Managing Financial Resources and Decision Making - Exeter Cafe

VerifiedAdded on 2020/01/28

|22

|4938

|33

Report

AI Summary

This report examines the financial aspects of establishing a coffee concession, focusing on managing financial resources and making sound decisions. It begins by identifying various sources of finance, including equity, debt, and lease options, evaluating their implications, and determining the most suitable sources for the business. The report then delves into cost analysis of different finance sources, emphasizing the importance of financial planning and outlining the information needs of key decision-makers like shareholders and creditors. It includes the creation of cash and sales budgets, calculation of unit costs, and application of project evaluation methods such as payback period, ARR, NPV, and IRR to assess project viability. Furthermore, the report presents financial statements, including income statements and balance sheets, and concludes with a ratio analysis to evaluate the firm's performance. Overall, the report provides a comprehensive overview of financial management principles applied to a real-world business scenario, offering valuable insights for students and professionals alike.

MANAGING FINANCIAL RESOURCES

AND DECISION MAKING

AND DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.....................................................................................................................................4

TASK 1.......................................................................................................................................................4

1.1Sources of finance available to the business firms..............................................................................4

1.2 Implications of different sources of finance.......................................................................................5

1.3 Appropriate source of finance for business projects..........................................................................6

TASK 2.......................................................................................................................................................7

2.1 Analysis of cost of varied source of finance......................................................................................7

2.2 Importance of financial planning.......................................................................................................7

2.3 Information needs of different decision makers.................................................................................8

2.4 Impact of finance on the financial statements....................................................................................9

TASK 3.....................................................................................................................................................10

3.1Cash budgets and sales budget for business firm..............................................................................10

3.2 Calculation of unit cost....................................................................................................................11

3.3 Project evaluation method...............................................................................................................11

TASK 4.....................................................................................................................................................14

4.1 Financial statement of business firms..............................................................................................14

4.2 Format of financial statements.........................................................................................................15

4.3 Ratio analysis...................................................................................................................................20

CONCLUSION........................................................................................................................................20

REFERENCES........................................................................................................................................22

Table 1 Computation of cash budget.............................................................................................10

Table 2 Sales budget......................................................................................................................10

Table 3 Computation of unit cost..................................................................................................11

Table 4 Calculation of payback period..........................................................................................11

Table 5 Calculation of ARR..........................................................................................................12

Table 6 Calculation of NPV..........................................................................................................12

Table 7 Computation of IRR.........................................................................................................13

Table 8 Ratio analysis....................................................................................................................20

INTRODUCTION.....................................................................................................................................4

TASK 1.......................................................................................................................................................4

1.1Sources of finance available to the business firms..............................................................................4

1.2 Implications of different sources of finance.......................................................................................5

1.3 Appropriate source of finance for business projects..........................................................................6

TASK 2.......................................................................................................................................................7

2.1 Analysis of cost of varied source of finance......................................................................................7

2.2 Importance of financial planning.......................................................................................................7

2.3 Information needs of different decision makers.................................................................................8

2.4 Impact of finance on the financial statements....................................................................................9

TASK 3.....................................................................................................................................................10

3.1Cash budgets and sales budget for business firm..............................................................................10

3.2 Calculation of unit cost....................................................................................................................11

3.3 Project evaluation method...............................................................................................................11

TASK 4.....................................................................................................................................................14

4.1 Financial statement of business firms..............................................................................................14

4.2 Format of financial statements.........................................................................................................15

4.3 Ratio analysis...................................................................................................................................20

CONCLUSION........................................................................................................................................20

REFERENCES........................................................................................................................................22

Table 1 Computation of cash budget.............................................................................................10

Table 2 Sales budget......................................................................................................................10

Table 3 Computation of unit cost..................................................................................................11

Table 4 Calculation of payback period..........................................................................................11

Table 5 Calculation of ARR..........................................................................................................12

Table 6 Calculation of NPV..........................................................................................................12

Table 7 Computation of IRR.........................................................................................................13

Table 8 Ratio analysis....................................................................................................................20

Figure 1 income statement of partners...........................................................................................16

Figure 2 Income statement of sole trader......................................................................................16

Figure 3 Balance sheet of sole trader.............................................................................................17

Figure 4 Income statement of company.........................................................................................18

Figure 5Balance sheet of company................................................................................................19

Figure 2 Income statement of sole trader......................................................................................16

Figure 3 Balance sheet of sole trader.............................................................................................17

Figure 4 Income statement of company.........................................................................................18

Figure 5Balance sheet of company................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A contract for an opening of Coffee concession is obtained. Café premises will be established in

the 1350 sq feet that offer 65 covers. This café will be opened in the museum and art gallery of the

Exeter. There is a huge opportunity in this business. Office of the firm will be opened in the Cleevdon

area of England. Firm is new in the industry and lots of financial problems will come in existence in

upcoming time period. Finance is the important resource for the firm and it must be used with due

care because mentioned resource is scarcely available to the business firms. In the report sources

of finance are described and their cost is evaluated. In middle part of the report, budgets are

prepared and their values are interpreted in proper way. Project evaluation techniques are applied

on cash flows and most viable project is selected for the firm. At end of the report, ratio analysis

is done and comments are given on the firm performance.

TASK 1

1.1Sources of finance available to the business firms

There are varied sources of finance that are available to the Coffee concession. All these

sources of finance have some merits and demerits. It depends on the firm that which source of

finance it think is suitable for its business. Some sources of finance that readily available to the

business firms are as follows.

External sources of finance

Equity: It is the source of finance that are widely used by the business firms. Venture capital

and private equity are common variants that are used by small size firms in their business.

Café business is opened at small level and for same there is no need to make use of equity.

However, on large scale small size firms make use of this source of finance.

Debt: It is a source of finance that is commonly used by each and every sort of the business

firm irrespective of its size (Cao and Zhang., 2011). Debt is available at fixed and floating

interest rate and firm have to select any option from available alternatives according to its

requirements. Fixed interest rate debt is one in which finance cost remain fixed and remain

unchanged even market conditions get changed. Contrary to this, in case of floating interest

rate finance cost get changed with slight variation in interest rates of central bank. Fixed rate

debt provide safe zone to firms and most of them prefer to take debt at fixed interest rate.

