FPC003: Superannuation & Retirement Advice Report - Perth, Australia

VerifiedAdded on 2023/04/10

|23

|6717

|284

Report

AI Summary

This report provides a comprehensive analysis of superannuation and retirement advice for Graham and Anna, a couple planning for retirement. The report examines their current financial positions, including income, expenses, assets, and liabilities, and outlines their retirement goals, such as purchasing a house and covering living expenses. It delves into their risk profile, asset allocation strategies, and investment recommendations, considering factors like tax savings and potential investment returns. The analysis includes discussions on the quality of advice, potential investment options, and the couple's concerns regarding existing property investments and aged care for Anna's mother. The report offers insights into managing superannuation funds, maximizing investment opportunities, and ensuring a secure financial future for Graham and Anna, considering various assumptions and external factors. It emphasizes the importance of systematic investments, risk management, and financial planning to achieve their desired retirement lifestyle.

Superannuation &

Retirement Advice

1

Retirement Advice

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary...................................................................................................................3

Present Position/Information about the clients, Financial Positions and Important assumptions

....................................................................................................................................................5

Risk profile and Assets allocation..............................................................................................8

Quality of advice and recommendation...................................................................................10

Analysis....................................................................................................................................18

Conclusion................................................................................................................................19

References................................................................................................................................21

2

Executive Summary...................................................................................................................3

Present Position/Information about the clients, Financial Positions and Important assumptions

....................................................................................................................................................5

Risk profile and Assets allocation..............................................................................................8

Quality of advice and recommendation...................................................................................10

Analysis....................................................................................................................................18

Conclusion................................................................................................................................19

References................................................................................................................................21

2

Executive Summary

A superannuation fund is an essential part of a financial plan. One should formulate a

financial plan by keeping superannuation fund in mind, as it plays a very important role in

cash inflows after retirement. In the given case the client Graham and Anna who are 53 and

51 years of age having two dependent children, plans to get retire after 9 years i.e. at the age

of 62 and 60 respectively. Before the retirement, they wish to accomplish their goals which

included to purchase a house and they're after retirement expenses including holiday expenses

once in two years. They wish to invest their money in such a way so that they can achieve

these objectives.

Both Graham and Anna has shared more than 25 years of their married life. If we talk about

the main earner, then Graham has always been the main source of income earner because due

to the future of their children and to focus on children’s career Anna has left her secretarial

job a long time ago.

As Graham has been working as a senior engineer with BlueScope Steel for the last 26 years

and recently as a part of major restructure he was offered voluntary redundancy. The benefits

are $175,000 in total as a redundancy benefit.

Subsequently, Graham has offered a new role in Pilbara Port Corporation as a site engineer in

an ongoing contract in Western Australia with the total package that he is earning now

$195,000 plus the superannuation benefits 9.5%, which Graham is going to join. Graham and

Anna with their 2 children will soon shift to Perth and he will start his new role as a site

engineer in Pilbara Port Corporation. (Ainsworth, et. al., 2016)

Anna is also willing to join a new job and found a part-time role as a personal assistant to a

training and development manager at “All brains Inc.” As confirmed by her she will soon

start her new role in three months’ time and her remunerations will be $52,000 p.a. plus

superannuation at 9.5%.

The couple is planning to rent initially an estimated $650 per week as rent per week. For the

purpose of buying a property in Perth, they have also approached an agent as they want to

own property rather than rent. Graham will manage to the Pilbara region as he will fly in fly

out. His work structure is designed in such a way that he will initially work for 10 days and

3

A superannuation fund is an essential part of a financial plan. One should formulate a

financial plan by keeping superannuation fund in mind, as it plays a very important role in

cash inflows after retirement. In the given case the client Graham and Anna who are 53 and

51 years of age having two dependent children, plans to get retire after 9 years i.e. at the age

of 62 and 60 respectively. Before the retirement, they wish to accomplish their goals which

included to purchase a house and they're after retirement expenses including holiday expenses

once in two years. They wish to invest their money in such a way so that they can achieve

these objectives.

Both Graham and Anna has shared more than 25 years of their married life. If we talk about

the main earner, then Graham has always been the main source of income earner because due

to the future of their children and to focus on children’s career Anna has left her secretarial

job a long time ago.

As Graham has been working as a senior engineer with BlueScope Steel for the last 26 years

and recently as a part of major restructure he was offered voluntary redundancy. The benefits

are $175,000 in total as a redundancy benefit.

Subsequently, Graham has offered a new role in Pilbara Port Corporation as a site engineer in

an ongoing contract in Western Australia with the total package that he is earning now

$195,000 plus the superannuation benefits 9.5%, which Graham is going to join. Graham and

Anna with their 2 children will soon shift to Perth and he will start his new role as a site

engineer in Pilbara Port Corporation. (Ainsworth, et. al., 2016)

Anna is also willing to join a new job and found a part-time role as a personal assistant to a

training and development manager at “All brains Inc.” As confirmed by her she will soon

start her new role in three months’ time and her remunerations will be $52,000 p.a. plus

superannuation at 9.5%.

