Financial Resource Management Report - Analysis and Ratios

VerifiedAdded on 2020/10/22

|12

|3100

|444

Report

AI Summary

This report evaluates the financial performance of two companies, Debrun and McGill, using ratio analysis. It calculates and interprets various financial ratios such as gross profit margin, return on capital employed, return on equity, inventory turnover, and accounts receivable/payable collection periods. The analysis compares the performance of the two companies, offering recommendations to Dipapa regarding investment decisions and the acceptance or rejection of a job quotation. The report also includes a job cost card preparation for Job No. 21, calculating direct material, direct labor, direct expenses, and overhead costs to determine the total production cost and ultimately, the price of the job. The conclusion summarizes the key findings and recommendations based on the financial analysis.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

a. Computing the following ratios...............................................................................................1

b. Recommendation.....................................................................................................................5

TASK 2............................................................................................................................................6

a) preparation of Job cost card for Job No. 21.............................................................................6

Interpretation:...................................................................................................................................7

b) Advising finance manger of on acceptance or rejection of quote sent by the consumer for

above job......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

a. Computing the following ratios...............................................................................................1

b. Recommendation.....................................................................................................................5

TASK 2............................................................................................................................................6

a) preparation of Job cost card for Job No. 21.............................................................................6

Interpretation:...................................................................................................................................7

b) Advising finance manger of on acceptance or rejection of quote sent by the consumer for

above job......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

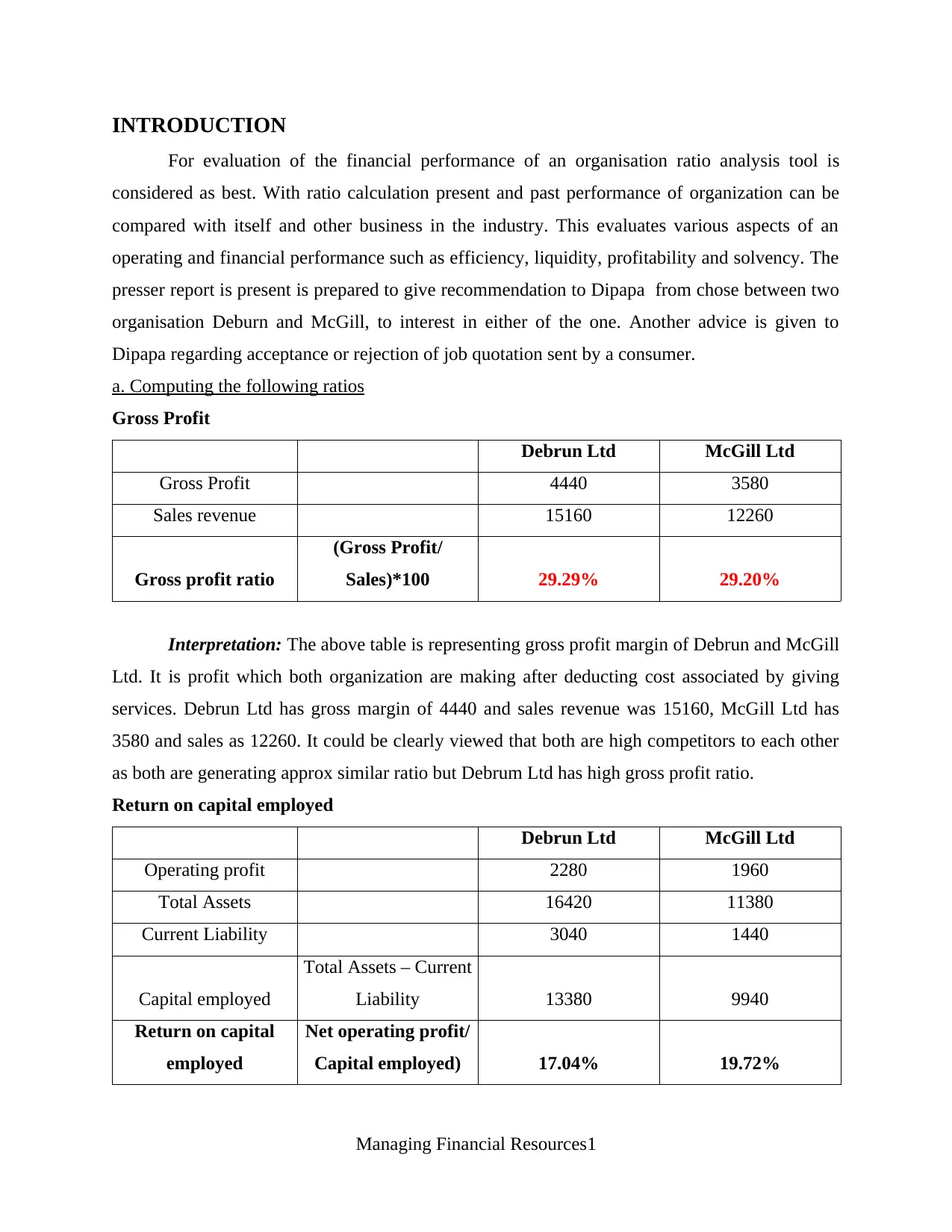

INTRODUCTION

For evaluation of the financial performance of an organisation ratio analysis tool is

considered as best. With ratio calculation present and past performance of organization can be

compared with itself and other business in the industry. This evaluates various aspects of an

operating and financial performance such as efficiency, liquidity, profitability and solvency. The

presser report is present is prepared to give recommendation to Dipapa from chose between two

organisation Deburn and McGill, to interest in either of the one. Another advice is given to

Dipapa regarding acceptance or rejection of job quotation sent by a consumer.

a. Computing the following ratios

Gross Profit

Debrun Ltd McGill Ltd

Gross Profit 4440 3580

Sales revenue 15160 12260

Gross profit ratio

(Gross Profit/

Sales)*100 29.29% 29.20%

Interpretation: The above table is representing gross profit margin of Debrun and McGill

Ltd. It is profit which both organization are making after deducting cost associated by giving

services. Debrun Ltd has gross margin of 4440 and sales revenue was 15160, McGill Ltd has

3580 and sales as 12260. It could be clearly viewed that both are high competitors to each other

as both are generating approx similar ratio but Debrum Ltd has high gross profit ratio.

