Financial Resources Report: Sources, Implications, and Decisions

VerifiedAdded on 2019/12/03

|19

|5136

|140

Report

AI Summary

This report provides a comprehensive analysis of managing financial resources, specifically tailored for a restaurant business. It begins by identifying various sources of finance, including internal sources like personal savings and retained profits, and external sources such as bank loans, overdrafts, and venture capitalists. The report then delves into the implications of each source, discussing factors like collateral requirements, dividend policies, and the potential impact on ownership and cash flow. Furthermore, it evaluates the suitability of different financing options for the restaurant, considering factors like flexibility and interest rates. The report also explores the costs associated with each financial source and highlights the significance of financial planning, emphasizing its role in managing cash flow, allocating resources, and anticipating future uncertainties. It examines the information needs of various decision-makers, including employees, suppliers, customers, and creditors. The report concludes by analyzing major financial statements and applying ratio analysis to assess the financial performance of the business. The report gives a detailed overview of how financial decisions are made using financial information.

MANAGING

FINANCIAL

RESOURCES

FINANCIAL

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MANAGING FINANCIAL RESOURCES....................................................................................1

Introduction......................................................................................................................................1

TASK 1 Sources of finance available to the business.....................................................................1

1.1 Sources of finance for Restaurant..........................................................................................1

1.2 Implications of sources..........................................................................................................2

1.3 Evaluation of sources.............................................................................................................3

TASK 2 Implications of finance as a resource................................................................................4

2.1 Costs associated with the sources..........................................................................................4

2.2 Significance of Financial Planning........................................................................................5

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on financial statements.............................................................................7

TASK 3 financial decisions based on financial information...........................................................8

3.1 Analyse Budget......................................................................................................................8

3.2 Calculation of unit costs........................................................................................................8

3.3 Capital Appraisal Methods....................................................................................................9

TASK 4..........................................................................................................................................12

4.1 Major financial statements...................................................................................................12

4.2 Difference between the statements......................................................................................13

4.3 Ratio Analysis......................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

MANAGING FINANCIAL RESOURCES....................................................................................1

Introduction......................................................................................................................................1

TASK 1 Sources of finance available to the business.....................................................................1

1.1 Sources of finance for Restaurant..........................................................................................1

1.2 Implications of sources..........................................................................................................2

1.3 Evaluation of sources.............................................................................................................3

TASK 2 Implications of finance as a resource................................................................................4

2.1 Costs associated with the sources..........................................................................................4

2.2 Significance of Financial Planning........................................................................................5

2.3 Information needs of different decision makers....................................................................6

2.4 Impact of finance on financial statements.............................................................................7

TASK 3 financial decisions based on financial information...........................................................8

3.1 Analyse Budget......................................................................................................................8

3.2 Calculation of unit costs........................................................................................................8

3.3 Capital Appraisal Methods....................................................................................................9

TASK 4..........................................................................................................................................12

4.1 Major financial statements...................................................................................................12

4.2 Difference between the statements......................................................................................13

4.3 Ratio Analysis......................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

Introduction

Finance is the backbone of every business whether it is small size or big size. The most

difficult task in front of the company is the management of financial resources. For that purpose,

knowledge of certain financial practices is must. The purpose of this report is understand the

sources of finance available for restaurant businesses. The study will show the implications of

finance as a resource within business. It will also reflect how the financial decisions are made on

the basis of available information. It will show the application and use of different investment

appraisal methods. At last the report will end in analysing the calculated ratios for the firms.

1

Finance is the backbone of every business whether it is small size or big size. The most

difficult task in front of the company is the management of financial resources. For that purpose,

knowledge of certain financial practices is must. The purpose of this report is understand the

sources of finance available for restaurant businesses. The study will show the implications of

finance as a resource within business. It will also reflect how the financial decisions are made on

the basis of available information. It will show the application and use of different investment

appraisal methods. At last the report will end in analysing the calculated ratios for the firms.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1 Sources of finance available to the business

