Analyzing Financial Resources and Decisions: Hardwood Ltd Report

VerifiedAdded on 2020/02/14

|18

|4433

|28

Report

AI Summary

This comprehensive report examines the financial resource management of Hardwood Ltd, a medium-sized furniture manufacturer. It explores various sources of finance, including short, medium, and long-term options such as trade credit, debentures, retained earnings, hire purchase, leasing, share capital, and bank loans, analyzing their implications and recommending the most appropriate choices for the company's expansion plans. The report emphasizes the importance of financial planning, detailing the information needs of decision-makers like shareholders, employees, suppliers, and financial institutions. It analyzes the impact of finance on financial statements, including balance sheets, profit and loss accounts, and cash flow statements. Furthermore, the report includes an analysis of a cash budget, cost calculations, and investment appraisal techniques such as net present value, internal rate of return and ratio analysis, providing a holistic view of Hardwood Ltd's financial strategy and performance.

MANAGING FINANCIAL

RESOURCES AND

DECISIONS

RESOURCES AND

DECISIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to Hardwood Ltd......................................................................1

1.2 Implications of sources of finance.........................................................................................2

1.3 Appropriate source of finance...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance.......................................................................................4

2.2 Importance of financial planning...........................................................................................4

2.3 Information need of decision makers....................................................................................5

2.4 Impact of finance on financial statements.............................................................................5

TASK 3............................................................................................................................................6

3.1 Analyzing cash budget...........................................................................................................6

3.2 Calculation of unit cost..........................................................................................................6

3.3 Investment appraisal technique..............................................................................................7

TASK 4............................................................................................................................................9

4.1 Main financial statements of company..................................................................................9

4.2 Appropriate format of financial statement...........................................................................11

4.3 Ratio analysis.......................................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance available to Hardwood Ltd......................................................................1

1.2 Implications of sources of finance.........................................................................................2

1.3 Appropriate source of finance...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Cost of different sources of finance.......................................................................................4

2.2 Importance of financial planning...........................................................................................4

2.3 Information need of decision makers....................................................................................5

2.4 Impact of finance on financial statements.............................................................................5

TASK 3............................................................................................................................................6

3.1 Analyzing cash budget...........................................................................................................6

3.2 Calculation of unit cost..........................................................................................................6

3.3 Investment appraisal technique..............................................................................................7

TASK 4............................................................................................................................................9

4.1 Main financial statements of company..................................................................................9

4.2 Appropriate format of financial statement...........................................................................11

4.3 Ratio analysis.......................................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Managing financial resources plays important role in the business as without proper

management of funds it is not possible for management to accomplish desired objectives.

Further, finance is one of the key resource without which no business can survive in the market

and is associated with growth along with overall performance of company in the market.

Moreover, at the time of taking expansion decision different sources of finance are considered by

company through which it becomes easy to carry out overall operations in effective manner

(Malina and Selto, 2006). Apart from this to assess financial viability of the project investment

appraisal techniques are used which involves net present value, internal rate of return etc.

Through all these methods it is possible to allocate funds in right project. Considering the present

scenario Hardwood Ltd is a medium sized private company which produces furniture for retail

sector along with private homes for last 6 years. At present business is planning to expand its

operations for which management of financial resources is must. Various tasks have been

covered in the study which involves sources of finance and its implication, information need for

decision makers etc.

TASK 1

1.1 Sources of finance available to Hardwood Ltd

Different sources of finance are available to Hardwood Ltd which company can consider

for expanding its operations. Such sources are for short, long and medium term.

Short Term Sources

(<1year)

Medium Term Sources

( 2 ~ 5 years)

Long Term Sources ( > ~5

years)

Trade credit

It is considered as an

appropriate short term

source of finance where

Hardwood Ltd can purchase

goods from its suppliers

without making immediate

payment for the same

(Mohsin, 2013).

Debenture

Hardwood Ltd can issue debenture and

can obtain expansion amount through

this source. Further, it is required for firm

to pay interest to the debenture holder.

Retained earning

It is one of the most appropriate

internal and long term sources of

finance which Hardwood Ltd can

consider. Firm can use the amount

kept as saving in order to meet

unforeseen contingency.

Hire purchase Leasing Share capital

1

Managing financial resources plays important role in the business as without proper

management of funds it is not possible for management to accomplish desired objectives.

Further, finance is one of the key resource without which no business can survive in the market

and is associated with growth along with overall performance of company in the market.

Moreover, at the time of taking expansion decision different sources of finance are considered by

company through which it becomes easy to carry out overall operations in effective manner

(Malina and Selto, 2006). Apart from this to assess financial viability of the project investment

appraisal techniques are used which involves net present value, internal rate of return etc.

Through all these methods it is possible to allocate funds in right project. Considering the present

scenario Hardwood Ltd is a medium sized private company which produces furniture for retail

sector along with private homes for last 6 years. At present business is planning to expand its

operations for which management of financial resources is must. Various tasks have been

covered in the study which involves sources of finance and its implication, information need for

decision makers etc.

TASK 1

1.1 Sources of finance available to Hardwood Ltd

Different sources of finance are available to Hardwood Ltd which company can consider

for expanding its operations. Such sources are for short, long and medium term.

Short Term Sources

(<1year)

Medium Term Sources

( 2 ~ 5 years)

Long Term Sources ( > ~5

years)

Trade credit

It is considered as an

appropriate short term

source of finance where

Hardwood Ltd can purchase

goods from its suppliers

without making immediate

payment for the same

(Mohsin, 2013).

Debenture

Hardwood Ltd can issue debenture and

can obtain expansion amount through

this source. Further, it is required for firm

to pay interest to the debenture holder.

Retained earning

It is one of the most appropriate

internal and long term sources of

finance which Hardwood Ltd can

consider. Firm can use the amount

kept as saving in order to meet

unforeseen contingency.

Hire purchase Leasing Share capital

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is an agreement in which

owner of the asset lets them

hire on for regular

instalment paid by the hirer.

It is an agreement between lessor and

lessee where lessor owns capital asset but

allows lessee to use it. Through this

company can obtain amount for

expansion purpose.

Hardwood Ltd can issue equity shares

in the market and amount can be

easily obtained through this

(Mumford, Schultz and Osburn,

2001).

Overdraft

It is considered as an

appropriate short term

source of finance where

Hardwood Ltd can withdraw

more amount that those

lying in the bank

Bank loan

Company can take loan for long

period of time and satisfying its

financial needs such as for expansion

etc.

