Managing Financial Resources: Budgeting, Costing and Performance

VerifiedAdded on 2023/06/15

|10

|2554

|126

Report

AI Summary

This assignment provides a comprehensive overview of managing financial resources, covering fixed and variable costs, budgeting, and forecasting techniques. It includes a practical scenario involving the Cleveland recreation centre's annual fundraiser, demonstrating the calculation of fixed and variable components to determine profitability. Furthermore, the report discusses variance analysis, differentiating between adverse and favorable variances, and highlights the importance of flexible budgets in tracking actual spending. The assignment also explores key performance indicators (KPIs) such as Average Daily Rate (ADR), Revenue per Available Room (RevPAR), Average Length of Stay, Average Rate Index, and Customer Satisfaction, illustrating their application with examples. The document is available on Desklib, a platform offering a range of study tools and resources for students.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

SECTION A ....................................................................................................................................3

Question 2 ..................................................................................................................................3

SECTION B ...................................................................................................................................5

Question 4 ..................................................................................................................................5

Question 5...................................................................................................................................6

REFERENCES..............................................................................................................................10

SECTION A ....................................................................................................................................3

Question 2 ..................................................................................................................................3

SECTION B ...................................................................................................................................5

Question 4 ..................................................................................................................................5

Question 5...................................................................................................................................6

REFERENCES..............................................................................................................................10

SECTION A

Question 2

Fixed components- This is the cost which does not get impacted with decrease or increase in the

number of products or services which has been sold or produced by firm. Fixed cost is known as

expenses that a firm must pay against any business related activities(Li, F., Zhu, Q. and Liang,

L., 2018). Hence, the company set these costs over a specified period of time and therefore do

not change with level of production.

Advantages- It is easier to account for this cost because fixed cost does not change and

affected by increase or decrease in the services or products. It does not change in line with the

goods sold or produced volume. This will ultimately encourage team members of production

department to produce more effectively. This cost is helpful for cash savings because it decreases

the net income of a company for the accounting period that results in tax liability reduction.

Disadvantages- sometimes fixed cost is very tough because when company is into

multiple products or services, it is difficult to find any direct relationship between the fixed costs

and goods. Hence, it will result in wrong financial productivity measurement which can impact

profit margins.

Variable components- It is an expense in corporate that changes in proportion to how much a

firm sells or produces their services or products(Casazza, M., 2019). The result of variable cost

means decrease or increase is totally depended on a firm's sales volume or production. For

example- variable costs increase when the production increase and it reduced as production

decline. Example includes cost of raw materials which is used in production, direct labor costs

and commission with respect to sales.

In order to calculate total variable costs, the company needs to multiply the total number

of units produced by the variable cost per unit.

Total variable cost= per unit variable cost* quantity of units produced

Advantages- financial planning requires managers to estimates future costs and

production. Variable cost is essential for making accurate cost estimation so that company can

easily determine the expenditure level at various production levels and cost behaviour

knowledge. It is helpful to make short term controlling, decision-making process and controlling.

Question 2

Fixed components- This is the cost which does not get impacted with decrease or increase in the

number of products or services which has been sold or produced by firm. Fixed cost is known as

expenses that a firm must pay against any business related activities(Li, F., Zhu, Q. and Liang,

L., 2018). Hence, the company set these costs over a specified period of time and therefore do

not change with level of production.

Advantages- It is easier to account for this cost because fixed cost does not change and

affected by increase or decrease in the services or products. It does not change in line with the

goods sold or produced volume. This will ultimately encourage team members of production

department to produce more effectively. This cost is helpful for cash savings because it decreases

the net income of a company for the accounting period that results in tax liability reduction.

Disadvantages- sometimes fixed cost is very tough because when company is into

multiple products or services, it is difficult to find any direct relationship between the fixed costs

and goods. Hence, it will result in wrong financial productivity measurement which can impact

profit margins.