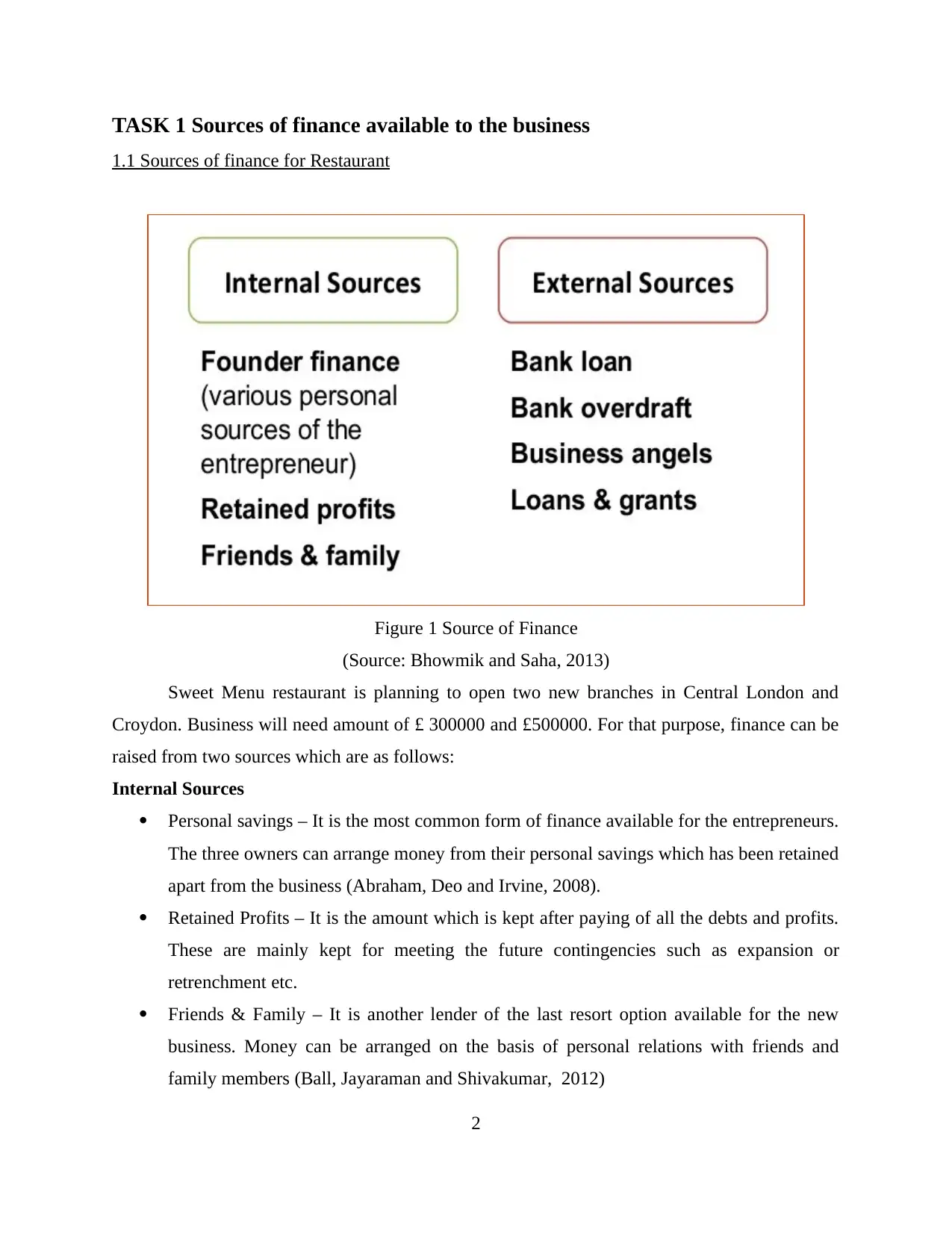

1.1 Sources of finance for Restaurant

Figure 1 Source of Finance

(Source: Bhowmik and Saha, 2013)

Sweet Menu restaurant is planning to open two new branches in Central London and

Croydon. Business will need amount of £ 300000 and £500000. For that purpose, finance can be

raised from two sources which are as follows:

Internal Sources

Personal savings – It is the most common form of finance available for the entrepreneurs.

The three owners can arrange money from their personal savings which has been retained

apart from the business (Abraham, Deo and Irvine, 2008).

Retained Profits – It is the amount which is kept after paying of all the debts and profits.

These are mainly kept for meeting the future contingencies such as expansion or

retrenchment etc.

Friends & Family – It is another lender of the last resort option available for the new

business. Money can be arranged on the basis of personal relations with friends and

family members (Ball, Jayaraman and Shivakumar, 2012)

2

1.1 Sources of finance for Restaurant

Figure 1 Source of Finance

(Source: Bhowmik and Saha, 2013)

Sweet Menu restaurant is planning to open two new branches in Central London and

Croydon. Business will need amount of £ 300000 and £500000. For that purpose, finance can be

raised from two sources which are as follows:

Internal Sources

Personal savings – It is the most common form of finance available for the entrepreneurs.