1.2 Implications of sources of finance

Source of

Finance

Description Advantages Disadvantages

Bank loan For satisfying financial

needs Hardwood Ltd can

take loan from bank

(Murphy, 2001)

Main advantage of using this

source is that it enhances

liquidity position of the firm

One of the main disadvantage of

considering this source is that

company has to pay interest to bank

for the amount obtained.

Overdraft It is the facility granted by

bank to withdraw more

amount than those lying in

the account

Main advantage of this

source is that it supports in

satisfying financial needs of

the company (Parmenter,

2010)

Company has to pay high rate of

interest to bank for the amount

obtained

2

owner of the asset lets them

hire on for regular

instalment paid by the hirer.

It is an agreement between lessor and

lessee where lessor owns capital asset but

allows lessee to use it. Through this

company can obtain amount for

expansion purpose.

Hardwood Ltd can issue equity shares

in the market and amount can be

easily obtained through this

(Mumford, Schultz and Osburn,

2001).

Overdraft

It is considered as an

appropriate short term

source of finance where

Hardwood Ltd can withdraw

more amount that those

lying in the bank

Bank loan

Company can take loan for long

period of time and satisfying its

financial needs such as for expansion

etc.

1.2 Implications of sources of finance

Source of

Finance

Description Advantages Disadvantages

Bank loan For satisfying financial

needs Hardwood Ltd can

take loan from bank

(Murphy, 2001)

Main advantage of using this

source is that it enhances

liquidity position of the firm

One of the main disadvantage of

considering this source is that

company has to pay interest to bank

for the amount obtained.

Overdraft It is the facility granted by

bank to withdraw more

amount than those lying in

the account

Main advantage of this

source is that it supports in

satisfying financial needs of

the company (Parmenter,

2010)

Company has to pay high rate of

interest to bank for the amount

obtained

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

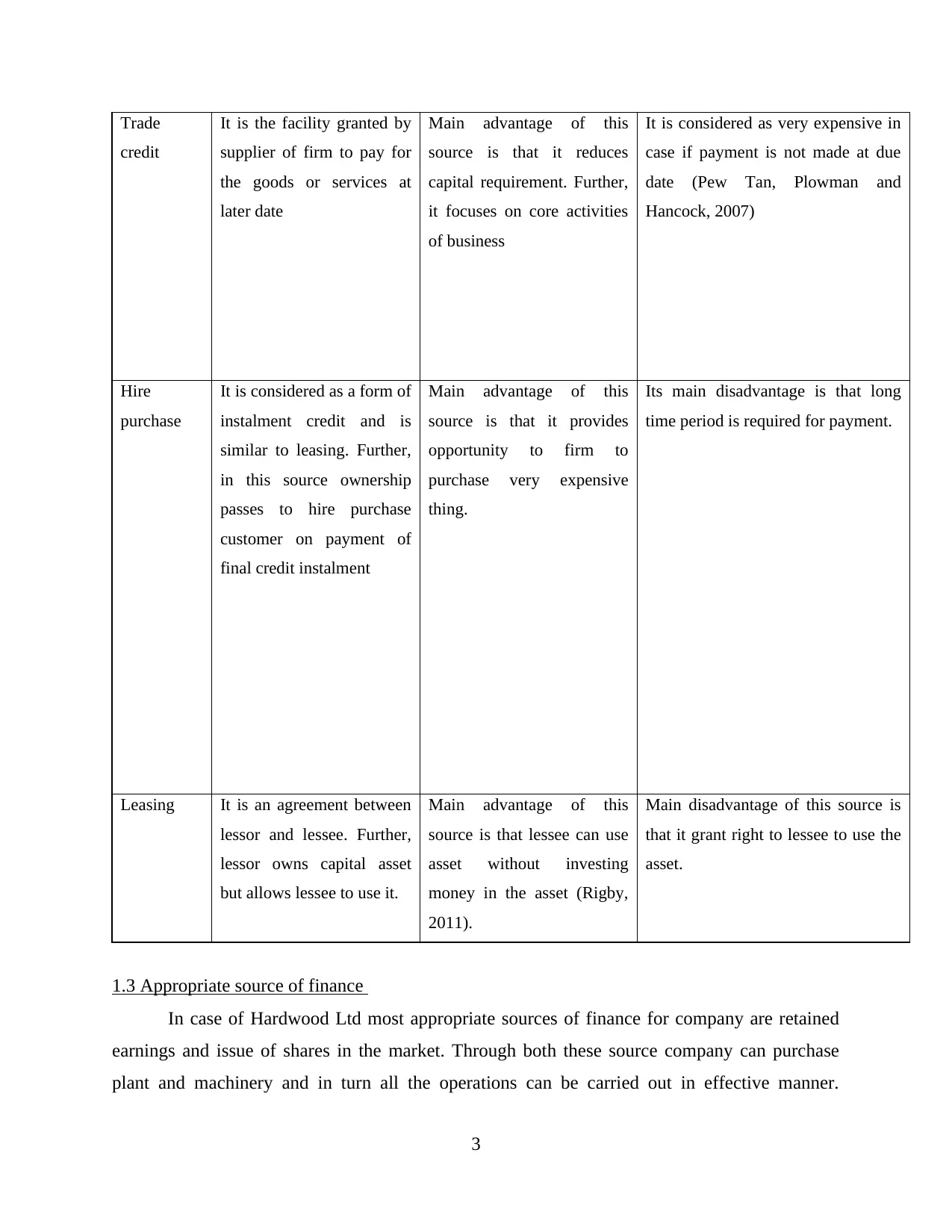

Trade

credit

It is the facility granted by

supplier of firm to pay for

the goods or services at

later date

Main advantage of this

source is that it reduces

capital requirement. Further,

it focuses on core activities

of business

It is considered as very expensive in

case if payment is not made at due

date (Pew Tan, Plowman and

Hancock, 2007)

Hire

purchase

It is considered as a form of

instalment credit and is

similar to leasing. Further,

in this source ownership

passes to hire purchase

customer on payment of

final credit instalment

Main advantage of this

source is that it provides

opportunity to firm to

purchase very expensive

thing.

Its main disadvantage is that long

time period is required for payment.

Leasing It is an agreement between

lessor and lessee. Further,

lessor owns capital asset

but allows lessee to use it.

Main advantage of this

source is that lessee can use

asset without investing

money in the asset (Rigby,

2011).

Main disadvantage of this source is

that it grant right to lessee to use the

asset.

1.3 Appropriate source of finance

In case of Hardwood Ltd most appropriate sources of finance for company are retained

earnings and issue of shares in the market. Through both these source company can purchase

plant and machinery and in turn all the operations can be carried out in effective manner.

