Financial Management and Development for Tyre Manufacturing Firm

VerifiedAdded on 2020/02/05

|16

|4415

|388

Report

AI Summary

This report delves into the critical aspects of financial resource management and development, specifically within the context of establishing a tyre manufacturing firm. It begins by identifying and evaluating various sources of finance, both internal (e.g., retained earnings, equity financing) and external (e.g., bank loans, mortgaging), along with their respective implications. The report emphasizes the importance of financial planning, outlining the steps involved and the roles of internal and external decision-makers. It further examines the impact of financial statements, such as profit and loss accounts and balance sheets, on a business's financial appearance. A budgeted cash flow plan for the initial six months of operation is presented, along with a unit cost calculation, and an investment proposal plan. The report underscores the significance of effective financial and pricing structures in achieving business objectives and highlights the need for careful management of financial resources to ensure sustainable growth and profitability. All the above mentioned information is contributed by a student to be published on the website Desklib.

MANAGING FINANCIAL

RESOURCES AND

DEVELOPMENT

L

e

g

a

l

I

L

e

g

a

l

I

RESOURCES AND

DEVELOPMENT

L

e

g

a

l

I

L

e

g

a

l

I

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

LO: 1...........................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................1

1.3................................................................................................................................................2

LO: 2...........................................................................................................................................3

2.1................................................................................................................................................3

2.2................................................................................................................................................3

2.3................................................................................................................................................4

2.4................................................................................................................................................4

LO: 3...........................................................................................................................................5

3.1................................................................................................................................................5

3.2................................................................................................................................................5

3.3................................................................................................................................................6

TASK 2............................................................................................................................................9

4.1................................................................................................................................................9

4.2................................................................................................................................................9

4.3..............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

LO: 1...........................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................1

1.3................................................................................................................................................2

LO: 2...........................................................................................................................................3

2.1................................................................................................................................................3

2.2................................................................................................................................................3

2.3................................................................................................................................................4

2.4................................................................................................................................................4

LO: 3...........................................................................................................................................5

3.1................................................................................................................................................5

3.2................................................................................................................................................5

3.3................................................................................................................................................6

TASK 2............................................................................................................................................9

4.1................................................................................................................................................9

4.2................................................................................................................................................9

4.3..............................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

A business needs to be specific and clear over their approaches of managing the financial

activities and making investment decisions in the operations. It would help them in maintaining

the level of revenue resources present among them and overcome all the funds crisis situations

(Broadbent and Cullen, 2012). Similar to this, the report is providing information about the

business approaches and processes which are requisite for an entrepreneur to establish the

manufacturing firm of tyres. For this, it is crucial that the person should be effective in

managing, controlling, allocating and utilising financial resources in the business activities.

TASK 1

LO: 1

1.1

It is an aim of every business to be effective and systematic in managing, controlling and

utilising the financial resources in best form. But, in the starting stage of establishment a

business needs to sum up high amount of capital to perform certain investments in the

organisational activities (Conway, 2013). In that context, the owner needs to address the most

beneficial and efficient financial sources which are able to acquire financial support: Internal sources: These sources are termed as the primary areas which are considered

prior most for a person for generating funds for their business. It includes the options

like personal contribution of the owner, taking borrowings from relatives, retained

earnings, equity financing, etc. The stated business requires high amount of capital,

hence the owner should opt for retained earnings and equity financing.

External sources: The secondary areas from where the business could gain financial

support for long or short term purpose (Rockey and Collins, 2010). The most common

external source of finance are taking loans from the banks or other institution, leasing,

debentures, mortgage, etc. Considering the business planning of the entrepreneur, he

should acquire funds through mortgaging and bank loans.

1.2

The following are the implications related with all the kinds of selected sources for the

planned business:

1

A business needs to be specific and clear over their approaches of managing the financial

activities and making investment decisions in the operations. It would help them in maintaining

the level of revenue resources present among them and overcome all the funds crisis situations

(Broadbent and Cullen, 2012). Similar to this, the report is providing information about the

business approaches and processes which are requisite for an entrepreneur to establish the

manufacturing firm of tyres. For this, it is crucial that the person should be effective in

managing, controlling, allocating and utilising financial resources in the business activities.

TASK 1

LO: 1

1.1

It is an aim of every business to be effective and systematic in managing, controlling and

utilising the financial resources in best form. But, in the starting stage of establishment a

business needs to sum up high amount of capital to perform certain investments in the

organisational activities (Conway, 2013). In that context, the owner needs to address the most

beneficial and efficient financial sources which are able to acquire financial support: Internal sources: These sources are termed as the primary areas which are considered

prior most for a person for generating funds for their business. It includes the options

like personal contribution of the owner, taking borrowings from relatives, retained

earnings, equity financing, etc. The stated business requires high amount of capital,

hence the owner should opt for retained earnings and equity financing.

External sources: The secondary areas from where the business could gain financial

support for long or short term purpose (Rockey and Collins, 2010). The most common

external source of finance are taking loans from the banks or other institution, leasing,

debentures, mortgage, etc. Considering the business planning of the entrepreneur, he

should acquire funds through mortgaging and bank loans.

1.2

The following are the implications related with all the kinds of selected sources for the

planned business:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bank Loans –

◦ Legal Implications – It could lead to seizing of the assets in case of default rules and

policies are used.

◦ Financial Implications – The payment of amortization per month/quarter/ annual

should be funded (Siano, Kitchen and Giovanna Confetto, 2010). Retained earnings – It is treated as a risk for entrepreneur to miss the business

opportunities at the times when he is unable to collect required funds for new venture.

The potentiality of the stated source is also limited up to certain extent (Trisha, 2016). Equity finance – The main implication of the specified source is to loose the control on

the business operations and functions.

Mortgaging – The bankruptcy is the major implication that could affect the entire

operation of the gaining better financial value.