Return on capital employed

Debrun Ltd McGill Ltd

Operating profit 2280 1960

Total Assets 16420 11380

Current Liability 3040 1440

Capital employed

Total Assets – Current

Liability 13380 9940

Return on capital

employed

Net operating profit/

Capital employed) 17.04% 19.72%

Managing Financial Resources1

For evaluation of the financial performance of an organisation ratio analysis tool is

considered as best. With ratio calculation present and past performance of organization can be

compared with itself and other business in the industry. This evaluates various aspects of an

operating and financial performance such as efficiency, liquidity, profitability and solvency. The

presser report is present is prepared to give recommendation to Dipapa from chose between two

organisation Deburn and McGill, to interest in either of the one. Another advice is given to

Dipapa regarding acceptance or rejection of job quotation sent by a consumer.

a. Computing the following ratios

Gross Profit

Debrun Ltd McGill Ltd

Gross Profit 4440 3580

Sales revenue 15160 12260

Gross profit ratio

(Gross Profit/

Sales)*100 29.29% 29.20%

Interpretation: The above table is representing gross profit margin of Debrun and McGill

Ltd. It is profit which both organization are making after deducting cost associated by giving

services. Debrun Ltd has gross margin of 4440 and sales revenue was 15160, McGill Ltd has

3580 and sales as 12260. It could be clearly viewed that both are high competitors to each other

as both are generating approx similar ratio but Debrum Ltd has high gross profit ratio.

Return on capital employed

Debrun Ltd McGill Ltd

Operating profit 2280 1960

Total Assets 16420 11380

Current Liability 3040 1440

Capital employed

Total Assets – Current

Liability 13380 9940

Return on capital

employed

Net operating profit/

Capital employed) 17.04% 19.72%

Managing Financial Resources1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: It is comprised in financial ratio which helps in measuring profitability of

business entity along with efficiency through employed capital. It is extracted through dividing

operating profit by capital employed. The operating profit of Debrun and McGill is 2280 and

1960 where Debrun Ltd is leading. In the similar aspect, total assets and current liability both are

higher, but high current liability is giving negative impact on return on capital employed. McGill

Ltd has high returns as compared to Debrun Ltd.

Return on equity

Debrun Ltd McGill Ltd

Profit after tax 1320 1440

Equity share capital 9880 9440

Net worth

equity share capital +

Reserves and surplus 9880 9440

Return on Equity

Profit after tax/ Net

worth 13.36% 15.25%

Interpretation: It is referred as measure of financial performance which is extracted by

dividing net income with shareholder's equity. McGill is generating high margin but net worth is

less from Debrun Ltd. McGill is producing 15.25% return by comparing to money invested by

shareholder (Return on Equity, 2018).

Inventory turnover

Particulars Formula DeBrun Ltd McGrill Ltd

Cost of goods sold

(COGS)

10720 8680

Average inventory 1580 1260

Stock turnover ratio Closing stock / cost

of sales * 365

1580 / 10720 * 365 =

54 days

1260 / 8680 * 365 =

53 days

Interpretation: It is considered as appropriate measure of time of selling inventory and

transform in liquid aspect. Debrun Ltd can sold its inventory in 54 days and McGill in 53 days.

Hence, there is cut throat competition among them and McGill Ltd is leading.

Accounts Receivable Collection period

Debrun Ltd McGill Ltd

Accounts receivable 1720 1360

Managing Financial Resources2

business entity along with efficiency through employed capital. It is extracted through dividing

operating profit by capital employed. The operating profit of Debrun and McGill is 2280 and

1960 where Debrun Ltd is leading. In the similar aspect, total assets and current liability both are

higher, but high current liability is giving negative impact on return on capital employed. McGill

Ltd has high returns as compared to Debrun Ltd.

Return on equity

Debrun Ltd McGill Ltd

Profit after tax 1320 1440

Equity share capital 9880 9440

Net worth

equity share capital +

Reserves and surplus 9880 9440

Return on Equity

Profit after tax/ Net

worth 13.36% 15.25%

Interpretation: It is referred as measure of financial performance which is extracted by

dividing net income with shareholder's equity. McGill is generating high margin but net worth is

less from Debrun Ltd. McGill is producing 15.25% return by comparing to money invested by

shareholder (Return on Equity, 2018).

Inventory turnover

Particulars Formula DeBrun Ltd McGrill Ltd

Cost of goods sold

(COGS)

10720 8680

Average inventory 1580 1260

Stock turnover ratio Closing stock / cost

of sales * 365

1580 / 10720 * 365 =

54 days

1260 / 8680 * 365 =

53 days

Interpretation: It is considered as appropriate measure of time of selling inventory and

transform in liquid aspect. Debrun Ltd can sold its inventory in 54 days and McGill in 53 days.

Hence, there is cut throat competition among them and McGill Ltd is leading.

Accounts Receivable Collection period

Debrun Ltd McGill Ltd

Accounts receivable 1720 1360

Managing Financial Resources2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