A contract for an opening of Coffee concession is obtained. Café premises will be established in

the 1350 sq feet that offer 65 covers. This café will be opened in the museum and art gallery of the

Exeter. There is a huge opportunity in this business. Office of the firm will be opened in the Cleevdon

area of England. Firm is new in the industry and lots of financial problems will come in existence in

upcoming time period. Finance is the important resource for the firm and it must be used with due

care because mentioned resource is scarcely available to the business firms. In the report sources

of finance are described and their cost is evaluated. In middle part of the report, budgets are

prepared and their values are interpreted in proper way. Project evaluation techniques are applied

on cash flows and most viable project is selected for the firm. At end of the report, ratio analysis

is done and comments are given on the firm performance.

TASK 1

1.1Sources of finance available to the business firms

There are varied sources of finance that are available to the Coffee concession. All these

sources of finance have some merits and demerits. It depends on the firm that which source of

finance it think is suitable for its business. Some sources of finance that readily available to the

business firms are as follows.

External sources of finance

Equity: It is the source of finance that are widely used by the business firms. Venture capital

and private equity are common variants that are used by small size firms in their business.

Café business is opened at small level and for same there is no need to make use of equity.

However, on large scale small size firms make use of this source of finance.

Debt: It is a source of finance that is commonly used by each and every sort of the business

firm irrespective of its size (Cao and Zhang., 2011). Debt is available at fixed and floating

interest rate and firm have to select any option from available alternatives according to its

requirements. Fixed interest rate debt is one in which finance cost remain fixed and remain

unchanged even market conditions get changed. Contrary to this, in case of floating interest

rate finance cost get changed with slight variation in interest rates of central bank. Fixed rate

debt provide safe zone to firms and most of them prefer to take debt at fixed interest rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

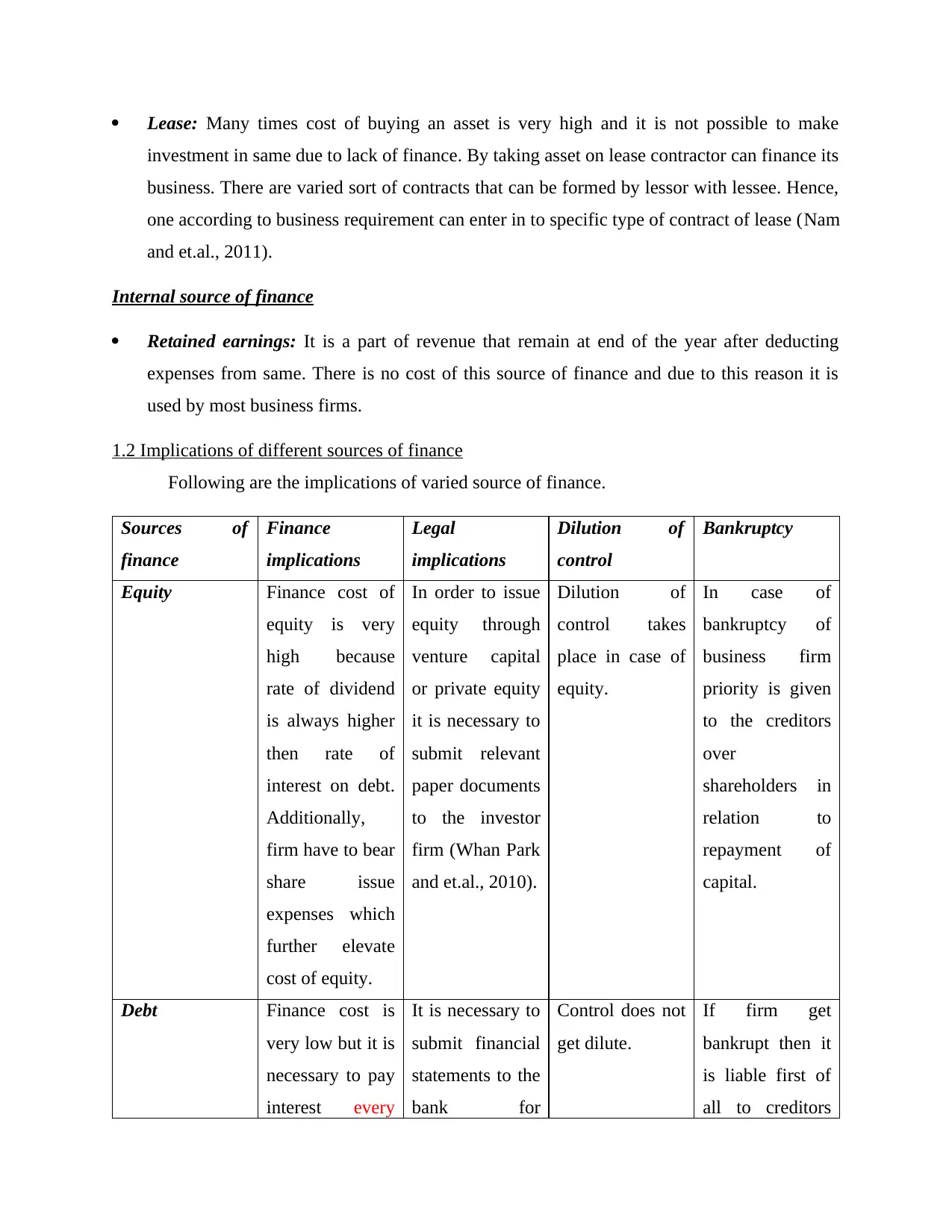

Lease: Many times cost of buying an asset is very high and it is not possible to make

investment in same due to lack of finance. By taking asset on lease contractor can finance its

business. There are varied sort of contracts that can be formed by lessor with lessee. Hence,

one according to business requirement can enter in to specific type of contract of lease (Nam

and et.al., 2011).

Internal source of finance

Retained earnings: It is a part of revenue that remain at end of the year after deducting

expenses from same. There is no cost of this source of finance and due to this reason it is

used by most business firms.

1.2 Implications of different sources of finance

Following are the implications of varied source of finance.

Sources of

finance

Finance

implications

Legal

implications

Dilution of

control

Bankruptcy

Equity Finance cost of

equity is very

high because

rate of dividend

is always higher

then rate of

interest on debt.