The couple is planning to rent initially an estimated $650 per week as rent per week. For the

purpose of buying a property in Perth, they have also approached an agent as they want to

own property rather than rent. Graham will manage to the Pilbara region as he will fly in fly

out. His work structure is designed in such a way that he will initially work for 10 days and

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then 6 days off. The company is supposed to bear all his travelling and living expenses. The

family home that they have been rented on $600 per week (Williams, 2018).

They will be planning to buy a house by borrowing money from their superannuation fund

and have done the formalities.

Graham and Anna have also made some investments in various properties that were

purchased more than a period of 18 months in 2011-12. There are 2 residential investment

units on the gold coast which are now valued at the cost which is less than their purchase

value. Below are the original purchase price of the properties:

Gold Coast: Unit 1 $159,000

Gold Coast: Unit 2 $268,000

Brisbane industrial property: $385,000

Wollongong family home: $310,000

It is expected that the investments in Gold Coast units will get double in the time frame of 10-

15 years, but Graham is getting very concerned now about his both gold coast units which are

valued below their original purchase price. He is also concerned about the properties and

wants the overall negative gearing as a tax advantage.

One more concern of them is to admit Anna’s mother Marie in an aged care facility. Marie

Francis, Anna’s mother is 78 years of age and has been living in their granny’s flat

(non-homeowner) in Wollongong, due to illness and other health issues, she been currently

assessed by a team of aged care facility and the aged care home has allowed her to shift in

their aged care facility (Bateman and Morris, 2015).

Marie has an investment worth $380,000 in the form of cash and also in the bank’s term-

deposit. She receives a part age pension. Graham, Anna and Marie have selected a church-

operated facility in Wollongong as per Marie’s comfortability. This has a deposit price of

accommodation is $240,000. Both Graham and Anna believe she will live with comfortability

with an income of $22,000.

4

family home that they have been rented on $600 per week (Williams, 2018).

They will be planning to buy a house by borrowing money from their superannuation fund

and have done the formalities.

Graham and Anna have also made some investments in various properties that were

purchased more than a period of 18 months in 2011-12. There are 2 residential investment

units on the gold coast which are now valued at the cost which is less than their purchase

value. Below are the original purchase price of the properties:

Gold Coast: Unit 1 $159,000

Gold Coast: Unit 2 $268,000

Brisbane industrial property: $385,000

Wollongong family home: $310,000

It is expected that the investments in Gold Coast units will get double in the time frame of 10-

15 years, but Graham is getting very concerned now about his both gold coast units which are

valued below their original purchase price. He is also concerned about the properties and

wants the overall negative gearing as a tax advantage.

One more concern of them is to admit Anna’s mother Marie in an aged care facility. Marie

Francis, Anna’s mother is 78 years of age and has been living in their granny’s flat

(non-homeowner) in Wollongong, due to illness and other health issues, she been currently

assessed by a team of aged care facility and the aged care home has allowed her to shift in

their aged care facility (Bateman and Morris, 2015).

Marie has an investment worth $380,000 in the form of cash and also in the bank’s term-

deposit. She receives a part age pension. Graham, Anna and Marie have selected a church-

operated facility in Wollongong as per Marie’s comfortability. This has a deposit price of

accommodation is $240,000. Both Graham and Anna believe she will live with comfortability

with an income of $22,000.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present Position/Information about the clients, Financial

Positions and Important assumptions

Currently, Graham and Anna Sutton who are 53 and 51 years of age having 2 children Sam

and Jodie, are working as a senior mining engineer at BlueScope Steel, Wollongong, NSW

and discharging home duties respectively. Graham’s total redundancy benefits are $1,75,000

and as Anna is discharging her home duties she is not earning anything in terms of money

(McGowan, 2018).

After the two-week time, Graham has an offer which he is going to accept to work as a site

engineer in an ongoing contract in Pilbara Port Corporation in Western Australia, with the

total package of $195,000 plus superannuation of 9.5%, simultaneously Anna is also looking

forward to engaging herself in the workforce and has found a suitable part-time role in Perth

as personal assistant to the training and development manager at All Brains Inc. Anna will

earn $52,000 P.A. plus superannuation at 9.5%.

Their children are still in school and the expenses are expected on them is $ 10,000 per year

on each child up to the age of 24. Graham wishes to retire after 9 years and Anna wishes to

work till Graham does.

Graham and Anna have to move for the purpose of their new job and the expenses are

expected to be $ 650 per week. They have also made some investments in their own names

and joint names. Apart from this their estimated annual growth income is $2,50,900 and

$71,650 for Graham and Anna respectively (Clark, et. al., 2018).

Basically, Graham and Anna have estimated that they will require $65,000 per year in terms

if today’s equivalent dollar, excluding their holiday cost which will occur in every second

year that was estimated to $15,000. Graham and Anna will both earn estimate $2,50,900 and

$71,650 p.a. in coming years, so and their annual expenses are $1,58,000, so they have

$1,64,550 for investments and other than house-related expenses (Willows, et. al., 2018).