The three owners can arrange money from their personal savings which has been retained

apart from the business (Abraham, Deo and Irvine, 2008).

Retained Profits – It is the amount which is kept after paying of all the debts and profits.

These are mainly kept for meeting the future contingencies such as expansion or

retrenchment etc.

Friends & Family – It is another lender of the last resort option available for the new

business. Money can be arranged on the basis of personal relations with friends and

family members (Ball, Jayaraman and Shivakumar, 2012)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

External Sources:

Bank Loan – These days’ loans are available at very considerable rate of interests and

requirements. Sweet Menu can obtain loan from any financial institution after submitting

the required formalities.

Bank overdraft – Sweet Menu will require cash for handling its day to day operations.

This need arses due to time gap between the collections and payments. To fulfil such gap,

bank overdraft is the preferred option (Bhowmik and Saha, 2013)

Venture Capitalists – These people are known as venture capitalists, as the capital is

invested generally at the initial stage of the business. The three owners can invite other

people to make investment within the operations.

1.2 Implications of sources

The implications of the identified sources can be defined in the following manner:

Bank Loan – Under bank loan, the owners of Sweet Menu are required to perform all the

legal formalities along with the deposition of collateral security to the bank. After the

completion of the paper work, the owners can make the use of funds as the ownership is

transferred to them (Ogayar, and Vidal, 2009). In case if the expansion fails and bank

does not receive payment, then the collateral security provided by the owners will go on

sale.

Retained earnings – Use of retained earnings will have an impact on the dividend policy

of the company. It can reduce the amount of dividend payments for the shareholders.

There is no dilution of control or ownership in this source (Winand and et. al. 2012).

Funds from this source is considered as the part of reserve and surplus hence it does not

affect the financial obligations.

Venture Capitalist – The level of ownership depends upon the terms and conditions of the

agreement which has been established between the parties (Benedict and Elliott, 2008). It

may be possible that venture capitalist can withdraw their investment from the business.

Bank Overdraft – In case of bank overdraft, extra money is provided by the lender to the

entrepreneur. There is no impact on the ownership, however cash flow issues can arise of

the bank demands the overdraft to be repaid at a short notice (Dada, Azim and Ullah,

2014).

3

Bank Loan – These days’ loans are available at very considerable rate of interests and

requirements. Sweet Menu can obtain loan from any financial institution after submitting

the required formalities.

Bank overdraft – Sweet Menu will require cash for handling its day to day operations.

This need arses due to time gap between the collections and payments. To fulfil such gap,

bank overdraft is the preferred option (Bhowmik and Saha, 2013)

Venture Capitalists – These people are known as venture capitalists, as the capital is

invested generally at the initial stage of the business. The three owners can invite other

people to make investment within the operations.

1.2 Implications of sources

The implications of the identified sources can be defined in the following manner:

Bank Loan – Under bank loan, the owners of Sweet Menu are required to perform all the

legal formalities along with the deposition of collateral security to the bank. After the

completion of the paper work, the owners can make the use of funds as the ownership is

transferred to them (Ogayar, and Vidal, 2009). In case if the expansion fails and bank

does not receive payment, then the collateral security provided by the owners will go on

sale.

Retained earnings – Use of retained earnings will have an impact on the dividend policy

of the company. It can reduce the amount of dividend payments for the shareholders.

There is no dilution of control or ownership in this source (Winand and et. al. 2012).

Funds from this source is considered as the part of reserve and surplus hence it does not

affect the financial obligations.

Venture Capitalist – The level of ownership depends upon the terms and conditions of the

agreement which has been established between the parties (Benedict and Elliott, 2008). It

may be possible that venture capitalist can withdraw their investment from the business.

Bank Overdraft – In case of bank overdraft, extra money is provided by the lender to the

entrepreneur. There is no impact on the ownership, however cash flow issues can arise of

the bank demands the overdraft to be repaid at a short notice (Dada, Azim and Ullah,

2014).

3

Hire purchasing & Leasing – When there is shortage of cash, this source of finance is

used. Hire purchasing and leasing can be done for any kind of machinery or equipment or

tools needed for business (Flynn, Uliana and Wormald, 2012). In this case the ownership

is transferred to the owner after the payment of the last instalments. This creates loss for

the hire purchasing company.