Additionally,

firm have to bear

share issue

expenses which

further elevate

cost of equity.

In order to issue

equity through

venture capital

or private equity

it is necessary to

submit relevant

paper documents

to the investor

firm (Whan Park

and et.al., 2010).

Dilution of

control takes

place in case of

equity.

In case of

bankruptcy of

business firm

priority is given

to the creditors

over

shareholders in

relation to

repayment of

capital.

Debt Finance cost is

very low but it is

necessary to pay

interest every

It is necessary to

submit financial

statements to the

bank for

Control does not

get dilute.

If firm get

bankrupt then it

is liable first of

all to creditors

investment in same due to lack of finance. By taking asset on lease contractor can finance its

business. There are varied sort of contracts that can be formed by lessor with lessee. Hence,

one according to business requirement can enter in to specific type of contract of lease (Nam

and et.al., 2011).

Internal source of finance

Retained earnings: It is a part of revenue that remain at end of the year after deducting

expenses from same. There is no cost of this source of finance and due to this reason it is

used by most business firms.

1.2 Implications of different sources of finance

Following are the implications of varied source of finance.

Sources of

finance

Finance

implications

Legal

implications

Dilution of

control

Bankruptcy

Equity Finance cost of

equity is very

high because

rate of dividend

is always higher

then rate of

interest on debt.

Additionally,

firm have to bear

share issue

expenses which

further elevate

cost of equity.

In order to issue

equity through

venture capital

or private equity

it is necessary to

submit relevant

paper documents

to the investor

firm (Whan Park

and et.al., 2010).

Dilution of

control takes

place in case of

equity.

In case of

bankruptcy of

business firm

priority is given

to the creditors

over

shareholders in

relation to

repayment of

capital.

Debt Finance cost is

very low but it is

necessary to pay

interest every

It is necessary to

submit financial

statements to the

bank for

Control does not

get dilute.

If firm get

bankrupt then it

is liable first of

all to creditors

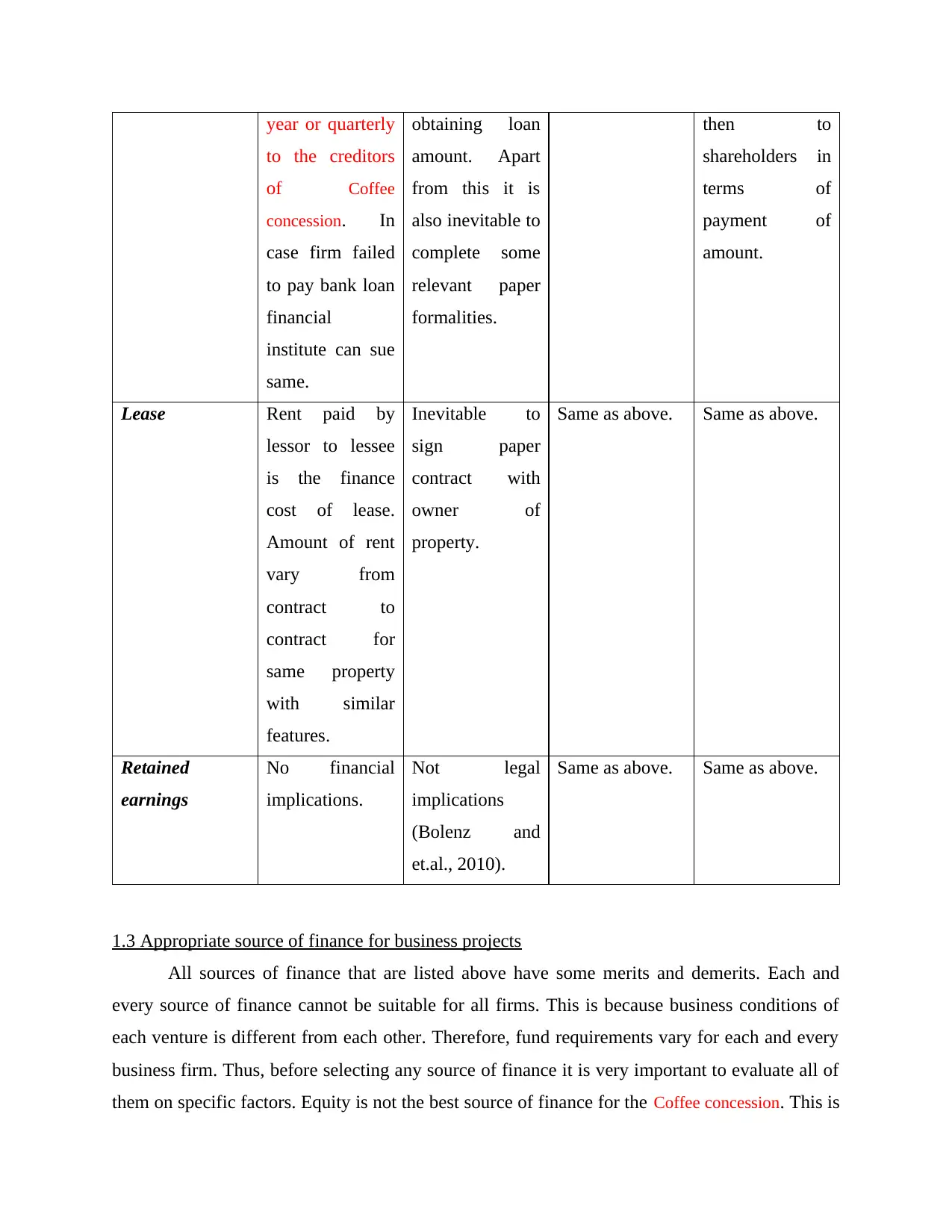

year or quarterly

to the creditors

of Coffee

concession. In

case firm failed

to pay bank loan

financial

institute can sue

same.

obtaining loan

amount. Apart

from this it is

also inevitable to

complete some

relevant paper

formalities.

then to

shareholders in

terms of

payment of

amount.

Lease Rent paid by

lessor to lessee

is the finance

cost of lease.

Amount of rent

vary from

contract to

contract for

same property

with similar

features.

Inevitable to

sign paper

contract with

owner of

property.

Same as above. Same as above.

Retained

earnings

No financial

implications.