1.3

The planned business should select the following specified sources and consider the

evaluation to determine their effectiveness for the planned business: Bank loans: The process of taking loans is quite long lasting and time consuming which

generally involves many types of verification and documentation which creates

consequences for the owner (Epstein and Buhovac, 2014). But, the money gained by the

source is highly crucial for the business in overcoming the organisational activities. Retained earnings: It is stated as the best method of contributing personally in the

business which includes less risk and overall expenditure. It would be beneficial for the

owner to gain successful return from the cited source. Equity finance: To share the possession, control and powers with the shareholders allows

the owner to divide the results, risk and impacts from the business which enables them to

suffer less (Farmer and et.al., 2012).

Mortgaging: This provides the entrepreneur high level of finance in return of transferring

the possession of the property. It continues up to long time period usually for more than

20 years.

2

◦ Legal Implications – It could lead to seizing of the assets in case of default rules and

policies are used.

◦ Financial Implications – The payment of amortization per month/quarter/ annual

should be funded (Siano, Kitchen and Giovanna Confetto, 2010). Retained earnings – It is treated as a risk for entrepreneur to miss the business

opportunities at the times when he is unable to collect required funds for new venture.

The potentiality of the stated source is also limited up to certain extent (Trisha, 2016). Equity finance – The main implication of the specified source is to loose the control on

the business operations and functions.

Mortgaging – The bankruptcy is the major implication that could affect the entire

operation of the gaining better financial value.

1.3

The planned business should select the following specified sources and consider the

evaluation to determine their effectiveness for the planned business: Bank loans: The process of taking loans is quite long lasting and time consuming which

generally involves many types of verification and documentation which creates

consequences for the owner (Epstein and Buhovac, 2014). But, the money gained by the

source is highly crucial for the business in overcoming the organisational activities. Retained earnings: It is stated as the best method of contributing personally in the

business which includes less risk and overall expenditure. It would be beneficial for the

owner to gain successful return from the cited source. Equity finance: To share the possession, control and powers with the shareholders allows

the owner to divide the results, risk and impacts from the business which enables them to

suffer less (Farmer and et.al., 2012).

Mortgaging: This provides the entrepreneur high level of finance in return of transferring

the possession of the property. It continues up to long time period usually for more than

20 years.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO: 2

2.1

It is essential for the business and their respective to assess the benefits and implications

related with the different sources of finance. This helps the aspects to determine the future crisis

and reduce their impact on the operational and functional activities (Bennett, Lutz and Jayaram,

2012). In that context, the following are the cost involved in the process of gaining financial

support from the stated sources: Interest: The high rate of interest is one of the major cost that add up the liabilities level

of the business owner. It reduces the profitability of the business by taking an appropriate

amount from the available funds with the owner for a certain period of time.

Charges and fees: At the time of processing the loans and mortgaging property, the

owner of the business has to pay fees and charges for documentation and overall

procedure of taking funds (Remund, 2010). This eventually increases the actual value

gained from the loans and other sources.

Different source of finance undertake various costs which business has to consider

necessarily. Issue of shares undertake dividend cost where it is necessary for business to deliver

return to the investors in the form of dividend. Apart from this bank loan is also another major

source of finance where organization has to bear interest cost. For the amount obtained from the

banks business has to pay interest. Retained earnings as one of the source undertaken does not

contain any such cost. So, in this case cost of each source of finance differs from each other

which organization has to consider necessarily.

2.2

Importance of financial planning

It is ascertained that financial planning is highly significant for a business for overcoming

the financial crisis and bankruptcy. The main purpose of the financial planning is to create and

implement a structure of investment and utilisation of capital in the business activities which

needs to positive and should determine a particular amount of return from overall investments

made by the owner (Wätzold and et.al., 2010).

Steps involved in financial planning

To define and evaluate the types and forms of financial objectives and goals for the

business.

3

2.1

It is essential for the business and their respective to assess the benefits and implications

related with the different sources of finance. This helps the aspects to determine the future crisis

and reduce their impact on the operational and functional activities (Bennett, Lutz and Jayaram,

2012). In that context, the following are the cost involved in the process of gaining financial

support from the stated sources: Interest: The high rate of interest is one of the major cost that add up the liabilities level

of the business owner. It reduces the profitability of the business by taking an appropriate

amount from the available funds with the owner for a certain period of time.

Charges and fees: At the time of processing the loans and mortgaging property, the

owner of the business has to pay fees and charges for documentation and overall

procedure of taking funds (Remund, 2010). This eventually increases the actual value

gained from the loans and other sources.

Different source of finance undertake various costs which business has to consider

necessarily. Issue of shares undertake dividend cost where it is necessary for business to deliver

return to the investors in the form of dividend. Apart from this bank loan is also another major

source of finance where organization has to bear interest cost. For the amount obtained from the

banks business has to pay interest. Retained earnings as one of the source undertaken does not

contain any such cost. So, in this case cost of each source of finance differs from each other

which organization has to consider necessarily.

2.2

Importance of financial planning

It is ascertained that financial planning is highly significant for a business for overcoming

the financial crisis and bankruptcy. The main purpose of the financial planning is to create and

implement a structure of investment and utilisation of capital in the business activities which

needs to positive and should determine a particular amount of return from overall investments

made by the owner (Wätzold and et.al., 2010).

Steps involved in financial planning

To define and evaluate the types and forms of financial objectives and goals for the

business.

3

To gather crucial information about the present financial and personal position.

To analyse the gathered information for assessing the required financial condition for the

business.

To develop and present an effective and systematic financial plan.

To implement and review the proposed financial plan by considering the business

approaches.

2.3

There are mainly two groups of decision makers in the business which are crucial in

making effective plans for the organisational operations and related functions. They are stated

below:

Internal users - Those who have directly bearing with the activities of the organization.

