Comprehensive Report: Managing Financial Resources for Business Growth

VerifiedAdded on 2019/12/03

|24

|4195

|431

Report

AI Summary

This report delves into the critical aspects of managing financial resources for businesses. It begins by exploring various sources of finance, including retained earnings, share capital, and bank loans, and analyzes their advantages, disadvantages, and associated costs. The report then evaluates the suitability of these sources for different business scenarios, such as small business startups, large business expansions, and acquisitions. Furthermore, it examines the importance of financial planning, including the creation of financial statements like income statements and balance sheets, for effective decision-making and risk mitigation. The report also discusses how financial information is used by various stakeholders, including customers, employees, government, suppliers, and shareholders, to assess a company's performance and make informed decisions. The report concludes by providing examples of how different financial transactions impact financial statements.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction .....................................................................................................................................3

TASK 1 ...........................................................................................................................................3

Task 2...............................................................................................................................................5

Task 3 ..............................................................................................................................................9

Task 4 ............................................................................................................................................17

Conclusion ....................................................................................................................................21

References......................................................................................................................................23

Introduction .....................................................................................................................................3

TASK 1 ...........................................................................................................................................3

Task 2...............................................................................................................................................5

Task 3 ..............................................................................................................................................9

Task 4 ............................................................................................................................................17

Conclusion ....................................................................................................................................21

References......................................................................................................................................23

Introduction

Management of financial resources is very essential in the process of decision making. It is

required at all levels as finance is the major element to be imposed in the business. In the

following report, the different sources of finance available to the firm will be presented.

Discussion of ratio analysis will be presented to elaborate the financial records of the business.

TASK 1

Sources of finance available to business

Finance is the key element which is required for every kind of business that is irrespective of its

nature. It is essential at every level of operation. Considering the different types of business such

as new and old, large and small business entities for the purpose of new business set-up and

expansions, the sources of finance are available to them which are as follows: Retained earnings – For old business firms who are operating since a long period, the

best source of funding that is available to them is retained earnings. It is the amount

which is kept as reserve out from the profits and is accumulated every year in a particular

proportion (Fridson and Alvarez, 2002). This amount could be used for the purpose of

expansion or for setting up the new venture of similar business. Share capital – The other source of finance which is available to the newly establishing

firm is raising fund through share capital. Under this method, company allot shares in the

market to the public and accumulate funds from them. It is available to new as well as old

firms in the form of liabilities which they have to pay back to their shareholders after

certain period with dividend (Funke, 2007).

Bank loan – It is the most common source of finance for new firms who are planning to

work at small level in the initial stage. Bank loan is the form of complete debts which

could be raised from the banks and other financial lending institutions (Helfert, 2004).

This source of finance could be raised even for the purpose of setting large business firms

after observing the repaying capacity of organization by financial lenders.

Management of financial resources is very essential in the process of decision making. It is

required at all levels as finance is the major element to be imposed in the business. In the

following report, the different sources of finance available to the firm will be presented.

Discussion of ratio analysis will be presented to elaborate the financial records of the business.

TASK 1

Sources of finance available to business

Finance is the key element which is required for every kind of business that is irrespective of its

nature. It is essential at every level of operation. Considering the different types of business such

as new and old, large and small business entities for the purpose of new business set-up and

expansions, the sources of finance are available to them which are as follows: Retained earnings – For old business firms who are operating since a long period, the

best source of funding that is available to them is retained earnings. It is the amount

which is kept as reserve out from the profits and is accumulated every year in a particular

proportion (Fridson and Alvarez, 2002). This amount could be used for the purpose of

expansion or for setting up the new venture of similar business. Share capital – The other source of finance which is available to the newly establishing

firm is raising fund through share capital. Under this method, company allot shares in the

market to the public and accumulate funds from them. It is available to new as well as old

firms in the form of liabilities which they have to pay back to their shareholders after

certain period with dividend (Funke, 2007).

Bank loan – It is the most common source of finance for new firms who are planning to

work at small level in the initial stage. Bank loan is the form of complete debts which

could be raised from the banks and other financial lending institutions (Helfert, 2004).

This source of finance could be raised even for the purpose of setting large business firms

after observing the repaying capacity of organization by financial lenders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implication of sources of finance with consideration of different factors

By adopting the sources of finance that are available to different types of business firms,

there are various benefits and disadvantages to business and legal aspects. Also, there are certain

costs which are available to them which companies have to bear. All the relative factors for

sources of finance are described as under: Retained earnings

Advantage - The fund raised through retained earnings is available in the form of assets.

Company does not have to pay any kind of debts to the third party (McMenamin, 2002).

