Comprehensive Finance Report: Clariton Antique Ltd Financial Analysis

VerifiedAdded on 2020/01/28

|18

|5091

|100

Report

AI Summary

This report provides a comprehensive analysis of financial resources and decisions, using Clariton Antique Ltd as a case study. It begins by identifying and evaluating various sources of finance, including internal and external options like retained earnings, owner’s capital, debt financing, and equity financing, assessing their implications and costs. The report then delves into financial planning, emphasizing the importance of budgeting and assessing the information needs of different stakeholders such as partners, venture capitalists, and finance brokers. A key component is the preparation and analysis of a cash budget, alongside calculations for per-unit costs and pricing decisions. Furthermore, the report assesses the viability of projects and explores different financial statement formats, comparing them in relation to organizational structure, and interpreting relevant financial ratios to assess the financial health and performance of the company. The analysis includes the impact of finance on financial statements and concludes with recommendations based on the findings.

Managing financial resources

and decisions

and decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

1.1 Identify the sources of finance...........................................................................................................3

1.2 Assess the implications of sources of finance....................................................................................3

1.3 Evaluate the sources of finance..........................................................................................................4

TASK 2..........................................................................................................................................................4

2.1Analyse the cost of sources of finance................................................................................................4

2.2 Explain the importance of financial planning....................................................................................5

2.3 Assess the information needs of users of finance...............................................................................5

2.4 Impact of finance on financial statements..........................................................................................6

TASK 3..........................................................................................................................................................7

3.1 Prepare cash budget and analyze......................................................................................................7

3.2 Calculation per unit and pricing decision...........................................................................................9

3.3 Assess the viability of projects........................................................................................................10

TASK 4........................................................................................................................................................13

4.1 Explain different financial statements format..................................................................................13

4.2 Compare different formats of financial statements with different organization structure................14

4.3 Interpretations of ratios....................................................................................................................16

CONCLUSION.............................................................................................................................................19

REFERENCES..............................................................................................................................................19

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

1.1 Identify the sources of finance...........................................................................................................3

1.2 Assess the implications of sources of finance....................................................................................3

1.3 Evaluate the sources of finance..........................................................................................................4

TASK 2..........................................................................................................................................................4

2.1Analyse the cost of sources of finance................................................................................................4

2.2 Explain the importance of financial planning....................................................................................5

2.3 Assess the information needs of users of finance...............................................................................5

2.4 Impact of finance on financial statements..........................................................................................6

TASK 3..........................................................................................................................................................7

3.1 Prepare cash budget and analyze......................................................................................................7

3.2 Calculation per unit and pricing decision...........................................................................................9

3.3 Assess the viability of projects........................................................................................................10

TASK 4........................................................................................................................................................13

4.1 Explain different financial statements format..................................................................................13

4.2 Compare different formats of financial statements with different organization structure................14

4.3 Interpretations of ratios....................................................................................................................16

CONCLUSION.............................................................................................................................................19

REFERENCES..............................................................................................................................................19

INTRODUCTION

Role of finance has increases which act as a fortune teller who identifies financial crisis

incurred in the future to rectify the deficiency of the business. Clariton Antique Ltd has been

selected in this report in explaining the importance of finance. This focuses on selecting finance

and assessed on various parameters. The cost of finance are assessed which further help in

selection of the best suitable sources of finance. Capital budgeting tools and ratio analysis are

applied by an entity in assessing viability of the business proposals.

TASK 1

1.1 Identify the sources of finance

Unincorporated users- The players of the business who have no legal identity in the eyes of law

as are not registered under the law (Kaplan and Atkinson, 2015). The companies who have not

registered in the companies act are not abiding by their rules and regulations.

Retained earnings-The commonly use internal source of finance which is personal property of

an individual. This amount generated after giving dividends out of the total profit earned by an

individual. This is often represents as secret profit kept by the owner as savings in form of

reserves to meet uncertainty. The current reserve will help in improving the efficiency of the

existing business.

Owner’s capital- Savings of an individual are used in meeting the funding requirement of the

business. The capital infused by the owner in their current business will generate minimum

return for all the business players. The efficiency of enterprises will get increases when the

investment has increases by applying their own resources in their business.

Incorporated business- The business which has registered in the companies act and other

federal and state laws has legal recognition in the outside business environment. The registration

of the business enterprise will provide further recognition form of public or private companies.

Debt financing- Cheapest sources of finance in the business and their capital structure are debt

finance. It is that kind of external sources of finance which is based on asset in which assets are

given on collateral security in order to get finance.

Equity cash flow- Applications are invited by sending offer to take up the shares of the business

enterprise. The shares are issues in order to accomplish the business requirements in order to

strengthen the existing resources.

1.2 Assess the implications of sources of finance

Internal sources of finance

Role of finance has increases which act as a fortune teller who identifies financial crisis

incurred in the future to rectify the deficiency of the business. Clariton Antique Ltd has been

selected in this report in explaining the importance of finance. This focuses on selecting finance

and assessed on various parameters. The cost of finance are assessed which further help in

selection of the best suitable sources of finance. Capital budgeting tools and ratio analysis are

applied by an entity in assessing viability of the business proposals.

TASK 1

1.1 Identify the sources of finance

Unincorporated users- The players of the business who have no legal identity in the eyes of law

as are not registered under the law (Kaplan and Atkinson, 2015). The companies who have not

registered in the companies act are not abiding by their rules and regulations.

Retained earnings-The commonly use internal source of finance which is personal property of

an individual. This amount generated after giving dividends out of the total profit earned by an

individual. This is often represents as secret profit kept by the owner as savings in form of

reserves to meet uncertainty. The current reserve will help in improving the efficiency of the

existing business.

Owner’s capital- Savings of an individual are used in meeting the funding requirement of the

business. The capital infused by the owner in their current business will generate minimum

return for all the business players. The efficiency of enterprises will get increases when the

investment has increases by applying their own resources in their business.

Incorporated business- The business which has registered in the companies act and other

federal and state laws has legal recognition in the outside business environment. The registration

of the business enterprise will provide further recognition form of public or private companies.

Debt financing- Cheapest sources of finance in the business and their capital structure are debt

finance. It is that kind of external sources of finance which is based on asset in which assets are

given on collateral security in order to get finance.

Equity cash flow- Applications are invited by sending offer to take up the shares of the business

enterprise. The shares are issues in order to accomplish the business requirements in order to

strengthen the existing resources.

1.2 Assess the implications of sources of finance

Internal sources of finance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings-It helps in boosting the performance of an entity as this utilizes the secret

profit in own business. This improves the economic growth of an enterprise in which existing

resources are utilized by an entity in accomplishing their goals and the objectives. This further

generated after paying taxes and dividends which remains with less amount.

Owner’s capital-The possession of the money are held with an entity in order to invest the

money in their business. The money can be invested by an entity according to their business

nature and requirements.

External sources of finance

Debt financing- The initial benefit of the enjoyed by the business by using these sources of

finance is that it can be taken in any quantity (Epstein and Buhovac, 2014). The obligation

involved in taking these sources of finance involves interest paid on the loan by depositing

collateral security with the bank or any kinds of financial institutions. This source of finance is

regarded as cheapest sources of finance as it doesn’t carry long term debt obligations.

Equity financing- This is another important sources of finance which helps in building

appropriate capital structure of the business concern. The cash flow increases by an entity as the

amount taken from all the shareholders to be kept by the owner for long term till the wound of

the business. This source of finance involves payment of dividend and all other legal and

agreement fees to be incurred in issuing equity shares. The maintenance of the issued shares is

essential in order to maintain the existing position.