5

Positions and Important assumptions

Currently, Graham and Anna Sutton who are 53 and 51 years of age having 2 children Sam

and Jodie, are working as a senior mining engineer at BlueScope Steel, Wollongong, NSW

and discharging home duties respectively. Graham’s total redundancy benefits are $1,75,000

and as Anna is discharging her home duties she is not earning anything in terms of money

(McGowan, 2018).

After the two-week time, Graham has an offer which he is going to accept to work as a site

engineer in an ongoing contract in Pilbara Port Corporation in Western Australia, with the

total package of $195,000 plus superannuation of 9.5%, simultaneously Anna is also looking

forward to engaging herself in the workforce and has found a suitable part-time role in Perth

as personal assistant to the training and development manager at All Brains Inc. Anna will

earn $52,000 P.A. plus superannuation at 9.5%.

Their children are still in school and the expenses are expected on them is $ 10,000 per year

on each child up to the age of 24. Graham wishes to retire after 9 years and Anna wishes to

work till Graham does.

Graham and Anna have to move for the purpose of their new job and the expenses are

expected to be $ 650 per week. They have also made some investments in their own names

and joint names. Apart from this their estimated annual growth income is $2,50,900 and

$71,650 for Graham and Anna respectively (Clark, et. al., 2018).

Basically, Graham and Anna have estimated that they will require $65,000 per year in terms

if today’s equivalent dollar, excluding their holiday cost which will occur in every second

year that was estimated to $15,000. Graham and Anna will both earn estimate $2,50,900 and

$71,650 p.a. in coming years, so and their annual expenses are $1,58,000, so they have

$1,64,550 for investments and other than house-related expenses (Willows, et. al., 2018).

5

Graham and Anna can attain the objective that they have set after their retirement by

following the below points:

They need to increase tax saving by taking the benefits of maximum deductions of the

income for the purpose of tax and ensuring handsome amount in government

securities which are also helpful in saving tax (Dwyer, et. al., 2018).

Invest in such securities from where they can get higher dividend and interest such as

debt fund, debenture and fixed deposits.

These forms of investment can help them for better investments opportunities and maximise

returns form the investments and secure money for their children to achieve their set financial

targets. It would also be possible for them to own their own house if they manage the tax

accordingly and also help them to have sufficient funds at the time of retirement. It would

really help them to better orientation and ensure effective financial development. Every

financial plan focused on generating more revenue from the investments that have done and

make the investments in such assets where the high return is generated (Niblock, et. al.,

2017).

For attaining the financial objective, the following assumptions need to be taken by

Graham and Anna:

The income that both Graham and Anna are earning will be increasing as their

increment comes into effect.

There will not be any major expenses will arrive which is not anticipated.

All the working conditions will be constant for them.

If we talk about the annual income of Graham and Anna, it can be better observed through

below table.

Details of estimated annual gross income

Graham Anna

Gross salary income $195,000 $52,000

6

following the below points:

They need to increase tax saving by taking the benefits of maximum deductions of the

income for the purpose of tax and ensuring handsome amount in government

securities which are also helpful in saving tax (Dwyer, et. al., 2018).

Invest in such securities from where they can get higher dividend and interest such as

debt fund, debenture and fixed deposits.

These forms of investment can help them for better investments opportunities and maximise

returns form the investments and secure money for their children to achieve their set financial

targets. It would also be possible for them to own their own house if they manage the tax

accordingly and also help them to have sufficient funds at the time of retirement. It would

really help them to better orientation and ensure effective financial development. Every

financial plan focused on generating more revenue from the investments that have done and

make the investments in such assets where the high return is generated (Niblock, et. al.,

2017).

For attaining the financial objective, the following assumptions need to be taken by

Graham and Anna:

The income that both Graham and Anna are earning will be increasing as their

increment comes into effect.

There will not be any major expenses will arrive which is not anticipated.

All the working conditions will be constant for them.

If we talk about the annual income of Graham and Anna, it can be better observed through

below table.

Details of estimated annual gross income

Graham Anna

Gross salary income $195,000 $52,000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

