Financial Resource Management and Decision Making: Report Analysis

VerifiedAdded on 2019/12/03

|15

|4544

|100

Report

AI Summary

This report delves into the critical aspects of financial resource management and decision-making, crucial for business operations. It begins by identifying various sources of finance, both internal (retained earnings, cash squeezed, sale of assets, share capital) and external (loan capital), analyzing their implications, including legal, financial, and bankruptcy risks. The report then evaluates the cost of different sources of finance and their presentation in financial statements. Financial planning's importance is highlighted, along with information needs of different decision-makers. A cash budget is presented, along with the calculation of selling price using a cost-plus pricing method and the implications of investment appraisal techniques. The report further includes financial statement analysis and interpretation using ratio analysis. The report uses the case of Green Supplies Ltd. and Health Ltd. to provide practical examples of financial management and decision making.

Managing Financial Resources and

decisions

decisions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Different sources of finance.................................................................................1

AC 1.2 Legal, Financial and dilution of control implication and bankruptcy risks..........1

AC 1.3 Appropriate source of finance..............................................................................2

AC 2.1 Cost of various sources shown in Income statement and Balance sheet..............2

TASK 2......................................................................................................................................3

AC 2.2 Importance of financial planning.........................................................................3

AC 2.3 Information needs of various decision makers.....................................................4

Task 3.........................................................................................................................................4

AC 3.1 Cash Budget for Four months..............................................................................4

AC 3.2 Calculation of selling price and profit..................................................................5

AC 3.3 Implication of investment appraisal techniques...................................................6

TASK 4......................................................................................................................................8

AC 4.1 Financial statement of the company.....................................................................8

AC 4.2 Appropriate formats of financial statements:.......................................................8

AC 4.3 Interpretation of financial statements by calculating various ratios.....................9

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................12

1 | P a g e

Introduction................................................................................................................................1

TASK 1......................................................................................................................................1

AC 1.1 Different sources of finance.................................................................................1

AC 1.2 Legal, Financial and dilution of control implication and bankruptcy risks..........1

AC 1.3 Appropriate source of finance..............................................................................2

AC 2.1 Cost of various sources shown in Income statement and Balance sheet..............2

TASK 2......................................................................................................................................3

AC 2.2 Importance of financial planning.........................................................................3

AC 2.3 Information needs of various decision makers.....................................................4

Task 3.........................................................................................................................................4

AC 3.1 Cash Budget for Four months..............................................................................4

AC 3.2 Calculation of selling price and profit..................................................................5

AC 3.3 Implication of investment appraisal techniques...................................................6

TASK 4......................................................................................................................................8

AC 4.1 Financial statement of the company.....................................................................8

AC 4.2 Appropriate formats of financial statements:.......................................................8

AC 4.3 Interpretation of financial statements by calculating various ratios.....................9

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................12

1 | P a g e

List of tables

Table 1: Cash budget for Health Limited...................................................................................4

Table 2: Profit earned with 500 units.........................................................................................5

Table 3: Profit for additional 1000 units....................................................................................6

Table 4: Net present value..........................................................................................................6

Table 5: Cumulative cash flow..................................................................................................7

2 | P a g e

Table 1: Cash budget for Health Limited...................................................................................4

Table 2: Profit earned with 500 units.........................................................................................5

Table 3: Profit for additional 1000 units....................................................................................6

Table 4: Net present value..........................................................................................................6

Table 5: Cumulative cash flow..................................................................................................7

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every Business is concerned with production and distribution of goods and services to

satisfy their customer needs. Hence, for carrying out various businesses activity organization

requires money. Therefore, finance is also called the life blood of business. A business cannot

operate well without adequate funds. Initial capital invested by entrepreneur is not always

sufficient to meet financial requirements (Peirson, & et. al., 2014). So, the organization has to

look for other sources from where the need for funds can be met. A clear assessment of

financial needs and the identification of various source of finance is significant aspect for

running a business organization. In the presented report, we will identify different type of

internal and external source of finance along with the cost factor and also the appropriate

source of finance for Green Supplies Ltd. in addition to it, we apply different investment

appraisal techniques for various proposals and also selling price will be decided using cost

based pricing method.

TASK 1

AC 1.1 Different sources of finance

Retained earnings: It is an internal source of finance available for Green Supplies Ltd.

It means reinvestment of profit to earn further return. It can provide return for investors by

ploughing back of the earnings and also help business to grow.

Cash Squeezed: It means that organizations will pay their bills later and receive its

cash earlier from the customers. This internal source of finance provides huge boost to cash

flow to Green Supplies Ltd.

Sale of assets: Disposable assets such as plant and machinery, furniture and land can

be sold out to get financial sources for Green Supplies Ltd (Chandra, 2011). It is also an

internal source which fulfils the temporary requirement of finance.

Loan Capital: The most common way of loan capital is borrowing from bank. It is an

external source of finance available for Green Supplies Ltd. It can be either in the form of

bank overdraft or bank loan. Overdraft fulfils the short term requirement of companies to a

limited extent. Whereas, loan may be for short term or long term period based on the business

requirement.

Share capital: It is an internal source of finance as Green Supplies Ltd. can raise it

funds by issuing additional shares (Hayre, 2013). Venture capital providers are interested in

investing in businesses with dynamic growth prospectus.

3 | P a g e

Every Business is concerned with production and distribution of goods and services to

satisfy their customer needs. Hence, for carrying out various businesses activity organization

requires money. Therefore, finance is also called the life blood of business. A business cannot

operate well without adequate funds. Initial capital invested by entrepreneur is not always

sufficient to meet financial requirements (Peirson, & et. al., 2014). So, the organization has to

look for other sources from where the need for funds can be met. A clear assessment of

financial needs and the identification of various source of finance is significant aspect for

running a business organization. In the presented report, we will identify different type of

internal and external source of finance along with the cost factor and also the appropriate

source of finance for Green Supplies Ltd. in addition to it, we apply different investment

appraisal techniques for various proposals and also selling price will be decided using cost

based pricing method.