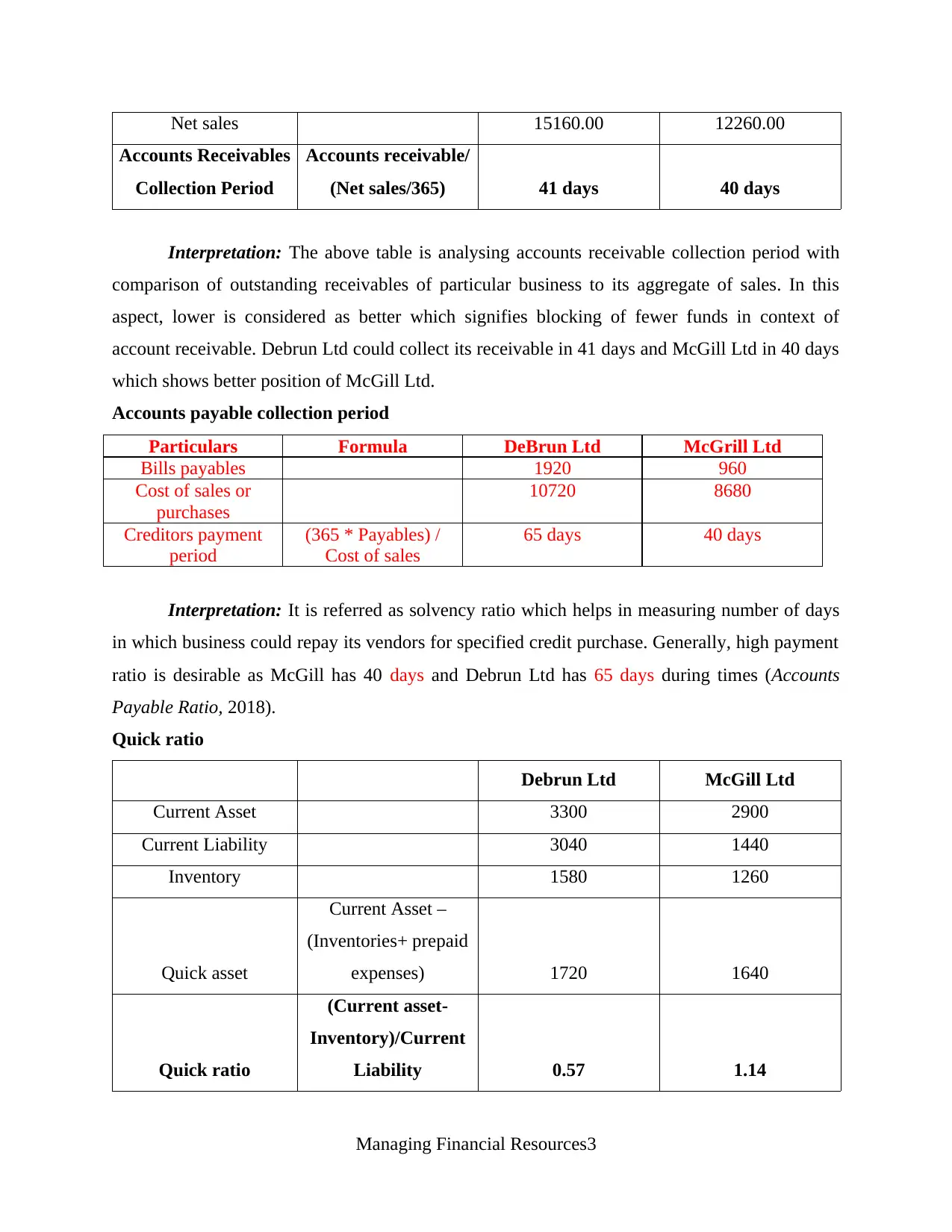

Net sales 15160.00 12260.00

Accounts Receivables

Collection Period

Accounts receivable/

(Net sales/365) 41 days 40 days

Interpretation: The above table is analysing accounts receivable collection period with

comparison of outstanding receivables of particular business to its aggregate of sales. In this

aspect, lower is considered as better which signifies blocking of fewer funds in context of

account receivable. Debrun Ltd could collect its receivable in 41 days and McGill Ltd in 40 days

which shows better position of McGill Ltd.

Accounts payable collection period

Particulars Formula DeBrun Ltd McGrill Ltd

Bills payables 1920 960

Cost of sales or

purchases

10720 8680

Creditors payment

period

(365 * Payables) /

Cost of sales

65 days 40 days

Interpretation: It is referred as solvency ratio which helps in measuring number of days

in which business could repay its vendors for specified credit purchase. Generally, high payment

ratio is desirable as McGill has 40 days and Debrun Ltd has 65 days during times (Accounts

Payable Ratio, 2018).

Quick ratio

Debrun Ltd McGill Ltd

Current Asset 3300 2900

Current Liability 3040 1440

Inventory 1580 1260

Quick asset

Current Asset –

(Inventories+ prepaid

expenses) 1720 1640

Quick ratio

(Current asset-

Inventory)/Current

Liability 0.57 1.14

Managing Financial Resources3

Accounts Receivables

Collection Period

Accounts receivable/

(Net sales/365) 41 days 40 days

Interpretation: The above table is analysing accounts receivable collection period with

comparison of outstanding receivables of particular business to its aggregate of sales. In this

aspect, lower is considered as better which signifies blocking of fewer funds in context of

account receivable. Debrun Ltd could collect its receivable in 41 days and McGill Ltd in 40 days

which shows better position of McGill Ltd.

Accounts payable collection period

Particulars Formula DeBrun Ltd McGrill Ltd

Bills payables 1920 960

Cost of sales or

purchases

10720 8680

Creditors payment

period

(365 * Payables) /

Cost of sales

65 days 40 days

Interpretation: It is referred as solvency ratio which helps in measuring number of days

in which business could repay its vendors for specified credit purchase. Generally, high payment

ratio is desirable as McGill has 40 days and Debrun Ltd has 65 days during times (Accounts

Payable Ratio, 2018).