Variable components- It is an expense in corporate that changes in proportion to how much a

firm sells or produces their services or products(Casazza, M., 2019). The result of variable cost

means decrease or increase is totally depended on a firm's sales volume or production. For

example- variable costs increase when the production increase and it reduced as production

decline. Example includes cost of raw materials which is used in production, direct labor costs

and commission with respect to sales.

In order to calculate total variable costs, the company needs to multiply the total number

of units produced by the variable cost per unit.

Total variable cost= per unit variable cost* quantity of units produced

Advantages- financial planning requires managers to estimates future costs and

production. Variable cost is essential for making accurate cost estimation so that company can

easily determine the expenditure level at various production levels and cost behaviour

knowledge. It is helpful to make short term controlling, decision-making process and controlling.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Managers can find out important and necessary information through variable costing. Managers

of the company requires skills and knowledge of cost behaviour under different category of

operating conditions and decisions about business. Also, the management team can make product

pricing decisions. Here, they have detailed data to determine when it is advisable to accept the

orders related to business . It is helpful to purpose of cost controlling process, in the company

costs should be split into variable and fixed costs. It supports the standard use, responsibility

reporting and budgeting control to help management team. The income statement of variable

costs highlights the relationship between income and sales. It shows an increase in income

statement corresponding to the sales performance.

Disadvantage- sometimes variable costing mislead managers during their decision-

making process when a business is facing recession, during which profit will be minimized due

to sales being lower than production of product or services.

