Managing Financial Resources: Cost Classification and Rate Analysis

VerifiedAdded on 2023/06/15

|11

|2439

|284

Report

AI Summary

This report provides a detailed analysis of managing financial resources within an organization, emphasizing financial planning and control to enhance business profitability. It includes two sections: the first calculates fixed and variable costs using data from Cleveland Recreation Centre, and the second classifies various expenses under different cost heads, such as direct material, direct labor, direct expenses, indirect production overhead, research and development costs, selling and distribution costs, administration costs, and finance costs. The report also explains key performance indicators (KPIs) like Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Length of Stay (ALOS), Occupancy Rate, Gross Operating Profit Per Available Room (GOPPAR), and Market Penetration Index (MPI), illustrating their application with examples. The conclusion underscores the importance of financial resource management for business success, achieved through accounting and management theories, and highlights the calculation and classification of different costs.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................4

SECTION A.....................................................................................................................................4

SECTION B.....................................................................................................................................5

Identify the various expenses given in the under the numerous cost heads................................5

Explain the following with the help of example:.........................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................4

SECTION A.....................................................................................................................................4

SECTION B.....................................................................................................................................5

Identify the various expenses given in the under the numerous cost heads................................5

Explain the following with the help of example:.........................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

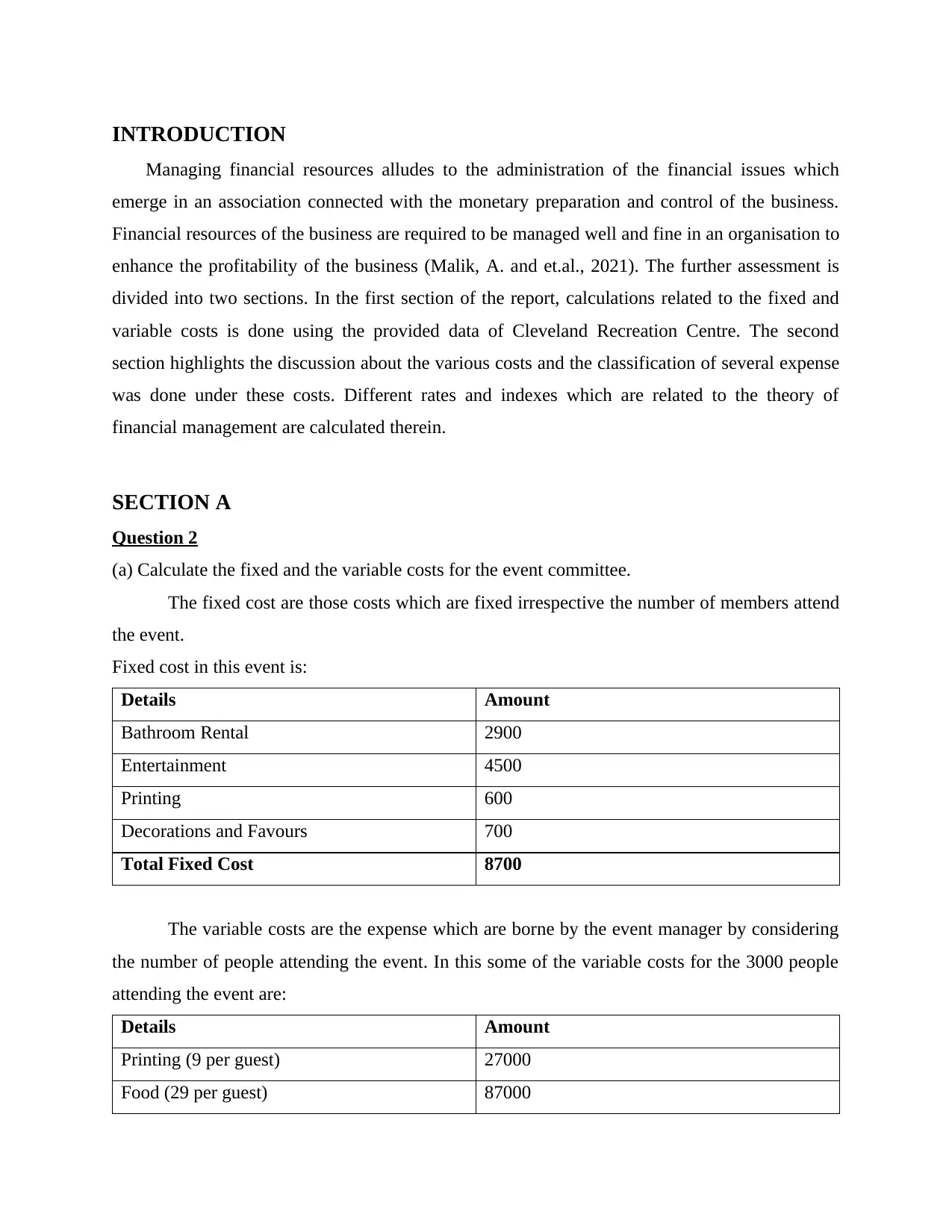

INTRODUCTION

Managing financial resources alludes to the administration of the financial issues which

emerge in an association connected with the monetary preparation and control of the business.

Financial resources of the business are required to be managed well and fine in an organisation to

enhance the profitability of the business (Malik, A. and et.al., 2021). The further assessment is

divided into two sections. In the first section of the report, calculations related to the fixed and