Quick ratio

Debrun Ltd McGill Ltd

Current Asset 3300 2900

Current Liability 3040 1440

Inventory 1580 1260

Quick asset

Current Asset –

(Inventories+ prepaid

expenses) 1720 1640

Quick ratio

(Current asset-

Inventory)/Current

Liability 0.57 1.14

Managing Financial Resources3

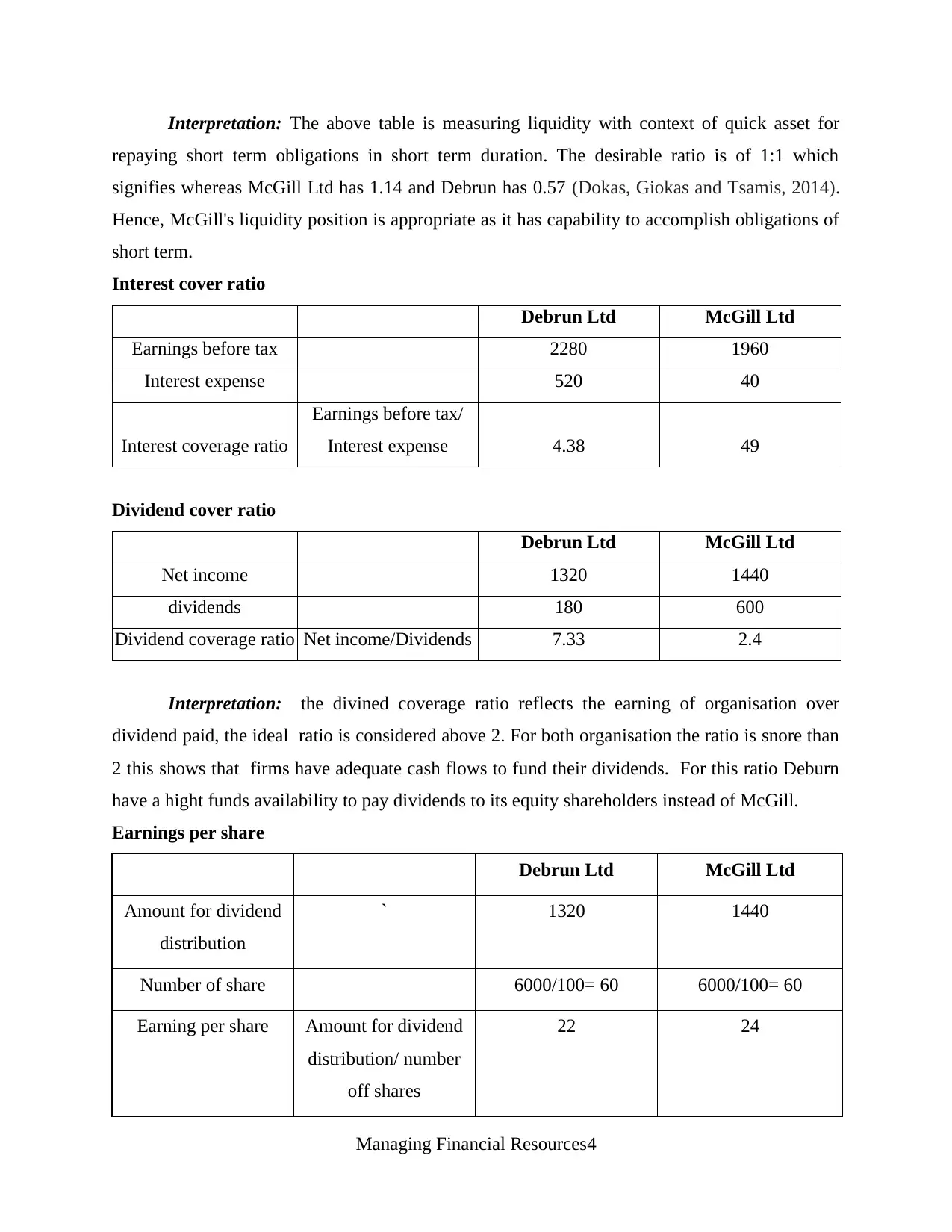

Interpretation: The above table is measuring liquidity with context of quick asset for

repaying short term obligations in short term duration. The desirable ratio is of 1:1 which

signifies whereas McGill Ltd has 1.14 and Debrun has 0.57 (Dokas, Giokas and Tsamis, 2014).

Hence, McGill's liquidity position is appropriate as it has capability to accomplish obligations of

short term.

Interest cover ratio

Debrun Ltd McGill Ltd

Earnings before tax 2280 1960

Interest expense 520 40

Interest coverage ratio

Earnings before tax/

Interest expense 4.38 49

Dividend cover ratio

Debrun Ltd McGill Ltd

Net income 1320 1440

dividends 180 600

Dividend coverage ratio Net income/Dividends 7.33 2.4

Interpretation: the divined coverage ratio reflects the earning of organisation over

dividend paid, the ideal ratio is considered above 2. For both organisation the ratio is snore than

2 this shows that firms have adequate cash flows to fund their dividends. For this ratio Deburn

have a hight funds availability to pay dividends to its equity shareholders instead of McGill.

Earnings per share

Debrun Ltd McGill Ltd

Amount for dividend

distribution

` 1320 1440

Number of share 6000/100= 60 6000/100= 60

Earning per share Amount for dividend

distribution/ number

off shares

22 24

Managing Financial Resources4

repaying short term obligations in short term duration. The desirable ratio is of 1:1 which

signifies whereas McGill Ltd has 1.14 and Debrun has 0.57 (Dokas, Giokas and Tsamis, 2014).

Hence, McGill's liquidity position is appropriate as it has capability to accomplish obligations of

short term.

Interest cover ratio

Debrun Ltd McGill Ltd

Earnings before tax 2280 1960

Interest expense 520 40

Interest coverage ratio

Earnings before tax/

Interest expense 4.38 49

Dividend cover ratio

Debrun Ltd McGill Ltd

Net income 1320 1440

dividends 180 600

Dividend coverage ratio Net income/Dividends 7.33 2.4

Interpretation: the divined coverage ratio reflects the earning of organisation over

dividend paid, the ideal ratio is considered above 2. For both organisation the ratio is snore than

2 this shows that firms have adequate cash flows to fund their dividends. For this ratio Deburn

have a hight funds availability to pay dividends to its equity shareholders instead of McGill.

Earnings per share

Debrun Ltd McGill Ltd

Amount for dividend

distribution

` 1320 1440

Number of share 6000/100= 60 6000/100= 60

Earning per share Amount for dividend

distribution/ number

off shares

22 24

Managing Financial Resources4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Both the firms are in a cut throat competition as this can be seen from the

above table that with same profitability states with minor changes both firms are giving same

earning on their share with a difference of 2 only. The different is not bid there is not a big

difference between net profits after tax of both organisation. McGill has this ratio above 1 while

Debrun's ratio is less than 1.

Performance evaluation:

On the basis of ratio analysis:

The probability ratios calculated here are gross profits margin, return on capital

employer and return on equity, this relation reflects that how much incomes is earned by an

organisation overs its sales, capital employed and for shares. The ROCE and ROE are better for

McGill and Gross profit margin are same for both the firms.

Solvency ratio calculates here is quick ratios which defines the ability of a firm to meet

its immediate current liabilities. An ideas ration is considered as 1:1. this reflects position of

the firms to meet the cash requirement in near future which is good for McGill as it have more

current assets than its current liabilities.

Other ratios calculated are turnover ratios and valuation ratios. With turnover time

frame of flow of cash payable and receivable and holding times of inventory from stock to

production and final product from warehouse to sales is determined (Enekwe, 2015). this is

good in McGill as it hold inventory for less time, gives debtor lesser time to repay and take more

time to pay to vendors.

From the valuation ratio of interest and dividend coverage and earning per share the

value of firm is determined in perspective of dividend and interest covered from profits of firm.

The interest covered and earning per shares are better in McGill but dividend coverage ratio is

good in Deburn.