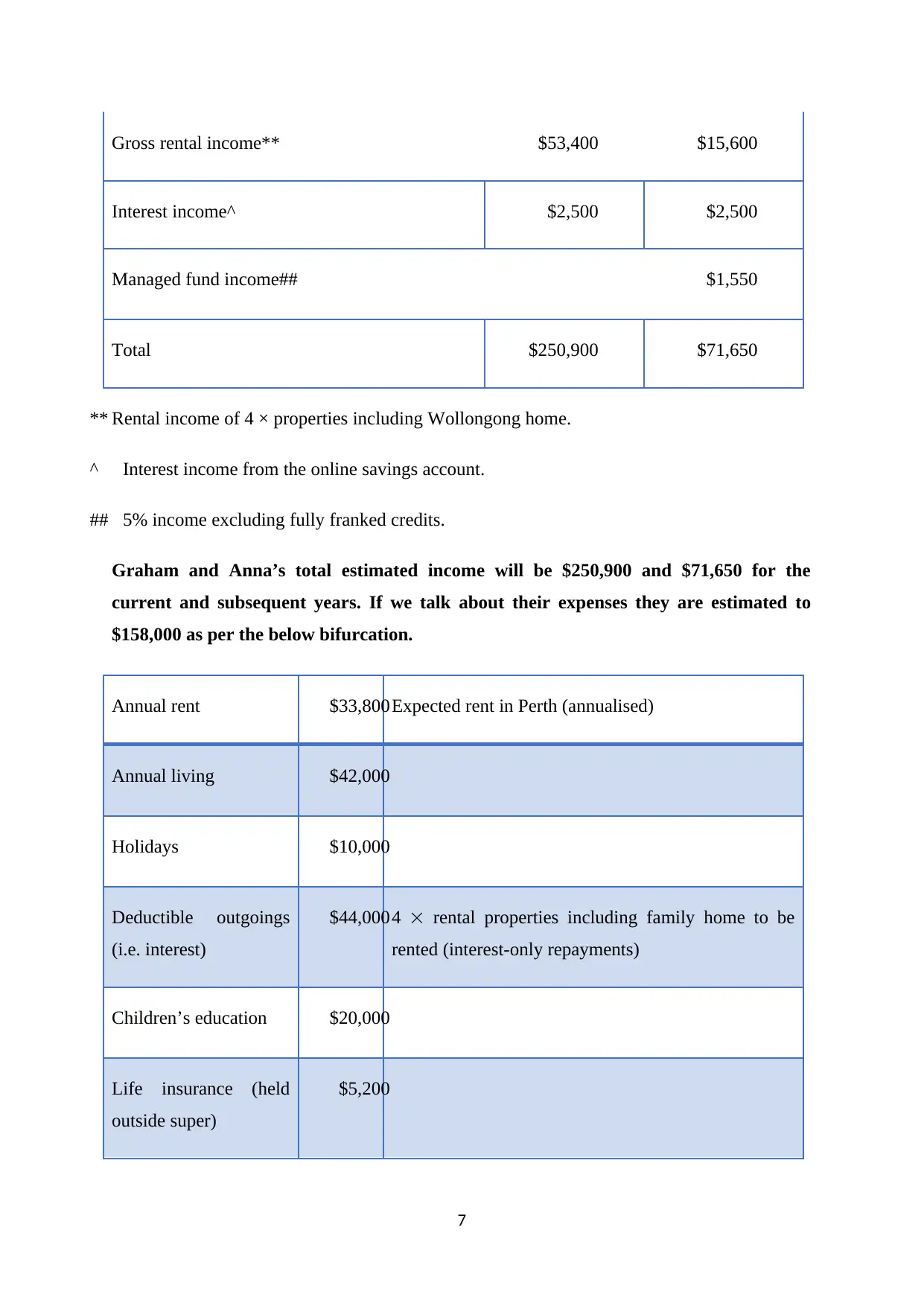

Gross rental income** $53,400 $15,600

Interest income^ $2,500 $2,500

Managed fund income## $1,550

Total $250,900 $71,650

** Rental income of 4 × properties including Wollongong home.

^ Interest income from the online savings account.

## 5% income excluding fully franked credits.

Graham and Anna’s total estimated income will be $250,900 and $71,650 for the

current and subsequent years. If we talk about their expenses they are estimated to

$158,000 as per the below bifurcation.

Annual rent $33,800Expected rent in Perth (annualised)

Annual living $42,000

Holidays $10,000

Deductible outgoings

(i.e. interest)

$44,0004 rental properties including family home to be

rented (interest-only repayments)

Children’s education $20,000

Life insurance (held

outside super)

$5,200

7

Interest income^ $2,500 $2,500

Managed fund income## $1,550

Total $250,900 $71,650

** Rental income of 4 × properties including Wollongong home.

^ Interest income from the online savings account.

## 5% income excluding fully franked credits.

Graham and Anna’s total estimated income will be $250,900 and $71,650 for the

current and subsequent years. If we talk about their expenses they are estimated to

$158,000 as per the below bifurcation.