3

credit

It is the facility granted by

supplier of firm to pay for

the goods or services at

later date

Main advantage of this

source is that it reduces

capital requirement. Further,

it focuses on core activities

of business

It is considered as very expensive in

case if payment is not made at due

date (Pew Tan, Plowman and

Hancock, 2007)

Hire

purchase

It is considered as a form of

instalment credit and is

similar to leasing. Further,

in this source ownership

passes to hire purchase

customer on payment of

final credit instalment

Main advantage of this

source is that it provides

opportunity to firm to

purchase very expensive

thing.

Its main disadvantage is that long

time period is required for payment.

Leasing It is an agreement between

lessor and lessee. Further,

lessor owns capital asset

but allows lessee to use it.

Main advantage of this

source is that lessee can use

asset without investing

money in the asset (Rigby,

2011).

Main disadvantage of this source is

that it grant right to lessee to use the

asset.

1.3 Appropriate source of finance

In case of Hardwood Ltd most appropriate sources of finance for company are retained

earnings and issue of shares in the market. Through both these source company can purchase

plant and machinery and in turn all the operations can be carried out in effective manner.

3

Hardwood Ltd operates on larger basis due to which its savings can be easily utilized for

conducting operations. Further, shares can be issued in the market where company can obtain

capital through its investors and it is beneficial for the entire business (Vos and et.al., 2007).

Main benefit of adopting retained earnings as a source is that large amount of fund can be

obtained internally and funds can be easily obtained for expansion purpose. But on the other

hand in case funds are obtained by issuing shares in the market then company has to pay

dividend to its shareholders which increase expenditure level. Therefore, the two sources

recommended are appropriate for the company with the objective to expand overall operations.

TASK 2

2.1 Cost of different sources of finance

Considering different sources of finance for satisfying overall needs of the business has

cost associated with it which Hardwood Ltd has to consider necessarily. In case when company

considers issuing shares as source of finance then cost associated with payment of dividend has

to bear and this increases overall expenditure level of the business. Further, when bank loan is

considered as one of the source of finance then it leads to rise in interest cost which is

unfavorable for business as company has to pay interest for the amount obtained (Wilmott,

2013). Therefore, this cost also has adverse impact on the business and for operating efficiently

business has to identify which source is cheap so that long term benefits can be obtained easily

by business. Apart from this when retained earnings is considered as an source of finance then it

leads to rise in overall cost of loss linked with investment in any other project which is regarded

as opportunity cost. So, these are some of the major costs associated with different sources of

finance which Hardwood Ltd has to consider while selecting any source.

2.2 Importance of financial planning

Financial planning is must for Hardwood Ltd as business is presently planning to expand

its operations and for the same planning is must. Further, the significant aspect of financial

planning takes into consideration development of budgets, financial forecasting, making fruitful

decisions and identifying the appropriate source of finance. Through, financial planning it is

possible for business to utilize all the resources in efficient manner and in turn acts as

development tool for the business (Davies and Crawford, 2011). In short, planning allows

business to gain competitive advantage and in turn unfavorable situations such as inadequacy of

finance can be tackled easily by business. Through financial planning company can know how

4

conducting operations. Further, shares can be issued in the market where company can obtain

capital through its investors and it is beneficial for the entire business (Vos and et.al., 2007).

Main benefit of adopting retained earnings as a source is that large amount of fund can be

obtained internally and funds can be easily obtained for expansion purpose. But on the other

hand in case funds are obtained by issuing shares in the market then company has to pay

dividend to its shareholders which increase expenditure level. Therefore, the two sources

recommended are appropriate for the company with the objective to expand overall operations.

TASK 2

2.1 Cost of different sources of finance

Considering different sources of finance for satisfying overall needs of the business has

cost associated with it which Hardwood Ltd has to consider necessarily. In case when company

considers issuing shares as source of finance then cost associated with payment of dividend has

to bear and this increases overall expenditure level of the business. Further, when bank loan is

considered as one of the source of finance then it leads to rise in interest cost which is

unfavorable for business as company has to pay interest for the amount obtained (Wilmott,

2013). Therefore, this cost also has adverse impact on the business and for operating efficiently

business has to identify which source is cheap so that long term benefits can be obtained easily

by business. Apart from this when retained earnings is considered as an source of finance then it

leads to rise in overall cost of loss linked with investment in any other project which is regarded

as opportunity cost. So, these are some of the major costs associated with different sources of

finance which Hardwood Ltd has to consider while selecting any source.

2.2 Importance of financial planning

Financial planning is must for Hardwood Ltd as business is presently planning to expand

its operations and for the same planning is must. Further, the significant aspect of financial

planning takes into consideration development of budgets, financial forecasting, making fruitful

decisions and identifying the appropriate source of finance. Through, financial planning it is

possible for business to utilize all the resources in efficient manner and in turn acts as

development tool for the business (Davies and Crawford, 2011). In short, planning allows

business to gain competitive advantage and in turn unfavorable situations such as inadequacy of

finance can be tackled easily by business. Through financial planning company can know how

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

much funds are required in carrying out key operations of the business and through this fund can

be allocated accordingly. Apart from this, due to rise in level of competition along with other

type of challenges in the market it is required for business to indulge into practices of financial

planning so that it can be utilized in appropriate manner keeping in view overall aims and

objectives of the business (Financial Planning - Definition, Objectives and Importance., 2016).

2.3 Information need of decision makers

Individuals who are associated with Hardwood Ltd require different type of information

so that decisions can be taken which varies from one another. Shareholders of the company are

interested in knowing profitability along with liquidity position of the company through which

they can take investment decision and it can be known whether to buy shares of the company or

not. Further, employees of the company are interested in gaining information through which they

can know their personal growth level. Suppliers of Hardwood Ltd are interested in knowing

liquidity position of the firm as through this they can know the payment capacity of company as

goods are supplied on credit (Dell'Ariccia, Detragiache and Rajan, 2008). Apart from this,

financial institutions are interested in knowing the profitability position of the firm as through

this it can be known the time period in which company can repay the amount. Management of

Hardwood Ltd is interested in knowing profitability position of firm as through investment

decision can be taken easily which is associated with growth of organization. Therefore, in this

way the information need of decision makers varies from each other and they are interested in

obtaining different type of information to satisfy their personal needs.

2.4 Impact of finance on financial statements

Finance has direct impact on the financial statements being prepared by enterprise.