Overall performance of the organisations

From the above detailed evaluation of the financial performance of the firms this can be

interpreted that McGill;s performance is excellence in every perceptive be it profitability,

solvency or valuation of shares (Omar and et.al., 2014). Rather, Deburns have good command

over profits and dividend coverage. Among both firms McGill's capital structure have lesser debt

as compared to Deburn.

Managing Financial Resources5

above table that with same profitability states with minor changes both firms are giving same

earning on their share with a difference of 2 only. The different is not bid there is not a big

difference between net profits after tax of both organisation. McGill has this ratio above 1 while

Debrun's ratio is less than 1.

Performance evaluation:

On the basis of ratio analysis:

The probability ratios calculated here are gross profits margin, return on capital

employer and return on equity, this relation reflects that how much incomes is earned by an

organisation overs its sales, capital employed and for shares. The ROCE and ROE are better for

McGill and Gross profit margin are same for both the firms.

Solvency ratio calculates here is quick ratios which defines the ability of a firm to meet

its immediate current liabilities. An ideas ration is considered as 1:1. this reflects position of

the firms to meet the cash requirement in near future which is good for McGill as it have more

current assets than its current liabilities.

Other ratios calculated are turnover ratios and valuation ratios. With turnover time

frame of flow of cash payable and receivable and holding times of inventory from stock to

production and final product from warehouse to sales is determined (Enekwe, 2015). this is

good in McGill as it hold inventory for less time, gives debtor lesser time to repay and take more

time to pay to vendors.

From the valuation ratio of interest and dividend coverage and earning per share the

value of firm is determined in perspective of dividend and interest covered from profits of firm.

The interest covered and earning per shares are better in McGill but dividend coverage ratio is

good in Deburn.

Overall performance of the organisations

From the above detailed evaluation of the financial performance of the firms this can be

interpreted that McGill;s performance is excellence in every perceptive be it profitability,

solvency or valuation of shares (Omar and et.al., 2014). Rather, Deburns have good command

over profits and dividend coverage. Among both firms McGill's capital structure have lesser debt

as compared to Deburn.

Managing Financial Resources5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

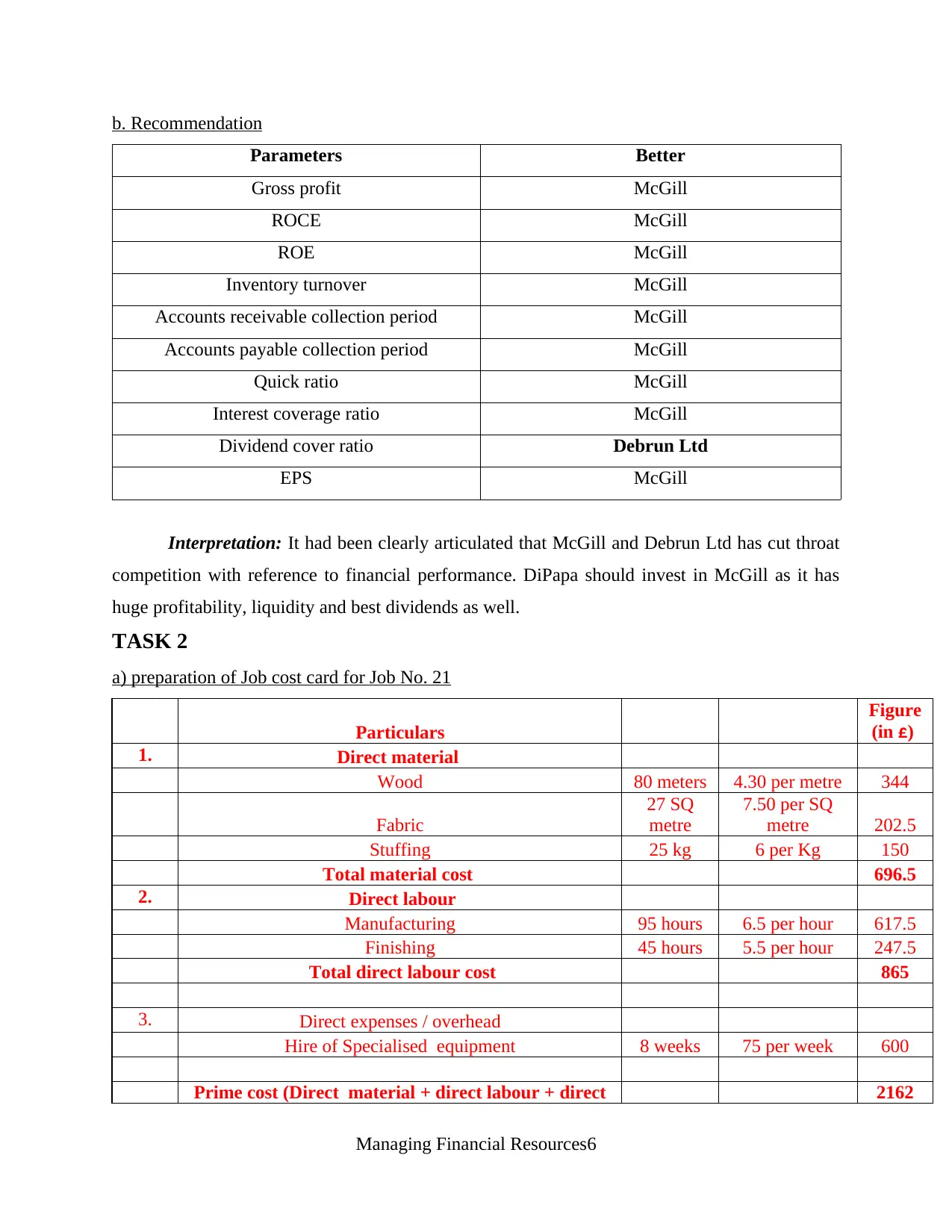

b. Recommendation

Parameters Better

Gross profit McGill

ROCE McGill

ROE McGill

Inventory turnover McGill

Accounts receivable collection period McGill

Accounts payable collection period McGill

Quick ratio McGill

Interest coverage ratio McGill

Dividend cover ratio Debrun Ltd

EPS McGill

Interpretation: It had been clearly articulated that McGill and Debrun Ltd has cut throat

competition with reference to financial performance. DiPapa should invest in McGill as it has

huge profitability, liquidity and best dividends as well.