Disadvantage – It eventually leads to reduction in the profitability of business which is to

be disclosed among stakeholders of the firm.

Cost – There may be chances of opportunity loss to the firm. This could directly impact

the working capital of organization (Neftci, 2004). Share capital

Advantage – By the means of raising share capital, company could raise huge amount of

fund through public.

Disadvantage – Liability of the firm increases which could negatively affect the financial

statements of company.

Cost – It includes payment to the shareholders in form of dividend which reduces the

profitability of organization (Beck, Levine and Loayza, 2000). Bank loan

Advantage – It is a very easy process of borrowing fund and raising capital which is

provided by all kinds of financial institutions.

Disadvantage – Loan taken for longer period leads to accumulation of interest which

increases the amount that is to be repaid by firm.

By adopting the sources of finance that are available to different types of business firms,

there are various benefits and disadvantages to business and legal aspects. Also, there are certain

costs which are available to them which companies have to bear. All the relative factors for

sources of finance are described as under: Retained earnings

Advantage - The fund raised through retained earnings is available in the form of assets.

Company does not have to pay any kind of debts to the third party (McMenamin, 2002).

Disadvantage – It eventually leads to reduction in the profitability of business which is to

be disclosed among stakeholders of the firm.

Cost – There may be chances of opportunity loss to the firm. This could directly impact

the working capital of organization (Neftci, 2004). Share capital

Advantage – By the means of raising share capital, company could raise huge amount of

fund through public.

Disadvantage – Liability of the firm increases which could negatively affect the financial

statements of company.

Cost – It includes payment to the shareholders in form of dividend which reduces the

profitability of organization (Beck, Levine and Loayza, 2000). Bank loan

Advantage – It is a very easy process of borrowing fund and raising capital which is

provided by all kinds of financial institutions.

Disadvantage – Loan taken for longer period leads to accumulation of interest which

increases the amount that is to be repaid by firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost – The capital raised from bank loan involves huge cost in the form of interest which

leads to reduction in the profitability of company (Bhowmik and Saha, 2013).

Evaluating the appropriate sources of finance for business projects

For every form of business, finance is required at the initial stage. There are different

sources of finance which are available to different types of business which are as follows:

Small business start-up – Loan taken from bank is the best source of finance that is

available to small business firms while starting up the business. The advantage available

in obtaining loan is that they can easily obtain loan from financial institution by fulfilling

the required formalities (Brigham and Ehrhardt, 2011). The cost which is to be bear by

the firm includes payment of interest over principle amount which has been taken.

At the initial stage, company have opted for bank loan to initiate their business from the primary

level. When they were at the level of small business start up, company have raised amount

through bank loans.

Large business expansions – For the purpose of expansion by large operating firm, the

best source of raising capital is generating through share capital. Company has an

advantage of their past business performance and goodwill. Hence, by disclosing their

plan to public, companies could easily raise funds. They have to pay dividend to

shareholders which will be treated as cost to company.

Considering the company which has adopted all the sources of finance in different phase of

business, SONY could be considered. As they grew bigger, SONY became able to collect

amount out of their own earnings. The amount accumulated through retained earning have been

utilized for the purpose of large business expansion.

Acquiring medium sized company – When there are plans to acquire some other firms, the

ideal source of capital is retained earnings by individual person or organization

(Broadbent and Cullen, 2012). Although, it might affect the profitability of every firm,

but they will not get bounded under any kind of liabilities or debts.

leads to reduction in the profitability of company (Bhowmik and Saha, 2013).

Evaluating the appropriate sources of finance for business projects

For every form of business, finance is required at the initial stage. There are different

sources of finance which are available to different types of business which are as follows:

Small business start-up – Loan taken from bank is the best source of finance that is

available to small business firms while starting up the business. The advantage available

in obtaining loan is that they can easily obtain loan from financial institution by fulfilling

the required formalities (Brigham and Ehrhardt, 2011). The cost which is to be bear by

the firm includes payment of interest over principle amount which has been taken.

At the initial stage, company have opted for bank loan to initiate their business from the primary

level. When they were at the level of small business start up, company have raised amount

through bank loans.

Large business expansions – For the purpose of expansion by large operating firm, the

best source of raising capital is generating through share capital. Company has an

advantage of their past business performance and goodwill. Hence, by disclosing their

plan to public, companies could easily raise funds. They have to pay dividend to

shareholders which will be treated as cost to company.

Considering the company which has adopted all the sources of finance in different phase of

business, SONY could be considered. As they grew bigger, SONY became able to collect

amount out of their own earnings. The amount accumulated through retained earning have been

utilized for the purpose of large business expansion.

