Financial Resource Management and Investment Appraisal Report

VerifiedAdded on 2020/01/23

|17

|4623

|189

Report

AI Summary

This report delves into the critical aspects of financial resource management and decision-making within a business context. It examines the identification of various funding sources, including bank loans, equity shares, and retained earnings, evaluating their implications, advantages, and disadvantages through case studies. The report analyzes the cost of different finance sources and underscores the importance of financial planning. It highlights the financial information necessary for informed decision-making and explores the impact of finance on financial statements. Furthermore, the report presents an evaluation of cash flow forecasts and sales budgets, providing recommendations for improvement. The application of investment appraisal techniques, such as payback period, net present value, and internal rate of return, is demonstrated. The report also covers unit cost calculations, pricing decisions, and break-even analysis, alongside a discussion of key financial statements and ratio analysis for performance interpretation. Overall, the report offers a comprehensive overview of financial management principles and their practical application.

Managing Financial Resources and

Decisions

Decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Identifying the source of finance currently available for different businesses......................1

1.2 Assessing the implications of each source including the relative advantages and

disadvantages...............................................................................................................................2

1.3 Providing three case study.....................................................................................................3

Task 2...............................................................................................................................................3

2.1 Analyzing the cost of different sources of Finance...............................................................3

2.2 Explaining the key aspects /importance of financial planning..............................................4

2.3 Highlighting the types of financial information required for decision making purposes......4

2.4 Explaining the impact of finance on the financial statements...............................................5

Task 3...............................................................................................................................................5

3.1 Evaluation of cash flow forecast and sales budget and presenting present findings and

recommendations in a formal written report to the Directors of ABC Manufacturing Ltd.........5

3.3 Application of different investment appraisal tactics and recommendation..........................5

3.2 Explaining the calculation of unit costs and make pricing decisions using relevant

information...................................................................................................................................7

Task 4.............................................................................................................................................12

4.1 Discussing the main financial statements............................................................................12

4.2 Comparing appropriate formats of financial statements for different types of business.....12

4.3. Interpreting financial statements using appropriate ratios and comparisons, both internal

and external................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

Introduction......................................................................................................................................1

Task 1...............................................................................................................................................1

1.1 Identifying the source of finance currently available for different businesses......................1

1.2 Assessing the implications of each source including the relative advantages and

disadvantages...............................................................................................................................2

1.3 Providing three case study.....................................................................................................3

Task 2...............................................................................................................................................3

2.1 Analyzing the cost of different sources of Finance...............................................................3

2.2 Explaining the key aspects /importance of financial planning..............................................4

2.3 Highlighting the types of financial information required for decision making purposes......4

2.4 Explaining the impact of finance on the financial statements...............................................5

Task 3...............................................................................................................................................5

3.1 Evaluation of cash flow forecast and sales budget and presenting present findings and

recommendations in a formal written report to the Directors of ABC Manufacturing Ltd.........5

3.3 Application of different investment appraisal tactics and recommendation..........................5

3.2 Explaining the calculation of unit costs and make pricing decisions using relevant

information...................................................................................................................................7

Task 4.............................................................................................................................................12

4.1 Discussing the main financial statements............................................................................12

4.2 Comparing appropriate formats of financial statements for different types of business.....12

4.3. Interpreting financial statements using appropriate ratios and comparisons, both internal

and external................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

INDEX OF TABLES

Table 1: Calculation of payback period...........................................................................................6

Table 2: Calculation of Net present value.......................................................................................6

Table 3: Calculation of internal rate of return.................................................................................6

Table 4: calculation of unit costs.....................................................................................................7

Table 5: Calculation of profit and BEP by varying the sales price.................................................8

Table 6: Calculation of BEP by varying the fixed cost...................................................................9

Table 7: Calculation of BEP by varying the material Cost...........................................................10

Table 8: Calculation of BEP by varying the labour cost...............................................................10

Table 9: Calculation of total profit................................................................................................11

Table 10: Calculation of ratios of XYZ co....................................................................................13

Table 1: Calculation of payback period...........................................................................................6

Table 2: Calculation of Net present value.......................................................................................6

Table 3: Calculation of internal rate of return.................................................................................6

Table 4: calculation of unit costs.....................................................................................................7

Table 5: Calculation of profit and BEP by varying the sales price.................................................8

Table 6: Calculation of BEP by varying the fixed cost...................................................................9

Table 7: Calculation of BEP by varying the material Cost...........................................................10

Table 8: Calculation of BEP by varying the labour cost...............................................................10

Table 9: Calculation of total profit................................................................................................11

Table 10: Calculation of ratios of XYZ co....................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The success of an organization is greatly affected by its ability of the management of

wide range of financial resources as per the distinct business requirements. In this process, the

managers of business requires to consider different tools of accounting and financial

management such as ratios, income statements, cash flow statements, costing, break even

analysis, etc (Galloway and Deakins, 2012). All these tools assist managers in the collection of

wide range of financial data through which management is able to take appropriate decisions

regarding the assessment and usage of wide range of accounting data.