Annual rent $33,800Expected rent in Perth (annualised)

Annual living $42,000

Holidays $10,000

Deductible outgoings

(i.e. interest)

$44,0004 rental properties including family home to be

rented (interest-only repayments)

Children’s education $20,000

Life insurance (held

outside super)

$5,200

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

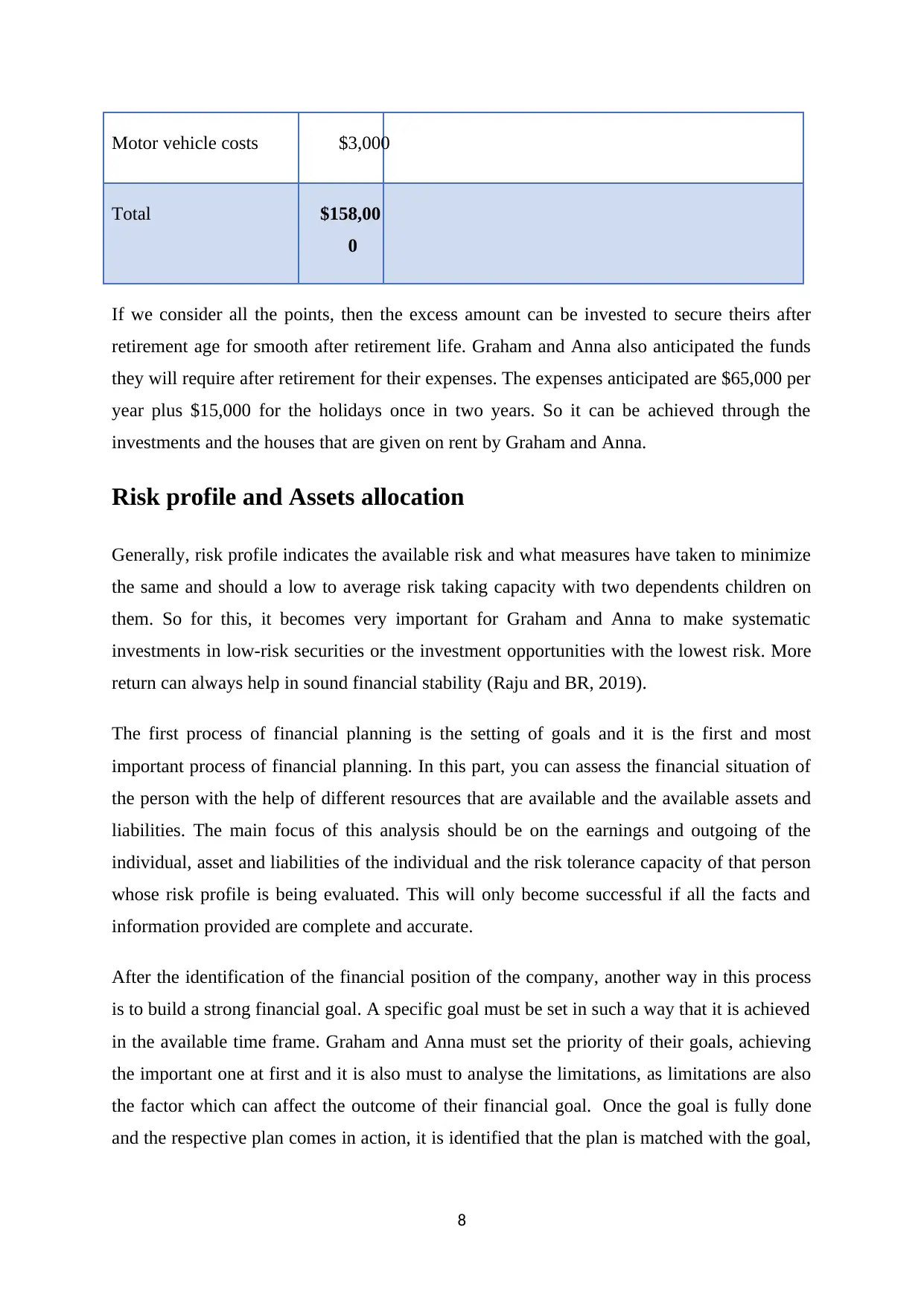

Motor vehicle costs $3,000

Total $158,00

0

If we consider all the points, then the excess amount can be invested to secure theirs after

retirement age for smooth after retirement life. Graham and Anna also anticipated the funds

they will require after retirement for their expenses. The expenses anticipated are $65,000 per

year plus $15,000 for the holidays once in two years. So it can be achieved through the

investments and the houses that are given on rent by Graham and Anna.

Risk profile and Assets allocation

Generally, risk profile indicates the available risk and what measures have taken to minimize

the same and should a low to average risk taking capacity with two dependents children on

them. So for this, it becomes very important for Graham and Anna to make systematic

investments in low-risk securities or the investment opportunities with the lowest risk. More

return can always help in sound financial stability (Raju and BR, 2019).

The first process of financial planning is the setting of goals and it is the first and most

important process of financial planning. In this part, you can assess the financial situation of

the person with the help of different resources that are available and the available assets and

liabilities. The main focus of this analysis should be on the earnings and outgoing of the

individual, asset and liabilities of the individual and the risk tolerance capacity of that person

whose risk profile is being evaluated. This will only become successful if all the facts and

information provided are complete and accurate.