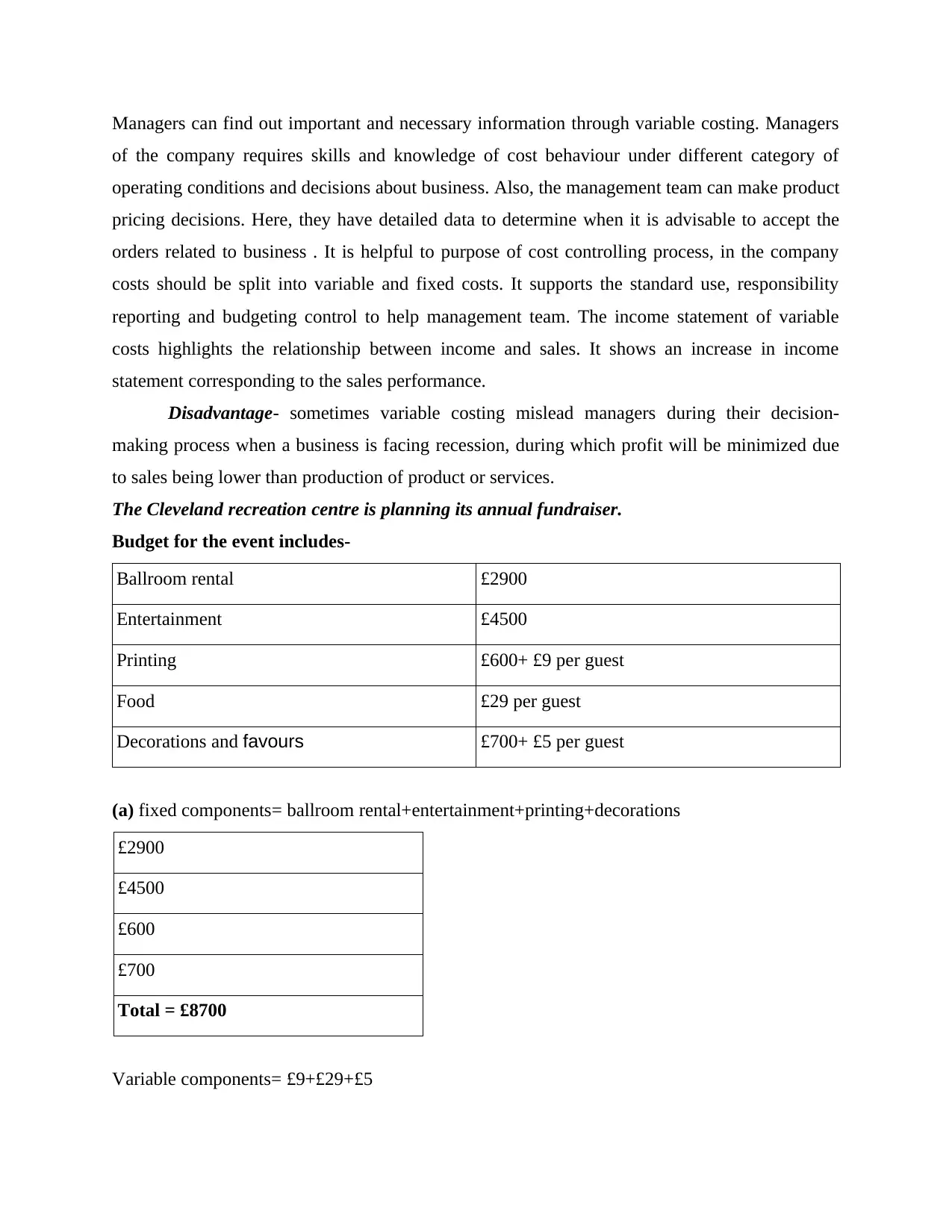

The Cleveland recreation centre is planning its annual fundraiser.

Budget for the event includes-

Ballroom rental £2900

Entertainment £4500

Printing £600+ £9 per guest

Food £29 per guest

Decorations and favours £700+ £5 per guest

(a) fixed components= ballroom rental+entertainment+printing+decorations

£2900

£4500

£600

£700

Total = £8700

Variable components= £9+£29+£5

of the company requires skills and knowledge of cost behaviour under different category of

operating conditions and decisions about business. Also, the management team can make product

pricing decisions. Here, they have detailed data to determine when it is advisable to accept the

orders related to business . It is helpful to purpose of cost controlling process, in the company

costs should be split into variable and fixed costs. It supports the standard use, responsibility

reporting and budgeting control to help management team. The income statement of variable

costs highlights the relationship between income and sales. It shows an increase in income

statement corresponding to the sales performance.

Disadvantage- sometimes variable costing mislead managers during their decision-

making process when a business is facing recession, during which profit will be minimized due

to sales being lower than production of product or services.

The Cleveland recreation centre is planning its annual fundraiser.

Budget for the event includes-

Ballroom rental £2900

Entertainment £4500

Printing £600+ £9 per guest

Food £29 per guest

Decorations and favours £700+ £5 per guest

(a) fixed components= ballroom rental+entertainment+printing+decorations

£2900

£4500

£600

£700

Total = £8700

Variable components= £9+£29+£5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=£43

(b)

If Cleveland recreation centre charges £100 per person, then money will be raised by this event=

=(£100×£3000)-[£8700+(£43×£3000)]

=£300000-(£8700+£129000)

=£300000-£137700

= £162300

For fixed cost, total number of expenses has been added that is £8700, for variable cost

total number of per guest has been added that is £43.

By evaluating the study, it has been determined that if committee expects that total

number of people that is £3000 will attend the event, and they will charge £100 per person= total

300000.

Number of total people that is £3000 is multiplied by variable cost £43 that is 129000

Total sales – cost

300000-137700= 162300 this is the final money will be raised by event for fundraising.

SECTION B

Question 4

1. Budgeting and Forecasting

These are the tools used by firm in order to establish a management plan, mostly both of

them are often used together. Budgeting quantifies the business expectation of revenues that

every company wants to accomplish for a future period. Manager of the company can know

about the financial position and financial health of firm by maintaining budget report (Boukari

and Veiga, 2018). They can understand cash inflow and outflow by managing budgetary reports.