This report is going to discuss different aspects of financial management and business

decision making process. In this process, report examines the role of different investment

appraisals in investment decisions of an organization. Apart from that, this report will use ratio

analysis for evaluating the business performance.

TASK 1

1.1 Identifying the source of finance currently available for different businesses

For handling different business requirements, an organization uses a wide range of

financial source for the attainment of different business objectives. Some important sources of

funds are examined as below:

Bank loan: It is one of the most common tools which are used by each type of

organization, that is, new or old as well as large or small. New companies take bank loan

for business start up and existing firms take bank loans for different business

requirements such as short term finance for the liquidity management (Brigham, 2011).

On the other hand, long term bank loans are used for the long term business decisions.

Equity shares: It is considered as an important source of finance for large companies.

This is because; small companies are not able to expand the capital of company through

equity shares. It provides significant support to large companies while taking major

expansion decisions along with the mergers or acquisition (Collis and Jarvis, 2002). In

this process, risk on investment is managed by investors.

Retained earnings: Every organization saves some portion of profit for the attainment of

distinct business requirements. It is called as retained earnings through which

organization is able to manage short and long term requirement of funds. This source of

1

The success of an organization is greatly affected by its ability of the management of

wide range of financial resources as per the distinct business requirements. In this process, the

managers of business requires to consider different tools of accounting and financial

management such as ratios, income statements, cash flow statements, costing, break even

analysis, etc (Galloway and Deakins, 2012). All these tools assist managers in the collection of

wide range of financial data through which management is able to take appropriate decisions

regarding the assessment and usage of wide range of accounting data.

This report is going to discuss different aspects of financial management and business

decision making process. In this process, report examines the role of different investment

appraisals in investment decisions of an organization. Apart from that, this report will use ratio

analysis for evaluating the business performance.

TASK 1

1.1 Identifying the source of finance currently available for different businesses

For handling different business requirements, an organization uses a wide range of

financial source for the attainment of different business objectives. Some important sources of

funds are examined as below:

Bank loan: It is one of the most common tools which are used by each type of

organization, that is, new or old as well as large or small. New companies take bank loan

for business start up and existing firms take bank loans for different business

requirements such as short term finance for the liquidity management (Brigham, 2011).

On the other hand, long term bank loans are used for the long term business decisions.

Equity shares: It is considered as an important source of finance for large companies.

This is because; small companies are not able to expand the capital of company through

equity shares. It provides significant support to large companies while taking major

expansion decisions along with the mergers or acquisition (Collis and Jarvis, 2002). In

this process, risk on investment is managed by investors.

Retained earnings: Every organization saves some portion of profit for the attainment of

distinct business requirements. It is called as retained earnings through which

organization is able to manage short and long term requirement of funds. This source of