Managers and owners:

◦ To make business decisions

◦ To ease up the financial analysis

◦ Formulate contractual terms between your company and other organization.

Employees:

◦ To assess the information for implementing collective bargaining agreements

(Coombs, 2014).

◦ To discuss promotions, rankings and salary hike.

External users who are the stakeholders or general public outside the organization. Financial Institutions: Information required to raise finance like to hike the loan amount

the business has to produce the Financial statements so that the bank can verify their

liquidity ratio and debt level (Shim and et.al., 2010).

Government: Information needed for -

◦ Investigation of tax payment and validity of profit declared.

◦ General Mass and Media

◦ General public and students.

2.4

Impact of financial statements on the business appearance Profit and loss account – It is crucial for the business to determine authenticate values

and determination of the all the transactions made by them in the accounting period. At

4

To analyse the gathered information for assessing the required financial condition for the

business.

To develop and present an effective and systematic financial plan.

To implement and review the proposed financial plan by considering the business

approaches.

2.3

There are mainly two groups of decision makers in the business which are crucial in

making effective plans for the organisational operations and related functions. They are stated

below:

Internal users - Those who have directly bearing with the activities of the organization.

Managers and owners:

◦ To make business decisions

◦ To ease up the financial analysis

◦ Formulate contractual terms between your company and other organization.

Employees:

◦ To assess the information for implementing collective bargaining agreements

(Coombs, 2014).

◦ To discuss promotions, rankings and salary hike.

External users who are the stakeholders or general public outside the organization. Financial Institutions: Information required to raise finance like to hike the loan amount

the business has to produce the Financial statements so that the bank can verify their

liquidity ratio and debt level (Shim and et.al., 2010).

Government: Information needed for -

◦ Investigation of tax payment and validity of profit declared.

◦ General Mass and Media

◦ General public and students.

2.4

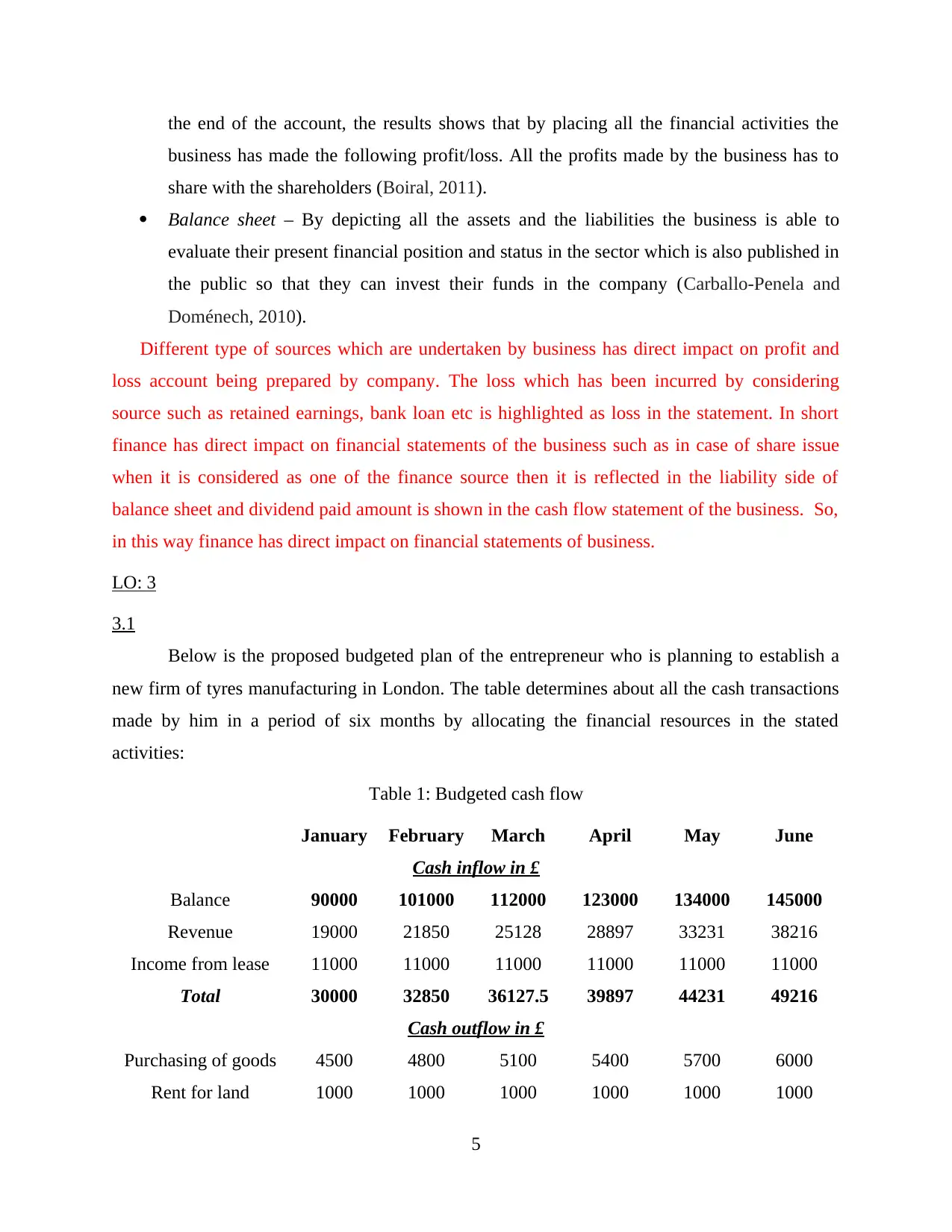

Impact of financial statements on the business appearance Profit and loss account – It is crucial for the business to determine authenticate values

and determination of the all the transactions made by them in the accounting period. At

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the end of the account, the results shows that by placing all the financial activities the

business has made the following profit/loss. All the profits made by the business has to

share with the shareholders (Boiral, 2011).