Sometimes management team may need to be flexible and allow the company's budget to be

adjusted throughout the year. On the other hand, forecasting is helpful to estimate the revenue

amount or income that will be achieved in a future period. For example- a management team of

team can use forecasting and budgeting in order to make important decisions and take immediate

action based on data. These tool tells the firm to move in right direction so that management plan

(b)

If Cleveland recreation centre charges £100 per person, then money will be raised by this event=

=(£100×£3000)-[£8700+(£43×£3000)]

=£300000-(£8700+£129000)

=£300000-£137700

= £162300

For fixed cost, total number of expenses has been added that is £8700, for variable cost

total number of per guest has been added that is £43.

By evaluating the study, it has been determined that if committee expects that total

number of people that is £3000 will attend the event, and they will charge £100 per person= total

300000.

Number of total people that is £3000 is multiplied by variable cost £43 that is 129000

Total sales – cost

300000-137700= 162300 this is the final money will be raised by event for fundraising.

SECTION B

Question 4

1. Budgeting and Forecasting

These are the tools used by firm in order to establish a management plan, mostly both of

them are often used together. Budgeting quantifies the business expectation of revenues that

every company wants to accomplish for a future period. Manager of the company can know

about the financial position and financial health of firm by maintaining budget report (Boukari

and Veiga, 2018). They can understand cash inflow and outflow by managing budgetary reports.

Sometimes management team may need to be flexible and allow the company's budget to be

adjusted throughout the year. On the other hand, forecasting is helpful to estimate the revenue

amount or income that will be achieved in a future period. For example- a management team of

team can use forecasting and budgeting in order to make important decisions and take immediate

action based on data. These tool tells the firm to move in right direction so that management plan

can be done successfully. Unlike budgeting process, forecasting does not able to analyse and

evaluate the variance between actual performance and financial forecasts.

2. Variance Analysis.

Managers of the firm used this to find out the overall over performance for particular

reporting period (Dai and et.al., 2021). It can be analysed through difference between actual and

planned numbers. Firm compare standard costs and actual costs in order to assess their

Favorability for each item related to business. For example- for raw materials, if the standard

cost is more than actual cost, it would lead to a favourable price variance. If the 20000 pieces

were required in production and standard quantity was 15000 pieces of raw material, this would

be an unfavourable quantity because more raw materials were used than predicted.

3. Adverse variances.

When actual income is less than budget or in other words actual expensed is more than

budget it is known as adverse variance. Adverse variance can occur due to instant change in

economic conditions, such as low customer spending, economic growth and development, or a

recession which can impact the whole economy and leads to high unemployment rate. For

example- Due to this market conditions can also impact, such as entry of new company with

something advanced services and new products.

4. Favourable variance

when actual expenses is less than budget or in other words actual income is more than

budget it is known as favourable variance. This variance is the similar to a surplus where

expenses of the company is less than the income. For example- if a company expected to pay

around $150000 for maintenance of tools and equipments but was able to contract a price of

$90000 then they will have a variance in favourable condition of $60000.

5. Flexible Budget

This budget is helpful for company to track the actual spending and adjust those spending

each month. This budget will accurately reflect the state of company's finances, where the

management team can decide the level of output to be produced (Zamfir and et.al., 2021). So,

that profit can be generated easily for the business based on cost at various activity level and

budgeted sales. For example- Morrisons has a budget of $4 million cost of goods sold, $1 million

is fixed and $10 million in revenues. $3 million varies directly with revenue so Morrisons, cost

of goods sold is 30% of revenues.

evaluate the variance between actual performance and financial forecasts.

2. Variance Analysis.

Managers of the firm used this to find out the overall over performance for particular

reporting period (Dai and et.al., 2021). It can be analysed through difference between actual and

planned numbers. Firm compare standard costs and actual costs in order to assess their

Favorability for each item related to business. For example- for raw materials, if the standard

cost is more than actual cost, it would lead to a favourable price variance. If the 20000 pieces

were required in production and standard quantity was 15000 pieces of raw material, this would

be an unfavourable quantity because more raw materials were used than predicted.

3. Adverse variances.

When actual income is less than budget or in other words actual expensed is more than

budget it is known as adverse variance. Adverse variance can occur due to instant change in

economic conditions, such as low customer spending, economic growth and development, or a

recession which can impact the whole economy and leads to high unemployment rate. For

example- Due to this market conditions can also impact, such as entry of new company with

something advanced services and new products.