1.3 Evaluate the sources of finance

Internal sources of finance- The internal sources of finance will includes retained earnings and

owner’s capital held by an enterprise for log term in their business. The internal capability of an

individual will be improved with the passage of time as it enhances the capability of the

organization.

External sources- The higher obligations covered while using these kinds of financial resources

which involve debt and equity financing as one of the commonly used techniques. The cost of

dividend and paying interest on the amount taken will involve additionally.

It can be recommended to the business to choose retained earnings as one of the

important sources of finance for an enterprise.

TASK 2

2.1Analyse the cost of sources of finance

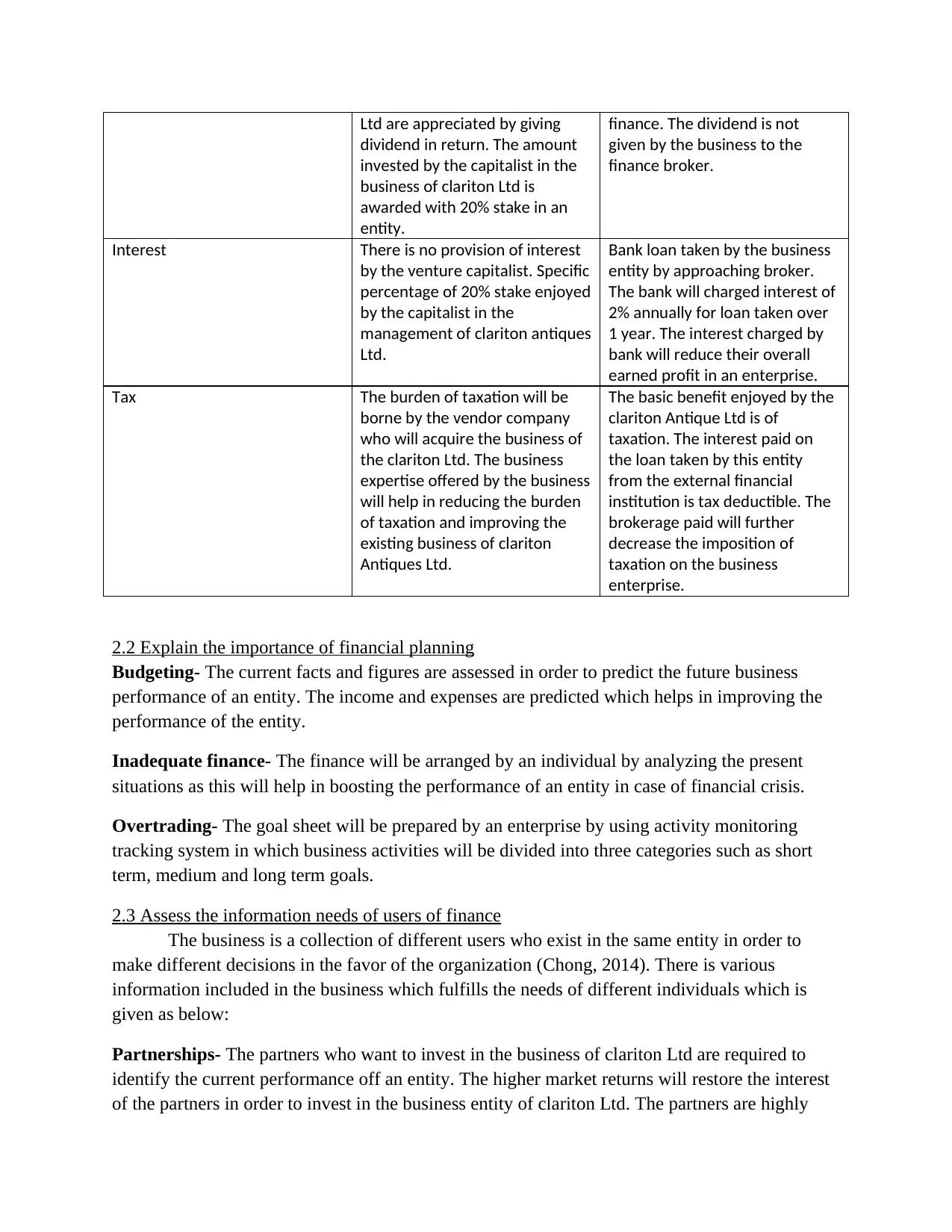

Basis Venture capitalist Finance broker

Dividends The amount given to all the

shareholders for applying their

money in the business of clariton

The term dividend will not affect

the business in terms of using

these particular sources of

profit in own business. This improves the economic growth of an enterprise in which existing

resources are utilized by an entity in accomplishing their goals and the objectives. This further

generated after paying taxes and dividends which remains with less amount.

Owner’s capital-The possession of the money are held with an entity in order to invest the

money in their business. The money can be invested by an entity according to their business

nature and requirements.

External sources of finance

Debt financing- The initial benefit of the enjoyed by the business by using these sources of

finance is that it can be taken in any quantity (Epstein and Buhovac, 2014). The obligation

involved in taking these sources of finance involves interest paid on the loan by depositing

collateral security with the bank or any kinds of financial institutions. This source of finance is

regarded as cheapest sources of finance as it doesn’t carry long term debt obligations.

Equity financing- This is another important sources of finance which helps in building

appropriate capital structure of the business concern. The cash flow increases by an entity as the

amount taken from all the shareholders to be kept by the owner for long term till the wound of

the business. This source of finance involves payment of dividend and all other legal and

agreement fees to be incurred in issuing equity shares. The maintenance of the issued shares is

essential in order to maintain the existing position.

1.3 Evaluate the sources of finance

Internal sources of finance- The internal sources of finance will includes retained earnings and

owner’s capital held by an enterprise for log term in their business. The internal capability of an

individual will be improved with the passage of time as it enhances the capability of the

organization.

External sources- The higher obligations covered while using these kinds of financial resources

which involve debt and equity financing as one of the commonly used techniques. The cost of

dividend and paying interest on the amount taken will involve additionally.

It can be recommended to the business to choose retained earnings as one of the

important sources of finance for an enterprise.

TASK 2

2.1Analyse the cost of sources of finance

Basis Venture capitalist Finance broker

Dividends The amount given to all the

shareholders for applying their

money in the business of clariton

The term dividend will not affect

the business in terms of using

these particular sources of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ltd are appreciated by giving

dividend in return. The amount

invested by the capitalist in the

business of clariton Ltd is

awarded with 20% stake in an

entity.

finance. The dividend is not

given by the business to the

finance broker.

Interest There is no provision of interest

by the venture capitalist. Specific

percentage of 20% stake enjoyed

by the capitalist in the

management of clariton antiques

Ltd.

Bank loan taken by the business

entity by approaching broker.

The bank will charged interest of

2% annually for loan taken over

1 year. The interest charged by

bank will reduce their overall

earned profit in an enterprise.

Tax The burden of taxation will be

borne by the vendor company

who will acquire the business of

the clariton Ltd. The business

expertise offered by the business

will help in reducing the burden

of taxation and improving the

existing business of clariton

Antiques Ltd.

The basic benefit enjoyed by the

clariton Antique Ltd is of

taxation. The interest paid on

the loan taken by this entity

from the external financial

institution is tax deductible. The

brokerage paid will further

decrease the imposition of

taxation on the business

enterprise.