TASK 1

AC 1.1 Different sources of finance

Retained earnings: It is an internal source of finance available for Green Supplies Ltd.

It means reinvestment of profit to earn further return. It can provide return for investors by

ploughing back of the earnings and also help business to grow.

Cash Squeezed: It means that organizations will pay their bills later and receive its

cash earlier from the customers. This internal source of finance provides huge boost to cash

flow to Green Supplies Ltd.

Sale of assets: Disposable assets such as plant and machinery, furniture and land can

be sold out to get financial sources for Green Supplies Ltd (Chandra, 2011). It is also an

internal source which fulfils the temporary requirement of finance.

Loan Capital: The most common way of loan capital is borrowing from bank. It is an

external source of finance available for Green Supplies Ltd. It can be either in the form of

bank overdraft or bank loan. Overdraft fulfils the short term requirement of companies to a

limited extent. Whereas, loan may be for short term or long term period based on the business

requirement.

Share capital: It is an internal source of finance as Green Supplies Ltd. can raise it

funds by issuing additional shares (Hayre, 2013). Venture capital providers are interested in

investing in businesses with dynamic growth prospectus.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AC 1.2 Legal, Financial and dilution of control implication and bankruptcy risks

Each sources of finance whether internal or external bring many risks to the company.

Each financial source has a set of legal as well as financial restriction such as bankruptcy and

so on.

Share Capital: Equity shareholders are owners of the company so legal implication

for Green Supplies Ltd. is that the shareholders have voting rights which they can use to

manage the company (Brigham, & Ehrhardt, 2013). Moreover, Green Supplies Ltd. is not

legally obliged to pay dividends to its shareholders. Moreover, the paying investment is not

obligatory. Diluted control exists in case of equity financing for the company and bankruptcy

implication means that the Green Supplies Ltd. has to pay return to shareholders from its

residual asset.

Debt financing: In case of debt financing, legal implication for Green Supplies Ltd. is

that it has to pay tax over the loan borrowed and interest paid. On other hand, financial

obligation for the company is about paying the interest and loan instalment periodically.

Moreover, bankruptcy implication is that assets can be sold out to repay bank loan in case of

default of the company. k. No diluted control exists in case of debt financing for the company

because creditors are not the owner of the organization.

AC 1.3 Appropriate source of finance

Retained earnings: It may be considered as an appropriate source of finance for Green

supplies Ltd. since it does not include any explicit cost such as interest and dividend.

Immediate requirements for funds can be met out by retained earnings. It has a greater degree

of freedom and flexibility (Van Horne, & Wachowicz, 2008). However, disadvantage is that

it provides funds to a limited extent. Moreover, excessive ploughing back may cause

dissatisfaction among shareholders as they will get limited amount of dividend.

Loan Capital: Green Supplies Ltd. can meet its financial requirements by borrowings.

It is considered to be an appropriate source because the company can take loan for short,

medium and long term. In addition to it, interest is an allowable expenditure for tax purpose.

Whereas, disadvantage is that the organization has to pay interest and instalment periodically.

The company has to mortgage a security against their loan. Secured assets can be sold out by

bank in case of default by the firm.

Share capital: Green Supplies Ltd. can raise its funds by issuing both equity and

preference shares. It is advantageous for the company because business is not obliged to pay

dividend and repay the capital to the shareholders (Sin ha, 2012). On contrary, disadvantage

4 | P a g e

Each sources of finance whether internal or external bring many risks to the company.

Each financial source has a set of legal as well as financial restriction such as bankruptcy and

so on.

Share Capital: Equity shareholders are owners of the company so legal implication

for Green Supplies Ltd. is that the shareholders have voting rights which they can use to

manage the company (Brigham, & Ehrhardt, 2013). Moreover, Green Supplies Ltd. is not

legally obliged to pay dividends to its shareholders. Moreover, the paying investment is not

obligatory. Diluted control exists in case of equity financing for the company and bankruptcy

implication means that the Green Supplies Ltd. has to pay return to shareholders from its

residual asset.

Debt financing: In case of debt financing, legal implication for Green Supplies Ltd. is

that it has to pay tax over the loan borrowed and interest paid. On other hand, financial

obligation for the company is about paying the interest and loan instalment periodically.

Moreover, bankruptcy implication is that assets can be sold out to repay bank loan in case of

default of the company. k. No diluted control exists in case of debt financing for the company

because creditors are not the owner of the organization.

AC 1.3 Appropriate source of finance

Retained earnings: It may be considered as an appropriate source of finance for Green

supplies Ltd. since it does not include any explicit cost such as interest and dividend.

Immediate requirements for funds can be met out by retained earnings. It has a greater degree

of freedom and flexibility (Van Horne, & Wachowicz, 2008). However, disadvantage is that

it provides funds to a limited extent. Moreover, excessive ploughing back may cause

dissatisfaction among shareholders as they will get limited amount of dividend.

Loan Capital: Green Supplies Ltd. can meet its financial requirements by borrowings.

It is considered to be an appropriate source because the company can take loan for short,

medium and long term. In addition to it, interest is an allowable expenditure for tax purpose.

Whereas, disadvantage is that the organization has to pay interest and instalment periodically.

The company has to mortgage a security against their loan. Secured assets can be sold out by

bank in case of default by the firm.

Share capital: Green Supplies Ltd. can raise its funds by issuing both equity and

preference shares. It is advantageous for the company because business is not obliged to pay

dividend and repay the capital to the shareholders (Sin ha, 2012). On contrary, disadvantage

4 | P a g e

is that equity shareholders are owners of the company. So, they have the voting rights and

substantial part of the ownership in the company.