variable costs is done using the provided data of Cleveland Recreation Centre. The second

section highlights the discussion about the various costs and the classification of several expense

was done under these costs. Different rates and indexes which are related to the theory of

financial management are calculated therein.

SECTION A

Question 2

(a) Calculate the fixed and the variable costs for the event committee.

The fixed cost are those costs which are fixed irrespective the number of members attend

the event.

Fixed cost in this event is:

Details Amount

Bathroom Rental 2900

Entertainment 4500

Printing 600

Decorations and Favours 700

Total Fixed Cost 8700

The variable costs are the expense which are borne by the event manager by considering

the number of people attending the event. In this some of the variable costs for the 3000 people

attending the event are:

Details Amount

Printing (9 per guest) 27000

Food (29 per guest) 87000

Managing financial resources alludes to the administration of the financial issues which

emerge in an association connected with the monetary preparation and control of the business.

Financial resources of the business are required to be managed well and fine in an organisation to

enhance the profitability of the business (Malik, A. and et.al., 2021). The further assessment is

divided into two sections. In the first section of the report, calculations related to the fixed and

variable costs is done using the provided data of Cleveland Recreation Centre. The second

section highlights the discussion about the various costs and the classification of several expense

was done under these costs. Different rates and indexes which are related to the theory of

financial management are calculated therein.

SECTION A

Question 2

(a) Calculate the fixed and the variable costs for the event committee.

The fixed cost are those costs which are fixed irrespective the number of members attend

the event.

Fixed cost in this event is:

Details Amount

Bathroom Rental 2900

Entertainment 4500

Printing 600

Decorations and Favours 700

Total Fixed Cost 8700

The variable costs are the expense which are borne by the event manager by considering

the number of people attending the event. In this some of the variable costs for the 3000 people

attending the event are:

Details Amount

Printing (9 per guest) 27000

Food (29 per guest) 87000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Decorations and Favours (5 per guest) 15000

Total Fixed Cost 129000

(b) If the charges charged by the Cleveland Recreation Centre by £ 100 per member. Then the

funds that can be raised by the centre will be

= (3000 * 100) – [8700 + (43 * 3000)]

= 300000 – (8700 + 129000)

= 300000 – 137700

= £ 162300.