Balance sheet – By depicting all the assets and the liabilities the business is able to

evaluate their present financial position and status in the sector which is also published in

the public so that they can invest their funds in the company (Carballo-Penela and

Doménech, 2010).

Different type of sources which are undertaken by business has direct impact on profit and

loss account being prepared by company. The loss which has been incurred by considering

source such as retained earnings, bank loan etc is highlighted as loss in the statement. In short

finance has direct impact on financial statements of the business such as in case of share issue

when it is considered as one of the finance source then it is reflected in the liability side of

balance sheet and dividend paid amount is shown in the cash flow statement of the business. So,

in this way finance has direct impact on financial statements of business.

LO: 3

3.1

Below is the proposed budgeted plan of the entrepreneur who is planning to establish a

new firm of tyres manufacturing in London. The table determines about all the cash transactions

made by him in a period of six months by allocating the financial resources in the stated

activities:

Table 1: Budgeted cash flow

January February March April May June

Cash inflow in £

Balance 90000 101000 112000 123000 134000 145000

Revenue 19000 21850 25128 28897 33231 38216

Income from lease 11000 11000 11000 11000 11000 11000

Total 30000 32850 36127.5 39897 44231 49216

Cash outflow in £

Purchasing of goods 4500 4800 5100 5400 5700 6000

Rent for land 1000 1000 1000 1000 1000 1000

5

business has made the following profit/loss. All the profits made by the business has to

share with the shareholders (Boiral, 2011).

Balance sheet – By depicting all the assets and the liabilities the business is able to

evaluate their present financial position and status in the sector which is also published in

the public so that they can invest their funds in the company (Carballo-Penela and

Doménech, 2010).

Different type of sources which are undertaken by business has direct impact on profit and

loss account being prepared by company. The loss which has been incurred by considering

source such as retained earnings, bank loan etc is highlighted as loss in the statement. In short

finance has direct impact on financial statements of the business such as in case of share issue

when it is considered as one of the finance source then it is reflected in the liability side of

balance sheet and dividend paid amount is shown in the cash flow statement of the business. So,

in this way finance has direct impact on financial statements of business.

LO: 3

3.1

Below is the proposed budgeted plan of the entrepreneur who is planning to establish a

new firm of tyres manufacturing in London. The table determines about all the cash transactions

made by him in a period of six months by allocating the financial resources in the stated

activities:

Table 1: Budgeted cash flow

January February March April May June

Cash inflow in £

Balance 90000 101000 112000 123000 134000 145000

Revenue 19000 21850 25128 28897 33231 38216

Income from lease 11000 11000 11000 11000 11000 11000

Total 30000 32850 36127.5 39897 44231 49216

Cash outflow in £

Purchasing of goods 4500 4800 5100 5400 5700 6000

Rent for land 1000 1000 1000 1000 1000 1000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