Not legal

implications

(Bolenz and

et.al., 2010).

Same as above. Same as above.

1.3 Appropriate source of finance for business projects

All sources of finance that are listed above have some merits and demerits. Each and

every source of finance cannot be suitable for all firms. This is because business conditions of

each venture is different from each other. Therefore, fund requirements vary for each and every

business firm. Thus, before selecting any source of finance it is very important to evaluate all of

them on specific factors. Equity is not the best source of finance for the Coffee concession. This is

to the creditors

of Coffee

concession. In

case firm failed

to pay bank loan

financial

institute can sue

same.

obtaining loan

amount. Apart

from this it is

also inevitable to

complete some

relevant paper

formalities.

then to

shareholders in

terms of

payment of

amount.

Lease Rent paid by

lessor to lessee

is the finance

cost of lease.

Amount of rent

vary from

contract to

contract for

same property

with similar

features.

Inevitable to

sign paper

contract with

owner of

property.

Same as above. Same as above.

Retained

earnings

No financial

implications.

Not legal

implications

(Bolenz and

et.al., 2010).

Same as above. Same as above.

1.3 Appropriate source of finance for business projects

All sources of finance that are listed above have some merits and demerits. Each and

every source of finance cannot be suitable for all firms. This is because business conditions of

each venture is different from each other. Therefore, fund requirements vary for each and every

business firm. Thus, before selecting any source of finance it is very important to evaluate all of

them on specific factors. Equity is not the best source of finance for the Coffee concession. This is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because it is going to build a small café for which huge investment is not required. Debt is best

source of finance that is available to the contractor. It can take loan at fixed interest rate and can

eliminate the market risk. At same time he will be able to control elevation in finance cost. Lease

is another best alternative that can be used by contractor. If he needs to purchase machine then

instead of buying same machine can be taken on lease (Hacker and Pierson, 2011). By doing so

firm can abstain from making heavy capital investment on project. It can invest money elsewhere

and can elevate return on investment. Retained earnings is the another source of finance that can

be used by the business firm because it does not have any cost of capital. Hence, these were

appropriate source of finance for the contractor.

TASK 2

2.1 Analysis of cost of varied source of finance

Cost of different sources of finance is explained below.

Equity: Cost of equity always remain whether fund is raised through issue of shares from

stock market or through venture capital firm. Dividend that firm pay to its shareholders is the

cost of finance for equity. With issue of shares firm lose control on the business which is

intangible cost of the mentioned source of finance.

Debt: Interest paid on debt is the cost of finance for bank loan. As mentioned above loan can

be taken at the fixed or floating interest rate by the Coffee concession. Finance cost may

decline or increase if debt will be taken at floating interest rate (Brockhaus and et.al., 2012).

The main benefit of debt is that firm get deduction in income tax for interest and principal

amount it paid to the bank or financial institution.

Lease: Rent paid for the use of specific asset to the property owner is the finance cost of this

source of finance. The interesting point is that one can keep finance cost low in case of this

source of finance. In lease contract is formed between lessor and lessee. It is terms of

contract that determine cost of lease for the business firm. Hence, firm by obtaining consent

of property owner on its terms can lower cost of lease. No tax benefits are received by the

firm on lease.

Retained earnings: There is no cost of finance of retained earnings because it is a portion of

profit that remain after deducting expenses from revenue of the Coffee concession. However,

source of finance that is available to the contractor. It can take loan at fixed interest rate and can

eliminate the market risk. At same time he will be able to control elevation in finance cost. Lease

is another best alternative that can be used by contractor. If he needs to purchase machine then

instead of buying same machine can be taken on lease (Hacker and Pierson, 2011). By doing so

firm can abstain from making heavy capital investment on project. It can invest money elsewhere

and can elevate return on investment. Retained earnings is the another source of finance that can

be used by the business firm because it does not have any cost of capital. Hence, these were

appropriate source of finance for the contractor.

TASK 2

2.1 Analysis of cost of varied source of finance

Cost of different sources of finance is explained below.

Equity: Cost of equity always remain whether fund is raised through issue of shares from

stock market or through venture capital firm. Dividend that firm pay to its shareholders is the

cost of finance for equity. With issue of shares firm lose control on the business which is

intangible cost of the mentioned source of finance.

Debt: Interest paid on debt is the cost of finance for bank loan. As mentioned above loan can

be taken at the fixed or floating interest rate by the Coffee concession. Finance cost may

decline or increase if debt will be taken at floating interest rate (Brockhaus and et.al., 2012).

The main benefit of debt is that firm get deduction in income tax for interest and principal

amount it paid to the bank or financial institution.

Lease: Rent paid for the use of specific asset to the property owner is the finance cost of this

source of finance. The interesting point is that one can keep finance cost low in case of this

source of finance. In lease contract is formed between lessor and lessee. It is terms of

contract that determine cost of lease for the business firm. Hence, firm by obtaining consent

of property owner on its terms can lower cost of lease. No tax benefits are received by the

firm on lease.

Retained earnings: There is no cost of finance of retained earnings because it is a portion of

profit that remain after deducting expenses from revenue of the Coffee concession. However,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

there is opportunity cost of retained earnings. Opportunity cost means the benefit that firm

cannot obtain because it is not possible to make next best use of specific asset.

2.2 Importance of financial planning

Financial planning refers to the plan under which it is determined that how cash will be

raised from the market and the way in which it will be utilized in the business. It is a tool that is

used to allocate funds among varied business activities in systematic way. In order to develop

café many things needs to be purchased like bricks and cement etc. Apart from this, many other

items will be purchased to evolve café in the park. Financial plan will be beneficial for the

chosen contract because by using same effective allocation of cash will be done among varied

business activities that are related to the Coffee concession. Allocation will be done in such a way

so that contractor does not face problem cash shortage in its business. Financial planning is

undertaken by the firm by following a systematic procedure (Wang and Shultz, 2010). Under this

budgeted amount is determined and thereafter list of business activities is prepared. Ranking on

the basis of priority is given to these activities. On the basis of ranking and availability of budget

amount allocation of fund is done among varied business activities. It is very important to

identify surplus and deficit balance under cash budget as part of financial planning. By preparing

suitable strategy deficit amount can be reduced or efforts can be made to arrange additional

finance on time. If there will be lack of finance then project will take long time to complete and

cost of same will increase.