AC 2.1 Cost of various sources shown in Income statement and Balance sheet

Cost of Debt: Cost of debt means the interest rate which is merely paid by the

company on such loans. In Income statement, interest will be shown in debit side of profit

and loss account. Moreover in balance sheet the interest expenses will be deducted from the

cash and loan amount will be added. Loan will also be shown in debt capital in liability side

of the balance sheet (Pike, & Neale, 2006). The loan instalment paid by the company is

deducted from cash and debt respectively.

Cost of share capital: Cost of equity is rate of return demanded by shareholders on

their investment. Dividend and flotation cost paid by the company is an indirect expense

hence, it will be shown in the profit and loss account (Haka, 2006). Moreover, the share

capital issued by the company will be shown as equity and preference share capital in liability

side. Moreover, issued share capital will be included in cash and dividend paid will be

deducted.

Cost of retained earnings: It includes the return which shareholder require on

company's common stock (Götze, Northcott, & Schuster, 2008). The amount of retained

earnings utilised will be deducted from equity. Moreover, it will be deducted from cash in

assets side.

TASK 2

AC 2.2 Importance of financial planning

Financial planning is the process of estimating capital required and identifies the

appropriate source of finance (Siano, Kitchen, & Confetto, 2010). It is the process of framing

financial policies in relation to procurement, investment and proper administration of funds.

Importance of financial planning is given below:

It determines the amount of finance which is needed by an enterprise to carry out its

operations smoothly.

It evaluates various sources of funds so as to identify appropriate source of finance.

It helps in making policies for proper utilisation and administration of funds.

It acts as a source checking financial activities by comparing its actual and estimated

revenue (Sian, & Roberts, 2009). It is also important controlling cost by comparing

actual cost with estimated amount.

5 | P a g e

substantial part of the ownership in the company.

AC 2.1 Cost of various sources shown in Income statement and Balance sheet

Cost of Debt: Cost of debt means the interest rate which is merely paid by the

company on such loans. In Income statement, interest will be shown in debit side of profit

and loss account. Moreover in balance sheet the interest expenses will be deducted from the

cash and loan amount will be added. Loan will also be shown in debt capital in liability side

of the balance sheet (Pike, & Neale, 2006). The loan instalment paid by the company is

deducted from cash and debt respectively.

Cost of share capital: Cost of equity is rate of return demanded by shareholders on

their investment. Dividend and flotation cost paid by the company is an indirect expense

hence, it will be shown in the profit and loss account (Haka, 2006). Moreover, the share

capital issued by the company will be shown as equity and preference share capital in liability

side. Moreover, issued share capital will be included in cash and dividend paid will be

deducted.

Cost of retained earnings: It includes the return which shareholder require on

company's common stock (Götze, Northcott, & Schuster, 2008). The amount of retained

earnings utilised will be deducted from equity. Moreover, it will be deducted from cash in

assets side.

TASK 2

AC 2.2 Importance of financial planning

Financial planning is the process of estimating capital required and identifies the

appropriate source of finance (Siano, Kitchen, & Confetto, 2010). It is the process of framing

financial policies in relation to procurement, investment and proper administration of funds.

Importance of financial planning is given below:

It determines the amount of finance which is needed by an enterprise to carry out its

operations smoothly.

It evaluates various sources of funds so as to identify appropriate source of finance.

It helps in making policies for proper utilisation and administration of funds.

It acts as a source checking financial activities by comparing its actual and estimated

revenue (Sian, & Roberts, 2009). It is also important controlling cost by comparing

actual cost with estimated amount.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It ensures balance between fund's inflow and outflow so that financial stability is

maintained.

It helps in making growth and expansion programmes which in turn help in long run

survival of the company.

It reduces uncertainties with regards to changing market trends. This helps in ensuring

stability and profitability of the business.

For the success of Green Supplies ltd, financial planning is very important so as to

determine its short term and long term capital requirements. The company can decide its

capital structure which includes decision regarding both debt and equity capital. Moreover, it

also assists the business for cost controlling purpose (Ellwood and Newberry, 2007).

Through financial planning, business can survive for long run by proper management of their

funds. It ensures financial stability for Green Supplies Ltd. by reducing uncertainties. Finance

manager ensures that scarce financial resources are optimally utilized at least cost. This in

turn provides maximum returns on investment.

AC 2.3 Information needs of various decision makers

Financial statement satisfies the need of different decision makers by providing

useful information to them (Claessens, 2006).

Managers: Managers are liable to manage all operations and growth of the company.

They require financial statement to manage affairs of the company by assessing financial

performance of the business.

Shareholders: They invest in the company with the objective of high return.

Therefore, they use financial statements so as to analyse risk and return of their investment so

as to make better investment decisions.

Investors: They require financial statements to assess viability of investment in the

company. They predict future dividend on the basis of profits because fluctuation in profits

indicate higher risk. Furthermore, they analyse risk associated with their respective

investment and take necessary decisions.

Financial Institutions: Lending decisions are based on sufficient assets and liquidity

position of the business. Therefore, banks use financial statements to analyse financial health

of a business.

Employees: They use financial statements for assessing profitability and its

consequences on their future remuneration and job security.

6 | P a g e

maintained.

It helps in making growth and expansion programmes which in turn help in long run

survival of the company.

It reduces uncertainties with regards to changing market trends. This helps in ensuring

stability and profitability of the business.

For the success of Green Supplies ltd, financial planning is very important so as to

determine its short term and long term capital requirements. The company can decide its

capital structure which includes decision regarding both debt and equity capital. Moreover, it

also assists the business for cost controlling purpose (Ellwood and Newberry, 2007).