2.2 Explain the importance of financial planning

Budgeting- The current facts and figures are assessed in order to predict the future business

performance of an entity. The income and expenses are predicted which helps in improving the

performance of the entity.

Inadequate finance- The finance will be arranged by an individual by analyzing the present

situations as this will help in boosting the performance of an entity in case of financial crisis.

Overtrading- The goal sheet will be prepared by an enterprise by using activity monitoring

tracking system in which business activities will be divided into three categories such as short

term, medium and long term goals.

2.3 Assess the information needs of users of finance

The business is a collection of different users who exist in the same entity in order to

make different decisions in the favor of the organization (Chong, 2014). There is various

information included in the business which fulfills the needs of different individuals which is

given as below:

Partnerships- The partners who want to invest in the business of clariton Ltd are required to

identify the current performance off an entity. The higher market returns will restore the interest

of the partners in order to invest in the business entity of clariton Ltd. The partners are highly

dividend in return. The amount

invested by the capitalist in the

business of clariton Ltd is

awarded with 20% stake in an

entity.

finance. The dividend is not

given by the business to the

finance broker.

Interest There is no provision of interest

by the venture capitalist. Specific

percentage of 20% stake enjoyed

by the capitalist in the

management of clariton antiques

Ltd.

Bank loan taken by the business

entity by approaching broker.

The bank will charged interest of

2% annually for loan taken over

1 year. The interest charged by

bank will reduce their overall

earned profit in an enterprise.

Tax The burden of taxation will be

borne by the vendor company

who will acquire the business of

the clariton Ltd. The business

expertise offered by the business

will help in reducing the burden

of taxation and improving the

existing business of clariton

Antiques Ltd.

The basic benefit enjoyed by the

clariton Antique Ltd is of

taxation. The interest paid on

the loan taken by this entity

from the external financial

institution is tax deductible. The

brokerage paid will further

decrease the imposition of

taxation on the business

enterprise.

2.2 Explain the importance of financial planning

Budgeting- The current facts and figures are assessed in order to predict the future business

performance of an entity. The income and expenses are predicted which helps in improving the

performance of the entity.

Inadequate finance- The finance will be arranged by an individual by analyzing the present

situations as this will help in boosting the performance of an entity in case of financial crisis.

Overtrading- The goal sheet will be prepared by an enterprise by using activity monitoring

tracking system in which business activities will be divided into three categories such as short

term, medium and long term goals.

2.3 Assess the information needs of users of finance

The business is a collection of different users who exist in the same entity in order to

make different decisions in the favor of the organization (Chong, 2014). There is various

information included in the business which fulfills the needs of different individuals which is

given as below:

Partnerships- The partners who want to invest in the business of clariton Ltd are required to

identify the current performance off an entity. The higher market returns will restore the interest

of the partners in order to invest in the business entity of clariton Ltd. The partners are highly

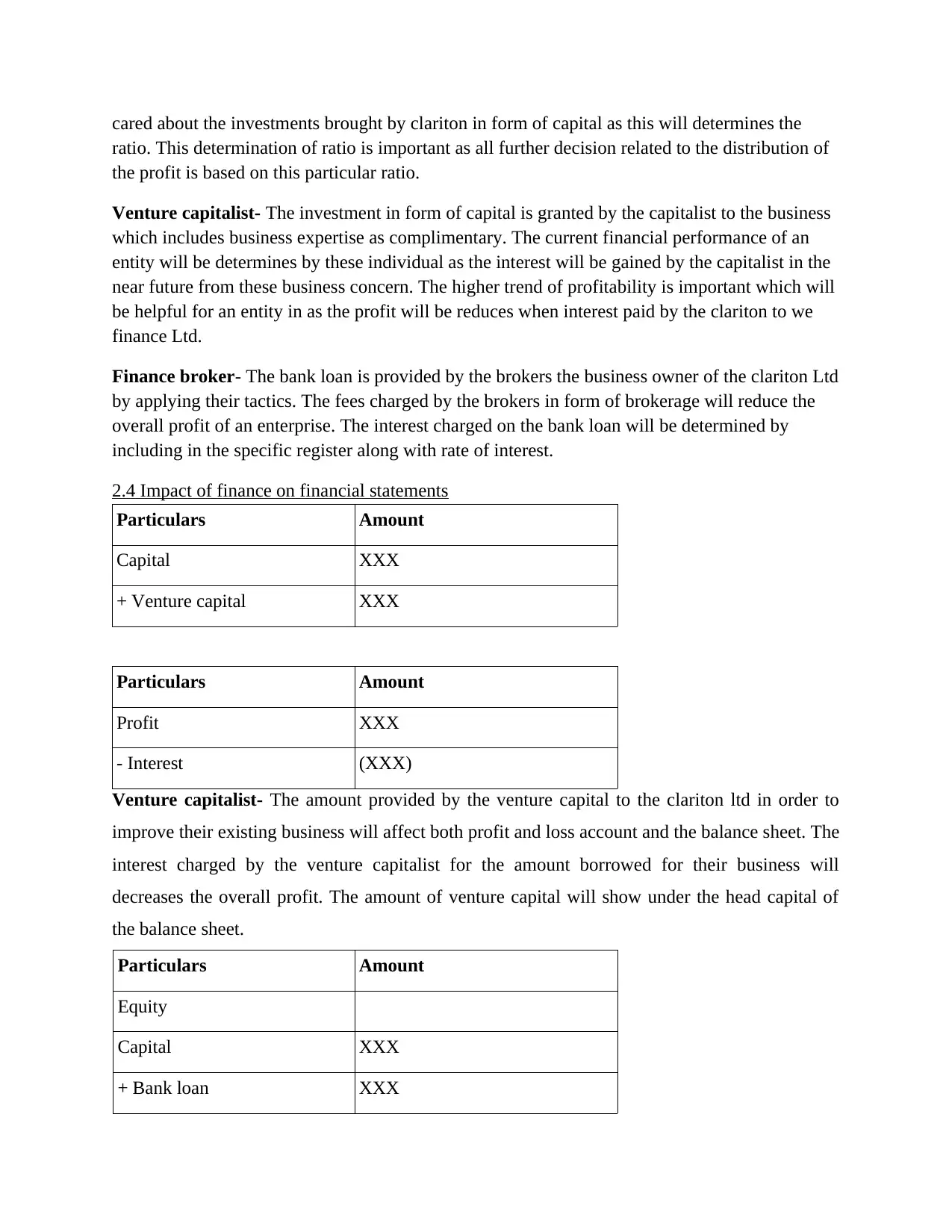

cared about the investments brought by clariton in form of capital as this will determines the

ratio. This determination of ratio is important as all further decision related to the distribution of

the profit is based on this particular ratio.

Venture capitalist- The investment in form of capital is granted by the capitalist to the business

which includes business expertise as complimentary. The current financial performance of an

entity will be determines by these individual as the interest will be gained by the capitalist in the

near future from these business concern. The higher trend of profitability is important which will

be helpful for an entity in as the profit will be reduces when interest paid by the clariton to we

finance Ltd.

Finance broker- The bank loan is provided by the brokers the business owner of the clariton Ltd

by applying their tactics. The fees charged by the brokers in form of brokerage will reduce the

overall profit of an enterprise. The interest charged on the bank loan will be determined by

including in the specific register along with rate of interest.