TASK 2

a) preparation of Job cost card for Job No. 21

Particulars

Figure

(in £)

1. Direct material

Wood 80 meters 4.30 per metre 344

Fabric

27 SQ

metre

7.50 per SQ

metre 202.5

Stuffing 25 kg 6 per Kg 150

Total material cost 696.5

2. Direct labour

Manufacturing 95 hours 6.5 per hour 617.5

Finishing 45 hours 5.5 per hour 247.5

Total direct labour cost 865

3. Direct expenses / overhead

Hire of Specialised equipment 8 weeks 75 per week 600

Prime cost (Direct material + direct labour + direct 2162

Managing Financial Resources6

Parameters Better

Gross profit McGill

ROCE McGill

ROE McGill

Inventory turnover McGill

Accounts receivable collection period McGill

Accounts payable collection period McGill

Quick ratio McGill

Interest coverage ratio McGill

Dividend cover ratio Debrun Ltd

EPS McGill

Interpretation: It had been clearly articulated that McGill and Debrun Ltd has cut throat

competition with reference to financial performance. DiPapa should invest in McGill as it has

huge profitability, liquidity and best dividends as well.

TASK 2

a) preparation of Job cost card for Job No. 21

Particulars

Figure

(in £)

1. Direct material

Wood 80 meters 4.30 per metre 344

Fabric

27 SQ

metre

7.50 per SQ

metre 202.5

Stuffing 25 kg 6 per Kg 150

Total material cost 696.5

2. Direct labour

Manufacturing 95 hours 6.5 per hour 617.5

Finishing 45 hours 5.5 per hour 247.5

Total direct labour cost 865

3. Direct expenses / overhead

Hire of Specialised equipment 8 weeks 75 per week 600

Prime cost (Direct material + direct labour + direct 2162

Managing Financial Resources6

expenditure)

Add: Factory overhead (20% of direct labour cost) 173

Total production cost (material + labour + specialised

equipment cost + factory overhead) 2335

Non-production expenditure

5. Administration overhead (15% of production cost) 350

6.

Selling and distribution overhead (12.5% of prime

cost )

27Man

aging

Financi

al

Resour

ces0

Total cost (material + labour + equipment +factory

overhead + S&D expenses + administration overhead) 2955

Profit margin 12.50%

Price

[cost + (cost * profit margin) 3324

Additional calculation:

1. Calculation of total cost of direct material:

Material Units Rate per unit Amount in £

Wood 80 meters 4.3 per meters 344

Fabric 27 sq meter

7.5 per sq

meter 202.5

Stuffing 25 kg 6 per kg 150

Total 696.5

2. Calculation of total cost of direct labor:

Labor Hours per week

Rate per

week Amount in £

Manufacturing 95 6.5 617.5

Finishing 45 5.5 247.5

Managing Financial Resources7

Add: Factory overhead (20% of direct labour cost) 173

Total production cost (material + labour + specialised

equipment cost + factory overhead) 2335

Non-production expenditure

5. Administration overhead (15% of production cost) 350

6.

Selling and distribution overhead (12.5% of prime

cost )

27Man

aging

Financi

al

Resour

ces0

Total cost (material + labour + equipment +factory

overhead + S&D expenses + administration overhead) 2955

Profit margin 12.50%

Price

[cost + (cost * profit margin) 3324

Additional calculation:

1. Calculation of total cost of direct material:

Material Units Rate per unit Amount in £

Wood 80 meters 4.3 per meters 344

Fabric 27 sq meter

7.5 per sq

meter 202.5

Stuffing 25 kg 6 per kg 150

Total 696.5

2. Calculation of total cost of direct labor:

Labor Hours per week

Rate per

week Amount in £

Manufacturing 95 6.5 617.5

Finishing 45 5.5 247.5

Managing Financial Resources7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total 140 865

