero or below

the bank allows withdrawal of an agreed amount limit on which interest is charged.

1.2 Implications of different sources of finance

Four factors determines how Radisson Plc gets financial support: its fiscal potential, the

maturity, the types of assets held by Radisson Plc and the preferences of the owner(s) between

debt and equity. And there are three privileges which deliver the choice between debt financing

and equity financing: Radisson Plc's budding profitability, financial risks, and voting power.

Bank Loans (debt) rather than issuing shares (owner’s equity) increases the probability of higher

rates of return to the owners. But debt finance exposes the owners to greater financial risk. On

the other hand, if Radisson Plc issues stock rather than bank loans/bank overdrafts, it reduces the

potential rates of return and entreats them to give up some voting control in order to reduce risk

(Whittington, Delaney, 2011).

1.3 Evaluation.

It requires the awareness of financial sources to match the finance which Radisson Plc

will need:

Establishing the company – financial investors like venture/angel investors are the best

choice.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working capital - overdraft facility from banks.

To acquire property - long-term loan is to be considered.

To purchase equipment and vehicles – personal savings and/or fixed-term loans.

Operations of business - retained earnings can be reinvested and rolled out.

Raising capital – by issuing further shares Radisson Plc can raise funds.

By understanding the exact requirements Radisson Plc can make decisions accordingly and

achieve its short term and long term objectives. However, after choosing the most appropriate

financing source, it is also important to select the most suitable financier, or investor respectively

(Blombäck, Brunninge, 2013).

TASK 2

2.1Analyse the cost of funding.

Equity financing means investment by the owner(s), it offers an advantage to Radisson

Plc of not having to be repay the amount and interest. Whereas debt finance is the financing that

Radisson Plc has borrowed and must repay with interest. It does not require Radisson Plc to give

up ownership in their companies (Berrone, ,et.al., 2010).

Cost of funding from equity financing

Personal savings: The cost is determined from compensation made by Radisson Plc in exchange

for investing and bearing the risk of ownership. This cost is unavoidable.

Profit earned/Retained Earnings. – The cost involved is bearing of loss if any, the reinvested

money will be in vain if not properly utilized.

Venture Capital: Cost involved is in the capital share and the ownership. The cost involved is

lesser than personal savings or the profit earned as they can be reserved or put in working capital.

Angel Investors: The cost involved in raising fund from business angels are comparatively lesser

than venture capital by giving very less shares the company can earn more from these

professionals (Brunninge, 2009).

Share capital (Equity Offerings) – Cost is very much higher since it involves bank dividends to

be paid and the cost involved during raising them.

Cost of funding from debt financing

To acquire property - long-term loan is to be considered.

To purchase equipment and vehicles – personal savings and/or fixed-term loans.

Operations of business - retained earnings can be reinvested and rolled out.

Raising capital – by issuing further shares Radisson Plc can raise funds.

By understanding the exact requirements Radisson Plc can make decisions accordingly and

achieve its short term and long term objectives. However, after choosing the most appropriate

financing source, it is also important to select the most suitable financier, or investor respectively

(Blombäck, Brunninge, 2013).

TASK 2

2.1Analyse the cost of funding.

Equity financing means investment by the owner(s), it offers an advantage to Radisson

Plc of not having to be repay the amount and interest. Whereas debt finance is the financing that

Radisson Plc has borrowed and must repay with interest. It does not require Radisson Plc to give

up ownership in their companies (Berrone, ,et.al., 2010).

Cost of funding from equity financing

Personal savings: The cost is determined from compensation made by Radisson Plc in exchange

for investing and bearing the risk of ownership. This cost is unavoidable.

Profit earned/Retained Earnings. – The cost involved is bearing of loss if any, the reinvested

money will be in vain if not properly utilized.

Venture Capital: Cost involved is in the capital share and the ownership. The cost involved is

lesser than personal savings or the profit earned as they can be reserved or put in working capital.

Angel Investors: The cost involved in raising fund from business angels are comparatively lesser

than venture capital by giving very less shares the company can earn more from these

professionals (Brunninge, 2009).

Share capital (Equity Offerings) – Cost is very much higher since it involves bank dividends to

be paid and the cost involved during raising them.