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

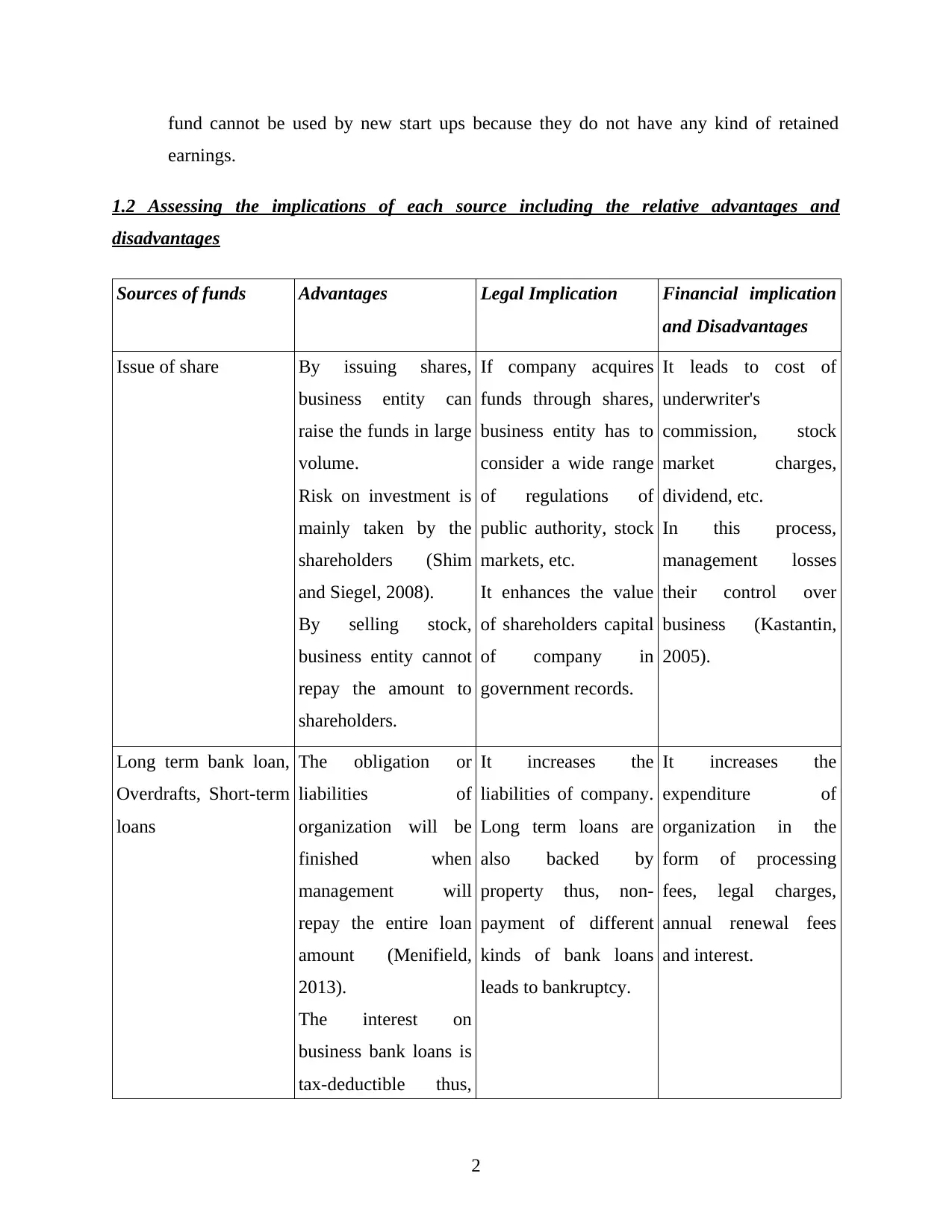

fund cannot be used by new start ups because they do not have any kind of retained

earnings.

1.2 Assessing the implications of each source including the relative advantages and

disadvantages

Sources of funds Advantages Legal Implication Financial implication

and Disadvantages

Issue of share By issuing shares,

business entity can

raise the funds in large

volume.

Risk on investment is

mainly taken by the

shareholders (Shim

and Siegel, 2008).

By selling stock,

business entity cannot

repay the amount to

shareholders.

If company acquires

funds through shares,

business entity has to

consider a wide range

of regulations of

public authority, stock

markets, etc.

It enhances the value

of shareholders capital

of company in

government records.

It leads to cost of

underwriter's

commission, stock

market charges,

dividend, etc.

In this process,

management losses

their control over

business (Kastantin,

2005).

Long term bank loan,

Overdrafts, Short-term

loans

The obligation or

liabilities of

organization will be

finished when

management will

repay the entire loan

amount (Menifield,

2013).

The interest on

business bank loans is

tax-deductible thus,

It increases the

liabilities of company.

Long term loans are

also backed by

property thus, non-

payment of different

kinds of bank loans

leads to bankruptcy.

It increases the

expenditure of

organization in the

form of processing

fees, legal charges,

annual renewal fees

and interest.

2

earnings.

1.2 Assessing the implications of each source including the relative advantages and

disadvantages

Sources of funds Advantages Legal Implication Financial implication

and Disadvantages

Issue of share By issuing shares,

business entity can

raise the funds in large

volume.

Risk on investment is

mainly taken by the

shareholders (Shim

and Siegel, 2008).

By selling stock,

business entity cannot

repay the amount to

shareholders.

If company acquires

funds through shares,

business entity has to

consider a wide range

of regulations of

public authority, stock

markets, etc.

It enhances the value

of shareholders capital

of company in

government records.

It leads to cost of

underwriter's

commission, stock

market charges,

dividend, etc.

In this process,

management losses

their control over

business (Kastantin,

2005).

Long term bank loan,

Overdrafts, Short-term

loans

The obligation or

liabilities of

organization will be

finished when

management will

repay the entire loan

amount (Menifield,

2013).

The interest on

business bank loans is

tax-deductible thus,

It increases the

liabilities of company.

Long term loans are

also backed by

property thus, non-

payment of different

kinds of bank loans

leads to bankruptcy.