SECTION B

Question 3

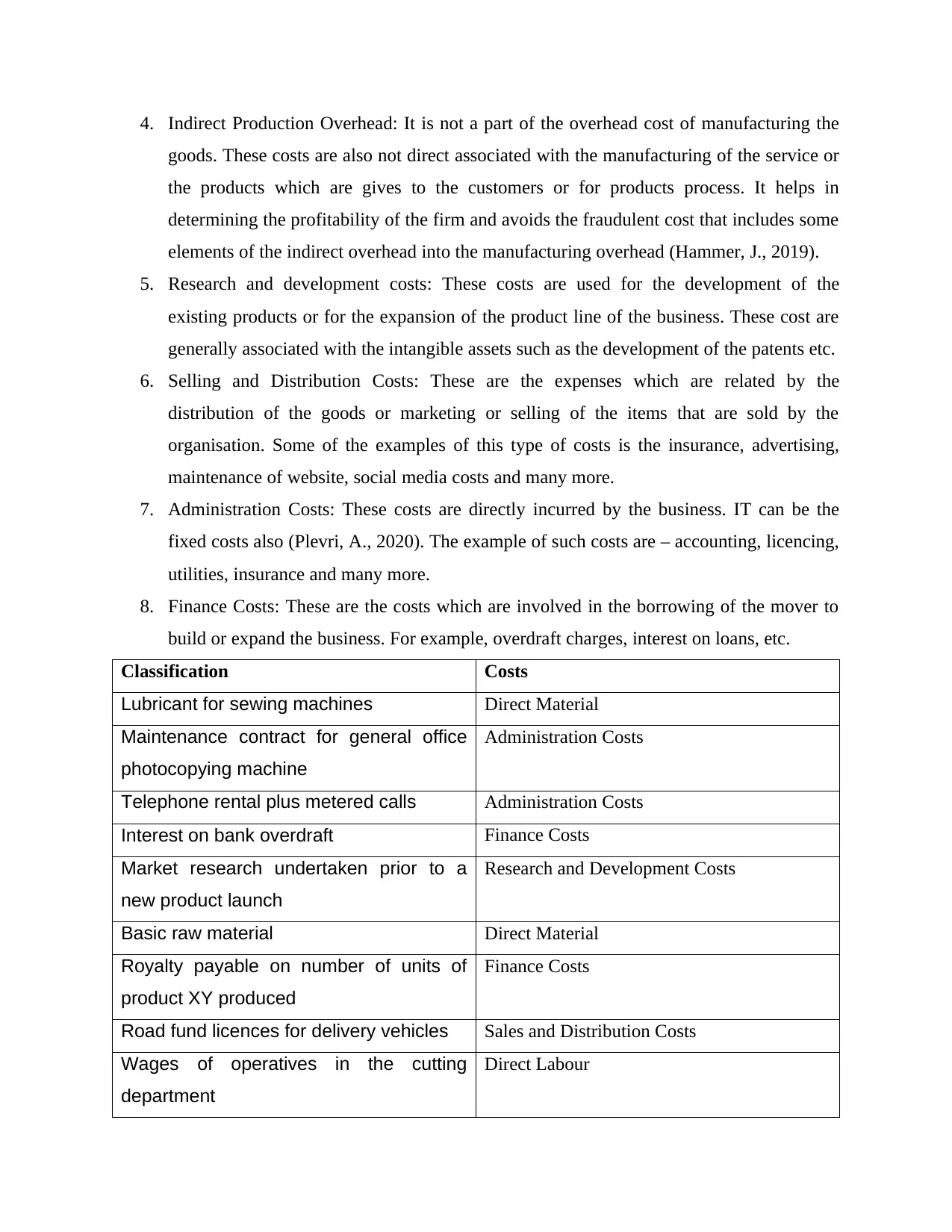

Identify the various expenses given in the under the numerous cost heads.

The several cost which are given for classification can be defined as:

1. Direct Material: These are those materials and supplies that are consumed during the

assembling of an item, and which are straightforwardly related to that item. Things

assigned as immediate materials are normally recorded in the bill of materials document

for an item. The bill of materials orders the unit amounts and standard expenses of all

materials utilized in an item, and may likewise incorporate an overhead allocation. These

cost also includes the scrap expenses borne by the organisation (Swärdh, J.E. and Genell,

A., 2020).

2. Direct Labour: These costs is related to the products which the business manufacture and

the labour used in that production of the goods. Such as the painter, operators, labour

used on the daily wages and many more. In the business which provides services in that

these are the people who provide the services which are directly related to the consumers

such as the lawyers, consultants and many more.

3. Direct Expenses: These expenses are incurred which differ with the changes that re direct

incurred by the volume of the cost of the object. These can be measure by the sales

regions, employees, services, products and much more. In this the material which is used

is used to manufacture the goods and also the cost of freight is included in this (Zurlo, R.

and et.al., 2019).