Cost of funding from debt financing

Banks loans and Other Commercial Lenders: Cost involved is higher than equity finance since

they involve repaying the principal amount with interest, and the interest will be an expense for

Radisson Plc.

Bank O/D: Interest is charged with the amount withdrawn by Radisson Plc, the cost involved is

lesser than a bank loan, still it is an expense and add up the cost for the company.

The best option for the Radisson Plc. is choosing angel investors and equity share capital

since the cost involved is lesser as compared to debt financing, though the company can go along

with bank overdraft for maintaining its working capital.

2.2.The importance of financial planning.

Financial planning can be defined as the framing up of goals and objectives with the

policies and procedures of the company and budgeting required for the financial activities of

Radisson Plc (De Tienne, Chirico, 2013). Financial planning will ensure an effective and

adequate fund flow management. Some of the importance of financial planning are:

Adequate funds are to be assured.

Ensures an authorised outflow and inflow of funds for maintaining stability in financial

structure of Radisson Plc.

Financial planning results in expansion programmes focused in long-run survival of

Radisson Plc.

Reduces uncertainties regarding changes in market trends by tackling with enough funds.

Financial planning also ensures profitability and the potentials of Radisson Plc. To

increase the same.

2.3 assessment of the information needs for financial decision making.

In financial decision making process Radisson Plc requires both financial and non-

financial informations. The significant financial information needed for decision making comes

from accounting in the form of financial statements (Eddleston, Kellermanns, Sarathy, 2008).

The most significant financial statements that we consider while exploring the attributes of

business as a whole and make decisions for the future are the final four statements which are

income statement or profit and loss account, balance sheet, cash flow statement and changes in

owner’s equity (Gomez-Mejia, Imperatore, 2014).

Importance of financial information are:

they involve repaying the principal amount with interest, and the interest will be an expense for

Radisson Plc.

Bank O/D: Interest is charged with the amount withdrawn by Radisson Plc, the cost involved is

lesser than a bank loan, still it is an expense and add up the cost for the company.

The best option for the Radisson Plc. is choosing angel investors and equity share capital

since the cost involved is lesser as compared to debt financing, though the company can go along

with bank overdraft for maintaining its working capital.

2.2.The importance of financial planning.

Financial planning can be defined as the framing up of goals and objectives with the

policies and procedures of the company and budgeting required for the financial activities of

Radisson Plc (De Tienne, Chirico, 2013). Financial planning will ensure an effective and

adequate fund flow management. Some of the importance of financial planning are:

Adequate funds are to be assured.

Ensures an authorised outflow and inflow of funds for maintaining stability in financial

structure of Radisson Plc.

Financial planning results in expansion programmes focused in long-run survival of

Radisson Plc.

Reduces uncertainties regarding changes in market trends by tackling with enough funds.

Financial planning also ensures profitability and the potentials of Radisson Plc. To

increase the same.

2.3 assessment of the information needs for financial decision making.

In financial decision making process Radisson Plc requires both financial and non-

financial informations. The significant financial information needed for decision making comes

from accounting in the form of financial statements (Eddleston, Kellermanns, Sarathy, 2008).

The most significant financial statements that we consider while exploring the attributes of

business as a whole and make decisions for the future are the final four statements which are

income statement or profit and loss account, balance sheet, cash flow statement and changes in

owner’s equity (Gomez-Mejia, Imperatore, 2014).

Importance of financial information are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

assessment of financial position of Radisson Plc, and can be used to comparing with the

competitors.

evaluates the preservation of resources within Radisson Plc.

analyse the efficiency and effectiveness of operations and resources, specially the human

resource.ok

The compliance of regular operations are determined with the directives mentioned by

Radisson Plc.

2.4 the impact of suggested financing option on the financial statement.

When angel investors, venture investors and are considered the liability of Radisson Plc

increases along with cash i.e., with the introduction of additional capital in the form of cash/bank

into the business. The profit earned will be divided in the form of dividends and be shared to the

respective investors and shareholders according to agreed ratios. Profit and loss account will be

credited against capital accounts of the investors and shareholders.