4. Favourable variance

when actual expenses is less than budget or in other words actual income is more than

budget it is known as favourable variance. This variance is the similar to a surplus where

expenses of the company is less than the income. For example- if a company expected to pay

around $150000 for maintenance of tools and equipments but was able to contract a price of

$90000 then they will have a variance in favourable condition of $60000.

5. Flexible Budget

This budget is helpful for company to track the actual spending and adjust those spending

each month. This budget will accurately reflect the state of company's finances, where the

management team can decide the level of output to be produced (Zamfir and et.al., 2021). So,

that profit can be generated easily for the business based on cost at various activity level and

budgeted sales. For example- Morrisons has a budget of $4 million cost of goods sold, $1 million

is fixed and $10 million in revenues. $3 million varies directly with revenue so Morrisons, cost

of goods sold is 30% of revenues.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 5

1. Average daily rate (ADR)

This is the statistical unit used by hotel or other lodging business in order to measure the

average rental revenue earned for a room which is occupied per day.

For example- if a Hyatt hotel has $30000 in room revenue and 300 rooms sold, the ADR would

be $100.

ADR= Rooms Revenue/ Rooms sold

= 30000/ 300

=100

2. Revenue per available room

Hotel industry or hospitality industry used this to measure performance and assess a

hotel's ability to fill its availability of room at an average rate (Chattopadhyay and Mitra, 2019).

With the help of RevPAR, company can find out its occupancy rate whether it is increasing or

decreasing. In other words, hoteliers can easily measures the overall success of their business.

For example- if a Radisson hotel is occupied at 60% with an ADR of $100, then RevPAR would

be $60. Average daily rate* occupancy rate

Another method CALCULATION EXAMPLE-

total revenue= 3250000

Considered period= 90days

Number of rooms= 600

RevPAR= 3250000/54000

= 60

3. Average length of stay

This is a tool used by healthcare industry in order to monitor and determine when and

where to make necessary changes so that they can easily improve efficiency. It is calculated by

adding the total length of stay for patients and dividing by the total number of discharge patient

in a month.

For example- A healthcare facility has 5 patients in the month of March 2022

Date admission/ discharge Patient Stay

March 2 to march 4 A 3 day

1. Average daily rate (ADR)

This is the statistical unit used by hotel or other lodging business in order to measure the

average rental revenue earned for a room which is occupied per day.

For example- if a Hyatt hotel has $30000 in room revenue and 300 rooms sold, the ADR would

be $100.

ADR= Rooms Revenue/ Rooms sold

= 30000/ 300

=100

2. Revenue per available room

Hotel industry or hospitality industry used this to measure performance and assess a

hotel's ability to fill its availability of room at an average rate (Chattopadhyay and Mitra, 2019).

With the help of RevPAR, company can find out its occupancy rate whether it is increasing or

decreasing. In other words, hoteliers can easily measures the overall success of their business.

For example- if a Radisson hotel is occupied at 60% with an ADR of $100, then RevPAR would

be $60. Average daily rate* occupancy rate

Another method CALCULATION EXAMPLE-

total revenue= 3250000

Considered period= 90days

Number of rooms= 600

RevPAR= 3250000/54000

= 60

3. Average length of stay

This is a tool used by healthcare industry in order to monitor and determine when and

where to make necessary changes so that they can easily improve efficiency. It is calculated by

adding the total length of stay for patients and dividing by the total number of discharge patient

in a month.

For example- A healthcare facility has 5 patients in the month of March 2022

Date admission/ discharge Patient Stay

March 2 to march 4 A 3 day

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

March 4 to march 5 B 2 day

March 14 and leaves same day C 1 day stay

March 16 to march 25 D 10 day

March 16 to march 24 E 9 day

Total 25

Average length of stay = 25/ 5 patient stays

= 5 days

4. Average rate index

Average rate index is calculated by hotel industry which shows them how their rates

compare with other competitors to help determine if they need to raise, hold or lower room rates

(Average rate index, 2022). If the rate is greater than 1 than hotel is said to be on averaged priced

higher than the other hotels.