2.4 Impact of finance on financial statements

Particulars Amount

Capital XXX

+ Venture capital XXX

Particulars Amount

Profit XXX

- Interest (XXX)

Venture capitalist- The amount provided by the venture capital to the clariton ltd in order to

improve their existing business will affect both profit and loss account and the balance sheet. The

interest charged by the venture capitalist for the amount borrowed for their business will

decreases the overall profit. The amount of venture capital will show under the head capital of

the balance sheet.

Particulars Amount

Equity

Capital XXX

+ Bank loan XXX

ratio. This determination of ratio is important as all further decision related to the distribution of

the profit is based on this particular ratio.

Venture capitalist- The investment in form of capital is granted by the capitalist to the business

which includes business expertise as complimentary. The current financial performance of an

entity will be determines by these individual as the interest will be gained by the capitalist in the

near future from these business concern. The higher trend of profitability is important which will

be helpful for an entity in as the profit will be reduces when interest paid by the clariton to we

finance Ltd.

Finance broker- The bank loan is provided by the brokers the business owner of the clariton Ltd

by applying their tactics. The fees charged by the brokers in form of brokerage will reduce the

overall profit of an enterprise. The interest charged on the bank loan will be determined by

including in the specific register along with rate of interest.

2.4 Impact of finance on financial statements

Particulars Amount

Capital XXX

+ Venture capital XXX

Particulars Amount

Profit XXX

- Interest (XXX)

Venture capitalist- The amount provided by the venture capital to the clariton ltd in order to

improve their existing business will affect both profit and loss account and the balance sheet. The

interest charged by the venture capitalist for the amount borrowed for their business will

decreases the overall profit. The amount of venture capital will show under the head capital of

the balance sheet.

Particulars Amount

Equity

Capital XXX

+ Bank loan XXX

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Non Current Liabilities

Bank loan XXX

Particulars Amount

Profit XXX

- Interest@2% (XXX)

-Brokerage@1% (XXX)

Finance broker- The brokers are external party appointed by an entity in order to accomplish

their work without any kind of legal complexities. The legal complications will be decreases by

appointing brokers who will charge fees for providing loan to the business. The brokerage fee

will reduce the profit of the business entity. The interest charged on the loan is 2% payable over

10 years for taking amount of 0.5 million amount. The current amount borrowed by an entity by

approaching the finance broker will increases the capital in the business. At the same time, bank

loan will also incorporated by an entity under the head long term debt in the liabilities section in

the balance sheet.

TASK 3

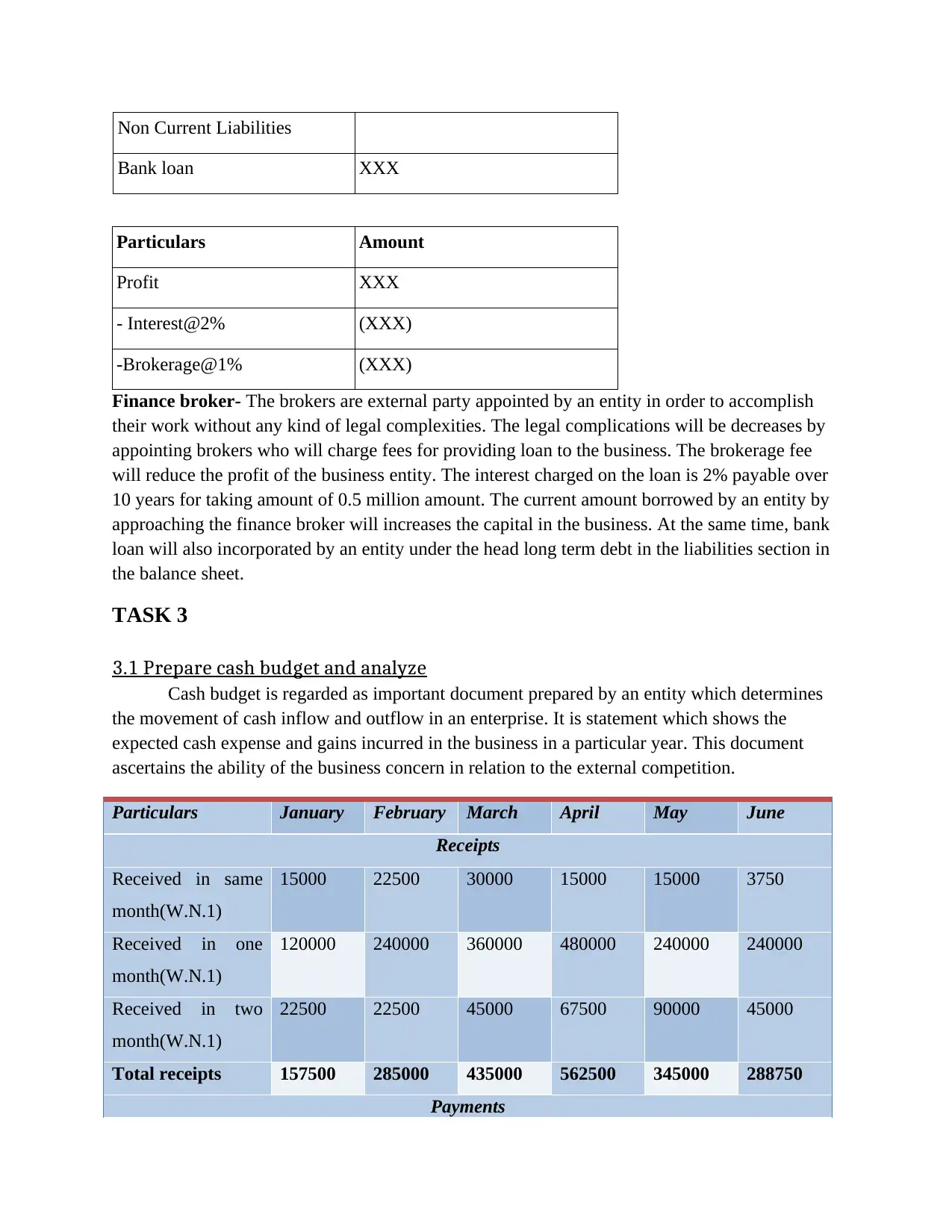

3.1 Prepare cash budget and analyze

Cash budget is regarded as important document prepared by an entity which determines

the movement of cash inflow and outflow in an enterprise. It is statement which shows the

expected cash expense and gains incurred in the business in a particular year. This document

ascertains the ability of the business concern in relation to the external competition.

Particulars January February March April May June

Receipts

Received in same

month(W.N.1)

15000 22500 30000 15000 15000 3750

Received in one

month(W.N.1)

120000 240000 360000 480000 240000 240000

Received in two

month(W.N.1)

22500 22500 45000 67500 90000 45000

Total receipts 157500 285000 435000 562500 345000 288750

Payments

Bank loan XXX

Particulars Amount

Profit XXX

- Interest@2% (XXX)

-Brokerage@1% (XXX)

Finance broker- The brokers are external party appointed by an entity in order to accomplish

their work without any kind of legal complexities. The legal complications will be decreases by

appointing brokers who will charge fees for providing loan to the business. The brokerage fee

will reduce the profit of the business entity. The interest charged on the loan is 2% payable over

10 years for taking amount of 0.5 million amount. The current amount borrowed by an entity by

approaching the finance broker will increases the capital in the business. At the same time, bank

loan will also incorporated by an entity under the head long term debt in the liabilities section in

the balance sheet.