Acquiring medium sized company – When there are plans to acquire some other firms, the

ideal source of capital is retained earnings by individual person or organization

(Broadbent and Cullen, 2012). Although, it might affect the profitability of every firm,

but they will not get bounded under any kind of liabilities or debts.

They increased their scope of business and acquired a musical medium sized company and took

them into their name. For the purpose of performing acquisition, SONY have generated revenue

through share capital from public and increased their level of business.

Task 2

Raising finance for business

Finance for business can be raised by many sources as discussed earlier in the report.

Considering the different types of business such as new and old, large and small business entities

for the purpose of new business set-up and expansions, the sources of finance available are

internal and external sources. Internal sources includes retained earnings, personal savings, share

capital, selling of assets etc (Ittelson, 2009). Retained earnings are the part of last year revenue

which can be used for financing existing operations. Sale of assets is another option under which

they can sell old assets or assets which are available in spare (Siano, Kitchen and Confetto,

2010). Personal savings and funds from friends & relatives can also be poured into the new

business.

External sources of finance include debt, equity, bank loan, hire purchase etc. Debt

financing is related with issue of debenture capital in the market and let general public to invest

in business. It act as loan for the company. Equity financing is concerned with issue of equity

and preference share (Sources of finance. 2012). Bank loan can also be adopted for funding at

the confined rate of interest and after fulfillment of certain legal obligations. Hire purchasing is

another good option under which company can acquire the necessary asset at a particular time by

paying the price in installments.

Financial planning for new business

Starting of a new business requires lot of research and development activities to be

performed. It is also important to identify and evaluate the risk associated with every business

decision. The factors which are to be taken into consideration includes sources of funds,

resources, and location and legal aspects (Fridso and Alvarez, 2002). Financial planning helps in

eliminating the uncertainties related with the business. It helps in estimating the needed funds

and establishing the financial policies related with management of finances. It is needed to

perform budgeting activities and then objectives, programs, policies, budgets etc are placed.

them into their name. For the purpose of performing acquisition, SONY have generated revenue

through share capital from public and increased their level of business.

Task 2

Raising finance for business

Finance for business can be raised by many sources as discussed earlier in the report.

Considering the different types of business such as new and old, large and small business entities

for the purpose of new business set-up and expansions, the sources of finance available are

internal and external sources. Internal sources includes retained earnings, personal savings, share

capital, selling of assets etc (Ittelson, 2009). Retained earnings are the part of last year revenue

which can be used for financing existing operations. Sale of assets is another option under which

they can sell old assets or assets which are available in spare (Siano, Kitchen and Confetto,

2010). Personal savings and funds from friends & relatives can also be poured into the new

business.

External sources of finance include debt, equity, bank loan, hire purchase etc. Debt

financing is related with issue of debenture capital in the market and let general public to invest

in business. It act as loan for the company. Equity financing is concerned with issue of equity

and preference share (Sources of finance. 2012). Bank loan can also be adopted for funding at

the confined rate of interest and after fulfillment of certain legal obligations. Hire purchasing is

another good option under which company can acquire the necessary asset at a particular time by

paying the price in installments.

Financial planning for new business

Starting of a new business requires lot of research and development activities to be

performed. It is also important to identify and evaluate the risk associated with every business

decision. The factors which are to be taken into consideration includes sources of funds,

resources, and location and legal aspects (Fridso and Alvarez, 2002). Financial planning helps in

eliminating the uncertainties related with the business. It helps in estimating the needed funds

and establishing the financial policies related with management of finances. It is needed to

perform budgeting activities and then objectives, programs, policies, budgets etc are placed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial planning manages the cash outflow and cash inflow in order to achieve stability within

the business (McMenamin, 2002). It can identify appropriate sources of finance needed and the

ways to avail them. Company can effectively invest in profitable projects on the basis of use of

investment appraisal methods. Planning can tell about the distribution of funds to all the

resources within business.

Financial decision making

Financial department of an company generates lot of information which is helpful in

taking many decisions. Balance sheet, income statement and cash flow statement are the

documents which renders lot of data. These documents generates data related to expenses,

income, sales, costs, profits, dividend, assets, liabilities, capital etc (Neftci, 2004). These

information can be very useful to many people such as:

Customers – Customers need this information to know about the reputation & goodwill of the

company in them market.

Employees – Employees need this information to take decision about their survival and retention

within the organization. They can analyze whether they have a long career with the company or

not.

Government – Government needs this information to keep an eye on the business operations of

the firm (Beck Levin and Loayza, 2000). They want to make sure that it is following ethical

practices.

Suppliers – Suppliers checks the payment making ability of company on the basis of sales and

profits. They want to identify whether company is capable of making timely payments for goods

or not .