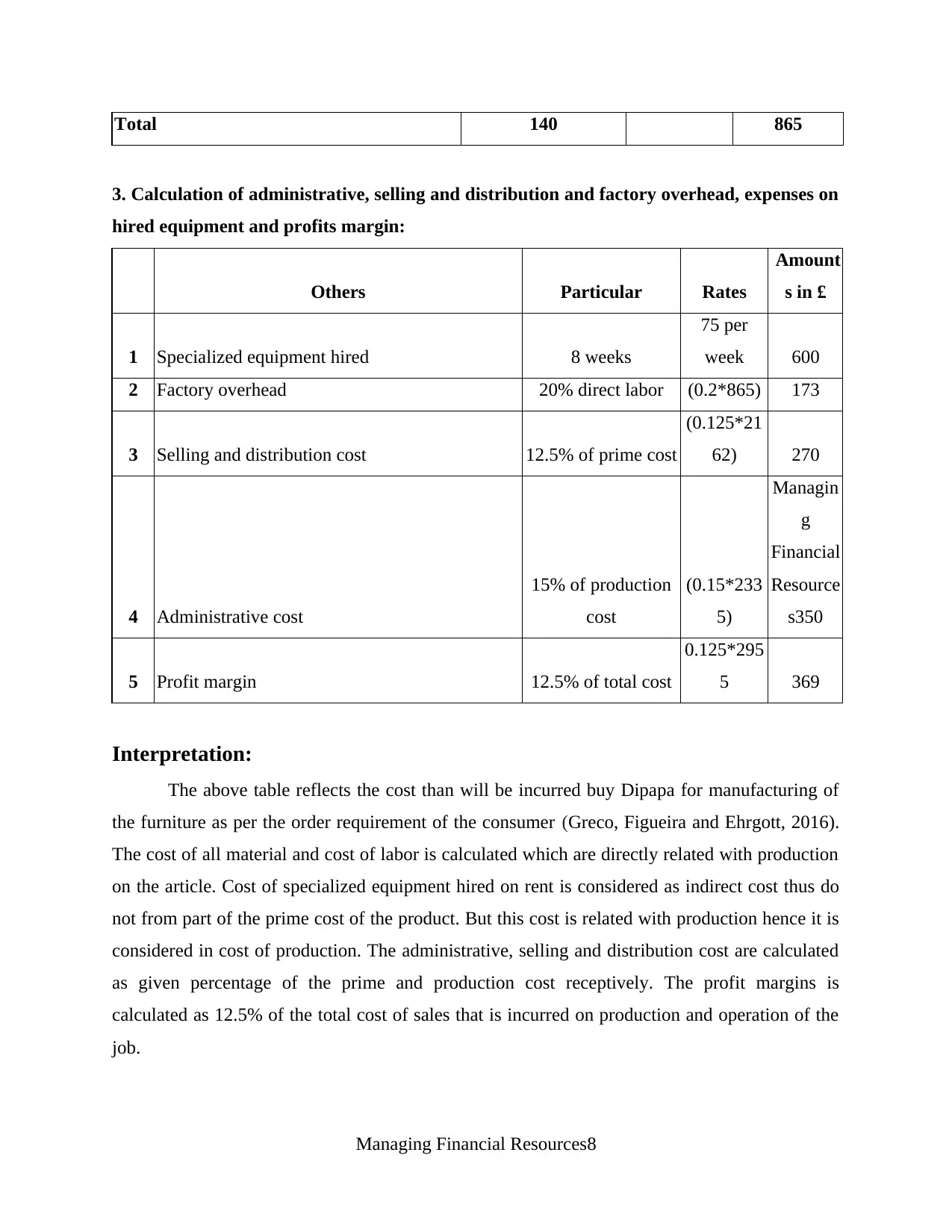

3. Calculation of administrative, selling and distribution and factory overhead, expenses on

hired equipment and profits margin:

Others Particular Rates

Amount

s in £

1 Specialized equipment hired 8 weeks

75 per

week 600

2 Factory overhead 20% direct labor (0.2*865) 173

3 Selling and distribution cost 12.5% of prime cost

(0.125*21

62) 270

4 Administrative cost

15% of production

cost

(0.15*233

5)

Managin

g

Financial

Resource

s350

5 Profit margin 12.5% of total cost

0.125*295

5 369

Interpretation:

The above table reflects the cost than will be incurred buy Dipapa for manufacturing of

the furniture as per the order requirement of the consumer (Greco, Figueira and Ehrgott, 2016).

The cost of all material and cost of labor is calculated which are directly related with production

on the article. Cost of specialized equipment hired on rent is considered as indirect cost thus do

not from part of the prime cost of the product. But this cost is related with production hence it is

considered in cost of production. The administrative, selling and distribution cost are calculated

as given percentage of the prime and production cost receptively. The profit margins is

calculated as 12.5% of the total cost of sales that is incurred on production and operation of the

job.

Managing Financial Resources8

3. Calculation of administrative, selling and distribution and factory overhead, expenses on

hired equipment and profits margin:

Others Particular Rates

Amount

s in £

1 Specialized equipment hired 8 weeks

75 per

week 600

2 Factory overhead 20% direct labor (0.2*865) 173

3 Selling and distribution cost 12.5% of prime cost

(0.125*21

62) 270

4 Administrative cost

15% of production

cost

(0.15*233

5)

Managin

g

Financial

Resource

s350

5 Profit margin 12.5% of total cost

0.125*295

5 369

Interpretation:

The above table reflects the cost than will be incurred buy Dipapa for manufacturing of

the furniture as per the order requirement of the consumer (Greco, Figueira and Ehrgott, 2016).

The cost of all material and cost of labor is calculated which are directly related with production

on the article. Cost of specialized equipment hired on rent is considered as indirect cost thus do

not from part of the prime cost of the product. But this cost is related with production hence it is

considered in cost of production. The administrative, selling and distribution cost are calculated

as given percentage of the prime and production cost receptively. The profit margins is

calculated as 12.5% of the total cost of sales that is incurred on production and operation of the

job.

Managing Financial Resources8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

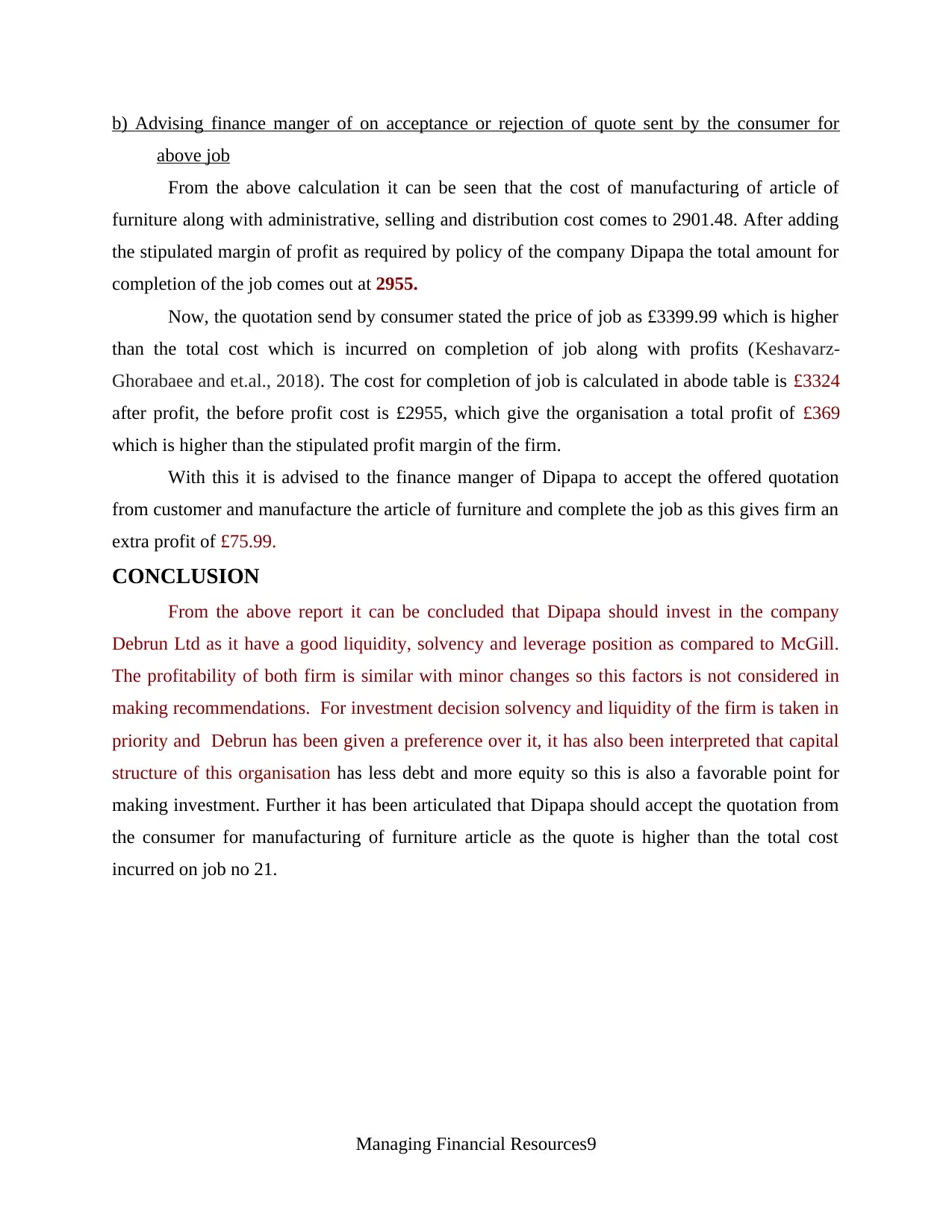

b) Advising finance manger of on acceptance or rejection of quote sent by the consumer for