After the identification of the financial position of the company, another way in this process

is to build a strong financial goal. A specific goal must be set in such a way that it is achieved

in the available time frame. Graham and Anna must set the priority of their goals, achieving

the important one at first and it is also must to analyse the limitations, as limitations are also

the factor which can affect the outcome of their financial goal. Once the goal is fully done

and the respective plan comes in action, it is identified that the plan is matched with the goal,

8

Total $158,00

0

If we consider all the points, then the excess amount can be invested to secure theirs after

retirement age for smooth after retirement life. Graham and Anna also anticipated the funds

they will require after retirement for their expenses. The expenses anticipated are $65,000 per

year plus $15,000 for the holidays once in two years. So it can be achieved through the

investments and the houses that are given on rent by Graham and Anna.

Risk profile and Assets allocation

Generally, risk profile indicates the available risk and what measures have taken to minimize

the same and should a low to average risk taking capacity with two dependents children on

them. So for this, it becomes very important for Graham and Anna to make systematic

investments in low-risk securities or the investment opportunities with the lowest risk. More

return can always help in sound financial stability (Raju and BR, 2019).

The first process of financial planning is the setting of goals and it is the first and most

important process of financial planning. In this part, you can assess the financial situation of

the person with the help of different resources that are available and the available assets and

liabilities. The main focus of this analysis should be on the earnings and outgoing of the

individual, asset and liabilities of the individual and the risk tolerance capacity of that person

whose risk profile is being evaluated. This will only become successful if all the facts and

information provided are complete and accurate.

After the identification of the financial position of the company, another way in this process

is to build a strong financial goal. A specific goal must be set in such a way that it is achieved

in the available time frame. Graham and Anna must set the priority of their goals, achieving

the important one at first and it is also must to analyse the limitations, as limitations are also

the factor which can affect the outcome of their financial goal. Once the goal is fully done

and the respective plan comes in action, it is identified that the plan is matched with the goal,

8

need, and priority, then only the plan moves further to the next step. There are so many

factors that will involve in the development of a financial goal.

The process of choosing investment options from the available options is known as asset

allocation. Asset allocation is there to match the personal risk profile of the individual and the

set investment goals in terms of return from assets. In general, terms, if you are less in age

and have a lot of assets and you do not expect any big expense in near future then you can

take more risk with your investments (Hanrahan, 2018).

After the financial goal is determined and actions which need to be taken are set even this

there must be a ready backup plan is prepared to make any decision a good decision. So,

there must be an alternative course of action as a backup, if the main plan doesn’t work then

they must get prepare themselves for the second plan. Alternatively, it can also be possible to

expand the existing plan or to make some modification in the plan. After this, we need to

move forward to the next step that is to examine the alternative.

Once the alternatives are set, we need to move to the next step which is to evaluate to what

extent the available alternatives are viable. Now there are few plans are in a single place and

in the next step we need to select plan among the plans that are available. The identification

of the risk and taking the corrective measure could help them to move forward in achieving

the set financial targets.

In this step, the actual implementation of the plan is done. The plan which we were preparing

to achieve the set financial targets is implemented in this step. There must be a short term

measure that should be first focused and then only the plan should proceed to the next stage.

It might require the help of other partiers to implement the plan.

Now after the plan is fully implemented the subsequent step in the process is to review the

plan timely. The plan must be regularly monitored to evaluate any changes and modifications

in the outside financial environment like the change in government requirements or the

market condition and other uncontrollable conditions. Changing the trend of the market and

the personal financial situation is also affect the financial plan.

Asset allocation strategy can only be developed by Graham and Anna by using their risk-

return profile. As discussed in the above paragraph for better allocation of assets and they

need to identify their risk-taking capacity and low-risk investments. There is an assumption

9

factors that will involve in the development of a financial goal.

The process of choosing investment options from the available options is known as asset

allocation. Asset allocation is there to match the personal risk profile of the individual and the

set investment goals in terms of return from assets. In general, terms, if you are less in age

and have a lot of assets and you do not expect any big expense in near future then you can

take more risk with your investments (Hanrahan, 2018).

After the financial goal is determined and actions which need to be taken are set even this

there must be a ready backup plan is prepared to make any decision a good decision. So,

there must be an alternative course of action as a backup, if the main plan doesn’t work then

they must get prepare themselves for the second plan. Alternatively, it can also be possible to

expand the existing plan or to make some modification in the plan. After this, we need to

move forward to the next step that is to examine the alternative.

Once the alternatives are set, we need to move to the next step which is to evaluate to what

extent the available alternatives are viable. Now there are few plans are in a single place and

in the next step we need to select plan among the plans that are available. The identification

of the risk and taking the corrective measure could help them to move forward in achieving

the set financial targets.

In this step, the actual implementation of the plan is done. The plan which we were preparing

to achieve the set financial targets is implemented in this step. There must be a short term

measure that should be first focused and then only the plan should proceed to the next stage.

It might require the help of other partiers to implement the plan.

Now after the plan is fully implemented the subsequent step in the process is to review the

plan timely. The plan must be regularly monitored to evaluate any changes and modifications

in the outside financial environment like the change in government requirements or the

market condition and other uncontrollable conditions. Changing the trend of the market and

the personal financial situation is also affect the financial plan.