Further, it directly depends on the business the range of sources adopted for satisfying its

financial needs. Generally statements such as balance sheet, profit and loss account, cash flow

statement etc are prepared by business for knowing its overall performance in the market. In case

if business uses retained earnings as a source to satisfy its financial needs then it increases the

value of equity in the balance sheet and enhances the gearing ratio. Further, in case if debenture

is undertaken by firm then interest paid is shown as an expense in profit and loss account and is

also considered in cash flow statement as an outflow in operating activities (Elliott and Meyer,

2007). Cash received from issuing debentures is represented in cash from financing activities.

Apart from this, if bank overdraft is considered as source then interest paid is charged as an

5

be allocated accordingly. Apart from this, due to rise in level of competition along with other

type of challenges in the market it is required for business to indulge into practices of financial

planning so that it can be utilized in appropriate manner keeping in view overall aims and

objectives of the business (Financial Planning - Definition, Objectives and Importance., 2016).

2.3 Information need of decision makers

Individuals who are associated with Hardwood Ltd require different type of information

so that decisions can be taken which varies from one another. Shareholders of the company are

interested in knowing profitability along with liquidity position of the company through which

they can take investment decision and it can be known whether to buy shares of the company or

not. Further, employees of the company are interested in gaining information through which they

can know their personal growth level. Suppliers of Hardwood Ltd are interested in knowing

liquidity position of the firm as through this they can know the payment capacity of company as

goods are supplied on credit (Dell'Ariccia, Detragiache and Rajan, 2008). Apart from this,

financial institutions are interested in knowing the profitability position of the firm as through

this it can be known the time period in which company can repay the amount. Management of

Hardwood Ltd is interested in knowing profitability position of firm as through investment

decision can be taken easily which is associated with growth of organization. Therefore, in this

way the information need of decision makers varies from each other and they are interested in

obtaining different type of information to satisfy their personal needs.

2.4 Impact of finance on financial statements

Finance has direct impact on the financial statements being prepared by enterprise.

Further, it directly depends on the business the range of sources adopted for satisfying its

financial needs. Generally statements such as balance sheet, profit and loss account, cash flow

statement etc are prepared by business for knowing its overall performance in the market. In case

if business uses retained earnings as a source to satisfy its financial needs then it increases the

value of equity in the balance sheet and enhances the gearing ratio. Further, in case if debenture

is undertaken by firm then interest paid is shown as an expense in profit and loss account and is

also considered in cash flow statement as an outflow in operating activities (Elliott and Meyer,

2007). Cash received from issuing debentures is represented in cash from financing activities.

Apart from this, if bank overdraft is considered as source then interest paid is charged as an

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expense in income statement and is also considered as an outflow in operating activity. Venture

capital as a source has impact on cash flow statement where cash proceed of the share issue is

regarded as an inflow which is considered under financing activity in cash flow statement.

TASK 3

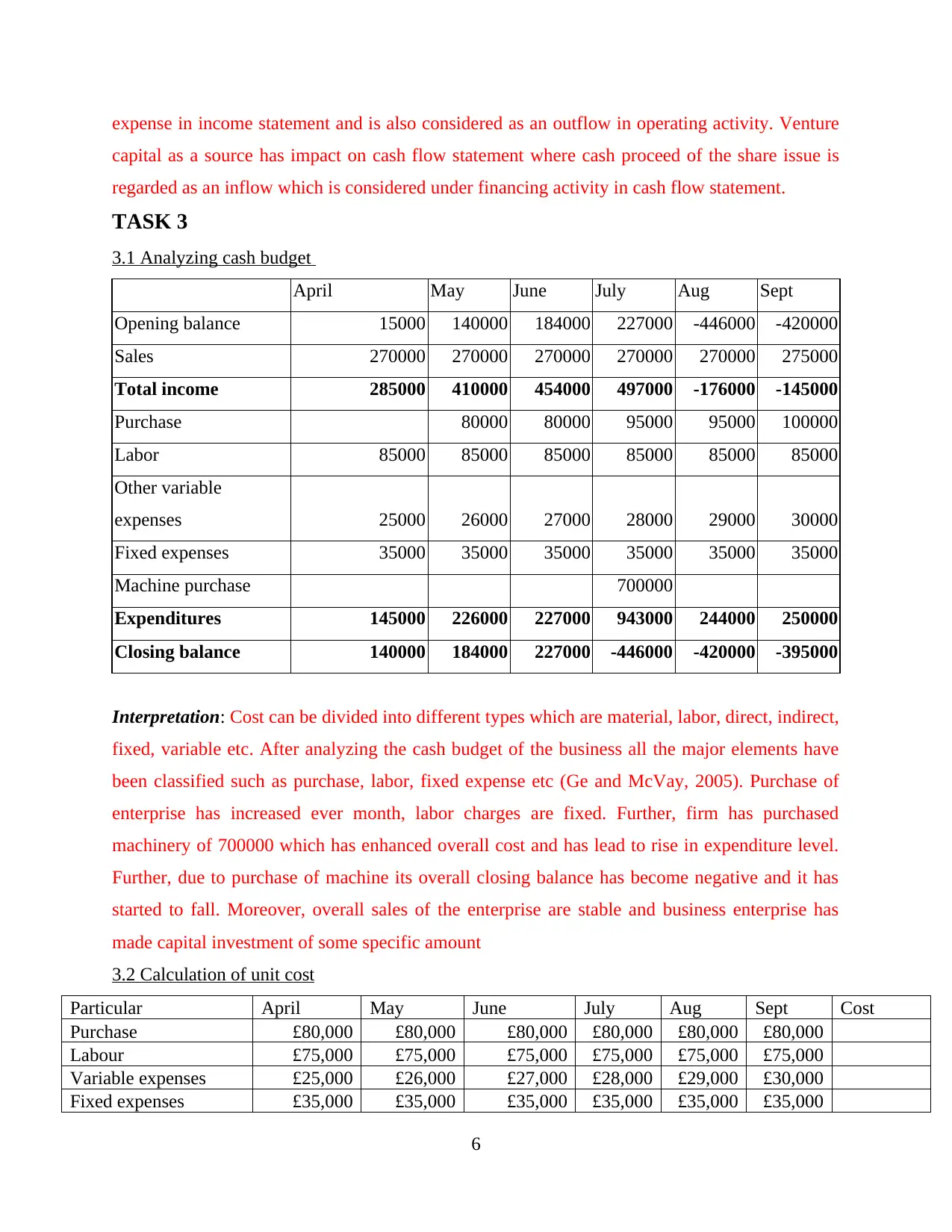

3.1 Analyzing cash budget

April May June July Aug Sept

Opening balance 15000 140000 184000 227000 -446000 -420000

Sales 270000 270000 270000 270000 270000 275000

Total income 285000 410000 454000 497000 -176000 -145000

Purchase 80000 80000 95000 95000 100000

Labor 85000 85000 85000 85000 85000 85000

Other variable

expenses 25000 26000 27000 28000 29000 30000

Fixed expenses 35000 35000 35000 35000 35000 35000

Machine purchase 700000

Expenditures 145000 226000 227000 943000 244000 250000

Closing balance 140000 184000 227000 -446000 -420000 -395000

Interpretation: Cost can be divided into different types which are material, labor, direct, indirect,

fixed, variable etc. After analyzing the cash budget of the business all the major elements have

been classified such as purchase, labor, fixed expense etc (Ge and McVay, 2005). Purchase of

enterprise has increased ever month, labor charges are fixed. Further, firm has purchased

machinery of 700000 which has enhanced overall cost and has lead to rise in expenditure level.