1.3 Evaluation of sources

After analysing the implications for all the financial sources, following sources have been

selected for Sweet Menu:

Bank Loan – This will be the best option for the restaurant owners. It is because the amount

needed for expansion is huge and is also enclosed with many risks. As compared to other

options, bank loan offers high flexibility (Gallén, 2006). These days the loan is available at very

flexible a considerable rate of interests. Further the process of obtaining funds is quicker in case

of this option. All that need is the fulfilment of all the legal formalities and guidelines.

Retained Earnings – It is another good option for the restaurant. As per the given information,

Sweet Menu is running its business operations from last 10 years. It is anticipated that company

has gathered an adequate amount of retained profits within the business due to such solid

reputation among the consumers (Sabău 2013). In such option, company will not have to incur

any legal charges or other financial obligations because the option is available from within the

business. This choice is very feasible in case if the financial position of the restaurant is good and

well equipped. It also appreciate the capital which ultimately enhance the market value of the

shares.

Bank Overdraft - It is also good for the two new ventures. This option is very useful in

handling the mismatch of the cash flows. It can help in maintaining a god payment history as any

kind of payment made through cheque does not bounce due to lack of funds. Overdraft makes

sure that timely payments are made and no late payments penalties are charged (Drake and

Fabozzi, 2012). Further there is very less involvement of paper work. Hence it can be a very

feasible source of money for Sweet Menu. It also provides immediate access to the cash. Making

payment to the suppliers becomes easy at any point of time. The short term operations can be

financed very easily

4

used. Hire purchasing and leasing can be done for any kind of machinery or equipment or

tools needed for business (Flynn, Uliana and Wormald, 2012). In this case the ownership

is transferred to the owner after the payment of the last instalments. This creates loss for

the hire purchasing company.

1.3 Evaluation of sources

After analysing the implications for all the financial sources, following sources have been

selected for Sweet Menu:

Bank Loan – This will be the best option for the restaurant owners. It is because the amount

needed for expansion is huge and is also enclosed with many risks. As compared to other

options, bank loan offers high flexibility (Gallén, 2006). These days the loan is available at very

flexible a considerable rate of interests. Further the process of obtaining funds is quicker in case

of this option. All that need is the fulfilment of all the legal formalities and guidelines.

Retained Earnings – It is another good option for the restaurant. As per the given information,

Sweet Menu is running its business operations from last 10 years. It is anticipated that company

has gathered an adequate amount of retained profits within the business due to such solid

reputation among the consumers (Sabău 2013). In such option, company will not have to incur

any legal charges or other financial obligations because the option is available from within the

business. This choice is very feasible in case if the financial position of the restaurant is good and

well equipped. It also appreciate the capital which ultimately enhance the market value of the

shares.

Bank Overdraft - It is also good for the two new ventures. This option is very useful in

handling the mismatch of the cash flows. It can help in maintaining a god payment history as any

kind of payment made through cheque does not bounce due to lack of funds. Overdraft makes

sure that timely payments are made and no late payments penalties are charged (Drake and

Fabozzi, 2012). Further there is very less involvement of paper work. Hence it can be a very

feasible source of money for Sweet Menu. It also provides immediate access to the cash. Making

payment to the suppliers becomes easy at any point of time. The short term operations can be

financed very easily

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2 Implications of finance as a resource

2.1 Costs associated with the sources

Every source of finance has costs associated with it. Sweet Menu is needed to perform

effective cost benefits analysis with every source so that suitable options can be availed for

raising the finance.

Bank Loan – It is not easy to avail a bank loan. It requires submission of different types of legal

formalities. The costs associated with the source is amount of interests which is charged on the

loan amount (Gibson, 2012). These interest charges can act as burden for the business. In case of

restaurant the amount of capital is high so interest charges will also be high on the loan. Further

fulfilment of legal requirements and paper work also require incurring of some charges which

can also be painful for the entrepreneurs. These associated costs are required to be managed in

effective manner.

Retained earnings – In such case there may be the problem of improper utilization of the funds.

If the objective related to utilization of retained earnings is not clearly stated, then it may incur

some unnecessary charges for the business (Palepu and Healy, 2007). Problem of over

capitalization may also arise which can be very difficult to handle. Another thing is the low rate

of dividend for the shareholders of the business which can be costly.