Example= ADR/ competitor set's ADR

= 60/50= 1.2 = 120

It means an ADR above 1 indicates that the hotel property is achieving more than its fair

market share which is beneficial for the company (Bartolomeo, Trerotoli and Serio, 2021). On

the other hand, below 1 shows that hotel price is lower and needs to improve their performance.

Knowing this data in detailed can help managers of the company decide whether to adjust rate to

improve bookings or attain low occupancy rate.

5. Customer satisfaction

This is most important term which is used in marketing, the firm evaluate its customer

satisfaction level which measure how company's service or product meet customer expectation.

In other words, it measures whether customers are happy with the services given by the firm and

if they meet the expectation. With the help of feedback, ratings, KPIs and benchmarking

company can determine how to best improve or make necessary changes to its services or

products. Customer satisfaction is one of the most important factor or indicators of customer

loyalty towards the brand (Khan and Hashim, 2020). By understanding, the customer satisfaction

level company can predict business revenue and growth. For example= If amazon wants to know

March 14 and leaves same day C 1 day stay

March 16 to march 25 D 10 day

March 16 to march 24 E 9 day

Total 25

Average length of stay = 25/ 5 patient stays

= 5 days

4. Average rate index

Average rate index is calculated by hotel industry which shows them how their rates

compare with other competitors to help determine if they need to raise, hold or lower room rates

(Average rate index, 2022). If the rate is greater than 1 than hotel is said to be on averaged priced

higher than the other hotels.

Example= ADR/ competitor set's ADR

= 60/50= 1.2 = 120

It means an ADR above 1 indicates that the hotel property is achieving more than its fair

market share which is beneficial for the company (Bartolomeo, Trerotoli and Serio, 2021). On

the other hand, below 1 shows that hotel price is lower and needs to improve their performance.

Knowing this data in detailed can help managers of the company decide whether to adjust rate to

improve bookings or attain low occupancy rate.

5. Customer satisfaction

This is most important term which is used in marketing, the firm evaluate its customer

satisfaction level which measure how company's service or product meet customer expectation.

In other words, it measures whether customers are happy with the services given by the firm and

if they meet the expectation. With the help of feedback, ratings, KPIs and benchmarking

company can determine how to best improve or make necessary changes to its services or

products. Customer satisfaction is one of the most important factor or indicators of customer

loyalty towards the brand (Khan and Hashim, 2020). By understanding, the customer satisfaction

level company can predict business revenue and growth. For example= If amazon wants to know

about customer satisfaction level then marketing and sales team will survey and collect feedback

from customer about their expectation. They will make questionnaire and ask customer to rate

their experience from 1 to 10 or from excellent to poor. This can be done through emails,

personal interviews, marketing campaigns and message.

Example=

Are you satisfied with the services or products offers by the company?

How did the employees of our company provide you services?

How do you rate your shopping experience with us ?

Any suggestion to improve product performance ?

Calculation of CSAT- customer satisfaction.

If Tesco plc had 400 positive responses out of 500 total responses than CSAT score would be

80%

=Number of positive responses/ total number of responses* 100

=400/500×100

=80%

from customer about their expectation. They will make questionnaire and ask customer to rate

their experience from 1 to 10 or from excellent to poor. This can be done through emails,

personal interviews, marketing campaigns and message.

Example=

Are you satisfied with the services or products offers by the company?

How did the employees of our company provide you services?

How do you rate your shopping experience with us ?

Any suggestion to improve product performance ?

Calculation of CSAT- customer satisfaction.