Asset allocation strategy can only be developed by Graham and Anna by using their risk-

return profile. As discussed in the above paragraph for better allocation of assets and they

need to identify their risk-taking capacity and low-risk investments. There is an assumption

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regarding the asset allocation which is actually true that the closure a person to his or her

retirement target date, the major investment should change to reflect less tolerance and

volatility of risk. Hence, for better allocation of assets, Graham and Anna need to identify

their risk-taking capacity and to assess their retirement and superannuation plan that actually

how they will be going to earn after their retirement. After the proper investment as per their

capacity has been done they need to monitor and manage their portfolio.

Quality of advice and recommendation

The first and most important thing for this is to set the goals which they actually want to

achieve. Graham and Anna have set their goals for both long and short term perspective,

considering all the relevant points including the expected expenses on their children.

For attaining the goals that are set by Graham and Anna it is advisable for them to manage

their expenses accordingly and focus on the investments. It is highly recommended to them to

invest their excess money in such securities from where they can earn more dividend and

interest and low risk-bearing investments. It is also recommended to them to invest in such a

manner from where they can save the tax also so that they have the option to invest more.

It is strictly recommended to manage their superannuation fund because it ensures money to

invest where the person wants to invest, so it should be invested in those securities where the

return is high and having low risk. To manage superannuation in such a way that one can also

plan to earn bonus as per the superannuation scheme. Superannuation is always tax-free on

retirement so it should be only withdrawn on retirement. By pooling the retirement savings

with other fund members with a large super fund, one can also take advantage of the

investments otherwise would not be able to access as an individual.

The current gap between income and expenses also needs to be filled by investing the excess

funds in the proper portfolio, from where high risk can be earned taking the lowest possible

risk. This technique will help them to reach their set financial targets with an easy manner

and also has additional liquidity when retiring from their services. This will take care of the

inflation also with their other important expenses such as children expenses, travelling

expenses that will come in future.

The strategies that are to be used mainly include to ensure higher dividend income and

interest income, all of this will help Graham and Anna to ensure that they will save money in

10

retirement target date, the major investment should change to reflect less tolerance and

volatility of risk. Hence, for better allocation of assets, Graham and Anna need to identify

their risk-taking capacity and to assess their retirement and superannuation plan that actually

how they will be going to earn after their retirement. After the proper investment as per their

capacity has been done they need to monitor and manage their portfolio.

Quality of advice and recommendation

The first and most important thing for this is to set the goals which they actually want to

achieve. Graham and Anna have set their goals for both long and short term perspective,

considering all the relevant points including the expected expenses on their children.

For attaining the goals that are set by Graham and Anna it is advisable for them to manage

their expenses accordingly and focus on the investments. It is highly recommended to them to

invest their excess money in such securities from where they can earn more dividend and

interest and low risk-bearing investments. It is also recommended to them to invest in such a

manner from where they can save the tax also so that they have the option to invest more.

It is strictly recommended to manage their superannuation fund because it ensures money to

invest where the person wants to invest, so it should be invested in those securities where the

return is high and having low risk. To manage superannuation in such a way that one can also

plan to earn bonus as per the superannuation scheme. Superannuation is always tax-free on

retirement so it should be only withdrawn on retirement. By pooling the retirement savings

with other fund members with a large super fund, one can also take advantage of the

investments otherwise would not be able to access as an individual.

The current gap between income and expenses also needs to be filled by investing the excess

funds in the proper portfolio, from where high risk can be earned taking the lowest possible

risk. This technique will help them to reach their set financial targets with an easy manner

and also has additional liquidity when retiring from their services. This will take care of the

inflation also with their other important expenses such as children expenses, travelling

expenses that will come in future.

The strategies that are to be used mainly include to ensure higher dividend income and

interest income, all of this will help Graham and Anna to ensure that they will save money in

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a better manner. It would not be correct to suggest Graham and Anna that they should reduce

their expenses as this will decrease their standard of living and which is not the objective.

Instead, they should be improving it is as the set objective. So based on prioritization of

expenses, schooling of their children and purchase house are the first two elements that need

to be provided for first and rest all expenses will be secondary. Apart from these savings for

their retirement and a holiday, is to be managed in a different manner. Investments should be

made for this purpose and try to generate additional returns from the investments that can to

be used for the purpose of housing and schooling. It is possible for Graham and Anna to

create good growth if the market conditions are a favourable i.e. good return on the area

where they have invested the funds and wise investment decisions are taken.

The methods to be used to reach the goals that are set by Graham and Anna include the below

points:

a. Increase tax savings through by taking the benefits of deductions and to ensure that the

investments that are made in government securities help them in tax saving.

b. to invest in such a way from where you get higher dividends income and interest.

c. Invest in bonds and shares of those companies which have a track record of paying a high

dividend.