When overdrafts are allowed by the bank for increasing the working capital of Radisson Plc and

the bank balance of the company will show credit balance for a short period after which the bank

account will be debited with interest and the interest charged is debited to profit and loss

account. When long term loans are taken the liabilities will increase and an equal asset will be

formed in the form of a fixed asset or cash or bank. The interest paid will be charged against the

same and debited to the profit and loss account. And when the retained profits of Radisson Plc

are rolled back for further operations profit and loss account gets credited and equivalent cash or

fixed assets will be increased in the balance sheet.

TASK3

3.1 The importance of budgets for variation.

Budgeting is done to provide foundation with which the actual performance of Radisson

Plc. is compared and measured. This process comes under the management accounting

(Jaskiewicz, Combs, Rau, 2014). There is no point in making budget and finding out the

variation and no action is taken on the basis of these management accounts and there is no point

in making them thus resulting in wasting management time discussing them. Four reasons are

there reasons and it is much important that the managers of Radisson Plc recognise the

competitors.

evaluates the preservation of resources within Radisson Plc.

analyse the efficiency and effectiveness of operations and resources, specially the human

resource.ok

The compliance of regular operations are determined with the directives mentioned by

Radisson Plc.

2.4 the impact of suggested financing option on the financial statement.

When angel investors, venture investors and are considered the liability of Radisson Plc

increases along with cash i.e., with the introduction of additional capital in the form of cash/bank

into the business. The profit earned will be divided in the form of dividends and be shared to the

respective investors and shareholders according to agreed ratios. Profit and loss account will be

credited against capital accounts of the investors and shareholders.

When overdrafts are allowed by the bank for increasing the working capital of Radisson Plc and

the bank balance of the company will show credit balance for a short period after which the bank

account will be debited with interest and the interest charged is debited to profit and loss

account. When long term loans are taken the liabilities will increase and an equal asset will be

formed in the form of a fixed asset or cash or bank. The interest paid will be charged against the

same and debited to the profit and loss account. And when the retained profits of Radisson Plc

are rolled back for further operations profit and loss account gets credited and equivalent cash or

fixed assets will be increased in the balance sheet.

TASK3

3.1 The importance of budgets for variation.

Budgeting is done to provide foundation with which the actual performance of Radisson

Plc. is compared and measured. This process comes under the management accounting

(Jaskiewicz, Combs, Rau, 2014). There is no point in making budget and finding out the

variation and no action is taken on the basis of these management accounts and there is no point

in making them thus resulting in wasting management time discussing them. Four reasons are

there reasons and it is much important that the managers of Radisson Plc recognise the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

differences among these reasons, hence the action needed might be completely different in each

case. They are:

The whole facts might be wrong

Arithmetic errors in the budgeted figures.

Differences in the budget assumptions and actual outcome.

Faults made in the the actual results (arithmetically).

Radisson Plc can make appropriate decisions by taking following steps:

1. Identifying the root causes of variations.

2. Bending the budget i.e., making it more flexible.

3. Analyse the variations.

4. Taking appropriate and immediate action.

The first three steps are interrelated, also directly related to step four and is to be taken in time to

help future results of Radisson Plc. This means that the first three steps should be done even

though it reduces accuracy.

3.2 Calculation of unit cost and pricing decisions.

Unit cost calculation

Suppose Radisson Plc commonly manufactures similar product/software in batches of

hundreds or thousands of units per batch. Then,

Unit cost = the total cost of a production /the number of units produced.

By using the data given , calculate the cost of one unit.

Average variable cost = £3/unit.

Fixed cost = £10000.

Number of units produced = 1000.

Solution

Average variable cost = £3/unit.

Fixed cost = £10000 p.a.

Total variable cost = AVC* No: of units produced = 3*1000=£3000.

Total Cost per month = FC + TVC = £10000+£3000 = £13000.

Unit Cost = 13000/1000= £13.

Pricing decisions.

case. They are:

The whole facts might be wrong

Arithmetic errors in the budgeted figures.

Differences in the budget assumptions and actual outcome.

Faults made in the the actual results (arithmetically).

Radisson Plc can make appropriate decisions by taking following steps:

1. Identifying the root causes of variations.

2. Bending the budget i.e., making it more flexible.

3. Analyse the variations.

4. Taking appropriate and immediate action.

The first three steps are interrelated, also directly related to step four and is to be taken in time to

help future results of Radisson Plc. This means that the first three steps should be done even

though it reduces accuracy.