If Tesco plc had 400 positive responses out of 500 total responses than CSAT score would be

80%

=Number of positive responses/ total number of responses* 100

=400/500×100

=80%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bartolomeo, N., Trerotoli, P. and Serio, G., 2021. Short-term forecast in the early stage of the

COVID-19 outbreak in Italy. Application of a weighted and cumulative average daily

growth rate to an exponential decay model. Infectious Disease Modelling. 6. pp.212-221.

Boukari, M. and Veiga, F. J., 2018. Disentangling political and institutional determinants of

budget forecast errors: A comparative approach. Journal of Comparative

Economics. 46(4). pp.1030-1045.

Casazza, M., 2019. New formulations for variable cost and size bin packing problems with item

fragmentation. Optimization Letters. 13(2). pp.379-398.

Chattopadhyay, M. and Mitra, S. K., 2019. Determinants of revenue per available room:

Influential roles of average daily rate, demand, seasonality and yearly trend. International

Journal of Hospitality Management. 77. pp.573-582.

Dai, M. and et.al., 2021. A dynamic mean-variance analysis for log returns. Management

Science. 67(2). pp.1093-1108.

Khan, M. A. A. and Hashim, H., 2020. Tourist satisfaction index for tourism destination,

integrating social media engagement into the European customer satisfaction index: a

conceptual paper. International Journal of Academic Research in Business and Social

Sciences. 10(9). pp.72-90.

Lapidus, N. and et.al., 2020. Biased and unbiased estimation of the average length of stay in

intensive care units in the Covid-19 pandemic. Annals of intensive care. 10(1). pp.1-9.

Li, F., Zhu, Q. and Liang, L., 2018. Allocating a fixed cost based on a DEA-game cross

efficiency approach. Expert Systems with Applications. 96. pp.196-207.

Zamfir, M. and et.al., 2021. Flexible Budget: Management Method for Cost Control and

Monitoring the Performance of Economic Entities. In CSR and Management Accounting

Challenges in a Time of Global Crises (pp. 128-155). IGI Global.

Online

Average rate index. 2022. [Online]. Available through: <https://www.siteminder.com/what-is-

average-rate-index-ari/>

Books and Journals

Bartolomeo, N., Trerotoli, P. and Serio, G., 2021. Short-term forecast in the early stage of the

COVID-19 outbreak in Italy. Application of a weighted and cumulative average daily

growth rate to an exponential decay model. Infectious Disease Modelling. 6. pp.212-221.

Boukari, M. and Veiga, F. J., 2018. Disentangling political and institutional determinants of

budget forecast errors: A comparative approach. Journal of Comparative

Economics. 46(4). pp.1030-1045.

Casazza, M., 2019. New formulations for variable cost and size bin packing problems with item

fragmentation. Optimization Letters. 13(2). pp.379-398.

Chattopadhyay, M. and Mitra, S. K., 2019. Determinants of revenue per available room:

Influential roles of average daily rate, demand, seasonality and yearly trend. International

Journal of Hospitality Management. 77. pp.573-582.

Dai, M. and et.al., 2021. A dynamic mean-variance analysis for log returns. Management

Science. 67(2). pp.1093-1108.

Khan, M. A. A. and Hashim, H., 2020. Tourist satisfaction index for tourism destination,

integrating social media engagement into the European customer satisfaction index: a

conceptual paper. International Journal of Academic Research in Business and Social

Sciences. 10(9). pp.72-90.

Lapidus, N. and et.al., 2020. Biased and unbiased estimation of the average length of stay in

intensive care units in the Covid-19 pandemic. Annals of intensive care. 10(1). pp.1-9.

Li, F., Zhu, Q. and Liang, L., 2018. Allocating a fixed cost based on a DEA-game cross

efficiency approach. Expert Systems with Applications. 96. pp.196-207.

Zamfir, M. and et.al., 2021. Flexible Budget: Management Method for Cost Control and

Monitoring the Performance of Economic Entities. In CSR and Management Accounting

Challenges in a Time of Global Crises (pp. 128-155). IGI Global.

Online

Average rate index. 2022. [Online]. Available through: <https://www.siteminder.com/what-is-

average-rate-index-ari/>

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.