Through financial planning, business can survive for long run by proper management of their

funds. It ensures financial stability for Green Supplies Ltd. by reducing uncertainties. Finance

manager ensures that scarce financial resources are optimally utilized at least cost. This in

turn provides maximum returns on investment.

AC 2.3 Information needs of various decision makers

Financial statement satisfies the need of different decision makers by providing

useful information to them (Claessens, 2006).

Managers: Managers are liable to manage all operations and growth of the company.

They require financial statement to manage affairs of the company by assessing financial

performance of the business.

Shareholders: They invest in the company with the objective of high return.

Therefore, they use financial statements so as to analyse risk and return of their investment so

as to make better investment decisions.

Investors: They require financial statements to assess viability of investment in the

company. They predict future dividend on the basis of profits because fluctuation in profits

indicate higher risk. Furthermore, they analyse risk associated with their respective

investment and take necessary decisions.

Financial Institutions: Lending decisions are based on sufficient assets and liquidity

position of the business. Therefore, banks use financial statements to analyse financial health

of a business.

Employees: They use financial statements for assessing profitability and its

consequences on their future remuneration and job security.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

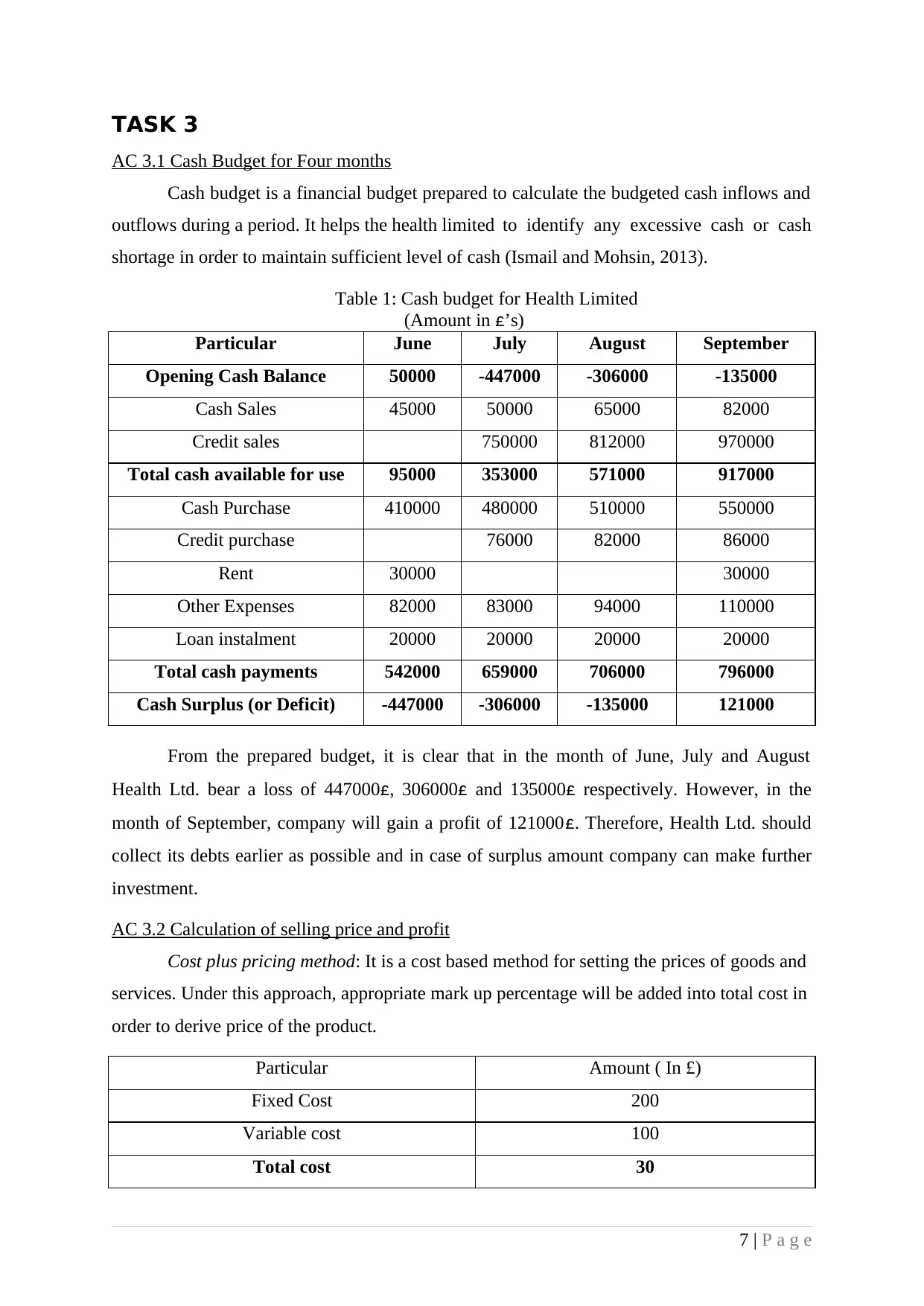

TASK 3

AC 3.1 Cash Budget for Four months

Cash budget is a financial budget prepared to calculate the budgeted cash inflows and

outflows during a period. It helps the health limited to identify any excessive cash or cash

shortage in order to maintain sufficient level of cash (Ismail and Mohsin, 2013).

Table 1: Cash budget for Health Limited

(Amount in £’s)

Particular June July August September

Opening Cash Balance 50000 -447000 -306000 -135000

Cash Sales 45000 50000 65000 82000

Credit sales 750000 812000 970000

Total cash available for use 95000 353000 571000 917000

Cash Purchase 410000 480000 510000 550000

Credit purchase 76000 82000 86000

Rent 30000 30000

Other Expenses 82000 83000 94000 110000

Loan instalment 20000 20000 20000 20000

Total cash payments 542000 659000 706000 796000

Cash Surplus (or Deficit) -447000 -306000 -135000 121000

From the prepared budget, it is clear that in the month of June, July and August

Health Ltd. bear a loss of 447000£, 306000£ and 135000£ respectively. However, in the

month of September, company will gain a profit of 121000£. Therefore, Health Ltd. should

collect its debts earlier as possible and in case of surplus amount company can make further

investment.