TASK 3

3.1 Prepare cash budget and analyze

Cash budget is regarded as important document prepared by an entity which determines

the movement of cash inflow and outflow in an enterprise. It is statement which shows the

expected cash expense and gains incurred in the business in a particular year. This document

ascertains the ability of the business concern in relation to the external competition.

Particulars January February March April May June

Receipts

Received in same

month(W.N.1)

15000 22500 30000 15000 15000 3750

Received in one

month(W.N.1)

120000 240000 360000 480000 240000 240000

Received in two

month(W.N.1)

22500 22500 45000 67500 90000 45000

Total receipts 157500 285000 435000 562500 345000 288750

Payments

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payment to

suppliers

807250 137250 119750 437250 227250 219750

Shortage/Surplus -649750 147750 315250 125250 117750 69000

Opening cash

balance

110000 -539750 -392000 -76750 48500 166250

Closing cash

balance

-539750 -392000 -76750 48500 166250 235250

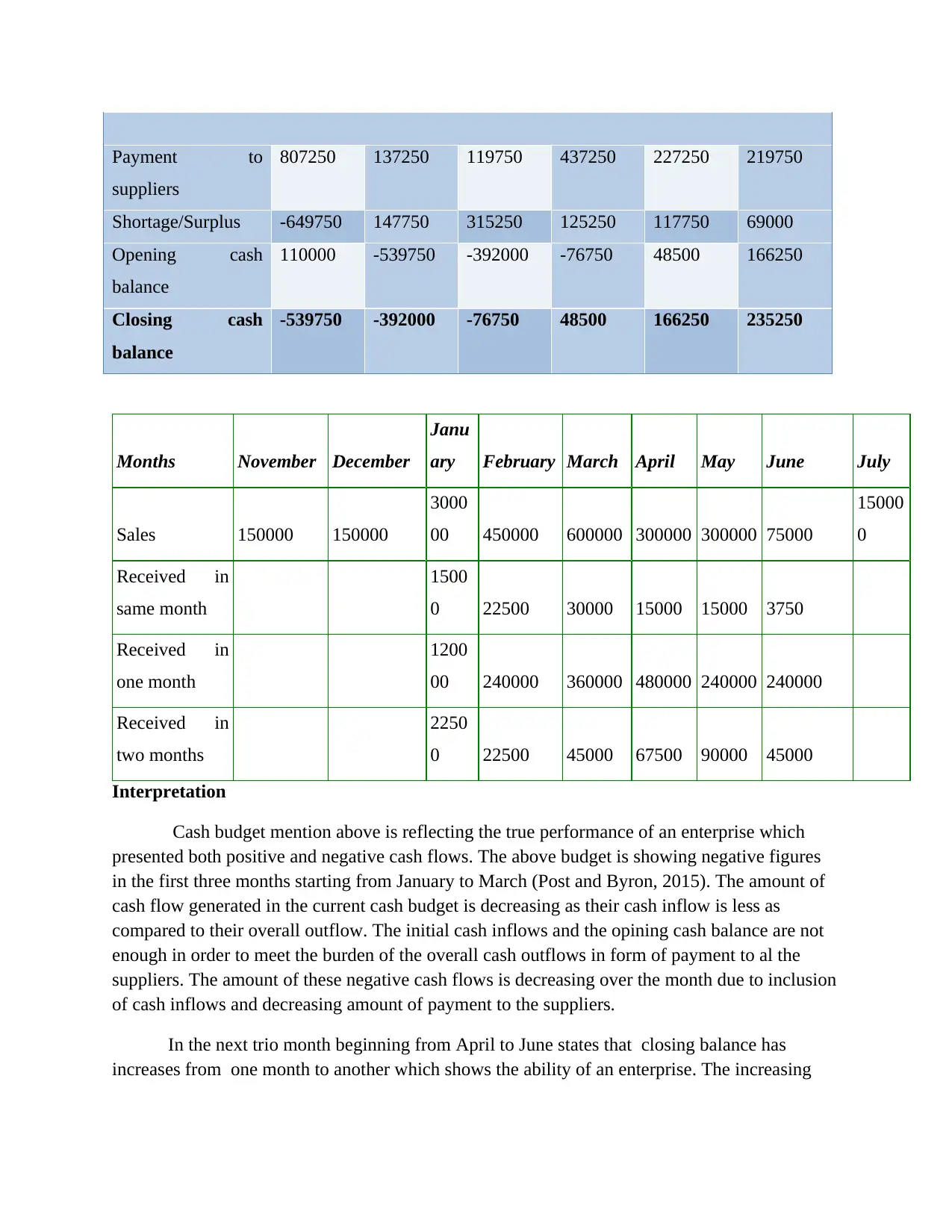

Months November December

Janu

ary February March April May June July

Sales 150000 150000

3000

00 450000 600000 300000 300000 75000

15000

0

Received in

same month

1500

0 22500 30000 15000 15000 3750

Received in

one month

1200

00 240000 360000 480000 240000 240000

Received in

two months

2250

0 22500 45000 67500 90000 45000

Interpretation

Cash budget mention above is reflecting the true performance of an enterprise which

presented both positive and negative cash flows. The above budget is showing negative figures

in the first three months starting from January to March (Post and Byron, 2015). The amount of

cash flow generated in the current cash budget is decreasing as their cash inflow is less as

compared to their overall outflow. The initial cash inflows and the opining cash balance are not

enough in order to meet the burden of the overall cash outflows in form of payment to al the

suppliers. The amount of these negative cash flows is decreasing over the month due to inclusion

of cash inflows and decreasing amount of payment to the suppliers.

In the next trio month beginning from April to June states that closing balance has

increases from one month to another which shows the ability of an enterprise. The increasing

suppliers

807250 137250 119750 437250 227250 219750

Shortage/Surplus -649750 147750 315250 125250 117750 69000

Opening cash

balance

110000 -539750 -392000 -76750 48500 166250

Closing cash

balance

-539750 -392000 -76750 48500 166250 235250

Months November December

Janu

ary February March April May June July

Sales 150000 150000

3000

00 450000 600000 300000 300000 75000

15000

0

Received in

same month

1500

0 22500 30000 15000 15000 3750

Received in

one month

1200

00 240000 360000 480000 240000 240000

Received in

two months

2250

0 22500 45000 67500 90000 45000

Interpretation

Cash budget mention above is reflecting the true performance of an enterprise which

presented both positive and negative cash flows. The above budget is showing negative figures

in the first three months starting from January to March (Post and Byron, 2015). The amount of

cash flow generated in the current cash budget is decreasing as their cash inflow is less as

compared to their overall outflow. The initial cash inflows and the opining cash balance are not

enough in order to meet the burden of the overall cash outflows in form of payment to al the

suppliers. The amount of these negative cash flows is decreasing over the month due to inclusion

of cash inflows and decreasing amount of payment to the suppliers.

In the next trio month beginning from April to June states that closing balance has

increases from one month to another which shows the ability of an enterprise. The increasing

cash flow is good sign of enhancing condition of an entity. There are various ways in which an

entity can control their higher amount of cash inflow which is give as below:

The higher cash flows can be invested in the same entity and in another business

The amount invested today will generate higher returns in the near future.