It increases the

expenditure of

organization in the

form of processing

fees, legal charges,

annual renewal fees

and interest.

2

management can

acquire tax benefits.

Retained earning It plays an important

role for managing then

short term business

requirement.

It does not have any

legal impact.

It cannot be considered

by the new

organization.

1.3 Providing three case study

Case 1: Multinational or big companies such as LMN Ltd. are mainly using equity shares

for raising the funds for different business requirement such as expansion of business in new

markets and new product development.

Case 2: Old companies also consider retained earnings for managing short term as well

as long term requirement of finance that assists the managers for assessing funds without any

cost of finance such as interest, dividend, etc (Norton and Larry Kelly, 2014).

Case 3: Two people want to start retail shop they have some money that is not enough for

business start up. Therefore, these individuals mainly consider banks and private lenders as a

source of finance. This is because; new start up can get loan from these sources without any

difficulties and within less time.

TASK 2

2.1 Analyzing the cost of different sources of Finance

Equity shares: When an organization acquires funds through equity share then

management has to manage wide range of expenditures such as dividend, stock market

charges, underwriter's commission etc. In addition to that management of business has to

consider various other expenditures while issuing of shares (Acquiring and managing

financial resources. n.d).

Bank loans: If bank loans are considered by an organisation for raising of funds then

management has to manage wide range of expenses such as interest, documentation

charges and legal fees.

3

acquire tax benefits.

Retained earning It plays an important

role for managing then

short term business

requirement.

It does not have any

legal impact.

It cannot be considered

by the new

organization.

1.3 Providing three case study

Case 1: Multinational or big companies such as LMN Ltd. are mainly using equity shares

for raising the funds for different business requirement such as expansion of business in new

markets and new product development.

Case 2: Old companies also consider retained earnings for managing short term as well

as long term requirement of finance that assists the managers for assessing funds without any

cost of finance such as interest, dividend, etc (Norton and Larry Kelly, 2014).

Case 3: Two people want to start retail shop they have some money that is not enough for

business start up. Therefore, these individuals mainly consider banks and private lenders as a

source of finance. This is because; new start up can get loan from these sources without any

difficulties and within less time.

TASK 2

2.1 Analyzing the cost of different sources of Finance

Equity shares: When an organization acquires funds through equity share then

management has to manage wide range of expenditures such as dividend, stock market

charges, underwriter's commission etc. In addition to that management of business has to

consider various other expenditures while issuing of shares (Acquiring and managing

financial resources. n.d).

Bank loans: If bank loans are considered by an organisation for raising of funds then

management has to manage wide range of expenses such as interest, documentation

charges and legal fees.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Retained earnings: Consideration of retained earnings as a source of finance does not

lead any kind of expenditure of company. But, it is mainly used for short-term business

requirement.

2.2 Explaining the key aspects /importance of financial planning

Financial planning is essential for every organization. The importance of financial

planning is examined below:

It helps managers for estimation of needs of finance for different business requirement.

This concept plays important role in formulation of wide range of budgets as per the

objectives and goals of organization through which management is able to examine the

performance of company as per the current market trends (Nga and Yien, 2013).

This approach also supports management in selection of best source of finance along with

their utilization in different business operations.

By conducting a systematic financial planning, management can avoid the wastage of

financial resources.

2.3 Highlighting the types of financial information required for decision making purposes

For taking different management decisions, different kind of financial information is

required.

The information related to cost of different source of finance assists finance manager

during selection of best source of finance for different needs of organization.

Information related to profitability and current market position of company provides

significant assistance to investors of company in their investment decisions (Srinivasan,

2012).

Every organization always tries to expand business with the help of new projects and

activities therefore it can be stated that information related to profitability of project helps

managers in selection of best project for company.

Banks and financial institutions facilitate funds to business in form of debt so as they

require information regarding solvency position of business in order to asses present

capability of business for repayment of loan (Vance, 2002).

4

lead any kind of expenditure of company. But, it is mainly used for short-term business

requirement.

2.2 Explaining the key aspects /importance of financial planning

Financial planning is essential for every organization. The importance of financial

planning is examined below:

It helps managers for estimation of needs of finance for different business requirement.

This concept plays important role in formulation of wide range of budgets as per the

objectives and goals of organization through which management is able to examine the

performance of company as per the current market trends (Nga and Yien, 2013).

This approach also supports management in selection of best source of finance along with

their utilization in different business operations.

By conducting a systematic financial planning, management can avoid the wastage of

financial resources.

2.3 Highlighting the types of financial information required for decision making purposes

For taking different management decisions, different kind of financial information is

required.