3.2 Calculation of unit cost and pricing decisions.

Unit cost calculation

Suppose Radisson Plc commonly manufactures similar product/software in batches of

hundreds or thousands of units per batch. Then,

Unit cost = the total cost of a production /the number of units produced.

By using the data given , calculate the cost of one unit.

Average variable cost = £3/unit.

Fixed cost = £10000.

Number of units produced = 1000.

Solution

Average variable cost = £3/unit.

Fixed cost = £10000 p.a.

Total variable cost = AVC* No: of units produced = 3*1000=£3000.

Total Cost per month = FC + TVC = £10000+£3000 = £13000.

Unit Cost = 13000/1000= £13.

Pricing decisions.

Radisson Plc is concerned at what cost it will be able to offer the product or service for

sale. But the cost is not the only factor to be considered while pricing. By considering Cost-plus

pricing method we can find out the price (Fizz, 2011).

Cost-plus pricing is a method in which SP of a product is determined by adding a profit margin

to the cost per unit of the product.

SP = Price = cost per unit × (1 + profit margin).

Where,

Cost per unit = actual direct materials+actual direct labour+actual variable manufacturing

overheads+allocated fixed manufacturing overheads.

Calculation of unit cost

Assume, Radisson Plc has designed a software that contains the following costs:

Direct material costs = £20

Direct labor costs = £5.50

Allocated overhead = £8.25

The company applies a standard 30% markup(profit margin) to all of its products. Calculate the

selling price.

Solution

Total cost per unit = £20+£5.50+£8.25 = £33.75

Selling Price = £33.75 * (1+30%) = £43.875

The Radisson Plc is making an profit as per the margin/markup percentage i.e., of £10.125.

3.3 Assessment of investment appraisal techniques.

Investment appraisal can be defined as a compilation of methods to be used for

identifying the attractiveness towards an investment. The simplest technique among all is the

payback method, it is the time taken for net cash inflow to equal the cash invested. It is normally

a rough evaluation and is often used as a basic screening process (Knauer, Wöhrmann, 2013).

Payback Period =Initial Investment ÷ Annual Cash Flow.

Net Present Value (NPV) or Internal Rate of Return (IRR)are the two main discounted

cash flow techniques, which best fits to evaluate the value of benefits and substitute the ways of

delivering them. NPV calculates the present value of cash flows related with an investment

(higher NPV is ideal). In calculation,we use a discount rate in order to show how value of money

sale. But the cost is not the only factor to be considered while pricing. By considering Cost-plus

pricing method we can find out the price (Fizz, 2011).

Cost-plus pricing is a method in which SP of a product is determined by adding a profit margin

to the cost per unit of the product.

SP = Price = cost per unit × (1 + profit margin).

Where,

Cost per unit = actual direct materials+actual direct labour+actual variable manufacturing

overheads+allocated fixed manufacturing overheads.

Calculation of unit cost

Assume, Radisson Plc has designed a software that contains the following costs:

Direct material costs = £20

Direct labor costs = £5.50

Allocated overhead = £8.25

The company applies a standard 30% markup(profit margin) to all of its products. Calculate the

selling price.

Solution

Total cost per unit = £20+£5.50+£8.25 = £33.75

Selling Price = £33.75 * (1+30%) = £43.875

The Radisson Plc is making an profit as per the margin/markup percentage i.e., of £10.125.

3.3 Assessment of investment appraisal techniques.

Investment appraisal can be defined as a compilation of methods to be used for

identifying the attractiveness towards an investment. The simplest technique among all is the

payback method, it is the time taken for net cash inflow to equal the cash invested. It is normally

a rough evaluation and is often used as a basic screening process (Knauer, Wöhrmann, 2013).

Payback Period =Initial Investment ÷ Annual Cash Flow.

Net Present Value (NPV) or Internal Rate of Return (IRR)are the two main discounted

cash flow techniques, which best fits to evaluate the value of benefits and substitute the ways of

delivering them. NPV calculates the present value of cash flows related with an investment

(higher NPV is ideal). In calculation,we use a discount rate in order to show how value of money

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gets decreased with time (Marttonen, Monto, Kärri, 2013). When the discount rate(interest rate)

gives an investment a NPV of zero, then the value is called the Internal Rate of Return (IRR).