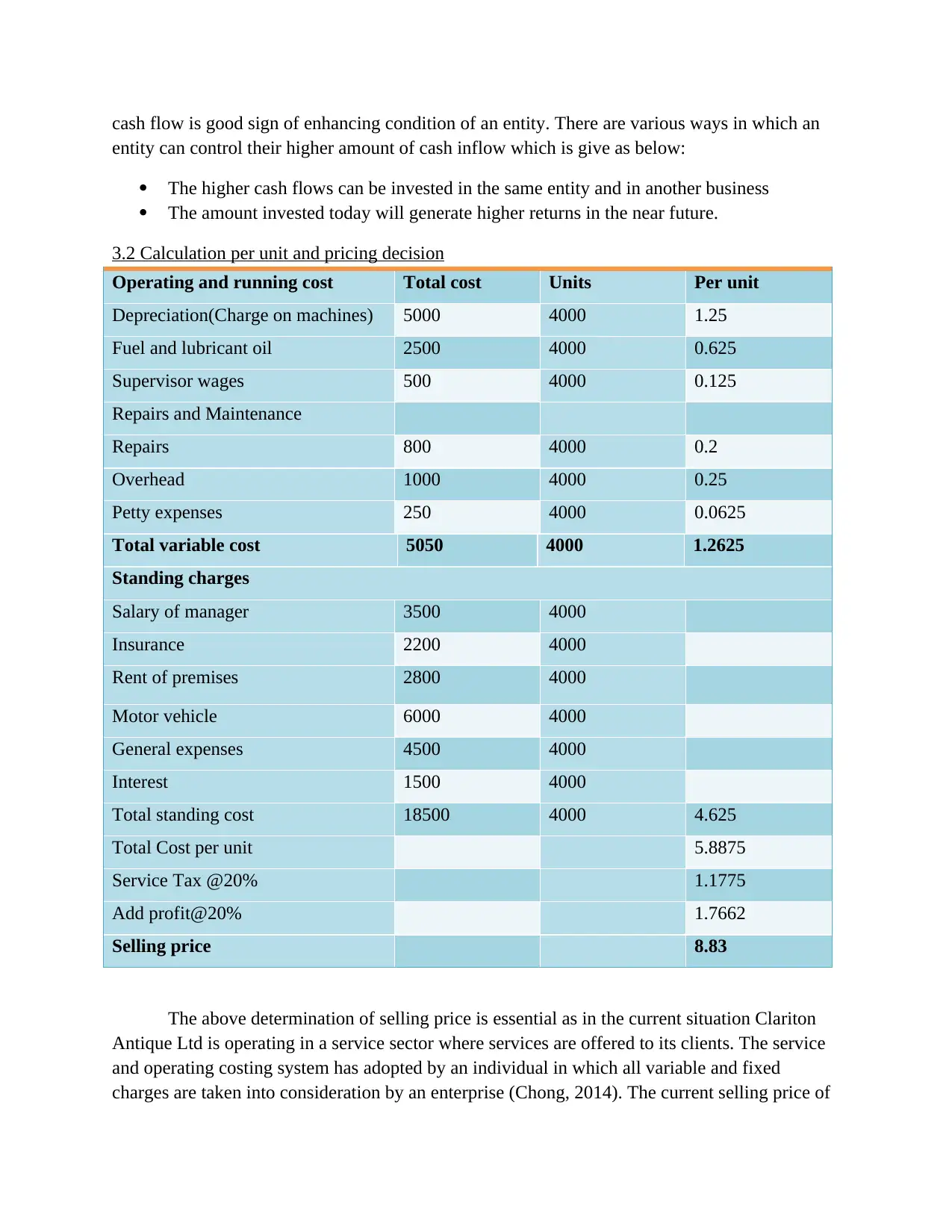

3.2 Calculation per unit and pricing decision

Operating and running cost Total cost Units Per unit

Depreciation(Charge on machines) 5000 4000 1.25

Fuel and lubricant oil 2500 4000 0.625

Supervisor wages 500 4000 0.125

Repairs and Maintenance

Repairs 800 4000 0.2

Overhead 1000 4000 0.25

Petty expenses 250 4000 0.0625

Total variable cost 5050 4000 1.2625

Standing charges

Salary of manager 3500 4000

Insurance 2200 4000

Rent of premises 2800 4000

Motor vehicle 6000 4000

General expenses 4500 4000

Interest 1500 4000

Total standing cost 18500 4000 4.625

Total Cost per unit 5.8875

Service Tax @20% 1.1775

Add profit@20% 1.7662

Selling price 8.83

The above determination of selling price is essential as in the current situation Clariton

Antique Ltd is operating in a service sector where services are offered to its clients. The service

and operating costing system has adopted by an individual in which all variable and fixed

charges are taken into consideration by an enterprise (Chong, 2014). The current selling price of

entity can control their higher amount of cash inflow which is give as below:

The higher cash flows can be invested in the same entity and in another business

The amount invested today will generate higher returns in the near future.

3.2 Calculation per unit and pricing decision

Operating and running cost Total cost Units Per unit

Depreciation(Charge on machines) 5000 4000 1.25

Fuel and lubricant oil 2500 4000 0.625

Supervisor wages 500 4000 0.125

Repairs and Maintenance

Repairs 800 4000 0.2

Overhead 1000 4000 0.25

Petty expenses 250 4000 0.0625

Total variable cost 5050 4000 1.2625

Standing charges

Salary of manager 3500 4000

Insurance 2200 4000

Rent of premises 2800 4000

Motor vehicle 6000 4000

General expenses 4500 4000

Interest 1500 4000

Total standing cost 18500 4000 4.625

Total Cost per unit 5.8875

Service Tax @20% 1.1775

Add profit@20% 1.7662

Selling price 8.83

The above determination of selling price is essential as in the current situation Clariton

Antique Ltd is operating in a service sector where services are offered to its clients. The service

and operating costing system has adopted by an individual in which all variable and fixed

charges are taken into consideration by an enterprise (Chong, 2014). The current selling price of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the business are included the amount of taxation and specific percentage of profit element in the

price of products. Service tax has especially include in this particular pricing as the service are

provided by the seller are required to charge this tax. This is indirect tax whose burden will be

imposed on the buyer.

Value based pricing- This kind of pricing is suitable in case of services provided by the seller to

their variety of customers. The prices are changed for the actual value of the product to different

individuals by using the products.

Target return- the targets are determined by an individual in which minimum amount of profit

margin are charged by the owner by selling their products or services to its variety of customers.