Shareholders – These people are interested in financial data because they want to check the

dividend paying ability of firm ( Bhowmik and Saha 2013). Obviously, shareholders

expects a high dividend on the shares which they purchased.

Sample of financial statements

Income statement

Revenue:

the business (McMenamin, 2002). It can identify appropriate sources of finance needed and the

ways to avail them. Company can effectively invest in profitable projects on the basis of use of

investment appraisal methods. Planning can tell about the distribution of funds to all the

resources within business.

Financial decision making

Financial department of an company generates lot of information which is helpful in

taking many decisions. Balance sheet, income statement and cash flow statement are the

documents which renders lot of data. These documents generates data related to expenses,

income, sales, costs, profits, dividend, assets, liabilities, capital etc (Neftci, 2004). These

information can be very useful to many people such as:

Customers – Customers need this information to know about the reputation & goodwill of the

company in them market.

Employees – Employees need this information to take decision about their survival and retention

within the organization. They can analyze whether they have a long career with the company or

not.

Government – Government needs this information to keep an eye on the business operations of

the firm (Beck Levin and Loayza, 2000). They want to make sure that it is following ethical

practices.

Suppliers – Suppliers checks the payment making ability of company on the basis of sales and

profits. They want to identify whether company is capable of making timely payments for goods

or not .

Shareholders – These people are interested in financial data because they want to check the

dividend paying ability of firm ( Bhowmik and Saha 2013). Obviously, shareholders

expects a high dividend on the shares which they purchased.

Sample of financial statements

Income statement

Revenue:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross Sales

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss):

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Balance sheet

Liabilities Amount Assets Amount

Current Liabilities

Creditors

Bills Payable

Bank Overdraft

Fixed Liabilities

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

Total Current Assets

Fixed Assets

Machinery & Equipments

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Less : Sales Returns / Allowance

Net Sales

Cost of Goods Sold:

Purchases

Delivery Charges

Cost of goods sold

Gross sales profit (Loss)

Expenses:

Expenses 1

Expenses 2

Expenses 3

Total Expenses:

Net Operating Income

Other Income:

Income 1

Income 2

Income 3

Total Other Income:

Net Income (Loss):

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Balance sheet

Liabilities Amount Assets Amount

Current Liabilities

Creditors

Bills Payable

Bank Overdraft

Fixed Liabilities

Bank Loan

Secured Loan

Other long term Loan

Capital and Net Profit

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Current Assets

Cash in bank

Accounts receivable

Inventory

Prepaid Expenses

Other Current Assets

Total Current Assets

Fixed Assets

Machinery & Equipments

Furniture & Fixtures

Leasehold Improvements

Land & Buildings

Other Fixed Assets (Less

Accumulated

depreciation)

Total Fixed Assets

Other Assets

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

XXXX.XX

Intangibles

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

•Retained earnings – It will have an impact on profit & loss account. The retained surplus under

the balance sheet will decrease. The transaction will be recorded under the heading “cash flow

from operating activities” in the cash flow statement

•Share capital – It will increase the liability side under the balance sheet. The event will be

recorded under the “cash flow from financing activities: in the cash flow statement.

•Bank loan - It will increase the liability side under the balance sheet. The transaction will be

recorded under the “cash flow from financing activities: in the cash flow statement.