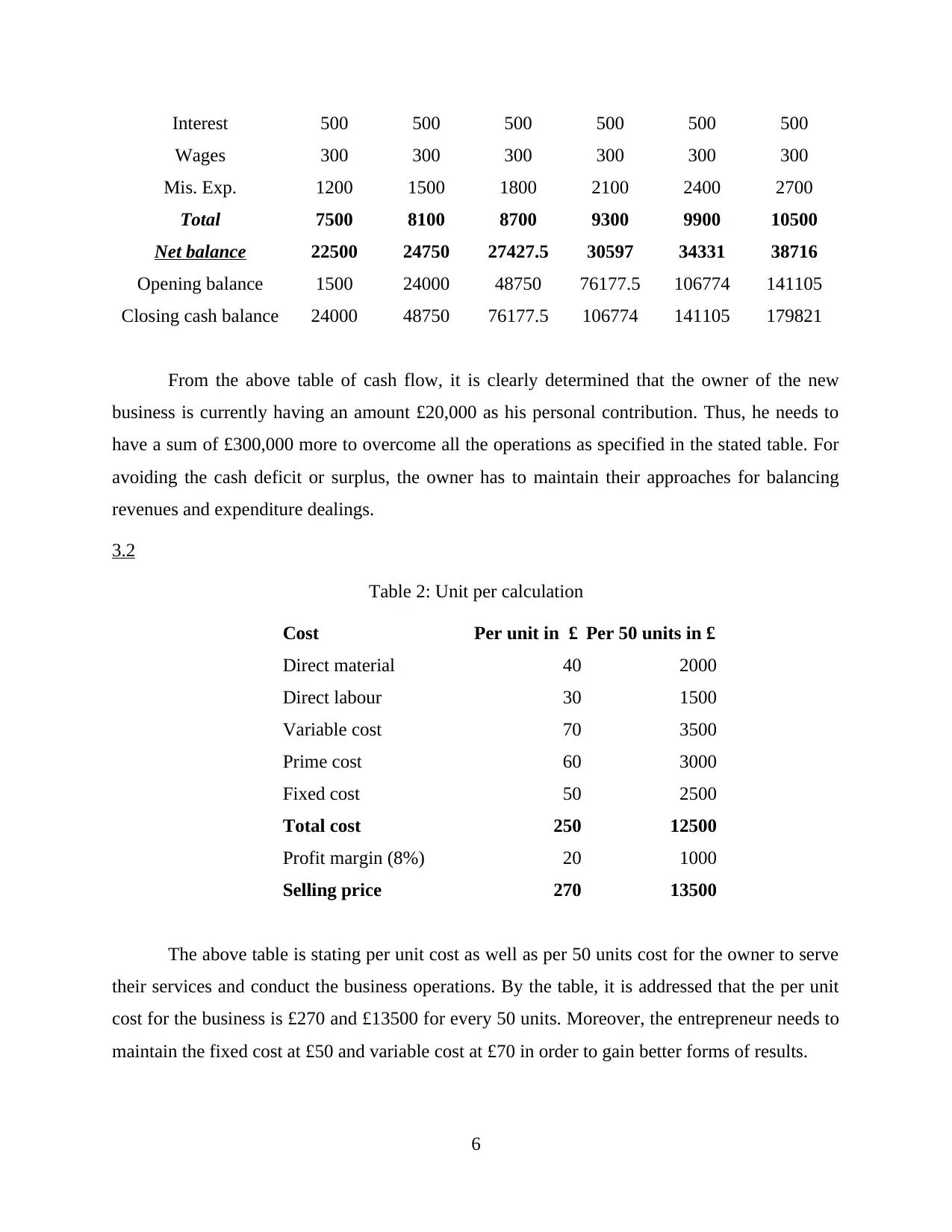

Interest 500 500 500 500 500 500

Wages 300 300 300 300 300 300

Mis. Exp. 1200 1500 1800 2100 2400 2700

Total 7500 8100 8700 9300 9900 10500

Net balance 22500 24750 27427.5 30597 34331 38716

Opening balance 1500 24000 48750 76177.5 106774 141105

Closing cash balance 24000 48750 76177.5 106774 141105 179821

From the above table of cash flow, it is clearly determined that the owner of the new

business is currently having an amount £20,000 as his personal contribution. Thus, he needs to

have a sum of £300,000 more to overcome all the operations as specified in the stated table. For

avoiding the cash deficit or surplus, the owner has to maintain their approaches for balancing

revenues and expenditure dealings.

3.2

Table 2: Unit per calculation

Cost Per unit in £ Per 50 units in £

Direct material 40 2000

Direct labour 30 1500

Variable cost 70 3500

Prime cost 60 3000

Fixed cost 50 2500

Total cost 250 12500

Profit margin (8%) 20 1000

Selling price 270 13500

The above table is stating per unit cost as well as per 50 units cost for the owner to serve

their services and conduct the business operations. By the table, it is addressed that the per unit

cost for the business is £270 and £13500 for every 50 units. Moreover, the entrepreneur needs to

maintain the fixed cost at £50 and variable cost at £70 in order to gain better forms of results.

6

Wages 300 300 300 300 300 300

Mis. Exp. 1200 1500 1800 2100 2400 2700

Total 7500 8100 8700 9300 9900 10500

Net balance 22500 24750 27427.5 30597 34331 38716

Opening balance 1500 24000 48750 76177.5 106774 141105

Closing cash balance 24000 48750 76177.5 106774 141105 179821

From the above table of cash flow, it is clearly determined that the owner of the new

business is currently having an amount £20,000 as his personal contribution. Thus, he needs to

have a sum of £300,000 more to overcome all the operations as specified in the stated table. For

avoiding the cash deficit or surplus, the owner has to maintain their approaches for balancing

revenues and expenditure dealings.

3.2

Table 2: Unit per calculation

Cost Per unit in £ Per 50 units in £

Direct material 40 2000

Direct labour 30 1500

Variable cost 70 3500

Prime cost 60 3000

Fixed cost 50 2500

Total cost 250 12500

Profit margin (8%) 20 1000

Selling price 270 13500

The above table is stating per unit cost as well as per 50 units cost for the owner to serve

their services and conduct the business operations. By the table, it is addressed that the per unit

cost for the business is £270 and £13500 for every 50 units. Moreover, the entrepreneur needs to

maintain the fixed cost at £50 and variable cost at £70 in order to gain better forms of results.

6

3.3

By planning effective and systematic financial and pricing structure, a business is able to

gain appropriate kind of results and achievements. In the below table, the initial investment

decisions and actions has been determined which would be able to lead their business to

accomplish better opportunities and make proper achievements.

Table 3: Investment proposal plans

Year Proposal A Proposal B

Initial investment 200000 200000

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

Pay back period

By the use of the stated technique, the owner is able to measure the time period which

would be required by his business to recover its initial amount of investment.

Year

Proposal

A

Cumulative cash

inflow

Proposal

B

Cumulative cash

inflow

Initial

investment 200000 200000

1 24000 24000 25000 25000

2 36000 60000 50000 75000

3 90000 150000 70000 145000

4 130000 280000 125000 270000

5 145000 425000 170000 440000

Proposal A: 3 + 80000/130000

= 3.615 years

Proposal B: 3 + 70000/125000

= 3.56 years

7

By planning effective and systematic financial and pricing structure, a business is able to

gain appropriate kind of results and achievements. In the below table, the initial investment

decisions and actions has been determined which would be able to lead their business to

accomplish better opportunities and make proper achievements.

Table 3: Investment proposal plans

Year Proposal A Proposal B

Initial investment 200000 200000

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

Pay back period

By the use of the stated technique, the owner is able to measure the time period which

would be required by his business to recover its initial amount of investment.

Year

Proposal

A

Cumulative cash

inflow

Proposal

B

Cumulative cash

inflow

Initial

investment 200000 200000

1 24000 24000 25000 25000

2 36000 60000 50000 75000

3 90000 150000 70000 145000

4 130000 280000 125000 270000

5 145000 425000 170000 440000

Proposal A: 3 + 80000/130000

= 3.615 years

Proposal B: 3 + 70000/125000

= 3.56 years

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of the above Payback Period calculation, it has been determined that Project

proposal B will be more productive and feasible for the owner of the firm. Through the stated the

investments decisions, the business will be able achieve its purpose.