AC 3.2 Calculation of selling price and profit

Cost plus pricing method: It is a cost based method for setting the prices of goods and

services. Under this approach, appropriate mark up percentage will be added into total cost in

order to derive price of the product.

Particular Amount ( In £)

Fixed Cost 200

Variable cost 100

Total cost 30

7 | P a g e

AC 3.1 Cash Budget for Four months

Cash budget is a financial budget prepared to calculate the budgeted cash inflows and

outflows during a period. It helps the health limited to identify any excessive cash or cash

shortage in order to maintain sufficient level of cash (Ismail and Mohsin, 2013).

Table 1: Cash budget for Health Limited

(Amount in £’s)

Particular June July August September

Opening Cash Balance 50000 -447000 -306000 -135000

Cash Sales 45000 50000 65000 82000

Credit sales 750000 812000 970000

Total cash available for use 95000 353000 571000 917000

Cash Purchase 410000 480000 510000 550000

Credit purchase 76000 82000 86000

Rent 30000 30000

Other Expenses 82000 83000 94000 110000

Loan instalment 20000 20000 20000 20000

Total cash payments 542000 659000 706000 796000

Cash Surplus (or Deficit) -447000 -306000 -135000 121000

From the prepared budget, it is clear that in the month of June, July and August

Health Ltd. bear a loss of 447000£, 306000£ and 135000£ respectively. However, in the

month of September, company will gain a profit of 121000£. Therefore, Health Ltd. should

collect its debts earlier as possible and in case of surplus amount company can make further

investment.

AC 3.2 Calculation of selling price and profit

Cost plus pricing method: It is a cost based method for setting the prices of goods and

services. Under this approach, appropriate mark up percentage will be added into total cost in

order to derive price of the product.

Particular Amount ( In £)

Fixed Cost 200

Variable cost 100

Total cost 30

7 | P a g e

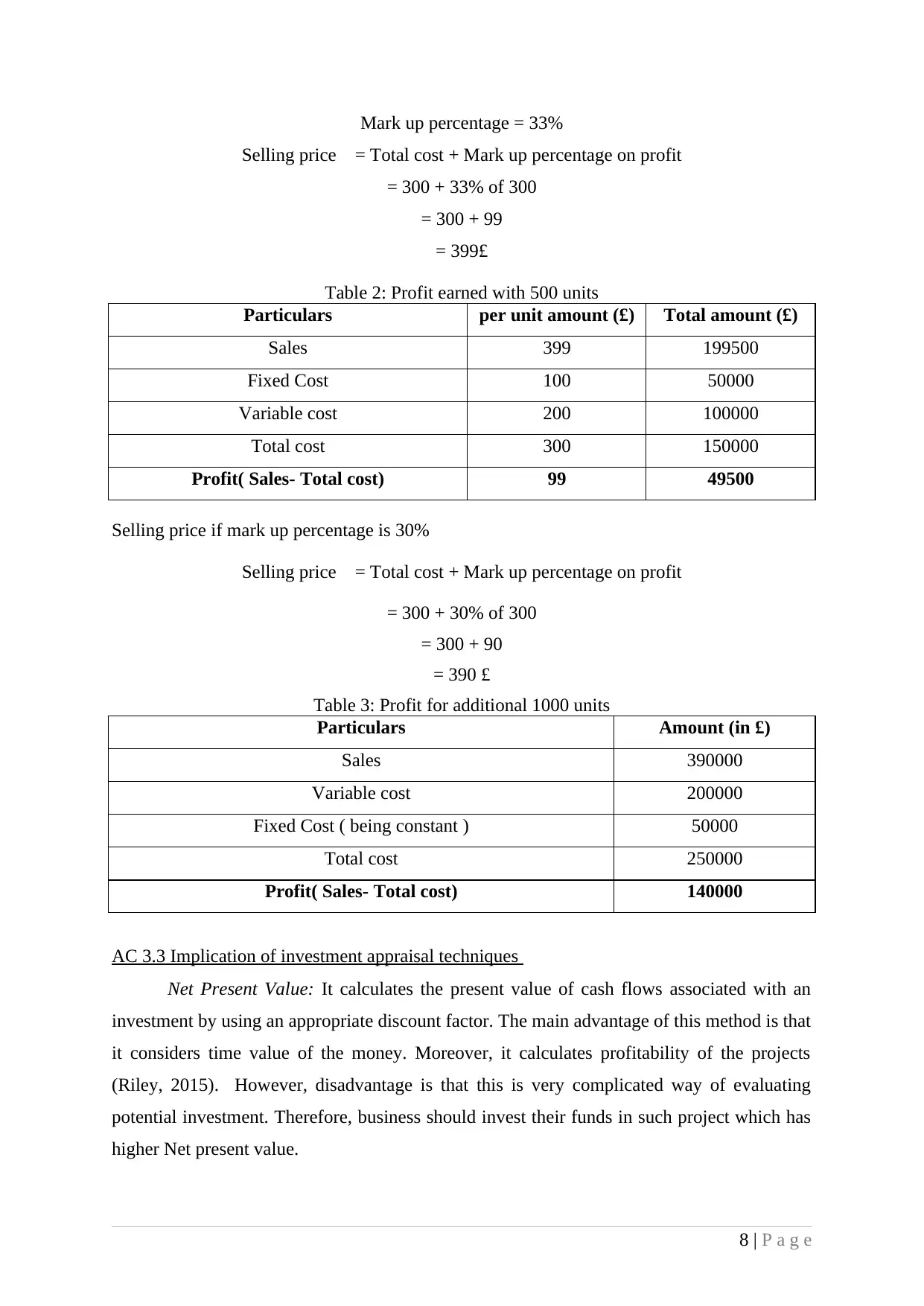

Mark up percentage = 33%

Selling price = Total cost + Mark up percentage on profit

= 300 + 33% of 300

= 300 + 99

= 399£

Table 2: Profit earned with 500 units

Particulars per unit amount (£) Total amount (£)