2.3 Information needs of different decision makers

There are different stakeholders of the firm and they always needs some information to

make business decisions and to ensure that their interest are safe with the firm. Information needs

of different decision makers is given below.

Shareholders: These are those who makes an investment in the company or intends to do

same. In both cases then needed financial statements of the firm to make business decisions.

If one already makes an investment in the firm then he needed financial statements in order

to decide whether he must keep an investment in the firm or exit same from the company

(Bascom, 2016). On other hand, one who intends to make investment in the firm also needed

financial statements in order to assess firm profitability and making investment decisions.

Shareholders apart from financial statements also needed annual report because from same

cannot obtain because it is not possible to make next best use of specific asset.

2.2 Importance of financial planning

Financial planning refers to the plan under which it is determined that how cash will be

raised from the market and the way in which it will be utilized in the business. It is a tool that is

used to allocate funds among varied business activities in systematic way. In order to develop

café many things needs to be purchased like bricks and cement etc. Apart from this, many other

items will be purchased to evolve café in the park. Financial plan will be beneficial for the

chosen contract because by using same effective allocation of cash will be done among varied

business activities that are related to the Coffee concession. Allocation will be done in such a way

so that contractor does not face problem cash shortage in its business. Financial planning is

undertaken by the firm by following a systematic procedure (Wang and Shultz, 2010). Under this

budgeted amount is determined and thereafter list of business activities is prepared. Ranking on

the basis of priority is given to these activities. On the basis of ranking and availability of budget

amount allocation of fund is done among varied business activities. It is very important to

identify surplus and deficit balance under cash budget as part of financial planning. By preparing

suitable strategy deficit amount can be reduced or efforts can be made to arrange additional

finance on time. If there will be lack of finance then project will take long time to complete and

cost of same will increase.

2.3 Information needs of different decision makers

There are different stakeholders of the firm and they always needs some information to

make business decisions and to ensure that their interest are safe with the firm. Information needs

of different decision makers is given below.

Shareholders: These are those who makes an investment in the company or intends to do

same. In both cases then needed financial statements of the firm to make business decisions.

If one already makes an investment in the firm then he needed financial statements in order

to decide whether he must keep an investment in the firm or exit same from the company

(Bascom, 2016). On other hand, one who intends to make investment in the firm also needed

financial statements in order to assess firm profitability and making investment decisions.

Shareholders apart from financial statements also needed annual report because from same

they come to know about challenges faced by the firm during the year and the way in which

handle challenges. These things reflect management capability handle business. Hence, apart

from accounting information annual report is also needed by the shareholders to make

investment decisions.

Creditors: These are the entities who lend money to the business firm like Coffee concession

and expect from the firm that it will pay interest on time and principal amount. Creditors in

order to ensure that they will receive payment on time require company financial statements.

On the basis of financial statements creditors identify the days that are taken by the firm to

make payment to its creditors. If they identify that management is taking more time in

paying debt amount then same abstain from further giving a loan to the business firm.

Employees: These are those who works for the firm and its growth entirely depends on their

performance (Nicot and Scanlon, 2012). Employees also needed firm financial statements in

order to obtain information about the firm business condition. If firm is not in profit for some

time then it is possible that it deny from making payment to the employees for two to six

months. Hence, on the basis of financial statements managers evaluate firm condition and

determine whether they must remain in the firm or leave same.

Managers: It is an entity that plays a very important role in growth of an organization like

Coffee concession. This is because it is managers who look after effective implementation of

the strategy that is formulated by the top managers (Frankel, 2010). Managers needed

financial statements in order to obtain an information about the direction in which firm is

going. On the basis of analysis of financial statements managers identify strong and weak

points of the firm. They create tactics that makes firm strong on those areas in which earlier it

was weak.

Government: Government also needed financial statements of the firm because it receive tax

from the company. On the basis of analysis of statements it ensured that firm pay accurate

amount of tax to the relevant authority.

2.4 Impact of finance on the financial statements

Finance to great extent affects the financial statement of the firm. If contractor take a debt

of 10,000£ then this transaction will affect both income statement and balance sheet of the firm.

Debt is taken by the contractor which means that he will pay interest on same at end of the year.

Interest amount will be deducted from the gross profit. Hence, firm profit will decline by the

handle challenges. These things reflect management capability handle business. Hence, apart

from accounting information annual report is also needed by the shareholders to make

investment decisions.

Creditors: These are the entities who lend money to the business firm like Coffee concession

and expect from the firm that it will pay interest on time and principal amount. Creditors in

order to ensure that they will receive payment on time require company financial statements.

On the basis of financial statements creditors identify the days that are taken by the firm to

make payment to its creditors. If they identify that management is taking more time in

paying debt amount then same abstain from further giving a loan to the business firm.

Employees: These are those who works for the firm and its growth entirely depends on their

performance (Nicot and Scanlon, 2012). Employees also needed firm financial statements in

order to obtain information about the firm business condition. If firm is not in profit for some

time then it is possible that it deny from making payment to the employees for two to six

months. Hence, on the basis of financial statements managers evaluate firm condition and

determine whether they must remain in the firm or leave same.

Managers: It is an entity that plays a very important role in growth of an organization like

Coffee concession. This is because it is managers who look after effective implementation of

the strategy that is formulated by the top managers (Frankel, 2010). Managers needed

financial statements in order to obtain an information about the direction in which firm is

going. On the basis of analysis of financial statements managers identify strong and weak

points of the firm. They create tactics that makes firm strong on those areas in which earlier it

was weak.

Government: Government also needed financial statements of the firm because it receive tax

from the company. On the basis of analysis of statements it ensured that firm pay accurate

amount of tax to the relevant authority.

2.4 Impact of finance on the financial statements

Finance to great extent affects the financial statement of the firm. If contractor take a debt

of 10,000£ then this transaction will affect both income statement and balance sheet of the firm.

Debt is taken by the contractor which means that he will pay interest on same at end of the year.