above job

From the above calculation it can be seen that the cost of manufacturing of article of

furniture along with administrative, selling and distribution cost comes to 2901.48. After adding

the stipulated margin of profit as required by policy of the company Dipapa the total amount for

completion of the job comes out at 2955.

Now, the quotation send by consumer stated the price of job as £3399.99 which is higher

than the total cost which is incurred on completion of job along with profits (Keshavarz-

Ghorabaee and et.al., 2018). The cost for completion of job is calculated in abode table is £3324

after profit, the before profit cost is £2955, which give the organisation a total profit of £369

which is higher than the stipulated profit margin of the firm.

With this it is advised to the finance manger of Dipapa to accept the offered quotation

from customer and manufacture the article of furniture and complete the job as this gives firm an

extra profit of £75.99.

CONCLUSION

From the above report it can be concluded that Dipapa should invest in the company

Debrun Ltd as it have a good liquidity, solvency and leverage position as compared to McGill.

The profitability of both firm is similar with minor changes so this factors is not considered in

making recommendations. For investment decision solvency and liquidity of the firm is taken in

priority and Debrun has been given a preference over it, it has also been interpreted that capital

structure of this organisation has less debt and more equity so this is also a favorable point for

making investment. Further it has been articulated that Dipapa should accept the quotation from

the consumer for manufacturing of furniture article as the quote is higher than the total cost

incurred on job no 21.

Managing Financial Resources9

above job

From the above calculation it can be seen that the cost of manufacturing of article of

furniture along with administrative, selling and distribution cost comes to 2901.48. After adding

the stipulated margin of profit as required by policy of the company Dipapa the total amount for

completion of the job comes out at 2955.

Now, the quotation send by consumer stated the price of job as £3399.99 which is higher

than the total cost which is incurred on completion of job along with profits (Keshavarz-

Ghorabaee and et.al., 2018). The cost for completion of job is calculated in abode table is £3324

after profit, the before profit cost is £2955, which give the organisation a total profit of £369

which is higher than the stipulated profit margin of the firm.

With this it is advised to the finance manger of Dipapa to accept the offered quotation

from customer and manufacture the article of furniture and complete the job as this gives firm an

extra profit of £75.99.

CONCLUSION

From the above report it can be concluded that Dipapa should invest in the company

Debrun Ltd as it have a good liquidity, solvency and leverage position as compared to McGill.

The profitability of both firm is similar with minor changes so this factors is not considered in

making recommendations. For investment decision solvency and liquidity of the firm is taken in

priority and Debrun has been given a preference over it, it has also been interpreted that capital

structure of this organisation has less debt and more equity so this is also a favorable point for

making investment. Further it has been articulated that Dipapa should accept the quotation from

the consumer for manufacturing of furniture article as the quote is higher than the total cost

incurred on job no 21.

Managing Financial Resources9

REFERENCES

Books and Journals

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA). 1(1). pp.40-59.

Enekwe, C. I., 2015. The relationship between financial ratio analysis and corporate

profitability: a study of selected quoted oil and gas companies in Nigeria. European

Journal of Accounting, Auditing and Finance Research. 3(2). pp.17-34.

Greco, S., Figueira, J. and Ehrgott, M., 2016. Multiple criteria decision analysis. New York:

Springer.

Keshavarz-Ghorabaee, M and et.al., 2018. An Extended Step-Wise Weight Assessment Ratio

Analysis with Symmetric Interval Type-2 Fuzzy Sets for Determining the Subjective

Weights of Criteria in Multi-Criteria Decision-Making Problems. Symmetry.10(4). p.91.

Omar, N and et.al., 2014. Financial statement fraud: A case examination using Beneish Model

and ratio analysis. International Journal of Trade, Economics and Finance. 5(2). p.184.

ONLINE

Accounts Payable Ratio. 2018. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounts-payable-

turnover-ratio/>.

Return on Equity. 2018. [Online]. Available through <https://investinganswers.com/financial-

dictionary/financial-statement-analysis/return-equity-roe-916>.

Managing Financial Resources10

Books and Journals

Dokas, I., Giokas, D. and Tsamis, A., 2014. Liquidity efficiency in the Greek listed firms: a

financial ratio based on data envelopment analysis. International Journal of Corporate

Finance and Accounting (IJCFA). 1(1). pp.40-59.

Enekwe, C. I., 2015. The relationship between financial ratio analysis and corporate

profitability: a study of selected quoted oil and gas companies in Nigeria. European

Journal of Accounting, Auditing and Finance Research. 3(2). pp.17-34.

Greco, S., Figueira, J. and Ehrgott, M., 2016. Multiple criteria decision analysis. New York:

Springer.

Keshavarz-Ghorabaee, M and et.al., 2018. An Extended Step-Wise Weight Assessment Ratio

Analysis with Symmetric Interval Type-2 Fuzzy Sets for Determining the Subjective

Weights of Criteria in Multi-Criteria Decision-Making Problems. Symmetry.10(4). p.91.

Omar, N and et.al., 2014. Financial statement fraud: A case examination using Beneish Model

and ratio analysis. International Journal of Trade, Economics and Finance. 5(2). p.184.

ONLINE

Accounts Payable Ratio. 2018. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounts-payable-

turnover-ratio/>.

Return on Equity. 2018. [Online]. Available through <https://investinganswers.com/financial-

dictionary/financial-statement-analysis/return-equity-roe-916>.

Managing Financial Resources10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.