Calculation based on payback method.

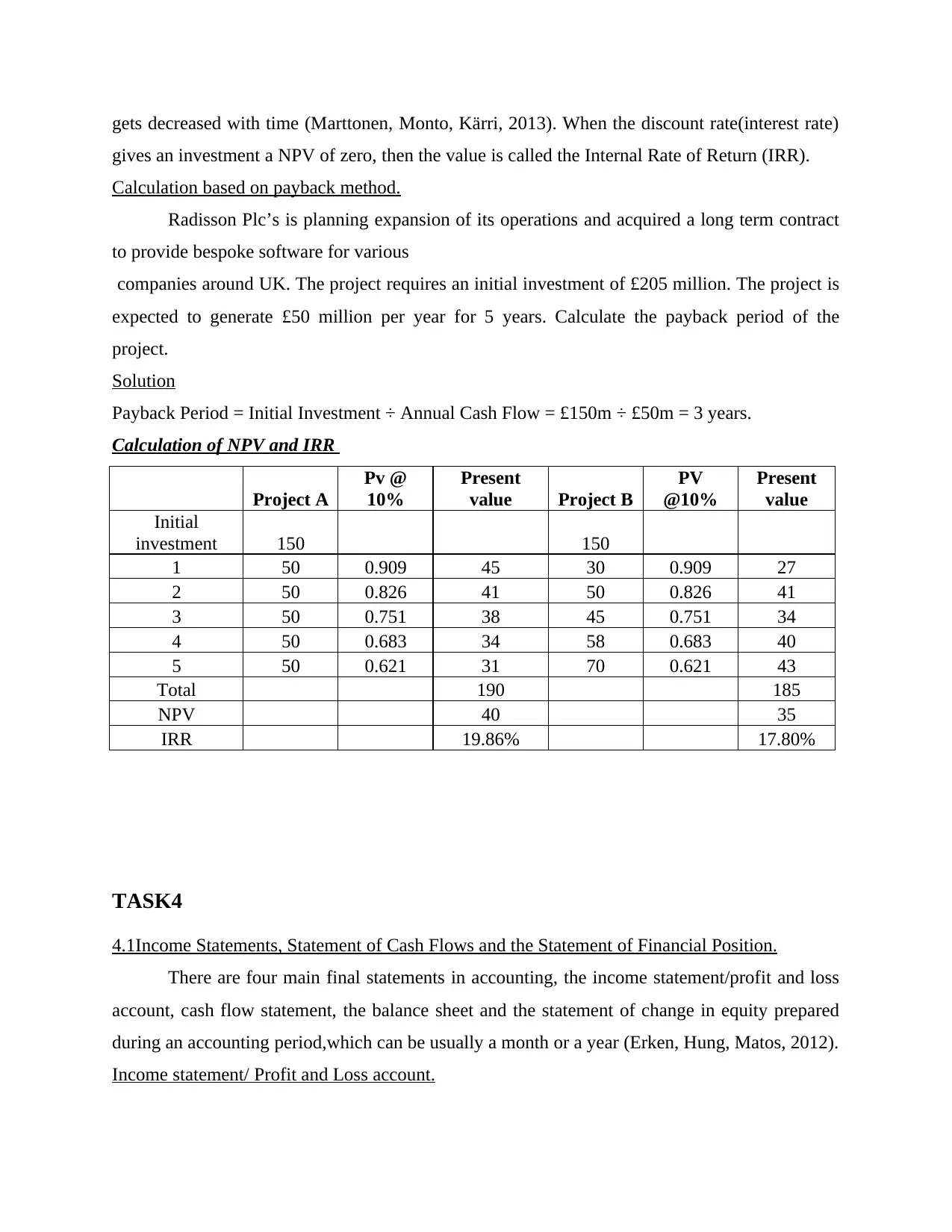

Radisson Plc’s is planning expansion of its operations and acquired a long term contract

to provide bespoke software for various

companies around UK. The project requires an initial investment of £205 million. The project is

expected to generate £50 million per year for 5 years. Calculate the payback period of the

project.