Interest amount will be deducted from the gross profit. Hence, firm profit will decline by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

interest amount. On other hand, contractor receive a bank loan of mentioned amount. Hence,

bank loan in long term loan section of liability side of balance sheet will increase. Bank give loan

to contractor which means he receive cash. Hence, cash on current assets side of balance sheet

will increase. In this way debt transaction affects the financial statements of the firm. In case of

equity also same thing is observed and shareholder equity in liability side of balance sheet get

increased. Similarly, cash on assets side of balance sheet also increases. In case dividend if

declared by the firm then revenue amount reduced by the dividend amount. It can be said that

both debt and equity affects financial statements in same way. If business is finance by lease then

leased asset are shown in asset side of balance sheet (Gertler, Kiyotaki and Queralto, 2012). Rent

amount is recorded in the income statement. By rent amount firm profit get reduced. Retained

earnings amount is added in the balance sheet under shareholder equity section of liability. On

same time cash section of asset also increase by retained earnings amount.

TASK 3

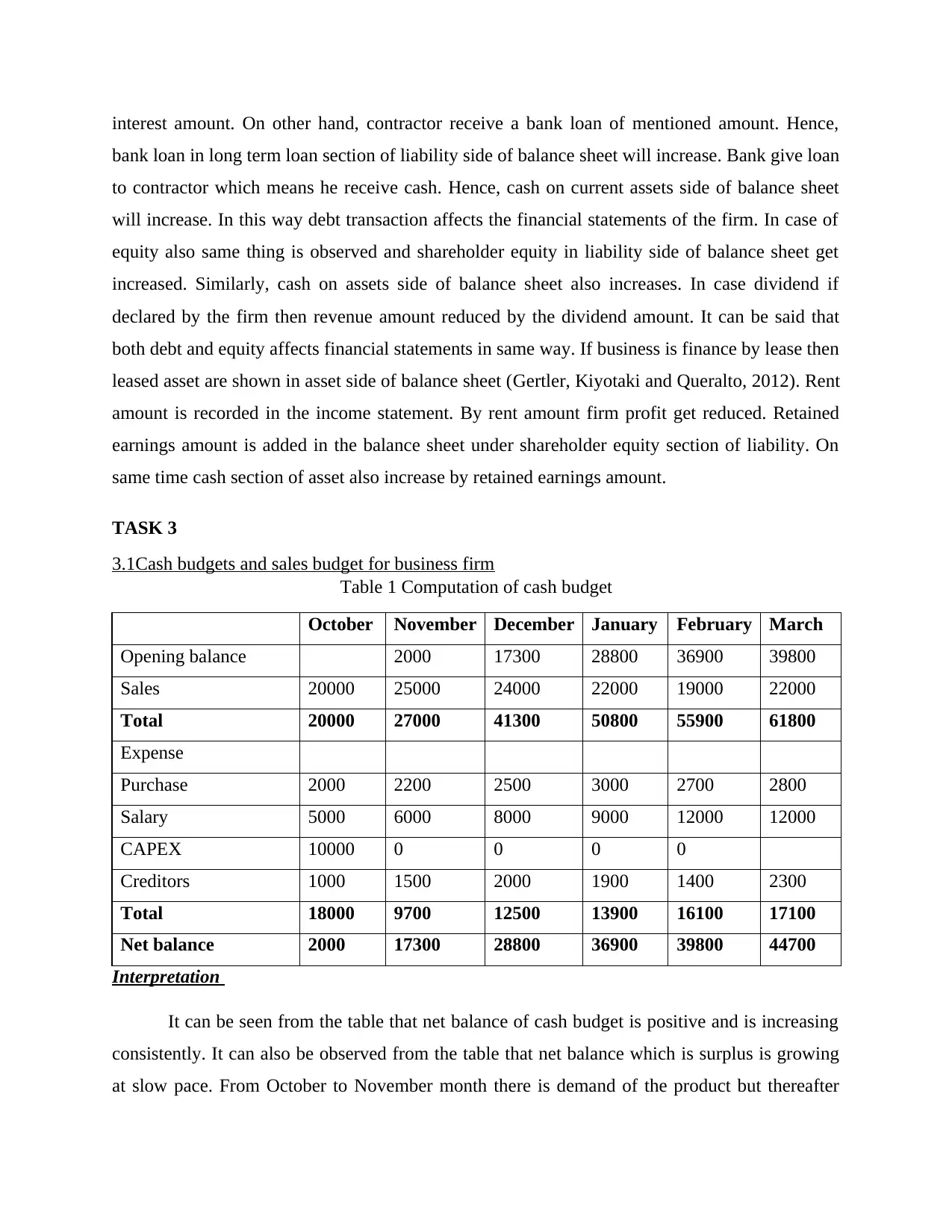

3.1Cash budgets and sales budget for business firm

Table 1 Computation of cash budget

October November December January February March

Opening balance 2000 17300 28800 36900 39800

Sales 20000 25000 24000 22000 19000 22000

Total 20000 27000 41300 50800 55900 61800

Expense

Purchase 2000 2200 2500 3000 2700 2800

Salary 5000 6000 8000 9000 12000 12000

CAPEX 10000 0 0 0 0

Creditors 1000 1500 2000 1900 1400 2300

Total 18000 9700 12500 13900 16100 17100

Net balance 2000 17300 28800 36900 39800 44700

Interpretation

It can be seen from the table that net balance of cash budget is positive and is increasing

consistently. It can also be observed from the table that net balance which is surplus is growing

at slow pace. From October to November month there is demand of the product but thereafter

bank loan in long term loan section of liability side of balance sheet will increase. Bank give loan

to contractor which means he receive cash. Hence, cash on current assets side of balance sheet

will increase. In this way debt transaction affects the financial statements of the firm. In case of

equity also same thing is observed and shareholder equity in liability side of balance sheet get

increased. Similarly, cash on assets side of balance sheet also increases. In case dividend if

declared by the firm then revenue amount reduced by the dividend amount. It can be said that

both debt and equity affects financial statements in same way. If business is finance by lease then

leased asset are shown in asset side of balance sheet (Gertler, Kiyotaki and Queralto, 2012). Rent

amount is recorded in the income statement. By rent amount firm profit get reduced. Retained

earnings amount is added in the balance sheet under shareholder equity section of liability. On

same time cash section of asset also increase by retained earnings amount.