Sales 399 199500

Fixed Cost 100 50000

Variable cost 200 100000

Total cost 300 150000

Profit( Sales- Total cost) 99 49500

Selling price if mark up percentage is 30%

Selling price = Total cost + Mark up percentage on profit

= 300 + 30% of 300

= 300 + 90

= 390 £

Table 3: Profit for additional 1000 units

Particulars Amount (in £)

Sales 390000

Variable cost 200000

Fixed Cost ( being constant ) 50000

Total cost 250000

Profit( Sales- Total cost) 140000

AC 3.3 Implication of investment appraisal techniques

Net Present Value: It calculates the present value of cash flows associated with an

investment by using an appropriate discount factor. The main advantage of this method is that

it considers time value of the money. Moreover, it calculates profitability of the projects

(Riley, 2015). However, disadvantage is that this is very complicated way of evaluating

potential investment. Therefore, business should invest their funds in such project which has

higher Net present value.

8 | P a g e

Selling price = Total cost + Mark up percentage on profit

= 300 + 33% of 300

= 300 + 99

= 399£

Table 2: Profit earned with 500 units

Particulars per unit amount (£) Total amount (£)

Sales 399 199500

Fixed Cost 100 50000

Variable cost 200 100000

Total cost 300 150000

Profit( Sales- Total cost) 99 49500

Selling price if mark up percentage is 30%

Selling price = Total cost + Mark up percentage on profit

= 300 + 30% of 300

= 300 + 90

= 390 £

Table 3: Profit for additional 1000 units

Particulars Amount (in £)

Sales 390000

Variable cost 200000

Fixed Cost ( being constant ) 50000

Total cost 250000

Profit( Sales- Total cost) 140000

AC 3.3 Implication of investment appraisal techniques

Net Present Value: It calculates the present value of cash flows associated with an

investment by using an appropriate discount factor. The main advantage of this method is that

it considers time value of the money. Moreover, it calculates profitability of the projects

(Riley, 2015). However, disadvantage is that this is very complicated way of evaluating

potential investment. Therefore, business should invest their funds in such project which has