Further, due to purchase of machine its overall closing balance has become negative and it has

started to fall. Moreover, overall sales of the enterprise are stable and business enterprise has

made capital investment of some specific amount

3.2 Calculation of unit cost

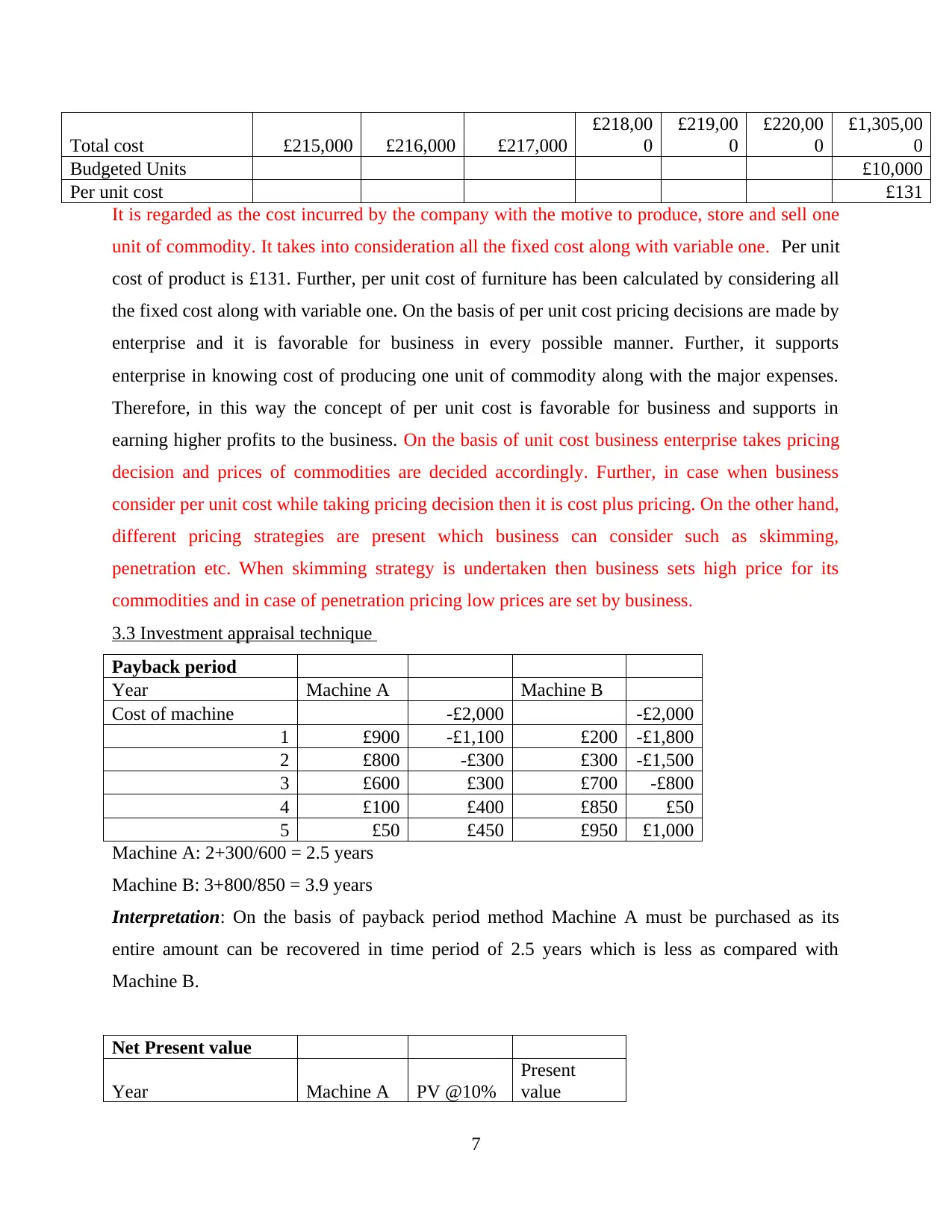

Particular April May June July Aug Sept Cost

Purchase £80,000 £80,000 £80,000 £80,000 £80,000 £80,000

Labour £75,000 £75,000 £75,000 £75,000 £75,000 £75,000

Variable expenses £25,000 £26,000 £27,000 £28,000 £29,000 £30,000

Fixed expenses £35,000 £35,000 £35,000 £35,000 £35,000 £35,000

6

capital as a source has impact on cash flow statement where cash proceed of the share issue is

regarded as an inflow which is considered under financing activity in cash flow statement.

TASK 3

3.1 Analyzing cash budget

April May June July Aug Sept

Opening balance 15000 140000 184000 227000 -446000 -420000

Sales 270000 270000 270000 270000 270000 275000

Total income 285000 410000 454000 497000 -176000 -145000

Purchase 80000 80000 95000 95000 100000

Labor 85000 85000 85000 85000 85000 85000

Other variable

expenses 25000 26000 27000 28000 29000 30000

Fixed expenses 35000 35000 35000 35000 35000 35000

Machine purchase 700000

Expenditures 145000 226000 227000 943000 244000 250000

Closing balance 140000 184000 227000 -446000 -420000 -395000

Interpretation: Cost can be divided into different types which are material, labor, direct, indirect,

fixed, variable etc. After analyzing the cash budget of the business all the major elements have

been classified such as purchase, labor, fixed expense etc (Ge and McVay, 2005). Purchase of

enterprise has increased ever month, labor charges are fixed. Further, firm has purchased

machinery of 700000 which has enhanced overall cost and has lead to rise in expenditure level.