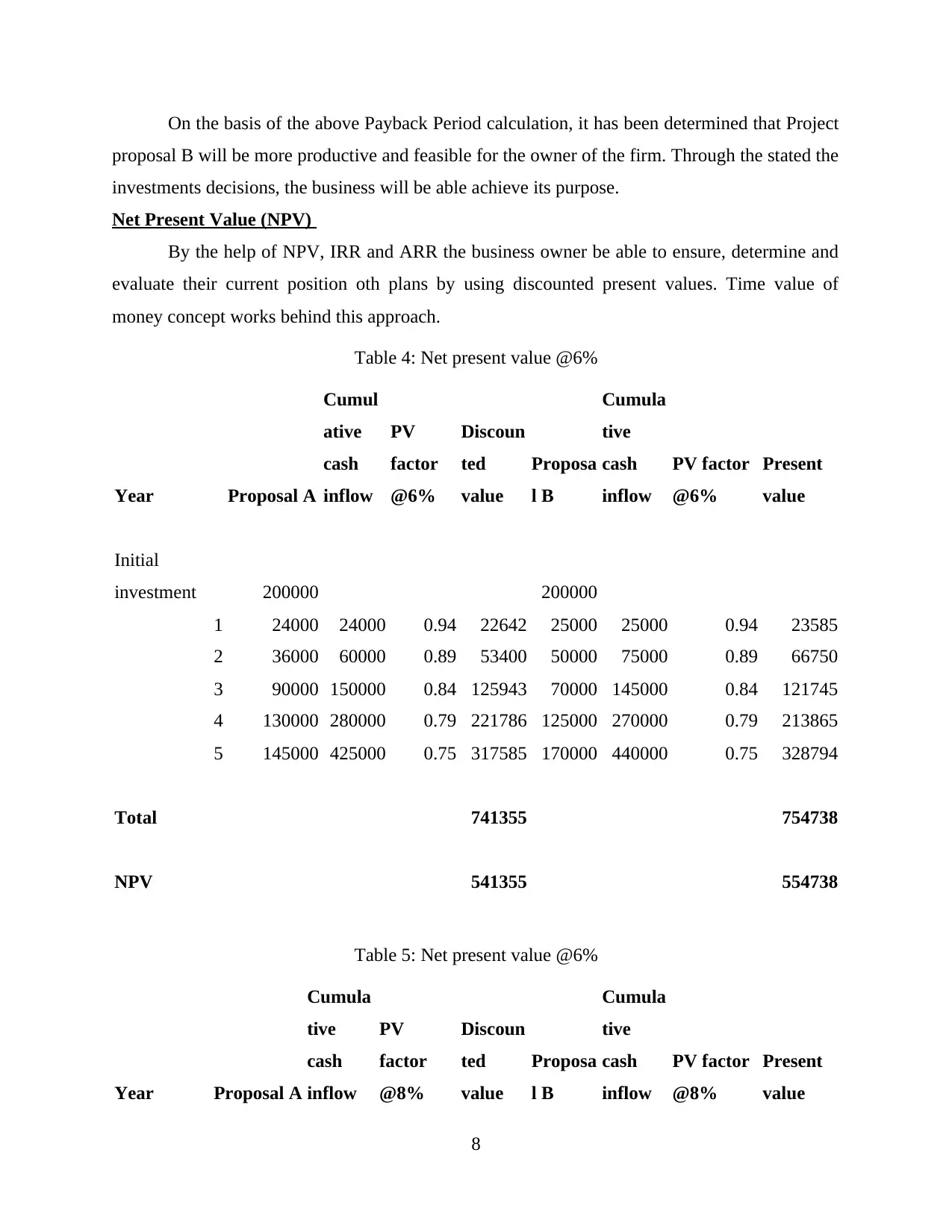

Net Present Value (NPV)

By the help of NPV, IRR and ARR the business owner be able to ensure, determine and

evaluate their current position oth plans by using discounted present values. Time value of

money concept works behind this approach.

Table 4: Net present value @6%

Year Proposal A

Cumul

ative

cash

inflow

PV

factor

@6%

Discoun

ted

value

Proposa

l B

Cumula

tive

cash

inflow

PV factor

@6%

Present

value

Initial

investment 200000 200000

1 24000 24000 0.94 22642 25000 25000 0.94 23585

2 36000 60000 0.89 53400 50000 75000 0.89 66750

3 90000 150000 0.84 125943 70000 145000 0.84 121745

4 130000 280000 0.79 221786 125000 270000 0.79 213865

5 145000 425000 0.75 317585 170000 440000 0.75 328794

Total 741355 754738

NPV 541355 554738

Table 5: Net present value @6%

Year Proposal A

Cumula

tive

cash

inflow

PV

factor

@8%

Discoun

ted

value

Proposa

l B

Cumula

tive

cash

inflow

PV factor

@8%

Present

value

8

proposal B will be more productive and feasible for the owner of the firm. Through the stated the

investments decisions, the business will be able achieve its purpose.

Net Present Value (NPV)

By the help of NPV, IRR and ARR the business owner be able to ensure, determine and

evaluate their current position oth plans by using discounted present values. Time value of

money concept works behind this approach.