Total Fixed Cost 129000

(b) If the charges charged by the Cleveland Recreation Centre by £ 100 per member. Then the

funds that can be raised by the centre will be

= (3000 * 100) – [8700 + (43 * 3000)]

= 300000 – (8700 + 129000)

= 300000 – 137700

= £ 162300.

SECTION B

Question 3

Identify the various expenses given in the under the numerous cost heads.

The several cost which are given for classification can be defined as:

1. Direct Material: These are those materials and supplies that are consumed during the

assembling of an item, and which are straightforwardly related to that item. Things

assigned as immediate materials are normally recorded in the bill of materials document

for an item. The bill of materials orders the unit amounts and standard expenses of all

materials utilized in an item, and may likewise incorporate an overhead allocation. These

cost also includes the scrap expenses borne by the organisation (Swärdh, J.E. and Genell,

A., 2020).

2. Direct Labour: These costs is related to the products which the business manufacture and

the labour used in that production of the goods. Such as the painter, operators, labour

used on the daily wages and many more. In the business which provides services in that

these are the people who provide the services which are directly related to the consumers

such as the lawyers, consultants and many more.

3. Direct Expenses: These expenses are incurred which differ with the changes that re direct

incurred by the volume of the cost of the object. These can be measure by the sales

regions, employees, services, products and much more. In this the material which is used

is used to manufacture the goods and also the cost of freight is included in this (Zurlo, R.

and et.al., 2019).

4. Indirect Production Overhead: It is not a part of the overhead cost of manufacturing the

goods. These costs are also not direct associated with the manufacturing of the service or

the products which are gives to the customers or for products process. It helps in

determining the profitability of the firm and avoids the fraudulent cost that includes some

elements of the indirect overhead into the manufacturing overhead (Hammer, J., 2019).

5. Research and development costs: These costs are used for the development of the

existing products or for the expansion of the product line of the business. These cost are

generally associated with the intangible assets such as the development of the patents etc.

6. Selling and Distribution Costs: These are the expenses which are related by the

distribution of the goods or marketing or selling of the items that are sold by the

organisation. Some of the examples of this type of costs is the insurance, advertising,

maintenance of website, social media costs and many more.

7. Administration Costs: These costs are directly incurred by the business. IT can be the

fixed costs also (Plevri, A., 2020). The example of such costs are – accounting, licencing,

utilities, insurance and many more.

8. Finance Costs: These are the costs which are involved in the borrowing of the mover to

build or expand the business. For example, overdraft charges, interest on loans, etc.

Classification Costs

Lubricant for sewing machines Direct Material

Maintenance contract for general office

photocopying machine

Administration Costs

Telephone rental plus metered calls Administration Costs

Interest on bank overdraft Finance Costs

Market research undertaken prior to a

new product launch

Research and Development Costs

Basic raw material Direct Material

Royalty payable on number of units of

product XY produced

Finance Costs

Road fund licences for delivery vehicles Sales and Distribution Costs

Wages of operatives in the cutting

department

Direct Labour

goods. These costs are also not direct associated with the manufacturing of the service or

the products which are gives to the customers or for products process. It helps in

determining the profitability of the firm and avoids the fraudulent cost that includes some

elements of the indirect overhead into the manufacturing overhead (Hammer, J., 2019).

5. Research and development costs: These costs are used for the development of the

existing products or for the expansion of the product line of the business. These cost are

generally associated with the intangible assets such as the development of the patents etc.

6. Selling and Distribution Costs: These are the expenses which are related by the

distribution of the goods or marketing or selling of the items that are sold by the

organisation. Some of the examples of this type of costs is the insurance, advertising,

maintenance of website, social media costs and many more.

7. Administration Costs: These costs are directly incurred by the business. IT can be the

fixed costs also (Plevri, A., 2020). The example of such costs are – accounting, licencing,

utilities, insurance and many more.

8. Finance Costs: These are the costs which are involved in the borrowing of the mover to

build or expand the business. For example, overdraft charges, interest on loans, etc.