Bank Overdraft - This source of finance is also enclosed with some costs. It comes with high

interest charges and it is usually higher than the other sources of borrowing. The charges may get

increased, if the borrower exceeds the overdraft limit (Vickerstaff and Johal, 2014). It has to be

remembered that it is a kind of temporary loan and needs regular revisit by the lending

institutions.

2.2 Significance of Financial Planning

Financial planning is the most essential part of running a particular business. The Sweet

Menu is planning to open two new restaurant branches in Central London and Croydon. The

planning is to be done in careful manner to make sure that all the things goes in the right

direction (Zoan, 2014). In respect with new ventures it can help in different ways

The planning will help in managing the cash inflow and cash outflow within the

operations by offering an appropriate structure for the company

5

2.1 Costs associated with the sources

Every source of finance has costs associated with it. Sweet Menu is needed to perform

effective cost benefits analysis with every source so that suitable options can be availed for

raising the finance.

Bank Loan – It is not easy to avail a bank loan. It requires submission of different types of legal

formalities. The costs associated with the source is amount of interests which is charged on the

loan amount (Gibson, 2012). These interest charges can act as burden for the business. In case of

restaurant the amount of capital is high so interest charges will also be high on the loan. Further

fulfilment of legal requirements and paper work also require incurring of some charges which

can also be painful for the entrepreneurs. These associated costs are required to be managed in

effective manner.

Retained earnings – In such case there may be the problem of improper utilization of the funds.

If the objective related to utilization of retained earnings is not clearly stated, then it may incur

some unnecessary charges for the business (Palepu and Healy, 2007). Problem of over

capitalization may also arise which can be very difficult to handle. Another thing is the low rate

of dividend for the shareholders of the business which can be costly.

Bank Overdraft - This source of finance is also enclosed with some costs. It comes with high

interest charges and it is usually higher than the other sources of borrowing. The charges may get

increased, if the borrower exceeds the overdraft limit (Vickerstaff and Johal, 2014). It has to be

remembered that it is a kind of temporary loan and needs regular revisit by the lending

institutions.

2.2 Significance of Financial Planning

Financial planning is the most essential part of running a particular business. The Sweet

Menu is planning to open two new restaurant branches in Central London and Croydon. The

planning is to be done in careful manner to make sure that all the things goes in the right

direction (Zoan, 2014). In respect with new ventures it can help in different ways

The planning will help in managing the cash inflow and cash outflow within the

operations by offering an appropriate structure for the company

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It becomes easy to monitor all the expenses related to the day to day operations and this

facilitates smooth working of all the business functions (Ball, Jayaraman and

Shivakumar, 2012)

Financial planning also offers strong capital foundation, hence in this manner it becomes

easy to allocate all the financial resources in effective manner.

The future and scope for two new branches can also be decided through this function

(Financial Management and Control, 2014)

Another important thing is that any kind of financial uncertainties related to the future

can be anticipated and the corrective actions can be taken at that time only

The tax planning can also be performed effectively as the unessential payment of taxes

can be avoided.

It also establishes a link between the future and the present requirements through the

estimation of sales & growth plans of the organization

The planning also facilities increase in the cash flow and this further enhance the increase

in capital. It is evident that if business has adequate capital, then the management can

think about making other investments (Lampe and Hofmann, 2013)

Greater amount of control on the income can be seen and further any suitable source of

finance can be selected for the business.

6

facilitates smooth working of all the business functions (Ball, Jayaraman and

Shivakumar, 2012)

Financial planning also offers strong capital foundation, hence in this manner it becomes

easy to allocate all the financial resources in effective manner.

The future and scope for two new branches can also be decided through this function

(Financial Management and Control, 2014)

Another important thing is that any kind of financial uncertainties related to the future

can be anticipated and the corrective actions can be taken at that time only

The tax planning can also be performed effectively as the unessential payment of taxes

can be avoided.

It also establishes a link between the future and the present requirements through the

estimation of sales & growth plans of the organization

The planning also facilities increase in the cash flow and this further enhance the increase

in capital. It is evident that if business has adequate capital, then the management can

think about making other investments (Lampe and Hofmann, 2013)

Greater amount of control on the income can be seen and further any suitable source of

finance can be selected for the business.