higher Net present value.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

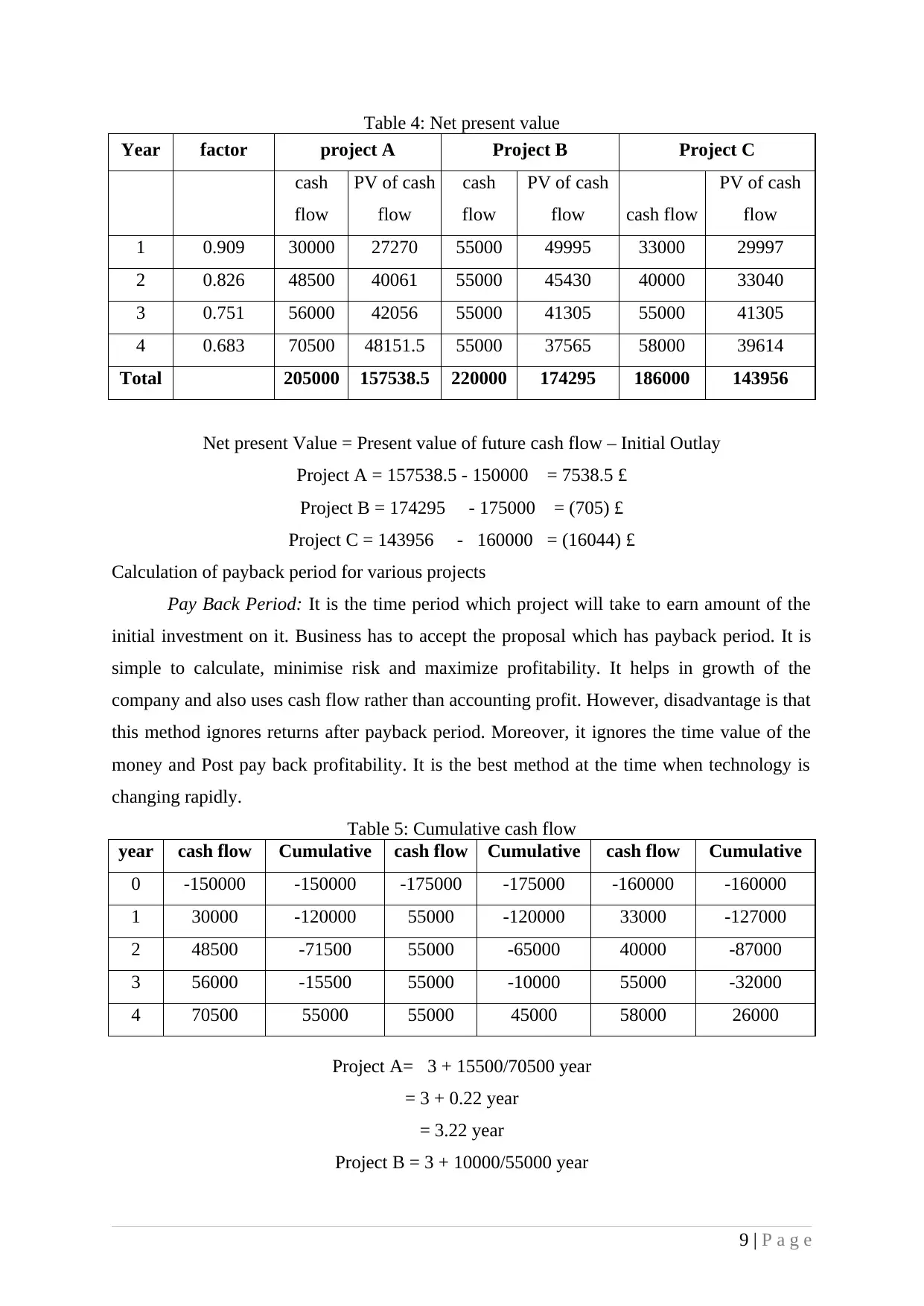

Table 4: Net present value

Year factor project A Project B Project C

cash

flow

PV of cash

flow

cash

flow

PV of cash

flow cash flow

PV of cash

flow

1 0.909 30000 27270 55000 49995 33000 29997

2 0.826 48500 40061 55000 45430 40000 33040

3 0.751 56000 42056 55000 41305 55000 41305

4 0.683 70500 48151.5 55000 37565 58000 39614

Total 205000 157538.5 220000 174295 186000 143956

Net present Value = Present value of future cash flow – Initial Outlay

Project A = 157538.5 - 150000 = 7538.5 £

Project B = 174295 - 175000 = (705) £

Project C = 143956 - 160000 = (16044) £

Calculation of payback period for various projects

Pay Back Period: It is the time period which project will take to earn amount of the

initial investment on it. Business has to accept the proposal which has payback period. It is

simple to calculate, minimise risk and maximize profitability. It helps in growth of the

company and also uses cash flow rather than accounting profit. However, disadvantage is that

this method ignores returns after payback period. Moreover, it ignores the time value of the

money and Post pay back profitability. It is the best method at the time when technology is

changing rapidly.

Table 5: Cumulative cash flow

year cash flow Cumulative cash flow Cumulative cash flow Cumulative

0 -150000 -150000 -175000 -175000 -160000 -160000

1 30000 -120000 55000 -120000 33000 -127000

2 48500 -71500 55000 -65000 40000 -87000

3 56000 -15500 55000 -10000 55000 -32000

4 70500 55000 55000 45000 58000 26000

Project A= 3 + 15500/70500 year

= 3 + 0.22 year

= 3.22 year

Project B = 3 + 10000/55000 year

9 | P a g e

Year factor project A Project B Project C

cash

flow

PV of cash

flow

cash

flow

PV of cash

flow cash flow

PV of cash

flow

1 0.909 30000 27270 55000 49995 33000 29997

2 0.826 48500 40061 55000 45430 40000 33040

3 0.751 56000 42056 55000 41305 55000 41305

4 0.683 70500 48151.5 55000 37565 58000 39614

Total 205000 157538.5 220000 174295 186000 143956

Net present Value = Present value of future cash flow – Initial Outlay

Project A = 157538.5 - 150000 = 7538.5 £

Project B = 174295 - 175000 = (705) £

Project C = 143956 - 160000 = (16044) £

Calculation of payback period for various projects

Pay Back Period: It is the time period which project will take to earn amount of the

initial investment on it. Business has to accept the proposal which has payback period. It is

simple to calculate, minimise risk and maximize profitability. It helps in growth of the

company and also uses cash flow rather than accounting profit. However, disadvantage is that

this method ignores returns after payback period. Moreover, it ignores the time value of the

money and Post pay back profitability. It is the best method at the time when technology is

changing rapidly.

Table 5: Cumulative cash flow

year cash flow Cumulative cash flow Cumulative cash flow Cumulative

0 -150000 -150000 -175000 -175000 -160000 -160000

1 30000 -120000 55000 -120000 33000 -127000

2 48500 -71500 55000 -65000 40000 -87000

3 56000 -15500 55000 -10000 55000 -32000

4 70500 55000 55000 45000 58000 26000

Project A= 3 + 15500/70500 year

= 3 + 0.22 year

= 3.22 year

Project B = 3 + 10000/55000 year

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 3 + 0.182 year

= 3.182 year

Project C = 3 + 32000/58000 year

= 3 + 0.552 year

= 3.552 year

Recommendation: By applying the net present value method, it is identified that net

present value of project A is 7538.5£ whereas project B and project C has negative NPV of

704£ and 16044£. Therefore, Day choice Ltd. should invest in project A. Moreover, the

payback period is 3.22, 3.182 and 3.552 respectively. It is lowest in project B, but if company

invest in this project then it will get a loss of 704£. Thus, by taking both the techniques into

consideration, it is clear that as finance manager of the company should invest in project A.

TASK 4

AC 4.1 Financial statement of the company

Financial statement includes both Income statement and balance sheet which is

produced by a business. Every business prepares financial statements periodically to know

the profitability as well as financial position of the business.

Income statement: It includes both Trading and Profit and loss Account of the company.

Trading Account: It is prepared by a trading company so as to identify gross profit of

the business. Gross profit is excess of sales over cost of goods sold. All the purchase and

direct expenses are shown in debit side and in credit side; sales and closing inventory are

shown in this account.

Profit and loss Account: It is prepared to identify the net profitability of the business.

The indirect expenses are shown in its debit side such as stationery, rent, Salary etc whereas

indirect income are shown in the credit side. Therefore, the excess of indirect income plus

gross profit over indirect expenses are termed as net profit. On contrary, excess of indirect

expenses over income is termed as net loss.

Balance sheet: Balance sheet is prepared at end of company's accounting period. It is

prepared to know financial position of the company. It shows liability and asset position of

the business (Paramasivan and Subramanian, 2010). Liability includes equity and preference

share capital, debt capital and current liability of the business. However, Assets includes all

fixed as well as current assets of the company.