Table 4: Net present value @6%

Year Proposal A

Cumul

ative

cash

inflow

PV

factor

@6%

Discoun

ted

value

Proposa

l B

Cumula

tive

cash

inflow

PV factor

@6%

Present

value

Initial

investment 200000 200000

1 24000 24000 0.94 22642 25000 25000 0.94 23585

2 36000 60000 0.89 53400 50000 75000 0.89 66750

3 90000 150000 0.84 125943 70000 145000 0.84 121745

4 130000 280000 0.79 221786 125000 270000 0.79 213865

5 145000 425000 0.75 317585 170000 440000 0.75 328794

Total 741355 754738

NPV 541355 554738

Table 5: Net present value @6%

Year Proposal A

Cumula

tive

cash

inflow

PV

factor

@8%

Discoun

ted

value

Proposa

l B

Cumula

tive

cash

inflow

PV factor

@8%

Present

value

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

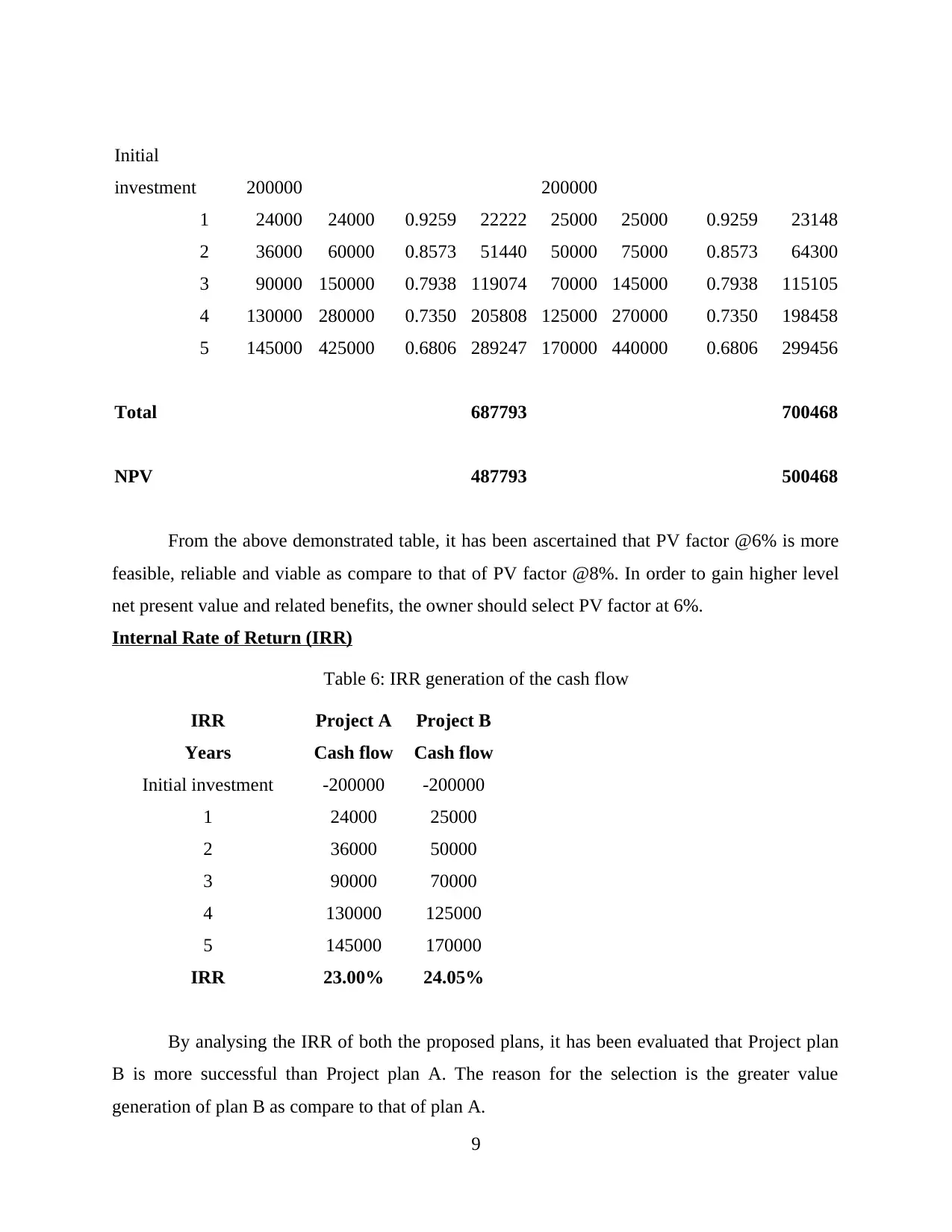

Initial

investment 200000 200000

1 24000 24000 0.9259 22222 25000 25000 0.9259 23148

2 36000 60000 0.8573 51440 50000 75000 0.8573 64300

3 90000 150000 0.7938 119074 70000 145000 0.7938 115105

4 130000 280000 0.7350 205808 125000 270000 0.7350 198458

5 145000 425000 0.6806 289247 170000 440000 0.6806 299456

Total 687793 700468

NPV 487793 500468

From the above demonstrated table, it has been ascertained that PV factor @6% is more

feasible, reliable and viable as compare to that of PV factor @8%. In order to gain higher level

net present value and related benefits, the owner should select PV factor at 6%.

Internal Rate of Return (IRR)

Table 6: IRR generation of the cash flow

IRR Project A Project B

Years Cash flow Cash flow

Initial investment -200000 -200000

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

IRR 23.00% 24.05%

By analysing the IRR of both the proposed plans, it has been evaluated that Project plan

B is more successful than Project plan A. The reason for the selection is the greater value

generation of plan B as compare to that of plan A.

9

investment 200000 200000

1 24000 24000 0.9259 22222 25000 25000 0.9259 23148

2 36000 60000 0.8573 51440 50000 75000 0.8573 64300

3 90000 150000 0.7938 119074 70000 145000 0.7938 115105

4 130000 280000 0.7350 205808 125000 270000 0.7350 198458

5 145000 425000 0.6806 289247 170000 440000 0.6806 299456

Total 687793 700468

NPV 487793 500468

From the above demonstrated table, it has been ascertained that PV factor @6% is more

feasible, reliable and viable as compare to that of PV factor @8%. In order to gain higher level

net present value and related benefits, the owner should select PV factor at 6%.

Internal Rate of Return (IRR)

Table 6: IRR generation of the cash flow

IRR Project A Project B

Years Cash flow Cash flow

Initial investment -200000 -200000

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

IRR 23.00% 24.05%

By analysing the IRR of both the proposed plans, it has been evaluated that Project plan

B is more successful than Project plan A. The reason for the selection is the greater value

generation of plan B as compare to that of plan A.