6

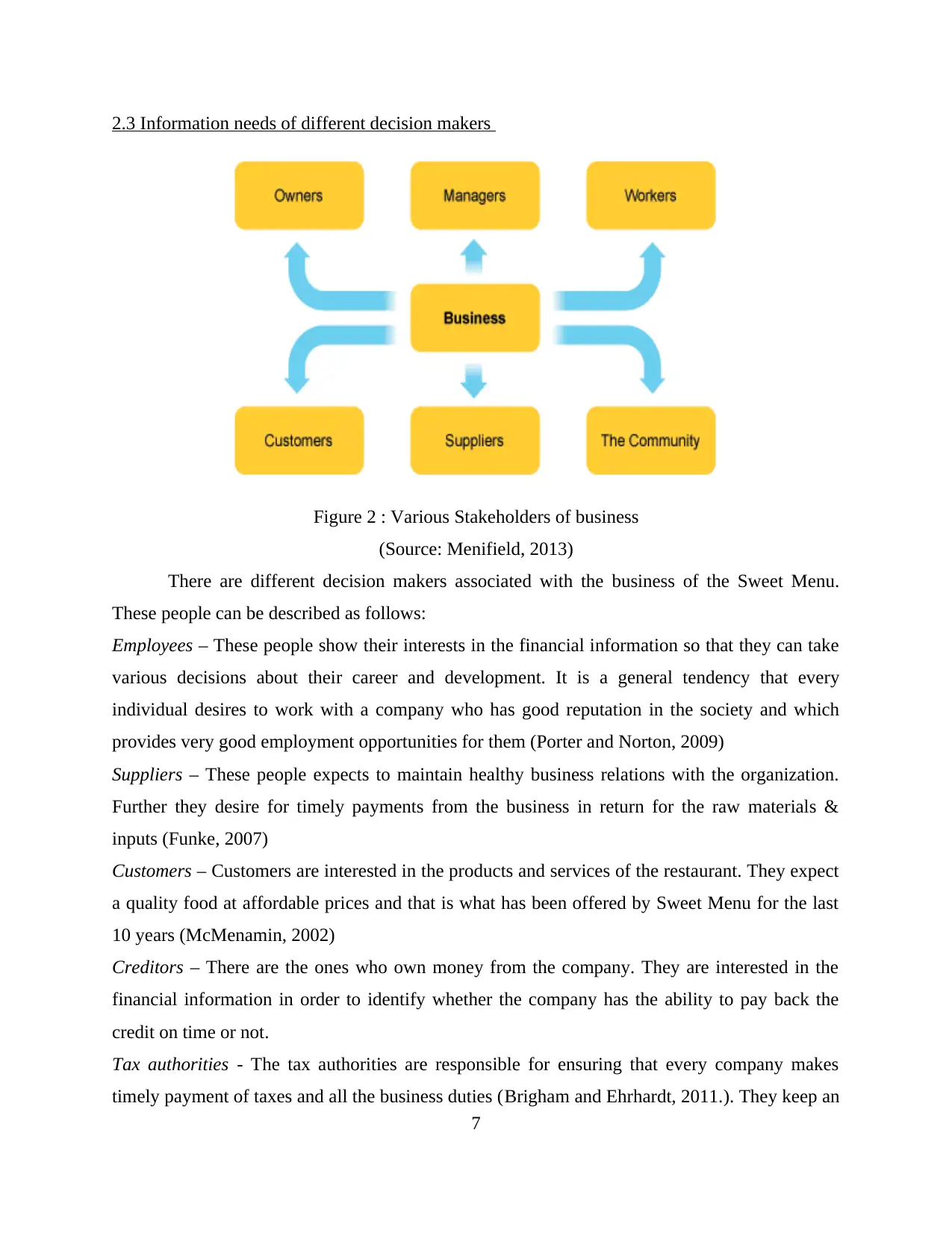

2.3 Information needs of different decision makers

Figure 2 : Various Stakeholders of business

(Source: Menifield, 2013)

There are different decision makers associated with the business of the Sweet Menu.

These people can be described as follows:

Employees – These people show their interests in the financial information so that they can take

various decisions about their career and development. It is a general tendency that every

individual desires to work with a company who has good reputation in the society and which

provides very good employment opportunities for them (Porter and Norton, 2009)

Suppliers – These people expects to maintain healthy business relations with the organization.

Further they desire for timely payments from the business in return for the raw materials &

inputs (Funke, 2007)

Customers – Customers are interested in the products and services of the restaurant. They expect

a quality food at affordable prices and that is what has been offered by Sweet Menu for the last

10 years (McMenamin, 2002)

Creditors – There are the ones who own money from the company. They are interested in the

financial information in order to identify whether the company has the ability to pay back the

credit on time or not.