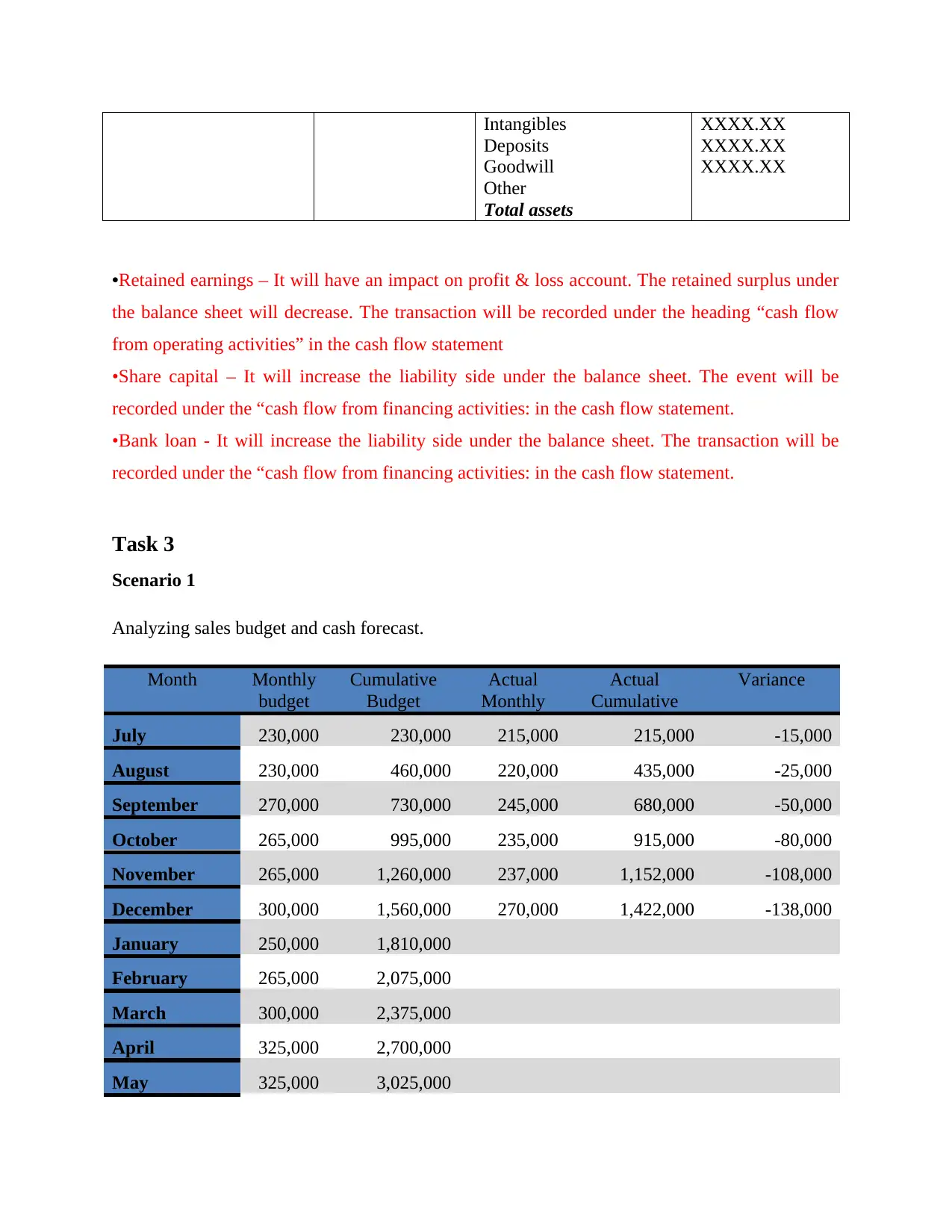

Task 3

Scenario 1

Analyzing sales budget and cash forecast.

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 230,000 230,000 215,000 215,000 -15,000

August 230,000 460,000 220,000 435,000 -25,000

September 270,000 730,000 245,000 680,000 -50,000

October 265,000 995,000 235,000 915,000 -80,000

November 265,000 1,260,000 237,000 1,152,000 -108,000

December 300,000 1,560,000 270,000 1,422,000 -138,000

January 250,000 1,810,000

February 265,000 2,075,000

March 300,000 2,375,000

April 325,000 2,700,000

May 325,000 3,025,000

Deposits

Goodwill

Other

Total assets

XXXX.XX

XXXX.XX

XXXX.XX

•Retained earnings – It will have an impact on profit & loss account. The retained surplus under

the balance sheet will decrease. The transaction will be recorded under the heading “cash flow

from operating activities” in the cash flow statement

•Share capital – It will increase the liability side under the balance sheet. The event will be

recorded under the “cash flow from financing activities: in the cash flow statement.

•Bank loan - It will increase the liability side under the balance sheet. The transaction will be

recorded under the “cash flow from financing activities: in the cash flow statement.

Task 3

Scenario 1

Analyzing sales budget and cash forecast.