The information related to cost of different source of finance assists finance manager

during selection of best source of finance for different needs of organization.

Information related to profitability and current market position of company provides

significant assistance to investors of company in their investment decisions (Srinivasan,

2012).

Every organization always tries to expand business with the help of new projects and

activities therefore it can be stated that information related to profitability of project helps

managers in selection of best project for company.

Banks and financial institutions facilitate funds to business in form of debt so as they

require information regarding solvency position of business in order to asses present

capability of business for repayment of loan (Vance, 2002).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.4 Explaining the impact of finance on the financial statements1. Income statement- Net profit of organization is reduced due to financial cost of sources

which is considered in income statements in the form of interest, dividend. These

expenses are recorded on the debit side of income statement.2. Balance sheet statement- When an organization acquires funds from different financial

sources then both asset and liabilities side of position statement are affected (Meyers,

2013). It makes increase in financial obligation either debt or equity or reduced the value

of retained earnings.

3. Cash flow statement- Amount of cash inflow is increased when company is raising funds

from different sources. This is considered in financing activities of cash flow statement.

TASK 3

3.1 Evaluation of cash flow forecast and sales budget and presenting present findings and

recommendations in a formal written report to the Directors of ABC Manufacturing Ltd

As per sales budget of ABC Manufacturing Ltd. it has been addressed that company is

continuously significant variation between budgeted sales and actual sales. In this context, it is

evaluated that firm is managing fewer sales as per the budgeted sales. In this regard, there have

been several causes evaluated that lead deficit in sales of company that could be wrong

forecasting of sales, change in interest of consumers, improper preparation of budgets, change in

business environment etc (Norton and Larry Kelly, 2014). In order to resolve these issues,

management should consider an appropriate budgeting technique through which business entity

is able to carry out appropriate forecasting.

The evaluation of cash flow forecast of ABC Manufacturing Ltd. has found that company

is facing negative cash flow due to significant up-down in income of company. Apart from that

high expenditure on purchase along with salaries etc. has increased the value of negative cash

flow. In order to resolve these issues, the management of company needs to select different short

term source of funds for attainment of shortage of cash such as working capital and bank

overdrafts etc.

3.3 Application of different investment appraisal tactics and recommendation

Scenario 2:

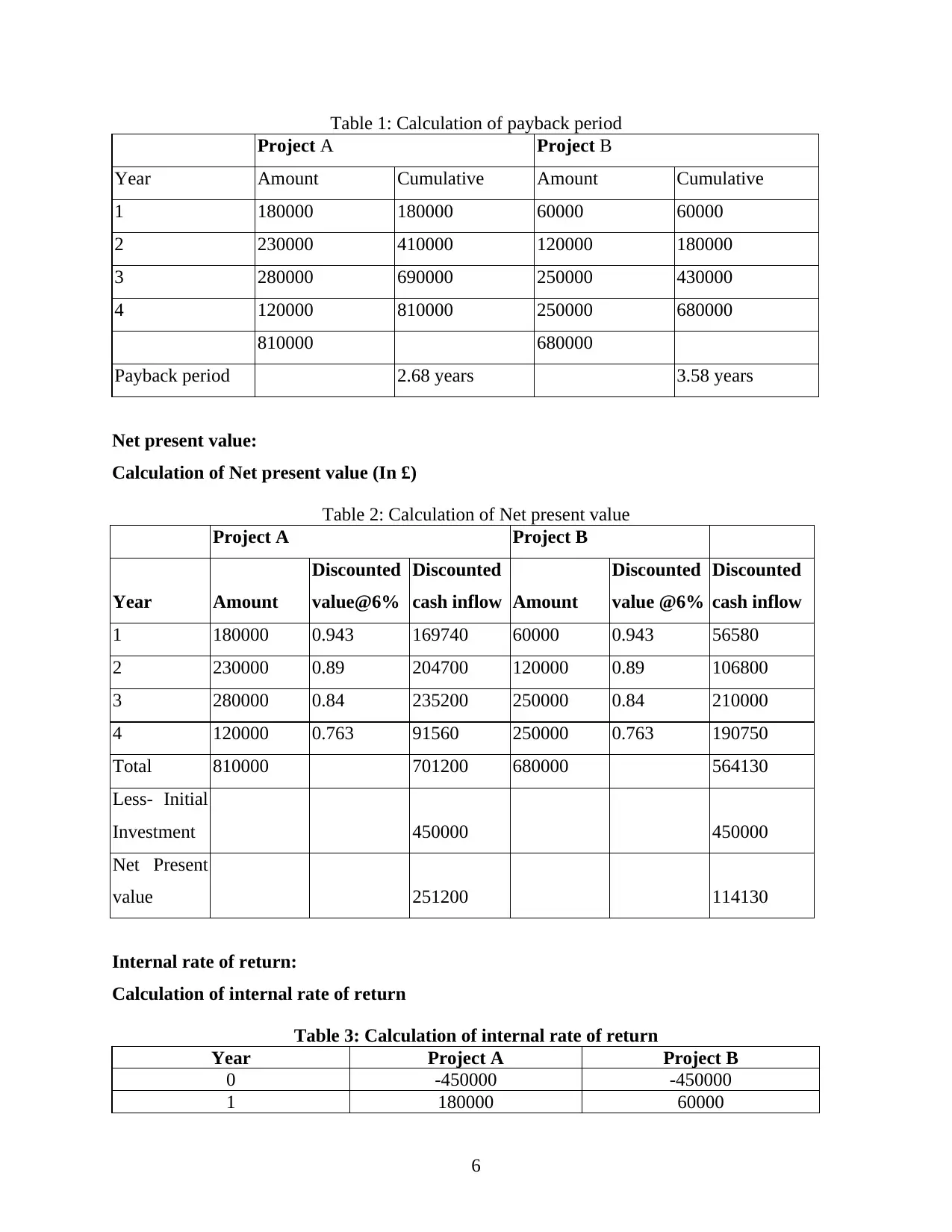

Calculation of payback period (In £)

5

which is considered in income statements in the form of interest, dividend. These

expenses are recorded on the debit side of income statement.2. Balance sheet statement- When an organization acquires funds from different financial

sources then both asset and liabilities side of position statement are affected (Meyers,

2013). It makes increase in financial obligation either debt or equity or reduced the value

of retained earnings.

3. Cash flow statement- Amount of cash inflow is increased when company is raising funds

from different sources. This is considered in financing activities of cash flow statement.

TASK 3

3.1 Evaluation of cash flow forecast and sales budget and presenting present findings and

recommendations in a formal written report to the Directors of ABC Manufacturing Ltd

As per sales budget of ABC Manufacturing Ltd. it has been addressed that company is

continuously significant variation between budgeted sales and actual sales. In this context, it is

evaluated that firm is managing fewer sales as per the budgeted sales. In this regard, there have

been several causes evaluated that lead deficit in sales of company that could be wrong

forecasting of sales, change in interest of consumers, improper preparation of budgets, change in

business environment etc (Norton and Larry Kelly, 2014). In order to resolve these issues,

management should consider an appropriate budgeting technique through which business entity

is able to carry out appropriate forecasting.

The evaluation of cash flow forecast of ABC Manufacturing Ltd. has found that company

is facing negative cash flow due to significant up-down in income of company. Apart from that

high expenditure on purchase along with salaries etc. has increased the value of negative cash

flow. In order to resolve these issues, the management of company needs to select different short

term source of funds for attainment of shortage of cash such as working capital and bank

overdrafts etc.

3.3 Application of different investment appraisal tactics and recommendation

Scenario 2:

Calculation of payback period (In £)

5

Table 1: Calculation of payback period

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

810000 680000

Payback period 2.68 years 3.58 years

Net present value:

Calculation of Net present value (In £)

Table 2: Calculation of Net present value

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value @6%

Discounted

cash inflow

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 810000 701200 680000 564130

Less- Initial

Investment 450000 450000

Net Present

value 251200 114130

Internal rate of return:

Calculation of internal rate of return

Table 3: Calculation of internal rate of return

Year Project A Project B

0 -450000 -450000

1 180000 60000

6

Project A Project B

Year Amount Cumulative Amount Cumulative

1 180000 180000 60000 60000

2 230000 410000 120000 180000

3 280000 690000 250000 430000

4 120000 810000 250000 680000

810000 680000

Payback period 2.68 years 3.58 years

Net present value:

Calculation of Net present value (In £)

Table 2: Calculation of Net present value

Project A Project B

Year Amount

Discounted

value@6%

Discounted

cash inflow Amount

Discounted

value @6%

Discounted

cash inflow

1 180000 0.943 169740 60000 0.943 56580

2 230000 0.89 204700 120000 0.89 106800

3 280000 0.84 235200 250000 0.84 210000

4 120000 0.763 91560 250000 0.763 190750

Total 810000 701200 680000 564130

Less- Initial

Investment 450000 450000

Net Present

value 251200 114130

Internal rate of return:

Calculation of internal rate of return

Table 3: Calculation of internal rate of return

Year Project A Project B

0 -450000 -450000

1 180000 60000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2 230000 120000

3 280000 250000

4 120000 250000

IRR 29.20% 15.02%

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

As per the above evaluation, it can be stated that management of ABC Engineering Ltd.

needs to consider Project A for business. This is because it is recovering initial investment in less

duration as compared to project B (The Investment Decision Making Process, 2011). In addition

to that value of NPV, IRR, and ARR are showing that Project A is better than Project B.