Classification Costs

Lubricant for sewing machines Direct Material

Maintenance contract for general office

photocopying machine

Administration Costs

Telephone rental plus metered calls Administration Costs

Interest on bank overdraft Finance Costs

Market research undertaken prior to a

new product launch

Research and Development Costs

Basic raw material Direct Material

Royalty payable on number of units of

product XY produced

Finance Costs

Road fund licences for delivery vehicles Sales and Distribution Costs

Wages of operatives in the cutting

department

Direct Labour

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Developing a new product in the

laboratory

Research and Development Costs

Question 5

Explain the following with the help of example:

1. Average Daily Rate (ADR) – It is mainly used in the industry of hospitality to compute

the average revenue which is earned on the occupied room in a day. It is the Key

Performance Indicator (KPI) of the industry. The ADR shows how much sales are made

per room on an average basis. The better ADR can be evaluated by its rate. The higher

rate determined the better is the ADR. The growth of it proposes that a hotel is expanding

the cash it's making from leasing rooms. To give an increase in the rate, hotels should

investigate ways of elevating the price of per room (De Koning, P.J., 2021).

The management of the hotels look to expand ADR by concentrating on the

strategies of pricing. This incorporates upselling, cross-sale advancements, and free

offers, for example, free transport services to the nearby air terminal. The general

economy is a major component in setting costs, with lodgings and inns trying to change

room rates to match current interest.

For example; In a hotel there are 300 rooms. So, the total revenue earned will be for So the ADR

for the hotel will be

= 150000 / 300 = £ 500.

2. Revenue per available room (RevPAR): It is a measurement utilized in the business of

the hospitality to gauge its performance. The can be evaluated by multiplying the hotel’s

ADR by the occupancy rate of the hotel. It is additionally determined by dividing an

hotel’s complete revenue of room by the total number of accessible rooms in the period

being estimated.

Average Daily Rate = Rooms Revenue Earned / Number of Rooms

Sold

laboratory

Research and Development Costs

Question 5

Explain the following with the help of example:

1. Average Daily Rate (ADR) – It is mainly used in the industry of hospitality to compute

the average revenue which is earned on the occupied room in a day. It is the Key

Performance Indicator (KPI) of the industry. The ADR shows how much sales are made

per room on an average basis. The better ADR can be evaluated by its rate. The higher

rate determined the better is the ADR. The growth of it proposes that a hotel is expanding

the cash it's making from leasing rooms. To give an increase in the rate, hotels should

investigate ways of elevating the price of per room (De Koning, P.J., 2021).

The management of the hotels look to expand ADR by concentrating on the

strategies of pricing. This incorporates upselling, cross-sale advancements, and free

offers, for example, free transport services to the nearby air terminal. The general

economy is a major component in setting costs, with lodgings and inns trying to change

room rates to match current interest.

For example; In a hotel there are 300 rooms. So, the total revenue earned will be for So the ADR

for the hotel will be

= 150000 / 300 = £ 500.

2. Revenue per available room (RevPAR): It is a measurement utilized in the business of

the hospitality to gauge its performance. The can be evaluated by multiplying the hotel’s

ADR by the occupancy rate of the hotel. It is additionally determined by dividing an

hotel’s complete revenue of room by the total number of accessible rooms in the period

being estimated.

Average Daily Rate = Rooms Revenue Earned / Number of Rooms

Sold

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

An increment in a property's RevPAR implies that its ARR or its occupancy rate

is improving. In any case, an increment in RevPAR does not really mean better

productivity.

RevPAR neglects to think about the size of the hotel. Thusly, it alone is certainly

not a decent proportion of by and large execution. A lodging might have a lower RevPAR

yet have more rooms that acquire higher incomes.

For example; the hotel has a capacity of 300 rooms, for which the rate of

occupancy is 90 %. So the average cost for the room is £ 200 per day. So the RevPAR

can be computed as –

= 200 * 90 % = £ 180.

3. Average length of stay (ALOS): It alludes to the normal number of days that the rooms

were filled in the hotel. It is for the most part estimated by dividing the total number of

days stayed by all clients during a year by the quantity of releases or discharges

(Stojanovski, J., 2018).

For example; if the room booked is 70 per night in the hotel then in whole year which can

represented by the 14 bookings. So the ALOS will be

= 70 / 14 = 5

It represents that the guests who stayed on an average on 5 nights in the hotel.

4. Occupancy rate, Gross Operating Profit Per Available Room (GOPPAR): It is a KPI

used in the hospitality sector for lodging owners, since it provides them with a thought of

the importance of the hotel for the business.