Solution

Payback Period = Initial Investment ÷ Annual Cash Flow = £150m ÷ £50m = 3 years.

Calculation of NPV and IRR

Project A

Pv @

10%

Present

value Project B

PV

@10%

Present

value

Initial

investment 150 150

1 50 0.909 45 30 0.909 27

2 50 0.826 41 50 0.826 41

3 50 0.751 38 45 0.751 34

4 50 0.683 34 58 0.683 40

5 50 0.621 31 70 0.621 43

Total 190 185

NPV 40 35

IRR 19.86% 17.80%

TASK4

4.1Income Statements, Statement of Cash Flows and the Statement of Financial Position.

There are four main final statements in accounting, the income statement/profit and loss

account, cash flow statement, the balance sheet and the statement of change in equity prepared

during an accounting period,which can be usually a month or a year (Erken, Hung, Matos, 2012).

Income statement/ Profit and Loss account.

gives an investment a NPV of zero, then the value is called the Internal Rate of Return (IRR).

Calculation based on payback method.

Radisson Plc’s is planning expansion of its operations and acquired a long term contract

to provide bespoke software for various

companies around UK. The project requires an initial investment of £205 million. The project is

expected to generate £50 million per year for 5 years. Calculate the payback period of the

project.

Solution

Payback Period = Initial Investment ÷ Annual Cash Flow = £150m ÷ £50m = 3 years.

Calculation of NPV and IRR

Project A

Pv @

10%

Present

value Project B

PV

@10%

Present

value

Initial

investment 150 150

1 50 0.909 45 30 0.909 27

2 50 0.826 41 50 0.826 41

3 50 0.751 38 45 0.751 34

4 50 0.683 34 58 0.683 40

5 50 0.621 31 70 0.621 43

Total 190 185

NPV 40 35

IRR 19.86% 17.80%

TASK4

4.1Income Statements, Statement of Cash Flows and the Statement of Financial Position.

There are four main final statements in accounting, the income statement/profit and loss

account, cash flow statement, the balance sheet and the statement of change in equity prepared

during an accounting period,which can be usually a month or a year (Erken, Hung, Matos, 2012).

Income statement/ Profit and Loss account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The income statement for Radisson Plc is prepared to analyse the financial performance

(profit making ability) of a business over an accounting period. Sometimes, this is also known as

statement of operations, income and expense statement or a profit and loss account statement.

The basic equation of an income statement is:

Revenues– Expenses = Net Income/Loss.

Where,

Income: What the business has earned over a period from operations e.g. sales revenue, dividend

income, etc

Expense: The cost incurred by the business over a period on operations e.g. wages and salaries,

rental charges, depreciation, etc

NB: When Profit and Loss account is prepared indirect expenses and indirect incomes are taken

to compute net profit/loss.

Cash flow statement.

The statement represents the movement/flow in cash (including bank balances) over a

time period (Fosu, 2013).

The cash flows is classified into the following three categories:

1. Operating Activities: the cash flow from primary activities of a business.

2. Investing Activities: the cash flow from purchase and sale of assets excluding inventories

(e.g. purchase of a building)

3. Financing Activities: the cash flow originated from or spent on raising or repaying share

capital and debentures altogether with the payments of interest and dividends.

The main purpose of cash flow statement is that it provides crucial insights on the liquidity as

well as the solvency of Radisson Plc, which is very vital for its growth and survival. The

statements is used by investors and analysts inside and outside Radisson Plc for

formation/projection of future cash flows (Julian, Ofori-Dankwa, 2013).

Balance sheet/ Statement of Financial Position.

A balance sheet is a depiction of the financial position of a business on a given date,

usually prepared at the end of a quarter or year. It is a summary of assets, liabilities, and owners'

capital. Another name for the balance sheet is the statement of financial position. The balance

sheet is divided into two parts Assets and Liabilities. The basic equation of balance sheet is:

(profit making ability) of a business over an accounting period. Sometimes, this is also known as

statement of operations, income and expense statement or a profit and loss account statement.

The basic equation of an income statement is:

Revenues– Expenses = Net Income/Loss.