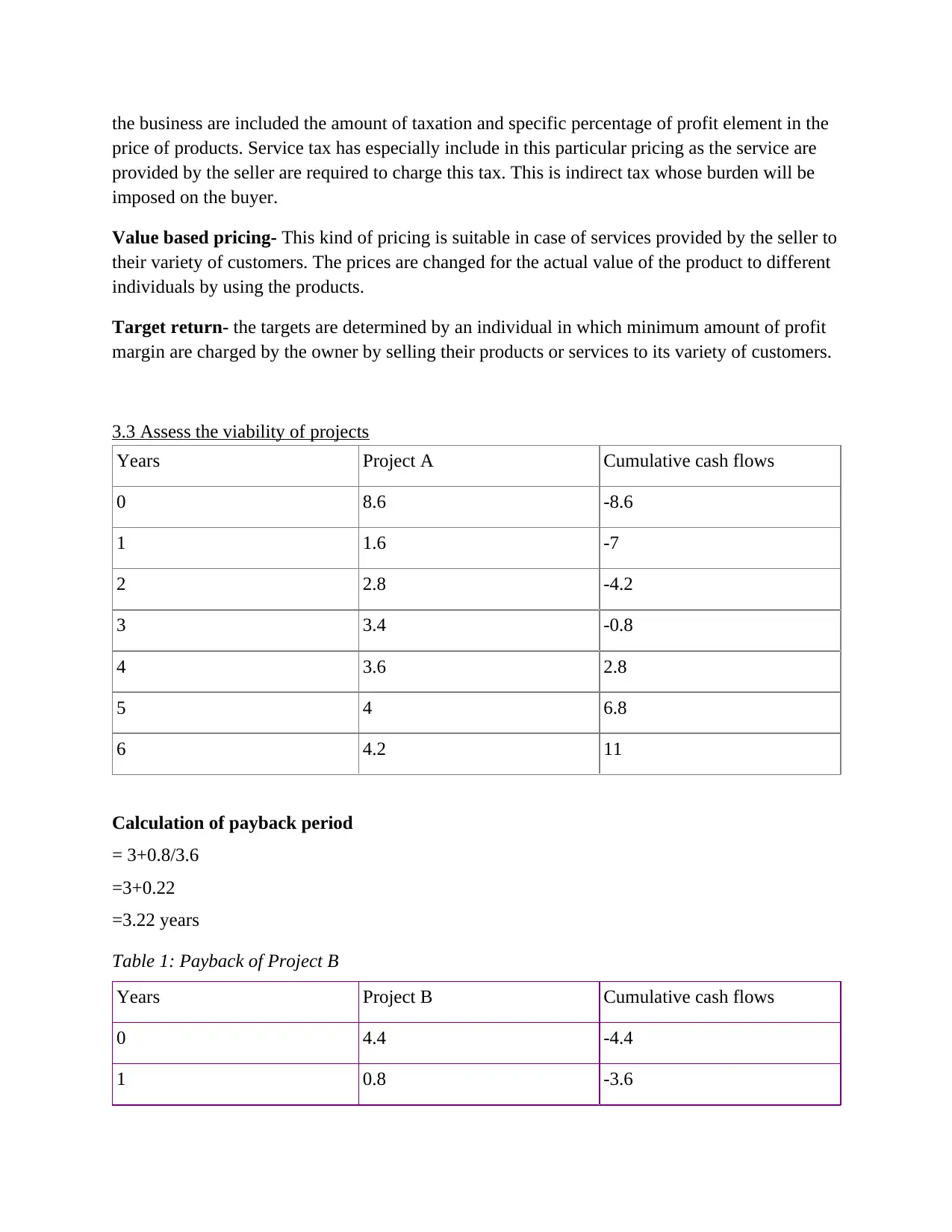

3.3 Assess the viability of projects

Years Project A Cumulative cash flows

0 8.6 -8.6

1 1.6 -7

2 2.8 -4.2

3 3.4 -0.8

4 3.6 2.8

5 4 6.8

6 4.2 11

Calculation of payback period

= 3+0.8/3.6

=3+0.22

=3.22 years

Table 1: Payback of Project B

Years Project B Cumulative cash flows

0 4.4 -4.4

1 0.8 -3.6

price of products. Service tax has especially include in this particular pricing as the service are

provided by the seller are required to charge this tax. This is indirect tax whose burden will be

imposed on the buyer.

Value based pricing- This kind of pricing is suitable in case of services provided by the seller to

their variety of customers. The prices are changed for the actual value of the product to different

individuals by using the products.

Target return- the targets are determined by an individual in which minimum amount of profit

margin are charged by the owner by selling their products or services to its variety of customers.

3.3 Assess the viability of projects

Years Project A Cumulative cash flows

0 8.6 -8.6

1 1.6 -7

2 2.8 -4.2

3 3.4 -0.8

4 3.6 2.8

5 4 6.8

6 4.2 11

Calculation of payback period

= 3+0.8/3.6

=3+0.22

=3.22 years

Table 1: Payback of Project B

Years Project B Cumulative cash flows

0 4.4 -4.4

1 0.8 -3.6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

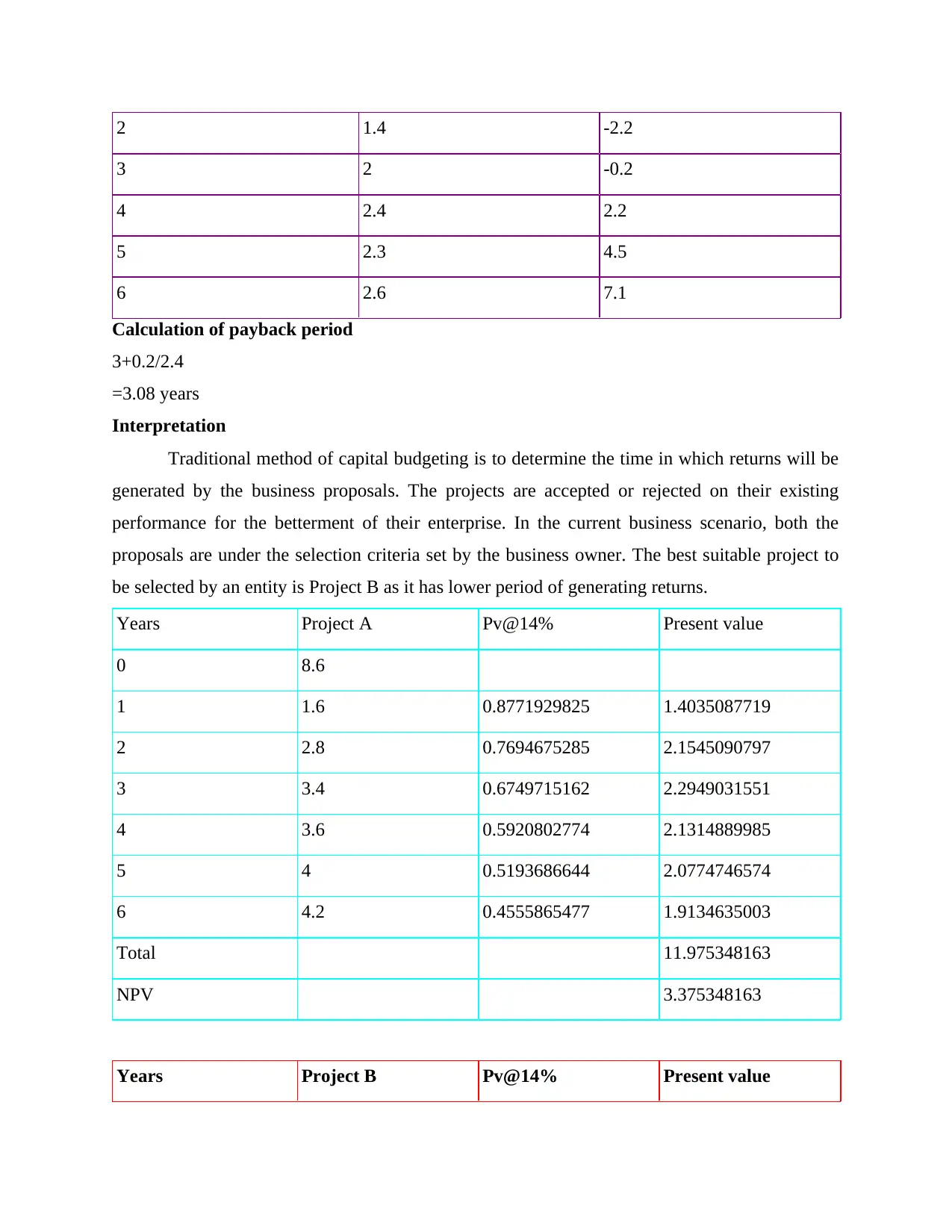

2 1.4 -2.2

3 2 -0.2

4 2.4 2.2

5 2.3 4.5

6 2.6 7.1

Calculation of payback period

3+0.2/2.4

=3.08 years

Interpretation

Traditional method of capital budgeting is to determine the time in which returns will be

generated by the business proposals. The projects are accepted or rejected on their existing

performance for the betterment of their enterprise. In the current business scenario, both the

proposals are under the selection criteria set by the business owner. The best suitable project to

be selected by an entity is Project B as it has lower period of generating returns.