Further, due to purchase of machine its overall closing balance has become negative and it has

started to fall. Moreover, overall sales of the enterprise are stable and business enterprise has

made capital investment of some specific amount

3.2 Calculation of unit cost

Particular April May June July Aug Sept Cost

Purchase £80,000 £80,000 £80,000 £80,000 £80,000 £80,000

Labour £75,000 £75,000 £75,000 £75,000 £75,000 £75,000

Variable expenses £25,000 £26,000 £27,000 £28,000 £29,000 £30,000

Fixed expenses £35,000 £35,000 £35,000 £35,000 £35,000 £35,000

6

Total cost £215,000 £216,000 £217,000

£218,00

0

£219,00

0

£220,00

0

£1,305,00

0

Budgeted Units £10,000

Per unit cost £131

It is regarded as the cost incurred by the company with the motive to produce, store and sell one

unit of commodity. It takes into consideration all the fixed cost along with variable one. Per unit

cost of product is £131. Further, per unit cost of furniture has been calculated by considering all

the fixed cost along with variable one. On the basis of per unit cost pricing decisions are made by

enterprise and it is favorable for business in every possible manner. Further, it supports

enterprise in knowing cost of producing one unit of commodity along with the major expenses.

Therefore, in this way the concept of per unit cost is favorable for business and supports in

earning higher profits to the business. On the basis of unit cost business enterprise takes pricing

decision and prices of commodities are decided accordingly. Further, in case when business

consider per unit cost while taking pricing decision then it is cost plus pricing. On the other hand,

different pricing strategies are present which business can consider such as skimming,

penetration etc. When skimming strategy is undertaken then business sets high price for its

commodities and in case of penetration pricing low prices are set by business.

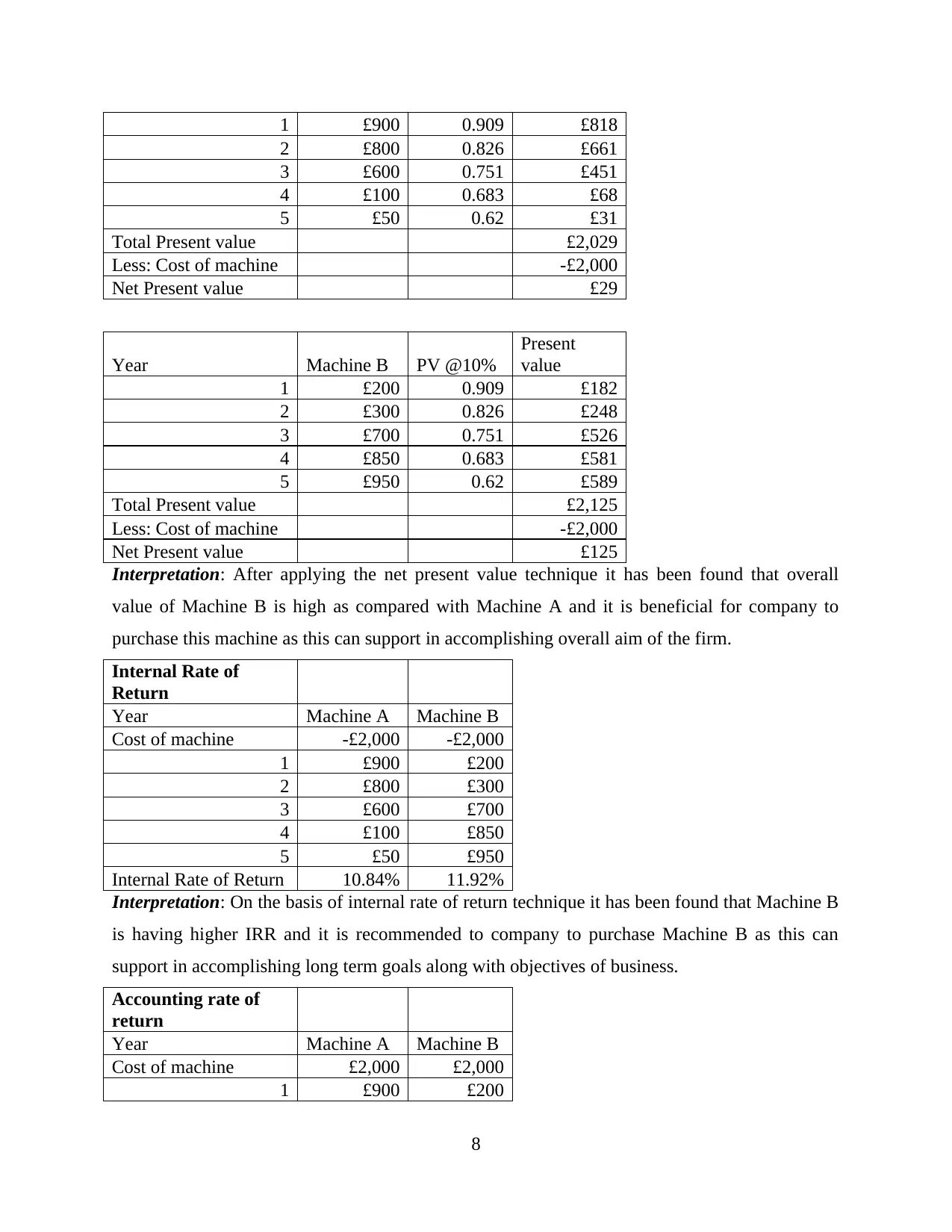

3.3 Investment appraisal technique

Payback period

Year Machine A Machine B

Cost of machine -£2,000 -£2,000

1 £900 -£1,100 £200 -£1,800

2 £800 -£300 £300 -£1,500

3 £600 £300 £700 -£800

4 £100 £400 £850 £50

5 £50 £450 £950 £1,000

Machine A: 2+300/600 = 2.5 years

Machine B: 3+800/850 = 3.9 years

Interpretation: On the basis of payback period method Machine A must be purchased as its

entire amount can be recovered in time period of 2.5 years which is less as compared with

Machine B.

Net Present value

Year Machine A PV @10%

Present

value

7

£218,00

0

£219,00

0

£220,00

0

£1,305,00

0

Budgeted Units £10,000

Per unit cost £131

It is regarded as the cost incurred by the company with the motive to produce, store and sell one

unit of commodity. It takes into consideration all the fixed cost along with variable one. Per unit

cost of product is £131. Further, per unit cost of furniture has been calculated by considering all

the fixed cost along with variable one. On the basis of per unit cost pricing decisions are made by

enterprise and it is favorable for business in every possible manner. Further, it supports

enterprise in knowing cost of producing one unit of commodity along with the major expenses.