Where,

Income: What the business has earned over a period from operations e.g. sales revenue, dividend

income, etc

Expense: The cost incurred by the business over a period on operations e.g. wages and salaries,

rental charges, depreciation, etc

NB: When Profit and Loss account is prepared indirect expenses and indirect incomes are taken

to compute net profit/loss.

Cash flow statement.

The statement represents the movement/flow in cash (including bank balances) over a

time period (Fosu, 2013).

The cash flows is classified into the following three categories:

1. Operating Activities: the cash flow from primary activities of a business.

2. Investing Activities: the cash flow from purchase and sale of assets excluding inventories

(e.g. purchase of a building)

3. Financing Activities: the cash flow originated from or spent on raising or repaying share

capital and debentures altogether with the payments of interest and dividends.

The main purpose of cash flow statement is that it provides crucial insights on the liquidity as

well as the solvency of Radisson Plc, which is very vital for its growth and survival. The

statements is used by investors and analysts inside and outside Radisson Plc for

formation/projection of future cash flows (Julian, Ofori-Dankwa, 2013).

Balance sheet/ Statement of Financial Position.

A balance sheet is a depiction of the financial position of a business on a given date,

usually prepared at the end of a quarter or year. It is a summary of assets, liabilities, and owners'

capital. Another name for the balance sheet is the statement of financial position. The balance

sheet is divided into two parts Assets and Liabilities. The basic equation of balance sheet is:

Assets = Liabilities + Shareholders' Equity(Owners' capital)

The purpose of the balance sheet is to give the users an image of Radisson Plc's financial

positions. It also depicts what the company owes as well as owns. Another purpose of using this

statement is that it allows the decision makers/administration of Radisson Plc, to evaluate and

bring changes accordingly (Lemma, Negash, 2013).

NB: The stake holders of Radisson Plc., at first will be focusing on the balance sheet.

4.2 Comparing the formats of financial statements.

Companies selected are Radisson Plc and Hilton Pvt. Ltd.

The annual report of Hilton Pvt. Ltd. Includes the following statements:

Directors’ remuneration report.

Statements of Directors’ responsibilities.

Independent auditors’ report.

Consolidated income statement.

Consolidated statement of comprehensive income.

Consolidated balance sheet.

Consolidated statement of changes in equity.

Consolidated cash flow statement.

Additional notes to the financial statements.

The annual report of Radisson Plc includes:

Strategic Report.

Directors’ Report.

Independent Auditor’s Report.

Profit and Loss Account.

Cash flow statement.

Balance Sheet.

Notes to the Financial Statements.

The main difference in the formats of the financial statements of both companies are that Hilton

Pvt Ltd., maintain income statements and Radisson Plc prepares profit & loss account. The

income statement comprise of income and revenues only and expenses are not shown, whereas

the profit and loss account of Radisson Plc shows all the incomes generated and expeditures.

The purpose of the balance sheet is to give the users an image of Radisson Plc's financial

positions. It also depicts what the company owes as well as owns. Another purpose of using this

statement is that it allows the decision makers/administration of Radisson Plc, to evaluate and

bring changes accordingly (Lemma, Negash, 2013).

NB: The stake holders of Radisson Plc., at first will be focusing on the balance sheet.

4.2 Comparing the formats of financial statements.

Companies selected are Radisson Plc and Hilton Pvt. Ltd.

The annual report of Hilton Pvt. Ltd. Includes the following statements:

Directors’ remuneration report.

Statements of Directors’ responsibilities.

Independent auditors’ report.

Consolidated income statement.

Consolidated statement of comprehensive income.

Consolidated balance sheet.

Consolidated statement of changes in equity.

Consolidated cash flow statement.

Additional notes to the financial statements.

The annual report of Radisson Plc includes:

Strategic Report.

Directors’ Report.

Independent Auditor’s Report.

Profit and Loss Account.

Cash flow statement.

Balance Sheet.

Notes to the Financial Statements.

The main difference in the formats of the financial statements of both companies are that Hilton

Pvt Ltd., maintain income statements and Radisson Plc prepares profit & loss account. The

income statement comprise of income and revenues only and expenses are not shown, whereas

the profit and loss account of Radisson Plc shows all the incomes generated and expeditures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.