TASK 3

3.1Cash budgets and sales budget for business firm

Table 1 Computation of cash budget

October November December January February March

Opening balance 2000 17300 28800 36900 39800

Sales 20000 25000 24000 22000 19000 22000

Total 20000 27000 41300 50800 55900 61800

Expense

Purchase 2000 2200 2500 3000 2700 2800

Salary 5000 6000 8000 9000 12000 12000

CAPEX 10000 0 0 0 0

Creditors 1000 1500 2000 1900 1400 2300

Total 18000 9700 12500 13900 16100 17100

Net balance 2000 17300 28800 36900 39800 44700

Interpretation

It can be seen from the table that net balance of cash budget is positive and is increasing

consistently. It can also be observed from the table that net balance which is surplus is growing

at slow pace. From October to November month there is demand of the product but thereafter

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

demand for same declined till the month of February. Trend get reversed in last month of March

in which sales elevate to some extent for the Coffee concession. It can be observed from the table

that even sales decline the also expenses increase at rapid pace in the month of December and

January. However, in month of February and April good control was maintained on expenses.

This reflect that firm needs to evaluate surrounding conditions very closely in order to make

business decisions.

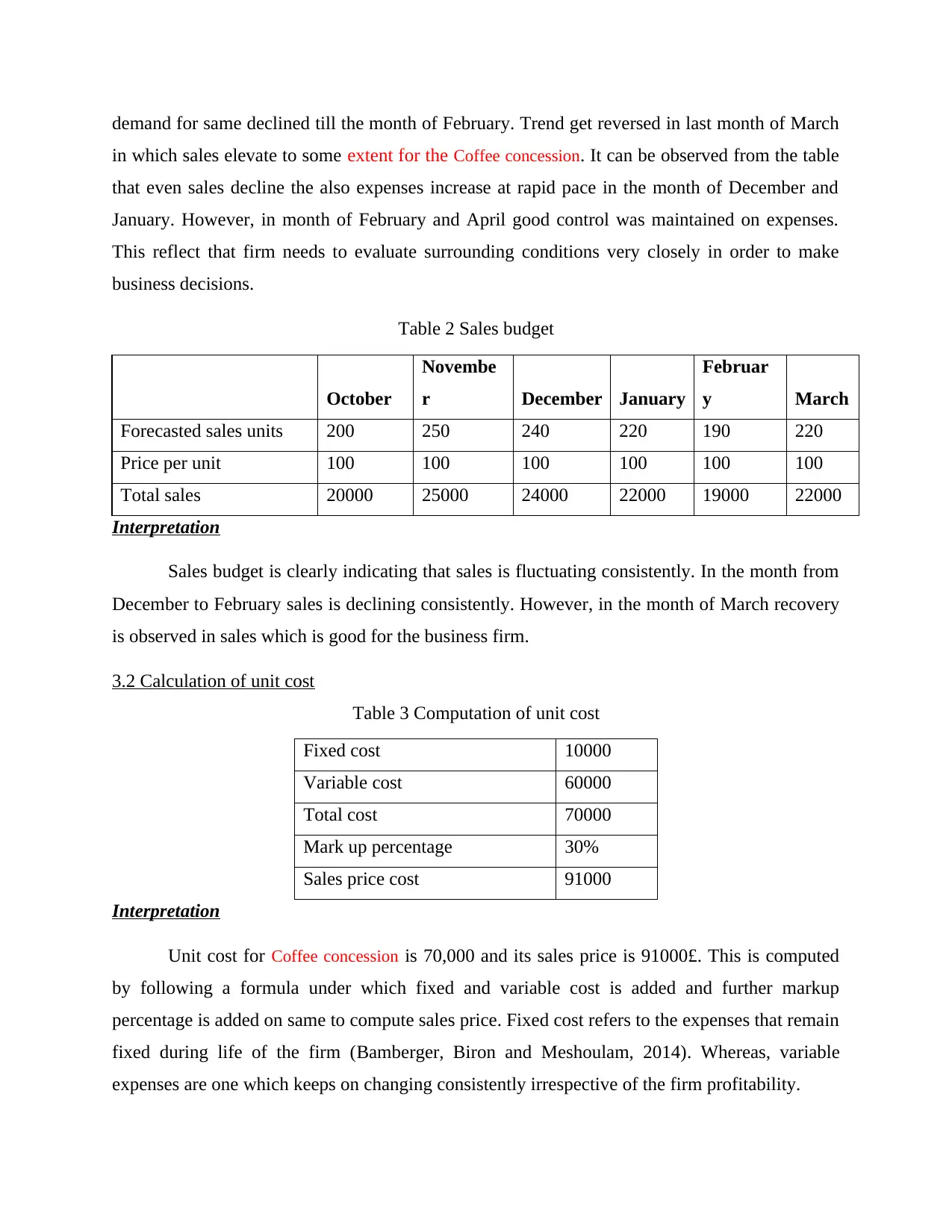

Table 2 Sales budget

October

Novembe

r December January

Februar

y March

Forecasted sales units 200 250 240 220 190 220

Price per unit 100 100 100 100 100 100

Total sales 20000 25000 24000 22000 19000 22000

Interpretation

Sales budget is clearly indicating that sales is fluctuating consistently. In the month from

December to February sales is declining consistently. However, in the month of March recovery

is observed in sales which is good for the business firm.

3.2 Calculation of unit cost

Table 3 Computation of unit cost

Fixed cost 10000

Variable cost 60000

Total cost 70000

Mark up percentage 30%

Sales price cost 91000

Interpretation

Unit cost for Coffee concession is 70,000 and its sales price is 91000£. This is computed

by following a formula under which fixed and variable cost is added and further markup

percentage is added on same to compute sales price. Fixed cost refers to the expenses that remain

fixed during life of the firm (Bamberger, Biron and Meshoulam, 2014). Whereas, variable

expenses are one which keeps on changing consistently irrespective of the firm profitability.

in which sales elevate to some extent for the Coffee concession. It can be observed from the table

that even sales decline the also expenses increase at rapid pace in the month of December and

January. However, in month of February and April good control was maintained on expenses.

This reflect that firm needs to evaluate surrounding conditions very closely in order to make

business decisions.