3.2 Explaining the calculation of unit costs and make pricing decisions using relevant

information

Scenario 3:

Table 4: calculation of unit costs

Particular Per unit Amount

Sales 120 900000

-Material cost 52.5 393750

labour cost 35.75 268125

Variable overhead 10.2 76500

Total Variable cost 98.45 738375

7

3 280000 250000

4 120000 250000

IRR 29.20% 15.02%

Accounting rate of return

Accounting rate of return (ARR) = Average profit/Initial Investment*100

Project A Average Profit = Total Profit/number of year

= 810000£/4

= 202500£

ARR = 202500£/450000£*100

= 45%

Project B

Average Profit = 680000£/4

= 170000£

ARR = 170000£/450000*100

= 37.78%

As per the above evaluation, it can be stated that management of ABC Engineering Ltd.

needs to consider Project A for business. This is because it is recovering initial investment in less

duration as compared to project B (The Investment Decision Making Process, 2011). In addition

to that value of NPV, IRR, and ARR are showing that Project A is better than Project B.

3.2 Explaining the calculation of unit costs and make pricing decisions using relevant

information

Scenario 3:

Table 4: calculation of unit costs

Particular Per unit Amount

Sales 120 900000

-Material cost 52.5 393750

labour cost 35.75 268125

Variable overhead 10.2 76500

Total Variable cost 98.45 738375

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contribution 21.55 161625

-fixed cost 120000

Profits 41625

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio = 161625£/900000£*100

= 17.96%.

Break-even point ( In units)= Total Fixed Cost/CPU

= 120000£/21.55£

= 5568.45 Units

Break-even point ( In £)