These tactics are helpful to manage a smart investment portfolio and returns for Graham and

Anna and help them to attain their financial goals. It would be possible for Graham and Anna

to purchase a house and it would also be helpful for them to have sufficient funds at the time

when they retire from their service. It would help them for growth’s perspective and overall

development of full family (Taylor, et. al., 2017).

11

their expenses as this will decrease their standard of living and which is not the objective.

Instead, they should be improving it is as the set objective. So based on prioritization of

expenses, schooling of their children and purchase house are the first two elements that need

to be provided for first and rest all expenses will be secondary. Apart from these savings for

their retirement and a holiday, is to be managed in a different manner. Investments should be

made for this purpose and try to generate additional returns from the investments that can to

be used for the purpose of housing and schooling. It is possible for Graham and Anna to

create good growth if the market conditions are a favourable i.e. good return on the area

where they have invested the funds and wise investment decisions are taken.

The methods to be used to reach the goals that are set by Graham and Anna include the below

points:

a. Increase tax savings through by taking the benefits of deductions and to ensure that the

investments that are made in government securities help them in tax saving.

b. to invest in such a way from where you get higher dividends income and interest.

c. Invest in bonds and shares of those companies which have a track record of paying a high

dividend.

These tactics are helpful to manage a smart investment portfolio and returns for Graham and

Anna and help them to attain their financial goals. It would be possible for Graham and Anna

to purchase a house and it would also be helpful for them to have sufficient funds at the time

when they retire from their service. It would help them for growth’s perspective and overall

development of full family (Taylor, et. al., 2017).

11

The investment in the properties which were purchased over a period of 18 months by

Graham and Anna in the year 2011-12. Both the below residential investment units on the

Gold Coast valued at the price below their purchase price. The actual price of the properties

plus cost of properties are depicted below:

• Gold Coast: Unit 1 $159,000

• Gold Coast: Unit 2 $268,000

• Brisbane industrial property: $385,000

• Wollongong family home: $310,000

As per the books read by Graham on building wealth through property investments and has

become part of some investment related seminars which recommended the negative gearing

onto the property. It was expected from this that the investment in property could double in

coming 10-15 years but Graham is very concerned about the same and he valued both his

Gold coast units less than their actual purchase price. He is not fully sure that what he needs

to do with these properties. Graham has also said that he wants to explore the establishment

of a self-managed superannuation fund (SMSF) as he has gathered information from some

source that he can borrow funds through an SMSF to buy a property. So instead of generating

cash liquidity from the Gold Coast Properties, Graham has opted the option to borrow money

from his superannuation fund. If this happens i.e. he borrow money from his superannuation

fund, then he has to be ready that he will be having very less amount at the time of retirement

and he has also kept in mind that at the time of his retirement his younger child Jodie will

become 22 years old and he will also have Jodie’s expenses $10,000 per year for next 2

years. Contrary to this he would not be having any liability from Sam’s side.

Now Graham and Anna will able to take the benefit of the instalments for the tax saving

purpose and they are able to save their taxes in future years. As per them, it is estimated that

they have settled all their debt till their retirement and they will require $65,000 per year in

terms of today’s equivalent dollar excluding their major holidays, which they are planning to

take once in every second year at a cost of $15,000. At this point in time, they want to retire

in Wollongong or near the south coast of New South Wales (Hunt and Terry, 2018).

12

Graham and Anna in the year 2011-12. Both the below residential investment units on the

Gold Coast valued at the price below their purchase price. The actual price of the properties

plus cost of properties are depicted below:

• Gold Coast: Unit 1 $159,000

• Gold Coast: Unit 2 $268,000

• Brisbane industrial property: $385,000

• Wollongong family home: $310,000

As per the books read by Graham on building wealth through property investments and has

become part of some investment related seminars which recommended the negative gearing

onto the property. It was expected from this that the investment in property could double in

coming 10-15 years but Graham is very concerned about the same and he valued both his

Gold coast units less than their actual purchase price. He is not fully sure that what he needs

to do with these properties. Graham has also said that he wants to explore the establishment

of a self-managed superannuation fund (SMSF) as he has gathered information from some

source that he can borrow funds through an SMSF to buy a property. So instead of generating

cash liquidity from the Gold Coast Properties, Graham has opted the option to borrow money

from his superannuation fund. If this happens i.e. he borrow money from his superannuation

fund, then he has to be ready that he will be having very less amount at the time of retirement

and he has also kept in mind that at the time of his retirement his younger child Jodie will

become 22 years old and he will also have Jodie’s expenses $10,000 per year for next 2

years. Contrary to this he would not be having any liability from Sam’s side.

Now Graham and Anna will able to take the benefit of the instalments for the tax saving

purpose and they are able to save their taxes in future years. As per them, it is estimated that

they have settled all their debt till their retirement and they will require $65,000 per year in

terms of today’s equivalent dollar excluding their major holidays, which they are planning to

take once in every second year at a cost of $15,000. At this point in time, they want to retire

in Wollongong or near the south coast of New South Wales (Hunt and Terry, 2018).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.