Table 2 Sales budget

October

Novembe

r December January

Februar

y March

Forecasted sales units 200 250 240 220 190 220

Price per unit 100 100 100 100 100 100

Total sales 20000 25000 24000 22000 19000 22000

Interpretation

Sales budget is clearly indicating that sales is fluctuating consistently. In the month from

December to February sales is declining consistently. However, in the month of March recovery

is observed in sales which is good for the business firm.

3.2 Calculation of unit cost

Table 3 Computation of unit cost

Fixed cost 10000

Variable cost 60000

Total cost 70000

Mark up percentage 30%

Sales price cost 91000

Interpretation

Unit cost for Coffee concession is 70,000 and its sales price is 91000£. This is computed

by following a formula under which fixed and variable cost is added and further markup

percentage is added on same to compute sales price. Fixed cost refers to the expenses that remain

fixed during life of the firm (Bamberger, Biron and Meshoulam, 2014). Whereas, variable

expenses are one which keeps on changing consistently irrespective of the firm profitability.

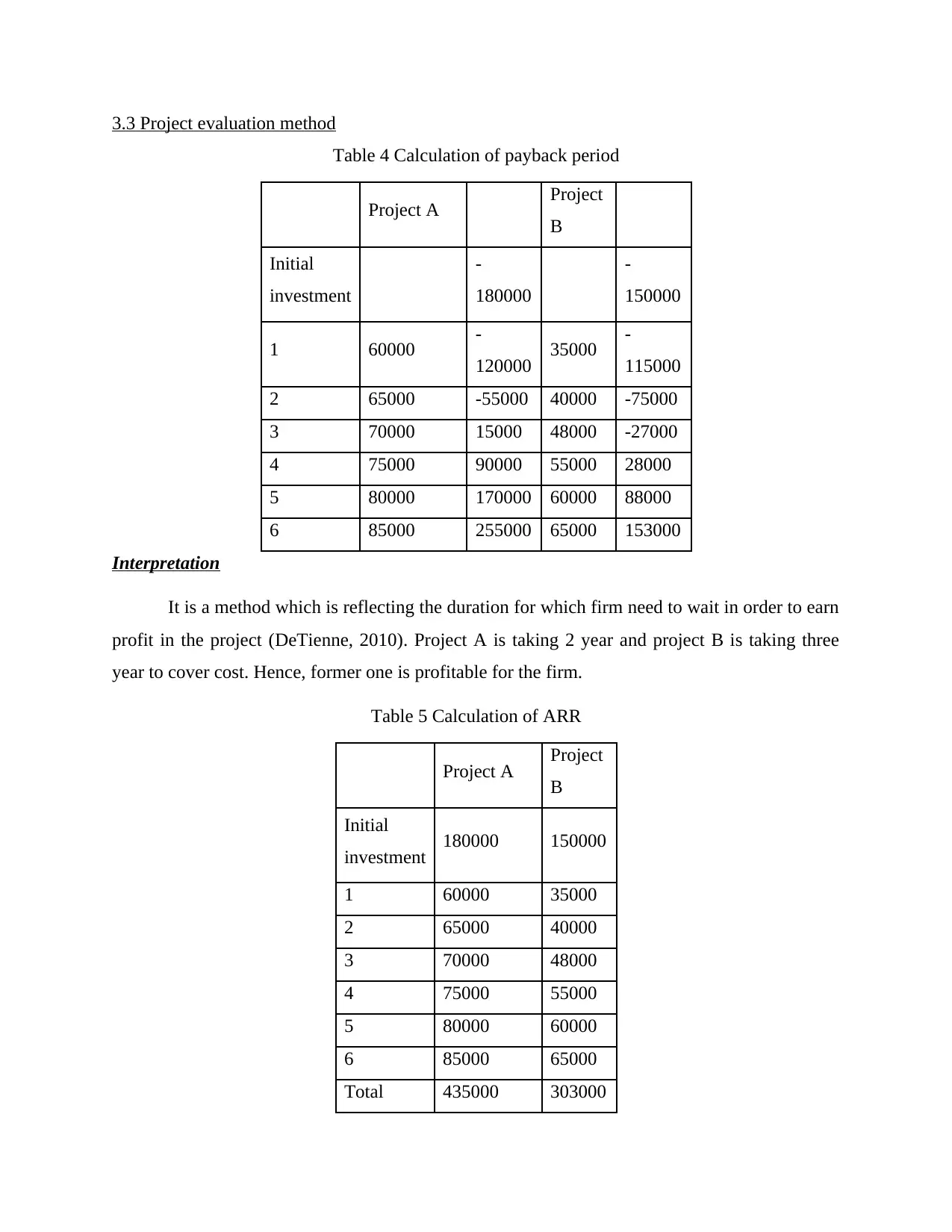

3.3 Project evaluation method

Table 4 Calculation of payback period

Project A Project

B

Initial

investment

-

180000

-

150000

1 60000 -

120000 35000 -

115000

2 65000 -55000 40000 -75000

3 70000 15000 48000 -27000

4 75000 90000 55000 28000

5 80000 170000 60000 88000

6 85000 255000 65000 153000

Interpretation

It is a method which is reflecting the duration for which firm need to wait in order to earn

profit in the project (DeTienne, 2010). Project A is taking 2 year and project B is taking three

year to cover cost. Hence, former one is profitable for the firm.

Table 5 Calculation of ARR

Project A Project

B

Initial

investment 180000 150000

1 60000 35000

2 65000 40000

3 70000 48000

4 75000 55000

5 80000 60000

6 85000 65000

Total 435000 303000

Table 4 Calculation of payback period

Project A Project

B

Initial

investment

-

180000

-

150000

1 60000 -

120000 35000 -

115000

2 65000 -55000 40000 -75000

3 70000 15000 48000 -27000

4 75000 90000 55000 28000

5 80000 170000 60000 88000

6 85000 255000 65000 153000

Interpretation

It is a method which is reflecting the duration for which firm need to wait in order to earn

profit in the project (DeTienne, 2010). Project A is taking 2 year and project B is taking three

year to cover cost. Hence, former one is profitable for the firm.

Table 5 Calculation of ARR

Project A Project

B

Initial

investment 180000 150000

1 60000 35000

2 65000 40000

3 70000 48000

4 75000 55000

5 80000 60000

6 85000 65000

Total 435000 303000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.