Month Monthly

budget

Cumulative

Budget

Actual

Monthly

Actual

Cumulative

Variance

July 230,000 230,000 215,000 215,000 -15,000

August 230,000 460,000 220,000 435,000 -25,000

September 270,000 730,000 245,000 680,000 -50,000

October 265,000 995,000 235,000 915,000 -80,000

November 265,000 1,260,000 237,000 1,152,000 -108,000

December 300,000 1,560,000 270,000 1,422,000 -138,000

January 250,000 1,810,000

February 265,000 2,075,000

March 300,000 2,375,000

April 325,000 2,700,000

May 325,000 3,025,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

June 350,000 3,375,000

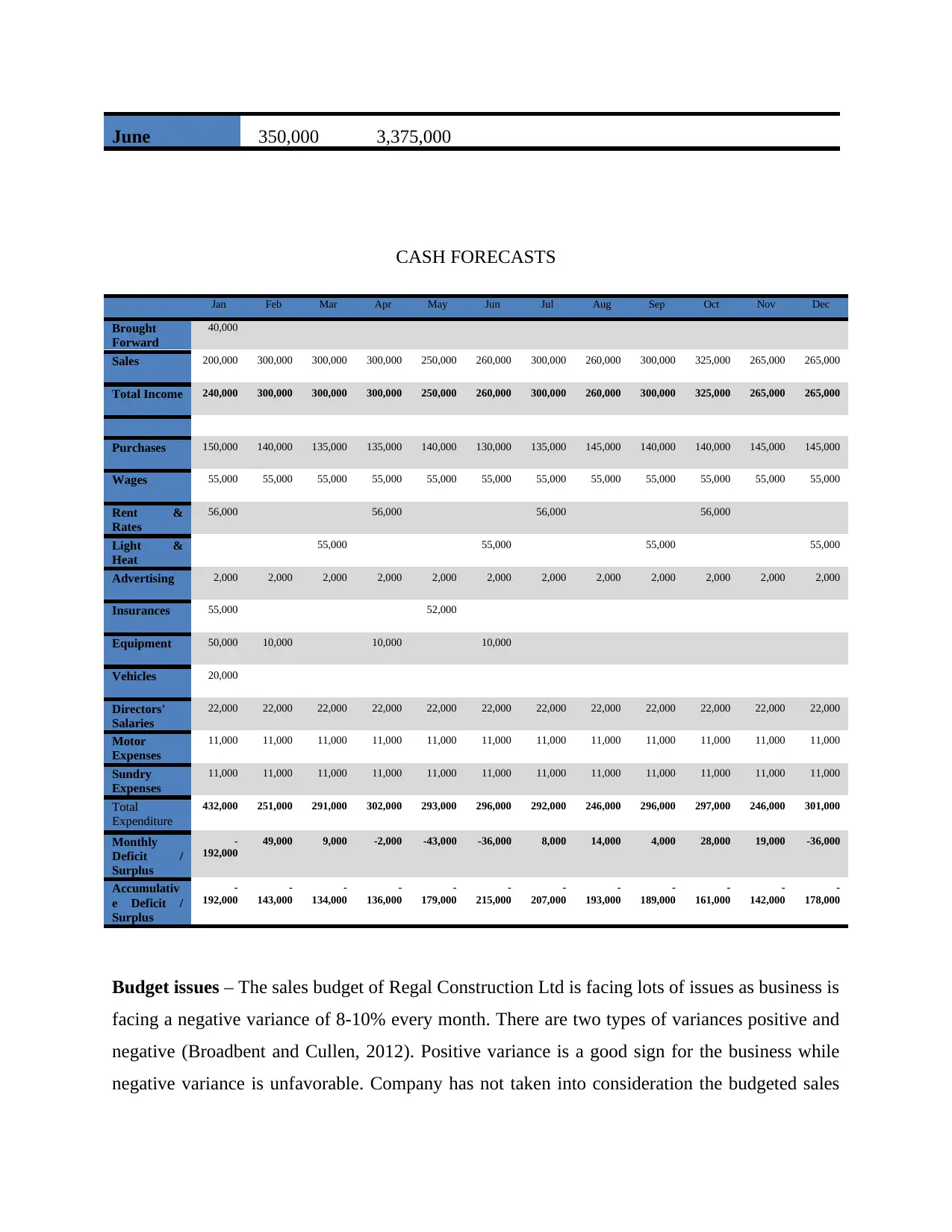

CASH FORECASTS

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brought

Forward

40,000

Sales 200,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Total Income 240,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Purchases 150,000 140,000 135,000 135,000 140,000 130,000 135,000 145,000 140,000 140,000 145,000 145,000

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

Equipment 50,000 10,000 10,000 10,000

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,000 251,000 291,000 302,000 293,000 296,000 292,000 246,000 296,000 297,000 246,000 301,000

Monthly

Deficit /

Surplus

-

192,000

49,000 9,000 -2,000 -43,000 -36,000 8,000 14,000 4,000 28,000 19,000 -36,000

Accumulativ

e Deficit /

Surplus

-

192,000

-

143,000

-

134,000

-

136,000

-

179,000

-

215,000

-

207,000

-

193,000

-

189,000

-

161,000

-

142,000

-

178,000

Budget issues – The sales budget of Regal Construction Ltd is facing lots of issues as business is

facing a negative variance of 8-10% every month. There are two types of variances positive and

negative (Broadbent and Cullen, 2012). Positive variance is a good sign for the business while

negative variance is unfavorable. Company has not taken into consideration the budgeted sales

CASH FORECASTS

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Brought

Forward

40,000

Sales 200,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Total Income 240,000 300,000 300,000 300,000 250,000 260,000 300,000 260,000 300,000 325,000 265,000 265,000