9

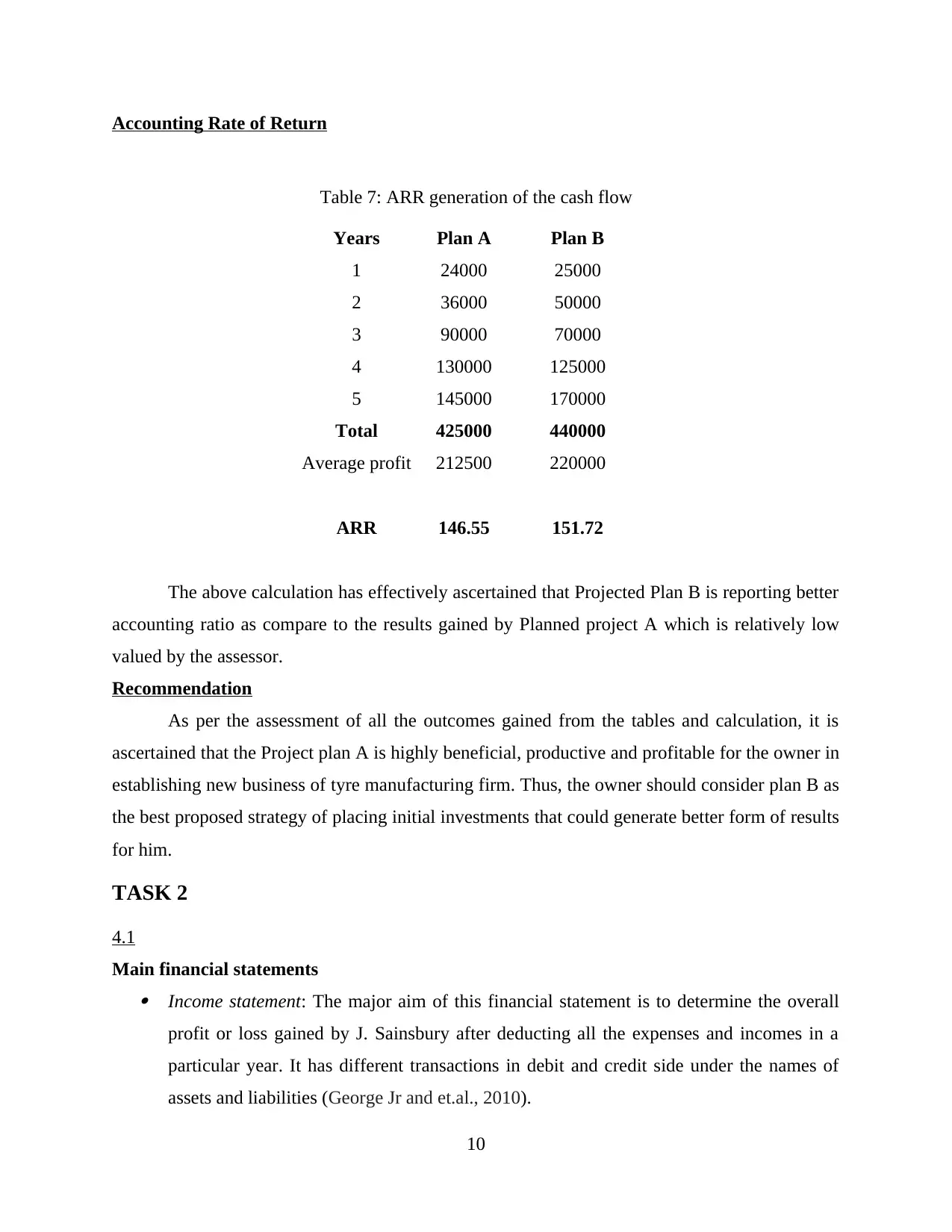

Accounting Rate of Return

Table 7: ARR generation of the cash flow

Years Plan A Plan B

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

Total 425000 440000

Average profit 212500 220000

ARR 146.55 151.72

The above calculation has effectively ascertained that Projected Plan B is reporting better

accounting ratio as compare to the results gained by Planned project A which is relatively low

valued by the assessor.

Recommendation

As per the assessment of all the outcomes gained from the tables and calculation, it is

ascertained that the Project plan A is highly beneficial, productive and profitable for the owner in

establishing new business of tyre manufacturing firm. Thus, the owner should consider plan B as

the best proposed strategy of placing initial investments that could generate better form of results

for him.

TASK 2

4.1

Main financial statements Income statement: The major aim of this financial statement is to determine the overall

profit or loss gained by J. Sainsbury after deducting all the expenses and incomes in a

particular year. It has different transactions in debit and credit side under the names of

assets and liabilities (George Jr and et.al., 2010).

10

Table 7: ARR generation of the cash flow

Years Plan A Plan B

1 24000 25000

2 36000 50000

3 90000 70000

4 130000 125000

5 145000 170000

Total 425000 440000

Average profit 212500 220000

ARR 146.55 151.72

The above calculation has effectively ascertained that Projected Plan B is reporting better

accounting ratio as compare to the results gained by Planned project A which is relatively low

valued by the assessor.

Recommendation

As per the assessment of all the outcomes gained from the tables and calculation, it is

ascertained that the Project plan A is highly beneficial, productive and profitable for the owner in

establishing new business of tyre manufacturing firm. Thus, the owner should consider plan B as

the best proposed strategy of placing initial investments that could generate better form of results

for him.

TASK 2

4.1

Main financial statements Income statement: The major aim of this financial statement is to determine the overall

profit or loss gained by J. Sainsbury after deducting all the expenses and incomes in a

particular year. It has different transactions in debit and credit side under the names of

assets and liabilities (George Jr and et.al., 2010).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.