Years Project A Pv@14% Present value

0 8.6

1 1.6 0.8771929825 1.4035087719

2 2.8 0.7694675285 2.1545090797

3 3.4 0.6749715162 2.2949031551

4 3.6 0.5920802774 2.1314889985

5 4 0.5193686644 2.0774746574

6 4.2 0.4555865477 1.9134635003

Total 11.975348163

NPV 3.375348163

Years Project B Pv@14% Present value

3 2 -0.2

4 2.4 2.2

5 2.3 4.5

6 2.6 7.1

Calculation of payback period

3+0.2/2.4

=3.08 years

Interpretation

Traditional method of capital budgeting is to determine the time in which returns will be

generated by the business proposals. The projects are accepted or rejected on their existing

performance for the betterment of their enterprise. In the current business scenario, both the

proposals are under the selection criteria set by the business owner. The best suitable project to

be selected by an entity is Project B as it has lower period of generating returns.

Years Project A Pv@14% Present value

0 8.6

1 1.6 0.8771929825 1.4035087719

2 2.8 0.7694675285 2.1545090797

3 3.4 0.6749715162 2.2949031551

4 3.6 0.5920802774 2.1314889985

5 4 0.5193686644 2.0774746574

6 4.2 0.4555865477 1.9134635003

Total 11.975348163

NPV 3.375348163

Years Project B Pv@14% Present value

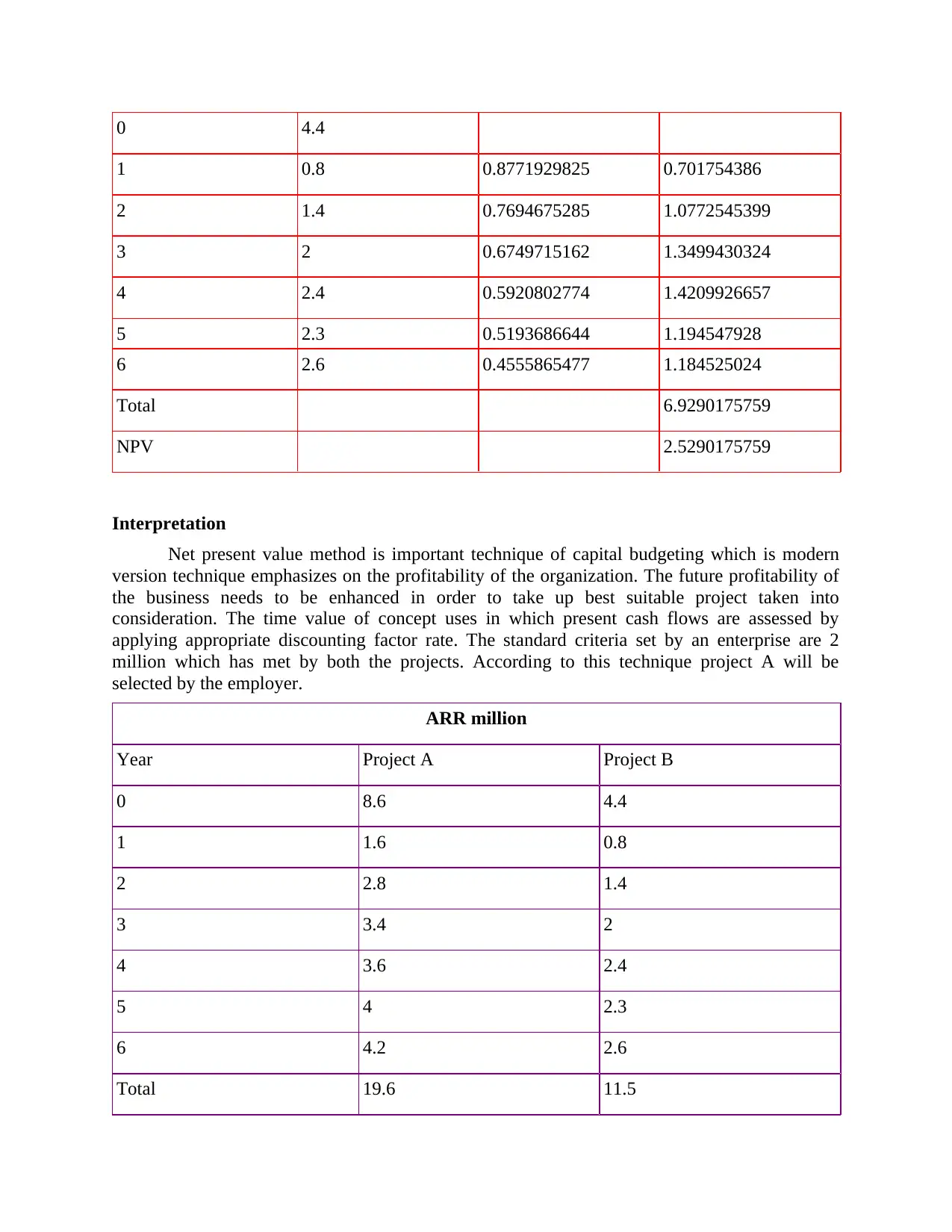

0 4.4

1 0.8 0.8771929825 0.701754386

2 1.4 0.7694675285 1.0772545399

3 2 0.6749715162 1.3499430324

4 2.4 0.5920802774 1.4209926657

5 2.3 0.5193686644 1.194547928

6 2.6 0.4555865477 1.184525024

Total 6.9290175759

NPV 2.5290175759

Interpretation

Net present value method is important technique of capital budgeting which is modern

version technique emphasizes on the profitability of the organization. The future profitability of

the business needs to be enhanced in order to take up best suitable project taken into

consideration. The time value of concept uses in which present cash flows are assessed by

applying appropriate discounting factor rate. The standard criteria set by an enterprise are 2

million which has met by both the projects. According to this technique project A will be

selected by the employer.

ARR million

Year Project A Project B

0 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

1 0.8 0.8771929825 0.701754386

2 1.4 0.7694675285 1.0772545399

3 2 0.6749715162 1.3499430324

4 2.4 0.5920802774 1.4209926657

5 2.3 0.5193686644 1.194547928

6 2.6 0.4555865477 1.184525024

Total 6.9290175759

NPV 2.5290175759

Interpretation

Net present value method is important technique of capital budgeting which is modern

version technique emphasizes on the profitability of the organization. The future profitability of

the business needs to be enhanced in order to take up best suitable project taken into

consideration. The time value of concept uses in which present cash flows are assessed by

applying appropriate discounting factor rate. The standard criteria set by an enterprise are 2

million which has met by both the projects. According to this technique project A will be

selected by the employer.

ARR million

Year Project A Project B

0 8.6 4.4

1 1.6 0.8

2 2.8 1.4

3 3.4 2

4 3.6 2.4

5 4 2.3

6 4.2 2.6

Total 19.6 11.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.