Purchases 150,000 140,000 135,000 135,000 140,000 130,000 135,000 145,000 140,000 140,000 145,000 145,000

Wages 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000 55,000

Rent &

Rates

56,000 56,000 56,000 56,000

Light &

Heat

55,000 55,000 55,000 55,000

Advertising 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000

Insurances 55,000 52,000

Equipment 50,000 10,000 10,000 10,000

Vehicles 20,000

Directors'

Salaries

22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000 22,000

Motor

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Sundry

Expenses

11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000 11,000

Total

Expenditure

432,000 251,000 291,000 302,000 293,000 296,000 292,000 246,000 296,000 297,000 246,000 301,000

Monthly

Deficit /

Surplus

-

192,000

49,000 9,000 -2,000 -43,000 -36,000 8,000 14,000 4,000 28,000 19,000 -36,000

Accumulativ

e Deficit /

Surplus

-

192,000

-

143,000

-

134,000

-

136,000

-

179,000

-

215,000

-

207,000

-

193,000

-

189,000

-

161,000

-

142,000

-

178,000

Budget issues – The sales budget of Regal Construction Ltd is facing lots of issues as business is

facing a negative variance of 8-10% every month. There are two types of variances positive and

negative (Broadbent and Cullen, 2012). Positive variance is a good sign for the business while

negative variance is unfavorable. Company has not taken into consideration the budgeted sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

figure while preparing the cash flow forecasts. Accumulate deficit can be seen which shows that

they have incurred extra expenses which are required to be minimized.

Cause of the budget – There can be several reasons for these variances in budget. Market is

always surrounded with unpredictable shifts. Plans prepared for business may have reflected in

contrast from which was estimated. Poor planning and estimations can also be the cause for it.

Estimation of prices was not done correctly due to which sales aroused at different prices from

what was planned (Brigham and Ehrhardt, 2011). Failure of business strategies can also be the

cause for variances. Liquidity position of the company may be affected due to bad results in cash

flow forecasts. Further there can be an impact on its operational affairs.

Recommendations – Company need to focus on effective sales strategies which can increase

their sales. It also needs to follow an appropriate pricing strategy taking into consideration the

prices from competitors. A suitable budgeting technique is to be applied suitable to their business

operations. Further business can adopt an appropriate costing system. For company like Regal

Construction Ltd, process costing system can be more suitable. Deficits can be improved by

employing a skilled workforce, which has the potential to make hard efforts. All resources are to

be utilized effectively avoiding any kind of wastage. Further there is a need to do correct

estimation of expenses and income. For that purpose, analysis of marketing trends is very

essential.