10 | P a g e

= 3.182 year

Project C = 3 + 32000/58000 year

= 3 + 0.552 year

= 3.552 year

Recommendation: By applying the net present value method, it is identified that net

present value of project A is 7538.5£ whereas project B and project C has negative NPV of

704£ and 16044£. Therefore, Day choice Ltd. should invest in project A. Moreover, the

payback period is 3.22, 3.182 and 3.552 respectively. It is lowest in project B, but if company

invest in this project then it will get a loss of 704£. Thus, by taking both the techniques into

consideration, it is clear that as finance manager of the company should invest in project A.

TASK 4

AC 4.1 Financial statement of the company

Financial statement includes both Income statement and balance sheet which is

produced by a business. Every business prepares financial statements periodically to know

the profitability as well as financial position of the business.

Income statement: It includes both Trading and Profit and loss Account of the company.

Trading Account: It is prepared by a trading company so as to identify gross profit of

the business. Gross profit is excess of sales over cost of goods sold. All the purchase and

direct expenses are shown in debit side and in credit side; sales and closing inventory are

shown in this account.

Profit and loss Account: It is prepared to identify the net profitability of the business.

The indirect expenses are shown in its debit side such as stationery, rent, Salary etc whereas

indirect income are shown in the credit side. Therefore, the excess of indirect income plus

gross profit over indirect expenses are termed as net profit. On contrary, excess of indirect

expenses over income is termed as net loss.

Balance sheet: Balance sheet is prepared at end of company's accounting period. It is

prepared to know financial position of the company. It shows liability and asset position of

the business (Paramasivan and Subramanian, 2010). Liability includes equity and preference

share capital, debt capital and current liability of the business. However, Assets includes all

fixed as well as current assets of the company.

10 | P a g e

AC 4.2 Appropriate formats of financial statements:

Financial statement in case of sole trader: It comprises of both income statement and

balance sheet. In income statement both trading and profit and loss account are prepared by

sole trader. It shows the income and expenditure which business has received or paid over a

given period. Sole trader receives income by selling the product and services provided to

others such as rent and interest income. However, expenditure includes both direct as well as

indirect expenditure. Direct expenses are expenses which are incurred for trading purpose

whereas indirect expenses are incurred for the purpose of running business. Profit is

computed by subtracting company's expenses from income. Hence, it shows overall

profitability of the business (Llias, 2010). Balance sheet indicates the financial position of

the business by showing its assets and liabilities respectively. Assets include fixed assets such

as plant and machinery, building and current assets include debtors, stock and cash.

Liabilities include long term liability and current liability such as creditors and provisions.

Capital is computed by subtracting liability from assets.

Financial statement of Public Ltd. Company: A company is a legal body in its own

right with an existence that is separate from its owners. They have to prepare their financial

statements according to requirement of respective companies act. They prepare only profit

and loss account to know its profitability. Gross profit is calculated by subtracting cost of

goods sold from the turnover. Moreover, operating incomes are added and expenditures are

subtracted to know the net profit. In addition to it, dividend paid to shareholders is also

shown in the balance sheet. It collects its funds by issuing shares and debt capital. Therefore,

balance sheet shows the assets and liability together with debt and equity capital. Moreover,

they also prepare the statements of changes in equity, cash flow and fund flow statement.

Profit = Revenues – Expenditures

Assets – Liabilities = Equity + Long term debt

AC 4.3 Interpretation of financial statements by calculating various ratios

Gross profit ratio = Gross profit / sales *100

Wholesale Business = 150000/580000*100

= 25.86%

Retail Business = 101000/426000*100

= 3.71%

Interpretation: Gross profit ratio of wholesale business and retail business are 25.86%

and 23.71% respectively. Thus on the basis of profitability ratio, Wholesale business is more

profitable because of higher gross profit ratio.

11 | P a g e

Financial statement in case of sole trader: It comprises of both income statement and

balance sheet. In income statement both trading and profit and loss account are prepared by

sole trader. It shows the income and expenditure which business has received or paid over a

given period. Sole trader receives income by selling the product and services provided to

others such as rent and interest income. However, expenditure includes both direct as well as

indirect expenditure. Direct expenses are expenses which are incurred for trading purpose

whereas indirect expenses are incurred for the purpose of running business. Profit is

computed by subtracting company's expenses from income. Hence, it shows overall

profitability of the business (Llias, 2010). Balance sheet indicates the financial position of

the business by showing its assets and liabilities respectively. Assets include fixed assets such

as plant and machinery, building and current assets include debtors, stock and cash.

Liabilities include long term liability and current liability such as creditors and provisions.

Capital is computed by subtracting liability from assets.

Financial statement of Public Ltd. Company: A company is a legal body in its own

right with an existence that is separate from its owners. They have to prepare their financial

statements according to requirement of respective companies act. They prepare only profit

and loss account to know its profitability. Gross profit is calculated by subtracting cost of

goods sold from the turnover. Moreover, operating incomes are added and expenditures are

subtracted to know the net profit. In addition to it, dividend paid to shareholders is also

shown in the balance sheet. It collects its funds by issuing shares and debt capital. Therefore,

balance sheet shows the assets and liability together with debt and equity capital. Moreover,

they also prepare the statements of changes in equity, cash flow and fund flow statement.

Profit = Revenues – Expenditures

Assets – Liabilities = Equity + Long term debt

AC 4.3 Interpretation of financial statements by calculating various ratios

Gross profit ratio = Gross profit / sales *100

Wholesale Business = 150000/580000*100

= 25.86%

Retail Business = 101000/426000*100

= 3.71%

Interpretation: Gross profit ratio of wholesale business and retail business are 25.86%

and 23.71% respectively. Thus on the basis of profitability ratio, Wholesale business is more

profitable because of higher gross profit ratio.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.