= 5568.45Units *120£

= 668213.46£

Margin of safety ( In £)= Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

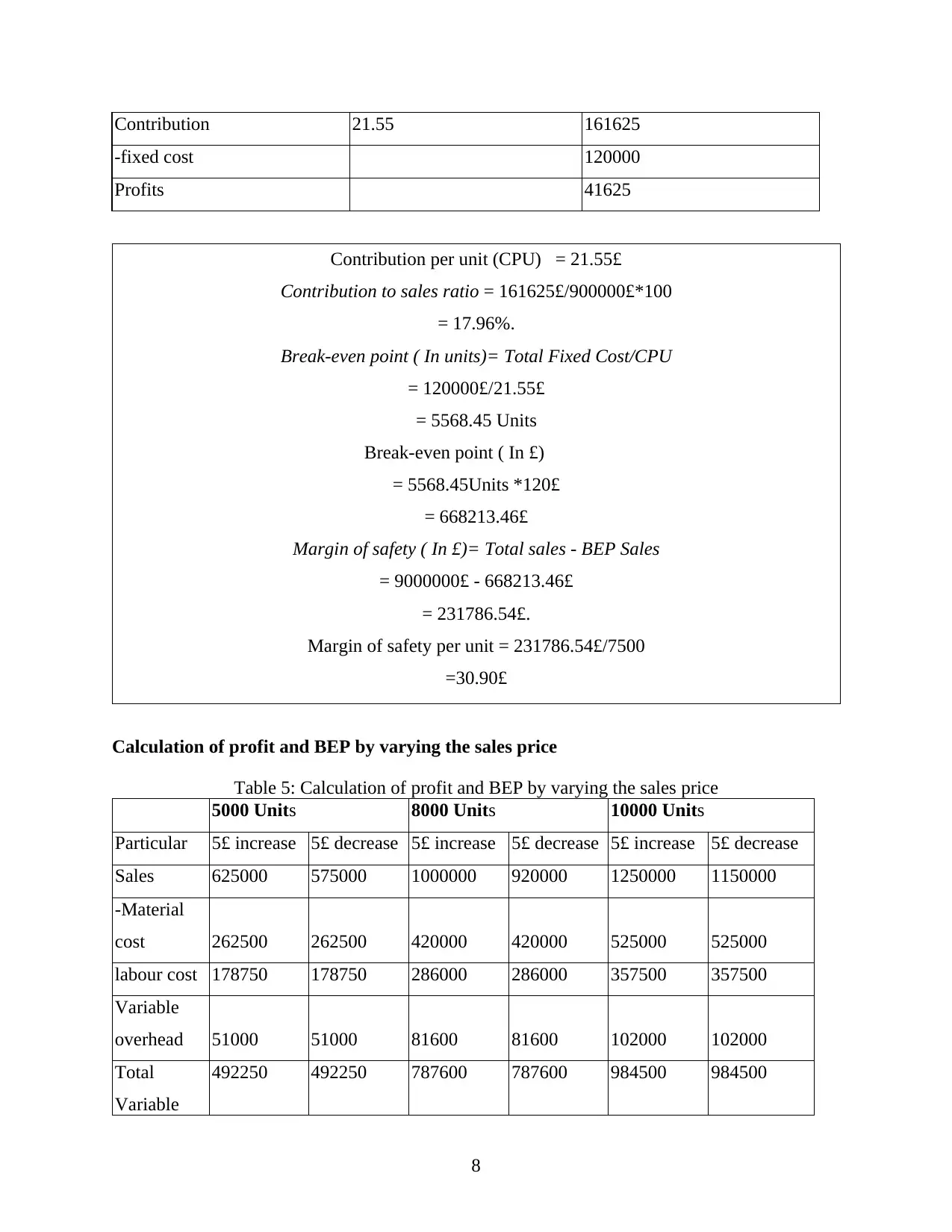

Calculation of profit and BEP by varying the sales price

Table 5: Calculation of profit and BEP by varying the sales price

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

Sales 625000 575000 1000000 920000 1250000 1150000

-Material

cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

492250 492250 787600 787600 984500 984500

8

-fixed cost 120000

Profits 41625

Contribution per unit (CPU) = 21.55£

Contribution to sales ratio = 161625£/900000£*100

= 17.96%.

Break-even point ( In units)= Total Fixed Cost/CPU

= 120000£/21.55£

= 5568.45 Units

Break-even point ( In £)

= 5568.45Units *120£

= 668213.46£

Margin of safety ( In £)= Total sales - BEP Sales

= 9000000£ - 668213.46£

= 231786.54£.

Margin of safety per unit = 231786.54£/7500

=30.90£

Calculation of profit and BEP by varying the sales price

Table 5: Calculation of profit and BEP by varying the sales price

5000 Units 8000 Units 10000 Units

Particular 5£ increase 5£ decrease 5£ increase 5£ decrease 5£ increase 5£ decrease

Sales 625000 575000 1000000 920000 1250000 1150000

-Material

cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

492250 492250 787600 787600 984500 984500

8

cost

Contributio

n 132750 82750 212400 132400 265500 165500

-fixed cost 120000 120000 120000 120000 120000 120000

Profits 12750 -37250 92400 12400 145500 45500

Contributio

n per unit 26.55 16.55 26.55 16.55 26.55 16.55

BEP 4519.77 7250.75 4519.77 7250.75 4519.77 7250.75

Calculation of BEP by varying the fixed cost

Table 6: Calculation of BEP by varying the fixed cost

5000 Units 8000 Units 10000 Units

Particular

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

Sales 600000 600000 960000 960000 1200000 1200000

-Material

cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 107750 107750 172400 172400 215500 215500

-fixed cost 125000 115000 125000 115000 125000 115000

Profits -17250 -7250 47400 57400 90500 100500

CPU 21.55 21.55 21.55 21.55 21.55 21.55

BEP 5800.46 5336.42 5800.46 5336.42 5800.46 5336.43

Calculation of BEP by varying the material Cost

9

Contributio

n 132750 82750 212400 132400 265500 165500

-fixed cost 120000 120000 120000 120000 120000 120000

Profits 12750 -37250 92400 12400 145500 45500

Contributio

n per unit 26.55 16.55 26.55 16.55 26.55 16.55

BEP 4519.77 7250.75 4519.77 7250.75 4519.77 7250.75

Calculation of BEP by varying the fixed cost

Table 6: Calculation of BEP by varying the fixed cost

5000 Units 8000 Units 10000 Units

Particular

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

5000£

increase

5000£

Decrease

Sales 600000 600000 960000 960000 1200000 1200000

-Material

cost 262500 262500 420000 420000 525000 525000

labour cost 178750 178750 286000 286000 357500 357500

Variable

overhead 51000 51000 81600 81600 102000 102000

Total

Variable

cost 492250 492250 787600 787600 984500 984500

Contributio

n 107750 107750 172400 172400 215500 215500

-fixed cost 125000 115000 125000 115000 125000 115000

Profits -17250 -7250 47400 57400 90500 100500

CPU 21.55 21.55 21.55 21.55 21.55 21.55

BEP 5800.46 5336.42 5800.46 5336.42 5800.46 5336.43

Calculation of BEP by varying the material Cost

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.