Scenario 2

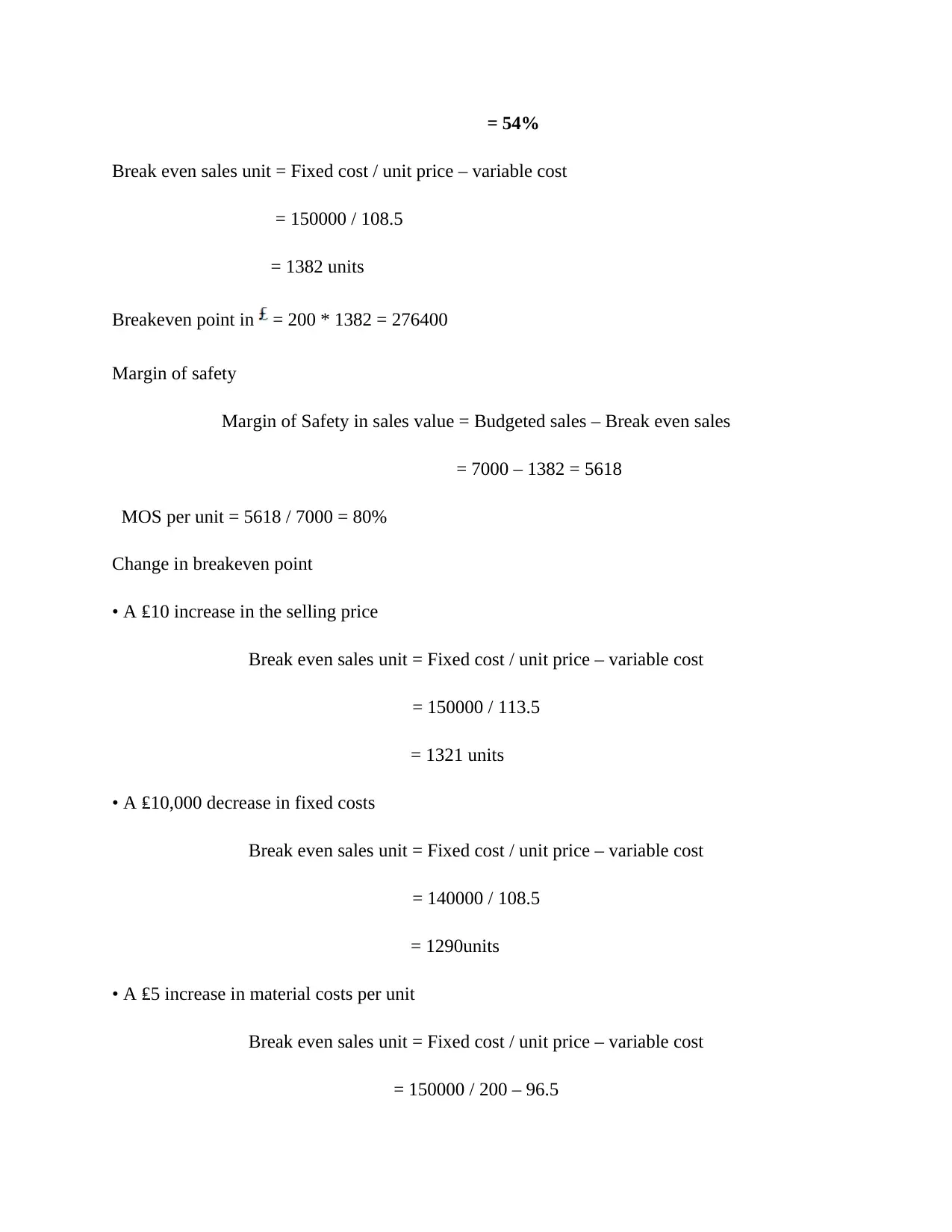

Performance of machine A

For machine A

Variable cost per unit=50.50+30.75+10.25

Variable cost per unit=£ 91.5

Unit CM=200 – 91.5 = 108.5

Unit CM = 108.5

Contribution per unit = 108.5 / 200 = 0.54

they have incurred extra expenses which are required to be minimized.

Cause of the budget – There can be several reasons for these variances in budget. Market is

always surrounded with unpredictable shifts. Plans prepared for business may have reflected in

contrast from which was estimated. Poor planning and estimations can also be the cause for it.

Estimation of prices was not done correctly due to which sales aroused at different prices from

what was planned (Brigham and Ehrhardt, 2011). Failure of business strategies can also be the

cause for variances. Liquidity position of the company may be affected due to bad results in cash

flow forecasts. Further there can be an impact on its operational affairs.

Recommendations – Company need to focus on effective sales strategies which can increase

their sales. It also needs to follow an appropriate pricing strategy taking into consideration the

prices from competitors. A suitable budgeting technique is to be applied suitable to their business

operations. Further business can adopt an appropriate costing system. For company like Regal

Construction Ltd, process costing system can be more suitable. Deficits can be improved by

employing a skilled workforce, which has the potential to make hard efforts. All resources are to

be utilized effectively avoiding any kind of wastage. Further there is a need to do correct

estimation of expenses and income. For that purpose, analysis of marketing trends is very

essential.

Scenario 2

Performance of machine A

For machine A

Variable cost per unit=50.50+30.75+10.25

Variable cost per unit=£ 91.5

Unit CM=200 – 91.5 = 108.5

Unit CM = 108.5

Contribution per unit = 108.5 / 200 = 0.54

= 54%

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 108.5

= 1382 units

Breakeven point in = 200 * 1382 = 276400

Margin of safety

Margin of Safety in sales value = Budgeted sales – Break even sales

= 7000 – 1382 = 5618

MOS per unit = 5618 / 7000 = 80%

Change in breakeven point

• A ₤10 increase in the selling price

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 113.5

= 1321 units

• A ₤10,000 decrease in fixed costs

Break even sales unit = Fixed cost / unit price – variable cost

= 140000 / 108.5

= 1290units

• A ₤5 increase in material costs per unit

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 200 – 96.5

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 108.5

= 1382 units

Breakeven point in = 200 * 1382 = 276400

Margin of safety

Margin of Safety in sales value = Budgeted sales – Break even sales

= 7000 – 1382 = 5618

MOS per unit = 5618 / 7000 = 80%

Change in breakeven point

• A ₤10 increase in the selling price

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 113.5

= 1321 units

• A ₤10,000 decrease in fixed costs

Break even sales unit = Fixed cost / unit price – variable cost

= 140000 / 108.5

= 1290units

• A ₤5 increase in material costs per unit

Break even sales unit = Fixed cost / unit price – variable cost

= 150000 / 200 – 96.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.