It is troubled about the quantity of rooms accessible in the hotel, rather than the

number of room that has been sold. Likewise, it sees operating profit, rather than sales

which is generated by selling the rooms of the hotel and it is, subsequently, an excellent

mark of how successful the hotel is.

The gross operating profit can be evaluated by taking the gross income and

deducting the gross expenses borne by the hotel owner. This number can then be divided

by the quantity of rooms accessible in the hotel to give the GOPPAR.

Observing GOPPAR will permit to detect patterns in the genuine business

performance of the lodging house. It very well may be determined consistently, or toward

is improving. In any case, an increment in RevPAR does not really mean better

productivity.

RevPAR neglects to think about the size of the hotel. Thusly, it alone is certainly

not a decent proportion of by and large execution. A lodging might have a lower RevPAR

yet have more rooms that acquire higher incomes.

For example; the hotel has a capacity of 300 rooms, for which the rate of

occupancy is 90 %. So the average cost for the room is £ 200 per day. So the RevPAR

can be computed as –

= 200 * 90 % = £ 180.

3. Average length of stay (ALOS): It alludes to the normal number of days that the rooms

were filled in the hotel. It is for the most part estimated by dividing the total number of

days stayed by all clients during a year by the quantity of releases or discharges

(Stojanovski, J., 2018).

For example; if the room booked is 70 per night in the hotel then in whole year which can

represented by the 14 bookings. So the ALOS will be

= 70 / 14 = 5

It represents that the guests who stayed on an average on 5 nights in the hotel.

4. Occupancy rate, Gross Operating Profit Per Available Room (GOPPAR): It is a KPI

used in the hospitality sector for lodging owners, since it provides them with a thought of

the importance of the hotel for the business.

It is troubled about the quantity of rooms accessible in the hotel, rather than the

number of room that has been sold. Likewise, it sees operating profit, rather than sales

which is generated by selling the rooms of the hotel and it is, subsequently, an excellent

mark of how successful the hotel is.

The gross operating profit can be evaluated by taking the gross income and

deducting the gross expenses borne by the hotel owner. This number can then be divided

by the quantity of rooms accessible in the hotel to give the GOPPAR.

Observing GOPPAR will permit to detect patterns in the genuine business

performance of the lodging house. It very well may be determined consistently, or toward

the finish of a year by dividing the operating profit by the total daily rooms that are

accessible throughout the span of the year.

For example; the total rooms in a hotel is 150 available for 365 days in a year.

The revenue generated by the hotel is 6000000 and the expenses are 2850000. So here

the

Gross Operating Profit = Revenue – Expenses

= 6000000 – 2850000 = £ 3150000

The GOPPAR = GOP / Number of total room available in a year

= 3150000 / (150 * 365)

= 3150000 - 54750 = 57

5. Market Penetration Index (MPI): It is a proportion of how much an item or service is

being utilized by clients contrasted with the total estimated market for that goods or

services. It can likewise be utilized in creating techniques utilized to build the market

share of the overall industry of the products. It can be utilized to decide the size of the

possible market. Assuming the complete market is huge, new business might enter in the

which may be stimulated that they can acquire market share.

It is a unit of estimation used to show the how your lodging's occupancy contrast

with the set of competitors which are previously set. This is especially useful in showing

how your business is doing according to your opposition and the market overall.

MPI = Occupancy rate / Competitor’s set occupancy rate

For Example; a hotel has an occupancy rate of 90 % and the competitor’s occupancy rate is

85 %. So the MPI will be

MPI = 90 / 85 = 1.05

It means that the contrasted clients which come in the hotel in of 1.05 %.

CONCLUSION

The above assessment can be concluded by saying that management of financial resources is

a crucial prospect for the business to achieve success. This management can be done using

different accounting and management theories. Different costs are highlighted in the report

which have been calculated with all the workings provided therein. The variable cost and the

fixed costs are calculated using the different formulations and the methods of cost accounting.

accessible throughout the span of the year.

For example; the total rooms in a hotel is 150 available for 365 days in a year.