Tax authorities - The tax authorities are responsible for ensuring that every company makes

timely payment of taxes and all the business duties (Brigham and Ehrhardt, 2011.). They keep an

7

Figure 2 : Various Stakeholders of business

(Source: Menifield, 2013)

There are different decision makers associated with the business of the Sweet Menu.

These people can be described as follows:

Employees – These people show their interests in the financial information so that they can take

various decisions about their career and development. It is a general tendency that every

individual desires to work with a company who has good reputation in the society and which

provides very good employment opportunities for them (Porter and Norton, 2009)

Suppliers – These people expects to maintain healthy business relations with the organization.

Further they desire for timely payments from the business in return for the raw materials &

inputs (Funke, 2007)

Customers – Customers are interested in the products and services of the restaurant. They expect

a quality food at affordable prices and that is what has been offered by Sweet Menu for the last

10 years (McMenamin, 2002)

Creditors – There are the ones who own money from the company. They are interested in the

financial information in order to identify whether the company has the ability to pay back the

credit on time or not.

Tax authorities - The tax authorities are responsible for ensuring that every company makes

timely payment of taxes and all the business duties (Brigham and Ehrhardt, 2011.). They keep an

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

eye on the financial information to identify whether there is any illegal tax avoidance from the

side of the business.

Shareholders – These people takes their decisions related to buying and selling of shares.

Shareholders always expects a decent return on the shares which they have invested in the

market. (Ittelson, 2009)

Government – Governing authorities wants to make sure that company is fulfilling all its

corporate social responsibilities to the fullest. All business practices are to be performed within

the confined ethical framework and as per the laws.

The decisions related to the stakeholders are made at these levels:

Strategic level - In the making of these decisions, the directors of the organization are

involved. These are very crucial and sensitive decisions.

Tactical level – The middle level managers are involved in the decision making process.

At this level, more technical decisions are made

Operational level – At this level, supervisors are involved to make the decisions. These

are related to day to day operations and working.

2.4 Impact of finance on financial statements

The selected source of finance will have an impact on the different financial statements:

Source of finance Impact on financial statements

Bank Loan This option will bring an increase in the value of liabilities

under the balance sheet and amount of capital will

increase. This activity will be recorded in the cash flow

statement under the heading of cash flow from financing

activities. The interest applied on the loan amount will be

recorded under the profit and loss account (Project and

Investment Appraisal for Sustainable Value Creation.

2013)

Retained profit This option will have an impact on the reserve & surplus

within the balance sheet. This activity will be recorded in

the cash flow statement under the heading of cash flow

from investing activities. It will also have an impact on the

8

side of the business.

Shareholders – These people takes their decisions related to buying and selling of shares.

Shareholders always expects a decent return on the shares which they have invested in the

market. (Ittelson, 2009)

Government – Governing authorities wants to make sure that company is fulfilling all its

corporate social responsibilities to the fullest. All business practices are to be performed within

the confined ethical framework and as per the laws.

The decisions related to the stakeholders are made at these levels:

Strategic level - In the making of these decisions, the directors of the organization are

involved. These are very crucial and sensitive decisions.

Tactical level – The middle level managers are involved in the decision making process.

At this level, more technical decisions are made

Operational level – At this level, supervisors are involved to make the decisions. These

are related to day to day operations and working.

2.4 Impact of finance on financial statements

The selected source of finance will have an impact on the different financial statements:

Source of finance Impact on financial statements

Bank Loan This option will bring an increase in the value of liabilities

under the balance sheet and amount of capital will

increase. This activity will be recorded in the cash flow

statement under the heading of cash flow from financing

activities. The interest applied on the loan amount will be

recorded under the profit and loss account (Project and

Investment Appraisal for Sustainable Value Creation.

2013)

Retained profit This option will have an impact on the reserve & surplus

within the balance sheet. This activity will be recorded in

the cash flow statement under the heading of cash flow

from investing activities. It will also have an impact on the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit and loss statement (Porter and Norton, 2009)

Bank overdraft This source will enhance the value of liabilities within the

balance sheet and the amount of capital will also increase.

The event will be recorded under the heading of cash flow

from financing activities within the cash flow statement

The interest charges applied on the overdraft will be

recorded in the profit and loss statement (Lampe and

Hofmann, 2013)

Government grant It is a kind of loan for the company. It will appear in the

cash flow statement under the heading of cash flow from

financing activities (Ball, Jayaraman and Shivakumar,

2012). It is recorded as a liability in the balance sheet.