Therefore, in this way the concept of per unit cost is favorable for business and supports in

earning higher profits to the business. On the basis of unit cost business enterprise takes pricing

decision and prices of commodities are decided accordingly. Further, in case when business

consider per unit cost while taking pricing decision then it is cost plus pricing. On the other hand,

different pricing strategies are present which business can consider such as skimming,

penetration etc. When skimming strategy is undertaken then business sets high price for its

commodities and in case of penetration pricing low prices are set by business.

3.3 Investment appraisal technique

Payback period

Year Machine A Machine B

Cost of machine -£2,000 -£2,000

1 £900 -£1,100 £200 -£1,800

2 £800 -£300 £300 -£1,500

3 £600 £300 £700 -£800

4 £100 £400 £850 £50

5 £50 £450 £950 £1,000

Machine A: 2+300/600 = 2.5 years

Machine B: 3+800/850 = 3.9 years

Interpretation: On the basis of payback period method Machine A must be purchased as its

entire amount can be recovered in time period of 2.5 years which is less as compared with

Machine B.

Net Present value

Year Machine A PV @10%

Present

value

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 £900 0.909 £818

2 £800 0.826 £661

3 £600 0.751 £451

4 £100 0.683 £68

5 £50 0.62 £31

Total Present value £2,029

Less: Cost of machine -£2,000

Net Present value £29

Year Machine B PV @10%

Present

value

1 £200 0.909 £182

2 £300 0.826 £248

3 £700 0.751 £526

4 £850 0.683 £581

5 £950 0.62 £589

Total Present value £2,125

Less: Cost of machine -£2,000

Net Present value £125

Interpretation: After applying the net present value technique it has been found that overall

value of Machine B is high as compared with Machine A and it is beneficial for company to

purchase this machine as this can support in accomplishing overall aim of the firm.

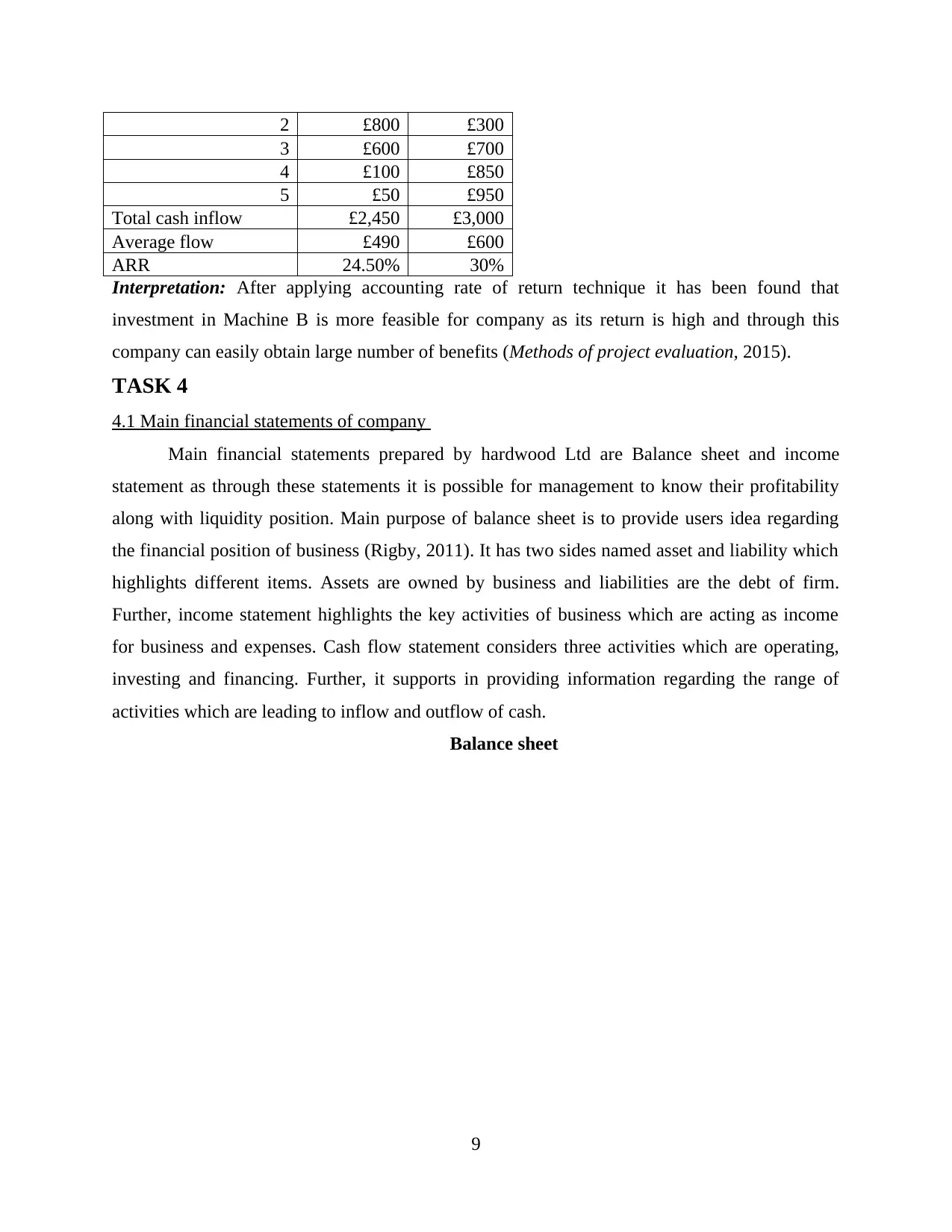

Internal Rate of

Return

Year Machine A Machine B

Cost of machine -£2,000 -£2,000

1 £900 £200

2 £800 £300

3 £600 £700

4 £100 £850

5 £50 £950

Internal Rate of Return 10.84% 11.92%

Interpretation: On the basis of internal rate of return technique it has been found that Machine B

is having higher IRR and it is recommended to company to purchase Machine B as this can

support in accomplishing long term goals along with objectives of business.

Accounting rate of

return

Year Machine A Machine B

Cost of machine £2,000 £2,000

1 £900 £200

8

2 £800 0.826 £661

3 £600 0.751 £451

4 £100 0.683 £68

5 £50 0.62 £31

Total Present value £2,029

Less: Cost of machine -£2,000

Net Present value £29

Year Machine B PV @10%

Present

value

1 £200 0.909 £182

2 £300 0.826 £248

3 £700 0.751 £526

4 £850 0.683 £581

5 £950 0.62 £589

Total Present value £2,125

Less: Cost of machine -£2,000

Net Present value £125

Interpretation: After applying the net present value technique it has been found that overall

value of Machine B is high as compared with Machine A and it is beneficial for company to

purchase this machine as this can support in accomplishing overall aim of the firm.