The revenue generated by the hotel is 6000000 and the expenses are 2850000. So here

the

Gross Operating Profit = Revenue – Expenses

= 6000000 – 2850000 = £ 3150000

The GOPPAR = GOP / Number of total room available in a year

= 3150000 / (150 * 365)

= 3150000 - 54750 = 57

5. Market Penetration Index (MPI): It is a proportion of how much an item or service is

being utilized by clients contrasted with the total estimated market for that goods or

services. It can likewise be utilized in creating techniques utilized to build the market

share of the overall industry of the products. It can be utilized to decide the size of the

possible market. Assuming the complete market is huge, new business might enter in the

which may be stimulated that they can acquire market share.

It is a unit of estimation used to show the how your lodging's occupancy contrast

with the set of competitors which are previously set. This is especially useful in showing

how your business is doing according to your opposition and the market overall.

MPI = Occupancy rate / Competitor’s set occupancy rate

For Example; a hotel has an occupancy rate of 90 % and the competitor’s occupancy rate is

85 %. So the MPI will be

MPI = 90 / 85 = 1.05

It means that the contrasted clients which come in the hotel in of 1.05 %.

CONCLUSION

The above assessment can be concluded by saying that management of financial resources is

a crucial prospect for the business to achieve success. This management can be done using

different accounting and management theories. Different costs are highlighted in the report

which have been calculated with all the workings provided therein. The variable cost and the

fixed costs are calculated using the different formulations and the methods of cost accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further the classification of different costs that are occurred in the business are classified into the

actual cost heads in the cost sheet. And the last part discusses how different rates and indexes are

used in the business for its financial management.

actual cost heads in the cost sheet. And the last part discusses how different rates and indexes are

used in the business for its financial management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

De Koning, P.J., 2021. CDR in Belgium: The Special Place of the Belgian Residual ADR Body.

In New Pathways to Civil Justice in Europe. (pp. 131-148). Springer, Cham.

Hammer, J., 2019. This is Revenue Management: How the Best Revenue Managers Create

Massive Value. Johan Hammer.

Malik, A. and et.al., 2021. Managing sustainability using financial accounting data: The value of

input-output analysis. Journal of Cleaner Production. 293. p.126128.

Plevri, A., 2020. Alternative Dispute Resolution (ADR) & Online Dispute Resolution (ODR) for

EU Consumers: The European and Cypriot Framework. In EU Internet Law in the

Digital Era. (pp. 367-392). Springer, Cham.

Stojanovski, J., 2018, November. Consistency of publication types and costs among Croatian

Social Sciences journals. In Septentrio Conference Series (No. 1).

Swärdh, J.E. and Genell, A., 2020. Marginal costs of road noise: Estimation, differentiation and

policy implications. Transport Policy. 88. pp.24-32.

Zurlo, R. and et.al., 2019. Tunnel costs related to the quality of the rock mass. In Tunnels and

Underground Cities: Engineering and Innovation meet Archaeology, Architecture and

Art. (pp. 4289-4298). CRC Press.

Books and Journals

De Koning, P.J., 2021. CDR in Belgium: The Special Place of the Belgian Residual ADR Body.

In New Pathways to Civil Justice in Europe. (pp. 131-148). Springer, Cham.

Hammer, J., 2019. This is Revenue Management: How the Best Revenue Managers Create

Massive Value. Johan Hammer.

Malik, A. and et.al., 2021. Managing sustainability using financial accounting data: The value of

input-output analysis. Journal of Cleaner Production. 293. p.126128.

Plevri, A., 2020. Alternative Dispute Resolution (ADR) & Online Dispute Resolution (ODR) for

EU Consumers: The European and Cypriot Framework. In EU Internet Law in the

Digital Era. (pp. 367-392). Springer, Cham.

Stojanovski, J., 2018, November. Consistency of publication types and costs among Croatian

Social Sciences journals. In Septentrio Conference Series (No. 1).

Swärdh, J.E. and Genell, A., 2020. Marginal costs of road noise: Estimation, differentiation and

policy implications. Transport Policy. 88. pp.24-32.

Zurlo, R. and et.al., 2019. Tunnel costs related to the quality of the rock mass. In Tunnels and

Underground Cities: Engineering and Innovation meet Archaeology, Architecture and

Art. (pp. 4289-4298). CRC Press.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.