TASK 3 financial decisions based on financial information

3.1 Analyse Budget

Budget is a forecasting tool which contributes towards finding out the financial position

of the company and also identifies the risks and uncertainties concerned with the functioning of

the business in future. The presented cash budget is of Blue Island Restaurant. From the figures

of the cash budget it can be analysed that sales are showing a fluctuating trend (Vickerstaff and

Johal, 2014). It is affecting the demand of the service of the restaurant within the market. The

outflows in the month of the September are indicating the inability of the business is meeting its

expenses through cash sales. Expenses related to Van, Furniture and Fittings are showing

negative balances. However in the month of October, the business managed to generate positive

net balance of 3870 (Drake and Fabozzi, 2012). The level of expenditures was also decreased. In

the month of November due to increasing demand for products, company is able to maintain a

positive cash balance of 4770. It shows the competency level and efficiency of the business. In

the last month of the cash budget, the expense on Furniture and Fittings raised the outflow. This

thing generated negative balance despite of increase in the revenue. Above all it can be said that

financial position of the Blue Island Restaurant is stable and there are many opportunities for

then to explore (Gibson, 2012).

9

Bank overdraft This source will enhance the value of liabilities within the

balance sheet and the amount of capital will also increase.

The event will be recorded under the heading of cash flow

from financing activities within the cash flow statement

The interest charges applied on the overdraft will be

recorded in the profit and loss statement (Lampe and

Hofmann, 2013)

Government grant It is a kind of loan for the company. It will appear in the

cash flow statement under the heading of cash flow from

financing activities (Ball, Jayaraman and Shivakumar,

2012). It is recorded as a liability in the balance sheet.

TASK 3 financial decisions based on financial information

3.1 Analyse Budget

Budget is a forecasting tool which contributes towards finding out the financial position

of the company and also identifies the risks and uncertainties concerned with the functioning of

the business in future. The presented cash budget is of Blue Island Restaurant. From the figures

of the cash budget it can be analysed that sales are showing a fluctuating trend (Vickerstaff and

Johal, 2014). It is affecting the demand of the service of the restaurant within the market. The

outflows in the month of the September are indicating the inability of the business is meeting its

expenses through cash sales. Expenses related to Van, Furniture and Fittings are showing

negative balances. However in the month of October, the business managed to generate positive

net balance of 3870 (Drake and Fabozzi, 2012). The level of expenditures was also decreased. In

the month of November due to increasing demand for products, company is able to maintain a

positive cash balance of 4770. It shows the competency level and efficiency of the business. In

the last month of the cash budget, the expense on Furniture and Fittings raised the outflow. This

thing generated negative balance despite of increase in the revenue. Above all it can be said that

financial position of the Blue Island Restaurant is stable and there are many opportunities for

then to explore (Gibson, 2012).

9

3.2 Calculation of unit costs

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

Calculation of Food Cost Percentage

Food Cost Percentage = Total Costs of Ingredients/ Selling Price * 100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

The above calculation shows that 62.50% of food costs has to be beard by the restaurant.

At the selling price of £16 per meal, business is generating a profit of £6. Although restaurant is

expecting a 40% profit on the mark up cost and 20% of VAT. The VAT is to be imposed by the

third party that is government which is to be charged from the customers.

3.3 Capital Appraisal Methods

Blue Island is looking to assess the viability of two business proposals. The viability of

the options is judged through two capital investment techniques which are Net Present Value and

Payback Period.

The cash Flows

Year Proposal 1 Proposal 2

0 £1200 £1200

10

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

Calculation of Food Cost Percentage

Food Cost Percentage = Total Costs of Ingredients/ Selling Price * 100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

The above calculation shows that 62.50% of food costs has to be beard by the restaurant.

At the selling price of £16 per meal, business is generating a profit of £6. Although restaurant is

expecting a 40% profit on the mark up cost and 20% of VAT. The VAT is to be imposed by the

third party that is government which is to be charged from the customers.

3.3 Capital Appraisal Methods

Blue Island is looking to assess the viability of two business proposals. The viability of

the options is judged through two capital investment techniques which are Net Present Value and

Payback Period.

The cash Flows

Year Proposal 1 Proposal 2

0 £1200 £1200

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.