Internal Rate of

Return

Year Machine A Machine B

Cost of machine -£2,000 -£2,000

1 £900 £200

2 £800 £300

3 £600 £700

4 £100 £850

5 £50 £950

Internal Rate of Return 10.84% 11.92%

Interpretation: On the basis of internal rate of return technique it has been found that Machine B

is having higher IRR and it is recommended to company to purchase Machine B as this can

support in accomplishing long term goals along with objectives of business.

Accounting rate of

return

Year Machine A Machine B

Cost of machine £2,000 £2,000

1 £900 £200

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 £800 £300

3 £600 £700

4 £100 £850

5 £50 £950

Total cash inflow £2,450 £3,000

Average flow £490 £600

ARR 24.50% 30%

Interpretation: After applying accounting rate of return technique it has been found that

investment in Machine B is more feasible for company as its return is high and through this

company can easily obtain large number of benefits (Methods of project evaluation, 2015).

TASK 4

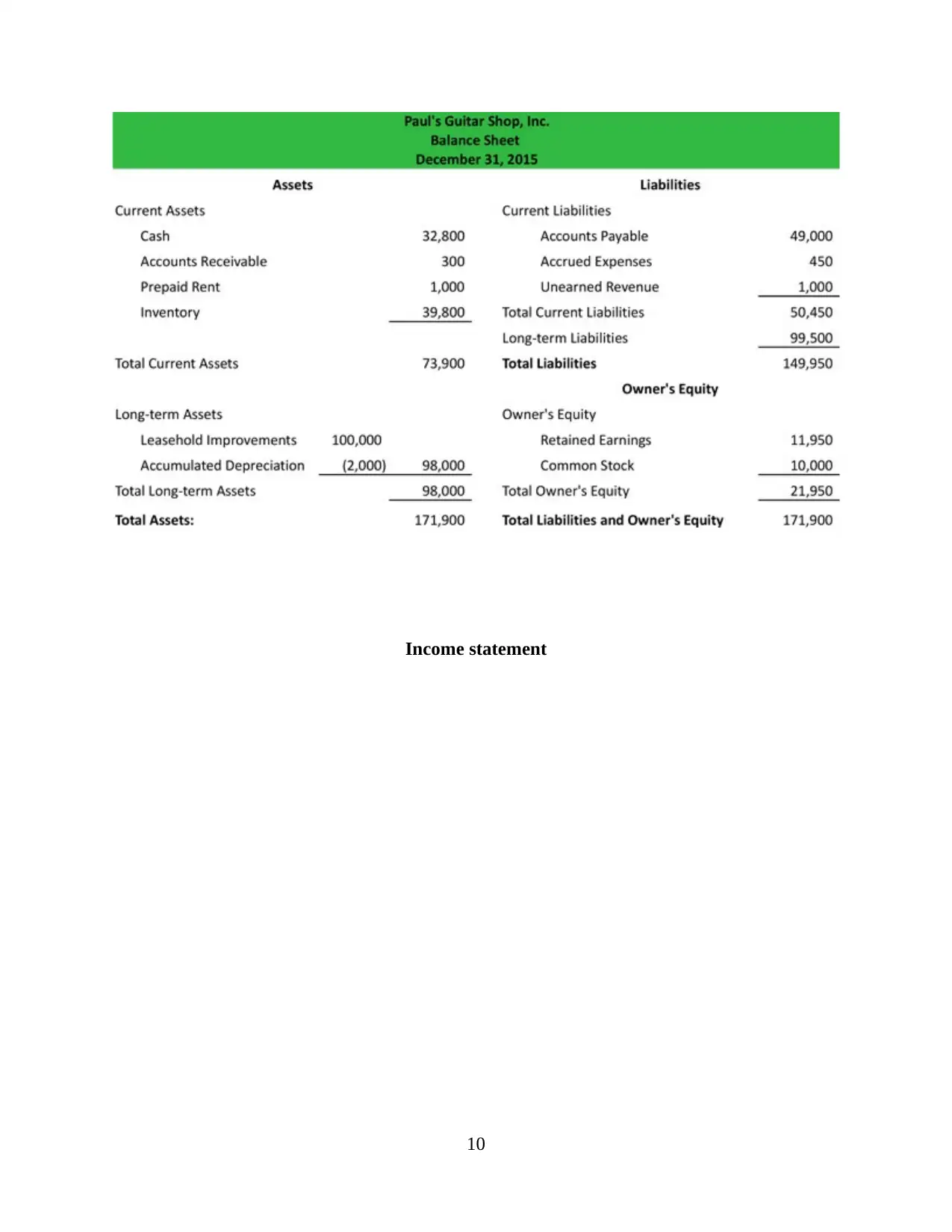

4.1 Main financial statements of company

Main financial statements prepared by hardwood Ltd are Balance sheet and income

statement as through these statements it is possible for management to know their profitability

along with liquidity position. Main purpose of balance sheet is to provide users idea regarding

the financial position of business (Rigby, 2011). It has two sides named asset and liability which

highlights different items. Assets are owned by business and liabilities are the debt of firm.

Further, income statement highlights the key activities of business which are acting as income

for business and expenses. Cash flow statement considers three activities which are operating,

investing and financing. Further, it supports in providing information regarding the range of

activities which are leading to inflow and outflow of cash.

Balance sheet

9

3 £600 £700

4 £100 £850

5 £50 £950

Total cash inflow £2,450 £3,000

Average flow £490 £600

ARR 24.50% 30%

Interpretation: After applying accounting rate of return technique it has been found that

investment in Machine B is more feasible for company as its return is high and through this

company can easily obtain large number of benefits (Methods of project evaluation, 2015).

TASK 4

4.1 Main financial statements of company

Main financial statements prepared by hardwood Ltd are Balance sheet and income

statement as through these statements it is possible for management to know their profitability

along with liquidity position. Main purpose of balance sheet is to provide users idea regarding

the financial position of business (Rigby, 2011). It has two sides named asset and liability which

highlights different items. Assets are owned by business and liabilities are the debt of firm.

Further, income statement highlights the key activities of business which are acting as income

for business and expenses. Cash flow statement considers three activities which are operating,

investing and financing. Further, it supports in providing information regarding the range of

activities which are leading to inflow and outflow of cash.

Balance sheet

9

Income statement

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.